Innovating banking for greater financial inclusion David Ferrand, FSD Kenya.

THEUSEANDIMPACTOFM-SHWARIASAFINANCIALINCLUSIONBANKINGPRODUCTIN

URBANANDRURALAREASOFKENYA

FINALREPORT

Submittedto:

InstituteforMoney,Technology,andFinancialInclusion(IMTFI)

UniversityofCalifornia,Irvine

October,2016

Presentedby:

NdungeKiiti,Ph.D.(MarketMatters,Inc./CornellUniversity)

MoniqueHennink,Ph.D.(Consultant,AssociateProfessor,RollinsSchoolofPublicHealth,EmoryUniversity)

i

ACKNOWLEDGEMENTS

To be successful, the research process requires and involves a whole team of individuals andinstitutions. We are grateful for the financial and technical support of the Institute for Money,TechnologyandFinancial Inclusion(IMTFI),UniversityofCalifornia-Irvine. Without theircommitmenttosupportresearchersintheGlobalSouth,thisprojectwouldnothavehappened.

InbothKenyaand theUnitedStates,weare indebted to: theKenyaNational Federationof JuaKaliAssociations and the Micro and Small Enterprise Authority (MSEA) officials, who facilitated therecruitmentanddatacollectionprocesswithfervorandenthusiasm;thestudyparticipants,whowereextremely gracious with their time and rich insights; the team of dedicated Kenyan researchassistants,whodidtremendousworkfromcompletingtheone-weektrainingtopilotingandcollectingthedata;thedataanalysisteamoftworesearchassistantsinKenyaandtwointheUnitedStates,whoworkedwithgreatdiligencetoensurethefinalresults;andthecinematographerfromMcCordMediaGroup,whoamplifiedourresultsthroughtheuseofaudiovisualmedia.

Finally, we would like to acknowledge all the academic institutions, service providers anddevelopment organizationswhose staff committed time to bringing this research process to fruitionandasuccessfulcompletion—CommercialBankofAfrica (CBA),MarketMatters Inc.,Safaricom,andacademic institutions (Kenyatta University, University of Nairobi, University of California-Irvine,CornellUniversity,andEmoryUniversity).

Researchers,ConsultantandresearchassistantsduringtraininginNairobi

ii

CONTENTS

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i i

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

STUDY BACKGROUND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

INTRODUCTION .............................................................................................................................................................. 5

INTRODUCING M-SHWARI ............................................................................................................................................. 5

WHY FOCUS ON THE INFORMAL SECTOR? ............................................................................................................. 6

Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

SELECTION OF STUDY SITES ....................................................................................................................................... 6

STUDY PARTICIPANTS AND RECRUITMENT ............................................................................................................... 7

DATA COLLECTION AND ANALYSIS ............................................................................................................................. 9

RESULTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

AWARENESS OF M-SHWARI ........................................................................................................................................ 10

PERCEPTIONS OF M-SHWARI ..................................................................................................................................... 11

BARRIERS TO ADOPTION AND USE OF M-SHWARI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

LACK OF FINANCIAL KNOWLEDGE ............................................................................................................................... 12

LACK OF TRUST ............................................................................................................................................................ 13

LACK OF ACCESS TO TECHNOLOGY ............................................................................................................................. 13

LACK OF INTEREST/ABILITY TO USE M-SHWARI SERVICES ......................................................................................... 14

PERCEIVED FINANCIAL RISKS OF USING M-SHWARI ................................................................................................... 14

CHALLENGES OF USING M-SHWARI ............................................................................................................................ 14

FACILITATORS TO USING M-SHWARI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

EASY TO USE ................................................................................................................................................................ 15

M-SHWARI SERVICES OFFERED ................................................................................................................................... 16

SECURITY OF THE M-PESA PLATFORM ........................................................................................................................ 16

TRUSTED SOURCE OF INFORMATION ......................................................................................................................... 16

FINANCIAL LITERACY .................................................................................................................................................... 17

SERVICE IMPROVEMENT ............................................................................................................................................. 17

Conclusion and RECOMMENDATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3

EXECUTIVESUMMARY

In Kenya, the rapid increase of mobile money technology presents an opportunity for increasedfinancial inclusion.However,littleisknownabouttheuseofmobilemoneybyKenya’sinformalsector,theJuaKali. ThisstudyfocusedonthemobilemoneytechnologyproductM-ShwariofferedbySafaricomasanextension ofthesuccessfulM-Pesaplatform. ItexploredtheJuaKali’sexperiencesandperceptionswithM-Shwari.

Data were collected using qualitative and quantitative methods, including in-depth interviews, focusgroup discussions,andademographicsurvey.Theresearchwasconducted ineightStudySitesacrossfour regions of Kenya. The Sites represented semi-urban and semi-rural areas. Overall, 156 in-depthinterviewswere collectedwith84M-Shwariusersand72non-users. Inaddition,12focusgroupswereconductedwithboth usersandnon-users.

All qualitative data were transcribed, coded, and analyzed for common themes using MAXQDA 11.Results were compared by region, gender, and user status. Quantitative data were collected on thedemographic and socioeconomic characteristics from interview participants. SPSS statistical softwarewas used to compute descriptive analyses on the quantitative data. This report will focus on twothematicareas:thebarriersandfacilitatorstotheadoptionofM-Shwari.

ln summary, the results revealed that the Jua Kali became aware of M-Shwari through mediaadvertisements, Safaricom promoters, and by word-of-mouth. Awareness had a direct influence onwhetherparticipantsadoptedthe service.Specifically,membersoftheJuaKaliwhowerenotawareofM-Shwarididnotsignupfortheservice. Otherswere awareof theproduct, but decidednot to registerdue to one or more barriers that included accessibility, lack of information, lack of interest, andperceivedrisksofuse. ThosewhoadoptedM-Shwari reportedthattheyhadheardpositivethingsaboutitfrompromotersandotherusers,andthateaseofuse, perceivedbenefitsoftheservice,andsecurityoftheplatforminfluencedtheirdecision.

The JuaKaliwhoadoptedM-Shwariused the service foreither savingsor loans,orboth.Users foundthe loanservicesbeneficialtoboosttheirbusinessesandtoaddresspersonalfinancialneeds.However,theyregistered dissatisfactionwiththeloanapplicationprocessandtheloanrepaymentterms.Insomecases,userswere repeatedlydenied loans,whichmeanttheycouldonlyusethesavingsserviceofM-Shwari. The Jua Kali used the savings facility to set asidemoney for large purchases or to save foremergency expenses. However, some felt that the interest generated by the savings was too low,whileothersreportedthattheywere unabletosetasidesavingsinthefirstplace.

Followingcarefulanalysisofdata,weconcludedthatawarenesswasthefirststeptowardsadoptionofa new product, and people’s experiences with and perceptions of the promotional methodsinfluenced whether theychoose to tryaproduct in the first place. Whentryinganewproduct,usersapproacheditfromthelensoftheirneedsandexpectations. Theirassessmentoftheproductwasdirectlyinfluenced by how well the product met their needs and expectations. The extent to which the

4

productaddressedusers’needsaccountedforthe diversityofopinionsthestudyuncoveredabouttheproduct.

Finally,itisimportanttokeepinmindthatJuaKaliusers’needswilllikelyevolveastheirbusinessesorgeneral life circumstances change. We also know that mobile products change as service providersinclude refinements and new product innovations. The combination of these twomeans that users’experiencesandopinions willbedynamicandshouldbeassessedperiodicallytoensuretheprotectionofconsumers’interests.

5

STUDYBACKGROUND

INTRODUCTION

While traditional microfinance institutions and banks remain relevant in Africa, new financialproducts basedonamobileplatformhaveenteredthemarketandofferproductalternativestothelow-income market (Johnson & Nino-Zarazua, 2011). Africa’s fast-growing Information andCommunication Technologies ( ICT) sector (Ondiege, 2010) provides infrastructure needed for thenewservices.

In the last few years, Safaricom, Kenya’s biggest mobile network, has launched several mobilemoney products. Among those linked to banks are M-Shwari, M-Kesho, and M-Benki. The mobileproducts operate inpartnershipwith the formalbankingsector to improve financialcapacityamongsmall businesses and microcredit groups. The Jua Kali (informal) sector is of particular interest tofinancial institutionsbecausebusinesses in the informal sectorhave,until now,often fallenoutsidethe reachof formal banking systems.TheCentralBankofKenyaestimates thatoverKsh300billion(approx.$3.5billion)sits outsidetheformalbankingsystem,andmillionsofKenyansdonotmakeuseofbankingservices(Ramah, 2013).

This study focuses on M-Shwari, a product that moves M-Pesa from a basic product for sending,receiving, andstoringmoneytoaplatformthatfacilitatessavingsandloansandisarguablytargetedtosmalland medium-sizebusinesses.

INTRODUCINGM-SHWARI

Launched in November 2012, M-Shwari is a paperless, mobile-based service provided by theCommercial Bank of Africa in cooperation with Safaricom and Vodafone. M-Shwari is available tocustomers ofM-Pesa, the already popularmobilemoney transfer service, and it allows subscribersto save and borrow money using theirmobile phone (Safaricom, 2012;Morawczynski &Miscione,2008). Loansareavailable atvariableinterestrates,andsavingsalsoearninterest.

According to Safaricom, M-Shwari has changed people’s lives since it was launched. MichaelJoseph, directorforM-PesainsideVodafone,hasdescribedM-Shwariasa,“transformationalservice;savingisno longer theprivilegeof theelite” (as cited inRichardHandford,2013,p.2).Othershavedescribed the productasrevolutionary—“wearewitnessingthereinventionoffinancialservicesforthepoor”(Kendall, WrightandAlmazan,n.d.).

Despitesuchclaimstodate,littleempiricalresearchhasexploredthebenefitsandlimitationsofmobilemoneyproducts,especiallyfromtheperspectivesofusersoftheseproducts, and amonglow-incomepopulations(Brooks,Morrison,OwenandShelton,2013). M-Shwari targets low-incomecommunitiesand,giventhepaucityofresearch,itisessentialtounderstandtheirexperienceswithandopinionsofthe product. Thus, this research sought to explore these issues further by asking key questions.What are the opportunities and challenges of M-Shwari within the Jua Kali sector? What is the

6

Astudyparticipant,oneofthefewfemalewoodcarversinMombasa.

significanceof the findings in relation to financial inclusion/exclusion in Kenya?How can policiesbemoreconducivetomobile-driveneconomicdevelopment?

WHY FOCUSON THE INFORMAL SECTOR?

InKenya,severaltermsareusedtodescribetheinformalsector,suchas‘JuaKali’(meaning‘hotsun’in Swahili), microfinance, small enterprises, and small to medium-size enterprises (SMEs). Those inthe informalsectoroftenusetheterms“microandsmallenterprise(MSEs)”todescribetheirsector.Amicro enterprise isdefinedas“a farm,trade,service, industryorabusinessactivity”withanannualturnoverof lessthanKsh.500,000[approx.USD5,000]andwithfewerthantenemployees(Muteti,etal.,2011,p. 28). Incomparison,asmallenterprisehasanannualturnoverbetweenKsh.500,000andKsh. 5million (approx. USD5000-50,000)andbetween10-50employees (Muteti, et al,2011,p.29).Micro and small enterprises contribute to approximately 18% of the country’s GDP and create74%ofallnewjobsannually (Muteti,et al.,2011,p.30).Thus,thesectorplaysan importantrole inKenya’s economy, especially when it comes toimprovinglivelihoodsinlow-incomecommunities.

The role of this sector has been recognized by mobilebankingproviders,whotargetproductslikeM-Shwariattheinformalsector. Indeed,asurveycarriedoutbyFSDKenya and the Central Bank of Kenya found that theinformalsectorisamongstsomeofthehighestusersoffinancialservicesbymobilemoneyproviders(Safaricom,2013). This is especially important since “existingliteratureonSMEsindicatethatlackofcapitalisastrongconstrainttogrowth”(Bowen,Morara&Mureithi,2009,p.24). However, the question remainswhethermobilebankingproducts likeM-Shwaricanprovidethekindofcapital needed for sustained business growth. In aneffort to shed light on this – and other relatedquestions, this study has set out to explore the userexperiencesofM- ShwariamongKenya’sJuaKalisector.

METHODS

The purpose of this study was to understand perceptions of theM-Shwari mobile money service,and barriersandfacilitatorstoitsuseamongsttheJuaKalisectorinKenya.

SELECTIONOF STUDY SITES

7

The study was conducted in eight counties across Kenya that together capture diversity in socio-demographics(culture,language,incomelevels),JuaKalibusinesssector(manufacturing,service,agro-based,andsmall trade)anduseofmobilebankingservices.Withineachcounty, twostudysiteswereselected, one semi-urban and one semi-rural area. Counties in the northern regions of Kenya wereexcludedfromthestudyduetosecurityconcerns.Thefollowingcountiesandstudysiteswereincluded:Nairobi2 (Westlands and Eastlands), Eastern (Machakos and Embu), Mombasa (Mombasa Island andKaloleni),andNyanza(KisumuandBondo).

STUDYPARTICIPANTS ANDRECRUITMENT

Participants were eligible for this study if they were part of the Jua Kali sector, owned theirown independentbusinessorweremembersofacooperative.WerecruitedJuaKaliwhowerebothusers and non-users of M-Shwari. A ‘user’ was defined as having used any M-Shwari service (e.g.savingsorloans) at leastonce.A‘non-user’wasdefinedashavingneverusedanyM-Shwariservice.Participant recruitment began by contacting the CEO of the Kenya National Federation of Jua KaliAssociations. He linked the research teamwith theMicro and Small EnterpriseAuthority (MSEA) ofKenya,where many Jua Kali businesses are registered. The Director of theMSEA based in Nairobiprovided a s t u d y a p p r o v a l letter and put the researchers in touchwith the County EnterpriseDevelopmentOfficer(s)ineachstudysite.

1UseofmobilebankingservicesbasedondataprovidedbyFSDKenyaandCentralBank (2013)wasusedasaproxy todefineregionswithlow,moderate,andhighusage.

2SinceNairobiisafulladministrativecounty,the‘rural’areawasoneofthesurroundingslumareas.

8

Agro5%

Manufacturing55%

Service19%

Smalltraders16%

Noanswer5%

Studyparticipantsbybusinesssectors.

2

44

60

32

13

7

1

0 20 40 60 80

19andunder

20-29

30-39

40-49

50-59

60-69

70-79

NUMBEROFRESPONDENTS

AGE

None1%

Primary50%

Secondary

36%

[CATEGORYNAME][PERCENTAGE]

[CATEGORYNAME][PERCENTAGE]

None Primary Secondary

Technical University

Studyparticipantsbyage. Studyparticipantsbyeducation.

County Officers were then contacted toobtain informal permission for the study andto request assistance with participantrecruitment. County Officers used their localMSEA business registry to identify eligibleparticipants whom they contacted in person,by phone, or by text message to describethe study and invite their participation.County Officers were asked to contact adiverse range of participants who used anddid not use M-Shwari services from all thefour Jua Kali employment sectors. Theseincluded both men and women from thesmall trade, small trade, manufacturing,

service providers,andagriculture.

Each County Officer aimed to recruit a diverse range of Jua Kali, comprising 10 users and 10 non-usersofM- Shwari.Given the structureddiversity in selectionof study sites and study participants,data saturation was reached with 20 participants or fewer in each study site. Adding moreparticipantswouldnothave led tonew information in relation toour researchquestions. Theresearchers began to hear the same thematic topics highlighted which led them to be empiricallyconfident that their categories were saturated. This led to 84 M-Shwari users and 72 non- usersrecruitedacrossallstudysites.

9

Vision,mission,andvaluesoftheMSEA.

DATACOLLECTIONAND ANALYSIS

Qualitativein-depthinterviewswereundertakentoenableusto identify detailed narratives on participants’ perceptionsand experiences of M-Shwari. Interviews were conductedusing a semi-structured question guide that included thefollowing topics: exposure to mobile money technology,exposure toM-Shwari (e.g. knowledge of product, exposureto promotional messages), reasons for adopting or notadopting M-Shwari, experiences of use, and strengths andweaknesses of M-Shwari. Basic demographic informationwas also collected from all participants, includingparticipants’ age, gender, household income,marital status,workstatus,education,supportof familymembers,andtheirloanandsavingshistory. Theinterview guidewaspilottestedandrefinedpriortodatacollection.Datawere collectedby15interviewers from local universities who were fluent inEnglish, Kiswahili (the official national language), and thelocal languages of their county. Interviewerswere trained inqualitative research methods and ethical research conduct,and were briefed on the M-Shwari product and thecharacteristics of the Jua Kali sector. Interviews wereconductedat thework locationsof the JuaKali or in nearbycommunityfacilities.

Incentiveswerenotgivento individualparticipants,buteachMSEACountyOfficerwasgivenasmallpaymenttoassisttheJuaKali intheirregion. All interviewsweredigitally recordedwithpermissionfromparticipants. Permissionwasalso requestedandgranted forall thephotosandvideo footageobtainedinthestudy.

Alldataweretranscribed,translatedintoEnglishandde-identifiedbeforebeingenteredMAXQDA11,a qualitative data analysis package. Data were reviewedmultiple times to identify core issues andlisteda codebook.Thecodebookwasusedto labeldata for focusedanalysisofeach issue.Detaileddescriptions of each issue were developed, structured comparisons were conducted to identifyany patterns by geographic region, socio-demographic characteristics orM-Shwari user status. Thedemographiccharacteristicsofparticipantswereentered intoSPSSstatisticalsoftwaretosummarizethestudypopulation.

EthicalApprovals

This study was submitted to the Kenyatta University Institutional Review Board in Kenya, asKenyatta Universitywasafieldpartnerforthisstudyandwasdeemedexempt.DataanalysisreceivedIRBapproval fromCornellUniversity,wheretheleadresearcherisbased.

10

RESULTS

AWARENESSOFM-SHWARI

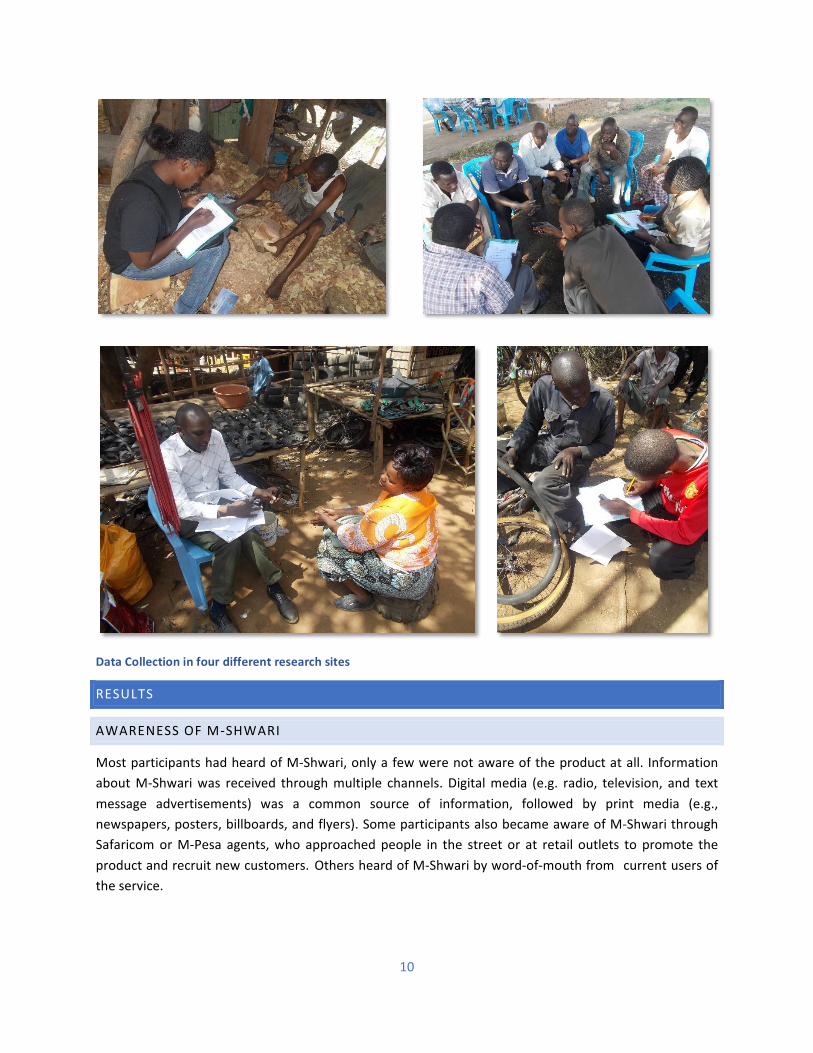

MostparticipantshadheardofM-Shwari,onlyafewwerenotawareoftheproductatall. InformationaboutM-Shwariwas received throughmultiple channels. Digitalmedia (e.g. radio, television, and textmessage advertisements) was a common source of information, followed by print media (e.g.,newspapers,posters,billboards,andflyers).SomeparticipantsalsobecameawareofM-ShwarithroughSafaricomorM-Pesa agents,who approachedpeople in the street or at retail outlets to promote theproductandrecruitnewcustomers. OthersheardofM-Shwaribyword-of-mouthfrom currentusersoftheservice.

DataCollectioninfourdifferentresearchsites

11

PERCEPTIONSOFM-SHWARI

ParticipantsdescribedarangeofperceptionsabouttheM-Shwariproduct.

a. Trust of Product: Participants were divided in their opinions about trusting M-Shwari.When discussing messages from various types of media, some participants felt that theimages, ideas, and words used to present the product gave a true representation, whileothersweresuspicious ofthepromotionalmessagesandviewedM-Shwariasapotentialcon.

The question of trust was also relevant to word-of-mouth promotion. Many currentusers reported that they had registered for the product after receiving information fromanotheruser. Incontrast,manynon-usershadlimitedaccesstoinformationaboutM-Shwari-theyeitherdid not knowotherM-Shwari users, or they did not feel comfortable discussingfinancialmatters, includingM-Shwari,withothers. Somenon-users reported that theywerereluctanttotrustM- Shwariafterhearingaboutotherusers’negativeexperiences(suchasaloanbeingdeniedorthe customerbeingchargedunexpectedfees). Forexample:

Ihaveneverknownhowitworks…butifyouwillexplaintomemaybeIwilljoinit.IheardoneyoungmanwhohadborrowedfromM-Shwari...Andthatonetimehewantedtoborrowanotherloanbuthewasdeniedbecausehehadnotclearedthefirstloan.ThenIstartedfearingM-Shwari.(Femalenon-user,Machakos)

b. Inadequate Product Information. Participants also had wide-ranging views about theadequacy of the promotional messages. Some felt that the promotional messagescontained sufficient detail,while otherswouldhave liked to receivemore information. Thecommentssuggestedthat participantswouldhavelikedtolearnmoreabouttheproductandto hear client testimonials and promotional offers for M-Shwari and related products. Thisopinionwas voiced especially by participantswho had been exposed to only one source ofpromotion about M-Shwari. Importantly, both users and non-users felt that agents shouldhave promoted the product more extensively among the Jua Kali by visiting their retaillocations and offering one-on-one product demonstrations. This lack of promotion wasviewedasalackofinterestinthesectorasapotential customerbase.

c. Focus on Mainstream Media. Most participants reported receiving promotional messagesabout M-Shwari in English and through mainstream media channels (e.g. radio, television,newspapers). However, they felt that promoting M-Shwari on local radio stations and inregionallanguageswouldhave beenmoreeffectiveinreachingtheJuaKali.

d. Interpersonalcommunication:InterpersonalcommunicationaboutM-Shwariwasinfluentialina personbecoming a userof theproduct. ParticipantswhousedM-Shwari stated that theyhad initially heard about it from other users through interpersonal communication. Theywere informedaboutthebenefitsoftheproduct,suchasprovidingcashinemergencies,andtrusted theinformationgivenbyotherusers.Theyweremotivatedtojoinwhentheylearnedsomeone they knew used the services. Several users discussed how conversations with afriend,familymemberorcolleaguegavethemconfidencetoregisterfortheservice,because

12

they learned M-Shwari was not a con and could help them in their financial matters. Incontrast, non-users knew fewpeoplewho usedM-Shwari. They relied on information frommediasourcesandhadmixedopinionsabouttheproduct.

e. Entertainment vs education. Participants often described the promotion of M-Shwari as“entertainment, not education.” They reported seeing M-Shwari promoted using music,dance, and by vehicles with loudspeakers driving through neighborhoods. Some felt thatthis type of promotion raised awareness but did not provide sufficient education aboutthe product (e.g. benefits,risks)forexample;

People think that these promotions consume a lot of money and this moneyis recovered from the interest thatM-Shwari charges. Promotions that are notaccompanied with adequate explanations are not beneficial to the service atall. People move from one stage to another doing entertainment rather thanpromoting aproduct.Topromote isnot toentertain!Youentertainpeopleandyou leave them the same.No knowledge about your product. (Male non-user,Embu)

BARRIERSTOADOPTIONANDUSEOFM-SHWARI

BarrierstoadoptingM-Shwarifallintoseveralcategories.Thisnextsectionfocusesonbarriersfornon-userswhohadnotyetadoptedM-Shwari.Thesechallengesaredescribedbelow.

LACKOFFINANCIALKNOWLEDGE

Lack of knowledgewas a barrier to adoptingM-Shwari. Due to limited incomes,many Jua Kali hadlittle or no prior exposure to a culture of savings and, more specifically, savings accounts.Furthermore, some participants lacked knowledge about M-Shwari, including specifics about loaneligibility and amounts, repayment terms and conditions. One non-user from Embu shared thequestionshewouldwanttoknowinrelationtoM-Shwari:

I:Sowhatspecificallywouldyousayyouhaven’tbeeninformedabout[M-Shwari]? P:IfIsavemoneyinM-Shwariwilltheydeductanyfeesfrommyaccountwhetherwhen[ornot]IamsavingorwhenIamwithdrawing?WhatisthedifferencebetweenmoneyinM-PesaaccountandthatinM-ShwariaccountofthesamepersoninthesamephoneinthesameSIMcardandnetworkprovider?WhatistheprocessofsavinginM-Shwari? I:WhatwouldyousayisyourmainreasonthathasmadeyounotuseM-Pesa? P:Lackofinformation.Nobodyhasexplainedittome.

Another barrier to adoption was low literacy, both language literacy, as well as financial andtechnological literacy. Lackof literacyposedachallenge for female participants in particular. It alsocontributed to participants’ fear of falling victim to theft and deceptionwhenusingM-Shwari. It isconceivablethattherewasaparallelbetweenlevelsofliteracyandeducation.Datashowedthat50%of the Jua Kali participants, who participated in this research, reported that they had a primaryeducationlevelwhile36%hadasecondarylevelofeducation.Wedidnotexplorethislinkagefurther.

13

LACKOFTRUST

a. Interviews revealed t h a t lack of trust w as a significant barrier to adopting M-Shwari.Participants expressed that they were cautious in who to trust with discussions ofmoney.Someparticipants indicated that they did notwant others to knowhowmuchmoney theyhad, how they stored theirmoney, or how they transacted their funds. For example, somesaidthattheydidnotdiscusshowmuchmoneytheyhadwithclosefamilymembers,suchastheir spouse or dependents. This led them to feel they could control household spending.OtherssaidtheydidnotdiscusstheirfinancialmatterswithothersintheJuaKaliasamatterofprivacy.Inaddition,somedidnotfeelcomfortablemakingtraditionalbankingtransactions,because it exposed their finances to banking agents. Aside from general knowledge abouttheirfinances,theJuaKalimemberskepttheirM-PesaPINprivateandwouldnotshareitwithothers. However, a few Jua Kalimembers recounted experiences of trusting a person or acompanywith theirM-Pesa PIN and losing theirmoney. Thismade them, and others whoheardsimilarstories,waryofdiscussingmoneyorsharingprivatefinancialinformation.

b. Another aspect of the lack of trust related to the safekeeping of one’s money. Jua Kaliparticipantssaidtheywereconcernedaboutstoringtheirmoneysecurely. A l t h o u g h theytrustedM-Pesaasa safeplace to storemoney and to make f i n anc i a l transfers, theydidnot use any other f inanc ia l products, includingM- Shwari,becausetheyfearedthattheirmoneywasnotsafewhentheyusedotherproducts.

LACKOFACCESSTOTECHNOLOGY

Lack of access to technologiesneededtousemobilemoneywas reported as a barrier to adoption.Specifically, not having amobile phone or a Safaricom linewere ident i f ied as barriers, becauseboth are prerequisites for using M- Shwari. Participants described accessibility as a barrierparticularlyfortheJuaKalisector.Accessibilityissuesincludedownershipofamobilephone,useofaSafaricom line, ability to read, fluency in the language of the application, and technology literacy.Somenonusersexpressedthattheydonothaveamobilephoneortheyshareamobilephonewhichinhibiteduseof the service for financial transactions. For example, onenonuser explained thatnothaving a private cell phone,meant that theirM-Pesa accountwas at risk of being usedor abused.OthersdidnothaveaSafaricomlineanddidnotwanttochangeprovidersorpurchaseanewphonetoaccessM-Shwari.Inaddition,usersdescribedthatotheraccessibilityissuesmayinhibitsomeoftheJuaKalimembersfromenrollinginM-Shwari,suchasthelanguageoftheapplicationandtheabilitytoreadorusetechnology,especiallyamongtheelderly.Userssaidthatlanguageandliteracychallengesmaypromptotherstoseektheassistanceoffriendsorfamily,whichcouldexposetheirfinancialdatatoothersandrisktheftordeception.

Usersalsoreportedthatnetworkoutagespreventedthemfromaccessingtheserviceperiodically.Lackof English literacy and experience with mobile technology compounded the technological barriers,becausetheM-ShwariphoneappisinEnglish.

14

LACKOFINTEREST/ABILITYTOUSEM-SHWARISERVICES

SeveralnonusersindicatedalackofinterestinusingM-Shwariservice,becausetheywerenotattractedtotheservicesofferedor lackedmoneytotakeadvantageofthese.The loanservicesdidnot interestsome Jua Kalimembers, because the loan amountwas too low or the period of repaymentwas tooshort.Someuserswouldutilizethesavingsservicesbutnottheloanfacilitiesduetothelowamountofloansavailable.Nonusersalsolackedinterestintheservicesbecausetheydidnothavemoneytosaveortorepayaloan.Additionally,nonusersperceivedthatM-ShwariwasnotintendedfortheJuaKali,butforotherbusinessesandwere thereforenot interestedasa result. Lastly, somedidnotseeanyclearbenefitstousingM-ShwariorwerecontenttouseM-Pesatofulfilltheirfinancialserviceneeds.OthersexpressedthattheyhadotherprioritiesanddidnothavetimetoconsiderM-Shwari.

PERCEIVEDFINANCIALRISKSOFUSINGM-SHWARI

NonusersperceivedriskstousingM-Shwarithatdiscouragedthemfromregisteringfortheservice.Forexample, theyfearedtakingouta loanandnotbeingabletorepay itbytheendofthemonth.Somenonusersreportedthattheinstabilityoftheirincomemaderepaymentdifficultwithinthetimeframeoftheservice,andrecountedstoriesofotherswhohaddefaultedontheir loan. Inaddition, theJuaKalinonusers expressed concerns about hidden fees and the possibility of theirmoney not being secure.Some were concerned about losing all of their money in M-Shwari if the service was a con or theaccountwasnotsecure.Thisrelatestotheearlierconcernabouttrustingotherswithfinancialmatters,asexpressedbyanon-userinMachakos.

P:ThetruthisthatIjustseeitonmyphonemenuandthenIscrollandreadthedetailsformyself.AndeventhenIimagineitcouldbelies.Itcouldbeacongameonphone[laughter]I:Youstillthinkyoumaybeconned?P:Yes,Ifear.Ithinkitcouldbeascamandpeoplewillonedaylosealltheirmoney[…]thebiggestproblemisthatIhaveneverfoundsometrustedpersontoexplaintomehowthisthingworks.–Malenon-userinMachakos

CHALLENGESOFUSINGM-SHWARI

The barriers described thus far (e.g., lackof trust, perceived risks, etc.) apply tonon-users – peoplewho had not adoptedM-Shwari. Thosewho had decided to use the product reported another setof challenges,whichactedas initialbarriersastheyadoptedtheservice. Overcomingthesebarriersmayleadtoamorepositiveuserexperience.

M-Shwari users highlighted difficulties with the loan application process. They reported that theapplication process and the criteria used to determine eligibility and loan amounts were notcommunicated clearly to consumers by the company. One user expressed this as he narrated hisattempttouseM-Shwariforaloan:

15

Iwanted toborrowsomemoney.So…okay, Iwanted tobuyaMotorbike so Iused tosavemoneyforbuyingthemotorbikethroughM-Shwari.Isavedupto30,000,littledidIknow… I thought that if I save 30,000, they can give me another 30,000 to make it60,000(laughs).SoIsendandtheytoldmetheminimumamount…themaximummoneyI caneeh… I can’t really remember itwasM-Shwari1,000orwhat….” Hewenton tohighlight the positive unintended consequence: “M-Shwari has helped me because IsavedmymoneythroughM-Shwariandboughtamotorbike.”-MaleUserKamkunji

Some participants reported being turned down for a loan, even after multiple applications. Thismeant that their useofM-Shwariwouldbe restrictedonly to thesavings facility. Ruralusersweredeniedloansmoreoftenthanurbanusers. Anotherconcernwasthesmallamountoftheloan,whichusersfeltwastoosmalltohelpimprovetheirbusinesses.

Anothersetofconcernsfocusedonloanrepayment.Mostparticipantsreportedthattherepaymentperiodwas too short, although some felt that the loanswere too small towarrant evenamonth-longrepaymentperiod.

Issues with technology were also reported among the challenges. Some participants reported thatthey had encountered problems with the mobile app due to network outages or their ownunfamiliaritywith theM-Shwariproduct. Suchissuesledtolatepaymentswhichoftenincurredfeeswhichwerereportedastoohighforusers.

Thestudydidnotfindanynotabledifferencesinthechallengesreportedbyregion;however,genderinfluenced the issues reported. In particular, women reported concerns about the small loanamounts,networkoutages,andtechnological literacy,whilemenprimarilyreporteddifficultieswithrepayment.

FACILITATORSTOUSINGM-SHWARI

EASYTOUSE

ParticipantswhousedM-Shwarisaidthatitwaseasytoregisteranduse,andwasaccessibleatanytimeorplace.Theeaseofusewasan importantaspectofM-Shwari that theycouldnot find in traditionalbanks,whichrequiredtheJuaKaliworkersto leavetheirbusinesstotraveltoabankandwait in longlines.Instead,M-ShwariofferednearlyinstantregistrationandimmediateaccesstosavingsandloansasdescribedbyauserinNairobiWestlands:

M-Shwari isgoodbecause...youwillnotwastetimewalkingtothebanks.Youseeheretherearenobanksandwhen youwant towithdraw it is also instant…yeah. It hasnobarriers.-FemaleUserNairobiWestlands

Inaddition,theconnectionbetweenM-ShwariandM-Pesafacilitatedeasyregistrationandtheabilitytotransfer funds between the two accounts. M-Shwari also uses the information from a Safaricomaccount,whichsimplifiedtheloanapplicationprocessforJuaKaliandsavedtime.

16

M-SHWARISERVICESOFFERED

JuaKaliuserssaidthattheyweremotivatedtoenroll inM-Shwaribecauseofthebenefits theservicecould offer them. Some saw that the loan services could help them purchase supplies that couldstrengthenandexpandtheirbusiness.Otherssawtheopportunitytosavemoneyforemergenciesortosetasidemoneyfora largepurchasethatcouldsupport themintheirbusinessorpersonal life.Someusers especially liked that their money was earning interest, and this motivated them to continuedepositingfundsintotheirsavingsaccount.Otherssawpeopletheyknewbenefitfromtheservicesandweremotivatedtoreapthesamebenefits.

Nonusers said thatunderstanding thebenefitsofM-Shwari serviceswouldencourage them toenroll.Indeed,whenfacedwithsuddenneedforasmallamountofcash,someparticipantsweremotivatedtoenrolltotakeoutan instant loan.TheseparticipantswereawareofthebenefitsofM-Shwariorknewuserswhopromptedthemtousetheserviceforanemergency,andthencontinuetouseM-Shwariforothermatters.

Another benefit ofM-Shwari, identified by users,was that the product provides amore confidentialalternativetoborrowingmoneythanothersources,suchasrelatives,friends,microfinancegroups,orcooperatives, allofwhichareseenaslessprivatethanM-Shwariandapotentialsourceofinterpersonalconflict.Asonemaleuserexplained:

P:Ifyouwanttobuysomethingintheshopit’snotamustyougowithcashmoney,youtransfer themoneyyouhavesaved inM-Shwariandyouwillbeable tobuywhatyouwantedtobuy.YougotoM-ShwariaccountthentransfermoneytoMpesa,nowyouseethingsareeasyandyouhavenotborrowedanyoneandifyouborrowyoucanfailtopaythentheconflictarisesuntilyouarereportedtothepolicestationandyouhaveaphoneinyourpocketwhichyoucanborrowfromM-Shwari–MaleUserinEmbu

SECURITYOFTHEM-PESAPLATFORM

M-ShwariusestheM-Pesaplatform.BecauseM-PesaiswidelyusedandtrustedinKenya,byextensionusersviewedM-Shwariasasecuretooltowithdraw,saveandtransfermoney.JuaKaliusersreportedthat the security of the platform was another facilitator to enroll in M-Shwari. They considered M-Shwariasafewaytostoreandsavemoneywhilealsobenefitingfromprivatetransactions.Asamobilebankingservice,M-Shwariallowedusers tomovemoneyto their savingsaccountsandtakeout loanswithoutinvolvingothers.Thisappealedtothedesiretokeepfinancialtransactionsprivatefromothers.NonuserssaidthatknowingthatM-Shwariisasecureplatformmaymotivatethemadoptit.

TRUSTEDSOURCEOFINFORMATION

Usersreportedthathavingaccessto(perceived)trustedsourcesofinformationfacilitatedtheadoptionofM-Shwari.Thesesourcesincludedmediaadvertisement(radioandTV),otheruserswhohadsharedpositiveexperiences,aswellasSafaricomagentswhoprovidedclearandadequateexplanationoftheproductandhelpedwiththeregistrationprocess.

17

FINANCIALLITERACY

PriorexposuretoandfamiliaritywithinformalandformallendingsystemsaidedtheprocessofadoptingandusingM-Shwari.

SERVICEIMPROVEMENT

While many users reported positive experiences withM-Shwari, they also shared areas for productimprovement,whichtheyfeltwouldenhancetheproductforexistingusersandfacilitatenewusers.These included expanding the range of services offered, improving communication with customersthrough increased transparency, increasing the amount of loans available especially for businessgrowth,andofferingvariableinterestratesforsavingsandloans.

CONCLUSIONANDRECOMMENDATIONS

TheJuaKalisectorisessentialforKenya’seconomicgrowthandservesasasubstantialandkeymarketformobilemoney services. With theneedof increasedopportunities for financingbusinessespairedwithpersonalneedsoftheJuaKalimembers,mobilemoneyproducts,likeM-Shwari,couldpotentiallyfacilitatepositivechangeandgrowth.Thisstudyidentifiedvariousbarriers(lackoffinancialknowledge,lackof trust, lackof the access to technology, etc.) aswell as benefits (easeof use, services offered,security, trust in source of information, etc.) that can guide mobile money service providers, likeSafaricom,tohelpmembersoftheJuaKalisector.

Basedonthefindingsofthisstudy,wesuggestthefollowingrecommendationsfor increasedfinancialinclusionoftheJuaKalisectorforM-ShwariinKenya:

1. Increase awareness of M-Shwari by disseminating information through trusted sources, such asfamiliarbusinessandcommunitymemberswhoareM-ShwariusersorlocalSafaricomagents.

2. Provide informationaboutM-Shwari in formats,mediaand language tailored specifically to theJuaKalisector–suchasthroughregionalradiostationsandinlocallanguages.

3. Provide basic information about the M-Shwari services, benefits, procedures and costs toovercomelackofknowledgeabouttheproduct.

4. IncludetestimonialsfromM-ShwariuserstopromoteawarenessandallayconcernsamongsttheJuaKaliinrelationtosecurityofM-Shwari.

5. FocusM-ShwaripromotionontheproductbenefitsfortheJuaKalisectortoovercomeperceivedlackofrelevance.

6. EnsurethateducationaboutM-Shwariisknowledge-basedratherthanpurelyentertainment.

7. Providegreatertransparencyinthefees,loanrepaymentconditionsandsecurityofmoneyinM-Shwaritoovercomethelackoftrust.

18

8. Provide trainings on how to use the M-Shwari platform, money transfer, savings and loanfeatures,andsecurityfunctionstoovercometechnologybarriersamongJuaKali.

9. Review and improve the loan conditions for business enhancement (loan amount, interest andrepaymentrequirements)specificallyforJuaKali.

10. ExploreimprovementstointerestonsavingstoencouragetheuseofthisserviceamongsttheJuaKali.

11. ReviewtheoverallM-Shwariloanapplicationprocess(format,language,length)toensureJuaKalicapacitytoapplyfortheservice.

12. Develop and facilitate amore effective help-line service to assistwith queries, registration andtroubleshootingwhenusingM-Shwari.

19

REFERENCES

Bowen, M., Morara, M. & Mureithi, S. (2009). Management of Business Challenges Among SmallandMicro Enterprises inNairobi-Kenya. KCA Journal of BusinessManagement, 2(1),16-31.

Brooks,Morrison,Owen and Shelton. (2013)Mobile Banking and theUser Experience Lessons fromKenya,thePhilippinesandHaiti.SanfordSchoolofPublicPolicy,DukeUniversity.

Handford,R. (2012). M-Pesa to Offer Mobile Banking, Mobile Word Live:http://www.mobileworldlive.com/vodafone-broadens-range-of-m-pesa-offering.

Johnson, S.&Nino-Zarazua,M. (2011). FinancialAccessandExclusion inKenyaandUganda. Journalof DevelopmentStudies,47(3):475-496.

Kendall, J., Wright, G. & Almazan, M. (n.d.) New Sales and DistributionModels in MobileFinancialServices.http://ssrn.com/abstract=2241839.

Morawczynski, O. & Miscione, G., 2008, in IFIP International Federation for InformationProcessing, Volume 282; Social Dimensions of Information and Communication Technology Policy,Chrisanthi Avgerouu,MatthewSmith,PetervandenBesselaar; (Boston: Springer),pp.287-298.

Muteti, R. et al (2011). The SME Handbook: Information, Services, and Products for SmallBusinessOwnersinKenya.Nairobi:AquariusMedia.

Ondiege, P. (2010).Mobile Banking in Africa: Taking the Bank to the People. AfricanDevelopmentBank,AfricaEconomicBrief,Volume1,Issue8.

Ramah, (2013) Kenya: New Mobile Service M-Shwari Brings Banking to Underserved Kenyans.http://allafrica.com/stories/201301170167.html

Safaricom. (2013). LughaYaM-Pesa. TheQuarterlyAgentNewsletter,October-December.