15 May 2011 Chris Howse Expensive Pearls: Medicolegal Session Consent.

The Year Ahead: 2016 Jill Wong

2016 Awards Who's Who Legal: Banking 2016 Legal 500 2016 IFLR 2016: Leading Lawyer Chambers Asia Pacific 2016

January 2016

What To Look Out For

Looking back – 2015

Predictions

AML

Tax evasion

Increased

creativity

Individual Accountability

Information Disclosure

Technology and Whistle

Blowers

2

Looking forward - 2016

AML

Accountability

Disclosure of Information

Regulators' increased creativity

Investor Protection

Competition

Privacy

Fight or

Flight

3

• Smart

• Quick

• Energetic

• Flexible

4

Money Laundering / Terrorist

Financing

Employee or Management knowingly causing or permitting FI to

contravene the AMLO 2 years imprisonment / Fine HK$1mn

The (new) AMLO

Contravention with intent to defraud 7 years imprisonment / Fine HK$1mn

Employee or Management causing or permitting FI to contravene the AMLO

with intent to defraud 7 years imprisonment /

Fine HK$1mn

Anti-Money Laundering & Counter-Terrorist Financing (Financial Institutions) Ordinance

Knowing contravention of AMLO provision

2 years imprisonment / Fine HK$1mn

6

AMLO Investigations?

"We found that meeting AML/CFT expectations, particularly around higher risk customers remains a challenge for some banks, while some banks have at times underestimated the effort and resources required by our AML/CFT regime."

HKMA – 4 June 2015

"Hong Kong authorities are expected to crack down harder on money laundering this year."

SCMP – 18 January 2015

7

First AMLO Case

State Bank of India • Fine HK$7.5 million • Public reprimand • Remedial plan by

Independent Advisor

28 Corporate Customers • No CDD • No identification of

intermediate layers

High risk-rated customers not periodically reviewed

AML risk ratings not updated

Did not screen out PEPs

"Copied" HKMA AML guidelines

Did not identify risky transactions • relied on 4 system

generated reports 8

AMLO Prosecutions

Money service operator convicted for contravention of

record-keeping requirements

A proprietor of a licensed money service operator was sentenced to 200

hours of community service on 18 June 2015 at the Fanling Magistrates'

Courts after pleading guilty earlier to 12 charges of failing to comply with

the customer due diligence and record-keeping requirements as stipulated

in AMLO.

The sole proprietor had failed to keep customers’ records and documents

in connection with 12 remittance transactions conducted between May

2013 and April 2014.

9

AMLO Prosecutions (2)

Money service operator convicted for contravention of

customer due diligence requirements

A proprietor of a licensed money service operator was fined $428,000 in

total on 24 June 2015 at the Kowloon City Magistrates' Courts after

pleading guilty to 22 charges of failing to comply with the customer due

diligence requirements as stipulated in AMLO.

The sole proprietor had failed to identify, verify and record the identification

of customers in connection with 22 remittance and money changing

transactions conducted between July 2013 and May 2014.

10

Section 19 Schedule 2

FI must, for each kind of

customer, business

relationship, product and

transaction establish and

maintain EFFECTIVE

PROCEDURES

Section 23 Schedule 2

FI must take ALL REASONABLE

MEASURES to –

- ensure proper safeguards to

prevent contravention

- mitigate ML/TF risks

Next cases?

11

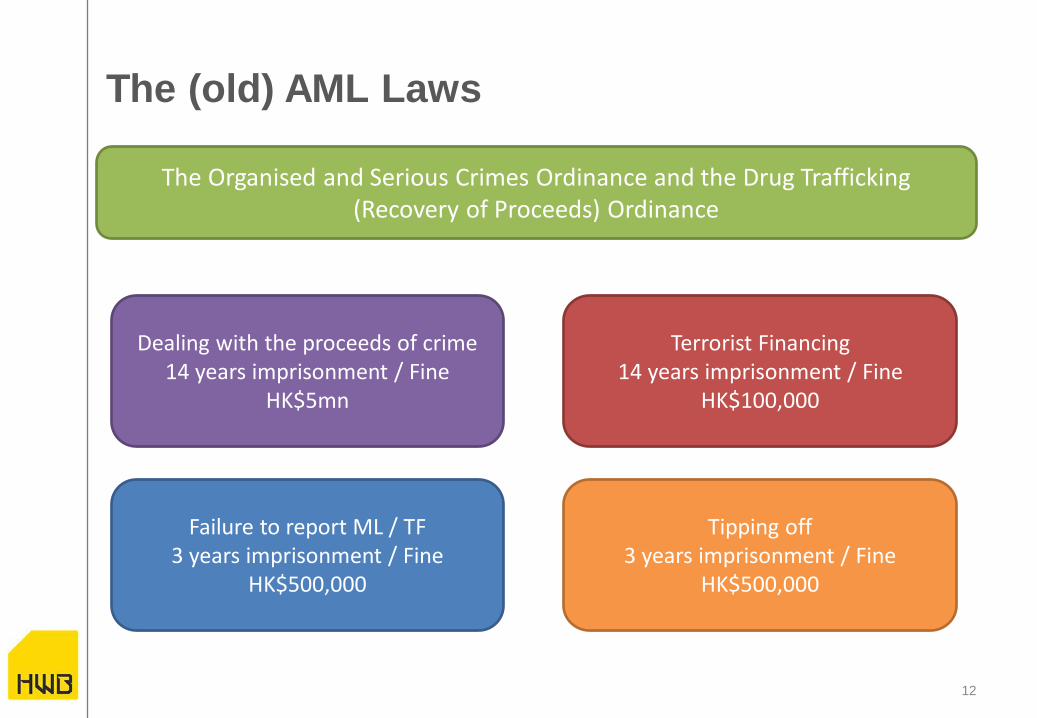

Failure to report ML / TF 3 years imprisonment / Fine

HK$500,000

The (old) AML Laws

Terrorist Financing 14 years imprisonment / Fine

HK$100,000

Tipping off 3 years imprisonment / Fine

HK$500,000

The Organised and Serious Crimes Ordinance and the Drug Trafficking (Recovery of Proceeds) Ordinance

Dealing with the proceeds of crime 14 years imprisonment / Fine

HK$5mn

12

The Bad News

US FinCEN $1mn fine Bar from financial industry - Power of FinCEN to penalise upheld in US Court (Jan 2016)

Chief Compliance Officer allegedly did not file STRs, did not take action on complaints on high risk agents, no DD on agents

US FINRA $25,000 fine One month suspension - Settlement with no admission of guilt

Global AML compliance officer allegedly did not establish AML program that could reasonably detect / report suspicious activity

Hong Kong? ? ?

13

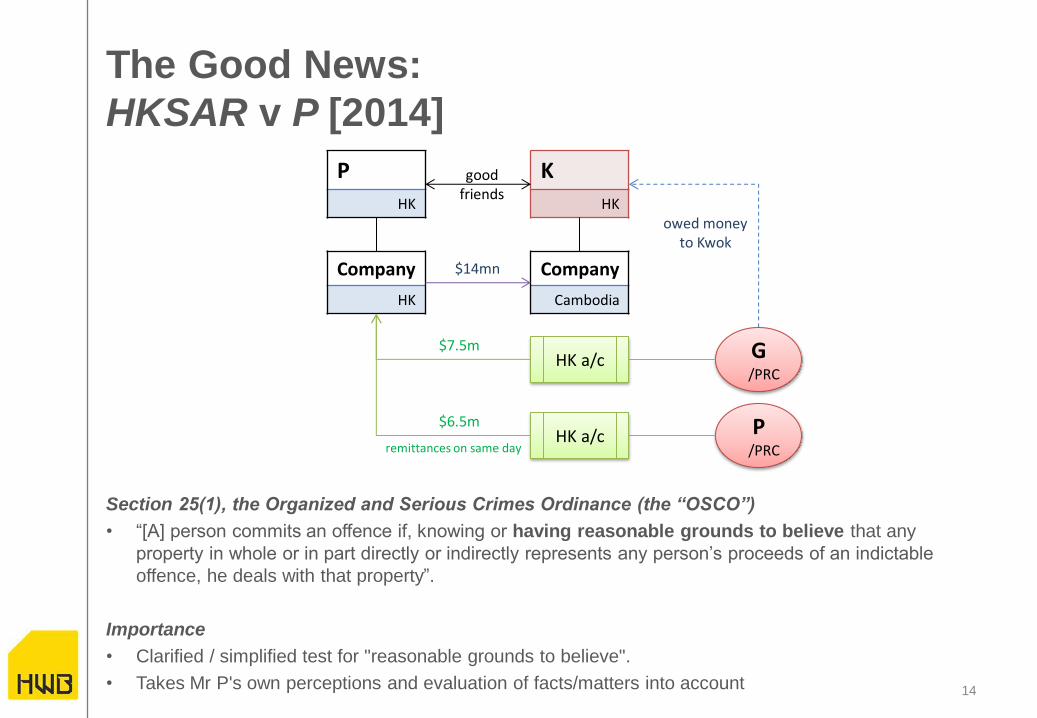

The Good News:

HKSAR v P [2014]

Section 25(1), the Organized and Serious Crimes Ordinance (the “OSCO”)

• “[A] person commits an offence if, knowing or having reasonable grounds to believe that any

property in whole or in part directly or indirectly represents any person’s proceeds of an indictable

offence, he deals with that property”.

Importance

• Clarified / simplified test for "reasonable grounds to believe".

• Takes Mr P's own perceptions and evaluation of facts/matters into account

P

HK

K

HK

Company

HK

Company

Cambodia

G /PRC

P /PRC

good friends

$14mn

owed money to Kwok

HK a/c

HK a/c

$7.5m

$6.5m

remittances on same day

14

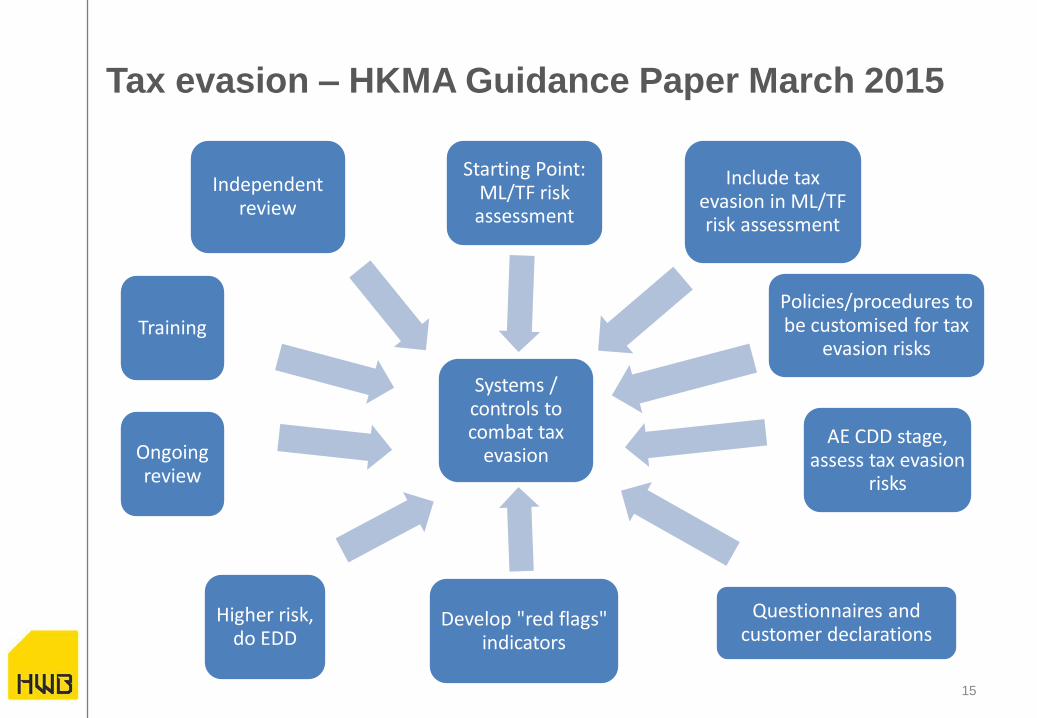

Tax evasion – HKMA Guidance Paper March 2015

Systems / controls to combat tax

evasion

Starting Point: ML/TF risk assessment

Include tax evasion in ML/TF risk assessment

Policies/procedures to be customised for tax

evasion risks

AE CDD stage, assess tax evasion

risks

Questionnaires and customer declarations

Develop "red flags" indicators

Higher risk, do EDD

Ongoing review

Training

Independent review

15

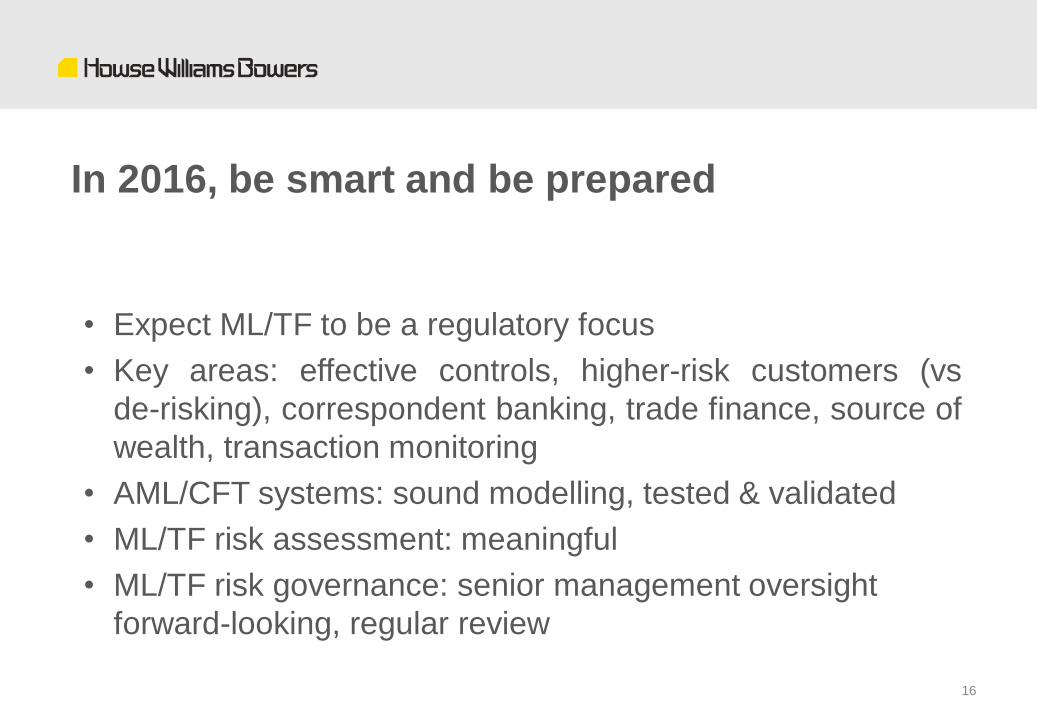

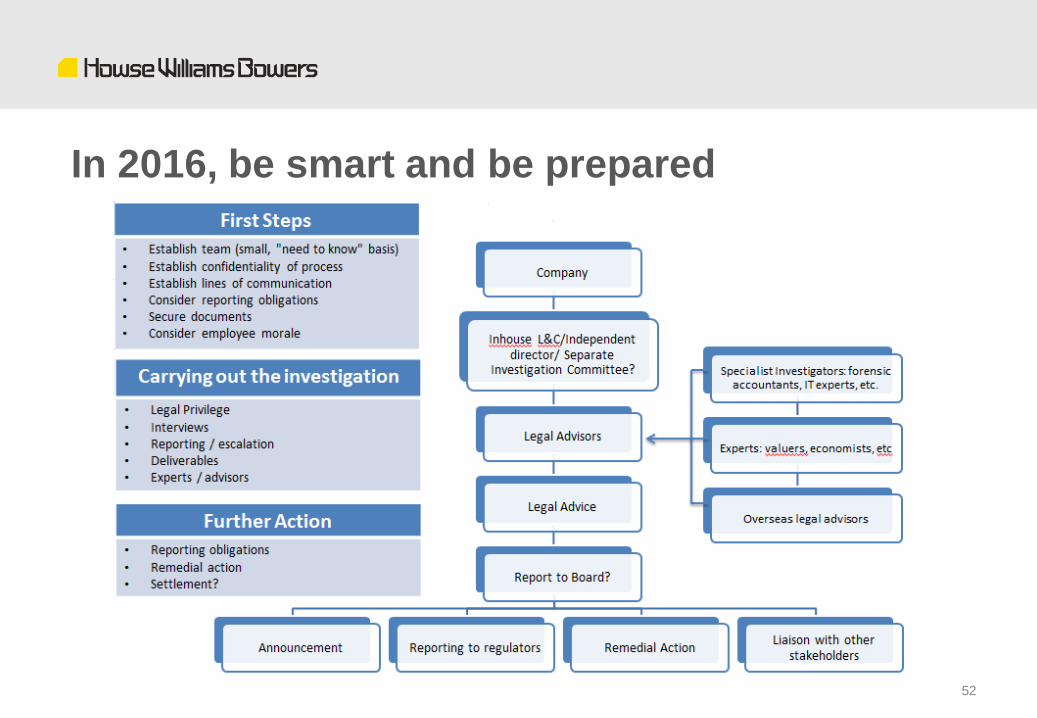

In 2016, be smart and be prepared

• Expect ML/TF to be a regulatory focus

• Key areas: effective controls, higher-risk customers (vs

de-risking), correspondent banking, trade finance, source of

wealth, transaction monitoring

• AML/CFT systems: sound modelling, tested & validated

• ML/TF risk assessment: meaningful

• ML/TF risk governance: senior management oversight

forward-looking, regular review

16

Individual Accountability

Individual accountability : a re-cap

• SFO – Responsible Officers, licensed intermediaries, officer

• BO – Executive Officers, managers

• AMLO – Employees and managers

• HK Listing Rules – Directors

And… (generally) directors

And… anyone aiding and abetting

18

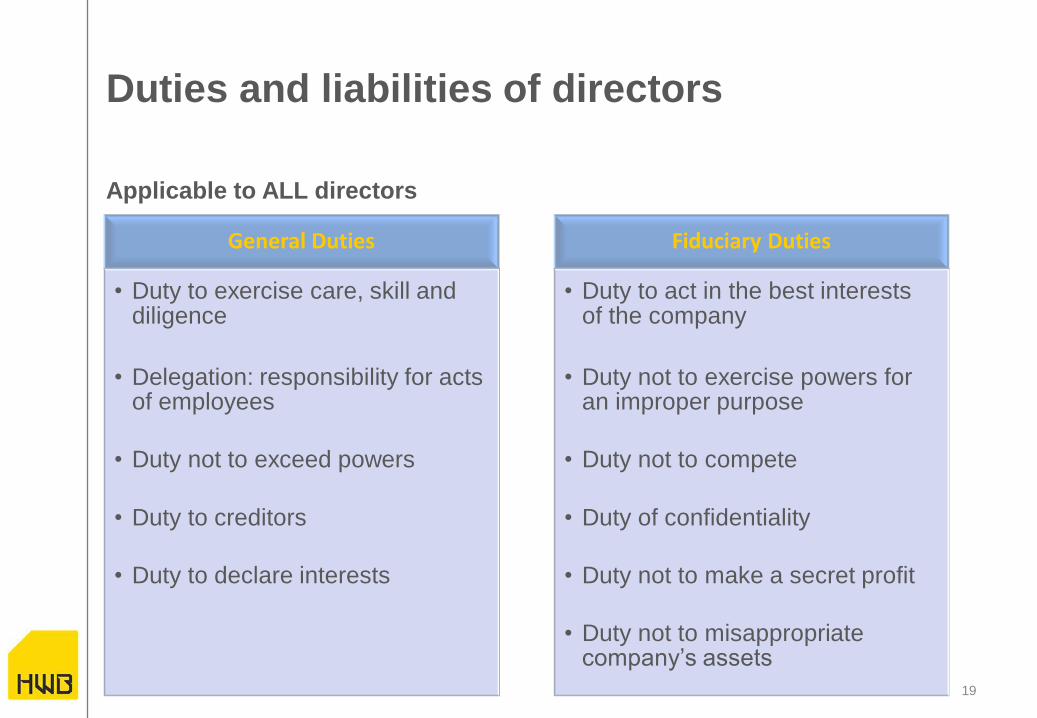

Duties and liabilities of directors

Applicable to ALL directors

General Duties

• Duty to exercise care, skill and diligence

• Delegation: responsibility for acts of employees

• Duty not to exceed powers

• Duty to creditors

• Duty to declare interests

Fiduciary Duties

• Duty to act in the best interests of the company

• Duty not to exercise powers for an improper purpose

• Duty not to compete

• Duty of confidentiality

• Duty not to make a secret profit

• Duty not to misappropriate company’s assets

19

Duties and liabilities of directors

Duties applicable to directors of listed companies

HKEx expects every director to understand and be reasonably familiar

with the obligations and duties imposed on him and the listed company

under the Listing Rules and other applicable laws and regulations

Each director must collectively and individually ensure that the

company complies with the Listing Rules

20

No delegation

HKSAR v L

Facts

• L held a securities trading account with KGI Asia Ltd

• L bought and sold shares in Victory Group Limited through KGI in 2 separate

transactions which were both disclosable transactions

• L gave instructions to KGI to do "what is necessary" in relation to disclosure

• Within 3 days of each transaction, L notified the SEHK but failed to notify

Victory of the transactions (duty of disclosure to both)

• L argued that he had a reasonable excuse for failing to make all the necessary

disclosures as he had delegated the duty to KGI

21

No delegation

Held

• It is incumbent on a substantial shareholder of a listed corporation to know and

understand the duty of disclosure and notification imposed by the SFO

• There is no evidence to show that L had made any effort to know and

understand his duties under the SFO

• L did not exercise due diligence in ensuring that KGI knew what the nature and

requirements of the duties were

• Simply instructing an agent to do whatever that is necessary in the agent's

mind is not a reasonable excuse

• If the task of the duty is delegated to another by the person who owes the duty,

he must make sure that it is strictly complied with for he bears the ultimate

responsibility and liability for any failure to perform the duty as described by law

22

Care & Skill

23

Director's Duties

Company Matter Consequences

Care & Skill Riverhill (2007)

Director failed to exercise skill and care in pledging $10mn of Riverhill's money to secure a loan for a third party, did not ensure the funds were recoverable on commercial terms and failed to disclose the transaction

Court order disqualifying the Director from being a director or directly/indirectly involved in the management of any listed company or its subsidiary/affiliate for 4 years

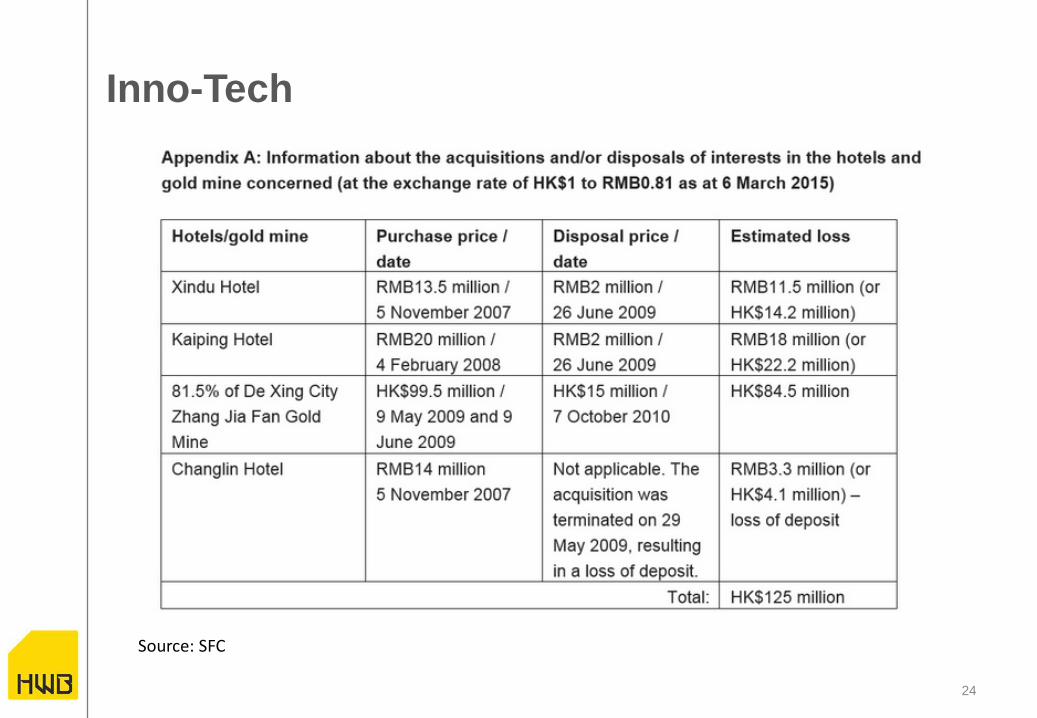

Inno-Tech (2015)

SFC alleges former Chairman/3 Directors failed to do adequate due diligence/negotiate/do proper assessments of certain acquisitions/disposals of assets, resulting in substantial losses to Inno-Tech

Seeking court orders (1) to disqualify Directors (2) that Inno-Tech sue Chairman and Directors for compensation or that they pay compensation to Inno-Tech directly

23

Inno-Tech

24

Source: SFC

25

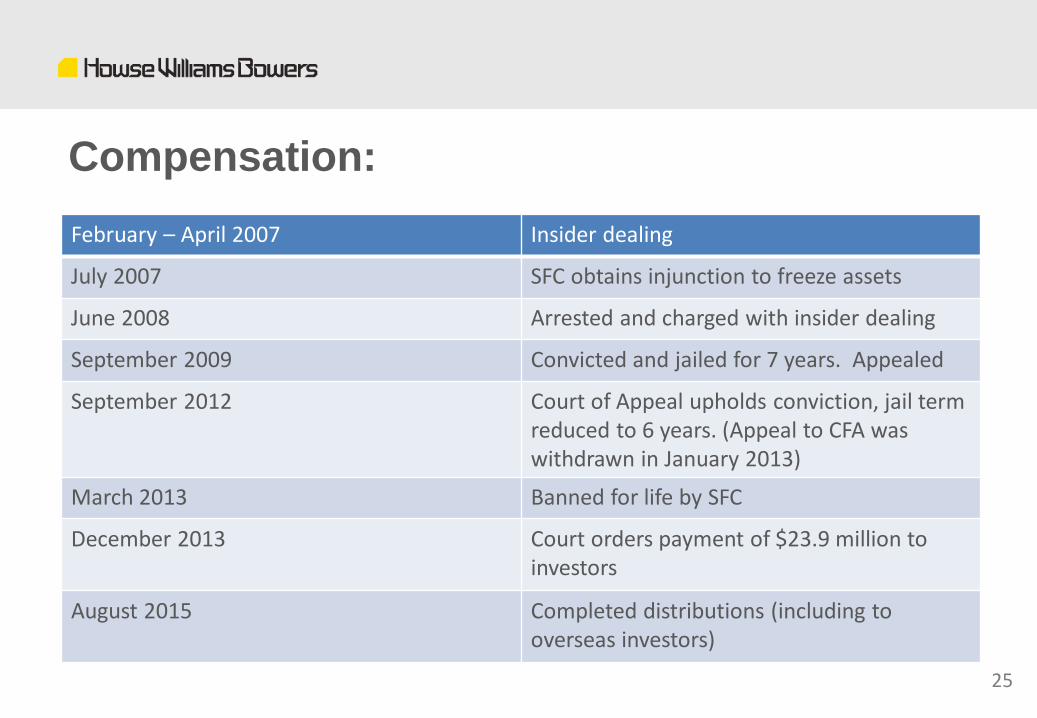

Compensation:

February – April 2007 Insider dealing

July 2007 SFC obtains injunction to freeze assets

June 2008 Arrested and charged with insider dealing

September 2009 Convicted and jailed for 7 years. Appealed

September 2012 Court of Appeal upholds conviction, jail term reduced to 6 years. (Appeal to CFA was withdrawn in January 2013)

March 2013 Banned for life by SFC

December 2013 Court orders payment of $23.9 million to investors

August 2015 Completed distributions (including to overseas investors)

Revocation of licence

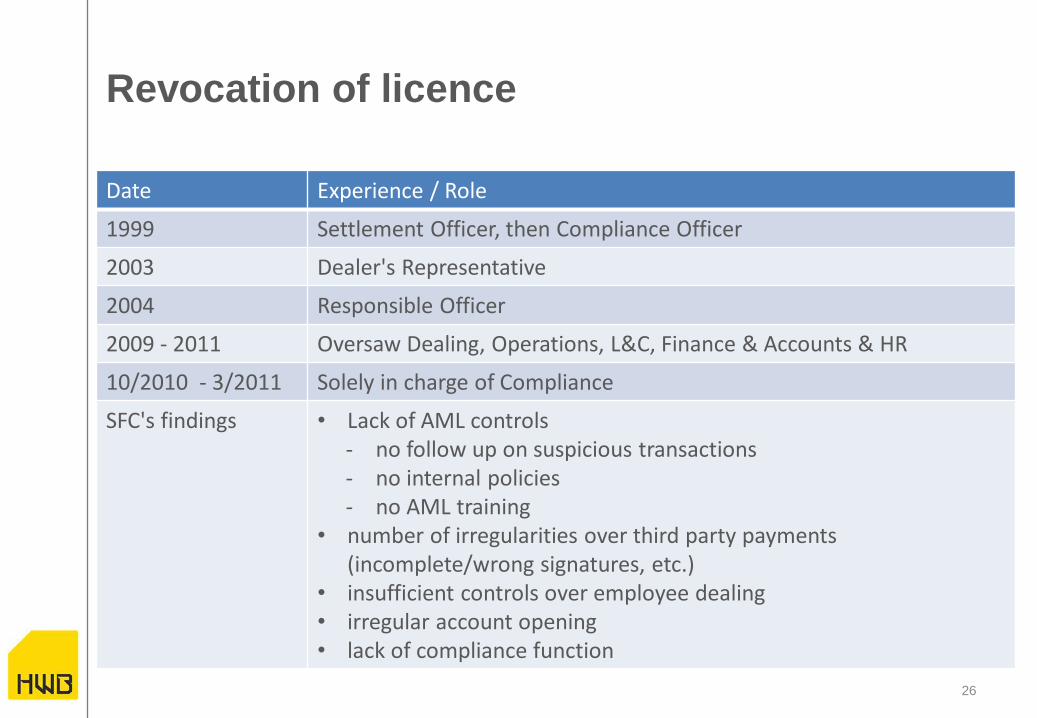

Date Experience / Role

1999 Settlement Officer, then Compliance Officer

2003 Dealer's Representative

2004 Responsible Officer

2009 - 2011 Oversaw Dealing, Operations, L&C, Finance & Accounts & HR

10/2010 - 3/2011 Solely in charge of Compliance

SFC's findings • Lack of AML controls - no follow up on suspicious transactions - no internal policies - no AML training

• number of irregularities over third party payments (incomplete/wrong signatures, etc.)

• insufficient controls over employee dealing • irregular account opening • lack of compliance function

26

In 2016, be smart and be prepared

• Expect individuals to continue to be held accountable

• Focus on compensation, challenges of commercial

decisions, scrutiny of key control functions

• Check insurance cover, organisation charts, job duties

27

Disclosure of Information

29

Disclosure of Inside Information • Part XIVA of the SFO

• Listed corporation must disclose to the public as soon as reasonably practicable after any "inside information" has come to its knowledge.

• A listed corporation will be regarded as having knowledge of inside information if:

1. information has come to the knowledge of any of its officers (including director, manager or secretary of, or any person involving in the management of the corporation) in the course of performance of his/her duties; and

2. a reasonable person acting as an officer of a listed corporation would consider that the information is inside information in relation to the corporation.

• "Inside information" means any specific information about: (i) the listed corporation; (ii) a shareholder or officer of the listed corporation; or (iii) the listed securities of the listed corporation or their derivatives, which is not generally known to the persons who are accustomed or would be likely to deal in the listed securities of the corporation, but which would, if it were generally known to them, be likely to materially affect the price of the listed securities.

Part 14A SFO:

Disclosure of Price Sensitive Information

Date Event 20 December 2012 First Media filed "Petition for Suspension of Obligation for Payment of Debts"

against AcrossAsia, on the basis that AcrossAsia could not continue paying its debts

26 December 2012

Petition registered with the Indonesian courts

28 December 2012

Summons issued by Indonesian courts requiring AcrossAsia to appear in court on 4 January 2013

2 January 2013

AcrossAsia receives petition and summons in Indonesian Bahasa

4 January 2013 AcrossAsia receives English translation of petition and summons

8 - 15 January 2013

Hearing in Jakarta

15 January 2013

Indonesian courts grant orders sought by the petition

17 January 2013

AcrossAsia issues announcement on Hong Kong Exchange

30

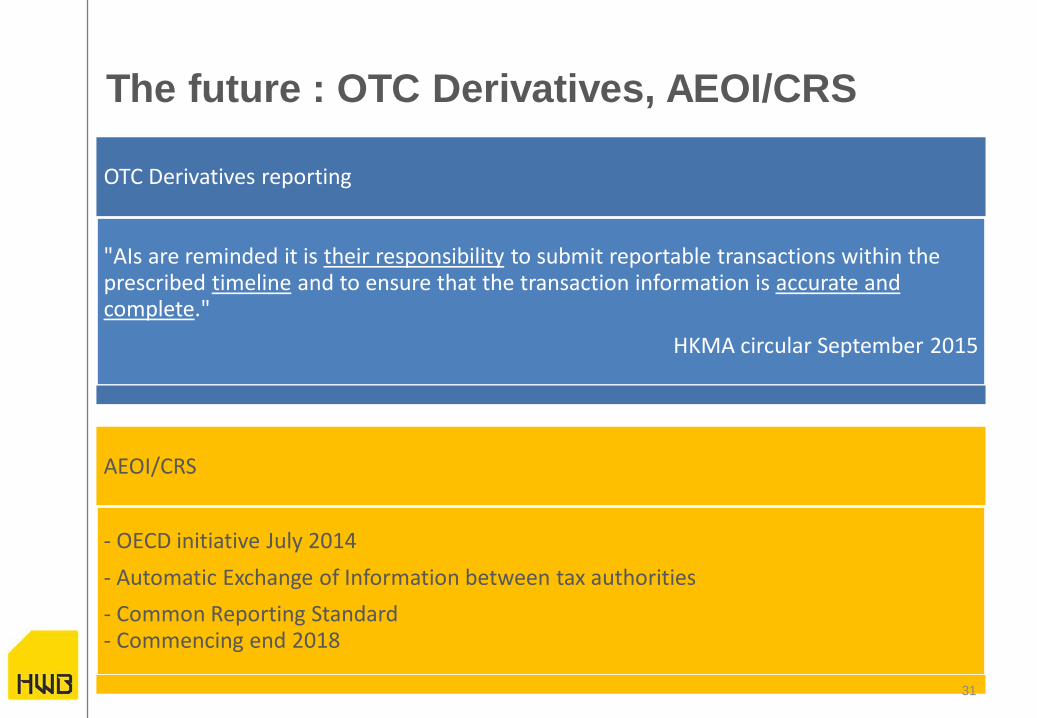

The future : OTC Derivatives, AEOI/CRS

OTC Derivatives reporting

"AIs are reminded it is their responsibility to submit reportable transactions within the prescribed timeline and to ensure that the transaction information is accurate and complete."

HKMA circular September 2015

AEOI/CRS

- OECD initiative July 2014

- Automatic Exchange of Information between tax authorities

- Common Reporting Standard - Commencing end 2018

31

In 2016, be smart and be prepared

• More disclosure between regulators

• More disclosure between jurisdictions

• More Part 14A cases

• Exercise care in reports / returns / applications to regulators

32

Increased creativity

34

Section 213 Where a person has contravened any provisions of the SFO or it appears to the

Commission that such matter has occurred, is occurring or may occur, the Court of

First Instance at the application of the SFC may make certain orders –

• restraining or prohibiting the misconduct

• restraining or prohibiting a person from dealing in property, or appointing an

administrator to a person's property

• requiring steps to restore parties to the position they were in

• directing a person to do or refrain from doing an act

• declaring a contract to be void or voidable

• requiring payment of damages

And…any ancillary order the court considers necessary

35

• Discrepancies in financial information

• SFC applied for court order under section

213

• H acknowledged it was "reckless in allowing

materially false and misleading information

to be included in its prospectus"

• On this basis, the SFC obtained an order

requiring H to repurchase shares –

repurchase completed October 2012

• No determination of a contravention under

sections 298, 300 or 384 SFO

HONTEX SFC

• Assets (just under HK$1bn) frozen under s.213 application

• s298 : provision of false or misleading information inducing investors to purchase shares in its IPO

• s300 : a fraudulent and deceptive scheme

• s384 : false or misleading information to HKEx/SFC

• s342F CO : Untrue statements in prospectus

• Sponsor investigated and fined HK$42mn; licence revoked

36

TIGER ASIA • Short selling by TA, a New York hedge fund, of HK listed shares based on inside

information; SFC applied for court orders (injunctions, etc.)

• No MMT or court proceedings commenced

Landmark Decision:

In May 2013, Court of Final Appeal confirmed section 213 is a free standing remedy, meant to augment the SFC's ability to protect the investing public.

Section 213 may be used without the need for proceedings before the Market Misconduct Tribunal or relevant criminal court

Legislation intended remedial and preventative orders to be available separately from criminal or deterrent sanctions

T A argued : need pre-

existing MMT or criminal court finding of contravention

37

More section 213 cases 10 November 2015

• The Court of First Instance granted various interim orders against Maxim Capital Limited (Maxim Capital), an unlicensed investment firm, including freezing all its monies in Hong Kong totalling approximately $23.5 million following legal proceedings brought by the SFC under section 213

• The SFC alleges that Maxim Capital and Maxim Trader contravened the SFO by carrying on a business in SFC regulated activities in Hong Kong without an SFC licence and issuing related advertisements.

• On 27 October 2015, the SFC commenced proceedings under section 213 seeking various final orders against Maxim Capital and Maxim Trader, including injunctive relief and restitutionary orders requiring them to restore the affected investors to their pre-transaction positions. Pending the substantive determination of the SFC’s claims, the SFC also applied on the same day for various interlocutory injunction orders.

• The SFC has identified approximately $23.5 million held in an account maintained by Maxim Capital with a licensed money service operator in Hong Kong. Those funds are now frozen under the terms of the interim injunction order. This order will remain in force until the trial of these proceedings, the date of which has yet to be fixed.

38

More section 213 cases

15 January 2016

• The SFC obtained interim injunctions in the Court of First Instance under section 213 freezing approximately $600,000 in bank accounts suspected of receiving monies from investors of alleged fraudulent activities known as boiler rooms

• The Court has also granted the SFC’s application for interim orders to restrain the following entities from holding themselves out as carrying on regulated activities whilst unlicensed and suspending their websites:

Waldmann Asset Management (Waldmann)

Doyle Hutton Associates (Doyle)

Cardell Limited and/or Cardell Company Limited (Cardell)

• The interim orders will remain in force until the hearing of the SFC’s application for final orders against all the parties, the date of which has yet to be fixed

• The SFC is seeking final orders against Waldmann, Doyle and Cardell including permanent injunctions and other orders to provide relief to any victims

(Almost) new : section 300

Use of fraudulent or deceptive schemes in

transactions involving securities

Fraud/deception under section 300 Insider dealing

Boyfriend

Girlfriend

Boyfriend's sisters

Knew About

Tender offer for Hsinchu

Bank (Taiwan Listco)

Boyfriend

Girlfriend

His sisters

Knew About

Privatisation for Asia Satellite

(Hong Kong Listco)

39

Told Told

In 2016, be smart and be prepared

• More use of section 213 and 300

• Focus on remedial action / investor protection / directors &

substantial shareholders

40

Investor Protection

Suitability

• JS Cresvale Securities (JCS) was reprimanded and fined HK$2.5 million by the SFC over deficiencies

in its systems & controls in the sale of two unlisted investment products involving US$99 million

between 2008 and 2010.

• The SFC found that JCS:

☒ did not conduct any product due diligence or risk assessment on the products;

☒ did not have complete risk profiles of its clients as no steps were taken to assess the

clients’ risk tolerance levels;

☒ had no systems and controls to guide its representatives to conduct proper suitability

assessment when selling the products; and

☒ did not maintain documentary records of the investment advice or recommendations

given to its clients nor provide clients with a copy of the written advice.

• In determining the penalty, the SFC took into account that:

☑ JCS co-operated in resolving the disciplinary proceedings;

☑ it agreed to conduct an independent review of its systems and controls for distribution of

unlisted investment products and to enhance its complaint handling procedures; and

☑ there is no evidence of client loss suffered from its distribution of the two unlisted

products.

42

Suitability

L v Standard Chartered International (USA) Limited

HCA 498/2010

Facts of the case

• L sued to recover his losses from investing in a Madoff fund, introduced to him by SCB

• Fund was presented as a low-risk investment with consistent historic returns and low volatility

• Fund was consistent with L’s risk profile and investment objectives

• Fund was a Ponzi scheme, L lost his whole investment

• L sued SCB for (1) misrepresentation and (2) breach of duty of care

• L also relied on section 108 SFO : SCB liable to pay compensation for fraudulent/reckless/negligent misrepresentation inducing the investment

The good news (for banks)

Ultimately, SCB successfully defended itself -

• DD conducted with reasonable care and skill

• reasonable grounds to believe that representations made to L were true

• not negligent in failing to discover Ponzi scheme

• no breach of duty of care

43

Suitability (2)

L v Standard Chartered International (USA) Limited

HCA 498/2010

The not-so-good news (for banks)

• Fund fact sheets were adopted by SCB and were also SCB's representations to L

• Springwell and San-Hot cases not applicable – fact specific

• SCB could not rely on “protective” terms in Risk Disclosure – not applicable to this

investment

• Certain Risk Disclosure terms were exemption clauses and did not meet

"reasonableness" test in Control of Exemption Clauses/Misrepresentation Ordinance

(however, they were not "unconscionable")

• section 108 of SFO did apply

• SCB did provide advice/recommendations – fact specific

• SCB assumed a duty of care when giving advice/recommendations

44

Suitability – soon a contractual duty

"If we [the intermediary] solicit the sale or recommend any

financial product to you [the client], the financial product must

be reasonably suitable for you having regard to your financial

situation; investment experience and investment objectives.

No other provision of this agreement or any other document

we may ask you to sign and no statement we may ask you to

make derogates from this clause."

SFC Consultation Conclusions December 2015

45

Due Diligence

• In June 2015, the SFC reprimanded and fined Phillip Securities (Hong Kong) Limited

(Phillip Securities) $1 million for failures in its sale of a fund to four clients

• The SFC's investigation revealed that Phillip Securities sold the American Pegasus Fixed

Income Fund – Series II Segregated Portfolio to the clients around August 2004,

involving transaction amount of approximately $819,000. The fund was liquidated in July

2011 and the clients have not been able to recover their investment

The SFC found that Phillip Securities failed to:

☒ conduct adequate due diligence on the fund before selling it to clients;

☒ provide adequate training and/or sufficient product information to its sales staff

to ensure they fully understand the nature of the fund, the risks involved, and

for which types of investors the fund would have been suitable; and

☒ implement sufficient measures to ensure that its sales staff had assessed the

suitability of the fund to clients, and to monitor and review the selling process.

46

Due Diligence (2)

• In November 2015, the SFC reprimanded and fined Okasan International (Asia)

Limited (Okasan) $4 million for failures in its sale of unlisted investment products

and making proper disclosure of trading profits

• The SFC's investigation found that Okasan:

☒ did not ensure adequate product due diligence had been conducted on

the products before recommending them to clients;

☒ did not ensure that recommendations and/or solicitations made to its

clients in relation to the products were suitable for and reasonable in all

the circumstances of the clients;

☒ did not maintain adequate documentary records of the investment advice

or recommendations given to its clients nor provide clients with a copy of

the written advice; and

☒ failed to make adequate disclosure to clients of the trading profits it made

from back-to-back transactions

47

In 2016, be smart and be prepared

• Suitability and product DD will remain areas of regulatory

scrutiny

• Continued use of administrative powers by regulators to

change market behaviour

48

Fight or flight?

Fight

• Pacific Sun and Mr. M were charged in 2013 with issuing unauthorized

advertisements to the public at large to subscribe for interests in a collective

investment scheme (CIS) in contravention of section 103 of the SFO

• The Court of Final Appeal (CFA) upheld an appeal by Pacific Sun and M and

both were acquitted after they argued successfully that they could rely upon an

exclusion contained in section 103(3)(k) of the SFO which applies if the

securities are or are intended to be disposed of only to professional investors

• It was not necessary for the advertisement to be expressed as being confined

to, or for, PIs

50

Flight (i.e. settle)

• SFC recently in December 2015 reprimanded and fined three JP Morgan entities a sum of $30 million for regulatory breaches and/or internal control failings

• An SFC investigation revealed that JP Morgan had failed to implement adequate systems and controls in its institutional equities business in Hong Kong to ensure compliance with the rules and regulations applicable to the following areas:

☒ short selling activities;

☒ client facilitation and principal trading business; and

☒ operation of dark liquidity pool trading services.

• Many of the failings were not identified or corrected until the SFC brought them to JP Morgan’s attention in the course of a SFC inspection

• In determining the disciplinary action, the SFC took into account that JP Morgan:

☑ co-operated with the SFC in resolving the SFC’s concerns;

☑ has taken steps to rectify the concerns raised by the SFC;

☑ agreed to engage an independent reviewer to conduct a forward-looking review of its internal controls and systems

☑ has a clean disciplinary record in relation to its regulated activities.

51

In 2016, be smart and be prepared

52

Competition Law

54

PROHIBITED CONDUCT

OBJECT OR EFFECT TEST

CONDUCT PREVENTING, RESTRICTING OR DISTORTING COMPETITION IN HONG KONG

FIRST CONDUCT RULE

RULE AGAINST ANTI-COMPETITIVE AGREEMENTS

SECOND CONDUCT RULE

RULE AGAINST ABUSE OF MARKET POWER

55

EXCLUSIONS & EXEMPTIONS

Type Applicable to First Conduct Rule

Applicable to Second Conduct Rule

Compliance with a legal requirement Yes Yes

Operation of services of general economic interest by an undertaking entrusted to do so by the Hong Kong Government

Yes Yes

Public policy grounds Yes Yes

To avoid conflict with international obligations Yes Yes

Block Exemption Yes No

Economic Efficiency exclusion – an agreement that improves production or distribution; promotes technical or economic progress with a fair share of benefits to consumers

Yes No

And the thresholds:

FCR: Agreements of Lesser Significance

SCR: Conduct of Lesser Significance

56

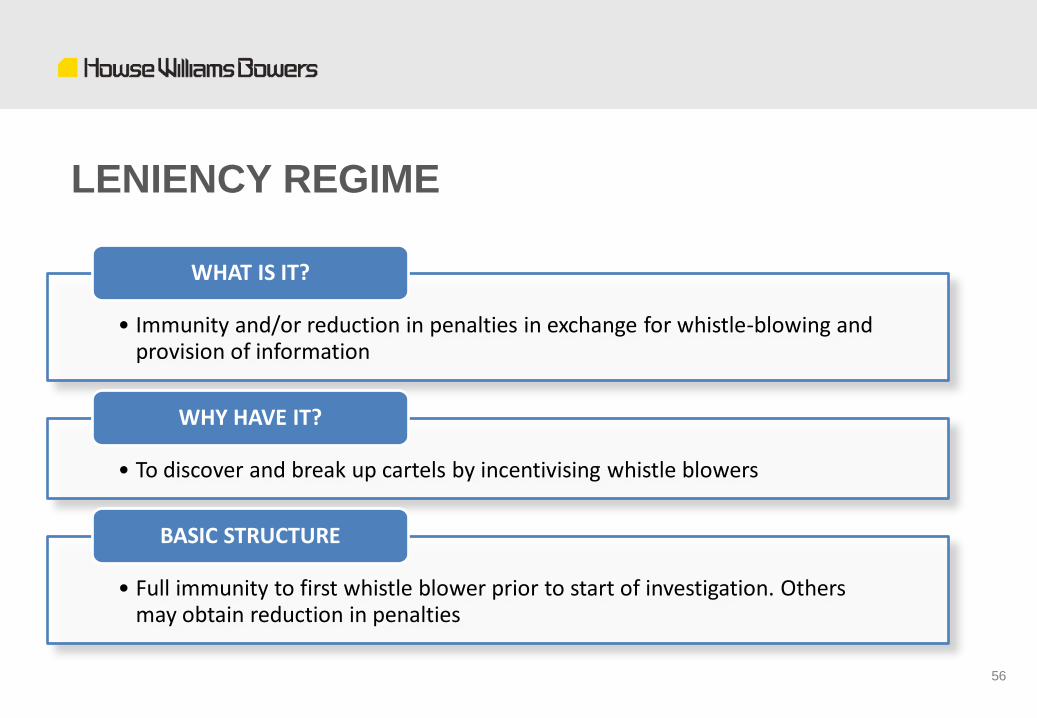

LENIENCY REGIME

• Immunity and/or reduction in penalties in exchange for whistle-blowing and provision of information

WHAT IS IT?

• To discover and break up cartels by incentivising whistle blowers

WHY HAVE IT?

• Full immunity to first whistle blower prior to start of investigation. Others may obtain reduction in penalties

BASIC STRUCTURE

57

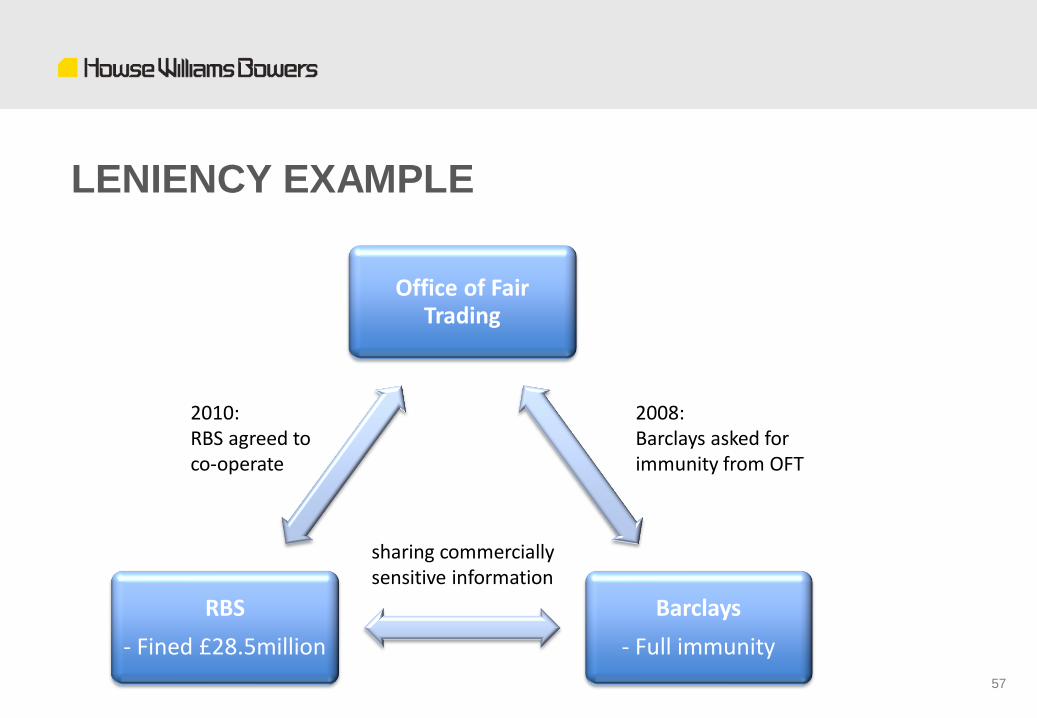

LENIENCY EXAMPLE

Office of Fair Trading

Barclays

- Full immunity

RBS

- Fined £28.5million

2010: RBS agreed to co-operate

2008: Barclays asked for immunity from OFT

sharing commercially sensitive information

58

In 2016, be smart and be prepared

• Review your practices / agreements

• Establish compliance controls

• Cartels will be a regulatory focus

• Leniency?

• Expect some enforcement action

Whistle-blowing

• US Office of the Whistle-Blower

• Hong Kong? Anyone can complain to the regulators

• Competition law: leniency for whistle-blowers

• Who can whistle blow?

Staff

Customers / Clients

Auditors

Competitors

Anyone else!

59

Whistle-blower tips from other countries

60 Source: 2015 Annual Report to Congress on the Dodd-Frank Whistleblower Program

61

In 2016, be smart and be prepared

• Establish internal hotline & escalation procedures

• Have clear & comprehensive response plan to complaints &

whistle-blowers

And to wrap up…

Retail Payment Systems

• The Payment Systems and Stored Value Facilities Ordinance (the Ordinance)

commenced operation on 13 November 2015

• Under the Ordinance, the Hong Kong Monetary Authority (HKMA) is

empowered to implement a mandatory licensing system for multi-purpose

stored value facilities and perform relevant supervision and enforcement

functions.

• After the expiry of the one-year period (i.e. from November 13, 2016 onwards),

it will be illegal for any issuers, unless being exempt, to issue or operate any

stored value facilities without a licence. In addition, licensed banks will be

deemed to be licensed to issue and operate stored value facilities.

• The HKMA has issue an “Explanatory Note on Licensing for Stored Value

Facilities” setting out its policies and approach in implementing the regime for

regulating SVFs.

63

• Financial institutions resolution regime

• Enhanced deposit protection

• New Insurance Authority

• Hong Kong as CTC hub

• Mainland – Hong Kong initiatives

• Technology challenges – cybersecurity, email

scams

64

65

Questions?

Jill Wong Partner

Direct +852 2803 3670

Mobile +852 5180 1836

Fax +852 2803 3608

Email [email protected]

Jill specialises in financial services and corporate regulatory and compliance issues, and has been identified as a leading lawyer in legal directories such as Chambers Asia Pacific, IFLR 1000, AsiaLaw Leading Lawyers and Legal 500. She is named as an External Counsel of the Year in Asian-Mena's annual "Representing Corporate Asia and Middle East Survey 2013".

She shows "exceptional understanding of Hong Kong's regulatory environment, and her relationships with many of the regulatory bodies allow her to provide us with excellent guidance"

Chambers Asia Pacific 2014

She was previously Deputy General Counsel at the Hong Kong Monetary Authority and was in-house counsel as Head of the Asia-Pacific Regulatory Advisory Group, Legal and Compliance at Credit Suisse. In addition, Jill has also worked in leading international law firms in Hong Kong. Her experience with a regulator and as in-house counsel, combined with many years of advising financial institutions and corporates during times of great regulatory changes, allows her to provide in-depth and constructive insights into the issues and challenges facing financial institutions and corporations.

Jill's experience compasses all aspects of banking and securities laws and rules affecting listed companies. She is also active in new areas of regulatory scrutiny such as money-laundering, privacy, retail payment systems and competition. She advises on both on contentious and non-contentious issues, and often in both capacities for the same clients; making Howse Williams Bowers' regulatory practice unique in its ability to advise clients from all perspectives.

2016 Awards Who's Who Legal: Banking 2016 Legal 500 2016 IFLR 2016: Leading Lawyer Chambers Asia Pacific 2016