Third edition governance landscape meetings under the new ... · CONTENTS 1 Introduction 1 2 The...

84

A DIRECTOR’S GUIDE Navigating the way through board meetings under the new corporate governance landscape Third edition

Transcript of Third edition governance landscape meetings under the new ... · CONTENTS 1 Introduction 1 2 The...

A DIRECTOR’S GUIDE Navigating the way through board meetings under the new corporate governance landscape

Third edition

CONTACTS

Queries regarding any topic contained in the guide can be directed to Johan Holtzhausen ([email protected]) or David Tosi ([email protected]) or any other member of the PSG Capital team on 021 887 9602/011 032 7400. Further information regarding PSG Capital can be found on our website at www.psgcapital.com.

CONTENTS

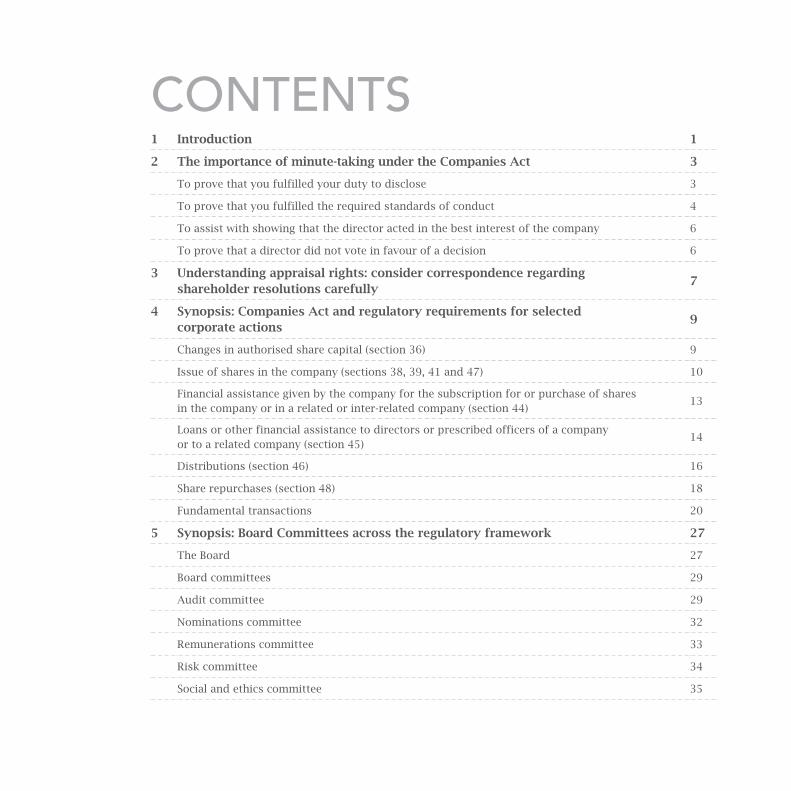

CONTENTS1 Introduction 1

2 The importance of minute-taking under the Companies Act 3

To prove that you fulfilled your duty to disclose 3

To prove that you fulfilled the required standards of conduct 4

To assist with showing that the director acted in the best interest of the company 6

To prove that a director did not vote in favour of a decision 6

3 Understanding appraisal rights: consider correspondence regarding shareholder resolutions carefully

7

4 Synopsis: Companies Act and regulatory requirements for selected corporate actions

9

Changes in authorised share capital (section 36) 9

Issue of shares in the company (sections 38, 39, 41 and 47) 10

Financial assistance given by the company for the subscription for or purchase of shares in the company or in a related or inter-related company (section 44)

13

Loans or other financial assistance to directors or prescribed officers of a company or to a related company (section 45)

14

Distributions (section 46) 16

Share repurchases (section 48) 18

Fundamental transactions 20

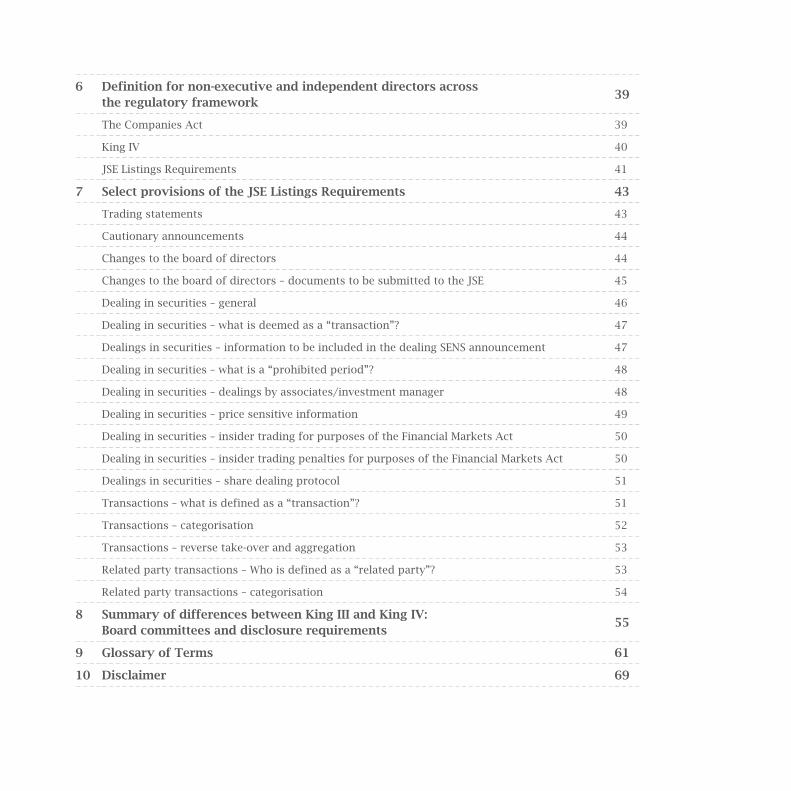

5 Synopsis: Board Committees across the regulatory framework 27

The Board 27

Board committees 29

Audit committee 29

Nominations committee 32

Remunerations committee 33

Risk committee 34

Social and ethics committee 35

6 Definition for non-executive and independent directors across the regulatory framework

39

The Companies Act 39

King IV 40

JSE Listings Requirements 41

7 Select provisions of the JSE Listings Requirements 43

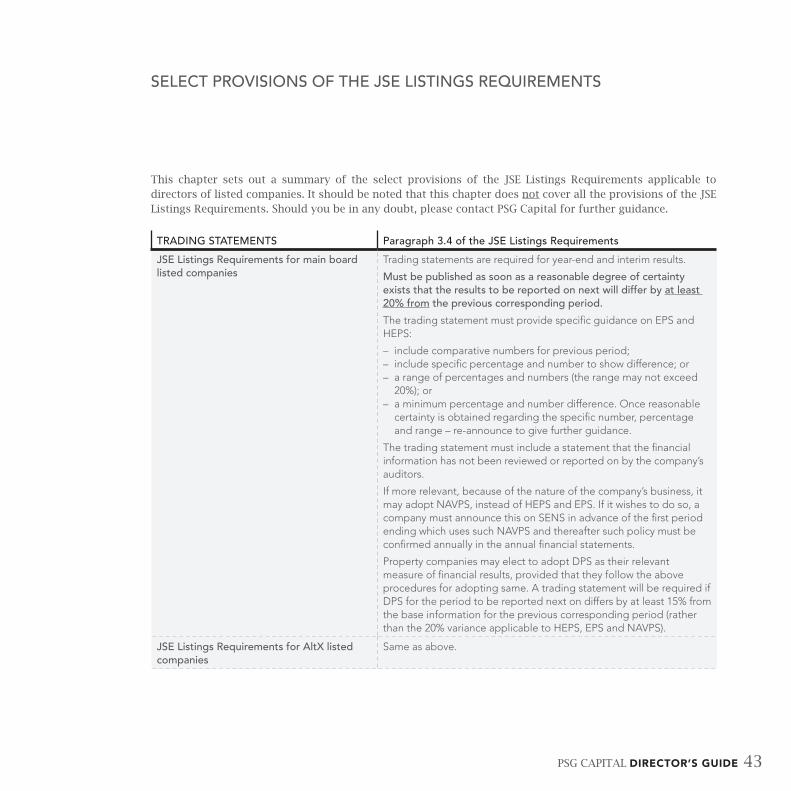

Trading statements 43

Cautionary announcements 44

Changes to the board of directors 44

Changes to the board of directors – documents to be submitted to the JSE 45

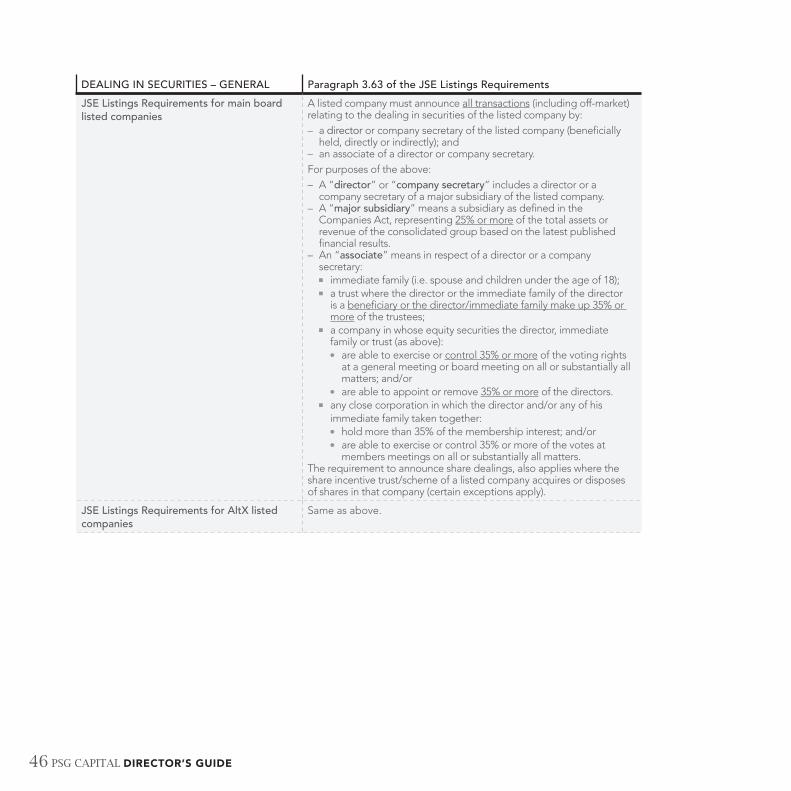

Dealing in securities – general 46

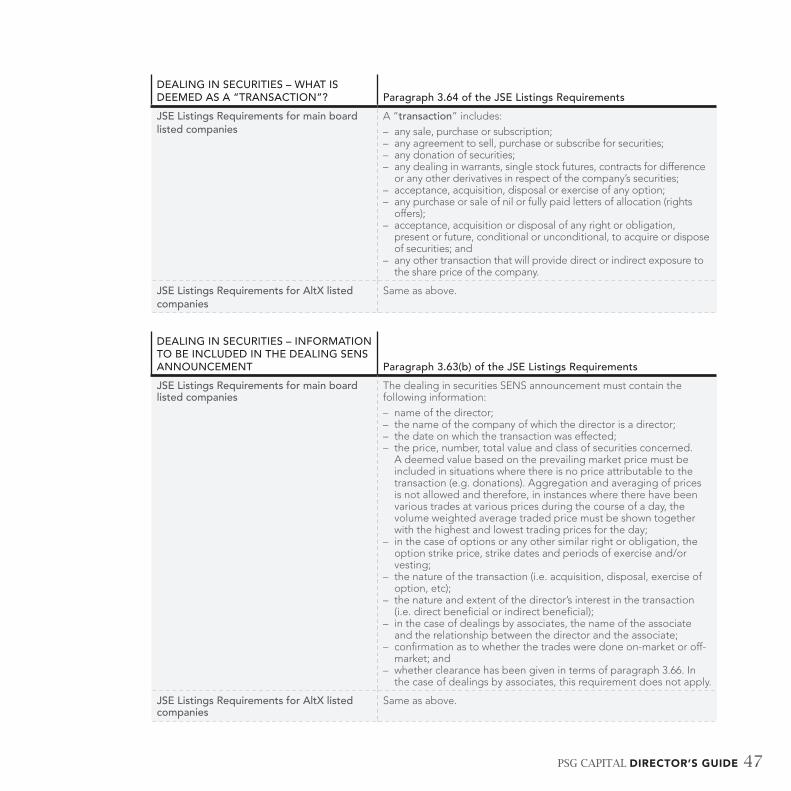

Dealing in securities – what is deemed as a “transaction”? 47

Dealings in securities – information to be included in the dealing SENS announcement 47

Dealing in securities – what is a “prohibited period”? 48

Dealing in securities – dealings by associates/investment manager 48

Dealing in securities – price sensitive information 49

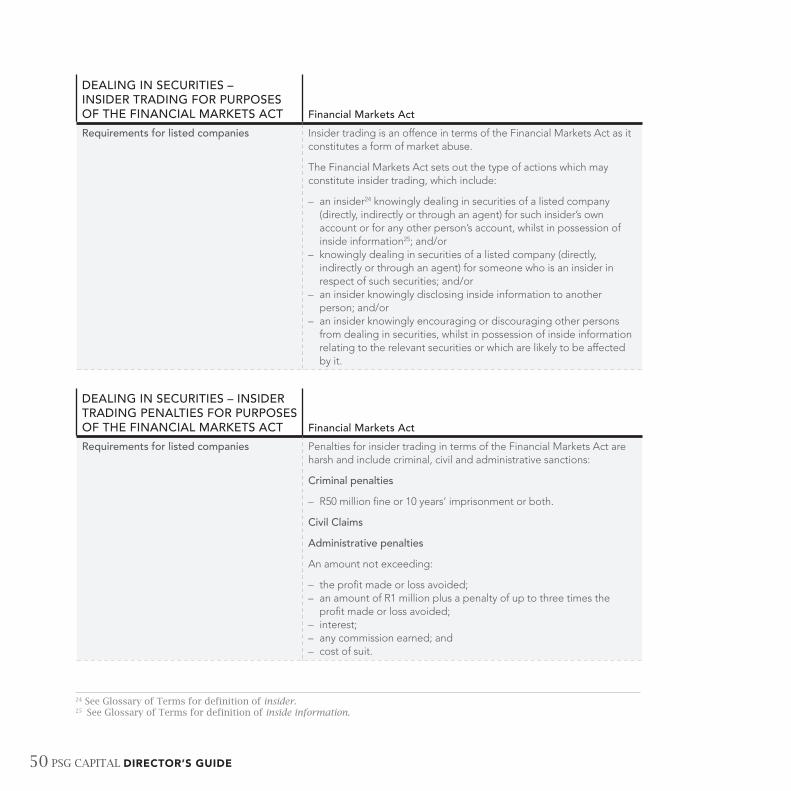

Dealing in securities – insider trading for purposes of the Financial Markets Act 50

Dealing in securities – insider trading penalties for purposes of the Financial Markets Act 50

Dealings in securities – share dealing protocol 51

Transactions – what is defined as a “transaction”? 51

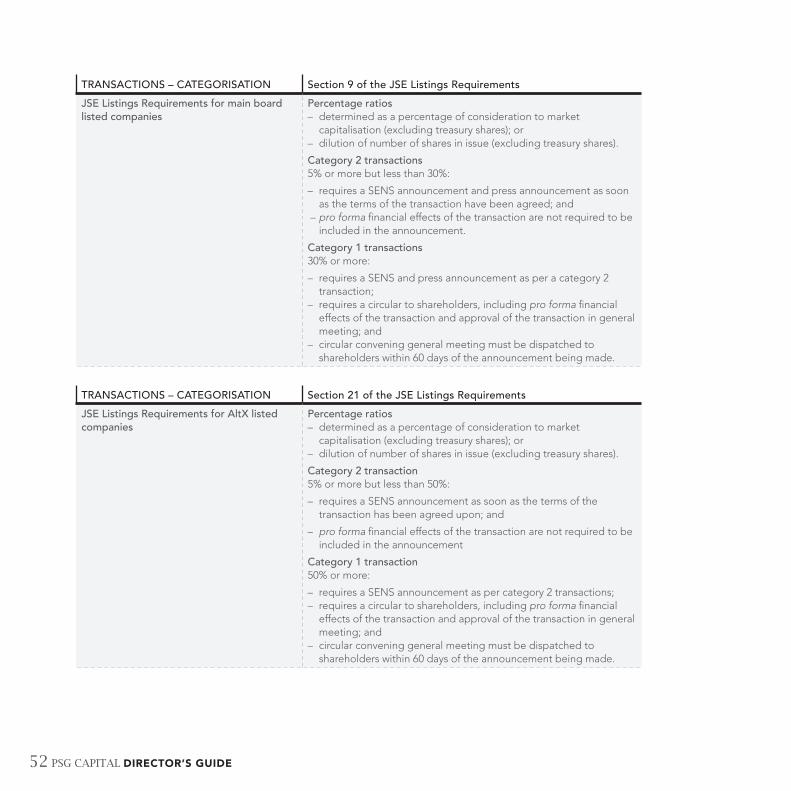

Transactions – categorisation 52

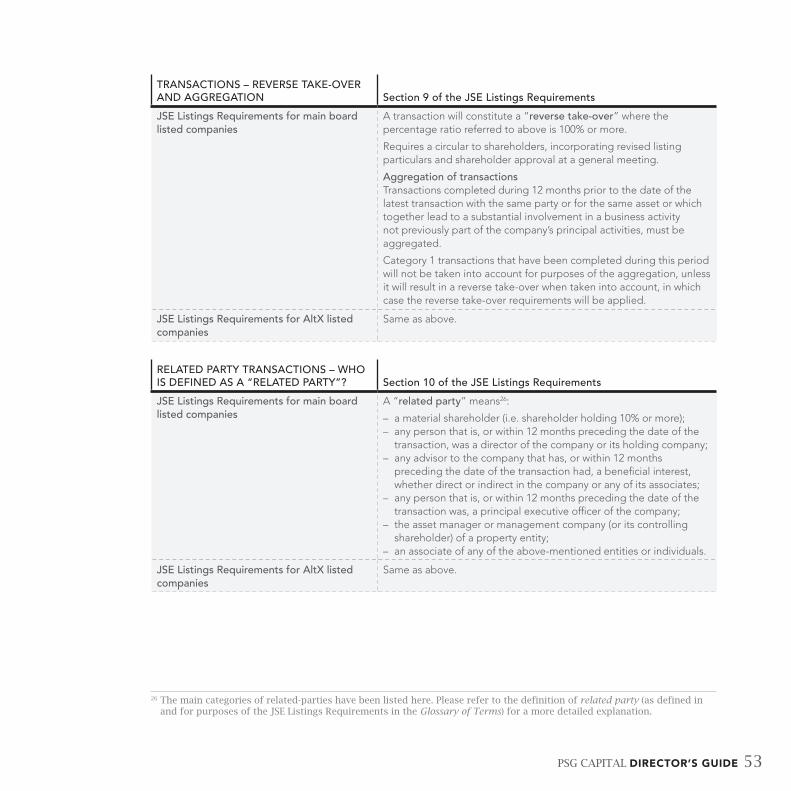

Transactions – reverse take-over and aggregation 53

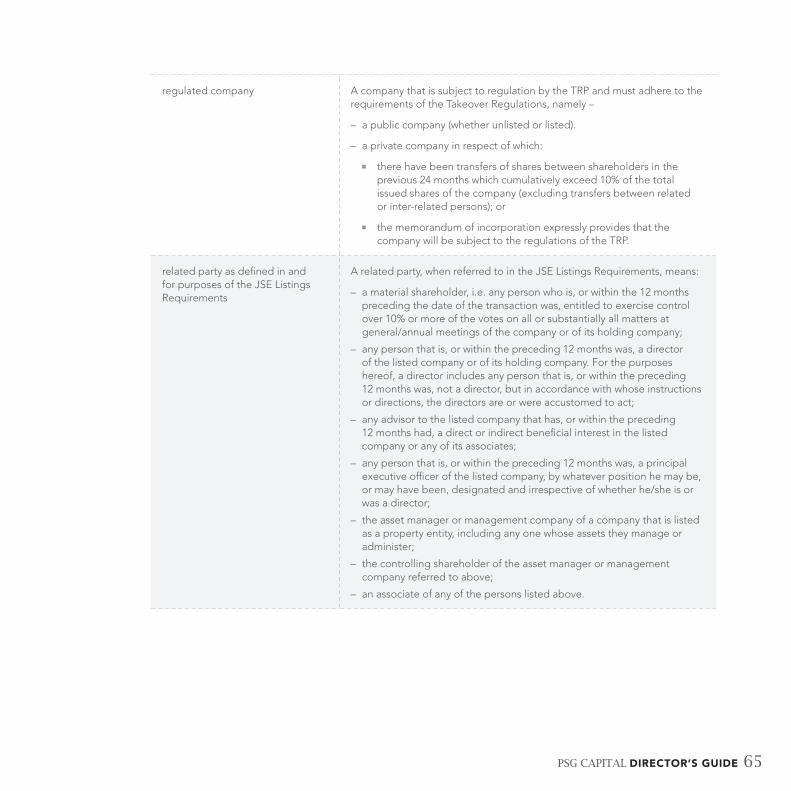

Related party transactions – Who is defined as a “related party”? 53

Related party transactions – categorisation 54

8 Summary of differences between King III and King IV: Board committees and disclosure requirements

55

9 Glossary of Terms 61

10 Disclaimer 69

PSG CAPITAL DIRECTOR’S GUIDE 1

INTRODUCTION 1This guide is intended to serve as a useful tool for directors and company secretaries when attending board meetings and board committee meetings. Depending on the industry in which directors operate, there may be other legislation (such as the Banks Act, No. 94 of 1990 that stipulates, for example, certain thresholds for a bank controlling company) or requirements by regulators, such as the Financial Services Board, that could have an influence. Directors are most welcome to contact PSG Capital with any specific queries in this regard.

The guide provides directors and company secretaries with general guidance on fulfilling the required standards of conduct and disclosure requirements in terms of the Companies Act and general guidance on the requirements of the JSE Listings Requirements when considering the approval of significant corporate actions.

The Companies Act provides shareholders with appraisal rights in certain circumstances. Companies that hold investments as a shareholder in other companies must comply with certain procedural formalities, failing which they could unintentionally forfeit their appraisal rights. This guide provides further guidance in this regard.

In addition, this guide sets out the requirements of the Companies Act, King IV and the JSE Listings Requirements regarding the composition of various board committees, and summarises select provisions of the JSE Listings Requirements as at the date hereof. Please contact us to provide you with updates or amendments until a new edition is published. PSG Capital, from time to time, notifies clients of amendments to the JSE Listings Requirements, as well as other statutory and regulatory changes. We have, for your convenience, included a sleeve at the back of this guide where such updates can be inserted.

The guide includes:

1. An important note on minute-taking and the disclosures, questions and notes that should be included in minutes of shareholder and board meetings.

2. Procedural steps for enforcing appraisal rights in terms of the Companies Act.

3. A synopsis of certain material corporate actions and the approvals required in order to implement such corporate actions, including the requirements to be met by the board in considering and approving the proposed corporate actions. PSG Capital has prepared standard templates for the board resolutions that can be tabled at board meetings to authorise each of the material corporate actions referred to in this manual. These templates will be made available on request to your company secretary and compliance officer in electronic format.

4. A synopsis of the requirements for, and functions of, board committees across the regulatory framework.

5. A synopsis of the definitions for non-executive and independent directors across the regulatory framework.

6. A summary of select provisions of the JSE Listings Requirements.

7. A summary of the differences between King III and King IV in relation to board committees and disclosure requirements.

Should you have questions or queries outside of this framework, you are welcome to contact PSG Capital.

The terminology used in this manual is explained and defined in the Glossary of Terms commencing on page 61.

2 PSG CAPITAL DIRECTOR’S GUIDE

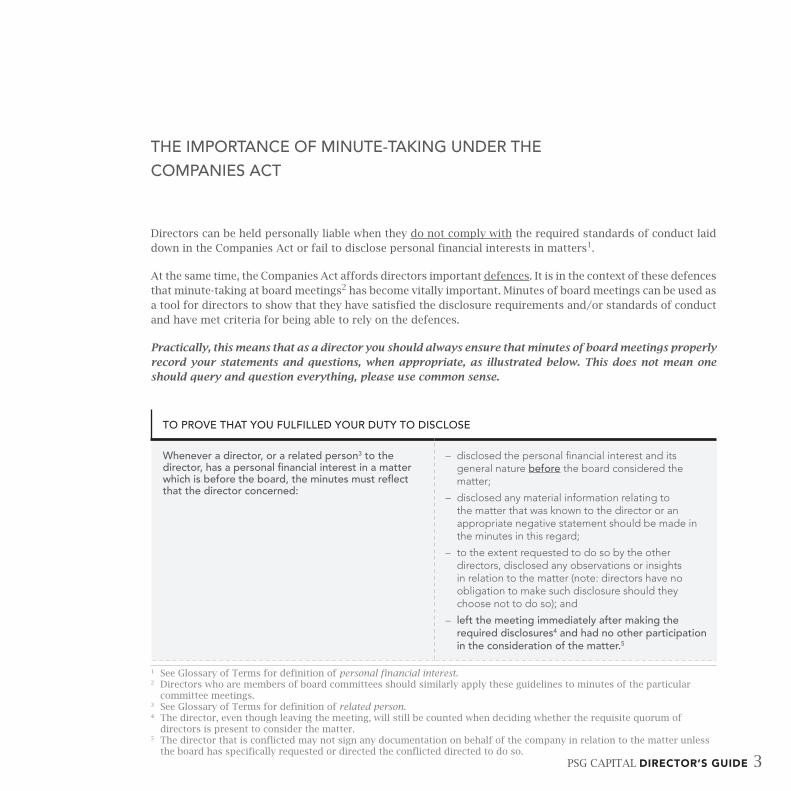

THE IMPORTANCE OF MINUTE-TAKING UNDER THE COMPANIES ACT

2chapter

PSG CAPITAL DIRECTOR’S GUIDE 3

THE IMPORTANCE OF MINUTE-TAKING UNDER THE COMPANIES ACT

Directors can be held personally liable when they do not comply with the required standards of conduct laid down in the Companies Act or fail to disclose personal financial interests in matters1.

At the same time, the Companies Act affords directors important defences. It is in the context of these defences that minute-taking at board meetings2 has become vitally important. Minutes of board meetings can be used as a tool for directors to show that they have satisfied the disclosure requirements and/or standards of conduct and have met criteria for being able to rely on the defences.

Practically, this means that as a director you should always ensure that minutes of board meetings properly record your statements and questions, when appropriate, as illustrated below. This does not mean one should query and question everything, please use common sense.

TO PROVE THAT YOU FULFILLED YOUR DUTY TO DISCLOSE

Whenever a director, or a related person3 to the director, has a personal financial interest in a matter which is before the board, the minutes must reflect that the director concerned:

– disclosed the personal financial interest and its general nature before the board considered the matter;

– disclosed any material information relating to the matter that was known to the director or an appropriate negative statement should be made in the minutes in this regard;

– to the extent requested to do so by the other directors, disclosed any observations or insights in relation to the matter (note: directors have no obligation to make such disclosure should they choose not to do so); and

– left the meeting immediately after making the required disclosures4 and had no other participation in the consideration of the matter.5

1 See Glossary of Terms for definition of personal financial interest.2 Directors who are members of board committees should similarly apply these guidelines to minutes of the particular

committee meetings.3 See Glossary of Terms for definition of related person.4 The director, even though leaving the meeting, will still be counted when deciding whether the requisite quorum of

directors is present to consider the matter.5 The director that is conflicted may not sign any documentation on behalf of the company in relation to the matter unless

the board has specifically requested or directed the conflicted directed to do so.

4 PSG CAPITAL DIRECTOR’S GUIDE

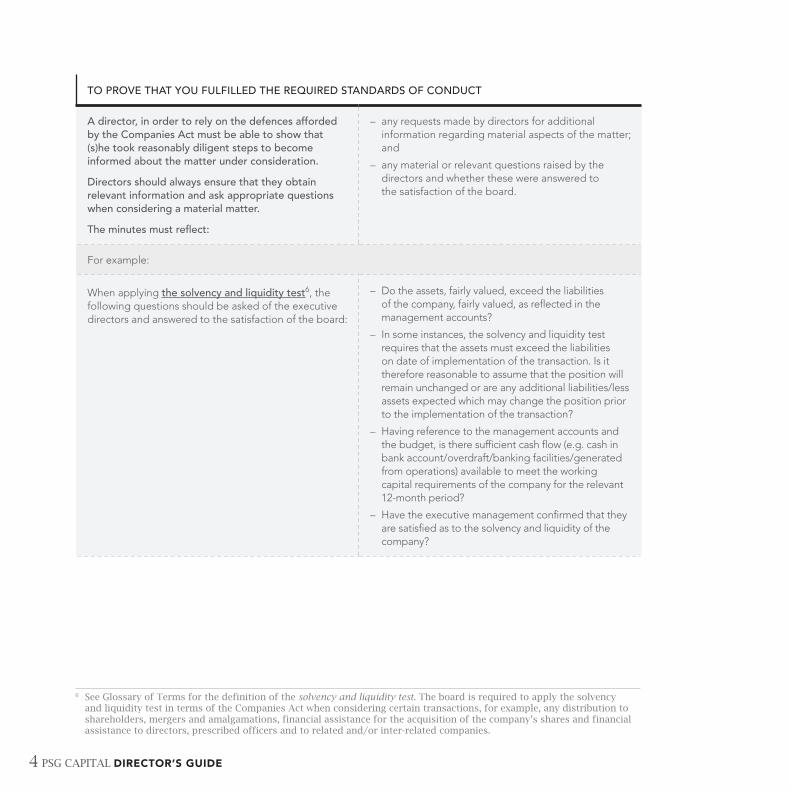

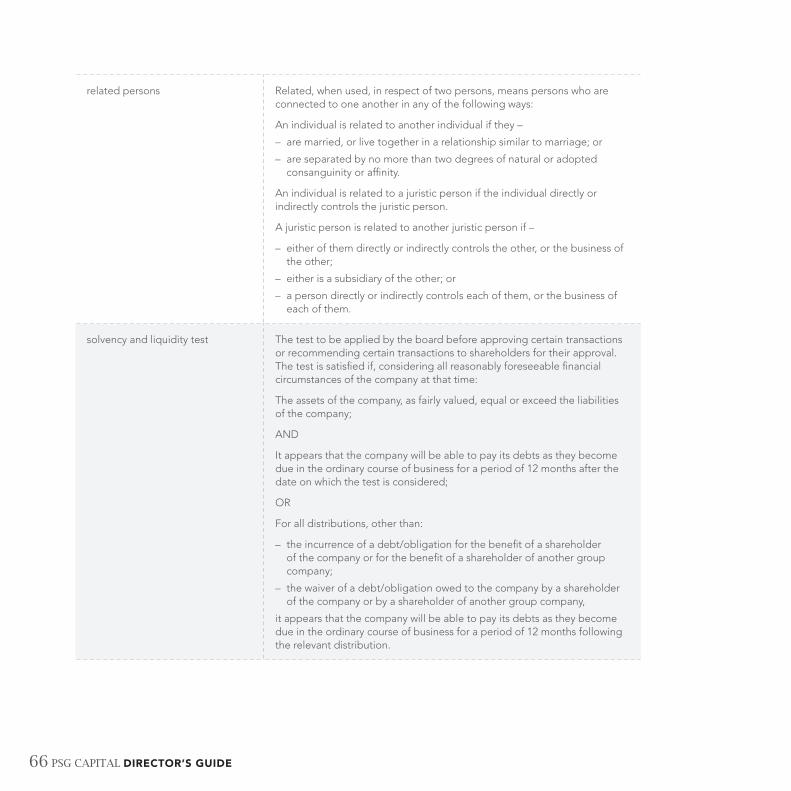

6 See Glossary of Terms for the definition of the solvency and liquidity test. The board is required to apply the solvency and liquidity test in terms of the Companies Act when considering certain transactions, for example, any distribution to shareholders, mergers and amalgamations, financial assistance for the acquisition of the company’s shares and financial assistance to directors, prescribed officers and to related and/or inter-related companies.

TO PROVE THAT YOU FULFILLED THE REQUIRED STANDARDS OF CONDUCT

A director, in order to rely on the defences afforded by the Companies Act must be able to show that (s)he took reasonably diligent steps to become informed about the matter under consideration.

Directors should always ensure that they obtain relevant information and ask appropriate questions when considering a material matter.

The minutes must reflect:

– any requests made by directors for additional information regarding material aspects of the matter; and

– any material or relevant questions raised by the directors and whether these were answered to the satisfaction of the board.

For example:

When applying the solvency and liquidity test6, the following questions should be asked of the executive directors and answered to the satisfaction of the board:

– Do the assets, fairly valued, exceed the liabilities of the company, fairly valued, as reflected in the management accounts?

– In some instances, the solvency and liquidity test requires that the assets must exceed the liabilities on date of implementation of the transaction. Is it therefore reasonable to assume that the position will remain unchanged or are any additional liabilities/less assets expected which may change the position prior to the implementation of the transaction?

– Having reference to the management accounts and the budget, is there sufficient cash flow (e.g. cash in bank account/overdraft/banking facilities/generated from operations) available to meet the working capital requirements of the company for the relevant 12-month period?

– Have the executive management confirmed that they are satisfied as to the solvency and liquidity of the company?

PSG CAPITAL DIRECTOR’S GUIDE 5

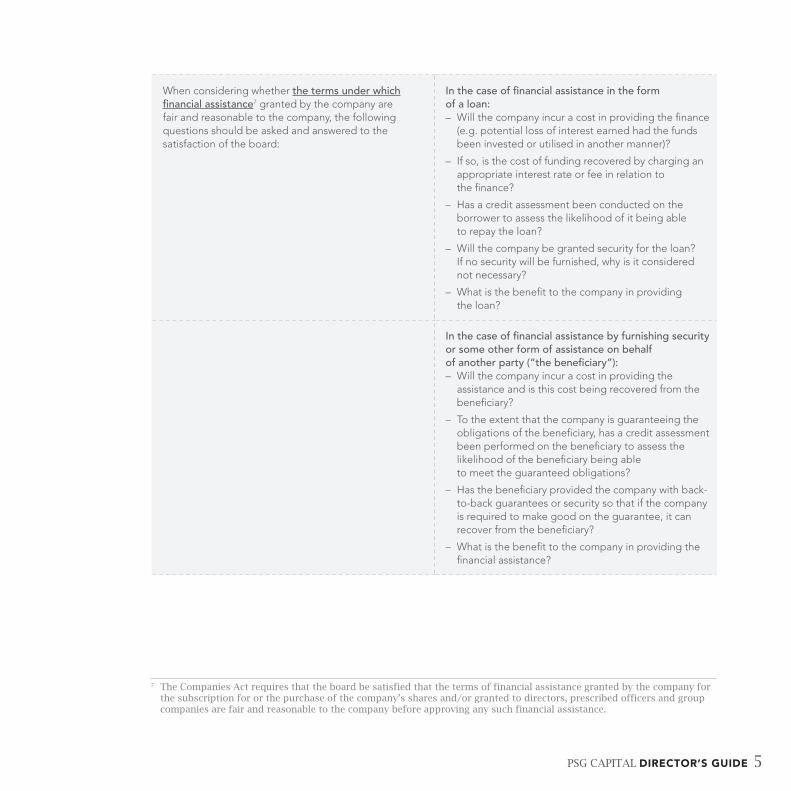

When considering whether the terms under which financial assistance7 granted by the company are fair and reasonable to the company, the following questions should be asked and answered to the satisfaction of the board:

In the case of financial assistance in the form of a loan:– Will the company incur a cost in providing the finance

(e.g. potential loss of interest earned had the funds been invested or utilised in another manner)?

– If so, is the cost of funding recovered by charging an appropriate interest rate or fee in relation to the finance?

– Has a credit assessment been conducted on the borrower to assess the likelihood of it being able to repay the loan?

– Will the company be granted security for the loan? If no security will be furnished, why is it considered not necessary?

– What is the benefit to the company in providing the loan?

In the case of financial assistance by furnishing security or some other form of assistance on behalf of another party (“the beneficiary”):– Will the company incur a cost in providing the

assistance and is this cost being recovered from the beneficiary?

– To the extent that the company is guaranteeing the obligations of the beneficiary, has a credit assessment been performed on the beneficiary to assess the likelihood of the beneficiary being able to meet the guaranteed obligations?

– Has the beneficiary provided the company with back-to-back guarantees or security so that if the company is required to make good on the guarantee, it can recover from the beneficiary?

– What is the benefit to the company in providing the financial assistance?

7 The Companies Act requires that the board be satisfied that the terms of financial assistance granted by the company for the subscription for or the purchase of the company’s shares and/or granted to directors, prescribed officers and group companies are fair and reasonable to the company before approving any such financial assistance.

6 PSG CAPITAL DIRECTOR’S GUIDE

Directors can rely on information, opinions, recommendations, reports or statements, including financial statements and other financial data, prepared or presented by employees, legal counsel, accountants or other professional persons retained by the company or presented by board committees of which the director is not a member, unless the director has reason to believe that the particular person or committee does not merit confidence.

Have the directors in considering any matters relied on any advice given, presentations made or documentation presented by an employee, board committee member or external professional expert?

If so, note this for recordal purposes in the minutes.

TO ASSIST WITH SHOWING THAT THE DIRECTORS ACTED IN THE BEST INTEREST OF THE COMPANY

The minutes, to the extent possible, should reflect that the director(s) took reasonably diligent steps to become informed about a matter and made the decision with a rational basis for believing, and did believe, that the decision was in the best interests of the company. This can be achieved by minuting the following:

That the directors expressly discussed the expected benefit of the particular transaction to the company.

The outcome of the discussion must be noted in the minutes.

TO PROVE THAT A DIRECTOR DID NOT VOTE IN FAVOUR OF A DECISION

Directors who conclude that they cannot support a particular matter for any reason, must ensure that the minutes reflect that:

The director voted against the decision.

Note: It is not sufficient to avoid liability simply by abstaining from voting on a matter8.

8 See section 77(3)(e) of the Companies Act which requires that a director votes against certain transactions (such as distributions, financial assistance to certain parties, share repurchases and issuing of shares) where such transactions do not meet the requirements of the Companies Act.

UNDERSTANDING APPRAISAL RIGHTS: CONSIDER CORRESPONDENCE REGARDING SHAREHOLDER RESOLUTIONS CAREFULLY

3chapter

PSG CAPITAL DIRECTOR’S GUIDE 7

UNDERSTANDING APPRAISAL RIGHTS: CONSIDER CORRESPONDENCE REGARDING SHAREHOLDER RESOLUTIONS CAREFULLY

The Companies Act creates appraisal rights for dissenting shareholders in cases where the requisite majority of the shareholders of a company have approved:

–ꢀ a fundamental transaction (i.e. a disposal of the whole or greater part of its assets or undertaking or a scheme of arrangement or an amalgamation or merger); and

–ꢀ an amendment to its MOI by altering the preferences, rights, limitations or other terms of any class of its shares which will have a material adverse affect on the rights or interests of the dissenting shareholder.

The appraisal rights allow a dissenting shareholder to sell its full shareholding back to the company at the fair value of the shares. This creates an effective put option for the minority shareholder in circumstances where the below-mentioned steps are followed.

Dissenting shareholders may inadvertently forfeit their appraisal rights if they receive correspondence from investee companies tabling a resolution to vote on any of these matters and do not take the required procedural steps.

This means that if your company holds shares in investee companies, special attention must always be paid to notices or correspondence issued by the investee companies convening a meeting or tabling a resolution to decide on any the matters referred to above.

The procedural formalities are as follows:

Step 1: At any time before the proposed resolution is to be voted on, the dissenting shareholder must give the investee company written notice objecting to the resolution.

Step 2: The dissenting shareholder must then vote against the resolution (note: it is not sufficient simply to abstain from voting). The dissenting shareholder should ensure that his dissenting vote is adequately recorded by the investee company.

Step 3: If the resolution is passed, the investee company is obliged to notify the dissenting shareholder, within 10 business days, of the adoption of the resolution. The dissenting shareholder then has 20 business days from receipt of the notice, or if no notice is sent by the investee company, within 20 business days of becoming aware that the resolution was passed, to send the investee company a written demand to pay the dissenting shareholder the fair value for all of the shares held by that shareholder (a copy of this demand must also be delivered to the TRP).

8 PSG CAPITAL DIRECTOR’S GUIDE

Step 4: After receiving the demand, the investee company will make an offer to the dissenting shareholder to buy its shares at a price as determined by the directors to be the fair value thereof. The dissenting shareholder has 30 business days after receipt of the offer:

–ꢀ to accept the offer; or

–ꢀ approach a court for relief if it considers that the price is not the fair value of the shares, failing which the offer lapses and the dissenting shareholder has no further appraisal rights.

The offer will include a statement showing how the fair value was determined. Dissenting shareholders who disagree with the fair value can refer the matter to court for a final determination of the fair value.

SYNOPSIS: COMPANIES ACT AND REGULATORY REQUIREMENTS FOR SELECTED CORPORATE ACTIONS

4chapter

PSG CAPITAL DIRECTOR’S GUIDE 9

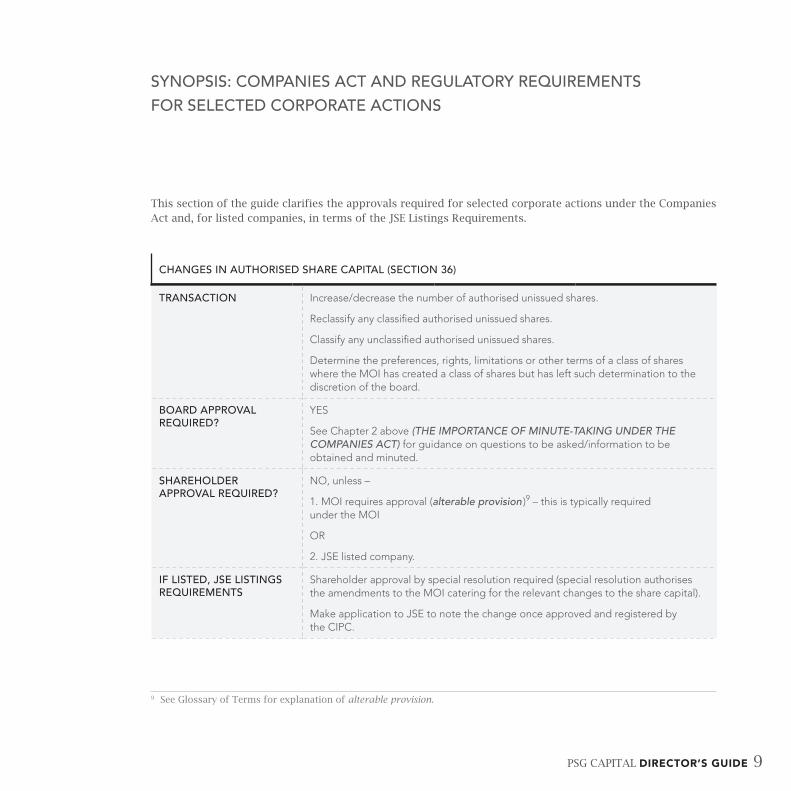

SYNOPSIS: COMPANIES ACT AND REGULATORY REQUIREMENTS FOR SELECTED CORPORATE ACTIONS

This section of the guide clarifies the approvals required for selected corporate actions under the Companies Act and, for listed companies, in terms of the JSE Listings Requirements.

CHANGES IN AUTHORISED SHARE CAPITAL (SECTION 36)

TRANSACTION Increase/decrease the number of authorised unissued shares.

Reclassify any classified authorised unissued shares.

Classify any unclassified authorised unissued shares.

Determine the preferences, rights, limitations or other terms of a class of shares where the MOI has created a class of shares but has left such determination to the discretion of the board.

BOARD APPROVAL REQUIRED?

YES

See Chapter 2 above (THE IMPORTANCE OF MINUTE-TAKING UNDER THE COMPANIES ACT) for guidance on questions to be asked/information to be obtained and minuted.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

1. MOI requires approval (alterable provision )9 – this is typically required under the MOI

OR

2. JSE listed company.

IF LISTED, JSE LISTINGS REQUIREMENTS

Shareholder approval by special resolution required (special resolution authorises the amendments to the MOI catering for the relevant changes to the share capital).

Make application to JSE to note the change once approved and registered by the CIPC.

9 See Glossary of Terms for explanation of alterable provision.

10 PSG CAPITAL DIRECTOR’S GUIDE

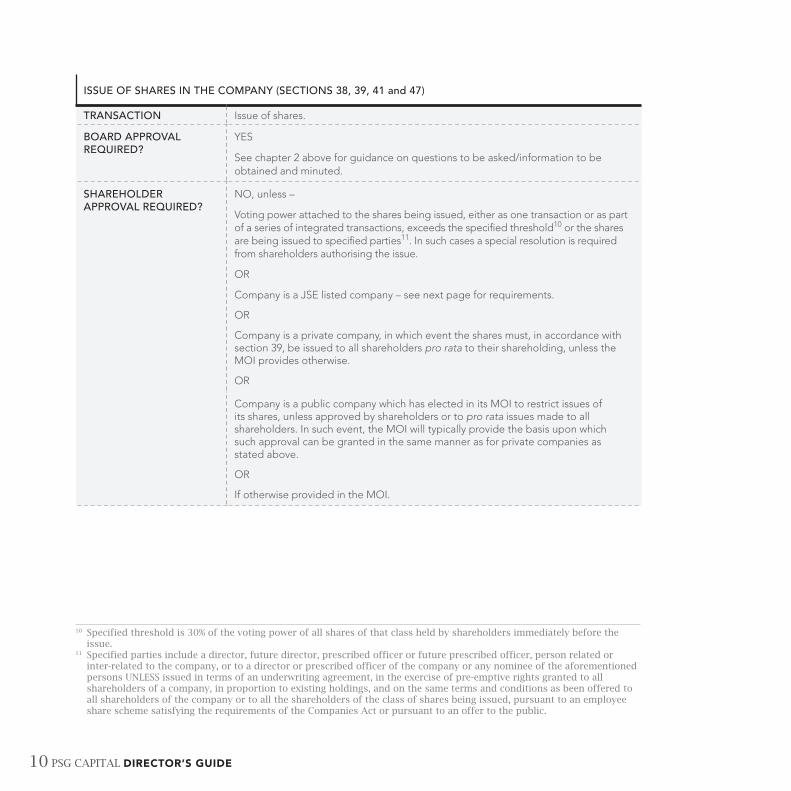

10 Specified threshold is 30% of the voting power of all shares of that class held by shareholders immediately before the issue.

11 Specified parties include a director, future director, prescribed officer or future prescribed officer, person related or inter-related to the company, or to a director or prescribed officer of the company or any nominee of the aforementioned persons UNLESS issued in terms of an underwriting agreement, in the exercise of pre-emptive rights granted to all shareholders of a company, in proportion to existing holdings, and on the same terms and conditions as been offered to all shareholders of the company or to all the shareholders of the class of shares being issued, pursuant to an employee share scheme satisfying the requirements of the Companies Act or pursuant to an offer to the public.

ISSUE OF SHARES IN THE COMPANY (SECTIONS 38, 39, 41 and 47)

TRANSACTION Issue of shares.

BOARD APPROVAL REQUIRED?

YES

See chapter 2 above for guidance on questions to be asked/information to be obtained and minuted.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

Voting power attached to the shares being issued, either as one transaction or as part of a series of integrated transactions, exceeds the specified threshold10 or the shares are being issued to specified parties11. In such cases a special resolution is required from shareholders authorising the issue.

OR

Company is a JSE listed company – see next page for requirements.

OR

Company is a private company, in which event the shares must, in accordance with section 39, be issued to all shareholders pro rata to their shareholding, unless the MOI provides otherwise.

OR

Company is a public company which has elected in its MOI to restrict issues of its shares, unless approved by shareholders or to pro rata issues made to all shareholders. In such event, the MOI will typically provide the basis upon which such approval can be granted in the same manner as for private companies as stated above.

OR

If otherwise provided in the MOI.

PSG CAPITAL DIRECTOR’S GUIDE 11

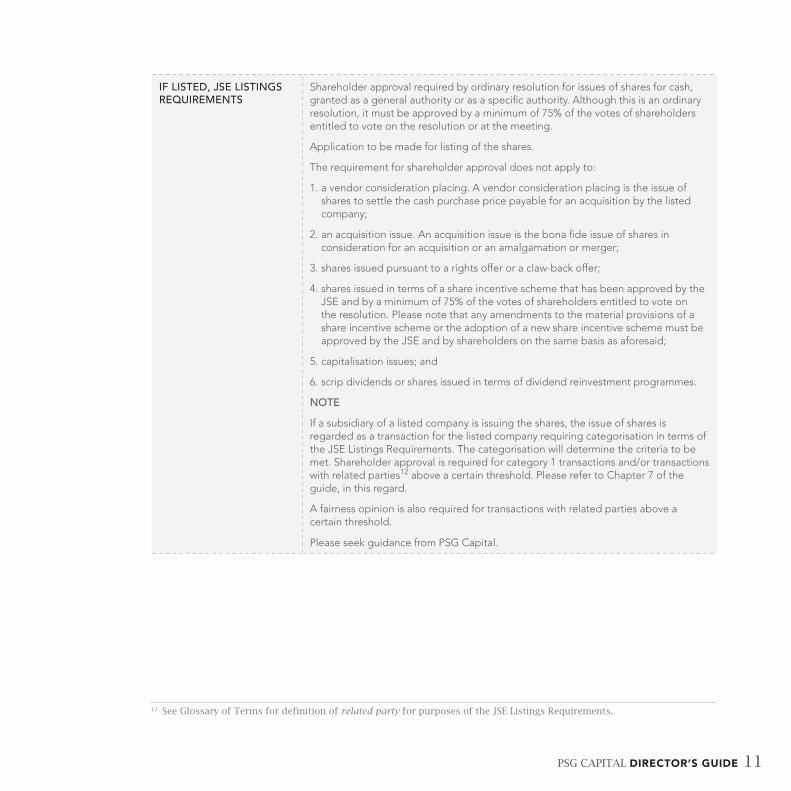

IF LISTED, JSE LISTINGS REQUIREMENTS

Shareholder approval required by ordinary resolution for issues of shares for cash, granted as a general authority or as a specific authority. Although this is an ordinary resolution, it must be approved by a minimum of 75% of the votes of shareholders entitled to vote on the resolution or at the meeting.

Application to be made for listing of the shares.

The requirement for shareholder approval does not apply to:

1. a vendor consideration placing. A vendor consideration placing is the issue of shares to settle the cash purchase price payable for an acquisition by the listed company;

2. an acquisition issue. An acquisition issue is the bona fide issue of shares in consideration for an acquisition or an amalgamation or merger;

3. shares issued pursuant to a rights offer or a claw-back offer;

4. shares issued in terms of a share incentive scheme that has been approved by the JSE and by a minimum of 75% of the votes of shareholders entitled to vote on the resolution. Please note that any amendments to the material provisions of a share incentive scheme or the adoption of a new share incentive scheme must be approved by the JSE and by shareholders on the same basis as aforesaid;

5. capitalisation issues; and

6. scrip dividends or shares issued in terms of dividend reinvestment programmes.

NOTE

If a subsidiary of a listed company is issuing the shares, the issue of shares is regarded as a transaction for the listed company requiring categorisation in terms of the JSE Listings Requirements. The categorisation will determine the criteria to be met. Shareholder approval is required for category 1 transactions and/or transactions with related parties12 above a certain threshold. Please refer to Chapter 7 of the guide, in this regard.

A fairness opinion is also required for transactions with related parties above a certain threshold.

Please seek guidance from PSG Capital.

12 See Glossary of Terms for definition of related party for purposes of the JSE Listings Requirements.

12 PSG CAPITAL DIRECTOR’S GUIDE

ISSUE OF SHARES IN THE COMPANY (SECTIONS 38, 39, 41 and 47) (continued)

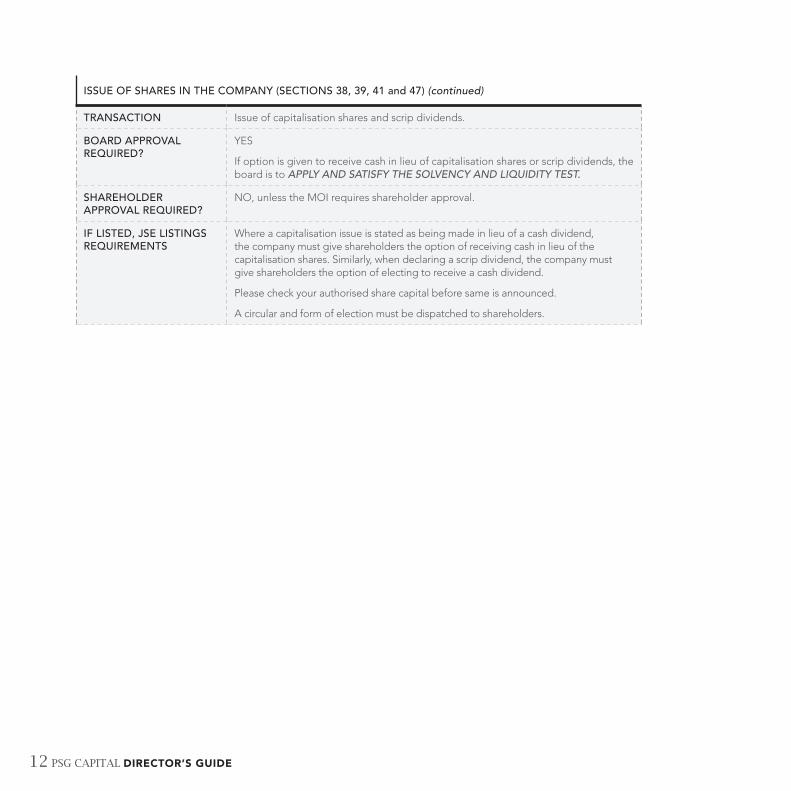

TRANSACTION Issue of capitalisation shares and scrip dividends.

BOARD APPROVAL REQUIRED?

YES

If option is given to receive cash in lieu of capitalisation shares or scrip dividends, the board is to APPLY AND SATISFY THE SOLVENCY AND LIQUIDITY TEST.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless the MOI requires shareholder approval.

IF LISTED, JSE LISTINGS REQUIREMENTS

Where a capitalisation issue is stated as being made in lieu of a cash dividend, the company must give shareholders the option of receiving cash in lieu of the capitalisation shares. Similarly, when declaring a scrip dividend, the company must give shareholders the option of electing to receive a cash dividend.

Please check your authorised share capital before same is announced.

A circular and form of election must be dispatched to shareholders.

PSG CAPITAL DIRECTOR’S GUIDE 13

FINANCIAL ASSISTANCE GIVEN BY THE COMPANY FOR THE SUBSCRIPTION FOR OR PURCHASE OF SHARES IN THE COMPANY OR IN A RELATED OR INTER-RELATED COMPANY (SECTION 44)13

Not applicable to lending money in the ordinary course of business by a company whose primary business is money lending (for example, a bank).

TRANSACTION Company making a loan for the acquisition of or subscription for its shares.

Company making a loan for the acquisition of or subscription for shares in a related or inter-related company14.

Company giving any other form of assistance for such acquisition or subscription (e.g. providing security for a loan).

BOARD APPROVAL REQUIRED?

YES

APPLY AND SATISFY SOLVENCY AND LIQUIDITY TEST

Board must be satisfied that immediately after giving the assistance, the company will satisfy the solvency and liquidity test.

TERMS FAIR AND REASONABLE

Board must be satisfied that the terms of the assistance are fair and reasonable to the company15.

MOI PROVISIONS MET, IF APPLICABLE

Board to ensure that any conditions/restrictions set out in the MOI have been satisfied.

SHAREHOLDER APPROVAL REQUIRED?

YES – by special resolution authorising the assistance for a specific recipient or generally for a category of potential recipients. The authority, once granted, is valid for a two-year period.

EXCEPTION

Shareholder approval is not required where the assistance is granted pursuant to an employee share scheme meeting the requirements of the Companies Act.

IF LISTED, JSE LISTINGS REQUIREMENTS

Depending on the circumstances, the JSE may regard the financing and any security furnished by the company as an acquisition. If so, the financial assistance should be categorised.

Shareholder approval required for category 1 transactions and/or transactions with related parties above a certain threshold.

Fairness opinions also required for transactions with related parties above a certain threshold.

Please seek guidance from PSG Capital at an early stage to confirm the application of the JSE Listings Requirements to the particular financial assistance.

13 Boards must, when considering financial assistance, take cognisance of the National Credit Act and ensure compliance with its provisions, to the extent applicable.

14 See Glossary of Terms for definitions of related persons and inter-related persons.15 The board, depending on the circumstances of the particular financial assistance, should consider whether it would be

appropriate to brief an independent third party to express an opinion on whether the terms of the financial assistance are fair and reasonable to the company.

14 PSG CAPITAL DIRECTOR’S GUIDE

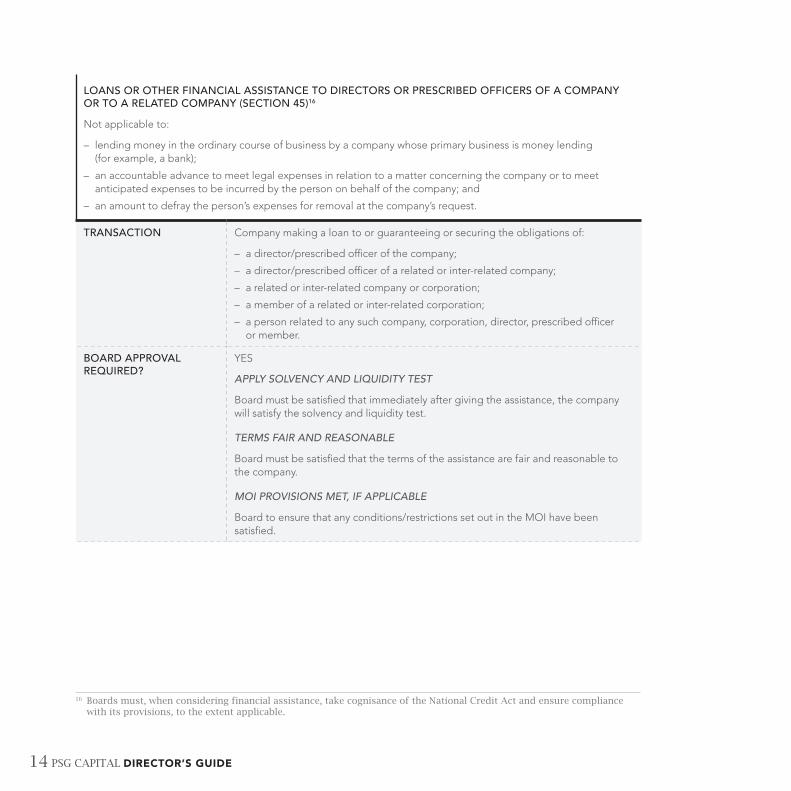

LOANS OR OTHER FINANCIAL ASSISTANCE TO DIRECTORS OR PRESCRIBED OFFICERS OF A COMPANY OR TO A RELATED COMPANY (SECTION 45)16

Not applicable to:

– lending money in the ordinary course of business by a company whose primary business is money lending (for example, a bank);

– an accountable advance to meet legal expenses in relation to a matter concerning the company or to meet anticipated expenses to be incurred by the person on behalf of the company; and

– an amount to defray the person’s expenses for removal at the company’s request.

TRANSACTION Company making a loan to or guaranteeing or securing the obligations of:

– a director/prescribed officer of the company;– a director/prescribed officer of a related or inter-related company;– a related or inter-related company or corporation;– a member of a related or inter-related corporation;– a person related to any such company, corporation, director, prescribed officer

or member.

BOARD APPROVAL REQUIRED?

YES

APPLY SOLVENCY AND LIQUIDITY TEST

Board must be satisfied that immediately after giving the assistance, the company will satisfy the solvency and liquidity test.

TERMS FAIR AND REASONABLE

Board must be satisfied that the terms of the assistance are fair and reasonable to the company.

MOI PROVISIONS MET, IF APPLICABLE

Board to ensure that any conditions/restrictions set out in the MOI have been satisfied.

16 Boards must, when considering financial assistance, take cognisance of the National Credit Act and ensure compliance with its provisions, to the extent applicable.

PSG CAPITAL DIRECTOR’S GUIDE 15

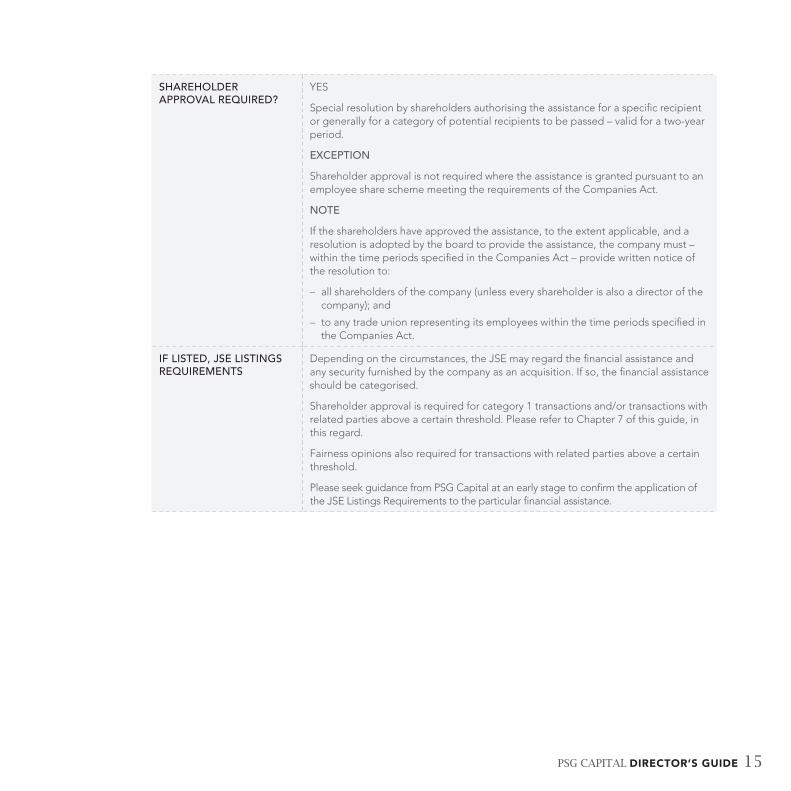

SHAREHOLDER APPROVAL REQUIRED?

YES

Special resolution by shareholders authorising the assistance for a specific recipient or generally for a category of potential recipients to be passed – valid for a two-year period.

EXCEPTION

Shareholder approval is not required where the assistance is granted pursuant to an employee share scheme meeting the requirements of the Companies Act.

NOTE

If the shareholders have approved the assistance, to the extent applicable, and a resolution is adopted by the board to provide the assistance, the company must – within the time periods specified in the Companies Act – provide written notice of the resolution to:

– all shareholders of the company (unless every shareholder is also a director of the company); and

– to any trade union representing its employees within the time periods specified in the Companies Act.

IF LISTED, JSE LISTINGS REQUIREMENTS

Depending on the circumstances, the JSE may regard the financial assistance and any security furnished by the company as an acquisition. If so, the financial assistance should be categorised.

Shareholder approval is required for category 1 transactions and/or transactions with related parties above a certain threshold. Please refer to Chapter 7 of this guide, in this regard.

Fairness opinions also required for transactions with related parties above a certain threshold.

Please seek guidance from PSG Capital at an early stage to confirm the application of the JSE Listings Requirements to the particular financial assistance.

16 PSG CAPITAL DIRECTOR’S GUIDE

DISTRIBUTIONS (SECTION 46)

Distributions include the declaration of dividends, payments in lieu of capitalisation shares, share repurchases, any other payment to shareholders, incurrence of debt obligations for the benefit of a shareholder of the company or a shareholder of a group company or the waiver of an obligation owing by a shareholder or shareholder of a group company.

Not applicable to distributions made on final liquidation of the company or share repurchases resulting from a shareholder exercising the appraisal rights in terms of section 164 of the Companies Act.

TRANSACTION Declaration of dividends/payment in lieu of capitalisation shares/other payments to shareholders.

BOARD APPROVAL REQUIRED?

YES, unless –

Done pursuant to an existing legal obligation or a court order, in which case the board need not approve the distribution per se but even then must apply the solvency and liquidity test.

APPLY SOLVENCY AND LIQUIDITY TEST

Board may only approve, if it reasonably appears that immediately after making the distribution, the company will satisfy the solvency and liquidity test.

NOTE

If the distribution, or any part thereof, contemplated in the authorising board resolution, court order or existing legal obligation is not carried out within 120 business days after the board applied the solvency and liquidity test, the board must reconsider the test with respect to the distribution or any remaining portion thereof and must adopt a further resolution acknowledging that the test was applied and met, before proceeding with the distribution.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

The MOI requires shareholder approval.

OR

There is legal precedent that a distribution amounting to a disposal by the company of all or the greater part of its assets or undertakings requires shareholder approval by way of the special resolution (certain exceptions apply where such shareholder approval is not required, for example, when the distribution is by a wholly-owned subsidiary to its holding company).

OR

Company is listed and the distribution is not being made to all shareholders pro rata to their shareholding or involves unbundling of unlisted shares to shareholders.

IF LISTED, JSE LISTINGS REQUIREMENTS

Shareholder approval is not required if the distribution is being made to all shareholders pro rata to their shareholding and does not relate to unbundling of unlisted shares to shareholders.

Otherwise, require approval from shareholders in terms of the JSE Listings Requirements.

PSG CAPITAL DIRECTOR’S GUIDE 17

DISTRIBUTIONS (SECTION 46) (continued)

Distributions include the declaration of dividends, payments in lieu of capitalisation shares, share repurchases, any other payment to shareholders, incurrence of debt obligations for a shareholder of the company or a shareholder of a group company or the waiver of an obligation owing by a shareholder or shareholder of a group company.

Not applicable to distributions made on final liquidation of the company or share repurchases resulting from a shareholder exercising the appraisal rights in terms of section 164 of the Companies Act.

TRANSACTION The incurrence of a debt/obligation for the benefit of a shareholder of the company or for the benefit of a shareholder of another group company.

OR

The waiver of a debt/obligation owed to the company by a shareholder of the company or by a shareholder of another group company.

BOARD APPROVAL REQUIRED?

YES, unless –

Pursuant to an existing legal obligation or a court order, in which case the board need not approve the distribution per se but even then must apply the solvency and liquidity test.

APPLY SOLVENCY AND LIQUIDITY TEST

Board may only approve, if it reasonably appears that immediately after making the distribution, the company will satisfy the solvency and liquidity test.

NOTE

Requirement only applies at the time that the board resolves that the company may incur the obligation and not to any subsequent satisfaction of the obligation (unless resolution or terms of the obligation provide otherwise).

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

The MOI requires shareholder approval.

OR

The company is listed, in which event the incurrence of a debt/obligation or the waiver of debt/obligation may have to comply with the JSE Listings Requirements.

IF LISTED, JSE LISTINGS REQUIREMENTS

Depending on the circumstances, the JSE may regard a waiver of a debt/obligation as a disposal. If so, the transaction should be categorised.

Shareholder approval is required for category 1 transactions and/or transactions with related parties above a certain threshold.

Depending on the circumstances, the JSE may regard the incurrence of a debt/obligation on behalf of a shareholder, or the waiver thereof, to be a specific payment to a shareholder.

Please seek guidance from PSG Capital at an early stage to confirm the application of the JSE Listings Requirements to the particular transaction.

18 PSG CAPITAL DIRECTOR’S GUIDE

SHARE REPURCHASES (SECTION 48)

Not applicable to shares acquired and consideration paid by a company pursuant to shareholders exercising their appraisal rights in terms of section 164 of the Companies Act or the redemption of securities in accordance with the terms of those securities.

TRANSACTION Company repurchasing its own shares.

BOARD APPROVAL REQUIRED?

YES

APPLY SOLVENCY AND LIQUIDITY TEST

Board may only approve the repurchase if it reasonably appears that immediately after making the distribution (i.e repurchasing the shares), the company will satisfy the solvency and liquidity test.

NOTE

If the share repurchase, or any part thereof, contemplated in the authorising board resolution, court order or existing legal obligation, is not carried out within 120 business days after the board applied the test, the board must reconsider the test with respect to the share repurchase or any remaining portion thereof and must adopt a further resolution acknowledging that the test was applied and met, before proceeding with the share repurchase.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

The company is listed and the shares are not being repurchased from all shareholders on a pro rata basis.

OR

The MOI requires shareholder approval.

OR

The shares are to be acquired by the company from a director or prescribed officer of the company, or a person related to a director or prescribed officer of the company, in which case shareholder approval by way of a special resolution will be required.

OR

The repurchase considered alone or together with other transactions in an integrated series of transactions involves the acquisition by the company of more than 5% of the issued shares of any class of the company’s shares. In this instance, a report will need to be prepared by an independent expert, and will be distributed to shareholders, and the repurchase will require shareholder approval by way of a special resolution.

IF LISTED, JSE LISTINGS REQUIREMENTS

If shares are not being repurchased from all shareholders pro rata to their shareholding, a special resolution is required authorising the repurchase as a general authority or as a specific authority and compliance is required with relevant JSE Listings Requirements.

PSG CAPITAL DIRECTOR’S GUIDE 19

SHARE REPURCHASES (SECTION 48) (continued)

Not applicable to shares acquired and consideration paid by a company pursuant to shareholders exercising their appraisal rights in terms of section 164 of the Companies Act, or the redemption of securities in accordance with the terms of those securities.

TRANSACTION Subsidiary company purchasing shares of its holding company.

BOARD APPROVAL REQUIRED?

YES

APPLY SOLVENCY AND LIQUIDITY TEST

The board may only approve the distribution if it reasonably appears that immediately after making the distribution, the company will satisfy the solvency and liquidity test.

NOTE

If the share repurchase, or any part thereof, contemplated in the authorising board resolution, court order or existing legal obligation is not carried out within 120 business days after the board applied test, board must reconsider the test with respect to the share repurchase or any remaining portion thereof and must adopt a further resolution acknowledging that the test was applied and met, before proceeding with the share repurchase.

SHAREHOLDER APPROVAL REQUIRED?

NO, unless –

The holding company is listed and shares are not being repurchased by the subsidiary from all shareholders of the holding company on a pro rata basis.

OR

The MOI requires shareholder approval.

IF LISTED, JSE LISTINGS REQUIREMENTS

If the shares are not repurchased pro rata from all shareholders of the listed holding company, a special resolution is required authorising the repurchase as a general authority or as a specific authority and compliance is required with relevant JSE Listings Requirements.

20 PSG CAPITAL DIRECTOR’S GUIDE

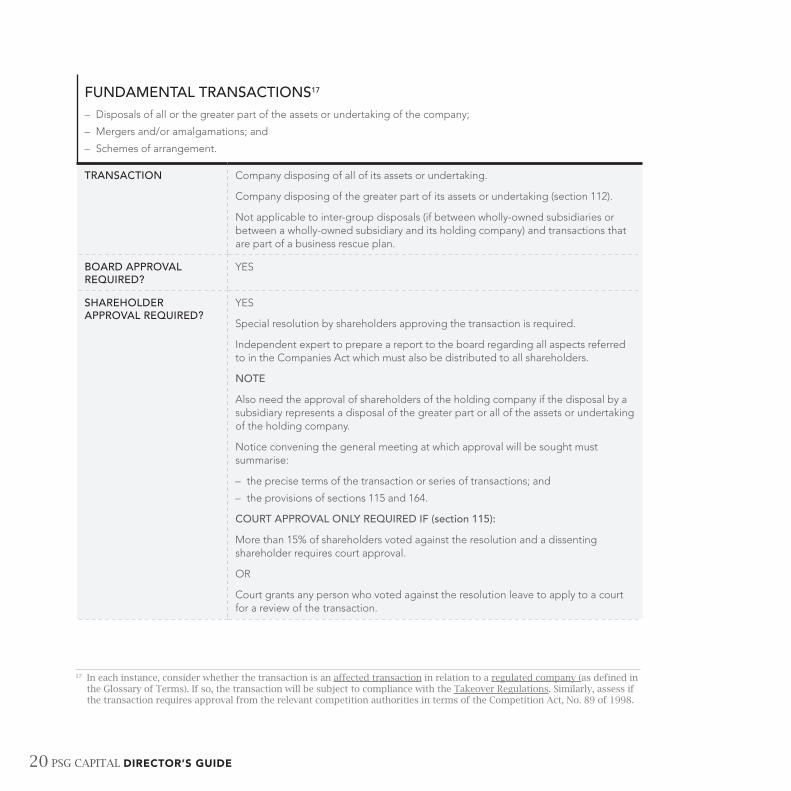

FUNDAMENTAL TRANSACTIONS17

– Disposals of all or the greater part of the assets or undertaking of the company;– Mergers and/or amalgamations; and– Schemes of arrangement.

TRANSACTION Company disposing of all of its assets or undertaking.

Company disposing of the greater part of its assets or undertaking (section 112).

Not applicable to inter-group disposals (if between wholly-owned subsidiaries or between a wholly-owned subsidiary and its holding company) and transactions that are part of a business rescue plan.

BOARD APPROVAL REQUIRED?

YES

SHAREHOLDER APPROVAL REQUIRED?

YES

Special resolution by shareholders approving the transaction is required.

Independent expert to prepare a report to the board regarding all aspects referred to in the Companies Act which must also be distributed to all shareholders.

NOTE

Also need the approval of shareholders of the holding company if the disposal by a subsidiary represents a disposal of the greater part or all of the assets or undertaking of the holding company.

Notice convening the general meeting at which approval will be sought must summarise:

– the precise terms of the transaction or series of transactions; and– the provisions of sections 115 and 164.

COURT APPROVAL ONLY REQUIRED IF (section 115):

More than 15% of shareholders voted against the resolution and a dissenting shareholder requires court approval.

OR

Court grants any person who voted against the resolution leave to apply to a court for a review of the transaction.

17 In each instance, consider whether the transaction is an affected transaction in relation to a regulated company (as defined in the Glossary of Terms). If so, the transaction will be subject to compliance with the Takeover Regulations. Similarly, assess if the transaction requires approval from the relevant competition authorities in terms of the Competition Act, No. 89 of 1998.

PSG CAPITAL DIRECTOR’S GUIDE 21

TRIGGERS APPRAISAL RIGHTS (section 164)18

If an eligible shareholder has invoked its shareholder appraisal rights, the company must repurchase such shareholder’s shares at the fair value thereof in accordance with the requirements of section 164.

IF LISTED, JSE LISTINGS REQUIREMENTS

Category 1 disposal requiring an announcement, circular and shareholder approval. If transaction is concluded with a related party, a fairness opinion will be required.

There are a number of other implications for the continued listing of the company which must also be considered. For example, will the company be a cash shell going forward? Will it be necessary to delist the company? Please seek guidance from PSG Capital at an early stage in the process regarding the requirements and implications of the transaction from a JSE Listings Requirements perspective.

18 Since all fundamental transactions trigger an appraisal right for shareholders, companies that would be obliged to repurchase the shares of their shareholders in light of a proposed transaction should, to the extent appropriate, ensure that the contract regulating the transaction gives them recourse to recoup any amounts paid to shareholders in this regard from the counterparty.

22 PSG CAPITAL DIRECTOR’S GUIDE

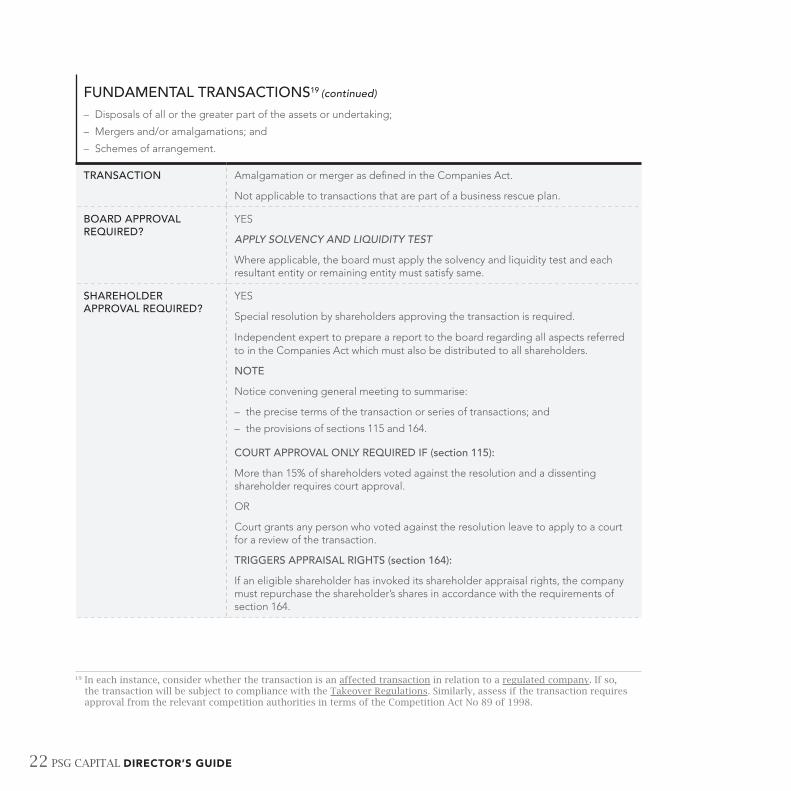

FUNDAMENTAL TRANSACTIONS19 (continued)

– Disposals of all or the greater part of the assets or undertaking;– Mergers and/or amalgamations; and– Schemes of arrangement.

TRANSACTION Amalgamation or merger as defined in the Companies Act.

Not applicable to transactions that are part of a business rescue plan.

BOARD APPROVAL REQUIRED?

YES

APPLY SOLVENCY AND LIQUIDITY TEST

Where applicable, the board must apply the solvency and liquidity test and each resultant entity or remaining entity must satisfy same.

SHAREHOLDER APPROVAL REQUIRED?

YES

Special resolution by shareholders approving the transaction is required.

Independent expert to prepare a report to the board regarding all aspects referred to in the Companies Act which must also be distributed to all shareholders.

NOTE

Notice convening general meeting to summarise:

– the precise terms of the transaction or series of transactions; and– the provisions of sections 115 and 164.

COURT APPROVAL ONLY REQUIRED IF (section 115):

More than 15% of shareholders voted against the resolution and a dissenting shareholder requires court approval.

OR

Court grants any person who voted against the resolution leave to apply to a court for a review of the transaction.

TRIGGERS APPRAISAL RIGHTS (section 164):

If an eligible shareholder has invoked its shareholder appraisal rights, the company must repurchase the shareholder’s shares in accordance with the requirements of section 164.

19 In each instance, consider whether the transaction is an affected transaction in relation to a regulated company. If so, the transaction will be subject to compliance with the Takeover Regulations. Similarly, assess if the transaction requires approval from the relevant competition authorities in terms of the Competition Act No 89 of 1998.

PSG CAPITAL DIRECTOR’S GUIDE 23

20 See section 116 of the Companies Act for remedies available to creditors.

PRACTICALITIES THAT MUST BE ATTENDED TO

Once the special resolution has been approved:

– The company must give notice of the proposed merger/amalgamation to every creditor of the company; and

– File a notice of amalgamation or merger in accordance with requirements of the Companies Act with CIPC20.

IF LISTED, JSE LISTINGS REQUIREMENTS

Myriad of potential implications from the perspective of the JSE Listings Requirements. For example, a merger or amalgamation may result in:

– Listed entity having to be delisted;– Revised listing particulars having to be issued for a listed company;– A category 1 transaction for a listed entity; or– A related party transaction requiring shareholder approval and/or a fairness

opinion.Please seek guidance from PSG Capital at an early stage in this regard.

24 PSG CAPITAL DIRECTOR’S GUIDE

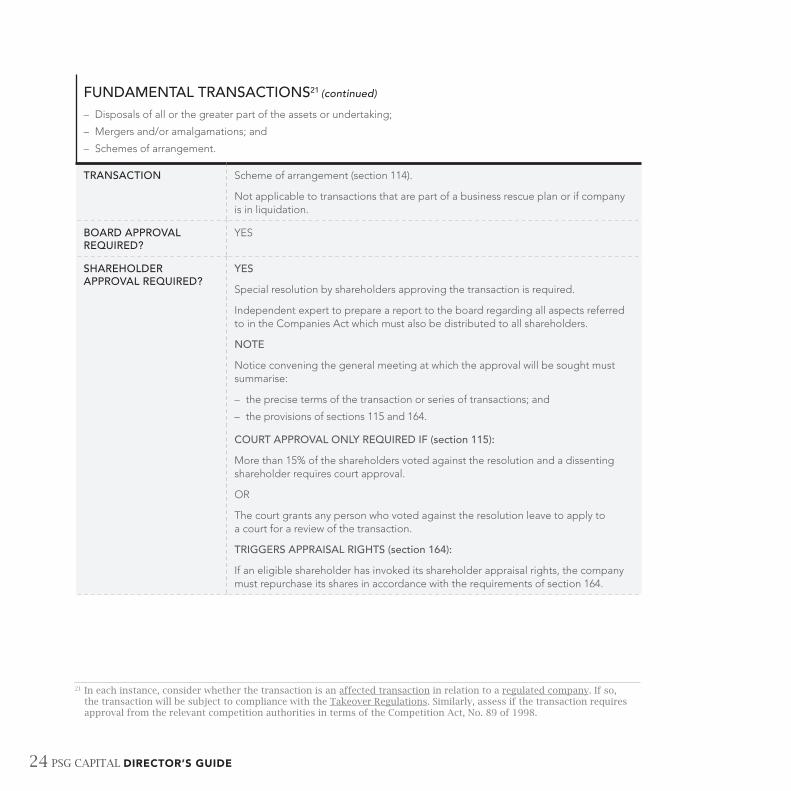

FUNDAMENTAL TRANSACTIONS21 (continued)

– Disposals of all or the greater part of the assets or undertaking;– Mergers and/or amalgamations; and– Schemes of arrangement.

TRANSACTION Scheme of arrangement (section 114).

Not applicable to transactions that are part of a business rescue plan or if company is in liquidation.

BOARD APPROVAL REQUIRED?

YES

SHAREHOLDER APPROVAL REQUIRED?

YES

Special resolution by shareholders approving the transaction is required.

Independent expert to prepare a report to the board regarding all aspects referred to in the Companies Act which must also be distributed to all shareholders.

NOTE

Notice convening the general meeting at which the approval will be sought must summarise:

– the precise terms of the transaction or series of transactions; and– the provisions of sections 115 and 164.

COURT APPROVAL ONLY REQUIRED IF (section 115):

More than 15% of the shareholders voted against the resolution and a dissenting shareholder requires court approval.

OR

The court grants any person who voted against the resolution leave to apply to a court for a review of the transaction.

TRIGGERS APPRAISAL RIGHTS (section 164):

If an eligible shareholder has invoked its shareholder appraisal rights, the company must repurchase its shares in accordance with the requirements of section 164.

21 In each instance, consider whether the transaction is an affected transaction in relation to a regulated company. If so, the transaction will be subject to compliance with the Takeover Regulations. Similarly, assess if the transaction requires approval from the relevant competition authorities in terms of the Competition Act, No. 89 of 1998.

PSG CAPITAL DIRECTOR’S GUIDE 25

IF LISTED, JSE LISTINGS REQUIREMENTS

Myriad of potential implications from the perspective of the JSE Listings Requirements. For example, the transaction may result in:

– Listed entity having to be delisted;

– Revised listing particulars having to be issued for a listed company;

– A category 1 transaction for a listed entity; or

– A related party transaction requiring shareholder approval and/or fairness opinion.

Please seek guidance from PSG Capital at an early stage in this regard.

26 PSG CAPITAL DIRECTOR’S GUIDE

SYNOPSIS: BOARD COMMITTEES ACROSS THE REGULATORY FRAMEWORK

5chapter

PSG CAPITAL DIRECTOR’S GUIDE 27

SYNOPSIS: BOARD COMMITTEES ACROSS THE REGULATORY FRAMEWORK

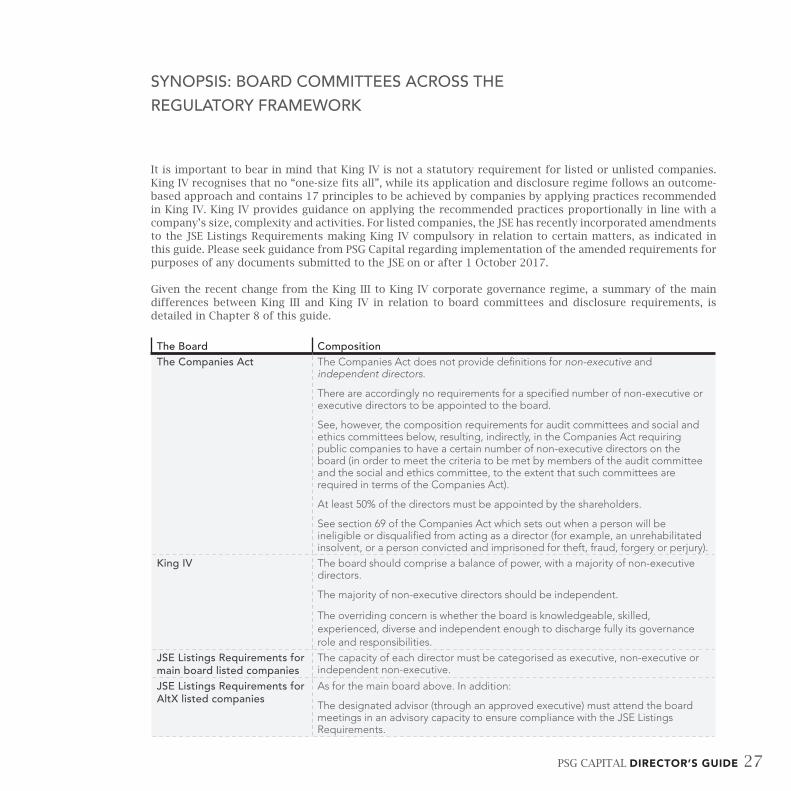

It is important to bear in mind that King IV is not a statutory requirement for listed or unlisted companies. King IV recognises that no “one-size fits all”, while its application and disclosure regime follows an outcome-based approach and contains 17 principles to be achieved by companies by applying practices recommended in King IV. King IV provides guidance on applying the recommended practices proportionally in line with a company’s size, complexity and activities. For listed companies, the JSE has recently incorporated amendments to the JSE Listings Requirements making King IV compulsory in relation to certain matters, as indicated in this guide. Please seek guidance from PSG Capital regarding implementation of the amended requirements for purposes of any documents submitted to the JSE on or after 1 October 2017.

Given the recent change from the King III to King IV corporate governance regime, a summary of the main differences between King III and King IV in relation to board committees and disclosure requirements, is detailed in Chapter 8 of this guide.

The Board CompositionThe Companies Act The Companies Act does not provide definitions for non-executive and

independent directors.

There are accordingly no requirements for a specified number of non-executive or executive directors to be appointed to the board.

See, however, the composition requirements for audit committees and social and ethics committees below, resulting, indirectly, in the Companies Act requiring public companies to have a certain number of non-executive directors on the board (in order to meet the criteria to be met by members of the audit committee and the social and ethics committee, to the extent that such committees are required in terms of the Companies Act).

At least 50% of the directors must be appointed by the shareholders.

See section 69 of the Companies Act which sets out when a person will be ineligible or disqualified from acting as a director (for example, an unrehabilitated insolvent, or a person convicted and imprisoned for theft, fraud, forgery or perjury).

King IV The board should comprise a balance of power, with a majority of non-executive directors.

The majority of non-executive directors should be independent.

The overriding concern is whether the board is knowledgeable, skilled, experienced, diverse and independent enough to discharge fully its governance role and responsibilities.

JSE Listings Requirements for main board listed companies

The capacity of each director must be categorised as executive, non-executive or independent non-executive.

JSE Listings Requirements for AltX listed companies

As for the main board above. In addition:

The designated advisor (through an approved executive) must attend the board meetings in an advisory capacity to ensure compliance with the JSE Listings Requirements.

28 PSG CAPITAL DIRECTOR’S GUIDE

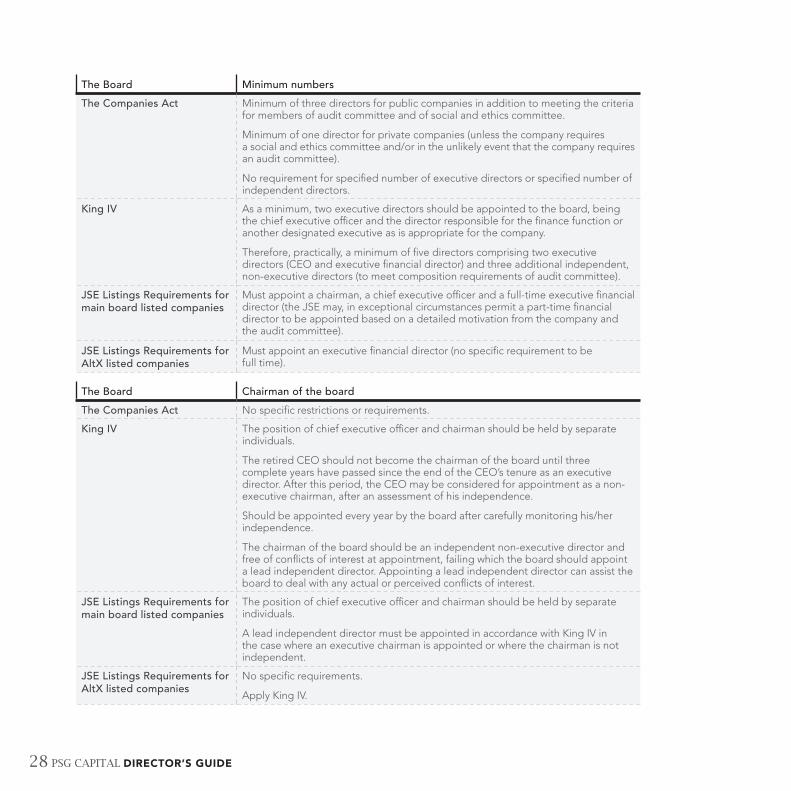

The Board Minimum numbers

The Companies Act Minimum of three directors for public companies in addition to meeting the criteria for members of audit committee and of social and ethics committee.

Minimum of one director for private companies (unless the company requires a social and ethics committee and/or in the unlikely event that the company requires an audit committee).

No requirement for specified number of executive directors or specified number of independent directors.

King IV As a minimum, two executive directors should be appointed to the board, being the chief executive officer and the director responsible for the finance function or another designated executive as is appropriate for the company.

Therefore, practically, a minimum of five directors comprising two executive directors (CEO and executive financial director) and three additional independent, non-executive directors (to meet composition requirements of audit committee).

JSE Listings Requirements for main board listed companies

Must appoint a chairman, a chief executive officer and a full-time executive financial director (the JSE may, in exceptional circumstances permit a part-time financial director to be appointed based on a detailed motivation from the company and the audit committee).

JSE Listings Requirements for AltX listed companies

Must appoint an executive financial director (no specific requirement to be full time).

The Board Chairman of the board

The Companies Act No specific restrictions or requirements.

King IV The position of chief executive officer and chairman should be held by separate individuals.

The retired CEO should not become the chairman of the board until three complete years have passed since the end of the CEO’s tenure as an executive director. After this period, the CEO may be considered for appointment as a non-executive chairman, after an assessment of his independence.

Should be appointed every year by the board after carefully monitoring his/her independence.

The chairman of the board should be an independent non-executive director and free of conflicts of interest at appointment, failing which the board should appoint a lead independent director. Appointing a lead independent director can assist the board to deal with any actual or perceived conflicts of interest.

JSE Listings Requirements for main board listed companies

The position of chief executive officer and chairman should be held by separate individuals.

A lead independent director must be appointed in accordance with King IV in the case where an executive chairman is appointed or where the chairman is not independent.

JSE Listings Requirements for AltX listed companies

No specific requirements.

Apply King IV.

PSG CAPITAL DIRECTOR’S GUIDE 29

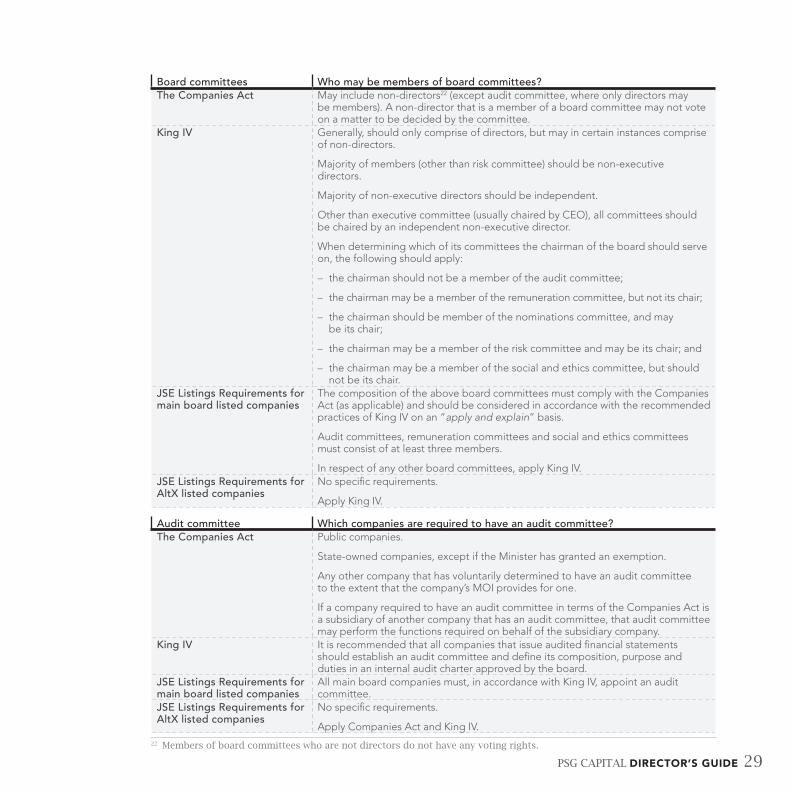

Board committees Who may be members of board committees?The Companies Act May include non-directors22 (except audit committee, where only directors may

be members). A non-director that is a member of a board committee may not vote on a matter to be decided by the committee.

King IV Generally, should only comprise of directors, but may in certain instances comprise of non-directors.

Majority of members (other than risk committee) should be non-executive directors.

Majority of non-executive directors should be independent.

Other than executive committee (usually chaired by CEO), all committees should be chaired by an independent non-executive director.

When determining which of its committees the chairman of the board should serve on, the following should apply:

– the chairman should not be a member of the audit committee;

– the chairman may be a member of the remuneration committee, but not its chair;

– the chairman should be member of the nominations committee, and may be its chair;

– the chairman may be a member of the risk committee and may be its chair; and

– the chairman may be a member of the social and ethics committee, but should not be its chair.

JSE Listings Requirements for main board listed companies

The composition of the above board committees must comply with the Companies Act (as applicable) and should be considered in accordance with the recommended practices of King IV on an “apply and explain” basis.

Audit committees, remuneration committees and social and ethics committees must consist of at least three members.

In respect of any other board committees, apply King IV.JSE Listings Requirements for AltX listed companies

No specific requirements.

Apply King IV.

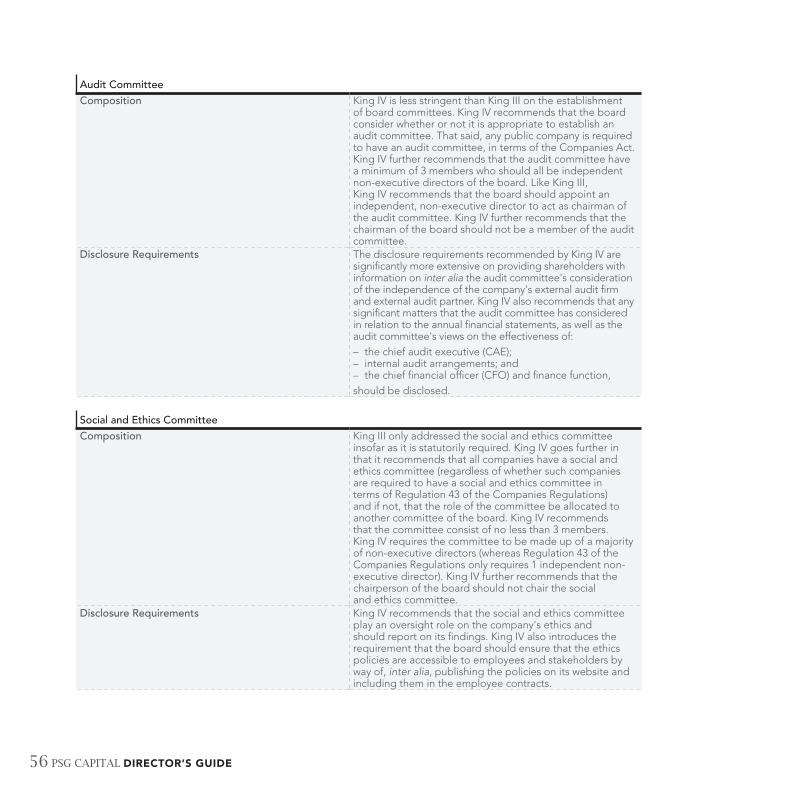

Audit committee Which companies are required to have an audit committee?The Companies Act Public companies.

State-owned companies, except if the Minister has granted an exemption.

Any other company that has voluntarily determined to have an audit committee to the extent that the company’s MOI provides for one.

If a company required to have an audit committee in terms of the Companies Act is a subsidiary of another company that has an audit committee, that audit committee may perform the functions required on behalf of the subsidiary company.

King IV It is recommended that all companies that issue audited financial statements should establish an audit committee and define its composition, purpose and duties in an internal audit charter approved by the board.

JSE Listings Requirements for main board listed companies

All main board companies must, in accordance with King IV, appoint an audit committee.

JSE Listings Requirements for AltX listed companies

No specific requirements.

Apply Companies Act and King IV.22 Members of board committees who are not directors do not have any voting rights.

30 PSG CAPITAL DIRECTOR’S GUIDE

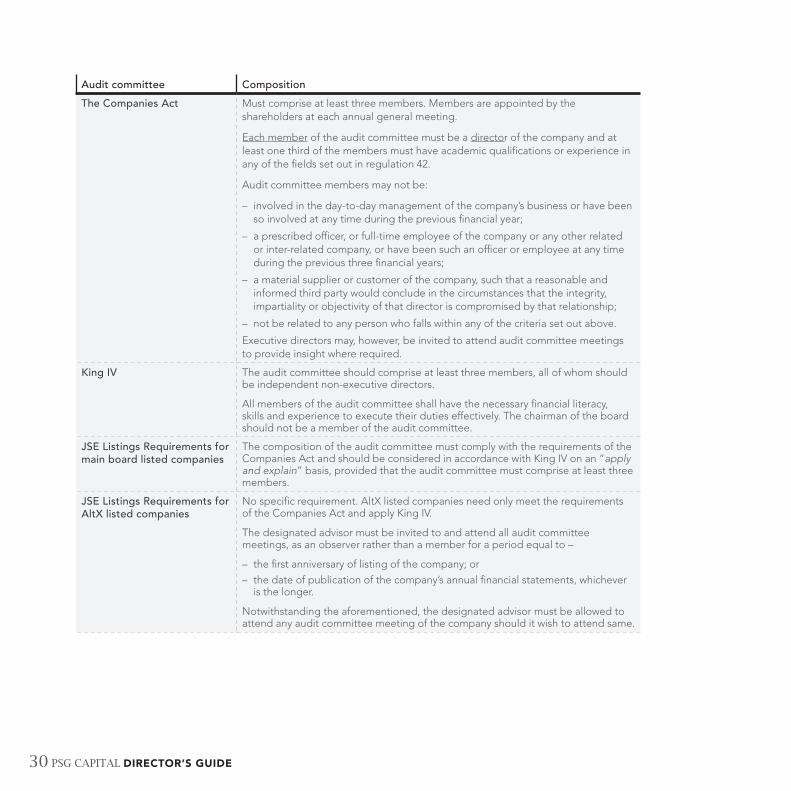

Audit committee Composition

The Companies Act Must comprise at least three members. Members are appointed by the shareholders at each annual general meeting.

Each member of the audit committee must be a director of the company and at least one third of the members must have academic qualifications or experience in any of the fields set out in regulation 42.

Audit committee members may not be:

– involved in the day-to-day management of the company’s business or have been so involved at any time during the previous financial year;

– a prescribed officer, or full-time employee of the company or any other related or inter-related company, or have been such an officer or employee at any time during the previous three financial years;

– a material supplier or customer of the company, such that a reasonable and informed third party would conclude in the circumstances that the integrity, impartiality or objectivity of that director is compromised by that relationship;

– not be related to any person who falls within any of the criteria set out above.Executive directors may, however, be invited to attend audit committee meetings to provide insight where required.

King IV The audit committee should comprise at least three members, all of whom should be independent non-executive directors.

All members of the audit committee shall have the necessary financial literacy, skills and experience to execute their duties effectively. The chairman of the board should not be a member of the audit committee.

JSE Listings Requirements for main board listed companies

The composition of the audit committee must comply with the requirements of the Companies Act and should be considered in accordance with King IV on an “apply and explain” basis, provided that the audit committee must comprise at least three members.

JSE Listings Requirements for AltX listed companies

No specific requirement. AltX listed companies need only meet the requirements of the Companies Act and apply King IV.

The designated advisor must be invited to and attend all audit committee meetings, as an observer rather than a member for a period equal to –

– the first anniversary of listing of the company; or– the date of publication of the company’s annual financial statements, whichever

is the longer.

Notwithstanding the aforementioned, the designated advisor must be allowed to attend any audit committee meeting of the company should it wish to attend same.

PSG CAPITAL DIRECTOR’S GUIDE 31

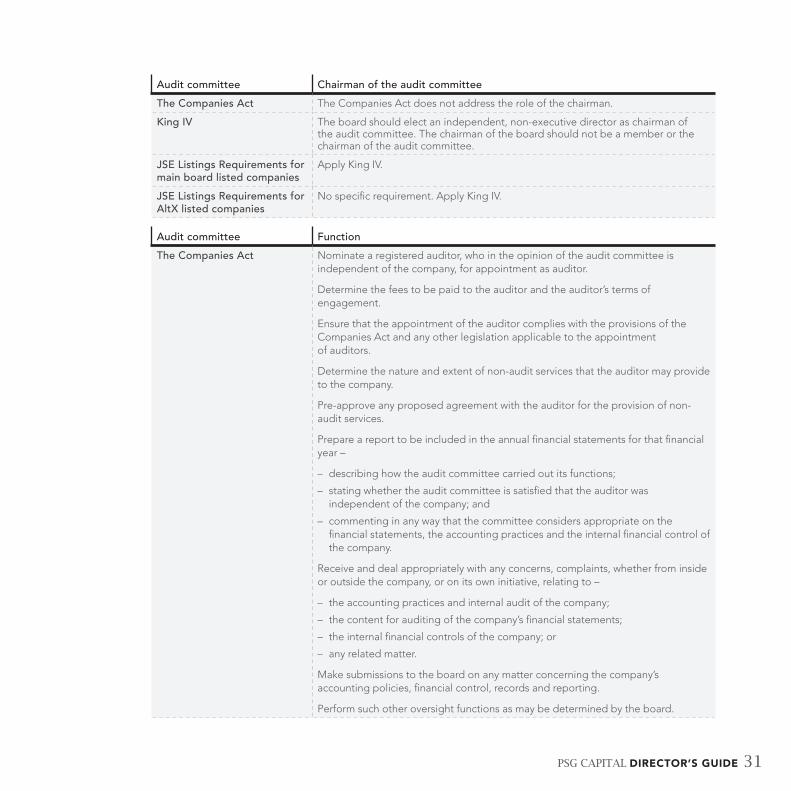

Audit committee Chairman of the audit committee

The Companies Act The Companies Act does not address the role of the chairman.

King IV The board should elect an independent, non-executive director as chairman of the audit committee. The chairman of the board should not be a member or the chairman of the audit committee.

JSE Listings Requirements for main board listed companies

Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Audit committee Function

The Companies Act Nominate a registered auditor, who in the opinion of the audit committee is independent of the company, for appointment as auditor.

Determine the fees to be paid to the auditor and the auditor’s terms of engagement.

Ensure that the appointment of the auditor complies with the provisions of the Companies Act and any other legislation applicable to the appointment of auditors.

Determine the nature and extent of non-audit services that the auditor may provide to the company.

Pre-approve any proposed agreement with the auditor for the provision of non-audit services.

Prepare a report to be included in the annual financial statements for that financial year –

– describing how the audit committee carried out its functions; – stating whether the audit committee is satisfied that the auditor was

independent of the company; and– commenting in any way that the committee considers appropriate on the

financial statements, the accounting practices and the internal financial control of the company.

Receive and deal appropriately with any concerns, complaints, whether from inside or outside the company, or on its own initiative, relating to –

– the accounting practices and internal audit of the company;– the content for auditing of the company’s financial statements;– the internal financial controls of the company; or– any related matter.

Make submissions to the board on any matter concerning the company’s accounting policies, financial control, records and reporting.

Perform such other oversight functions as may be determined by the board.

32 PSG CAPITAL DIRECTOR’S GUIDE

King IV The audit committee should oversee integrated reporting.

The audit committee should ensure that a combined assurance model is applied to provide a coordinated approach to all assurance activities.

The audit committee should satisfy itself of the expertise, resources and experience of the company’s finance function.

The audit committee should be responsible for overseeing internal audit.

The audit committee should be an integral component of the risk management process.

Whether or not the governance of risk is delegated to the audit committee, the audit committee should oversee the management of financial and other risks that affect the integrity of external reports issued by the company.

The audit committee is responsible for recommending the appointment of the external auditor and overseeing the external audit process.

The audit committee is responsible for ensuring that the external auditor is independent of the company.

The audit committee should consider IT as it relates to financial reporting and the going concern of the company.

The audit committee should consider the use of technology to improve audit coverage and efficiency.

The audit committee should report to the board and shareholders on how it has discharged its duties.

JSE Listings Requirements for main board listed companies

Apply King IV.

In addition, the audit committee must consider, on an annual basis, and satisfy itself of the appropriateness of the expertise and experience of the financial director. The company must confirm this by reporting to shareholders in its annual report that the audit committee has executed this responsibility.

The audit committee must also ensure that the company has established appropriate financial reporting procedures and that such procedures are operating.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply the Companies Act and King IV.

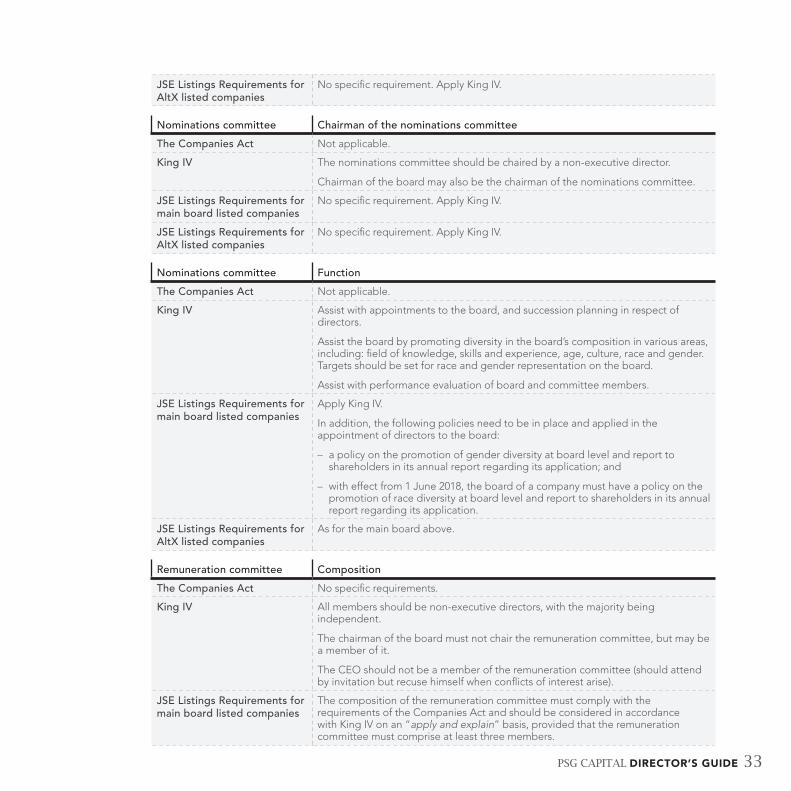

Nominations committee Composition

The Companies Act No specific requirements.

King IV All members should be non-executive directors and the majority should be independent.

Should be chaired by an independent non-executive director. The chairman of the board should be a member of the nominations committee, and may also be its chair.

The CEO should not be a member of the nominations committee (should attend by invitation, but recuse himself when conflicts of interest arise).

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

PSG CAPITAL DIRECTOR’S GUIDE 33

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Nominations committee Chairman of the nominations committee

The Companies Act Not applicable.

King IV The nominations committee should be chaired by a non-executive director.

Chairman of the board may also be the chairman of the nominations committee.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Nominations committee Function

The Companies Act Not applicable.

King IV Assist with appointments to the board, and succession planning in respect of directors.

Assist the board by promoting diversity in the board’s composition in various areas, including: field of knowledge, skills and experience, age, culture, race and gender. Targets should be set for race and gender representation on the board.

Assist with performance evaluation of board and committee members.

JSE Listings Requirements for main board listed companies

Apply King IV.

In addition, the following policies need to be in place and applied in the appointment of directors to the board:

– a policy on the promotion of gender diversity at board level and report to shareholders in its annual report regarding its application; and

– with effect from 1 June 2018, the board of a company must have a policy on the promotion of race diversity at board level and report to shareholders in its annual report regarding its application.

JSE Listings Requirements for AltX listed companies

As for the main board above.

Remuneration committee Composition

The Companies Act No specific requirements.

King IV All members should be non-executive directors, with the majority being independent.

The chairman of the board must not chair the remuneration committee, but may be a member of it.

The CEO should not be a member of the remuneration committee (should attend by invitation but recuse himself when conflicts of interest arise).

JSE Listings Requirements for main board listed companies

The composition of the remuneration committee must comply with the requirements of the Companies Act and should be considered in accordance with King IV on an “apply and explain” basis, provided that the remuneration committee must comprise at least three members.

34 PSG CAPITAL DIRECTOR’S GUIDE

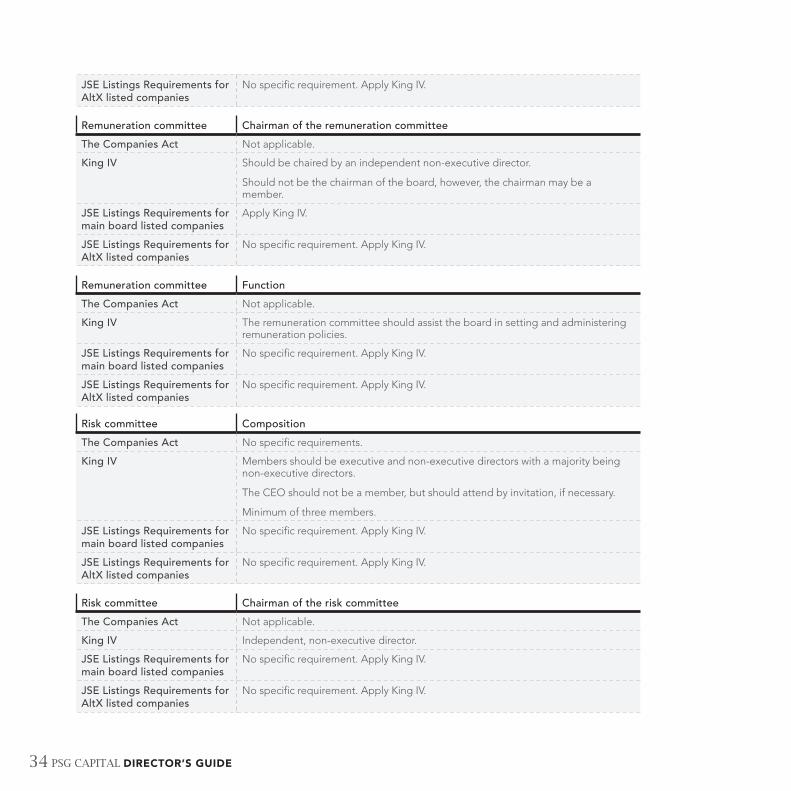

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Remuneration committee Chairman of the remuneration committee

The Companies Act Not applicable.

King IV Should be chaired by an independent non-executive director.

Should not be the chairman of the board, however, the chairman may be a member.

JSE Listings Requirements for main board listed companies

Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Remuneration committee Function

The Companies Act Not applicable.

King IV The remuneration committee should assist the board in setting and administering remuneration policies.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

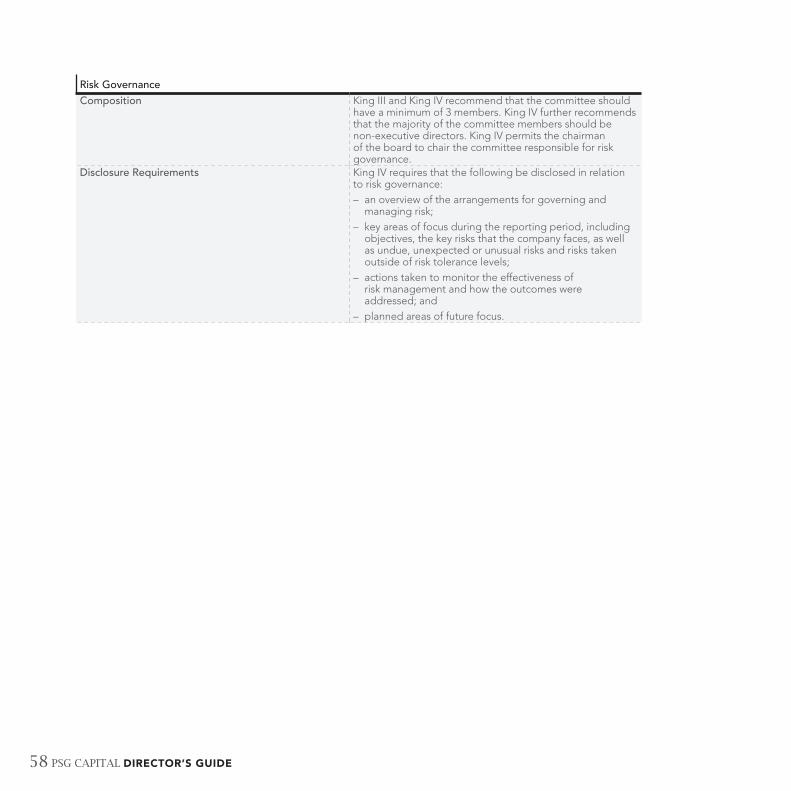

Risk committee Composition

The Companies Act No specific requirements.

King IV Members should be executive and non-executive directors with a majority being non-executive directors.

The CEO should not be a member, but should attend by invitation, if necessary.

Minimum of three members.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Risk committee Chairman of the risk committee

The Companies Act Not applicable.

King IV Independent, non-executive director.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

PSG CAPITAL DIRECTOR’S GUIDE 35

Risk committee Function

The Companies Act Not applicable.

King IV Consider the risk management policy and plan and monitor the risk management process.

The risk committee should ensure that IT risks are adequately addressed.

The risk committee should obtain appropriate assurance that controls are in place and effective in addressing IT risks.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

Social and ethics committee Who is required to have a social and ethics committee?

The Companies Act Every listed company.

Every state-owned company.

Any other company that has in any two of the previous five years scored above 500 points on its “public interest score” in terms of the regulations. These would typically be large private and unlisted public companies.

A company must calculate its public interest score as the sum of the following:

– a number of points equal to the average number of employees of the company during the financial year;

– one point for every R1 million (or portion thereof) in outstanding unsecured debt of the company held by creditors at the financial year-end;

– one point for every R1 million (or portion thereof) in turnover during the financial year; and

– one point for every individual who, at the end of the financial year, is known by the company (i) in the case of a profit company, to directly or indirectly have a beneficial interest in any of the company’s issued securities or (ii) in the case of a non-profit company, to be a member of the company, or a member of an association that is a member of the company.

A company is not required to have a social and ethics committee if it is a subsidiary of another company that has such a committee which fulfils the functions for the subsidiary company.

King IV King IV encourages companies not legally required to establish a social and ethics committee, to nevertheless consider creating a structure that would achieve similar aims.

JSE Listings Requirements for main board listed companies

All main board companies must, in accordance with King IV and the Companies Act, appoint a social and ethics committee.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply the Companies Act and King IV.

36 PSG CAPITAL DIRECTOR’S GUIDE

Social and ethics committee Composition

The Companies Act Must compromise a minimum of three directors or prescribed officers of the company, at least one of whom must be a non-executive director and must have been non-executive in the previous three financial years.

The members are appointed by the board.

King IV The social and ethics committee should have executive and non-executive directors as members.King IV recommends a higher standard for composition than the Companies Act. Recommended practice would be to have a majority of non-executive directors.

JSE Listings Requirements for main board listed companies

The composition of the social and ethics committee must comply with the requirements of the Companies Act and should be considered in accordance with King IV on an “apply and explain” basis, provided that the social and ethics committee must comprise at least three members.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply the Companies Act and King IV.

Social and ethics committee Chairman of the social and ethics committee

The Companies Act No specific requirements.

King IV The chairman of the board may be a member of the committee, but should not be its chair.

JSE Listings Requirements for main board listed companies

Apply King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply King IV.

PSG CAPITAL DIRECTOR’S GUIDE 37

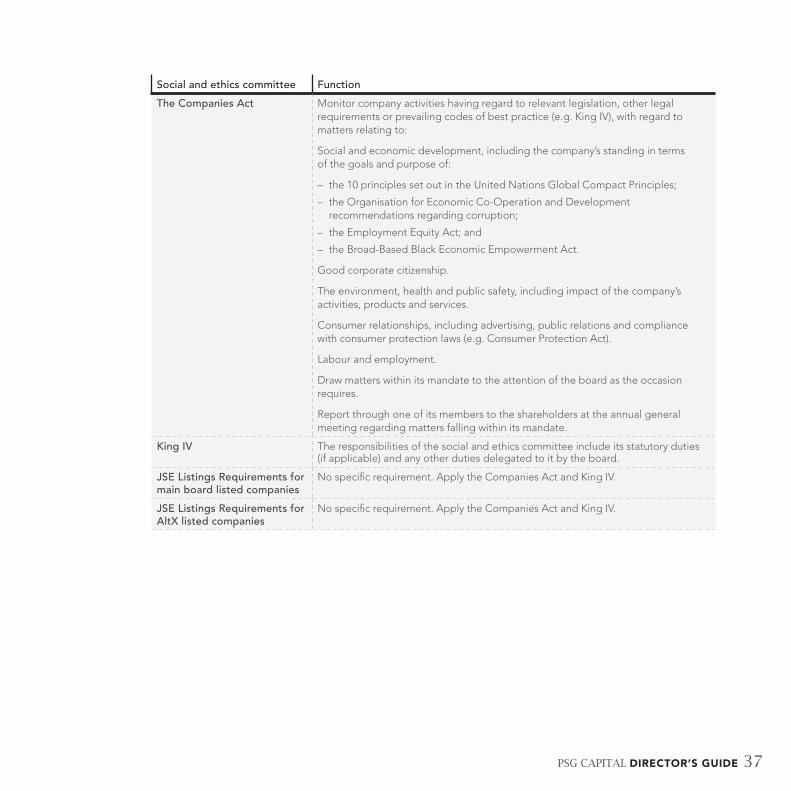

Social and ethics committee Function

The Companies Act Monitor company activities having regard to relevant legislation, other legal requirements or prevailing codes of best practice (e.g. King IV), with regard to matters relating to:

Social and economic development, including the company’s standing in terms of the goals and purpose of:

– the 10 principles set out in the United Nations Global Compact Principles;– the Organisation for Economic Co-Operation and Development

recommendations regarding corruption;– the Employment Equity Act; and– the Broad-Based Black Economic Empowerment Act.

Good corporate citizenship.

The environment, health and public safety, including impact of the company’s activities, products and services.

Consumer relationships, including advertising, public relations and compliance with consumer protection laws (e.g. Consumer Protection Act).

Labour and employment.

Draw matters within its mandate to the attention of the board as the occasion requires.

Report through one of its members to the shareholders at the annual general meeting regarding matters falling within its mandate.

King IV The responsibilities of the social and ethics committee include its statutory duties (if applicable) and any other duties delegated to it by the board.

JSE Listings Requirements for main board listed companies

No specific requirement. Apply the Companies Act and King IV.

JSE Listings Requirements for AltX listed companies

No specific requirement. Apply the Companies Act and King IV.

38 PSG CAPITAL DIRECTOR’S GUIDE

DEFINITION FOR NON-EXECUTIVE AND INDEPENDENT DIRECTORS ACROSS THE REGULATORY FRAMEWORK

6chapter

PSG CAPITAL DIRECTOR’S GUIDE 39

DEFINITION FOR NON-EXECUTIVE AND INDEPENDENT DIRECTORS ACROSS THE REGULATORY FRAMEWORK

At the outset it is important to note that the Companies Act does not per se provide a definition for non-executive or independence in relation to directors. Instead, it simply lays down criteria that must be met for directors to be eligible as members of the audit committee.

The Companies Act Regulated by section 94(4)

NB: Does not define non-executive or independent per se but rather sets the criteria that a member of the audit committee must satisfy, as set out below:

i. Not involved in the day-to-day management of the company’s business or has not been so involved at any time during the previous financial year;

ii. Not a prescribed officer or full-time employee of the company or of another related/inter-related company or has not been such officer/employee at any time during the previous three financial years (for the definition of related and inter-related companies, see section 2(1)(c) – essentially, it includes subsidiary companies, holding companies and companies controlled by the same party);

iii. Is not a material supplier or customer of the company, such that a reasonable and informed third party would conclude in the circumstances that the integrity, impartiality or objectivity of that director is comprised by that relationship;

iv. Not related to any person referred to in (i) to (iii) above.

40 PSG CAPITAL DIRECTOR’S GUIDE

King IV “Independence” means the exercise of objective, unfettered judgement. When used as a measure by which to judge the appearance of independence, or to categorise a non-executive member of the board or its committees as independent, it means the absence of an interest, position, association or relationship which, when judged from the perspective of a reasonable and informed third party, is likely to influence unduly or cause bias in decision-making.

Non-executive directors may be categorised by the board as independent if the board concludes that the relevant director satisfies the definition provided above.

The board should consider the following factors holistically on a substance over form basis, in assessing independence of non-executive directors.The director – is a significant provider of financial capital or is an officer/employee/