Think FundsIndia September 2015 - Fundsindia.com

8

www.fundsindia.com Do you really lose a lot in a market fall? There was a close to 6 per cent decline in a single day in the BSE Sensex on August 24. Many retail investors were spooked, as they were worried about the enormous impact on their wealth. Yes, the decline is steep and concerns over it are not invalid. But why is it that retail investors talk of losing their entire money in stock markets, when the average Indian household’s exposure to equities is quite low? Let me put this in perspective: the Reserve Bank of India's (RBI) data on household savings, if any indication, suggests that 65-70 per cent of an investor’s savings are in physical assets - that is, real estate and gold. According to the same RBI data, in recent years, savings in physical assets was twice that of financial assets such as deposits, small savings schemes, equities, and bonds. We do know that a majority of Indians have a high holding in real estate, given that it requires huge investments (or borrowing). A 10-15 per cent exposure also goes into gold. Of the financial assets, 50-60 per cent is in deposits, and a decent amount in provident funds and insurance funds, and the rest in small savings. Not much is left for equities. Indian investors are often under the delusion that their other asset classes are seemingly safe. Why? It’s merely because they do not have sufficient information on them. How many know that real estate prices have corrected 15-30 per cent in many pockets in the past 18 months, or that their every Rs. 100 worth of gold three years ago is down to Rs. 80 today?. Worse still, how many know that their deposits, until last year, were earning them a negative real return for at least 5 years, net of inflation? Even assuming you hold a good 20 per cent of your overall assets in equities, a 6 per cent fall will dent your overall wealth by 1.2 per cent. Not something to be scared of or to pull the panic button! The overload of information on equity – whether stocks, or mutual funds, forces you to believe that your wealth is completely eroded, when the impact really isn’t that big when you view it in totality. The primary point I am trying to make here is that when you are so inadequately exposed to equity, a decline does not hurt your overall savings that hard. The reverse holds good too. Vidya Bala Head – Mutual Fund Research FundsIndia.com September 2015 ■ Volume 05 ■ 09 We now have a New Address in Chennai Wealth India Financial Services Third Floor, Uttam Building 38 & 39, Whites Road Royapettah, Chennai 600014 A fresh look Greetings from FundsIndia! FundsIndia.com is sporting a new look on its website. Our home page has been refreshed, the dashboard is new, and the interfaces for transactions have been changed. Our objectives for these changes are these: 1. Home page – We wanted to update it to be modern, in keeping with international standards, more interactive for a fresh visitor to FundsIndia and have a strong focus on our core offerings. 2. Dashboard – Here, we wanted to provide a snapshot of an investor’s holdings in an interactively pictorial way. In one glance, we wanted the investor to know where he stands, and what action items he needs to take right away. 3. Transaction flows – Simplicity! We wanted to have a simple flow and reduce clutter in terms of the options and pathways for our investors. Do you like our new look? Please write to [email protected] and let us know! Happy investing! Srikanth Meenakshi Co-Founder & COO FundsIndia.com

-

Upload

fundsindiacom -

Category

Business

-

view

180 -

download

0

Transcript of Think FundsIndia September 2015 - Fundsindia.com

www.fundsindia.com

Do you really lose a lot in a market fall?There was a close to 6 per cent decline in a single day in the BSE Sensex onAugust 24. Many retail investors were spooked, as they were worried aboutthe enormous impact on their wealth. Yes, the decline is steep and concernsover it are not invalid. But why is it that retail investors talk of losing theirentire money in stock markets, when the average Indian household’sexposure to equities is quite low?

Let me put this in perspective: the Reserve Bank of India's (RBI) data onhousehold savings, if any indication, suggests that 65-70 per cent of aninvestor’s savings are in physical assets - that is, real estate and gold.According to the same RBI data, in recent years, savings in physical assets wastwice that of financial assets such as deposits, small savings schemes, equities,and bonds.

We do know that a majority of Indians have a high holding in real estate,given that it requires huge investments (or borrowing). A 10-15 per centexposure also goes into gold. Of the financial assets, 50-60 per cent is indeposits, and a decent amount in provident funds and insurance funds, andthe rest in small savings. Not much is left for equities.

Indian investors are often under the delusion that their other asset classes areseemingly safe. Why? It’s merely because they do not have sufficientinformation on them. How many know that real estate prices have corrected15-30 per cent in many pockets in the past 18 months, or that their every Rs.100 worth of gold three years ago is down to Rs. 80 today?.

Worse still, how many know that their deposits, until last year, were earningthem a negative real return for at least 5 years, net of inflation? Evenassuming you hold a good 20 per cent of your overall assets in equities, a 6per cent fall will dent your overall wealth by 1.2 per cent. Not something tobe scared of or to pull the panic button!

The overload of information on equity – whether stocks, or mutual funds,forces you to believe that your wealth is completely eroded, when the impactreally isn’t that big when you view it in totality.

The primary point I am trying to make here is that when you are soinadequately exposed to equity, a decline does not hurt your overall savingsthat hard. The reverse holds good too.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

September 2015 � Volume 05 � 09

We now have aNew Addressin Chennai

Wealth India Financial ServicesThird Floor, Uttam Building

38 & 39, Whites RoadRoyapettah, Chennai 600014

A fresh lookGreetings fromFundsIndia!

FundsIndia.com issporting a new look

on its website.

Our home page has beenrefreshed, the dashboard is new,and the interfaces for transactionshave been changed.

Our objectives for these changesare these:

1. Home page – We wanted toupdate it to be modern, inkeeping with internationalstandards, more interactive fora fresh visitor to FundsIndiaand have a strong focus on ourcore offerings.

2. Dashboard – Here, we wantedto provide a snapshot of aninvestor’s holdings in aninteractively pictorial way. Inone glance, we wanted theinvestor to know where hestands, and what action items heneeds to take right away.

3. Transaction flows – Simplicity!We wanted to have a simpleflow and reduce clutter in termsof the options and pathways forour investors.

Do you like our new look? Pleasewrite to [email protected] let us know!

Happy investing!

Srikanth MeenakshiCo-Founder & COOFundsIndia.com

FundsIndia Strategy: Past returns and how much to rely on it

How most investors view past returns

Here’s how past returns are typically used to choose afund:

- To pick a fund that has given high returns amongpeers, typically in the recent past, say the past oneyear

- To hope that the fund will continue to deliversimilar returns in the future as well

If the above did indeed play out, and your call works, thenthere would be no need to review a fund. You could picka fund sorting it as ‘largest to smallest in returns’ in yourExcel sheet and hold it forever!

We wish choosing a fund was that easy!

A fund’s past returns could be based on:

- market conditions

- its portfolio of stocks

- the strategy adopted by the fund

- the skill sets of the fund manager, and

- the fund house

It is an amalgam of a number of macro and microparameters playing out.

A fund that delivered superlative returns in a rising marketmay not be well placed to contain declines in a downmarket. A fund that went overweight on a sector and didnot cut exposure on time may suffer when that sector goesout of favour.

Hence, to go on the basis of past returns to set yourreturn expectations would not be the most prudent thing

to do.

But then, some of you ask us – “If stock price forecastscan be made, why not forecast fund returns?” Well, theanswer is simple:

- One, a stock has an underlying fundamental and it isnot too tough to gauge its performance (other externalfactors remaining the same). For example, if acompany increased its production from say 10,000units to 20,000 units, you know the impact on itsrevenue and earnings.

If a company increases or reduces its debt, you knowthe impact on its net profit. The underlyingfundamental can be measured, or reasonablyforecasted. An equity mutual fund is, however, a basketof stocks. Yes, the basket’s fundamentals can be gauged(as in an ‘index’ – which is a basket of stocks).

But how does one know what stocks continue toremain in the portfolio, what is removed, and what isadded? As analysts and as investors, we all have accessto a fund’s portfolio at the end of the month.

There could be many changes in between, and therecould be changes post when we see. To this extent, thedynamic nature of a fund’s portfolio makes it toughfor anybody to forecast future returns.

- Two, and more importantly, the regulator does notpermit any such forecasts. The case rests here.

How you need to view past returns

But yes, at research, we most certainly use past returns toassess the quality of a fund. Yes, to assess a fund’s quality,and not to forecast a fund’s future performance.

www.fundsindia.com

Vidya Bala

‘Past returns are not indicative of future performance’ goes the disclaimer. So, why do we relyon past performance? For most of you, past returns psychologically influence your returnexpectations for the future. And when that does not happen, there is disappointment thatsometimes leads to the dumping of an asset class such as equity funds.

We live in an increasingly uncertain world. Seven years after the financial crisis, advanced economiesare still growing slowly, while a number of emerging economies are experiencing difficulty as theold export-led growth model flounders.Dr Raghuram Rajan, Governor, Reserve Bank of India

Take a sports person – a tennis player, for instance. Aperson may have a record of matches won and lost, andmay be top seeded or top ranked. But that is not all.

Dig into numbers and you will see that their winningstreak (or losing streak) has a story to tell: whether theirstrengths lie in clay, grass or synthetic courts; how manysets they’ve won; in how many sets were they broken; howmany first serves they got right; how many aces they haveto their credit; how many games did they lose; are theyserve and volley players; and, what was their success withthat style, and so on. The data can be endless.

This is exactly the kind of data and analysis we like to digup from a fund’s past performance. We try andunderstand its style, its strategy, its strengths andweaknesses across market phases, its consistency, itsvolatility, and of course, how all of these finally helpedthe fund deliver returns superior to the market.

We see this in relation to the market, and in relation topeers. The returns that the fund generated could havebeen double digits in a good market, and even negative ina down market.

That is a fall out of the market’s broad performance. Howthe fund did in favourable and adverse conditions inrelation to its universe is what past data helps us gauge.

From there on, we try to understand where and how thesefunds fit in. A few funds are good for down market, a fewdo well in rallies but take a beating in falls, and then thereare a few others that remain all-weather friendly.

Once we understand this, we try to provide you with asuitable combination of funds that will fit yourrequirement based on the fund’s performance in variousparameters.

Hence, we derive the ‘quantitative metrics’ that help assessa fund’s performance using past data.

So, how do we know the future potential of the fund?This is where ‘qualitative factors’, i.e., the quality of theportfolio comes into the picture.

Given a set of market conditions (bull market, bearmarket, volatile market, a growth focused market, adefensive market, and so on), we look at how well a

portfolio is placed to generate returns.

Not only that, we also look at how well a fund is able totake advantage of macro events to position its portfolio.

For instance, what sort of sectors or stocks could benefitif the Iran nuclear deal goes through? It could be thosethat use crude directly as an input (oil marketingcompanies), or those that use crude as a raw material.

Let’s take another example. It is now clear that the ruralconsumption story has slowed.

So does that mean a fund with high weight to consumergoods is wrong, or is it doing something contrarian? Whatif the urban consumption story receives a boost from the7th Pay Commission hikes to be announced in early 2016?

What sort of a consumption revival can it cause, andwhich segments of consumption are best placed tobenefit from it? Is a fund able to see the early beneficiariesand take positions early on? Yes, this information needsplenty of reading and research, and also discussions withfund managers on their calls.

These help us understand the potential a portfolio holds.The market returns forecast by analysts based on marketvaluations, together with the kind of alpha generation thata good portfolio can deliver, is what finally determines afund’s returns. There is no one-shot formula for this, andit is best to not over-predict or forecast.

As an investor, it would suffice for you to know thelong-term returns that equity, as an asset class, hasdelivered in the near past (5-10 years).

It is fair to expect a fund to generate returns within 3-5percentage points of this. Anything more, certainlyreflects superior fund management, and of course, yourown fund choice.

Bottom line? Don’t ride on past returns. Ride on‘performance’. Performance speaks when it builds yourwealth; not when it breaks the charts in a single year.

Rest assured, we try our best to go with this philosophy.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

www.fundsindia.com

Recovery could be more gradual than expectations says Anoop Bhaskar, CIO, UTI Mutual Fund

Read this article, and much more at Marketplace – the official blog of FundsIndia.com

www.fundsindia.com

FundsIndia Features: The Instant Wealth Designer

• A lot of time is required – There are hundreds ofschemes in the mutual fund universe, and each oneclaims to be the best. That makes it difficult to shortlistthe best fund that will work for you.

• What is best for you? – That’s the million dollarquestion. The answer lies in understanding what yourequire (your goal, investment time frame, monthlyinvestment amount, and of course, your risk profile),and then picking the best funds that can help you meetyour requirement in time.

These nitty-gritties lie at the heart of successful investing.Get them right, and your investment journey will be asmooth ride; get them wrong, and you may either makethe wrong investments, or even worse, put off investing inmutual funds altogether.

The solution

Presenting FundsIndia’s ‘SIP Designer’ – a powerful toolthat will instantly design a portfolio of India’s best mutualfunds according to your requirements. Here’s how itworks:

1. It’s all about you – The SIP Designer needs to knowyour age, investment time frame, and monthlyinstalment amount. Your risk profile is also animportant determinant in designing your portfolio. Ifyou’re not too sure about your risk profile, then youcan take a quick and simple risk test by clicking on‘Check your risk’.

2. Get a customised portfolio instantly – That’s it! OurSIP Designer will instantly design a powerful mutualfund portfolio for systematic investing based on yourinputs. You can look at the funds shortlisted for youunder different categories, and get going with your

investment journey by clicking the ‘Create SIP’ buttonat the end of the page.

The instant wealth designer

Here’s why the SIP Designer will work for you:

• It’s consistent – The SIP Designer runs on a robustalgorithm. Based on your inputs, the system assigns arisk score to your portfolio and creates an assetallocation pattern. Depending on the categories offunds in the asset allocation pattern, the top schemesunder that category are used to build the portfolio. Youalso enjoy flexibility because if you do not want aparticular scheme that has been suggested to you inyour portfolio, then you have the freedom to change itwith an equivalent scheme.

• It gives you the best of both worlds – It is built withpowerful technological tools, along with the expertiseof FundsIndia’s Mutual Fund Research Desk. You canbe confident that the portfolio designed for you willonly pick the best funds for you in an unbiased manner,and in accordance with your needs.

• It is instant – That’s the best part! It will take you lessthan five minutes to kick-start your journey to wealthwith the SIP Designer. Moreover, you can get yourportfolio designed anytime and anywhere, without anytime or geographical restrictions.

Investing is truly easy when you invest with the best, isn’tit?

Noorain MohammedCorporate Communications

FundsIndia.com

Investing regularly helps builds wealth. You may have heard this axiom several times, and youmight even agree to it. The world’s most successful investors swear by it. But there’s still somedifficulty in getting started, isn’t it?

You may put off investing, and thereby put off building wealth, due to one or more of thefollowing reasons:

Noorain Mohammed

www.fundsindia.com

Leverage is a dangerous beast. It can’t ever turn a bad investment good, but can turn a goodinvestment bad.James Montier, GMO

How much you save matters

Reach your goals

But did you ever think about what are you going to dowith this amount? Meet the down payment for a homeloan? Go on a holiday abroad? The truth is, investing Rs.3,000 or even Rs. 5,000 a month may appear a reasonablesum to you, but is unlikely to get you to your goals.

The toll inflation takes in the long term may have escapedyour calculation. For example, a management degree thesedays costs around Rs. 6,00,000 at good schools. Ten yearsfrom now, this nearly doubles to Rs. 11.8 lakh, assuming arelatively modest 7 per cent cost inflation.

The monthly saving required is Rs. 5,131 (assuming areasonable 12 per cent annual return). And remember,education is just one goal. If you have more than onechild, it will be still higher.

Add to that others such as meeting the down payment fora home loan, your children’s weddings, or your retirement.Consider retirement, for which you need to build wealth.

A monthly expense of Rs. 20,000 today (and this is aconservative number for most families) will be Rs. 64,143twenty years from now at an inflation rate of 6 per cent.The corpus you need to build to last you for the 25 yearsor so after you retire amounts to a whopping Rs. 1.5 crorerequiring a saving of Rs. 15,157 a month for the nexttwenty years.

Build your wealth

The wealth you build is thus directly a function of thequantum you save. And in order to accumulate this kindof wealth over the very long term, the best tool is equities.

So if you are saving 15-20 per cent of your incometowards long-term goals, but are investing only 5 per cent

in equities and the remaining in debt, you will becompromising your wealth accumulation.

But here again, how much you save matters, even if yourightly choose to invest in a smart asset class such asequity. It could also be that you began saving at Rs. 2,000or so years ago but neglected to step it up as your incomegrew. Or you are putting in a good Rs. 20,000 each timeyou invest, but you do so on and off whenever the moodtakes you. Neither of these is advisable.

Bring focus into your saving by deciding how much youneed, over how many years and for what purpose. Youmay not have specific life goals such as children’seducation or retirement.

But nothing prevents you from setting goals for yourportfolio in terms of the wealth you would like to generatefrom that. That provides a direction to your savings andensures you are not grossly inadequate in what you save.

Averaging and compounding effect

Finally, meaningful averaging and compounding if you aredoing SIPs, or significant compounding for lump suminvestment is possible only when the amount invested isalso meaningful.

Imagine how much more powerful the averaging andsubsequent compounding would be if the amount hadbeen Rs. 10,000. When your SIP buys on dips, youaccumulate a far higher number of units with Rs. 10,000than you would with Rs. 1,000. The same applies to yourSIP investments too! So think about it.

Bhavana AcharyaAnalyst, Mutual Fund Research

FundsIndia.com

Bhavana Acharya

You know that for the long term, equity investments are the way to go. Knowing also the benefitsof disciplined monthly investments through the systematic investment plan route, you beganinvesting Rs. 3,000 each month five years ago. So let’s say this: Rs. 3,000 was invested in a large-capfund. At the end of five years, you will be sitting on Rs. 2,91,560, having saved Rs. 1,80,000translating into a yield of 20 per cent. All good.

www.fundsindia.comwww.fundsindia.com

Q: I hear that one should not invest lump sum when theSensex Price-Earnings (PE) ratio is above 21 times.

But the PE ratio of a few funds I have seen are at presentat 18, or are less than 18.

On the other hand, I look at the PE of somewell-performing mutual funds, and it is about 26 times.

In the present market situation, is it better to invest lumpsum in the low PE funds I had mentioned, and invest inthe other funds when their PEs come down? I am lookingat making lump sum investments.

A: There is no sanctity behind the cut-off PE of 21 times.Valuations are based on what the market expects theearnings of the basket of index stocks to be.

If improved earnings growth is expected, the premiumgiven now would be in anticipation of such delivery, andvice versa.

Also, different sectors have different valuation metrics.For a growing company/sector, a PE of 21 may benormal, while it may be very high for a companystruggling to get double-digit growth.

Hence, while seeing the index versus the fund’s PE, it isimportant to bear in mind the differences in theirexposure, as Indian mutual funds invest quite a bit outsideof indices.

Besides, a fund with a value focus will always sport arelatively low PE, when compared to a fund with a growthfocus. The funds you mentioned are value conscious andinvest based on valuations.

They would rather hold cash than invest in equity whenvaluations seem high based on their strategy. If you arekeen on such style of investing, you may go with suchfunds.

That does not, however, mean growth-focused fundscannot deliver. They hold stocks that are trading at highervaluation because their earnings growth is likely higher,or expected to be high.

They pay a price of quality and visibility of earnings.

Q & A

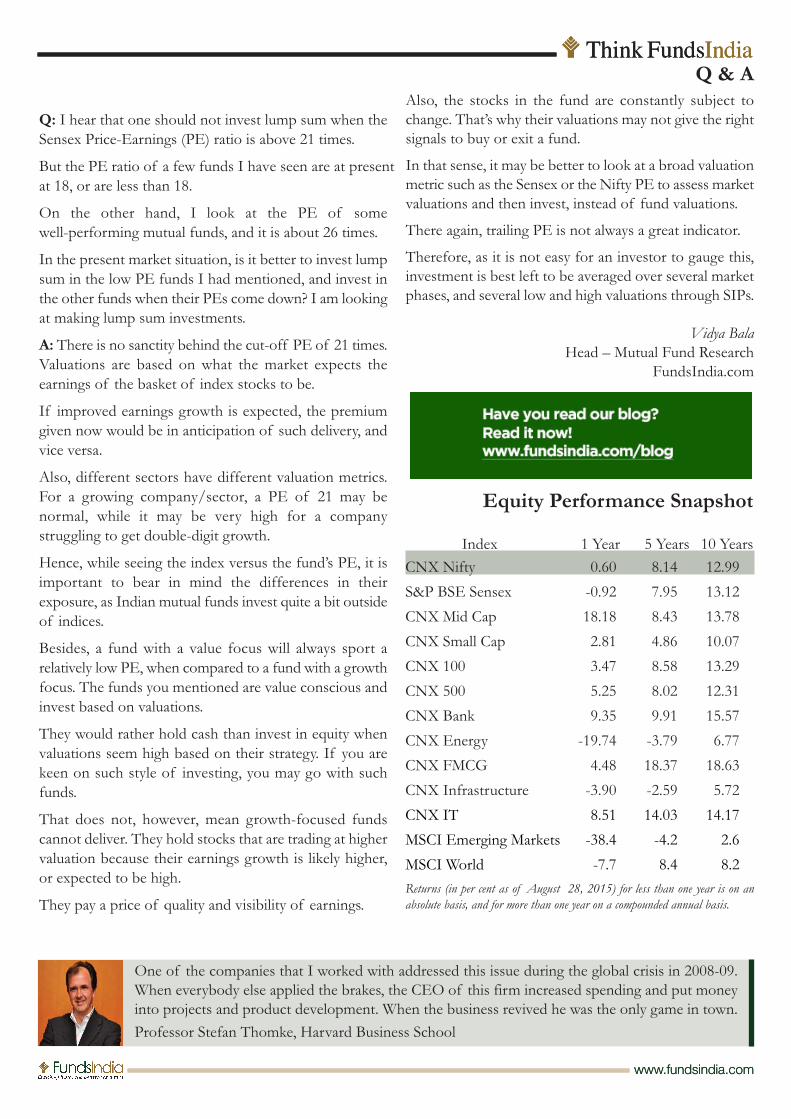

Equity Performance Snapshot

Index 1 Year 5 Years 10 YearsCNX Nifty 0.60 8.14 12.99

S&P BSE Sensex -0.92 7.95 13.12

CNX Mid Cap 18.18 8.43 13.78

CNX Small Cap 2.81 4.86 10.07

CNX 100 3.47 8.58 13.29

CNX 500 5.25 8.02 12.31

CNX Bank 9.35 9.91 15.57

CNX Energy -19.74 -3.79 6.77

CNX FMCG 4.48 18.37 18.63

CNX Infrastructure -3.90 -2.59 5.72

CNX IT 8.51 14.03 14.17

MSCI Emerging Markets -38.4 -4.2 2.6

MSCI World -7.7 8.4 8.2Returns (in per cent as of August 28, 2015) for less than one year is on anabsolute basis, and for more than one year on a compounded annual basis.

Also, the stocks in the fund are constantly subject tochange. That’s why their valuations may not give the rightsignals to buy or exit a fund.

In that sense, it may be better to look at a broad valuationmetric such as the Sensex or the Nifty PE to assess marketvaluations and then invest, instead of fund valuations.

There again, trailing PE is not always a great indicator.

Therefore, as it is not easy for an investor to gauge this,investment is best left to be averaged over several marketphases, and several low and high valuations through SIPs.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

One of the companies that I worked with addressed this issue during the global crisis in 2008-09.When everybody else applied the brakes, the CEO of this firm increased spending and put moneyinto projects and product development. When the business revived he was the only game in town.Professor Stefan Thomke, Harvard Business School

www.fundsindia.com

Bajaj AutoThe medium-term trend for Bajaj Auto has been in arange of Rs. 2,140 and Rs. 2,600. At present, thecorrection appears to have taken support at Rs. 2,140.There is a strong possibility of Bajaj Auto resuming itsupward rally from the present price. We recommend a buyat the current price for a target of Rs. 2,600. The stockcan be accumulated on declines. The latest 200-day simplemoving average is placed at Rs. 2,340. Its stop loss isplaced at Rs. 1,980.

This column is targeted at investors who are registered customers ofFundsIndia for trading and investing in equity as well as prospectiveinvestors who wish to open an equity account with FundsIndia.

The resistance that Nifty faced at 8,600 levels resulted inthe index forming a minor congestion band between8,300 and 8,600. The corrective phase was confirmedonce it slipped below 8,300. At current levels, the Niftyfaces support at 7,670 levels. A pullback rally is expectedin the short term. The latest 200-day Simple MovingAverage is at 8,453.5. The index can turn positive above8,000. A close below 7,650 will lead to further weaknessto test at 7,500 levels.

Perumal RajaTechnical Analyst (Equity Research Desk)

FundsIndia.com

Cummins IndiaCummins India has been in a consolidation band for overa year at Rs. 840 to Rs. 960. The breakout triggered anupward trend with resistance at Rs. 1,240. The presentcorrection is an opportunity to accumulate the stock fora target of Rs. 1,300. Its resistance is at Rs. 1,180. Supportis at Rs. 1,000. Its upward trend will continue as long asthe stock trades above Rs. 940. The stock’s latest 200-daysimple moving average is Rs. 912.6. Stop loss is Rs. 940.

Technical View Nifty

Disclaimer: Mutual fund investments are subject to market risks. Please read the scheme information and other related documents beforeinvesting. Past performance is not indicative of future returns. Please consider your specific investment requirements before choosing a fund,or designing a portfolio that suits your needs. Wealth India Financial Services Pvt. Ltd. (ARN code 69583) makes no warranties orrepresentations, express or implied, on products offered through the platform. It accepts no liability for any damages or losses, howevercaused, in connection with the use of, or reliance on its products or related services. The terms and conditions of the website are applicable.Think FundsIndia, a monthly publication of Wealth India Financial Services Pvt. Ltd., is for information purposes only. Think FundsIndiais not, and should not, be construed as a prospectus, scheme information document, offer document or recommendation. Information inthis document has been obtained from sources that are credible and reliable in the opinion of the Editor.Publisher:Wealth India Financial Services Pvt Ltd. Editor: Srikanth Meenakshi

To stay relevant now, there is a need to have an integrated approach. The business environmenthas changed and deals are increasingly won on what value an outsourcing provider can bring to thetable. This is true of not only Wipro but of the Indian outsourcing industry as well.Abid Ali Neemuchwala, Chief Operating Officer, Wipro

1 What is a liquid fund?

2 Which was the first bank in India to get into thebusiness of mutual funds?

3 What is the maximum limit for investing in the equityof a company in a diversified equity fund?

4 Who is the author of 'China Shakes The World'?

5 Name the person in the image. Heis the CEO of one of the leadingtechnology companies in the World.

Answers may be sent to [email protected].

Answers for August 2015 Investment Quiz:

1 Saudia Arabia 2 Peter Lynch 3 Quantum AssetManagement 4 65% 5 Vishwanath Pratap Singh, morepopularly known as V P Singh

There are no winners for August’s ‘Think FundsIndia’quiz.

www.fundsindia.com

FundsIndia Select Funds Investment QuizEquity (Moderate risk)

There are funds that will seek to generate inflation - beatingreturns and limit downside risks.

Axis Equity Birla SunLife Top 100

BNP Paribas Equity Franklin Bluechip

HDFC Top 200 ICICI Pru Dynamic

ICICI Pru Top 100 Kotak Select Focus

Mirae Opportunities SBI Bluechip

UTI Equity UTI Opportunities

Please click here for a complete listing of our preferredfunds.

@fundsindia.com:We have released a revamped equity section to provideimproved user experience to our stock trading customers.We have and improved our transaction pages. You canshare your feedback by writing to us [email protected].