Think FundsIndia - July 2014

10

www.fundsindia.com Renewed interest There is no better time to start investing in equity than right now - this is the conclusion that many FundsIndia investors are coming to, as we have seen a level of fresh activity, hitherto unmatched, in our system over the past six weeks. Investors with accounts that have been dormant for years are starting to invest now. Stopped SIPs are being restarted. We are registering a sizeable number of bank mandates to enable people to setup their SIPs. Perennial debt and liquid fund investors are setting up systematic transfer plans to equity funds. We agree, for once, with the broader sentiment that is guiding this activity. And we don’t want any FundsIndia investor to be left behind in this ride. As of now, about a third of FundsIndia account holders still do not have an active SIP. Over the course of this month, we are going to make an all-out effort to reach out to these folks and persuade them to join this pursuit of prosperity. Happy SIP investing! Srikanth Meenakshi Spacing out entry in risky assets If you go through a phase in one asset class where prices have risen steadily, as has been the case with Indian equities since mid 2013, there can be the urge to get tempted and throw out the plan and prudence books. This is what has to be avoided at all cost. For those who have abundant surplus funds and can afford to take risks, lump- sum investment may pay off. For it to do so though, either the investor and / or his advisor must be top notch in the ability to time the entry and exit so as make good money and do this several times over the years. This is also not the way for those starting off on savings and investment as a lifetime goal. The last thing you can afford at this stage is to lose sizeable sums at one go. When it comes to deploying short-term surplus or funds that are allocated to asset class such as deposits and bonds, you could go ahead with investing lump sums in fixed deposits and short-term bond funds. This would have to change when it comes deploying funds in riskier asset classes such as long-term bonds, equities, gold and commodities, to name a few. Investing in phased manner would help most of the time, as you are entering an asset class at multiple price points. You are avoiding getting locked in at one price point, which can hurt you badly, especially if it was after a sizeable rally in prices. If you are investing with long-term goals in mind and can be disciplined about, phased investing usually works well. Such investing, especially in difficult phases for the economy and market, tends to pay rich dividend, as your average entry points would be lower. A good example will be the 1998-mid 2003 when investors could persisted with investing in equity through Systematic Investment Plans benefited immensely with the rally post mid-2003. Even if you go through such phased investing methods, you cannot and must not assume that this should be invest, sit back and relax forever approach. You must track your investments and market trends. If there is a protracted bullish phase as between 2003-2007 in equities, you must be willing to take funds off the table. Similarly, if you get a 30%-50% cut in prices, that would usually be a good time to get back in. Even if you invest in a phased manner, make sure at least about 70% of your equity investments track the large-cap space. The rest can be spread across the rest of the cap curve and a few themes such as consumer goods and healthcare that could stabilise the riskier parts of your portfolio. S Vaidya Nathan July 2014 ■ Volume 07 ■ 07 FundsIndia Winner CNBC TV18 UTI Award 2013-14 National Online Advisory Services

-

Upload

fundsindia -

Category

Documents

-

view

214 -

download

1

description

Â

Transcript of Think FundsIndia - July 2014

www.fundsindia.com

Renewed interest

There is no bettertime to startinvesting in equitythan right now -

this is the conclusion that manyFundsIndia investors are comingto, as we have seen a level offresh activity, hithertounmatched, in our system overthe past six weeks.

Investors with accounts thathave been dormant for years arestarting to invest now. StoppedSIPs are being restarted.

We are registering a sizeablenumber of bank mandates toenable people to setup their SIPs.Perennial debt and liquid fundinvestors are setting upsystematic transfer plans toequity funds.

We agree, for once, with thebroader sentiment that is guidingthis activity. And we don’t wantany FundsIndia investor to beleft behind in this ride. As ofnow, about a third of FundsIndiaaccount holders still do not havean active SIP.

Over the course of this month,we are going to make an all-outeffort to reach out to these folksand persuade them to join thispursuit of prosperity.

Happy SIP investing!

Srikanth Meenakshi

Spacing out entry in risky assets

If you go through a phase in one asset class where prices have risen steadily,as has been the case with Indian equities since mid 2013, there can be the urgeto get tempted and throw out the plan and prudence books. This is what hasto be avoided at all cost.

For those who have abundant surplus funds and can afford to take risks, lump-sum investment may pay off. For it to do so though, either the investor and /or his advisor must be top notch in the ability to time the entry and exit so asmake good money and do this several times over the years. This is also not theway for those starting off on savings and investment as a lifetime goal. Thelast thing you can afford at this stage is to lose sizeable sums at one go.

When it comes to deploying short-term surplus or funds that are allocated toasset class such as deposits and bonds, you could go ahead with investing lumpsums in fixed deposits and short-term bond funds. This would have to changewhen it comes deploying funds in riskier asset classes such as long-term bonds,equities, gold and commodities, to name a few.

Investing in phased manner would help most of the time, as you are enteringan asset class at multiple price points. You are avoiding getting locked in at oneprice point, which can hurt you badly, especially if it was after a sizeable rallyin prices. If you are investing with long-term goals in mind and can bedisciplined about, phased investing usually works well.

Such investing, especially in difficult phases for the economy and market, tendsto pay rich dividend, as your average entry points would be lower. A goodexample will be the 1998-mid 2003 when investors could persisted withinvesting in equity through Systematic Investment Plans benefited immenselywith the rally post mid-2003.

Even if you go through such phased investing methods, you cannot and mustnot assume that this should be invest, sit back and relax forever approach.You must track your investments and market trends. If there is a protractedbullish phase as between 2003-2007 in equities, you must be willing to takefunds off the table. Similarly, if you get a 30%-50% cut in prices, that wouldusually be a good time to get back in. Even if you invest in a phased manner,make sure at least about 70% of your equity investments track the large-capspace. The rest can be spread across the rest of the cap curve and a few themessuch as consumer goods and healthcare that could stabilise the riskier parts ofyour portfolio.

S Vaidya Nathan

July 2014 � Volume 07 � 07

FundsIndiaWinner CNBC TV18 UTI Award 2013-14National Online Advisory Services

SIPs make anytime a good time to invest

SIPS build wealth by shielding your portfolio frommarketextremes. SIPs offer the best downside protection bysimply averaging at lower costs and lowering your overallinvestment cost. That said, many of you may have hadvery forgettable experience with equity funds, andtherefore shut the door to this clear wealth buildingoption. Knowing when you can get hurt will help you doaway with this fear.

When you can get hurt

A few reasons why you may have burnt your fingers inthe equity mutual fund market are:

• Very poor choice of funds (when I say very poor Imean those at the bottom quartile of performance;even the middle-rung ones would have fetched youdecent returns)

• Investing lump sum or through SIP for very shortperiods of say 1-2 years

• Investing lump sum and such an investment wasunfortunately made in the market peak

• Stopping SIPs way ahead of the stated goal

Points one and two are not difficult to tackle. On pointone, if your fund has been underperforming itsbenchmark for over four quarters, then you should nothave stuck to it. Else, the best you can do is ask youradvisor to review your portfolio annually.

On point two, equities are for the long haul. If you had avery short time frame, equity funds are not the place to be.So the real problem comes from the other 2; and all theyrequire you to do is keep it simple, keep it going, withSIPs.

Lump sum verses SIP

If you had invested in the market peak of January 2008,losing about 52 per cent of your capital by the end of thatyear is a classic example of the near-term impact of lump-sum investing. But had you held on and been a good long-term investor, the market would not have disappointedyou.

Better still, had you been doing an SIP, the equity marketwould have rewarded you more. Take a look at a fewsteady performing funds from our Select List and theindices to know how SIP rewards you for patientlycontinuing.

The table below shows returns lump sum investmentmade in mid-2007 (July 2007) when markets weretrending upwards and the return on SIPs made from thenon till date.

Performance from SIP returns Lump sumJuly 2007-June 2014 (%) returns (%)

HDFC Top 200 17.2 14.3

ICICI Value Discovery 24.6 17.2

UTI Opportunities 16.9 14.9

Sensex 12.0 8.1

CNX Mid Cap 13.3 8.6

SIP returns - IRR; SIP from July 2007 till dateLump sum returns - compounded annualized

SIPs worked better. Why? Because of the opportunity toaverage costs at lower levels in 2009, 2011 and partly in2013.

Lesson: Long-term investing is a must for equities. Evenfor the long term while lump sums are ok, SIPs work

www.fundsindia.com

What keeps me most excited and optimistic about India is how users have responded to Twitter andhow the country has now become one of the fastest-growing markets for us globally.

Rishi Jaitly, Head of Twitter, India

Vidya Bala

With equity markets zooming from September 2013 until now, you may either be feeling left outor fear entering the market rather late. You don’t have to, if you decide to go the SIP (SystematicInvestment Plan) way. Why? Because SIPs are good all-weather tool you can have to invest,especially in equities.

‘Do SIPs always offer me the best returns?’ - may be a question that many of you have askedyourself or your advisor. My answer is a NO. But what SIPs do, is insulate you best againstworst returns. And because of such insulation, you earn optimal and very often superior returns.

harder for you.

Stopping SIPs

Investors often stop their SIPs even with good funds fortwo reasons:

• One, equity market goes down and they get jittery andstop investing

• Two, equity market goes up and you therefore thinkaveraging at higher costs will not help and thereforestop SIPs

Let us take a more recent three-year period to know whathappens when you stop SIPs but hold your funds. Hadyou started SIPs in 2011 and continued for one year andstopped SIPs thinking the market was going up, yourreturns would have been 7-8 percentage points lower thancontinuing SIPs till date.

Returns between July 2011 and June 2014(%)

SIPs SIPs**Uninterrupted Stopped*

HDFC Top 200 20.4 27.2ICICI Value Discovery 29.8 37.8UTI Opportunities 18.3 22.3Sensex 17.0 21.0CNX Mid Cap 16.8 24.2

* SIPs between July 2011 to June 2012 and then stopped** SIPs between July 2011 to June 2014Returns as of June 13, 2014; SIP returns are IRR

Why? 2013 offered enough opportunities to average costsat lower levels. And with markets going up now, theaverage returns tend to be higher with the SIP that youcontinued.

Lesson: If you started your SIP for a specific long-term

goal, keep the SIP running until you near the goal.Stopping either because the equity market has gone up orgone down, not only disrupts returns, but prevents youfrom saving the necessary amount for the goal.

The bounce back

Above all these, the bounce back in the market is feltimmediately in SIP portfolios. Just take a look at the databelow. Not only has the SIP returns between March andnow bounced back, the returns are also far superior tolump-sum investing as a result of better averaging.

Investment in July 2011Returns as Returns as

of March 1, 2014 (%) of June 13, 2014 (%)SIP Lump sum SIP Lump sum

HDFC Top 200 7.0 0.6 22.8 9.3ICICI Value Discovery 13.7 6.1 32.2 16.4UTI Opportunities 9.8 5.2 19.7 10.9Sensex 8.5 0.9 17.6 6.1CNX Mid Cap 2.1 -4.1 19.8 5.3SIP from July 2011Returns as of June 13, 2014; SIP returns are IRRLump sum returns - compounded annualized

Lesson: The effect of all your averaging is felt in yourportfolio in a market revival and quite fast too. Hence, thekey is to keep it to SIPs and keep it going if you want toride the bullish and bearish phases in the equity market.The above data points clearly substantiate that with SIPs,you can enter the market any time and still gain over thelong term.

Use SIPs to build your wealth efficiently and to avoid rudeshocks to your portfolio.

www.fundsindia.com

Public sector banks are, if anything, in a worse position than private sector banks... As low riskenterprises migrate to financing from the markets, banks are left both with very large riskyinfrastructure projects and with lending to small and medium sized firms. The alternative totaking these risks is to plunge into very competitive retail lending, so public sector banks mayhave little option especially if the government pushes them to lend to infrastructure. Many ofthe projects being financed today, however, require sophisticated project evaluation skills andcareful design of the capital structure. Successful lending requires the lender to act to securehis position at the first sign of trouble, otherwise the slow banker ends up providing the losscover for more agile bankers or for unscrupulous promoters. To survive in the changingbusiness of lending, public sector banks need to have strong capabilities, undertake carefulproject monitoring, and move quickly to rectify problems when necessary.

Dr Raghuram Rajan, Governor, Reserve Bank of India

Viewpoint

source: www.rbi.org.in

www.fundsindia.com

The quarantine

Just as important as finding people with an excellent trackrecord of providing investing insights is avoiding thepeople who will result in money lost. Learning whoshould be ignored is the flip side of the favourites. I havespilled plenty of ink about the kinds of pundits who havebeen wrong too often to be taken seriously anymore. Myapproach is to quarantine these people like they havedeadly bubonic plague. Here is how I do that: WheneverI see a suspect analysis, an outrageous statement or anysort of forecast, I diary it for a year or two in the future.My favourite technique is to use any calendar.

It takes you some time, but you will eventually be able toidentify a bevy of people worthy of your disdain.Aggressively ignore their money losing blather. Snickereach time you see their latest nonsense. Once you figureout whose track record stinks, it is easy to not be fooledby their noise. You now have the makings of your own setof personal researchers. Find a balance that allows you toconsume as much information as you need. Myexperience has been that most investors can make muchbetter use of their time. That means less mindlessfinancial television viewing, and more reading of theclassic financial books.

Source: Barry Ritholtz is chief investment officer of Ritholtz WealthManagement. He is the author of “Bailout Nation” and runs afinance blog, the Big Picture (www.ritholtz.com). Read the full versionof his article at The Washington Post website athttp://www.washingtonpost.com.

The Sin of Late Payment

Wouldn’t it be great if missing a payment once in a whilewas no big deal? With the busy schedules these days, itreally is easy to forget dates…I mean due dates. But sadly,it is no casual matter and it is a big deal. And the big dealis that late payments hurt…your credit score and more.

Late Fees: Better late than never is a passé…its better ontime than late! If you pay your bills a single day after thescheduled due date, then be ready to pay the late paymentcharge. In case of credit cards, it either would be a fixedamount or a certain percentage of the minimum amountdue. In case of loans, you would be charged with a fixedamount as penalty for paying late plus interest on thedelayed payment.

High Interest Rate: Here is the second one…yourinterest rates could be reset to a higher level. Your latepayment or rather series of late payments could have justcautioned the bank to cover its risk of lending to you.Charging you a higher interest rate is one way of how thebank would minimize its risk.

Credit Report: And if you thought that the story of yourlate payments is known only to the bank then, well, here’sa surprise! The credit bureaus, which store and updatedata of all borrowers, also have a record of your paymenthistory. Your credit report would reflect the fact that youhave been delaying your repayments.

You can read the full version of this article by Satish Mehta is theFounder and Director of www.credexpert.in – a credit and debtcounseling company and other regular articles, check out the MarketPlace – FundsIndia, the official blog of FundsIndia.com, on a regularbasis at http://www.fundsindia.com/blog.

Market Place FundsIndia Blog

www.fundsindia.com

A lot of SBI customers opt for our products because of the brand and the trust factor. We don’twant to take undue advantage of that. We want to educate the customer before selling.

Bhaskar J Sarma, MD & CEO, SBI General Insurance

Blog Pick

Did you know?There was an interesting state-wise contribution of the Assets Under Management (AUM) of Mutual Funds inIndia in The Hindu Business Line. Just 10 of the 30-plus states and union territories account for 90% of the AUMof all mutual funds. Maharasthra accounts for about 48% - this is a both a reflection of reality as well as the locationof the registered / head offices of many of the major corporate and banking sector outfits. That 10 states hold sucha large share indicates the low penetration levels of not just mutual funds, but banking and financial services aswell. This also falls in line with the fact that a vast share of the industry AUM comes from the top 8 cities and mostmutual funds focus on them in a big way for development of business.

www.fundsindia.com

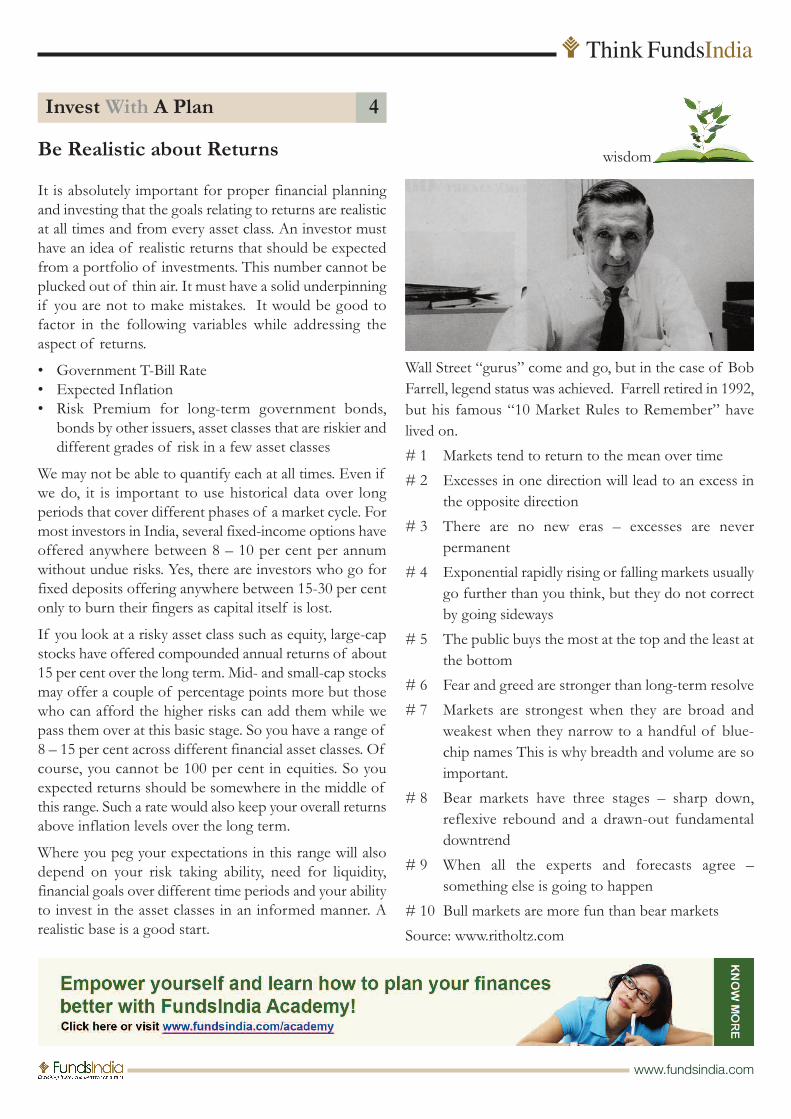

Be Realistic about Returns

It is absolutely important for proper financial planningand investing that the goals relating to returns are realisticat all times and from every asset class. An investor musthave an idea of realistic returns that should be expectedfrom a portfolio of investments. This number cannot beplucked out of thin air. It must have a solid underpinningif you are not to make mistakes. It would be good tofactor in the following variables while addressing theaspect of returns.

• Government T-Bill Rate• Expected Inflation• Risk Premium for long-term government bonds,

bonds by other issuers, asset classes that are riskier anddifferent grades of risk in a few asset classes

We may not be able to quantify each at all times. Even ifwe do, it is important to use historical data over longperiods that cover different phases of a market cycle. Formost investors in India, several fixed-income options haveoffered anywhere between 8 – 10 per cent per annumwithout undue risks. Yes, there are investors who go forfixed deposits offering anywhere between 15-30 per centonly to burn their fingers as capital itself is lost.

If you look at a risky asset class such as equity, large-capstocks have offered compounded annual returns of about15 per cent over the long term. Mid- and small-cap stocksmay offer a couple of percentage points more but thosewho can afford the higher risks can add them while wepass them over at this basic stage. So you have a range of8 – 15 per cent across different financial asset classes. Ofcourse, you cannot be 100 per cent in equities. So youexpected returns should be somewhere in the middle ofthis range. Such a rate would also keep your overall returnsabove inflation levels over the long term.

Where you peg your expectations in this range will alsodepend on your risk taking ability, need for liquidity,financial goals over different time periods and your abilityto invest in the asset classes in an informed manner. Arealistic base is a good start.

Wall Street “gurus” come and go, but in the case of BobFarrell, legend status was achieved. Farrell retired in 1992,but his famous “10 Market Rules to Remember” havelived on.

# 1 Markets tend to return to the mean over time

# 2 Excesses in one direction will lead to an excess inthe opposite direction

# 3 There are no new eras – excesses are neverpermanent

# 4 Exponential rapidly rising or falling markets usuallygo further than you think, but they do not correctby going sideways

# 5 The public buys the most at the top and the least atthe bottom

# 6 Fear and greed are stronger than long-term resolve

# 7 Markets are strongest when they are broad andweakest when they narrow to a handful of blue-chip names This is why breadth and volume are soimportant.

# 8 Bear markets have three stages – sharp down,reflexive rebound and a drawn-out fundamentaldowntrend

# 9 When all the experts and forecasts agree –something else is going to happen

# 10 Bull markets are more fun than bear markets

Source: www.ritholtz.com

Invest With A Plan 4

www.fundsindia.com

wisdom

Index 1 Year 5 Years 10 Years

CNX Nifty 28.6 11.9 17.4

S&P BSE Sensex 29.5 11.6 18.0

CNX Mid Cap 48.0 14.9 18.8

CNX Small Cap 82.1 14.7 21.0

CNX 100 30.2 12.4 17.6

CNX 500 34.9 11.9 17.2

CNX Bank 29.1 15.4 20.9

CNX Energy 22.5 3.2 13.3

CNX FMCG 3.5 24.2 23.3

CNX Infrastructure 46.1 -1.4 13.3

CNX IT 48.2 23.0 16.6

MSCI Emerging Markets 10.4 18.9 13.1

MSCI World 17.7 22.9 10.2

Returns (in per cent as of June 30, 2014) for less than one year is on an absolutebasis and for more than one year on a compounded annual basis.

Equity Performance Snapshot

Must Read

Mish makes mincemeat of Bloomberg

Bad economic analysis abounds. Some of it is so badyou wonder if the authors understand how anymarkets work, not just the topic of discussion. Forexample, please consider Gold Euphoria Won’t LastWith Yellen’s Rally Fading, a truly remarkable exercisebecause it took three Bloomberg writers to produce.In taking apart this article termed as Truly InanceBloomberg Analysis on Gold, blogger Mike Sherlockopines: `I do not know the future price of gold, nordoes anyone else. But I do know the fundamentaldrivers as well as the reasons to hold gold. Andneither of those has changed. I also know truly inaneeconomic reporting when I see it, and the Bloombergarticle quoted above is a perfect example’.(http://globaleconomicanalysis.blogspot.in)

www.fundsindia.com

Q. I feel that even in SIP mode of investment, if onecarefully watches market movements and for everyfall of the index, one utilizes the chance to enter themarket under SIP mode, it will marginally improvethe prospects by better averaging costs. That meansone need not formally set up SIP schedule but do itby watching the market trend. Please let me know ifI am right.

A. Timing the market is never easy. Market swings toomuch to catch it at the right time. Also, by waitingfor the 'right time' to invest, you may end up delayingthe investment and also your wealth accumulationplan especially when you are investing towards aspecific goal within a defined time frame.

What you said is a very ideal thing to do with stocksif one understands the reason behind a stock's fall.The advantage of mutual funds is that one need nottime the market; the fund manager does the job oftiming, by buying the right stocks at the right timeor accumulating them or exiting them. That is moreimportant and when you have a good fund managerto do it, market timing is secondary for a fundinvestor. Disciplined investment becomes theprimary goal.

If you are still keen to time the market using toolssuch as triggers, the best way is to keep an SIPrunning and make additional purchases on the samefunds when you are able to identify market falls. Thisway, you may continue to do your disciplinedmonthly investments and save the required amountfor your goals even as you average better by buyingmore on dips.

Vidya Bala

Q & A

I would argue that the tendency to cash out is not entirely irrational. The industry will soon begetting through this phase of continued redemptions and I expect to see fresh flows come in duringthe next quarter and beyond.

Leo Puri,Managing Director, UTI Asset Management Company

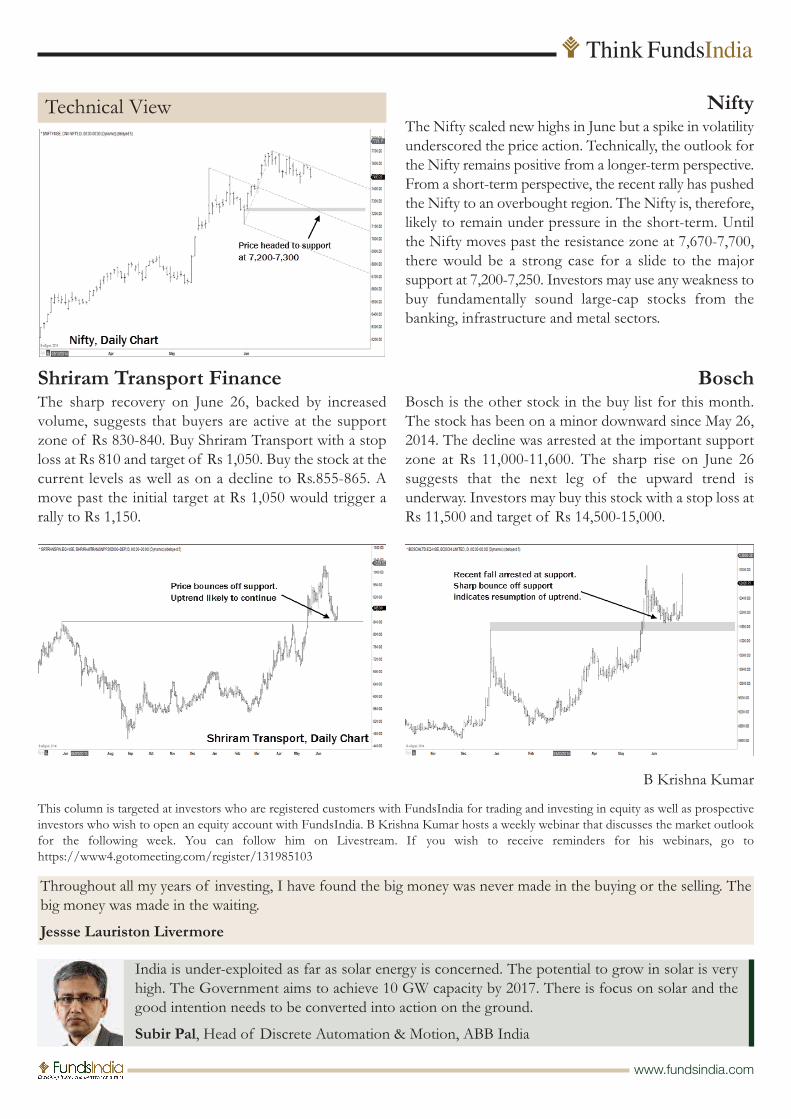

Technical View

BoschBosch is the other stock in the buy list for this month.The stock has been on a minor downward since May 26,2014. The decline was arrested at the important supportzone at Rs 11,000-11,600. The sharp rise on June 26suggests that the next leg of the upward trend isunderway. Investors may buy this stock with a stop loss atRs 11,500 and target of Rs 14,500-15,000.

Shriram Transport FinanceThe sharp recovery on June 26, backed by increasedvolume, suggests that buyers are active at the supportzone of Rs 830-840. Buy Shriram Transport with a stoploss at Rs 810 and target of Rs 1,050. Buy the stock at thecurrent levels as well as on a decline to Rs.855-865. Amove past the initial target at Rs 1,050 would trigger arally to Rs 1,150.

This column is targeted at investors who are registered customers with FundsIndia for trading and investing in equity as well as prospectiveinvestors who wish to open an equity account with FundsIndia. B Krishna Kumar hosts a weekly webinar that discusses the market outlookfor the following week. You can follow him on Livestream. If you wish to receive reminders for his webinars, go tohttps://www4.gotomeeting.com/register/131985103

www.fundsindia.com

NiftyThe Nifty scaled new highs in June but a spike in volatilityunderscored the price action. Technically, the outlook forthe Nifty remains positive from a longer-term perspective.From a short-term perspective, the recent rally has pushedthe Nifty to an overbought region. The Nifty is, therefore,likely to remain under pressure in the short-term. Untilthe Nifty moves past the resistance zone at 7,670-7,700,there would be a strong case for a slide to the majorsupport at 7,200-7,250. Investors may use any weakness tobuy fundamentally sound large-cap stocks from thebanking, infrastructure and metal sectors.

Throughout all my years of investing, I have found the big money was never made in the buying or the selling. Thebig money was made in the waiting.

Jessse Lauriston Livermore

India is under-exploited as far as solar energy is concerned. The potential to grow in solar is veryhigh. The Government aims to achieve 10 GW capacity by 2017. There is focus on solar and thegood intention needs to be converted into action on the ground.

Subir Pal, Head of Discrete Automation & Motion, ABB India

B Krishna Kumar

1 1 Name the first Exchange-Traded Funds-focusedfund house in India?

2 Which were the first, sector specific mutual fundslaunched in India?

3 Who is the author of The Intelligent Investor?4 Who is considered to be the founder of the concept

of index funds?5 Name the person in the image? She

occupies one of the more influentialpositions of power in the world ofeconomics and finance.

Answers can be emailed to [email protected]. Thefirst three to send in all correct answers will be entitled toa must-have book on investment. Answers for June 2014Quiz: 1) Arun Jaitley 2) Wholesale Debt Market Segment 3)Kothari Pioneer Money Market Scheme 4) Greed & Fear 5) R HPatil, first Chairman and Managing Director of National StockExchange.Prize Winner: There were no winners for June 2014.-

FundsIndia Select FundsFundsIndia's Select Funds is a list of mutual funds that wethink are most investment worthy for a regular investor.

There remains a larger ‘buy’ list of funds, Select Fundsmay be viewed as a more ‘what to buy today’ list; takingin account more qualitative factors such as marketconditions and a fund’s positioning to ride the same.

For a full list of FundsIndia Select funds, please go tohttp://www.fundsindia.com/select-funds. We review thislist on a quarterly basis.

At this juncture, we think it is worthwhile consideringfunds with a ‘growth’ approach, or those with higherweights to cyclical sectors than those loaded withdefensives.

It is for this reason that you may see some exits byotherwise sound funds. This is a relative call we have totake and is done to keep our list compact; not so muchbecause the funds that exited are underperformers.

We have quite a few funds that made the cut to our equityfund list. We added BNP Paribas Equity, ICICI Pru Top100, Birla Sun Life Top 100, Reliance Tax Saver (ELSS),SBI MagnumGlobal and Mirae Asset Emerging Bluechip.

We removed Canara Robeco Equity Diversified, HDFCIndex Fund Sensex Plus, Religare Tax Plan, SBI EmergingBusinesses and DSP BR Small and Midcap.

We have kept aside HDFC Index Fund Sensex Plus fromour Select list for now, given that in markets such as thepresent one, actively managed funds tend to outperform.

DSP BlackRock Small & Mid-Cap, as expected by us,made a lightning comeback, given that it is a high betafund. Its volatility, though, worries us a bit. We havetherefore put it in on our ‘watch’ list.

To know the reasons for the other changes, check out theFundsIndia Blog.

www.fundsindia.com

Disclaimer: Mutual Fund Investments are subject to market risks. Please read the offerdocuments available at the website of each mutual fund carefully before investing. Pastperformance does not indicate or guarantee future performance. There is risk of capitalloss and uncertainty of dividend distribution. Think FundsIndia, a monthly publicationof Wealth India Financial Services, is for information purposes only. Think FundsIndiais not and should not be construed as a prospectus, scheme information document oroffer document Information in this document has been obtained from sources that arecredible and reliable.Publisher: Wealth India Financial Services Editor: Srikanth Meenakshi

Quiz

Simplifying SIPs for instant investing

Starting June, we have made it easier for our instantinvesting customers to save through the SIP route.Earlier, they were required to register one mandate forevery SIP but now they will be able to use a singlemandate for all their SIPs.

Smart Solutions Updates

As indicated in the last update, we have rolled out thereviews of Your Smart Solutions by email. We have alsoenabled the ability to redeem money from Your SmartSolutions. The redemption can be done only at theportfolio level and will be done as per the asset allocation.

@fundsindia.com in June

...for every mid-cap stock that is a multi-bagger, there could be many that destroyed wealth... as much as 90 percent of investors’ wealth following the 2008 downturn writes Vidya Bala. Read more at FundsIndia Blog athttp://www.fundsindia.com/blog

To invest, call 0 7667 166 166