Thesis David Pozo

198

UNIVERSIDAD DE CASTILLA-LA MANCHA DEPARTAMENTO DE INGENIER ´ IA EL ´ ECTRICA, ELECTR ´ ONICA, AUTOM ´ ATICA Y COMUNICACIONES STOCHASTIC BILEVEL GAMES APPLICATIONS IN ELECTRICITY MARKETS TESIS DOCTORAL AUTOR: DAVID POZO C ´ AMARA DIRECTOR: JAVIER CONTRERAS SANZ Ciudad Real, Diciembre de 2012

-

Upload

jorge-hans-alayo-gamarra -

Category

Documents

-

view

45 -

download

6

description

Thesis David Pozo

Transcript of Thesis David Pozo

UNIVERSIDAD DE CASTILLA-LA MANCHA

DEPARTAMENTO DE INGENIERIA ELECTRICA,

ELECTRONICA, AUTOMATICA Y COMUNICACIONES

STOCHASTIC BILEVEL GAMES

APPLICATIONS IN ELECTRICITY

MARKETS

TESIS DOCTORAL

AUTOR: DAVID POZO CAMARA

DIRECTOR: JAVIER CONTRERAS SANZ

Ciudad Real, Diciembre de 2012

UNIVERSIDAD DE CASTILLA-LA MANCHA

DEPARTMENT OF ELECTRICAL ENGINEERING

STOCHASTIC BILEVEL GAMES

APPLICATIONS IN ELECTRICITY

MARKETS

PhD THESIS

AUTHOR: DAVID POZO CAMARA

SUPERVISOR: JAVIER CONTRERAS SANZ

Ciudad Real, December 2012

A mi madre.

Por su extraordinaria fuerza y coraje.

Preface

This thesis addresses the subject of bilevel games and their application for

modeling operational and planning problems in restructured power systems.

Such games are well fitted to model hierarchical competition but they are hard

to solve in general. Bilevel games set new challenges for power system operators

and planners and they constitute an ongoing topic for many researchers.

Bilevel games are generally modeled as equilibrium programs with equilib-

rium constraints (EPEC) within the operations research field. EPEC problems

are highly non-linear and non-convex, and the existence of global and unique

solutions is not guaranteed even in the simplest instances of EPECs. Hence, a

generalized theory and solution algorithms for solving EPECs have not been

firmly established so far. Only a few and specific instances of EPECs have been

shown to have equilibria. In many of these instances, the solution is stated as a

stationary equilibrium, which is not necessarily a global solution. Additionally,

most of the proposed solution techniques do not guarantee finding all pure

Nash equilibria. The difficulties both from a theoretical and a numerical point

of view arise because EPEC problems inherit the bad properties of the set of

MPEC problems that conform the corresponding EPEC.

In this thesis, we propose a special case of EPECs where leaders compete

among themselves at the upper level in a Nash equilibrium setting by making

decisions in finite strategies constrained by the solution of the lower level

problem, where the followers compete among themselves in a Nash equilibrium

setting by making continuous decisions. The upper and lower level problems

are linear and uncertainty is included at the lower level. Then, the bilevel

game is stated as a finite stochastic EPEC with the possibility of multiple

equilibria. This specific EPEC structure is appropriate for many problems

that appear in restructured power systems. We devote two chapters of this

thesis to show the applicability of this game structure in both operational and

planning frameworks.

ii

To overcome the difficulties described above, we propose a mixed integer lin-

ear reformulation (convexification) of the corresponding stochastic finite EPEC

problem. The advantage of this approach is two-fold. First, the linearized

formulation can be solved with standard mixed integer linear programming

(MILP) solvers and a global solution can be guaranteed for moderately-sized

problems. Second, the discrete strategies at the upper level problem allow us

to find all (pure) Nash equilibria. This is done by including a set of linear

constraints in the problem that represent “holes” in the feasible region for the

known Nash equilibria.

Finally, although the proposed methodology has several advantages, it is

important to recall its limitations. First, the linearization (convexification)

approach proposed in this thesis requires the inclusion of binary variables into

the model, which increases its complexity. And second, the lower-level problem

has to be a convex optimization problem (linear in this thesis) in order to

transform it into its equivalent and sufficient first-order optimality conditions.

Each chapter is fairly independent but they all share the same mathematical

notation. In Chapter 1 we give an overview of restructured power systems

and a review of the existing literature related with this thesis. In Chapter 2

we describe the mathematical framework for solving stochastic EPECs with

finite strategies. We apply the proposed stochastic EPEC models to electricity

markets in Chapters 3 and 4 in an operational and a planning framework,

respectively. In Chapter 3, a strategic bidding problem is proposed, where

electricity producers compete in the spot market. In Chapter 4 we present a

three-level problem for transmission and generation expansion. To conclude

the thesis, a short summary, conclusions and some hints on future research

topics are given in Chapter 5.

iii

Acknowledgments

This thesis would not have been possible without the financial support of

several institutions and the advice and guidance of many people.

I would like to express my deepest gratitude to my supervisor, Professor

Javier Contreras, for his excellent supervision, dedication, guidance and sup-

port over the past few years.

I am indebted to several relevant people that have helped with their sug-

gestions to add significant value to this thesis. They are not only relevant for

their suggestions, but also for their hospitality and for the exceptional human

and intellectual environment created. First of all, I wish to thank Professor

Felix F. Wu for giving me the opportunity to spend three months in 2009 and

six months in 2010 with his research group at the University of Hong Kong. I

would like to thank to Dr. Yunhe Hou for giving me the opportunity to visit

him at the University of Hong Kong for one month in 2011. I am also obliged

to Dr. Huifu Xu for receiving me in his research group at the University of

Southampton, United Kingdom, for three months in 2011. I would like to

acknowledge Antonio Canoyra, Antonio Guijarro and Angel Caballero, from

Gas Natural Fenosa company, for their suggestions at the beginning of this

thesis and their fruitful feedback to apply the models developed to the real

world. I am also obliged to Dr. Jose Ignacio Munoz and Dr. Javier Dıaz. My

sincere thanks to Professor Enzo E. Sauma for his relevant suggestions in this

work. It is also worth mentioning the contribution of Professor Sauma as a

co-author of two papers related to this thesis.

I thank several institutions that have supported my PhD studies allowing

me to spend part of this time at the University of Hong Kong, and at the

University of Southampton. First of all, I would like to thank Gas Natural

Fenosa company for their financial support at the beginning of my PhD. Also,

I wish to thank Junta de Comunidades de Castilla-La Mancha of Spain for its

financial support through the program “Formacion del Personal Investigador”

iv

grant 402/09. Additionally, I thank the University of Hong Kong for their

support during my visit. I am also indebted to the Universidad de Castilla-La

Mancha for allowing me to use its facilities and the financial support from the

program “Ayudas a la Investigacion para la realizacion de Tesis Doctorales”.

I wish to acknowledge all my colleagues and good friends I have made during

these years at the Escuela Tecnica Superior de Ingenieros Industriales at Ciu-

dad Real, at the Electrical Engineering Department of the University of Hong

Kong and at the School of Mathematics at the University of Southampton.

Claudia, Virginia, Agustın, Alberto, Rafa, Alex Street, Jesus Lopez, Cristiane,

Luis, Valentın, Juanda, Carlos Rocha, Roberto Lotero, Wilian, Rafaella, Diego,

Vıctor Hugo, Choco, Javi Fernandez, Dani, Jenny, Marco, Ali, Jalal, Benvindo,

He Yang, Kai Liu, Simon, Joshep Sun, Peter and Arash thank you for their

friendship.

To my family, Mum, Dad, Luis, Rocıo and Ramon, thank you for your

unconditional support.

Contents

Contents v

List of Figures ix

List of Tables xi

Acronyms xiv

1 Introduction 1

1.1 Electric Power Systems . . . . . . . . . . . . . . . . . . . . . . . 1

1.1.1 Power System Participants . . . . . . . . . . . . . . . . . 3

1.1.2 Electricity Markets . . . . . . . . . . . . . . . . . . . . . 4

1.1.3 Energy Transmission Activity . . . . . . . . . . . . . . . 5

1.2 Motivation, Aims and Solution Approach . . . . . . . . . . . . . 6

1.3 Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.3.1 Equilibrium Models under Restructured Environments . 10

1.3.2 Operational Framework: The Strategic Bidding Problem 14

1.3.3 Planning Framework: Capacity Expansion Problem . . . 16

1.3.4 From Bilevel to EPEC Optimization Modeling . . . . . . 18

1.4 Thesis Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . 23

1.5 Thesis Organization . . . . . . . . . . . . . . . . . . . . . . . . . 24

2 Mathematical Framework for Bilevel Games 27

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

2.2 Game Theory Definitions . . . . . . . . . . . . . . . . . . . . . . 32

2.3 One-Level Games . . . . . . . . . . . . . . . . . . . . . . . . . . 33

v

vi CONTENTS

2.3.1 Nash Equilibrium Problem . . . . . . . . . . . . . . . . . 33

2.3.2 Generalized Nash Equilibrium Problem . . . . . . . . . . 34

2.3.3 Generalized Nash Equilibrium Problem with Shared Con-

straints . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

2.3.4 Stochastic Generalized Nash Equilibrium Problem . . . . 39

2.3.5 Finite-Strategy Nash Equilibrium Problem . . . . . . . . 41

2.3.6 Finite Generalized Nash Equilibrium Problem with Shared

Constraints . . . . . . . . . . . . . . . . . . . . . . . . . 43

2.3.7 Finding All Pure Nash Equilibria in a Finite NEP . . . . 45

2.4 Bilevel Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2.4.1 Single-Leader-Single-Follower Games . . . . . . . . . . . 48

2.4.2 Single-Leader-Multiple-Follower Games . . . . . . . . . . 50

2.4.3 Multiple-Leader-Single-Follower Games . . . . . . . . . . 52

2.4.4 Multiple-Leader-Multiple-Follower Games . . . . . . . . 53

2.4.5 Stochastic Multiple-Leader-Multiple-Follower Games . . 54

2.4.6 Stochastic Multiple-Leader-Multiple-Follower Games in

Finite Strategies . . . . . . . . . . . . . . . . . . . . . . 56

2.4.7 Bilevel Games could be Special Cases of Generalized

Nash Equilibrium Problems . . . . . . . . . . . . . . . . 59

2.4.8 Other Bilevel Games Compositions . . . . . . . . . . . . 62

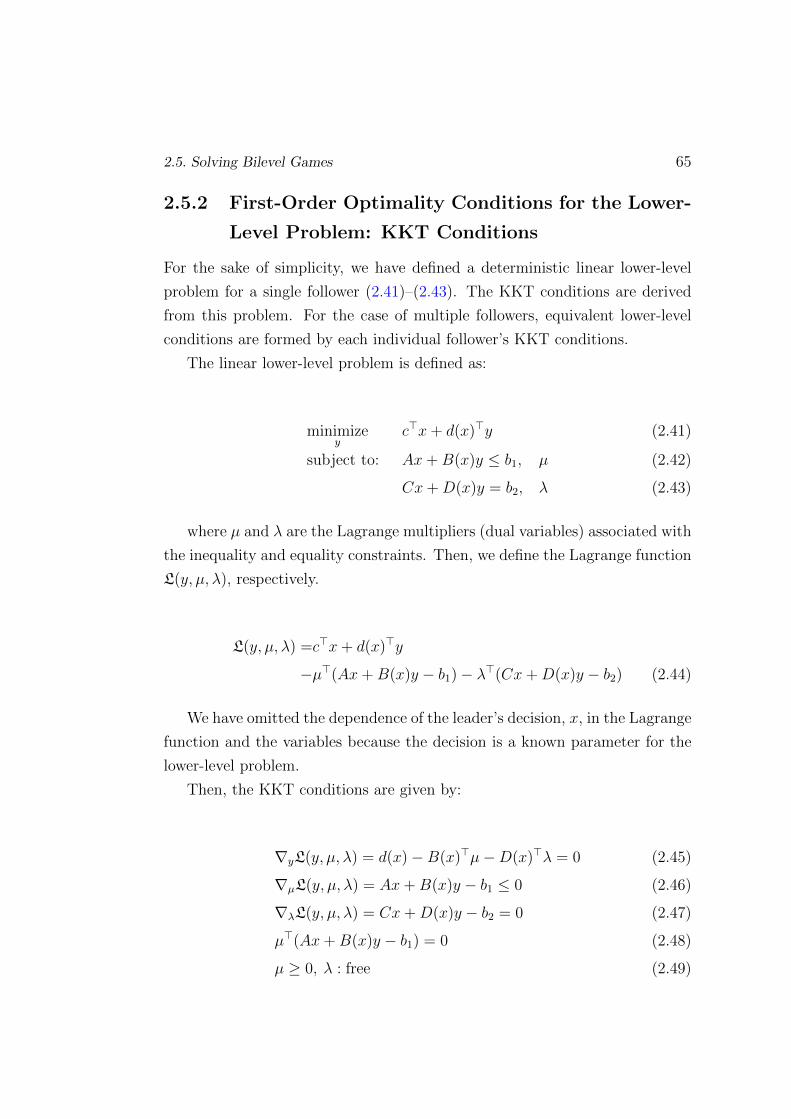

2.5 Solving Bilevel Games . . . . . . . . . . . . . . . . . . . . . . . 62

2.5.1 Manifolds of Lower-Level Solutions . . . . . . . . . . . . 64

2.5.2 First-Order Optimality Conditions for the Lower-Level

Problem: KKT Conditions . . . . . . . . . . . . . . . . . 65

2.5.3 First Order Optimality Conditions for the Lower-Level

Problem: Primal, Dual and Strong Duality Theorem . . 66

3 Strategic Bidding in Electricity Markets 69

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

3.2 Spot Market Strategic Bidding Equilibrium . . . . . . . . . . . . 76

3.2.1 Bilevel Formulation Disregarding the Network . . . . . . 76

3.2.2 MPEC Mixed Integer Linear Reformulation . . . . . . . 77

3.2.3 Stochastic EPEC MILP Formulation . . . . . . . . . . . 81

CONTENTS vii

3.2.4 Network-Constrained Stochastic EPEC Problem . . . . . 85

3.2.5 Finding All Pure Nash Equilibria . . . . . . . . . . . . . 90

3.3 Computational Complexity . . . . . . . . . . . . . . . . . . . . . 91

3.4 Illustrative Examples . . . . . . . . . . . . . . . . . . . . . . . . 92

3.4.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

3.4.2 Results for the Network-Unconstrained System . . . . . . 95

3.4.3 Results for the Network-Constrained System . . . . . . . 96

3.4.4 CPU Time and Computational Complexity . . . . . . . . 100

3.5 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . 100

4 Transmission and Generation Expansion 103

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 108

4.2 Transmission and Generation Expansion as a Three-Level Model 109

4.2.1 Third Level: Spot Market clearing . . . . . . . . . . . . . 110

4.2.1.1 ISO Problem Formulation . . . . . . . . . . . . 111

4.2.1.2 GENCO Problem Formulation . . . . . . . . . 113

4.2.2 Second Level: Generation Investment Equilibria . . . . . 115

4.2.3 First Level: Transmission Investment Planning . . . . . . 122

4.3 Finding All Pure Nash Equilibria at the Second Level . . . . . . 123

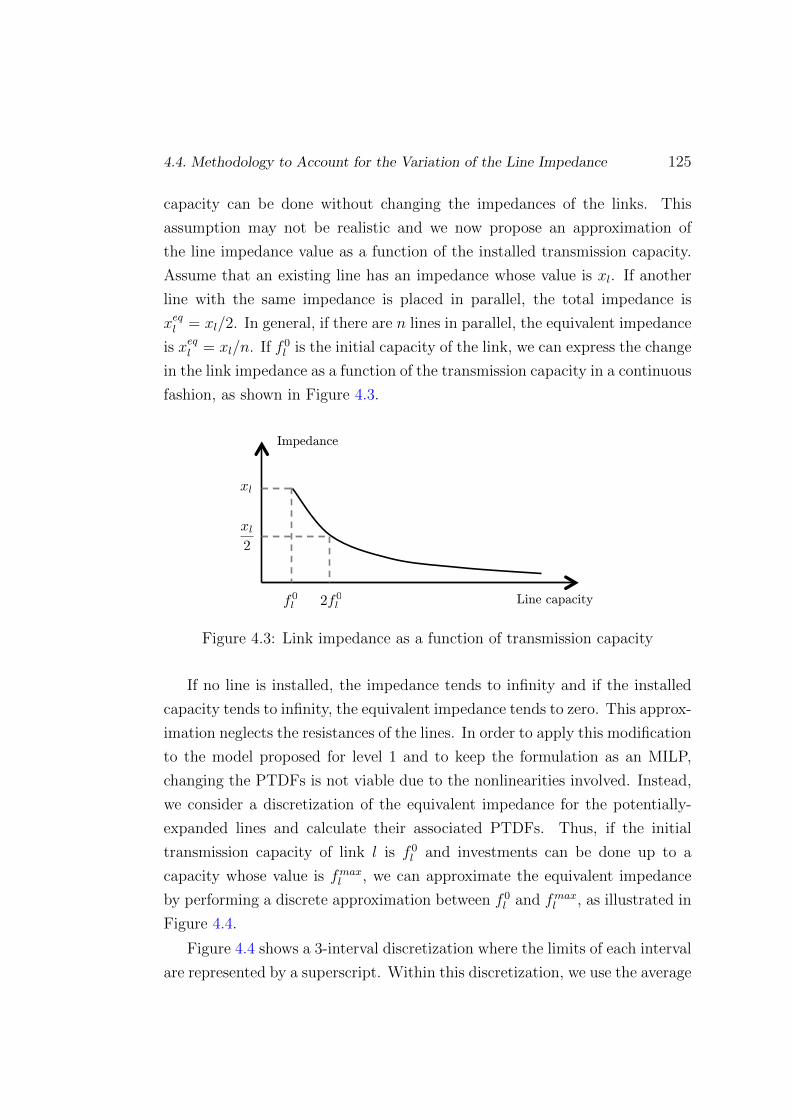

4.4 Methodology to Account for the Variation of the Line Impedance124

4.5 Computational Complexity . . . . . . . . . . . . . . . . . . . . . 128

4.6 Illustrative Examples . . . . . . . . . . . . . . . . . . . . . . . . 129

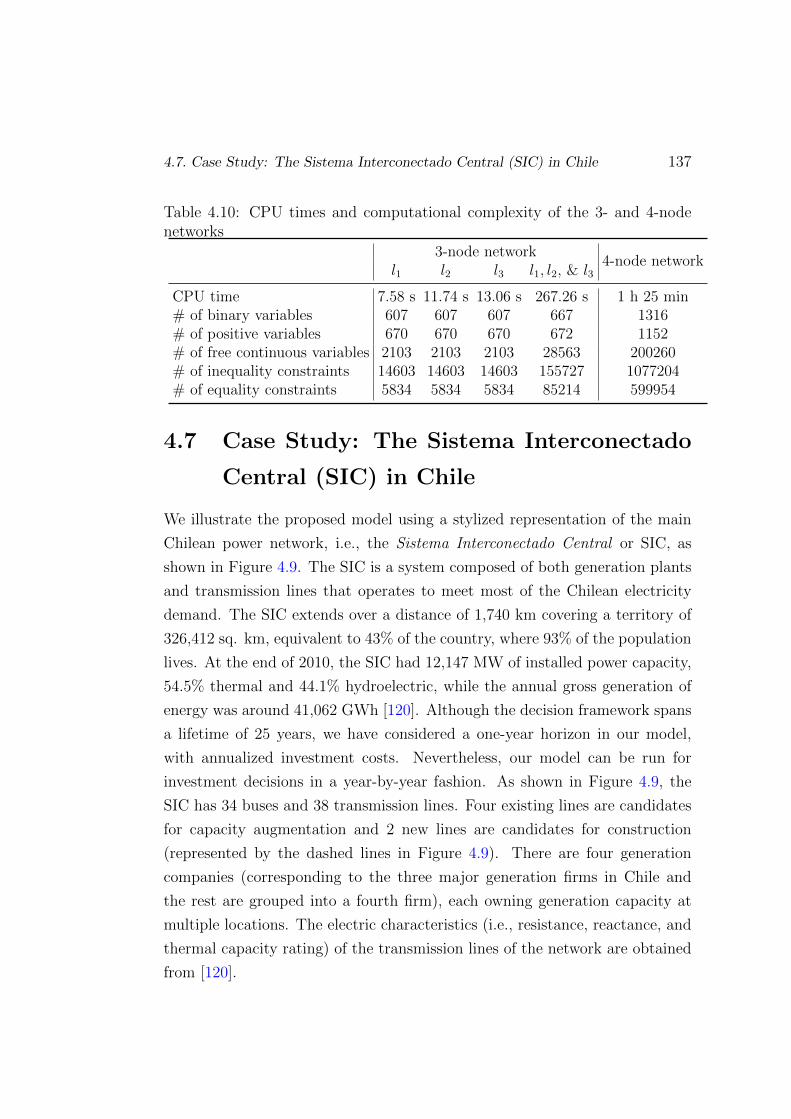

4.7 Case Study: The Sistema Interconectado Central (SIC) in Chile 137

4.8 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . 144

5 Summary, Conclusions, Contributions and Future Research 145

5.1 Thesis Summary . . . . . . . . . . . . . . . . . . . . . . . . . . 145

5.2 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

5.3 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

5.4 Future Research Suggestions . . . . . . . . . . . . . . . . . . . . 152

A Capacity Expansion SEPEC-MILP Formulation 155

B Main Chilean Power System (SIC) Data 159

viii CONTENTS

Bibliography 163

List of Figures

2.1 Bilevel game structure . . . . . . . . . . . . . . . . . . . . . . . 29

2.2 Example of (closed and convex) sets of strategies: Left for the

NEP defined in (2.7); Right for the GNEP defined in (2.8) . . . 35

2.3 Example of (closed and convex) sets of strategies: Left for the

GNEP with coupled constraints defined in (2.8); Right for the

GNEP with shared constraints defined in (2.11) . . . . . . . . . 37

2.4 NEP solution from equation (2.7) . . . . . . . . . . . . . . . . . 38

2.5 GNEP solution from equation (2.8) . . . . . . . . . . . . . . . . 39

2.6 GNEP with shared constraints solutions from equation (2.11) . 40

2.7 Discrete strategy set and solution for the finite NEP . . . . . . . 43

2.8 Discretized GNE with shared constraints . . . . . . . . . . . . . 45

2.9 Single-leader-single-follower game . . . . . . . . . . . . . . . . . 48

2.10 Single-leader-multiple-follower game . . . . . . . . . . . . . . . . 50

2.11 Multiple-leader-single-follower game . . . . . . . . . . . . . . . . 52

2.12 Multiple-leader-multiple-follower game . . . . . . . . . . . . . . 54

2.13 Strategies set for players x1, x2 and y . . . . . . . . . . . . . . . 61

3.1 4-node system . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

3.2 Stack offers (red) for the first equilibrium, competitive stack

offers (grey) and demand scenarios (blue) . . . . . . . . . . . . . 100

3.3 Stack offers (red) for the sixth equilibrium, competitive stack

offers (grey) and demand scenarios (blue) . . . . . . . . . . . . . 101

4.1 The three-level transmission and generation problem framework 109

4.2 Marginal generation cost functions . . . . . . . . . . . . . . . . 110

ix

x LIST OF FIGURES

4.3 Link impedance as a function of transmission capacity . . . . . 125

4.4 Discretization of the equivalent impedance as a function of in-

stalled transmission capacity . . . . . . . . . . . . . . . . . . . . 126

4.5 3-node case study . . . . . . . . . . . . . . . . . . . . . . . . . . 131

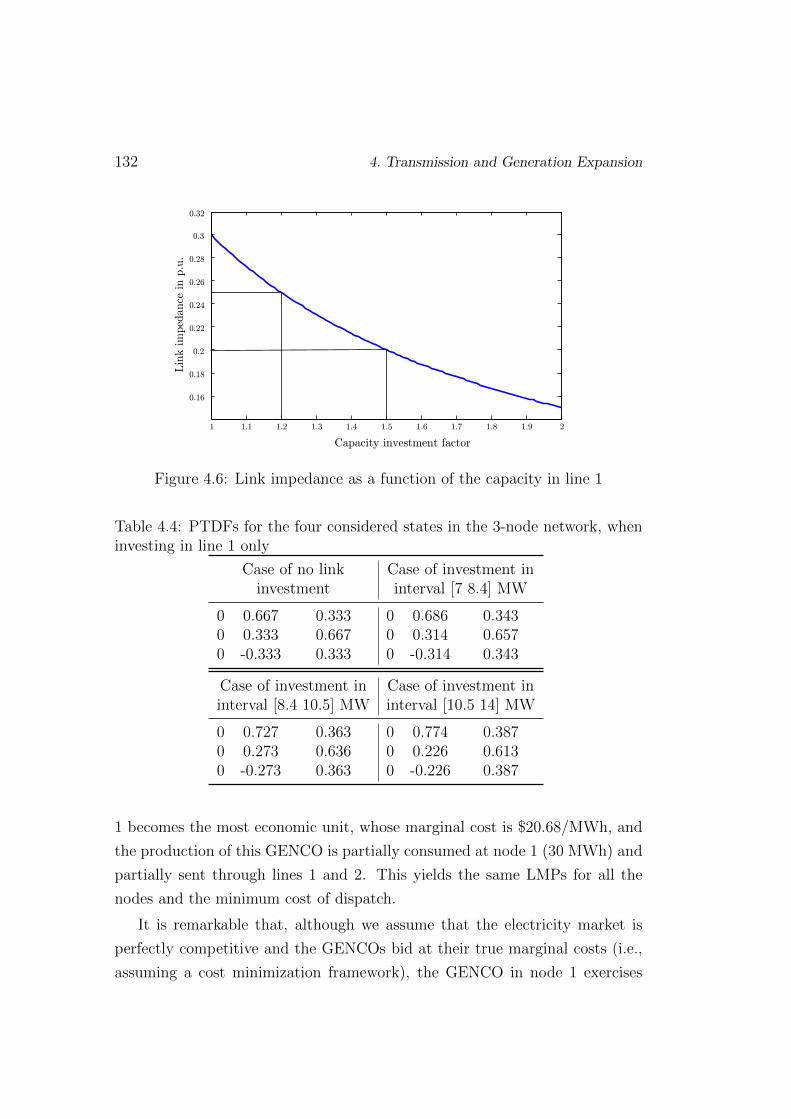

4.6 Link impedance as a function of the capacity in line 1 . . . . . . 132

4.7 Optimistic and pessimistic level 1 solutions for the case of in-

vesting only in line 1 . . . . . . . . . . . . . . . . . . . . . . . . 134

4.8 4-node case study . . . . . . . . . . . . . . . . . . . . . . . . . . 135

4.9 Stylized representation of the Chilean SIC network . . . . . . . 138

List of Tables

3.1 Computational complexity for the network-unconstrained problem 92

3.2 Computational complexity for the network-constrained problem 92

3.3 Generating units: power limits and marginal costs . . . . . . . . 93

3.4 Generating units: strategy bids . . . . . . . . . . . . . . . . . . 93

3.5 Demand scenario . . . . . . . . . . . . . . . . . . . . . . . . . . 93

3.6 PTDF matrix for the 4-node system . . . . . . . . . . . . . . . . 94

3.7 Pure Nash equilibria obtained from the payoff matrix method . 95

3.8 Thermal line limits (MW) . . . . . . . . . . . . . . . . . . . . . 96

3.9 GENCO’s expected profits for the congested network case . . . 98

3.10 Expected LMPs for the congested network case . . . . . . . . . 99

3.11 GENCO’s expected profits for the uncongested network case . . 99

3.12 Expected LMPs for the uncongested network case . . . . . . . . 99

3.13 CPU time comparison . . . . . . . . . . . . . . . . . . . . . . . 101

3.14 Case study computational complexity . . . . . . . . . . . . . . . 102

4.1 Computational complexity . . . . . . . . . . . . . . . . . . . . . 130

4.2 Order of complexity . . . . . . . . . . . . . . . . . . . . . . . . . 130

4.3 3-node case study data . . . . . . . . . . . . . . . . . . . . . . . 131

4.4 PTDFs for the four considered states in the 3-node network,

when investing in line 1 only . . . . . . . . . . . . . . . . . . . . 132

4.5 Optimal market clearing values given the solutions of level 1

and 2 in the 3-node network . . . . . . . . . . . . . . . . . . . . 133

4.6 Optimal values of the problem for level 1 of the 3-node network 133

4.7 4-node example data . . . . . . . . . . . . . . . . . . . . . . . . 135

4.8 4-node example line data . . . . . . . . . . . . . . . . . . . . . . 136

xi

xii LIST OF TABLES

4.9 Optimal values of the problem for level 1 of the 4-node network 136

4.10 CPU times and computational complexity of the 3- and 4-node

networks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

4.11 Line expansion data . . . . . . . . . . . . . . . . . . . . . . . . 139

4.12 Node expansion data: Generation limits . . . . . . . . . . . . . 140

4.13 Node expansion data: Costs . . . . . . . . . . . . . . . . . . . . 140

4.14 Transmission planner results . . . . . . . . . . . . . . . . . . . . 141

4.15 Annual profits and generation expansion results . . . . . . . . . 142

4.16 Generation capacity expansion . . . . . . . . . . . . . . . . . . . 142

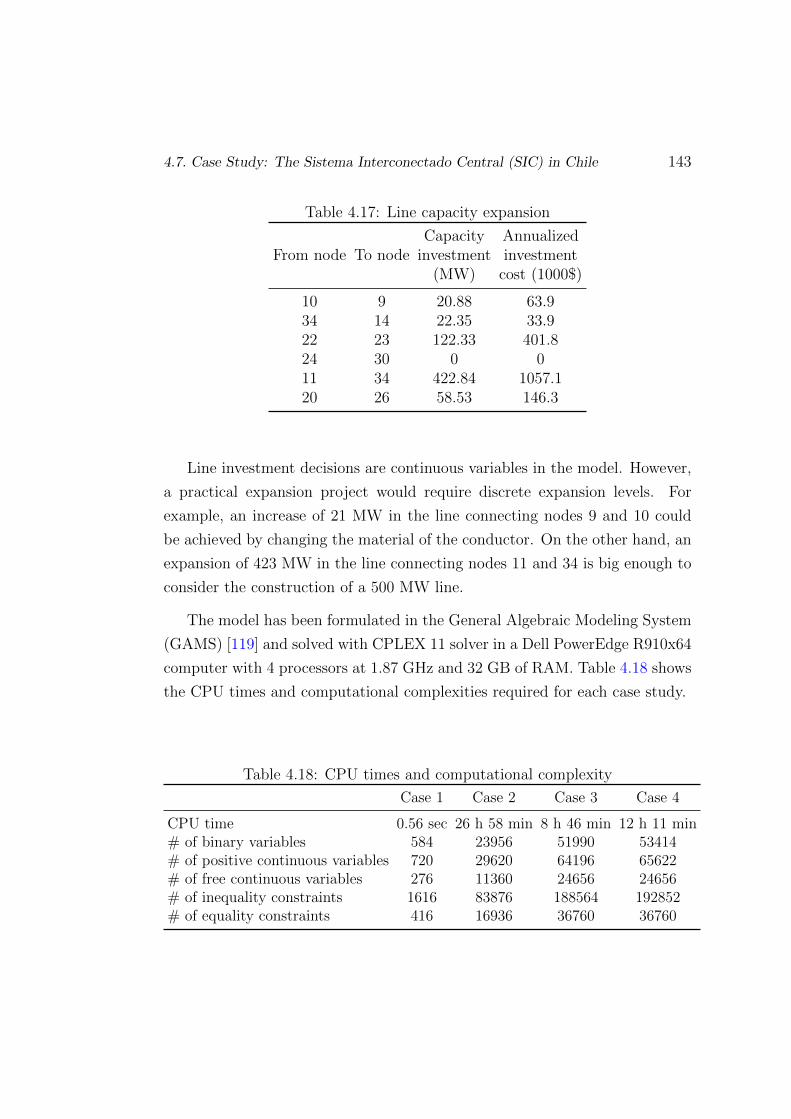

4.17 Line capacity expansion . . . . . . . . . . . . . . . . . . . . . . 143

4.18 CPU times and computational complexity . . . . . . . . . . . . 143

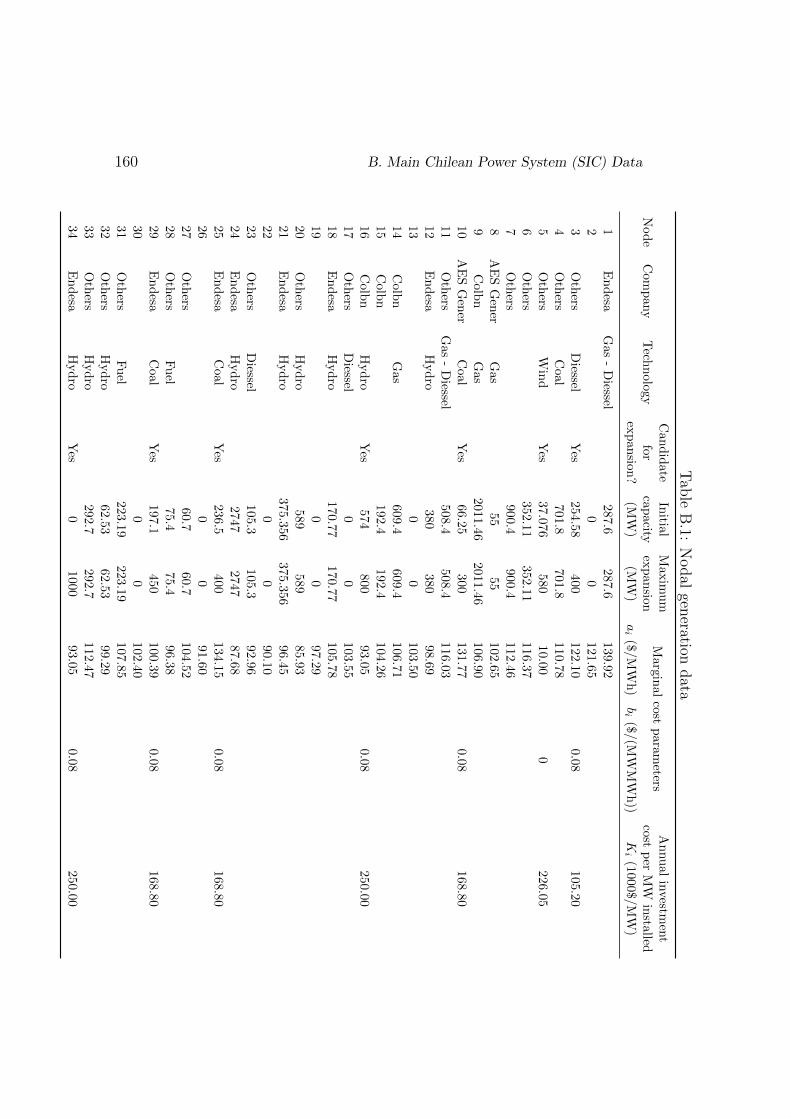

B.1 Nodal generation data . . . . . . . . . . . . . . . . . . . . . . . 160

B.2 Nodal load demand scenarios . . . . . . . . . . . . . . . . . . . 161

B.3 Lines transmission data . . . . . . . . . . . . . . . . . . . . . . . 162

Acronyms

CV Conjectural Variation.

CVaR Conditional Value at Risk

DC Direct Current.

EPEC Equilibrium Problem with Equilibrium Constraints.

GENCO Generating Company.

GNE Generalized Nash Equilibria.

GNEP Generalized Nash Equilibrium Problem.

ISO Independent System Operator.

KKT Karush-Kuhn-Tucker.

LHS Left Hand Side

LIQC Linear Independence Constraint Qualification.

LMP Locational Marginal Price.

LP Linear Programming.

MCP Marginal Clearing Price.

MFQC Mangasarian-Fromowitz Constraint Qualification.

MILP Mixed-Integer Linear Programming.

xiii

xiv Acronyms

MPCC Mathematical Program with Complementary Constraints.

MPEC Mathematical Program with Equilibrium Constraints.

NEP Nash Equilibrium Problem.

NLP Non-Linear Programming.

PTDF Power Transfer Distribution Factors.

RHS Right Hand Side

SEPEC Stochastic Equilibrium Problem with Equilibrium Constraints.

SFE Supply Function Equilibrium.

SMPEC Stochastic Mathematical Program with Equilibrium Constraints.

SIC Sistema Interconectado Central (Mainland Chilean Power Sys-

tem).

Chapter 1

Introduction

This chapter provides a general view of restructured electric power systems to

offer state-of-the-art bibliography for this dissertation, showing the motivation

and solution approach of this thesis.

Section 1.1 outlines the power system and the electricity market models

after the restructuring process that has taken place around the world. Section

1.2 summarizes the main assumptions and the solution approach taken in this

dissertation. Section 1.3 presents the main literature directly related with this

thesis. In Section 1.4 we list the main objectives of this dissertation. Finally,

in Section 1.5 we outline the document structure.

1.1 Electric Power Systems

In the last two decades there has been a gradual process of restructuring

of the electricity sector in many countries. Electricity markets have moved

towards market liberalization by privatizing large state-owned companies, or

more often, by de-regulating privately owned regulated utilities, as in Spain

or the United States, creating organisms that promote rules for the proper

operation of these electricity markets. Sometimes organisms, as Regulatory

Commissions, have been created that may or may not have antitrust juris-

diction. Almost always already extant organisms (e.g. the Federal Energy

Regulatory Commission [1]) have seen their jurisdiction expanded. There are

1

2 1. Introduction

many countries that have joined the restructuring process, learning valuable

lessons from other countries that had liberalized their own markets [2]. As a

result, complex regulatory frameworks have been created applying new and

usually complex economic theories.

There are four main activities related to electricity: generation, transport,

distribution and commercialization [3–6]. In traditional power systems all of

these activities are regulated, and in general they are part of a single vertically-

integrated company, usually state-owned. That is, decisions are made by a

centralized planner that minimizes total operating costs, respecting all the

technical constraints and ensuring a satisfactory level of reliability. In this

sense, mathematical programming techniques and tools have played a key role

in implementing these rules.

From the early eighties there has been an undergoing deregulation process

of the electricity business with a clear tendency towards disintegration and

separation of all the activities to foster competition. The motivation for this

evolution is the search for [4]:

• Cheaper electricity.

• Efficient capacity expansion planning.

• Price reflecting the real cost of the electricity supply rather than setting

a tariff.

• Cost minimization driving the operation and planning for the partici-

pants.

• Better service due to having a reliable power system.

• Enabling third party access.

• Encouraging transparency in the market.

Under this new environment for trading energy, the operation and planning

in power systems have to be considered from a decentralized perspective. For

example, each generating company (GENCO) decide how much energy to

1.1. Electric Power Systems 3

produce by itself, the management of its water reservoirs, and the maintenance

plan for its generating units. The investment on capacity expansion is not

centralized, hence the decisions are made by the GENCO who tries to maximize

profits obtained by the investment, as they do not typically have specific

responsibilities related to system adequacy.

Thus, decision making in the operation and planning of power systems is

economically driven. To help understand the behavior of the participants in

the market it is necessary to include basic concepts of microeconomic analysis.

Within this discipline, game theory market equilibrium models have played an

important role in shaping the markets for power systems.

1.1.1 Power System Participants

The agents that participate in the electricity market are: producers, con-

sumers, retailers, the market operator and the independent system operator.

• Producers. Their role is to produce electricity to supply demand as

well as the investment, operation and maintenance of their generation

facilities. They are also called generating companies (GENCOs).

• Consumers. Consumers are the energy buyers, usually buying energy

from the retailers. Some regulatory frameworks allow large consumers

to buy energy directly from the producers or from the market.

• Retailers. Retailers trade energy between producers and consumers.

They do not own generating units, therefore, they purchase the energy

in the electricity market to sell to the consumers.

• Market Operator. The market operator is responsible for the economic

management of the power system as a function of the supply generation

offers and the demand offers received. It enforces the market rules and,

in general, the market clearing procedure is based on the maximization

of social welfare or the minimization of generation costs.

• Independent System Operator. It is responsible for the technical

management of the system. The main objective is to guarantee a reliable

4 1. Introduction

real-time energy supply service. To do so, the Independent System

Operator (ISO) needs to coordinate the production, consumption and

electricity transport.

In some power systems, such as PJM and California, the market operator

is merged with the ISO. Hence, the ISO is responsible for the economic

and the technical management of the market.

Other important participants in the power system, but not directly involved

with the wholesale energy market are:

• Transmission companies. They are responsible for building, main-

taining and operating the transmission lines that they own. In some

systems there is a single transmission company that owns most of the

transmission grid as in the Spanish power system [7].

• Distribution companies. Distribution companies receive the bulk

energy from the transmission grid and distribute it to the consumers

located at different geographical regions.

• Market regulator. The market regulator is an independent entity that

monitors the electricity market and ensures that market operations are

correct, i.e. that they are transparent, efficient and competitive.

1.1.2 Electricity Markets

The most common market mechanisms for energy trading throughout the

world are listed below. In general, they support different time frames that

suit the needs for keeping the balance between supply and demand.

• Forward market. This is a market where the energy is traded for

delivery in future periods ranging from one week to one year or more

than one year in advance. In this market transactions can be done with

a physical delivery of energy, a financial agreement or simply settled by

price differences against the day-ahead market.

1.1. Electric Power Systems 5

• Bilateral contracts. Agents can freely sign purchase contracts (called

physical bilateral contracts) with other agents as an alternative to con-

tracting in organized markets. The energy associated with this type of

contract must be communicated to the ISO to be taken into account in

the dispatch of electricity.

• Day-ahead market. This is a short-term market where energy is traded

for each of the 24 hours of the next day in a hourly basis or a 30-min

basis. The price of this market is the best reference price of electricity

and is used for the settlement of the futures market and other elements

of the regulation of the sector. One day prior to the energy delivery, the

energy production is committed in this market with economic criteria

subject to the feasibility of the scheduled energy program to meet the

demand.

• Ancillary services. Power systems require that generating units adjust

their production levels to the level of demand at any given time. To

achieve this there are ancillary services that are divided into primary,

secondary, tertiary control and imbalance management. Without going

into detail, it should be noted that, except for primary regulation, the

rest are provided at market rates through auctions, where only producers

with the ability to meet the load variation are allowed.

1.1.3 Energy Transmission Activity

The transmission of electricity can improve the reliability of the electricity

system, fostering the use of technologies for generating electricity with the

cheapest sources.

Electricity transmission is a natural monopoly in most power systems, typ-

ically managed in each political jurisdiction by a single monopolist (although

not always, see the United States). That is, the network is operated as a

whole. This feature is especially important in the current situation of most

electricity sectors where the unbundling of activities of generation and sale

of electricity has taken place. In this case, the transmission of electrical

6 1. Introduction

energy is the meeting point for the sales and purchases of energy, being of

vital importance to ensure the proper state of the power system, and being an

essential facility, therefore, access must be also regulated.

From an economic point of view, the transmission network features can be

summarized in four points: i) operating costs of the network are negligible

(approximately 3% annually) compared to investment costs; ii) transmission

costs exhibit economies of scale; iii) the relative economic of the transmission

network variable depending on the geographic extension of the country and

the dispersion of generation and consumption centers; iv) the power system,

including the transmission network should be operated as a whole.

1.2 Motivation, Aims and Solution Approach

In restructured power systems, decision making in the short-, mid- or long-term

has become market-driven. From an economic point of view, electricity mar-

kets are often characterized by perfect competition models, but oligopolistic

models better represent the behavior of the markets. Numerous publications

propose and analyze models for these behaviors. Most of them use game

theory to model the interaction of players: generators, consumers and the

market regulator.

In this dissertation we study games within a bilevel optimization frame-

work. When there is only one player (leader) at the upper level and one player

(follower) at the lower level, this problem is the so-called Stackelberg game.

When the number of players at the upper and lower levels is more than one,

the model becomes an EPEC optimization problem. Then, the problem is also

called a Nash game or, sometimes, a Nash-Stackelberg game. Such problems

are in general non-convex and finding a global optimal solution is a challenge.

Therefore, the corresponding EPEC game may not have a Nash equilibrium,

may have just one, or may have multiple equilibria. This motivates the

development of mathematical tools for solving global optimal solutions and

for finding all Nash equilibria. Until now, it has not been possible to have

a methodology to do it. In this dissertation we propose a new methodology

for finding all (pure) Nash global equilibria for a specific game structure were

1.2. Motivation, Aims and Solution Approach 7

decisions at the upper level are discrete and decisions at the lower level are

continuous within a linear optimization problem. Additionally, we include

stochasticity at the lower level.

Several problems in power systems are well represented by an EPEC model,

such as the strategic bidding problem, generation capacity expansion or an-

nual unit maintenance scheduling among others. In this dissertation we have

addressed two problems: i) the strategic bidding equilibrium in the day-ahead

or short-term market; ii) the transmission and generation capacity expansion

planning in the long term.

1. Operations framework. Finding all (pure) Nash equilibria in oligopolis-

tic pool-based markets.

We present a compact formulation to find all pure Nash equilibria in a

pool-based electricity market with stochastic demands. The equilibrium

model is formulated as a stochastic EPEC. The problem is based on

a Stackelberg game where GENCOs optimize their strategic bids an-

ticipating the solution of the ISO market clearing. A finite strategy

approach both in price and quantity offers is applied to transform the

non-linear and non-convex set of Nash inequalities into an MILP model.

A procedure to find all Nash equilibria is developed by generating “holes”

that are added as linear constraints to the feasibility region. The result

of the problem is the set of all pure Nash equilibria, the market clearing

prices and energies assigned by the ISO to the GENCOs.

2. Planning framework. Anticipative transmission planning: interaction

with generation expansion.

We formulate a three-level mixed integer linear programming optimiza-

tion model of transmission planning that is inspired in the model pro-

posed by Sauma and Oren [8], which allows us to solve the optimal

transmission expansion problem. The proposed model integrates trans-

mission planning, generation investment, and market operation decisions.

Contrary to Sauma-and-Oren’s proactive methodology, we solve the op-

timal transmission expansion problem anticipating both the equilibria

8 1. Introduction

of generation investments made by GENCOs acting in a decentralized

market and the market clearing equilibria.

As in [8], our model accounts for transmission network constraints through

a lossless DC approximation of Kirchhoff’s laws. However, unlike [8],

we assume that the electricity market is perfectly competitive in order

to guarantee that the linear transformation of the three-level problem

is convex. Within this framework we are able to solve the three-level

problem and find the optimal transmission expansion.

The lower-level model represents the equilibrium of a pool-based market;

the intermediate level represents the Nash equilibrium in generation

capacity expansion, taking into account the outcomes on the spot market;

and the upper-level model represents the anticipation of transmission ex-

pansion planning to the investment in generation capacity and the pool-

based market equilibrium. Demand has been considered as exogenous

and locational marginal prices are obtained as endogenous variables of

the model.

The model is applied to a realistic power system in Chile to illustrate

the methodology and proper conclusions are reached.

The main assumptions in this dissertation are:

• Centrally-dispatched energy market. Centralized-dispatched mar-

kets have been included into deregulated markets [3–5] for electricity

trading. The spot or pool-based market is one the most common mar-

kets where an Independent System Operator (ISO) matches the energy

demanded with the energy supplied with economic criteria (maximization

of social welfare subject to technical constraints). In this dissertation we

assume that all the traded energy takes place in the day-ahead market.

• Physical electricity product. Different products can be traded in the

electricity market, some of them require physical delivery and others do

not (financial products). We have assumed a single product (electricity)

1.2. Motivation, Aims and Solution Approach 9

which is traded in a centrally-dispatched energy market with physical

delivery.

• Marginalist theory. The market price formation is calculated based on

the marginalist theory using the Lagrange multipliers associated to the

demand balance equation per node. We have used two approaches for

the calculation of market prices: i) Single-node price or MCP (Marginal

Clearing Price), where the network is disregarded and the power balance

is constrained for the whole system; ii) Multi-node price or LMP (Lo-

cational Marginal Price), when the network is considered and the power

balance equation must hold at each node. The marginal values for the

balance equation determine the LMPs for each node, which are the prices

for trading the energy in such nodes.

• Oligopolistic vs. perfect competition. The oligopolistic market

assumption is widely used in the literature where the participants can

influence the results of the market according to their behavior. Most of

the times oligopolistic competition implies imperfect competition. Exam-

ples of oligopolistic competition are Cournot, Bertrand or SFE (supply

function equilibrium) models. Perfect competition models assume that

market participants optimize their profits without influencing the results

of the market outcomes.

We assume oligopolistic competition in Chapter 3, but perfect competi-

tion is assumed in Chapter 4.

• DC network representation. The network representation has been

made disregarding line losses. The DC representation gives a linear

approach to the Kirchhoff’s laws in power systems. Equivalent linear

representations for the network have been developed for that, such as

distribution factors. We have used power transfer distribution factors

(PTDF) throughout the text for the network representation [9].

• Finite and non-cooperative Nash games with perfect informa-

tion. The models proposed are based on a game theory framework

and they are formulated as non-cooperative games, where the players do

10 1. Introduction

not cooperate. The space of the strategies for the players is discrete,

therefore, the game is classified as finite Nash game. Perfect information

is assumed, meaning that each player knows their utility function, the

available strategies, and the sets of constraints of the competitors.

1.3 Literature Review

This section reviews the technical literature related to the topics addressed in

this dissertation.

1.3.1 Equilibrium Models under Restructured Environ-

ments

In 1950 John F. Nash provided the mathematical framework for finding the

equilibrium in an n-person game, named Nash equilibrium [10] after him.

Hundreds of publications have appeared for developing new concepts of equi-

librium, new algorithms for their resolution and new applications in almost all

areas of knowledge. Game Theory has flourished as a new branch of knowledge.

Game theory captures the strategic behavior of the individual players, where

an individual player decision depends on the choice of the other players [11].

The application of game theory to power systems has answered new ques-

tions that have arisen after the deregulation process. Searching for possible

market equilibria is a desirable objective both for market participants and

market regulators. For participants, because an equilibrium shows the strate-

gies of their rivals; for market regulators, because market power monitoring

and corrective measures are possible. The knowledge of equilibria represents

a valuable tool for electric companies to implement their strategies.

Due to the oligopolistic nature of power systems, electricity markets do not

show perfect competition and equilibrium models are desirable for analyzing

market results and the participants’ behavior. Oligopolistic competition means

that market participants are able to affect the results of the market.

When the participants make decisions simultaneously (one-shot game) the

1.3. Literature Review 11

market equilibrium can be classified as:

• Cournot equilibrium. It is one of the major techniques used by the

researchers to study the market and the participants’ behavior [12, 13].

In the Cournot equilibrium the participants choose the output quantities

to submit to the electricity market maximizing their individual profits

and assuming the competitors do not change their outputs as a function

of their other competitors’ decisions.

In [12] two Cournot models are formulated as mixed linear complemen-

tary problems including a DC network representation. The first one

is proposed for bilateral contracts and the second one for a pool-based

market. Reference [13] proposes another model similar to [12]. They

search for the equilibrium using a relaxation algorithm based on the

Nikaido-Isoda function instead of the KKT conditions used in [12].

• Bertrand equilibrium. The participants use prices as strategic vari-

ables instead of quantities. When there are no capacity or transmission

constraints and there is a unique good, this model is equivalent to perfect

competition [14]. This model is not widely applied to electricity markets

and there are not many applications.

For example, in [15] they develop a linear model for finding the electricity

market equilibrium based on price competition. In another work [16],

Bertrand equilibrium results are compared with other equilibria, where

the Nash equilibrium is formulated for a three-player game in mixed

strategies for Cournot and Bertrand games.

• Supply function equilibrium (SFE). In this approach the partici-

pants submit their bids in both price and quantity. Each participant

needs to decide their whole supply curve for different prices and for

different quantities. It provides a good model but is hard to compute

for large power systems. SFE outcomes are similar to the Cournot

equilibrium at peak demands, when generation almost reaches its upper

limit, and close to the Bertrand equilibrium at off-peak demands, when

the capacity is significantly higher than the demand [17].

12 1. Introduction

Linear [18–22], piece-wise [23] and step-wise supply function [24–27]

models have been extensively applied for finding equilibria in electricity

markets.

Note that the participants maximize their profits independently assuming

that the competitors do not change their outputs as a function of the other

competitors’ decisions. Otherwise, each participant conjectures about the

competitors’ reactions using their belief or expectation of how their rivals will

react to the change of their output. The above equilibrium approaches are

sometimes merged with the term conjectural variation (CV) equilibrium

[28]. CV in Cournot decisions is applied in [29] for the GENCOs’ bidding

problem in the day-ahead market. Conjectured SFE is applied in [20] where

producers choose their supply functions for modeling how rival firms will adjust

their sales in response to price changes.

When the participants make decisions at different stages (sequential game)

the market equilibrium can be classified as:

• Stackelberg equilibrium. The fundamental Stackelberg equilibrium

consists of a single-leader-single-follower game where a participant called

the leader decides prior to the decisions of the other market partici-

pant called the follower. The leader maximizes their profits taking into

account the best response of the follower. The decision of the leader

affects the decision of the follower and vice versa. Thus, the leader takes

advantage of being the first to make a decision.

Stackelberg games are appropriately modeled by bilevel programming

and both terms have been alternatively used to refer to the same type

of game interaction. Examples of applications to power systems include:

the strategic bidding problem [21], the generation capacity investment

problem [30], and the analysis of the vulnerability of power systems under

deliberate attacks [31].

• Multi-Leader-Multi-Follower equilibrium. This is a generalized

version of the two-level or bilevel games. In fact, the Stackelberg equi-

librium is a particular case of a multi-leader-multi-follower equilibrium.

1.3. Literature Review 13

In the latter, there is more than one leader that decides in the first stage

subject to the optimal reactions of several followers and the other leader’s

decisions. After the leaders make their decisions, the followers also make

their own decisions maximizing their profits taking into account the other

followers’ decisions. At both levels a Nash game is formed.

Sometimes, these games are called Stackelberg-Nash games [32, 33] for

a single-leader-multi-follower case. These games can be appropriately

modeled as MPECs or MPCCs.

For the case of a multi-leader-multi-follower equilibrium, EPEC opti-

mization models are good for representing the interaction between the

participants [34–36]. But in general they are hard to solve and very

difficult to compute for large problems. In Chapter 2 we develop a

framework for solving a special case of stochastic multi-leader-multi-

follower equilibrium.

• Generalized hierarchical equilibrium. It is a generalized version of

the multi-leader-multi-follower equilibrium where there are more than

two stages. The requirement is that decisions are made in a sequential

manner. This means that participants who act later in the game have

additional information about the actions of other participants or states

of the world. This also means that participants who act first can often

influence the game.

At each stage we can have a single participant or multiple participants

forming an equilibrium. The decisions of each stage are optimized ac-

cording to the participants’ best response at later stages, where these

decisions affect the later stages as well.

These models are less common in literature due to the difficulty in solving

them. In general they are well represented by hierarchical optimization

models. As an example, [8] presents a three-stage model. In the first

stage a transmission network planner decides the optimal line expansion

subject to generation expansion (at the second stage) and the market

outcomes (at the third stage). At the second stage the problem is

14 1. Introduction

stated as an EPEC where multiple GENCOs optimize their capacity

expansions subject to the market equilibrium outcomes at the third stage.

In Chapter 4 we solve an improved version of this model.

Some authors have used the Cournot, Bertrand or supply function equi-

librium terms to describe hierarchical games with more accuracy. Hence,

we can find terms such as Stackelberg-Nash-Cournot equilibrium [32, 33] to

describe a Stackelberg game where decisions are made only for quantities, or

Nash-Cournot equilibrium [12, 13, 37] for solving multi-leader-multi-follower

equilibrium with Cournot decisions.

1.3.2 Operational Framework: The Strategic Bidding

Problem

Pool-based markets are effective frameworks for trading electricity. The strate-

gic bidding problem has become a recurrent problem in literature, providing

several solutions for choosing the best offer curve to bid to the ISO. In the

strategic bidding problem, a GENCO maximizes their profit for selling energy

in a pool-based market competing with other GENCOs. The ISO aggregates

the offers and bids provided by the producers and consumers, respectively,

creating the hourly offer and demand curves, respectively. Once the bids and

offers are submitted, a market clearing algorithm matches the production and

demand curves producing a series of hourly prices and accepted quantities

[3, 38,39].

SFE models have been applied since their introduction by the seminal

paper from Klemperer and Meyer [40]. One of the first applications of SFE

models is applied to the British spot market [41]. In subsequent studies,

[23,42], uncertainty is considered in their approaches [43]. The Nash-Cournot

concept has been applied to calculate equilibria in multi-period settings either

by iterative simulation [37], or by mathematical optimization methods [19].

Finding Nash equilibria by simulation is also possible combining mathematical

optimization and game theory, several works have applied game theory models

and/or agent-based models in electricity market simulators [44,45].

1.3. Literature Review 15

In this dissertation we use a stepwise supply function for finding the equi-

librium in a pool-based market in Chapter 3. Related works to this dissertation

are: [24,46,47], where only one GENCO faces the problem of optimizing their

profits bidding to the ISO, and [25,26], where several GENCOs optimize their

bidding strategies.

When a single GENCO optimizes their offer bidding curve [24, 46, 47]

propose a bilevel model where a GENCO decides the optimal supply function

to bid in quantities and prices at the upper level [24,46] or only in prices [47].

The ISO is represented at the lower-level problem. The bilevel problem is

reformulated as a single-level problem within an MPEC optimization problem.

To avoid local solutions the three works linearize the problem using techniques

such as duality theory or discretizing some variables [48]. [24,46] uses a binary

expansion approach to discretize the quantity and price to bid. However, since

quantity offers are not decided in the optimization process by the leader, an

exact linear reformulation can be used without any discretization [47]. The

three models are finally stated as MILP optimization problems. In [24, 47]

stochastically-obtained scenarios are considered.

When several GENCOs solve the same bilevel problem or the equivalent

single-level problem at the same time, the problem can be reformulated as

an MPEC optimization problem resulting in an equilibrium problem with

equilibrium constraints (EPEC). An extension of the work in [46] to several

GENCOs is presented in [25] for finding the Nash equilibrium with strategic

bidding in short-term electricity markets. The binary expansion approach that

we use is similar to the single GENCO problem, and an equivalent MILP is

proposed to solve the equilibrium. Reference [47] is extended to equilibrium

analysis [26]. The strong stationarity conditions for all MPECs conform a

set of constraints that can be stated as an EPEC. Linearization techniques

are applied to reformulate the problem as a MILP. The solutions for such a

model identify stationary points that can be Nash equilibria, local equilibria,

or saddle points.

16 1. Introduction

1.3.3 Planning Framework: Capacity Expansion Prob-

lem

With few exceptions, the primary drivers for transmission upgrades and ex-

pansions are reliability considerations and interconnection of new generation

facilities. However, because the operating and investment decisions by GEN-

COs are market-driven, the evaluation of transmission expansions must also

anticipate the impact of such investments on the market outcomes. Such

economic assessments must be carefully scrutinized since market outcomes

are influenced by a variety of factors including the network topology and

uncertainties in the time of connection to the grid of generation facilities,

among others.

Transmission systems are costly infrastructures, implying that their plan-

ning must be assertive in technical and economic terms. Accordingly, there are

many studies that propose reaching an “optimal” grid planning. They include

the use of techniques such as linear programming [49] , mixed integer linear

programming [50, 51] or Benders decomposition [52]. Other models make use

of heuristics, in particular genetic algorithms [53], simulated annealing [54].

Game theory models have been also applied [8,55–57]. Other models integrate

transmission expansion planning within a pool-based market [58], making use

of mixed integer linear programming. In the same vein, [30] formulates a bilevel

model where the transmission planner minimizes the transmission investment

costs in the upper level and the lower level is the market clearing of the

pool. The bilevel model is reformulated as a mixed-integer linear problem

using duality theory. Additionally, multi-period models have been proposed to

characterize investments in electricity markets: [59] proposes a two-stage model

of investments in generation capacity where generation investment decisions

are made in the first stage while spot market operations occur in the second

stage. Accordingly, the first-stage equilibrium problem is solved subject to

equilibrium constraints. However, this model does not take into consideration

the transmission constraints generally present in network planning problems.

Among the aforementioned methods, [8,57] are the only ones that assess the

economic impact of transmission investment while anticipating the strategic

1.3. Literature Review 17

response of oligopolistic GENCOs investing in generation and participating

in the spot market. In both [8] and [57], the authors formulate a three-

period model to study how the exercise of market power by GENCOs af-

fects the equilibrium between generation and transmission investments and

the evaluation of different transmission expansion projects. Their model is

named “proactive network planning” since the network planner may influence

generation investment and the subsequent spot market behavior. Comparisons

of this proactive model with both an ideal integrated resource network planning

model and a reactive network planning model are shown in [8]. However, this

methodology, based on an iterative process to find the equilibrium, does not

solve the optimal transmission planning, it only evaluates the social welfare

impact of some predetermined transmission expansion projects.

To avoid the problem of computing the equilibrium of generation capacity

investments subject to the equilibrium of the market operations presented in

[8], [60] uses an agent-based system and search-based optimization techniques

to solve a similar problem. In [60], the authors model each GENCO as a Q-

learning agent and use a heuristic to solve a three-stage four-level optimization

problem. In their problem, the four levels considered are: (i) GENCOs’ bidding

strategy, (ii) market clearing, (iii) GENCOs’ generation investments, and (iv)

transmission expansion.

Other authors have proposed multi-period models to characterize invest-

ments in electricity markets. Reference [59], for instance, proposes a two-

stage model of investments in generation capacity in restructured electricity

systems. Additionally, [30] proposes a bilevel model where the transmission

planner minimizes transmission investment costs in the upper level and the

lower level represents the market clearing. The bilevel model is reformulated

as a mixed integer linear problem using duality theory.

In [61] and [62], the authors describe the “Transmission Economic As-

sessment Methodology (TEAM)”, developed by the California Independent

System Operator (CAISO) and based on the “gain from trade” economic

principle. The TEAM’s model considers that transmission planning anticipates

the equilibrium of a perfectly-competitive energy market, but it ignores the po-

tential strategic response by generation investments to transmission upgrades.

18 1. Introduction

That is, the TEAM’s model assesses the economic impact of transmission

upgrades, given the current estimation of the generation capacity.

On the other hand, [63] presents an analysis of the relationship between

transmission capacity and generation competition in the context of a two-node

network. They argue that relatively small transmission investments may yield

large payoffs in terms of increased competition.

1.3.4 From Bilevel to EPEC Optimization Modeling

In this dissertation we start modeling a single agent with a bilevel model and

move towards EPEC modeling to represent the interaction between several

agents. The bilevel model is converted into a single-level problem stated as an

MPEC and the set of MPECs faced by each agent constitutes an EPEC.

Bilevel problems have interested many researchers [64]. Seminal mono-

graphs [65, 66] and state-of-the-art papers [67, 68] have been written among

hundreds of works related to bilevel programming.

Bilevel problems model the interaction between agents taking actions ac-

cording to a predefined sequence. The first author to represent this interaction

was Stackelberg [69] in his version of the duopoly equilibrium. In this context

bilevel problems have been included in the game theory framework as a tool for

modeling such interactions. A leader, represented by an optimization problem

at the upper level, optimizes their decisions taking into account the optimal

reaction of the follower. The optimal reactions of the follower constitute the

solution of the lower-level optimization problem. These models are relevant

in those situations where the actions of the follower affect the decisions of the

leader.

The oligopolistic nature of deregulated power systems is well represented

with bilevel models. Many applications of these models to power systems can

be found. For example, in [21] electricity producers maximize their profits

under the constraint that their dispatches and prices are determined by an

optimal power flow. In [31], bilevel programming is used to analyze the

vulnerability of power systems under multiple contingencies where the system

operator (upper level) reacts by minimizing the system load shed by an optimal

1.3. Literature Review 19

operation of the power system with a set of simultaneous outages in the

transmission network (lower level). Reference [70] solves the medium-term

decision-making problem faced by a power retailer, where the retailer decides

their level of involvement in the futures market and in the pool. An optimal

transmission expansion planning within a market environment is solved in [30].

At the upper level, the transmission planner minimizes the investment and

operational cost in a pool-based market, where market operation is represented

at the lower level.

In general, bilevel models are non-convex and non-differentiable optimiza-

tion problems that are intrinsically hard to solve. It has been proven that

a bilevel problem is NP-hard [66, 71]. Most of the works for solving bilevel

problems can be classified as continuous or combinatorial approaches.

For the continuous approach, the authors characterize the necessary optimal

conditions (e.g. KKT conditions) and the algorithms to converge to local

solutions. A global solution is seldom guaranteed. Descend methods [72, 73],

penalty functions [74,75] or smoothing approaches [76,77], among others, have

been adopted for solving bilevel problems.

The combinatorial approach is based on the bilevel problem formulation

as a combinatorial problem. Consequently, global optimality is guaranteed at

the expense of the tractability of the solution. Indeed, these algorithms are

limited to solve efficiently specific problems with linear, bilinear or quadratic

objectives. The main algorithms are branch-and-bound, branch-and-cut for

bilevel problems [78], or a mixed integer linear reformulation [48,79].

Mathematical Programs with Equilibrium Constraints (MPEC)

constitute a self-contained area of Operations Research closely related to bilevel

programming. In an MPEC, the decision maker optimizes an objective func-

tion subject to their own constraints and some constraints that represent the

equilibrium with (an) other agent(s). In general, the equilibrium constraints

correspond to a parametric variational inequality [80,81] or to complementarity

constraints [81, 82] under some suitable conditions. In the latter case the

MPEC is also called mathematical program with complementarity constraints

(MPCC). We refer to the monographs of [81, 83] for detailed applications of

20 1. Introduction

MPECs and MPCCs.

MPECs and MPCCs are close to bilevel programming and the reformula-

tion of bilevel problems into single-level problems leads to MPEC or MPCC.

However, bilevel programming is not always equivalent to MPEC (or MPCC)

problems, even when the lower-level problem is a parametric convex optimiza-

tion problem, as shown in [84]. MPECs and MPCCs are non-convex and

nonlinear optimization problems and NLP algorithms fail to solve such prob-

lems because the constraints’ qualification such as LICQ (linear independence

constraint qualification) and MFCQ (Mangasarian-Fromovitz constraint qual-

ification), fail in the complementarity constraints. Hence, the global optimal

solution is seldom reached.

A wide range of papers have studied this problem and they have proposed

NLP regularization [85–87], partial penalization [88] and mixed integer pro-

gramming reformulation [48], among others.

Applications of MPECs in power systems can be found in the strategic

bidding problem [19,24,46,47], where a GENCO optimizes their profits selling

energy in a pool-based market. The decisions are the stack offers to submit to

the ISO and the equilibrium constraints are the set of optimality conditions

of the ISO. In [89], an MPEC model is presented, where a GENCO bids in a

pool-based and a contract market simultaneously. The equilibrium constraints

are given by both sets of optimality conditions in the pool-based and contract

markets. For a long-term horizon, the MPEC formulation has been applied

to generation capacity expansion planning [59,90]. A GENCO optimizes their

capacity expansion within an equilibrium solution of the pool-based market.

Spot prices and energy productions are given by the equilibrium constraints.

A yearly transmission line maintenance problem is formulated as an MPEC

in [91]. A centralized transmission system operator schedules the maintenance

outages of a set of transmission lines. The equilibrium constraints represent

the clearing process of the market for all the time periods considered.

When several agents face an MPEC and they solve their problems jointly,

an Equilibrium Program with Equilibrium Constraints (EPEC) prob-

lem arises. In essence, an EPEC is a mathematical formulation for the general-

1.3. Literature Review 21

ized two-stage (two-level) multi-leader-multi-follower game [92]. Hence, there

are some players (leaders) that make decisions before other players (followers),

which involves finding equilibria at both the lower and the upper levels. The

decisions of the followers are parameters within the decision problems of the

leaders. Consequently, EPECs encompass bilevel problems as a starting point

[34] towards an EPEC representation.

Many engineering and economic applications are best modeled with EPECs.

Particulary, in deregulated power systems, EPECs have been applied for study-

ing the strategic behavior of GENCOs in [19,25,26,34,35,93] and [94–97].

In this regard, transmission constraints and market power are analyzed in

[19] under an MPEC setting. A similar model considering network constraints

uses MILP with disjunctive constraints and a linearization [79]. A bilevel

noncooperative model with locational marginal prices and transmission line

constraints is proposed in [34] as part of an EPEC, where the conditions for

the existence of Nash equilibria are examined.

EPEC problems represent a challenge nowadays because of the major com-

plications that arise from these models, namely:

• Computation of the global equilibrium. EPEC models are non-convex

and non-linear and they inherit the “bad” properties of MPECs that

constitute an EPEC. If it is difficult to find a global solution for MPECs,

thus it is much more difficult to jointly solve MPECs parameterized by

the solutions of the other MPECs. Consequently, the global solution is

seldom reached. The obtained solution may be a Nash equilibrium, a

local equilibrium or a saddle point.

Two main algorithms have been suggested in the literature for solving

EPECs: i) diagonalization approach [19,93], solving the MPECs of each

player sequentially until convergence. This approach can be further

classified into two methods, Jacobi and Gauss-Seidel method; ii) Simul-

taneous solution methods [36, 95] propose writing the strong stationary

necessary conditions for all MPECs and solving all the constraints simul-

taneously. The solution found is known as the strong stationary solution.

Furthermore, when an EPEC is solved rewriting the strong stationary

22 1. Introduction

necessary conditions, additional solutions can be formed because some

Lagrange multipliers become unbounded due to the fact that standard

constraints’ qualifications, such as LICQ or MFCQ, do not hold [98].

To solve this problem, some authors propose to use “price consistency”

[36,96] that limits some Lagrange multipliers to take common values due

to their economic meaning, or they fix some of these Lagrange multipliers

[26]. Because of the lack of a global search for these approaches, some

hybrid methods intend to find the “best” solution between different sets

of solutions found when the problem is solved with different starting

points.

• Mixed vs. pure equilibria. EPECs may not have solutions in pure strate-

gies but may have them in mixed strategies. But computing mixed

strategies constitutes a big challenge for games with more than two

players. On the other hand, mixed strategies have no straightforward

interpretation in many contexts.

• Multiple equilibria. EPECs may have multiple equilibria, but, in general,

most algorithms are only able to find just one. For example, supply

function equilibria in the strategic bidding problem has multiple solutions

because there are multiple supply functions to reach the same results.

Algorithms to compute all equilibria are not common and, in most cases,

they need to express the game in normal form and solve a polynomial

system of equations [99,100]. This involves building the game in normal

form, which may not be possible even for discrete decisions.

• Tractability. In general, EPECs show lack of tractability for solving large

problems . It is desirable to search for new and specific decomposition

techniques [101] for EPEC problems.

• Economic consistency. Most of the work about EPEC models has some

underlying assumptions such as perfect information (the players know

about the profit function or the set of strategies of the competitors)

or rationality (a player always acts in a rational way). However, these

assumptions can be argued. Furthermore, because of the mathematical

1.4. Thesis Objectives 23

properties of the EPEC models, a solution approach should pay attention

to the Lagrange multipliers used in a market environment. In addition,

when there is uncertainty, players want to manage their risks and a

new concept of equilibria under risk [102,103] appears, complicating the

economic interpretation, the solution approach, and the tractability of

the problem.

1.4 Thesis Objectives

The general objective of this thesis is to develop a mathematical framework

to find all pure Nash equilibria in bilevel games with discrete decisions and its

application to electricity markets in power systems. As general objectives we

seek for:

1. A mathematical definition of one- and two-level games and solution of

two-level finite-strategy games based on a stochastic EPEC formulation.

2. A methodology for finding all (pure) Nash equilibria in bilevel games in

finite strategies formulated as stochastic EPECs.

3. An illustration of the methodology proposed for operation and planning

problems in power systems.

The specific objectives are stated below:

1. Objectives pertaining to the operation framework: the strategic bidding

problem.

(a) Formulation of a bilevel model focusing on the strategic price and

quantity bidding variables of a GENCO in a multi-period and multi-

block framework and its reformulation as a mixed integer linear

MPEC.

(b) Formulation of a stochastic EPEC using an MILP model with un-

certainty associated with the demand.

(c) Proposal of a methodology for finding all pure Nash equilibria.

24 1. Introduction

(d) Illustrate the model proposed through case studies, considering network-

unconstrained and network-constrained models to analyze the ef-

fects of network congestion in the equilibria.

2. Objectives pertaining to the planning framework: the transmission and

generation expansion planning problem.

(a) Formulation of an MILP model that is able to solve the optimal

transmission expansion problem anticipating generation investment

and market clearing while considering demand uncertainty.

(b) Characterization of the equilibria of generation investments (which

correspond to the solution of a stochastic EPEC where the equilib-

rium constraints come from a perfectly-competitive equilibrium) as

a set of linear inequalities.

(c) Modeling approach for representing the change of the line impedances

when the lines are constructed or expanded. Implementation on a

stochastic EPEC model.

(d) Find all pure Nash equilibria for the second level and analyze the

optimistic and pessimistic solutions for the transmission planner at

the first level.

(e) Illustrate the model proposed with a 3- and 4-node case study.

(f) Application of the model to a real system (the Sistema Interconec-

tado Central -SIC-) in mainland Chile.

1.5 Thesis Organization

This thesis consists of five chapters that address both the power systems oper-

ation and planning problems in a game theory context. They are specifically

related to the mathematical modeling based on solving equilibrium problems

with equilibrium constraints (EPEC). Chapters 2–4 are fairly independent.

Because of the large number of symbols, we have repeated some of them in

different chapters. We have included a nomenclature section at the beginning

of each chapter to avoid any misunderstanding.

1.5. Thesis Organization 25

Chapter 1 introduces the thesis framework, literature review, motivation

and structure of the document. It starts with an overview of the electricity

sector describing the electricity agents, markets and transmission activity. A

motivation of our work is presented as well as the aims and solution approaches

to deal with the problems proposed in the thesis. Next, we show state-of-the-

art literature of restructured electricity markets in an equilibrium context, the

strategic bidding problem, the transmission and generation expansion planning

problem, and several mathematical tools are analyzed. Finally, the thesis

objectives are listed.

Chapter 2 presents the mathematical framework to deal with stochastic

bilevel games. In this chapter we introduce game theory definitions for one- and

two-level games. We also describe a methodology for finding all Nash equilibria

in finite-strategy games. A special case of a stochastic EPEC is presented,

where the upper-level decisions are discrete and the lower-level decisions are

continuous. Therefore, the stochastic EPEC represents a stochastic Nash game

in finite strategies with equilibrium constraints. The solution obtained is a

pure Nash equilibrium. The last section shows a methodology for solving the

stochastic finite EPEC by recasting it as an equivalent one-level inequality

system with equilibrium constraints.

Chapter 3 applies the mathematical framework presented in Chapter 2 to

solve an operational decision problem. It consists of the strategic bidding

problem, where the GENCOs submit their offers to the spot market in quantity

and price stacks, and the ISO dispatches the energy in the day-ahead market

maximizing social welfare based on the offers submitted by all GENCOs. Start-

ing with a bilevel model for a single GENCO, we reformulate the equivalent

MPEC model and, later, the stochastic EPEC model where all GENCOs face

a single MPEC at the same time. Two models are compared in this chapter:

a network-unconstrained system vs. a network-constrained system.

The chapter is mainly based on the publication by the author [27].

26 1. Introduction

Chapter 4 applies the mathematical framework proposed to transmission

and generation capacity expansion planning. First we describe a three-level

problem where a market equilibrium with perfect competition is at the lower

level. At the mid level we calculate a Nash equilibrium of the generation

capacity investment problem, where the GENCOs expand or invest in new

generating capacity based on the profits obtained at the lower level and the

generation expansions of the competitors. At the upper level, a transmission

planner optimizes the network expansion taking into account the mid- and

lower-level problems. A stochastic EPEC formulation is proposed for the mid-

and lower-level problems to recast them as MILPs. Because the EPEC does not

have an objective function, the set of equalities and inequalities from the EPEC

reformulation are used as constraints for the upper-level problem, transforming

it into an MILP problem. Next, we include the methodology to take into

account the changes in the physical properties of the network. Finally, we

show a methodology to find all (pure) Nash equilibria at the second level. An

application to realistic system based on the main Chilean power system (SIC)

is used for illustrating the methodology proposed.

The chapter is mainly based on two papers by the author [104]– [105].

Chapter 5 provides a summary of the dissertation as well as relevant con-

clusions and contributions related to the procedures proposed in this thesis.

In addition, future research work is suggested.

Additionally, this document includes two appendixes:

Appendix A provides a detailed formulation of the transmission planning

problem formulated as an MILP subject to the SEPEC and market equilibrium

constraints presented in Chapter 4.

Appendix B shows the data and a description of the main Chilean power

system (SIC) used for the simulations in Chapter 4.

Chapter 2

Mathematical Framework for

Bilevel Games

This chapter introduces and defines some basic game theory concepts. First

we provide an introduction and a general formulation of the problem. Af-

terwards we give some game theory definitions. Then, we describe one-level

games including the standard Nash equilibrium problem, the generalized Nash

equilibrium problem, and their mathematical formulations. We also introduce

a methodology for finding all pure Nash equilibria in finite-strategies Nash

games. Then we describe bilevel games formulated as EPECs, ranging from the

single-leader-single-follower game to the multi-leader-multi-follower game. At

the end of the chapter we describe the methodology for solving stochastic finite