The Valuation of Intangible Assets: Bridging the Divide ... · Divide between Transfer Pricing and...

35

The Valuation of Intangible Assets: Bridging the Divide between Transfer Pricing and Financial Reporting CBI Life Sciences Accounting & Reporting Congress Andreas Chrysostomou Susan Fickling-Munge March 17, 2015

-

Upload

nguyenkien -

Category

Documents

-

view

217 -

download

1

Transcript of The Valuation of Intangible Assets: Bridging the Divide ... · Divide between Transfer Pricing and...

The Valuation of Intangible Assets: Bridging the

Divide between Transfer Pricing and Financial

Reporting

CBI Life Sciences Accounting & Reporting Congress

Andreas Chrysostomou

Susan Fickling-Munge

March 17, 2015

Agenda

Section 1: Introduction

• Purpose & Benefits of Presentation

• Intellectual Property in the News

• Value of Intellectual Property for Financial Reporting

Section 2: Overview of Financial Reporting (“FR”) and Transfer Pricing (“TP”) Analyses

• Intellectual Property Guidance

• Motivating Factors

• Valuation Methodologies

• Summary of Differences

Section 3: Case Study

• Introduction: Case Study

• Scenario 1: Purchase Price Allocation (“PPA”) Completed and Used for Transfer Pricing

• Scenario 2: PPA and TP Performed Independently

• Scenario 3: PPA and TP Coordinated Together

Section 4: Review Environment

• Key Audit Concerns, Financial Reporting

• Key IRS Concerns, Transfer Pricing

Section 5: Summary

Duff & Phelps 2November 6, 2014

IntroductionSection 1

Purpose & Benefits of Presentation

• Understanding the potential differences in the stated objectives in valuing intangible

assets/intellectual property for financial reporting and transfer pricing purposes.

• Understanding the differences in the valuation guidance and framework for intangible

assets/intellectual property for financial reporting and transfer pricing purposes.

• Understanding appropriate points of consistency between transfer pricing and financial

statement valuation

• Understanding the importance of compliance with regulatory guidance

• Understanding the benefit of coordinated and contemporaneous financial reporting and

transfer pricing valuations

• Understanding current “hot-button” regulatory/compliance issues and how to avoid/address

such issues.

Duff & Phelps 4November 6, 2014

Duff & Phelps 5

Intellectual Property in the News this Past Year…

Tax Court: Western Union/First Data Settles $2B Transfer

Pricing Litigation“Western Union and First Data agreed to a total of $1.18 billion in transfer pricing

related adjustments. The total adjustment included the recognition of $885 million of

additional income in 2003 related to First Data’s restructuring plan, which transferred

certain intangible assets out of the United States, and additional adjustments

between 2004 and 2011 to reach the $1.18 billion total.” – TaxTrials 12/16/2011

…and it will continue to be a hot button…

November 6, 2014

6Duff & Phelps

Value of Intangible Assets in a Purchase Price Allocations

Intangibles

Tangibles

38%

62%

1982 (1)

62%

38%

1992 (1)

87%

13%

2002E (2)

Percentage of market value relating to…

Source: Presentation: TPI-EPO Symposium in Istanbul, Turkey; “EPO on the road to e-business: May 23, 2001”

(1) Brookings Institute; [Source: Balanced Scorecard European Summit May 22, 2001]

(2) Brookings Institute data updated as of 12/31/2001

38%

November 6, 2014

Overview of Financial Reporting

and Transfer Pricing Analyses

Section 2

Intellectual Property GuidanceRegulatory Framework

Financial Reporting

• Accounting Standards Codification (ASC) 805, Business Combinations / IFRS 3

• ASC 820, Fair Value Measurement

• ASC 350, Intangibles – Goodwill and Other

• ASC 360, Impairment or Disposal of Long-Lived Assets

Fair Value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Transfer Pricing

• The OECD Guidelines (Organisation for Economic Co-operation and Development) has issued transfer pricing guidelines (OECD Guidelines) that have been adopted in some form by more than 50 countries (including the US)

• Local Country Rules – Many countries (including those that follow the OECD framework) have issued transfer pricing regulations with country-specific requirements

• US transfer pricing regulations are in Section 482, and that those regulations are among the most voluminous and comprehensive in the world

The arm’s-length standard is achieved if the results of the transaction are consistent with the results that would have been realized if uncontrolled taxpayers had engaged in the same transaction under the same circumstances (arm's length result).

Duff & Phelps 8November 6, 2014

Intellectual Property GuidanceFinancial Reporting Valuations

• Under ASC 805, the cost of an acquired company should be assigned to the tangible and intangible

assets acquired and liabilities assumed on the basis of their Fair Values at the date of the acquisition

• An intangible asset does not derive its value from physical attributes but rather from the intellectual

content of the item or from other intangible properties

– It is identifiable

– Provides control over a resource

– Results in future economic benefits

– Should be considered equivalent to Intangible Property

– Categories include: Technology-based, Marketing-related, Customer-related, Artistic-related, and

Contract-based

• An intangible asset is recognized separately from goodwill if it meets the following criteria:

– Arises from contractual or legal rights (even if cannot be separated and/or sold), or

– Is capable of being separated or divided and sold, transferred, licensed, rented, or exchanged

» Regardless of intent

» Either individually or with a related contract, asset or liability

• Excess of the purchase price over the Fair Value of the net assets acquired, including the identified

intangible assets, is recorded as goodwill

Duff & Phelps 9November 6, 2014

Intellectual Property GuidanceTransfer Pricing

• Under Section 1.482-7 cost sharing regulations, the definition for Platform Contribution Transaction (“PCT”) is much broader than 482 and 936 below and allow for more similarities with the definitions used in a financial reporting valuation.

• Under Section 1.482-4(b), intangibles comprise any of the following items and have substantial value independent of the services of any individual:

– Patents, inventions, formulae, processes, designs, patterns, or know-how;

– Copyrights and literary, musical, or artistic compositions;

– Trademarks, trade names, or brand names;

– Franchises, licenses, or contracts;

– Methods, programs, systems, procedures, campaigns, surveys, studies, forecasts, estimates, customer lists, or technical data; and

– Other similar items.

• Under Section 936(h)(3)(B), intangibles include:

– Contractual/legally protected rights;

– Methods, programs, systems, procedures, campaigns, surveys, studies, forecasts, estimates, customer lists, or technical data;

– Other similar items that do not derive their value from physical attributes, but from the intellectual content of the item from other intangible properties

• Typically involves either an analysis of trademarks/trade names or technology/know-how

Duff & Phelps 10November 6, 2014

Motivating Factors

Valuation

• Low value for intangibles means low amortization; however, there’s a trade off….

• Need to consider potential for future intangible asset and goodwill impairment:

– Indefinite-lived intangibles and goodwill are not amortized; they are tested annually for impairment under ASC 350

» Impairment test based on standalone intangible asset cash flows exposes asset to an annual impairment test based on fair value

» Reporting Unit structure and relative contribution of organic growth vs. growth via acquisition are significant factors in goodwill impairment testing

– Long-lived intangibles are tested for impairment under ASC 360;

» Test depends on the way in which “Asset Groups” are defined and, in practice, is typically based on pre-tax, undiscounted cash flow

Transfer Pricing

• Tax authorities are keenly focused on protecting the domestic tax revenue base

• Tax rate management (Decreasing ETR with the largest cost item on the income statement)

• Non-compliance can lead to adjustments on audit, penalties on top of those adjustments, potential double taxation, and then impacting the tax provisions

• Mitigate risks, time and costs related to Audits(e.g., US ASC 740)

• To appease their external auditors

• Compliance with US Contemporaneous Annual Requirement (1.6662-6(d))

Duff & Phelps 11November 6, 2014

Intellectual Property GuidanceKey Differences of IP Definitions Between Financial Reporting and Transfer Pricing

Analyses

Duff & Phelps 12

Financial Reporting Valuations Transfer Pricing

Asset rather than entity perspective;

bifurcates similar assets based on

Unit of Account; highest and best use

premise of value

Analyses typically looks at a bundle of

intangible assets / legal entity

Buyer-specific synergies are excluded from

IP values; they would be reflected in the

residual goodwill amount to the extent they

were paid for as part of the purchase price

• Buyer-specific synergies may be

included in arm's length price to the

extent they would affect arm's length

outcome

• May increase the value of the

intellectual property, compared to PPA

Values existing technology as a wasting

asset as it exists at the date of acquisition

• Values not only the contributions of

technology as it exists currently, but also

the contributions of that technology to

future development efforts

• May also increase the value of the

intellectual property, compared to PPA

November 6, 2014

Valuation MethodologiesIncome Approach

Financial Reporting

• Income Approach is generally used in the valuation of income producing intangible assets under two common methods:

– Multi-Period Excess Earnings Method (MPEEM)

» value of the intangible is the present value of the after-tax cash flows in excess of contributory asset charges for the use of tangible and other intangible assets

– Relief-from-Royalty Method

» based on hypothetical royalties saved due to ownership of the asset

Transfer Pricing

• The income method calculates the NPV of profits attributable to relevant contributions/intangibles, which are derived through the calculation of income remaining after profits have been assigned to routine functions. While this is different than the PPA approach, it has the equivalent objective.

• Under US cost sharing regulations, the arm’s length amount is the value of the PCT Payment itself, without regard to such tax effects for either the payee or payor

• Outside cost sharing, the income method would be an “unspecified method” under Section 1.482-4

• There is no tax amortization benefit included in Transfer Pricing valuations, since the analysis is performed on a pre-tax basis

Duff & Phelps 13November 6, 2014

Valuation MethodologiesMarket Approach

Financial Reporting

• Market Approach - value based on market prices in actual transactions and on asking prices for

comparable assets; valuation process is a comparison and correlation between the subject

asset and other similar assets

– Although appropriate for certain tangible assets, difficult to apply to intangible assets due to

the lack of available public data in a format that could be reasonably used to infer a value

– This approach can be used to determine market-based royalty rates to apply in the Income

Approach, Relief-from-Royalty Method

Transfer Pricing

• The Acquisition Price Method (“APM”) under Section 1.482-7 is similar to a market approach

where the purchase price is the market price of the contributed intangible

• Only gets applied and is reliable under certain conditions

• A Market Capitalization Method (“MCM”) approach is rarely applied, but could be considered a

market method…likely would not be applied in an acquisition situation

• Both APM and MCM can be applied as “Unspecified Method” under Section 1.482-4

Duff & Phelps 14November 6, 2014

Valuation MethodologiesCost Approach

Financial Reporting

• Cost Approach considers the concept of replacement cost as an indicator of value

– Value determined on the basis of what it would cost (usually at the current price level) to

replace the asset in its current form/functionality

– Considers elements of developer’s profit and opportunity cost

– Distinguishable from a cost savings approach based on expected future savings

Transfer Pricing

• In the OECD draft intangibles guidance, it states that cost-based methods will rarely be reliable

for valuing intangibles

• Not typically used in Transfer Pricing Analyses

• Relative intangible development costs are sometimes used as a proxy for relative value of

contributions by each party in RPSM applications

Duff & Phelps 15November 6, 2014

Summary of Overall Key Differences

Financial Reporting Valuations Transfer Pricing Valuations

Standard and premise of value Fair Value / Unit of Account Arm’s Length Standard (Value) / Entity

Analysis

Goodwill Is a residual concept, as projections used to

value assets only include market participant

assumptions and exclude buyer-specific

synergies

• Buyer-specific synergies may be included

in arm's length price to the extent they

would affect arm's length outcome

• - May increase the value of the intellectual

property, compared to PPA

Treatment of future technology All future technology value, except for

IPR&D, accrues to goodwill; pre-existing IP

may be at the early, peak or later stages of

life cycle as reflected in projections;

amortization may begin immediately, but IP

value may increase for some time; if pre-

existing technology contributes to future

technology, its value contribution will be

captured and included as part of value

• Values not only the contributions of

technology as it exists currently, but also

the contributions of that technology to

future development efforts

• May also increase the value of the

intellectual property, compared to PPA

Reporting Unit / Legal Entity Fair value measured in the aggregate, and

then assigned or allocated to Reporting

Units; at times, though, cash flows may

reside at the RU level, which would align

some values to RUs

Legal Entity level analysis

Post-tax versus Pre-tax cash

flows

Valuation is performed on a post-tax basis;

add-back of tax amortization benefit

somewhat reduces the differential between

FR and TP values

Valuation is performed on a pre-tax basis

Duff & Phelps 16November 6, 2014

Case StudySection 3

Intro to Case Study

Summary of Facts

• Acquiring Company purchased the Acquired Company in a stock deal

• The Acquiring Company has a Qualified Cost Sharing Arrangement (“QCSA”) where IP is split

between USP (US) and the Ireland Holding Company (Rest of World)

• The Acquired Company has IP spread all over between Europe, US, and Asia

• For the stock deal, the Acquired Company is being purchased by the USP

Duff & Phelps 18

USP

European

Operations

IRE

(Euro Hold Co)

Acquiring Company

European

Operations

US Co.

Acquired Company (Pre-Deal)

Asia

Operations

Singapore

(Asia Co)

Germany

Parent

November 6, 2014

Intro to Case StudySummary of Purchase Price Allocation Results

• Acquiring Company structured as a single Reporting Unit; intangible assets and goodwill valued on a consolidated basis and not valued with respect to specific legal entities

• Identified intangible assets included: Customer Relationships, Technology, and trade/brand names (“Trade Names”)

• Acquired Company was direct competitor of Acquiring Company, who expected to achieve certain operating synergies, some deemed to be market participant-based and others buyer-specific

• Deal price was $460 million for debt and equity, plus $40 million for assumed current liabilities for an implied total asset value of $500 million. For ASC 805 purposes, intangibles were valued in the aggregate at $220 million, as follows:

– Customer Relationships = $90 million

– Technology = $90 million

– Trade Names = $40 million

Other Values were as follows:

– Tangible = $180 million

– Residual Purchase Price = $100 million

(excluding DTL)

• Pre-acquisition and post-acquisition/Fair Value balance sheets are presented on the next slide

Duff & Phelps 19

Acquired Company (Pre-Deal)

European

Operations

US Co.

Asia

Operations

Singapore

(Asia Co)

Germany

Parent

PPADeal $500MIP $220 M

November 6, 2014

20Duff & Phelps

Intro to Case StudyFair Value Balance Sheet

November 6, 2014

Intro to Case Study

Scenario Options

• Scenario 1: PPA Completed and Used for Transfer Pricing

• Scenario 2: PPA and TP Performed Independently

• Scenario 3: PPA and TP Coordinated Together

Duff & Phelps 21November 6, 2014

Scenario 1: PPA Completed and Used for Transfer Pricing

Potential Conflicts Post PPA during Transfer Pricing Review

• Client relied upon PPA to derive appropriate PCT payments associated with the transfer of

IP into the relevant entities to conform with client's existing CSA structure

• Client’s reliance on PPA value resulted in substantial undervaluation of transferred IP for

transfer pricing purposes because of different treatment and definitions of intangible life,

buyer specific synergies, pre-tax vs. post-tax analyses, etc.

• Upon audit, client subject to substantial adjustments and penalties due to lack of regulatory

compliance and potential double taxation (if Competent Authority not granted)

• Unexpected financial statement hit to tax rate when financial auditors evaluate income tax

provision in light of the undervaluation

Duff & Phelps 22

USP

European

Operations

IRE

(Euro Hold Co)

Acquiring Company

European

Operations

US Co.

Acquired Company

Asia

Operations

Singapore

(Asia Co)

Germany

Parent

November 6, 2014

Scenario 2: PPA and TP Performed Independently

Potential Conflict in Values not Bridged in PPA vs. Transfer Pricing

• Duplicative efforts of company personnel to produce the same information for two providers

• Different projections were inadvertently used (dates, sources, etc.) for the two different analyses

• Different approaches to valuing tangible assets and routine returns were inadvertently used

• Different discount rates were used because of different assumptions utilized by the practitioners (e.g., equity risk premiums)

• Different comparable sets used to examine the same intangible assets (e.g., trademarks)

• When independent studies examined by external auditor or tax authority (and they do ask for both), can cause concerns from inconsistent values. This is due in part to inconsistent projections and assumptions rather than appropriate differences driven by different regulatory guidance.

Duff & Phelps 23

USP

European

Operations

IRE

(Euro Hold Co)

Acquiring Company

European

Operations

US Co.

Acquired Company

Asia

Operations

Singapore

(Asia Co)

Germany

Parent

PPADeal $500MIP $220 M

November 6, 2014

Scenario 3: PPA and TP Coordinated Together

Duff & Phelps 24

Goal: Have studies not conflict with each other inappropriately

“Allocations or other valuations done for accounting purposes may provide a useful

starting point, but will not be conclusive for purposes of the best-method analysis in

evaluating the arm’s length charge….”

-IRS statement in BNA Transfer Pricing Report on April 22, 2010

“Reconciliation of Purchase Price Allocations and Transfer Pricing”

USP

European

Operations

IRE

(Euro Hold Co)

Acquiring Company

European

Operations

US Co.

Acquired Company

Asia

Operations

Singapore

(Asia Co)

Germany

Parent

November 6, 2014

Case Study Take AwayBenefits & Synergies when Financial Reporting & Transfer Pricing Coordinated

Together

• Company time savings of management and operational personnel through joint interviews

• Leverage same comparables (e.g., trademark/technology comparables) to save costs on both

analyses

• Utilize same initial financial projections that reduces company management‘s time and allows

single set of financials to be leveraged by both analyses

• Create “bridge” from financial reporting valuation of intangible assets to transfer pricing

valuation of IP

• Enhance ability to support tax positions (e.g., ASC 740) upon audit by IRS and/or other taxing

authorities

– Demonstrate same assumptions used to report information to investors which were signed

off on by Company‘s auditors

– Post-acquisition, demonstrate consistency with valuations prepared for intangible asset /

goodwill impairment purposes

• Reduce audit risks in both the US and non-US locations

• Enable identification of potential planning opportunities (e.g., intercompany debt , IP migration,

intercompany product or service pricing) through streamlined and more defensible legal entity

valuations

Duff & Phelps 25November 6, 2014

Review EnvironmentSection 4

“PCAOB inspection reports released in the past two years found a threefold increase in valuation-related audit

problems, spurring securities and audit regulators to alert managers and auditors that they are personally responsible for understanding the assumptions that underlie third-party

value estimates.”- “Delving Into the Value Riddle.” The Wall Street Journal. January 15, 2013.

Duff & Phelps 27

Key Audit Concerns - Fair Value in Financial ReportingThe PCAOB

November 6, 2014

Key Audit Concerns - Fair Value in Financial ReportingPCAOB - Fair Value Measurements (FVM)

• The PCAOB identified a number of audit risks based on its 2007 through 2010 inspection cycles of domestic registrants leading to the current heightened scrutiny from audit firms

• Audit risks for non-financial instruments included:

– Failure to sufficiently evaluate the reasonableness of significant assumptions used by issuers to estimate the fair value of reporting units in their goodwill impairment assessments and the fair value of intangible assets acquired in a business combination

– Failure to challenge issuers’ conclusions that goodwill did not need to be tested for impairment more frequently than annually despite the existence of impairment indicators

• Audit risks related to financial instruments included:

– Failure to sufficiently evaluate reasonableness of management’s assumptions

– Failure to adequately understand methods and/or assumptions used by third-party pricing services

– Failure to evaluate significant differences between independent estimates used or developed by firms and the fair values recorded by issuers

– Failure to sufficiently test significant, difficult-to-value securities

– Failure to sufficiently test to determine whether fair value disclosures were in conformity with ASC 820

Duff & Phelps 28November 6, 2014

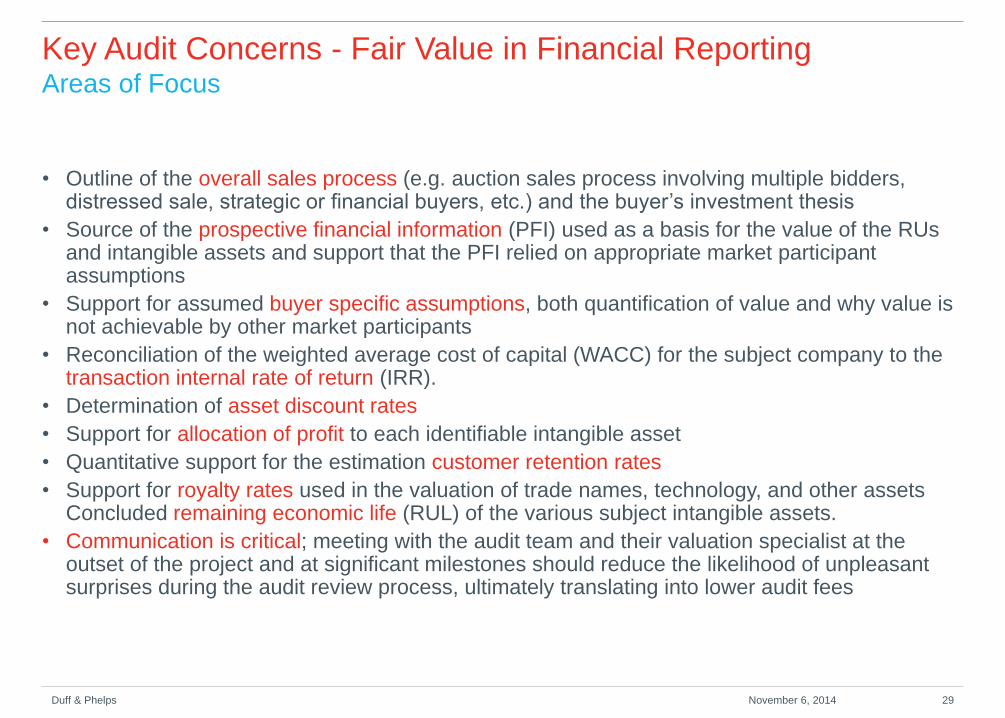

Key Audit Concerns - Fair Value in Financial ReportingAreas of Focus

• Outline of the overall sales process (e.g. auction sales process involving multiple bidders, distressed sale, strategic or financial buyers, etc.) and the buyer’s investment thesis

• Source of the prospective financial information (PFI) used as a basis for the value of the RUs and intangible assets and support that the PFI relied on appropriate market participant assumptions

• Support for assumed buyer specific assumptions, both quantification of value and why value is not achievable by other market participants

• Reconciliation of the weighted average cost of capital (WACC) for the subject company to the transaction internal rate of return (IRR).

• Determination of asset discount rates

• Support for allocation of profit to each identifiable intangible asset

• Quantitative support for the estimation customer retention rates

• Support for royalty rates used in the valuation of trade names, technology, and other assets Concluded remaining economic life (RUL) of the various subject intangible assets.

• Communication is critical; meeting with the audit team and their valuation specialist at the outset of the project and at significant milestones should reduce the likelihood of unpleasant surprises during the audit review process, ultimately translating into lower audit fees

Duff & Phelps 29November 6, 2014

Key Concerns - Transfer PricingAreas of Focus and Current Transfer Pricing Environment

• Any audit of intangible transfer pricing will focus on key factors such as validity of projections,

appropriate determination of discount rates, appropriateness of returns assigned to routine

contributions, appropriate valuation on a pre-tax basis

• Tax implications of the allocation of offshore profits among subsidiaries through transfer pricing

was the #1 tax concern for 2013 – CEB Survey in CFO Magazine (February 2013)

• Tax Authorities are focusing on key service charges such as IT, Marketing, Advertising,

Engineering, R&D and Legal as they may be viewed as intangible generating functions

• Extremely high level of press and attention that “risky” transfer pricing structures are

grabbing—especially for ANY type of valuable IP (e.g., Google in US Audit for ETR of 2.4%)

• Non-compliance can result in penalties, interest, and audit issues

• Tends to be largest tax exposure for company’s ASC 740 (FIN 48) disclosure

• Service, intangibles and financing transactions are increasingly in the sights of tax authorities

• Tax authorities are discussing and exchanging information on taxpayers

• Transfer pricing audits are increasing in significance, intrusiveness and scope

• Emerging markets are coming to the forefront of audit activity (e.g., India and China)

• Advanced markets are increasing their audits (e.g., Canada)

• BEPS !

Duff & Phelps 30November 6, 2014

SummarySection 5

Summary

Risks if PPA and Transfer Pricing Analysis are not Coordinated:

• Tax risks due to differences in values between analyses

• Misalignment of the placement of IP in global transfer pricing policy

• Audit risks due to inconsistent values of intellectual property (External Auditor or Tax Authority)

• Challenges to transfer intellectual property post acquisition

Benefits of Performing PPA and Transfer Pricing Analysis jointly:

• Time savings company management and operational personnel through joint interviews

• Leverage information gathering from company (and have same starting point)

• Cost saving through use of same initial comparables joint team efficiencies

• Enhance ability to support tax positions (e.g., ASC 740) upon audit by IRS and/or other taxing

authorities through bridging differences

• Reduce audit risks in both the US and non-US locations

• Enable identification of potential planning opportunities

Duff & Phelps 32November 6, 2014

Andreas Chrysostomou

Andreas Chrysostomou is a managing director in the New York office, part of the Valuation Advisory Services

business unit and the Duff & Phelps global industry leader for the Healthcare and Life Sciences industry group.

Andreas has more than 20 years of corporate finance and valuation experience.

Andreas has developed expertise in all areas of business valuations, including the determining of business

enterprise value, valuation intangible assets for corporate and individual clients with particular focus on

pharmaceutical, biotechnology and specialty chemicals industries. He also has extensive experience in the

telecom, consumer product and manufacturing and financial services industries.

Andreas is a member of the Duff & Phelps committee responsible for providing assistance and feedback to the

Financial Accounting Standards Board on valuation matters and responded to comments and had discussion

with the U.S. Securities and Exchange Commission on valuation issues. Additionally, Andreas has extensive

experience in performing valuation under the International Financial Reporting Standards. He has also been a

speaker on valuation of intangible assets issues at numerous conferences and has written a number of related

papers Andreas’ clients includes Shire, NPS, Merck, Sanofi, Genzyme, Novartis, Baxter, Amgen, Takeda

(Nycomed), Actelion, Bristol-Myers Squibb, Teva, HealthSouth, Radiation Therapy Services, Medco, GE Health,

Alere, MagnaCare, and many more.

Prior to Duff & Phelps, Andreas was a managing director for Standard & Poor’s Corporate Value Consulting

(CVC) for four years. Andreas was also with CVC for five years after spending two years with the Auditing and

Business Advisory Services of PricewaterhouseCoopers.

Andreas received his M.B.A. in international corporate finance and investments and his B.B.A. in accounting and

operations management from the Bernard M. Baruch College, City University of New York. He is a certified

public accountant in New York and also certified by the London Chamber of Commerce in accounting. Andreas

is also a member of the American Institute of Certified Public Accountants and an active member of the New

York State Society of Certified Public Accountants’ International Accounting and Auditing Committee.

Duff & Phelps, LLC

Managing Director, Valuation Advisory Services, Integrated HealthCare Industry Leader

New York

+1 212 871 5994

33

Susan Fickling-Munge

Susan Fickling-Munge is a managing director in the Chicago office of Duff & Phelps. She is a member of the

Transfer Pricing practice, leveraging more than 15 years of transfer pricing and valuation experience. Susan has

worked closely with global companies in a vast range of industries, assisting them with transfer pricing planning,

documentation and defense.

Susan has extensive experience in international and multistate tax planning projects, employing various transfer

pricing techniques to help support her clients’ tax strategies. She has also assisted clients on unilateral advance

pricing agreements. She has helped to develop real options models and valuation techniques to support

complex transfer pricing and tax structuring scenarios.

Before joining Duff & Phelps, Susan was a vice president of transfer pricing for Charles River Associates, a

transfer pricing manager in the international tax division of Arthur Andersen LLP and a transfer pricing consultant

at KPMG LLP.

Susan earned her MBA at the University of Chicago Booth School of Business and her BA from Scripps College.

She also studied at the Universidad San Francisco de Quito in Quito, Ecuador, and is fluent in Spanish.

Duff & Phelps 34

Duff & Phelps, LLC

Managing Director, Valuation Advisory Services

Chicago

+1 312 697 4647

Questions?

Duff & Phelps 35November 6, 2014