The Year in Charts - Kem C. Gardner Policy Institute · 2019-04-29 · The Year in Charts...

20

The Year in Charts UTAH’S HOUSING MARKET 2018 By James Wood

Transcript of The Year in Charts - Kem C. Gardner Policy Institute · 2019-04-29 · The Year in Charts...

The Year in Charts U T A H ’ S H O U S I N G M A R K E T 2 0 1 8

By James Wood

C O N T E N T S

2 Residential Construction, Best Year Since 2006

3 High Density Multifamily Housing Hits Record Level

4 Condominium/Townhome Construction at All-Time High

5 Top Ranked Cities: Herriman, St. George, and Salt Lake City Are Leaders in Residential Construction

6 New Homes Affordable to Fewer Households

7 Housing Shortage Persists, but Eased in 2018

I Residential Construction

8 Sales of Existing Homes at Record Levels, 2016-2018

9 Demand for Existing Homes Outstrips Listings

10 Housing Prices Increases Accelerate

12 Affordable Cities See Largest Price Increases

13 Pace of Sales Benefits Sellers, Frustrates Buyers

14 In Second Half of 2018 Sales Slump, but Prices Firm

15 Mortgage Payment Jumps as Prices and Interest Rates Increase

16 Rising Rents Price Some Out of the Market

17 Low Vacancy Rates Persist for Fifth Year

II Residential Real Estate Market

The Year in Charts summarizes the performance of Utah’s housing market in 2018. The following 25 charts provide a record of current conditions, show long-term trends, and highlight important changes underway in the home building and real estate markets. The charts are divided into two major groups: (1) Residential Construction and (2) Residential Real Estate Sales.

By almost any measure, 2018 was another exceptional year for Utah’s home building and real estate industries. Sales of new and existing homes were brisk, apartment and condominium construction was at an all-time high, and the demand for rental units remained exceptionally strong. Builders, realtors, and landlords benefit–

ted from strong housing demand; however, for households trying to buy or rent, conditions were not so upbeat. Both home prices and rental rates increased significantly in 2018, adding to several past years of escalating prices, which produced heightened concerns about deteriorating housing affordability.

The Year in Charts: U T A H ’ S H O U S I N G M A R K E T 2 0 1 8

Ivory-Boyer Real Estate Center The Year in Charts Residential Construction 1

I Residential Construction

Residential Construction, Best Year Since 2006

The number of residential building permits issued in Utah in 2018 was the highest in 12 years and marked the eighth year of gradual increases. Home building’s recovery from the Great Recession has been long and almost leisurely. The period from 2010 to 2018 represents the slowest recovery of any Utah housing cycle dating back to the 1940s. As we shall see in later charts, this unusually slow recovery contributed to Utah’s current housing shortage. A number of factors caused the slow recovery, but none more critical than the rapidly

rising prices of new homes. High prices have affected housing preferences, shaped patterns of new residential development, and generated a move to high density housing. In 2018, solid demographic and economic growth supported increased levels of building activity, distinguished by a bubble free market, in sharp contrast to the 2004-2006 period. Forecasts suggest a modest slowdown is likely in the near future. While 2018, with 24,226 new dwelling units, may not be the peak of this cycle it is very likely within a year of the peak.

23,737

28,285

9,066

24,226

0

5,000

10,000

15,000

20,000

25,000

30,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Chart 1: Number of Residential Building Permits Issued in Utah

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

The Year in Charts Ivory-Boyer Real Estate CenterResidential Construction2

High Density Multifamily Housing Hits Record Level

Prior to 2008, single-family homes averaged 70 to 75 percent of new residential construction, but since the Great Recession their share has dropped substantially. Most recently, in 2018, only 54 percent of all new residential units were single-family homes while 46 percent were multifamily units; either condominiums, town homes, or apartment units. Building permits were

issued for 11,025 multifamily units in 2018, the highest number on record. The shift to multifamily has been most pronounced since 2014 as new home prices have forced many households to pursue more affordable multifamily housing alternatives. Consequently, over the past few years, more high density housing has been built in Utah than in any time in the state’s housing history.

Chart 2 Single-Family and Multifamily Permits as Percent of Total Building Permits Issued in Utah

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

Chart 3 Building Permits Issued for Single-Family and Multifamily Units in Utah

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

10.8%

46.1%

89.2%

53.9%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%19

91

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

Percent Multifamily Units Percent Single Family Units

9,864

11,025

20,912

8,690

12,760

0

5,000

10,000

15,000

20,000

25,000

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

Multifamily Units Single Family Units

Chart 2: Single-Family and Multifamily Permits as Percent of Total Building Permits Issued in Utah

Chart 3: Building Permits Issued for Single-Family and Multifamily Units in Utah

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

Ivory-Boyer Real Estate Center The Year in Charts Residential Construction 3

Condominium/Townhome Construction at All-Time High

The multifamily housing boom is driven by high levels of both condominium/townhome and apartment construction. What distinguishes 2018 from past years is the record number of condominium units. In 2018, permits were issued for 5,728 condominium/townhome units, an all-time high. For the first time in ten years the number of permits issued for condominium/townhome units was higher than apartment units. While the apartment boom has been underway for five years the

surge in condominium/townhome development has occurred in just the past two years. The number of condominium/townhome units increased by 89 percent, from 3,000 units in 2016 to over 5,700 units in 2018. Nearly one in four new residential units statewide was a condominium/townhome unit in 2018. The demand is expected to remain very strong for these affordable homeownership units, likely pushing the number of new condominium/townhome units above 6,000 units in 2019.

4,551

5,728

5,327

6,742

5,185

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,00019

91

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Condominium and Townhome Units Apartment Units

Chart 4: Building Permits Issued for Condominium and Townhome and Apartment Units in Utah

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

The Year in Charts Ivory-Boyer Real Estate CenterResidential Construction4

0 200 400 600 800 1000 1200

249Orem

378South Jordan

475Midvale

615Lehi

1,084Herriman

0 200 400 600 800

337Blu�dale

342Herriman

378Millcreek

604Draper

749Salt Lake City

0 500 1,000 1,500 2,000 2,500

898Draper

1,092South Jordan

1,357St. George

1,444Lehi

2,053Herriman

0 200 400 600 800 1000

604Eagle Mountain

627Herriman

659South Jordan

829Lehi

940St. George

Top Ranked Cities: Herriman, St. George, and Salt Lake City Are Leaders in Residential Construction

For the second consecutive year, Herriman led all Utah cities in residential construction activity. The city issued 2,053 residential building permits in 2018. Herriman was far and away the leader in condominium/townhome permits with a total of 1,084 units, which carried the city to the number one ranking. The leader in single-family construction in 2018 was St. George with 940 units, the sixth consecutive year St. George has held the number one spot. A fair share of St George’s single-family activity is supported by the second home market. St. George, Lehi,

and South Jordan have been locked into the top three spots in single-family construction for the past eight years. The perennial leader in apartment development is Salt Lake City, which has been the leader for five consecutive years in apartment construction. In 2018, Salt Lake City issued building permits for 749 apartment units. Of the 28,000 new apartment units developed statewide since 2014, one out of four units—6,661 units—have been located in Salt Lake City.

Chart 5: Top Five Cities by Residential Building Permits Issued, 2018

0 200 400 600 800 1000 1200

249Orem

378South Jordan

475Midvale

615Lehi

1,084Herriman

0 200 400 600 800

337Blu�dale

342Herriman

378Millcreek

604Draper

749Salt Lake City

0 500 1,000 1,500 2,000 2,500

898Draper

1,092South Jordan

1,357St. George

1,444Lehi

2,053Herriman

0 200 400 600 800 1000

604Eagle Mountain

627Herriman

659South Jordan

829Lehi

940St. George

Chart 6: Top Five Cities by Permits Issued for Single-Family Units, 2018

Chart 7: Top Five Cities by Building Permits Issued for Condominium and Townhome Units, 2018

Chart 8: Top Five Cities by Building Permits Issued for Apartment Units, 2018

Source: Ivory-Boyer Construction Database, Kem C. Gardner Policy Institute.

Ivory-Boyer Real Estate Center The Year in Charts Residential Construction 5

New Homes Affordable to Fewer Households

The median sales price of a new home in Salt Lake County in 2018 was $418,376 up 61 percent from the median price in 2010. Three other Wasatch Front counties have had similar rates of increase; in Weber County the median price is up 50 percent, in Utah County 62 percent, and in Davis County 71 percent. The rapid rise in new home costs, due primarily to higher land, labor, and material costs, has reduced the size of the potential

buyer’s market and damaged housing affordability. For example, 60 percent of the households in Davis County were able to afford the median priced new home in 2010, but that share dropped to only 42 percent by 2018. Affordability was hurt most in Weber County where the share of households able to afford the median priced home dropped from 50 percent in 2010 to 30 percent in 2018.

Source: Metrostudy and Kem C. Gardner Policy Institute.

Chart 10: Percent of Households Able to Afford Median Priced New Single-Family Home in Wasatch Front Counties

30%

40%

35%

42%

50%

59%

47%

60%

0% 10% 20% 30% 40% 50% 60% 70%

Weber County

Utah County

Salt Lake County

Davis County

$391,403

$376,942

$418,376

$402,762

$262,048

$232,522

$258,776

$235,390

$0 $50 $100 $150 $200 $250 $300 $350 $400 $450

Weber County

Utah County

Salt Lake County

Davis County

2010 2018

2010 2018

(thousands)

30%

40%

35%

42%

50%

59%

47%

60%

0% 10% 20% 30% 40% 50% 60% 70%

Weber County

Utah County

Salt Lake County

Davis County

$391,403

$376,942

$418,376

$402,762

$262,048

$232,522

$258,776

$235,390

$0 $50 $100 $150 $200 $250 $300 $350 $400 $450

Weber County

Utah County

Salt Lake County

Davis County

2010 2018

2010 2018

(thousands)

Chart 9: Median Sales Price of New Single-Family Home in Wasatch Front Counties

Source: Metrostudy.

The Year in Charts Ivory-Boyer Real Estate CenterResidential Construction6

Housing Shortage Persists, but Eased in 2018

From 1970 to 2010 the number of new housing units outnumbered the increase in households by about 12 percent. This surplus of dwelling units was absorbed by the second home market and changes in vacancy rates; however, this historic relationship was upended by the Great Recession. Since 2010, new households have outnumbered new housing units by over 40,000 households. Construction of new homes has not keep pace with household growth resulting in a housing shortage accompanied by rapidly rising home prices and rents, low vacancy rates, multiple offers on for sale

homes, and the doubling-up of households. Almost 11 percent of the population in households are relatives or nonrelatives in doubled-up situations. A total of 333,000 doubled-up persons. In 2018, the first sign of some relief for these doubled-up households emerged. The number of new housing units outnumbered new households by about 1,000 units. Although the housing shortage will persist for some time, the gap between units and households has been closing over the past few years and finally turned positive in 2018.

24,4

60

22,6

15

20,9

98

17,6

31 20,2

10 24,1

52

24,4

26

25,9

99

23,1

39

9,06

6

9,06

5

11,2

67 14,9

51 18,7

88

17,6

67 20,0

23 22,9

68

24,2

00

-15,394-13,550

-9,731

-2,680-1,422

-6,485-4,403

-3,031

1,06

0

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Increase in Households Number of New Housing Units Shortage of Units Surplus of Units

Chart 11: Utah’s Housing Shortage Measured by Annual Increase in Households and Housing Units

Source: Ivory-Boyer Construction Database and Kem C. Gardner Policy Institute.

Ivory-Boyer Real Estate Center The Year in Charts Residential Construction 7

Sales of Existing Homes at Record Levels, 2016-2018

Real estate sales statewide have been at record levels for the past three years, averaging about 45,000 sales annually. In 2018, single-family sales totaled 35,486 homes, the third highest year on record, while condominium/townhome sales hit an all-time record of 10,154 units. The strength of condominium/townhomes sales parallels the record level of construction of

condominium/townhomes discussed above. In both cases, condominium/townhome sales and new construction, are driven by buyers in search of affordable homeownership options. This buyer’s rush to “get in” has produced three exceptional years for real estate agents and brokers.

II Residential Real Estate MarketChart 12: Sales of Single-Family Homes and Condominium/Townhome Units in Utah

Source: UtahRealEstate.com

42,46945,640

34,868

35,486

7,601 10,154

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Total Closings Single Family Condominiums and Townhomes

The Year in Charts Ivory-Boyer Real Estate CenterResidential Real Estate Market8

Demand for Existing Homes Outstrips Listings

The number of residential listings statewide has steadily increased over the past six years, reaching 62,600 in 2018, the fourth highest year on record. Only the three atypical years (2006-2008) leading up to the Great Recession had more listings than 2018. The four Wasatch Front counties accounted for 80 percent of statewide listings in 2018. Realtors, almost universally, complain of a scarcity of listings, but the data show relatively high levels of listings in recent years. The difference between the data and the

anecdotes is explained by the unusually high demand for housing. The shortage of listings combined with strong demand results in a very high percentage of sold listings. Over the past four years more than 70 percent of residential listings have been sold, far above the historic average of 55 percent. In 2018, 72.9 percent of residential listings were sold statewide and in the Wasatch Front counties 74.6 percent were sold.

83,464

62,612

69,90649,636

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

State Wasatch Front Counties State Wasatch Front Counties

72.9%

74.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Chart 13: Number of Listings of Residential Units in Utah and Wasatch Front Counties(includes single-family, condominiums/townhomes)

Source: UtahRealEstate.com

Chart 14: Residential Sales as a Percent of Total Listings in Utah and Wasatch Front Counties(includes single-family, condominiums/townhomes)

Source: UtahRealEstate.com

Ivory-Boyer Real Estate Center The Year in Charts Residential Real Estate Market 9

Housing Prices Increases Accelerate

The median sales price of homes and condominiums/townhomes continued to accelerate in 2018. Price increases for single-family homes have gone from 4.3 percent in 2014 to 10.7 percent in 2018. Condominiums/townhomes have followed a similar pattern with prices accelerating from a 4.8 percent increase in 2015 to 11.9 percent in 2018. Certainly low mortgage rates have been a major factor facilitating the acceleration of housing prices, along with the state’s high rate of demographic and economic growth. These forces have combined to fuel Utah’s housing demand and higher housing prices.

By 2018, the median sales price of a home statewide was $321,000 and $235,000 for a condominium/townhome. The median home price in the Salt Lake Metropolitan Area of $341,000 ranks 23rd out of 175 metropolitan areas surveyed quarterly by the National Association of Realtors. The Salt Lake Metropolitan area ranked in the top 15 percent of all metropolitan areas in median sales price; considerable higher than some cities in neighboring states; Boise, $263,800, Phoenix $272,700, and Las Vegas $295,100.

Chart 15: Percent Increase in the Median Sales Price of a Single-Family Home in Utah

-10.0%

-15.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1.0%

3.6%

0.7%

6.2%

5.7%

9.6%

15.8

%

0.0%

-3.0

%

-6.3

%

-8.7

%

0.7%

13.6

%

6.5%

4.8%

8.2%

10.9

%

11.9

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%2.

1%

1.0%

0.6%

3.2%

11.2

%

16.3

%

13.8

%

-1.5

%

-4.5

%

-6.4

%

-8.8

%

6.2%

13.4

%

4.3% 6.

8% 8.2% 9.

4% 10.7

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

$144,400

$227,500 $182,700

$321,000

$109,900

$165,000$137,000

$235,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Single Family Condominium and Townhome

Source: UtahRealEstate.com

The Year in Charts Ivory-Boyer Real Estate CenterResidential Real Estate Market10

Chart 16: Percent Increase in the Median Sales Price of a Condominiums/Townhome Unit in Utah

-10.0%

-15.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1.0%

3.6%

0.7%

6.2%

5.7%

9.6%

15.8

%

0.0%

-3.0

%

-6.3

%

-8.7

%

0.7%

13.6

%

6.5%

4.8%

8.2%

10.9

%

11.9

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2.1%

1.0%

0.6%

3.2%

11.2

%

16.3

%

13.8

%

-1.5

%

-4.5

%

-6.4

%

-8.8

%

6.2%

13.4

%

4.3% 6.

8% 8.2% 9.

4% 10.7

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

$144,400

$227,500 $182,700

$321,000

$109,900

$165,000$137,000

$235,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Single Family Condominium and Townhome

-10.0%

-15.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1.0%

3.6%

0.7%

6.2%

5.7%

9.6%

15.8

%

0.0%

-3.0

%

-6.3

%

-8.7

%

0.7%

13.6

%

6.5%

4.8%

8.2%

10.9

%

11.9

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2.1%

1.0%

0.6%

3.2%

11.2

%

16.3

%

13.8

%

-1.5

%

-4.5

%

-6.4

%

-8.8

%

6.2%

13.4

%

4.3% 6.

8% 8.2% 9.

4% 10.7

%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

$144,400

$227,500 $182,700

$321,000

$109,900

$165,000$137,000

$235,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Single Family Condominium and Townhome

Source: UtahRealEstate.com

Chart 17: Median Sales Price for Single-Family Home and Condominium/Townhome in Utah

Ivory-Boyer Real Estate Center The Year in Charts Residential Real Estate Market 11

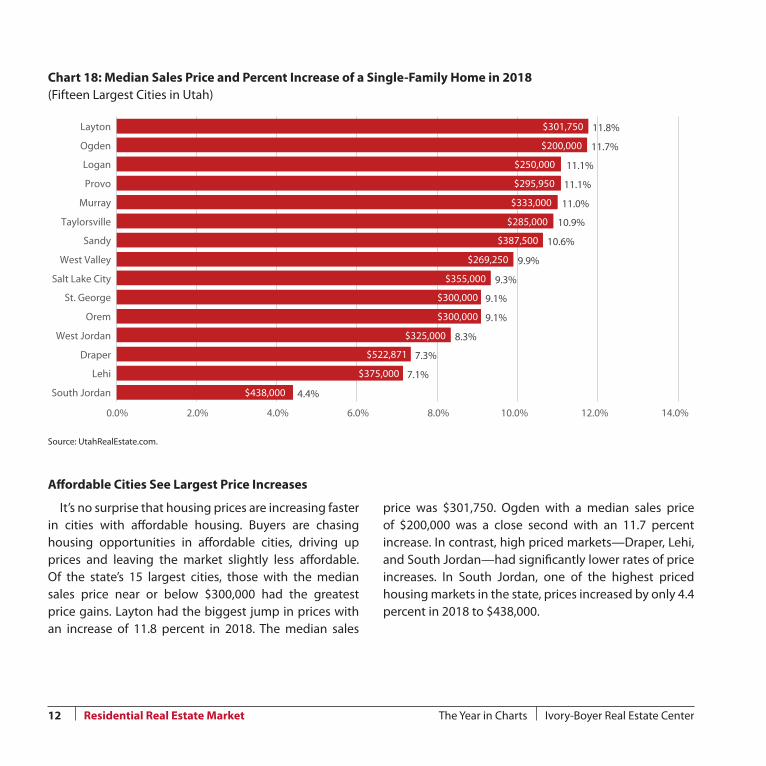

Affordable Cities See Largest Price Increases

It’s no surprise that housing prices are increasing faster in cities with affordable housing. Buyers are chasing housing opportunities in affordable cities, driving up prices and leaving the market slightly less affordable. Of the state’s 15 largest cities, those with the median sales price near or below $300,000 had the greatest price gains. Layton had the biggest jump in prices with an increase of 11.8 percent in 2018. The median sales

price was $301,750. Ogden with a median sales price of $200,000 was a close second with an 11.7 percent increase. In contrast, high priced markets—Draper, Lehi, and South Jordan—had significantly lower rates of price increases. In South Jordan, one of the highest priced housing markets in the state, prices increased by only 4.4 percent in 2018 to $438,000.

Chart 18: Median Sales Price and Percent Increase of a Single-Family Home in 2018 (Fifteen Largest Cities in Utah)

Source: UtahRealEstate.com.

$438,000

$375,000

$522,871

$325,000

$300,000

$300,000

$355,000

$269,250

$387,500

$285,000

$333,000

$295,950

$250,000

$200,000

$301,750

4.4%

7.1%

7.3%

8.3%

9.1%

9.1%

9.3%

9.9%

10.6%

10.9%

11.0%

11.1%

11.1%

11.7%

11.8%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

South Jordan

Lehi

Draper

West Jordan

Orem

St. George

Salt Lake City

West Valley

Sandy

Taylorsville

Murray

Provo

Logan

Ogden

Layton

The Year in Charts Ivory-Boyer Real Estate CenterResidential Real Estate Market12

Pace of Sales Benefits Sellers, Frustrates Buyers

In 2018, a “for sale” home typically sold within three weeks. The time span between listing and closing is known as the cumulative days on market (CDOM). The CDOM over the past 20 years has averaged 51 days,

more than twice as long as the 21 days in 2018. The CDOM’s exceptionally low level in recent years is a strong indicator of a housing shortage.

Chart 19: Cumulative Days on Market for a Single-Family Home in Utah Average CDOM is 51 days.

Source: UtahRealEstate.com.

63

69 70 70

52

40

26

41

77

83

77

83

52

34

46

28

18 20 21

0

10

20

30

40

50

60

70

80

9020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Ivory-Boyer Real Estate Center The Year in Charts Residential Real Estate Market 13

1. Why the Housing Market is Slumping Despite a Booming Economy, Neil Irwin, New York Times, November 15, 2018. Case-Shiller: Home Price Growth Continues to Lag, Alcynna Lloyd, Housing Wire, December 26, 2018.

Chart 20: Monthly Percent Change in Sales and Median Price of Single-Family Homes, Wasatch Front Counties 2018(year over change)

4.4%

13.2%

12.8%12.3%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Janu

ary

Febr

uary

Mar

ch

Apr

il

May

June July

Aug

ust

Sept

embe

r

Oct

ober

Nov

embe

r

Dec

embe

r

% change in Sales % Change in Median Sales Price

Source: UtahRealEstate.com.

The Year in Charts Ivory-Boyer Real Estate CenterResidential Real Estate Market14

In Second Half of 2018 Sales Slump, but Prices Firm

During the last half of 2018, homes sales and prices nationally softened producing headlines of a housing slump.1 To be clear, home prices at the national level didn’t decline but rather the rate of increase slowed whereas the number of homes sold did decline. How did the Wasatch Front real estate market perform in the last half of the year? A look at the monthly year-over data shows that single-family sales first registered a decline

in August with a 2.3 percent drop, which accelerated to 13.2 percent by December, thus following the national trend. Housing prices, however, didn’t show any signs of decelerating in the second half of the year. Counter to the national trend, home prices in the Wasatch Front increased at a consistent double-digit level in five of the last six months of the year.

Mortgage Payment Jumps as Prices and Interest Rates Increase

For many households, the dream of homeownership is seriously threatened by the rapid rise in home prices. The extent of that threat is shown by a simple example. In 2013, the monthly mortgage payment for the median priced home statewide was $1,167. Five years later,

that mortgage payment had increased by 56 percent to $1,821. During that same period, household income increased by only 20 percent. For many families, the possibility of homeownership is slipping away in the wake of double-digit housing price increases.

Chart 21: Mortgage Payment for the Median Priced Home in Selected Counties

$1,390

$1,798

$1,943

$2,014

$1,810

$1,821

$849

$1,124

$1,220

$1,299

$1,161

$1,167

$0 $500 $1,000 $1,500 $2,000 $2,500

Weber

Washington

Utah

Salt Lake

Davis

State

2013 2018

Source: UtahRealEstate.com and Kem C. Gardner Policy Institute.

Ivory-Boyer Real Estate Center The Year in Charts Residential Real Estate Market 15

Rising Rents Price Some Out of the Market

Renters also feel price pressure. In 2018, it took an income of $51,000 to afford the average two bedroom two bath unit in Salt Lake County. That two bedroom unit rents for $1,294, an increase of $100 in the last year. While two bedroom rents increased by eight percent renter’s income statewide increased a by only one percent. Consequently, the housing affordability crisis is even more dire for renters than homeowners. During past periods of rapidly rising housing prices, in the 1970s and 1990s, affordability was less an issue for renters.

In today’s market many households are not only priced out of the ownership market, but also the rental market. This distinguishing characteristic is likely due to the housing shortage, which was not present in past cycles. Rising rents means large numbers of renters face severe housing cost burdens. One in five renter households—nearly 60,000 renters—pay at least 50 percent of their income for housing costs. These households have the highest risk of homelessness.

Chart 22: Percent Increase in Rental Rates in Wasatch Front Counties, 2018

Chart 23: Rental Rates by Type of Unit in Wasatch Front Counties, 2018

Source: 2018 Greater Salt Lake Area Multifamily Marker Report, CBRE.

8.8% 9.1%

8.3%

7.9% 8.2%

3.3%

11.8

%

4.8%

9.3%

2.7%

6.0%

7.3%

5.6%

9.8%

5.1%

13.5

%

5.7%

16.4

%

4.5%

10.4

%0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

One Bedroom

TwoBedroomOne Bath

TwoBedroomTwo Bath

ThreeBedroomTwo Bath

Overall

Salt Lake Utah Davis Weber

One Bedroom

TwoBedroomOne Bath

TwoBedroomTwo Bath

ThreeBedroomTwo Bath

Overall

Salt Lake Utah Davis Weber

$997 $1

,056

$1,2

94 $1,4

54

$1,1

34

$975

$974

$1,2

40

$1,5

10

$1,1

22

$915 $1

,008 $1

,143

$1,3

63

$1,0

14

$806

$795

$1,1

07

$1,1

26

$878

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

The Year in Charts Ivory-Boyer Real Estate CenterResidential Real Estate Market16

Chart 24: Vacancy Rates in Wasatch Front Counties, 2007-2018*

Table 25: Vacancy Rates in Wasatch Front Counties for Selected Years

Low Vacancy Rates Persist for Fifth Year

Since 2014 low vacancy rates have defined the local rental market. For five consecutive years vacancy rates in the Wasatch Front counties have been below five percent. This is the longest period of low rates on record; a consequence of: (1) Utah’s housing shortage, (2) a modest shift in preferences from ownership to renting, (3) changing demographics, and (4) the high cost of homeownership. In 2018, vacancy rates were unchanged

in most markets with the exception of Utah County where they increased from 4.1 percent to 4.7 percent. Current vacancy rates are only a fraction of their peak levels during the Great Recession. In 2009, vacancies rates were as high as 9.0 percent in Weber County and 8.6 percent in Salt Lake County. In 2018, vacancy rate in Weber and Salt Lake counties were 2.8 percent and 3.9 percent respectively.

*vacancy rate for 2018 is mid-year estimate. Source: CBRE, 2018 First Half, Greater Salt Lake Area Multifamily Market Report.

3.9%

4.7%

3.8%

2.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Salt Lake Utah Davis Weber

8.6%

7.0%

8.0%

9.0%

3.9% 4.1%

3.6%

3.1%

3.9%

4.7%

3.8%

2.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Salt Lake Utah Davis Weber

2009 2017 2018 Mid-year

Ivory-Boyer Real Estate Center The Year in Charts Residential Real Estate Market 17

Kem C. Gardner Policy Institute I 411 East South Temple Street, Salt Lake City, Utah 84111 I 801-585-5618 I gardner.utah.edu

Partners in the Community The following individuals and entities help support the research mission of the Kem C. Gardner Policy Institute.

Legacy PartnersThe Gardner CompanyIntermountain HealthcareLarry H. & Gail Miller Family FoundationMountain America Credit UnionMitt and Ann RomneySalt Lake City CorporationSalt Lake CountyUniversity of Utah HealthUtah Governor’s Office of Economic Development

Zions Bank

Executive PartnersMark and Karen BouchardThe Boyer CompanyIvory HomesSalt Lake ChamberSorenson Impact Center

WCF Insurance

Sustaining PartnersClyde CompaniesDominion EnergyStaker Parson Companies

The Ivory-Boyer Real Estate Center partnered with the Kem C. Gardner Policy Institute to prepare this report. Both entities are located in the David Eccles School of Business. Together they seek to share data and analysis and train real estate professionals to support a vibrant housing, construction, and real estate industry in Utah. To learn more visit www.eccles.utah.edu or contact the Eccles School at 801-581-5588.

Ivory-Boyer Real Estate Center Advisory BoardDana BairdScott BatesRoger BoyerAndrew BybeePhil CookFlyn Dawson

Rocky DerrickJeff DukeFred Fairclough, Jr.Rob FetzerMarlise FisherJeff Gochnour

Clark IvoryBarb JohnsonRonda LandaBob MooreMichael MorrisShaun Nielson

Kip PaulWalt PlumbMike RoderickMichael W. SansomRick Woodbury

Kem C. Gardner Policy Institute Advisory BoardConveners

Michael O. LeavittMitt Romney

Board

Scott Anderson, Co-ChairGail Miller, Co-ChairDoug AndersonDeborah BayleCynthia A. BergRoger BoyerWilford ClydeSophia M. DiCaro

Cameron DiehlLisa EcclesSpencer P. EcclesMatt EyringKem C. GardnerChristian GardnerNatalie GochnourClark IvoryRon JibsonMike S. LeavittKimberly Gardner MartinDerek MillerAnn Millner

Sterling Nielsen Cristina OrtegaJason PerryTaylor RandallJill Remington LoveBrad RencherJosh RomneyCharles W. SorensonJames Lee SorensonVicki VarelaRuth V. WatkinsTed Wilson

Ex Officio (invited)

Governor Gary HerbertSpeaker Brad WilsonSenate President

Stuart AdamsRepresentative Brian KingSenator Karen MayneMayor of Salt Lake CountyMayor Jackie Biskupski