The U.S. Economy After the Great Recession: America’s Deleveraging and Recovery Experience Sherle...

47

The U.S. Economy After the Great Recession: America’s Deleveraging and Recovery Experience Sherle R. Schwenninger and Samuel Sherraden Economic Growth Program March 2014

-

Upload

allan-armstrong -

Category

Documents

-

view

214 -

download

2

Transcript of The U.S. Economy After the Great Recession: America’s Deleveraging and Recovery Experience Sherle...

The U.S. Economy After the Great Recession:America’s Deleveraging and Recovery Experience

Sherle R. Schwenninger and Samuel SherradenEconomic Growth Program

March 2014

IntroductionThe bursting of the housing bubble in 2008 plunged the U.S economy into a serious crisis, leaving American households with a huge debt overhang and the economy with a large gap in output and employment. This Report reviews the economy’s deleveraging and recovery experience more than five years after the crash. It explores the following questions: • How far has the economy come in the deleveraging process? Is private sector debt now at a sustainable level or do households and the financial sector continue to need to pay down debt? • To what extent has the U.S. economy recovered from the large plunge in output and employment? How close is the economy to full employment?

• What kind of recovery has the U.S economy had? What has driven the recovery and has it become self-sustaining?

• How has the recovery affected the long-term growth potential of the U.S. economy? Has it made U.S. economic growth less dependent on debt-financed and wealth-driven consumption? • To what extent does policy explain the kind of recovery the U.S. economy has had? What were the main shortcomings of policy?

2

3

Part I: The Deleveraging Experience: Has America Fully De-Levered?

Part II: The Recovery: What Kind of Recovery?

Part III: Policy: Explaining the Deleveraging and Recovery We Got

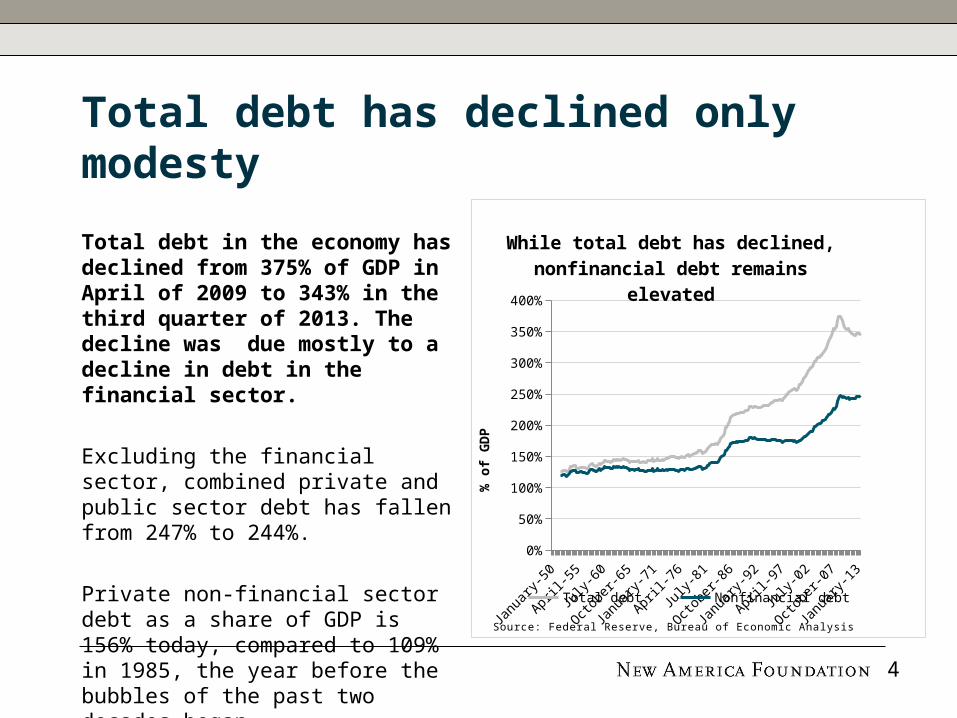

Total debt has declined only modesty

Total debt in the economy has declined from 375% of GDP in April of 2009 to 343% in the third quarter of 2013. The decline was due mostly to a decline in debt in the financial sector.

Excluding the financial sector, combined private and public sector debt has fallen from 247% to 244%.

Private non-financial sector debt as a share of GDP is 156% today, compared to 109% in 1985, the year before the bubbles of the past two decades began.

1950 1960 1970 1980 1990 2000 20100%

50%

100%

150%

200%

250%

300%

350%

400%

While total debt has declined, nonfinancial debt remains el-

evated

Total debt Nonfinancial debt

% o

f G

DP

Source: Federal Reserve, Bureau of Economic Analysis

4

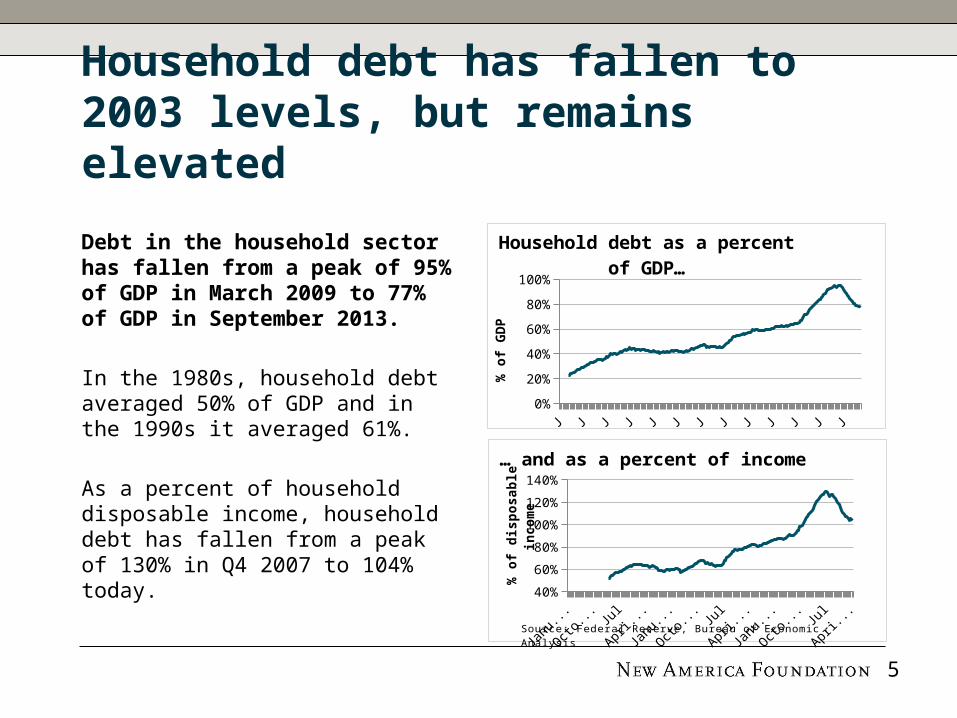

Household debt has fallen to 2003 levels, but remains elevated

Debt in the household sector has fallen from a peak of 95% of GDP in March 2009 to 77% of GDP in September 2013.

In the 1980s, household debt averaged 50% of GDP and in the 1990s it averaged 61%.

As a percent of household disposable income, household debt has fallen from a peak of 130% in Q4 2007 to 104% today.

1950 1960 1970 1980 1990 2000 20100%

20%

40%

60%

80%

100%

Household debt as a percent of GDP…

% o

f G

DP

1950 1960 1970 1980 1990 2000 201040%

60%

80%

100%

120%

140%

… and as a percent of income

% o

f dis

posa

ble

in

com

e

Source: Federal Reserve, Bureau of Economic Analysis

5

Other measures of deleveraging: low debt service burden and delinquency

Debt service has fallen from 13.2% of disposable income in 2007 to 9.9% today, due to low interest rates.

Mortgage delinquency rates (loans 30+ days past due) increased from 2% at the beginning of 2007 to 11.3% in the first quarter of 2010. Since then, they have fallen to 8.6%.

Only 2.5% of credit cards are today considered delinquent, the lowest rate on record. By these measures, the worst of the deleveraging is over.

1990 1995 2000 2005 20108%

10%

12%

14%

Household debt service burden

Source: Federal Reserve, Bureau of Economic Analysis

6

New credit growth for households, led by student loans

Household debt increased $127B in the third quarter of 2013 and $241B in the fourth quarter, the largest increase since the third quarter of 2007.

While household mortgage debt has declined, student debt has soared from $548B in the fourth quarter of 2007 to $1.08T, an increase of $533B.

Credit card loans have remained flat at around $700B since 2010, while auto loans have rebounded from $711B in the fourth quarter of 2010 to $863B today. 7

2007

2007

2008

2009

2010

2010

2011

2012

2013

2013

6.0

8.0

10.0

12.0

14.0

Household debt by instrument

Other

Student Loan

Credit Card

Auto Loan

HE Revolving

Mortgage

$T

Source: Federal Reserve Board of New York

Private sector deleveraging was made possible by an increase in public debt

The decline in private debt from 279% of GDP to 238% of GDP since 2007 was made possible by an increase in government debt.

Total government debt increased from 54% in the fourth quarter of 2007 to 90% in the first quarter of 2013. Since then, it has fallen to 88% of GDP.

State and local government debt, not including pension obligations, peaked in the first quarter of 2010 at 20.4% and has since declined to 17.5% of GDP.

1990 1995 2000 2005 201040%

50%

60%

70%

80%

90%

100%

110%

120%

Government leveraging, private sector deleveraging

GovernmentHouseholdsFinancial business

% o

f G

DP

Source: Federal Reserve, Bureau of Economic Analysis

8

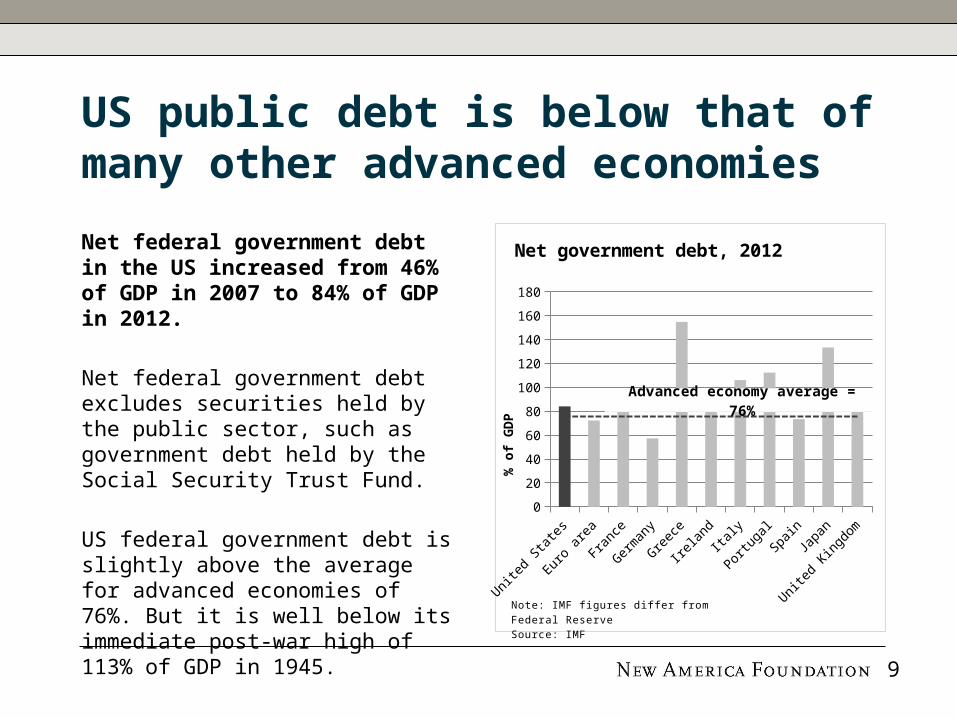

US public debt is below that of many other advanced economies

Net federal government debt in the US increased from 46% of GDP in 2007 to 84% of GDP in 2012.

Net federal government debt excludes securities held by the public sector, such as government debt held by the Social Security Trust Fund.

US federal government debt is slightly above the average for advanced economies of 76%. But it is well below its immediate post-war high of 113% of GDP in 1945.

Uni

ted

State

s

Euro

area

Franc

e

Germ

any

Greec

e

Irel

and

Italy

Portu

gal

Spain

Japa

n

Uni

ted

Kingd

om

0

20

40

60

80

100

120

140

160

180

Net government debt, 2012

% o

f G

DP

Note: IMF figures differ from Federal ReserveSource: IMF

Advanced economy average = 76%

9

The middle class remains burdened with debt

The bottom 95% have two times more debt than the top 5% of households.

The debt-to-income levels of the bottom 95% of households increased from 84% of disposable income in 1989 to 156% in 2007. The debt to income levels of the top 5% increased from 56% to 62%.

From 2007 to 2010, the bottom 95% of households have been forced to pay down debt and cut consumption, while the top 5% have taken on slightly more debt and increased consumption.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Debt-to-income

Bottom 95%

Top 5%

Source: Cynamon and Fazzari, “Inequality, the Great Recession, and Slow Recovery”

10

More private sector deleveraging is needed

Household debt is still higher than the pre-tech and housing bubble norm, and is only sustainable if interest rates remain low, housing prices continue to rise, and wages and incomes grow.

To get back to debt levels in 1996:• Households would have to reduce debt by $2.5T, or 15% of GDP• The financial sector would have to reduce by $4.5T, or 26% of GDP• And the non-financial business sector would have to reduce debt by $4.1T, or 24% of GDP

Gover

nmen

t

Hou

seho

lds

Finan

cial

bus

ines

s

Non

-fina

ncia

l bus

ines

s0%

10%20%30%40%50%60%70%80%90%

100%

Debt is high compared to the 1990s

19962013

% o

f G

DP

Source: Federal Reserve

11

12

Part I: The Deleveraging Experience: Has America Fully De-Levered?

Part II: The Recovery: What Kind of Recovery

Part III: Policy: Explaining the Deleveraging and Recovery We Got

Real GDP growth has been weak, weighed down by deleveraging

The economy returned to its 2007 peak of real output in the second quarter of 2011, and is currently 6.5% above its 2007 peak.

Recent growth has been slower than during previous recoveries. In the four and a half years since the recession ended, real GDP growth has averaged 2.4%.

In the four and half years following the recessions in 1982 and 1990, the average growth rate was 5% and 3.2%, respectively.

13

1 4 7 10 13 16 19 22 2590

95

100

105

110

115

120

125

The current recovery has been slow by historical

standards

1980199120012007

Quarters after business cycle peak

100=

busi

ness

cycle

peak

Source: Bureau of Economic Analysis

A still sizable output gap means the recovery is incomplete

The output gap—which is the difference between potential GDP and actual GDP—was 4.4% of GDP in the fourth quarter of 2013 ($740B), down from 7.4% in the third quarter of 2009.

Premature fiscal consolidation beginning in 2010 has kept the output gap larger than it would otherwise have been, costing the economy over this time hundreds of billions of dollars in lost income and millions of jobs.

14

2007

2008

2009

2010

2012

2013

2014

2015

2017

2018

2019

2020

10,000

12,000

14,000

16,000

18,000

20,000

Output gap

Actual GDPProjected GDPPotential GDP

2009 $

T

Source: Congressional Budget Office

The official unemployment rate declined from a peak of 10% in October 2009 to 6.6% in January 2014.

Including workers that are marginally attached to the workforce and those that are employed part-time for economic reasons, the U-6 unemployment rate is 12.7%, down from a peak of 17.2% in April 2010.

The labor force participation rate has declined from 66% before the recession to 63% today.

1990 1995 2000 2005 20100%

5%

10%

15%

20%

Unemployment rate

U-6*

Of-fi-cial rate

*Total unemployed, plus all marginally attached workers plus total employed part time for economic reasonsSource: Bureau of Labor Statistics

15

The unemployment rate has fallen, in part due to lower participation in the labor force

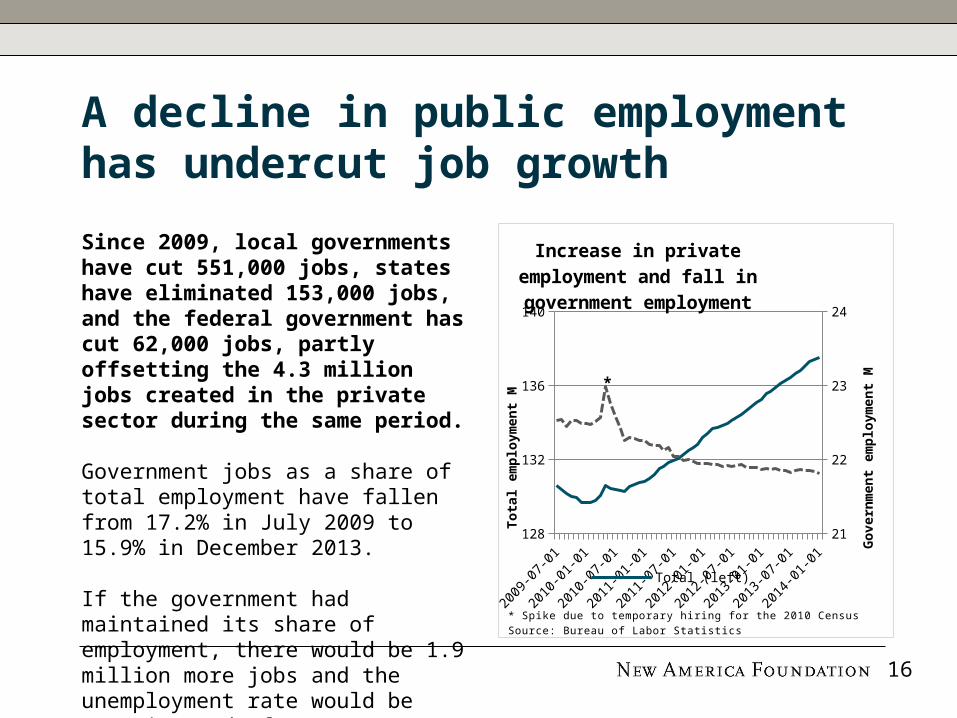

A decline in public employment has undercut job growth

Since 2009, local governments have cut 551,000 jobs, states have eliminated 153,000 jobs, and the federal government has cut 62,000 jobs, partly offsetting the 4.3 million jobs created in the private sector during the same period.

Government jobs as a share of total employment have fallen from 17.2% in July 2009 to 15.9% in December 2013.

If the government had maintained its share of employment, there would be 1.9 million more jobs and the unemployment rate would be 5.4% instead of 6.6%.

16

2009 2010 2011 2012 2013128

132

136

140

21

22

23

24

Increase in private employ-ment and fall in government

employment

Total (left)

Tota

l em

plo

ym

ent

M

Govern

ment

em

plo

ym

ent

M

* Spike due to temporary hiring for the 2010 CensusSource: Bureau of Labor Statistics

*

According to Daniel Alpert, 54% of the jobs created in 2013 were low-wage jobs, well above the percentage of low-wage jobs in the economy at the start of the year.

The BLS projects that many of the fastest growing categories of jobs in the period 2012-2022 will be in low-wage sectors like retail, food service, and personal care.

For example, the number of software developers in the higher wage tech sector is expected to increase by 140K, compared to 580K personal care aides.

100 200 300 400 500 600 7000

20,000

40,000

60,000

80,000

100,000

120,000

Personal care aides

Registered nurses

Retail

Home health aides

Food service

General managers

Software developers

Employment growth 2012-2022, and 2012 median

annual wage

‘000s of jobs created 2012-2022

2012 m

edia

n i

nco

me

$

Source: Bureau of Labor Statistics

Private-sector job growth has been mostly in

low-wage jobs

17

Many unemployed workers have left the labor force

The drop in the unemployment rate has been the result of private sector job creation (in mostly low-wage jobs) and workers leaving the labor force.

The average unemployed worker has been unemployed for 35 weeks—far above other recoveries.

The labor force participation rate is 63%, down from a peak of 67% in the late 1990s. Some of the decline is due to the aging of the population, but prolonged periods of unemployment can also cause people to give up looking for a job.

18

1990 1995 2000 2005 20100.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Average duration of un-employment

Source: Bureau of Labor Statistics

Unemployment disproportionately impacts the younger generation

The unemployment rate for 16-19 year olds has fallen from a peak of 27.2% in October 2009 to 20.7% today. The rate for 20-24 year olds has fallen from 17.2% in April 2010 to 11.9% today.

In 1996, the unemployment rates for 16-19 year olds and 20-24 year olds were 16.7% and 9.3%, respectively.

According to the Center for American Progress, long-term unemployment will result in $22,000 in lost earnings during the next decade for each of the million young workers who have experienced long-term unemployment.

1990 1995 2000 2005 20100%

5%

10%

15%

20%

25%

30%

Youth unemployment

16-19 20-24 25+

Source: Bureau of Labor Statistics

19

Real wages have been essentially flat

Real wages have not increased during the recovery because of high levels of unemployment and because of the increase in the proportion of low-wage jobs.

Real wages increased 3.9% in 2008, mostly due to a 3.5% decline in prices. Since then, wages have declined by 1%.

Since the end of the recession, retail trade employment increased by 734K but wages declined 1%. During the same period, leisure and hospitality jobs increased 962K, but wages fell 3.7%.

22.500

23.000

23.500

24.000

24.500

25.000

Real wages in the private sector

Source: Bureau of Labor Statistics

20

Median household income has fallen, even with the recovery

Median income declined during the recovery from $53,285 in 2009 to $51,017 in 2012.

Today median household income is 9% lower than it was at its peak of $56,080 in 1999.

Households income:• At the 20th percentile was $20,599• At the 40th percentile was $39,764• At the 60th percentile was $64,582• And at the 80th percentile was $104,096

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

44,000

46,000

48,000

50,000

52,000

54,000

56,000

58,000

Median household income

2012 $

Source: US Census Bureau

21

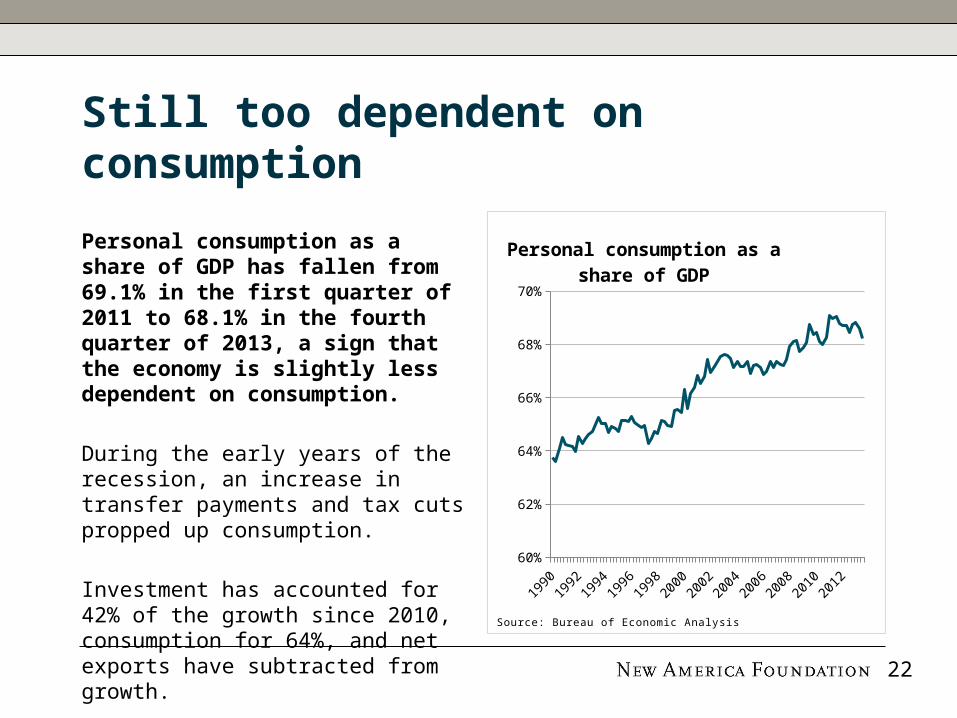

Still too dependent on consumption

Personal consumption as a share of GDP has fallen from 69.1% in the first quarter of 2011 to 68.1% in the fourth quarter of 2013, a sign that the economy is slightly less dependent on consumption.

During the early years of the recession, an increase in transfer payments and tax cuts propped up consumption.

Investment has accounted for 42% of the growth since 2010, consumption for 64%, and net exports have subtracted from growth.

1990

1991

1993

1995

1997

1998

2000

2002

2004

2005

2007

2009

2011

2012

60%

62%

64%

66%

68%

70%

Personal consumption as a share of GDP

Source: Bureau of Economic Analysis

22

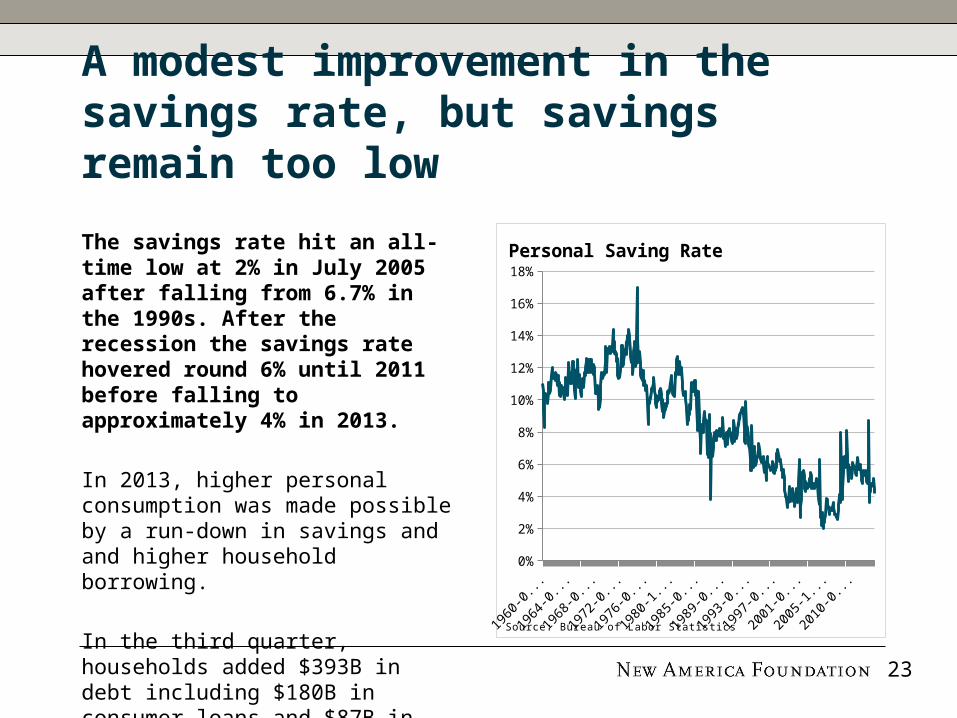

A modest improvement in the savings rate, but savings remain too low

The savings rate hit an all-time low at 2% in July 2005 after falling from 6.7% in the 1990s. After the recession the savings rate hovered round 6% until 2011 before falling to approximately 4% in 2013.

In 2013, higher personal consumption was made possible by a run-down in savings and and higher household borrowing.

In the third quarter, households added $393B in debt including $180B in consumer loans and $87B in mortgages.

1960 1970 1980 1990 2000 20100%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Personal Saving Rate

Source: Bureau of Labor Statistics

23

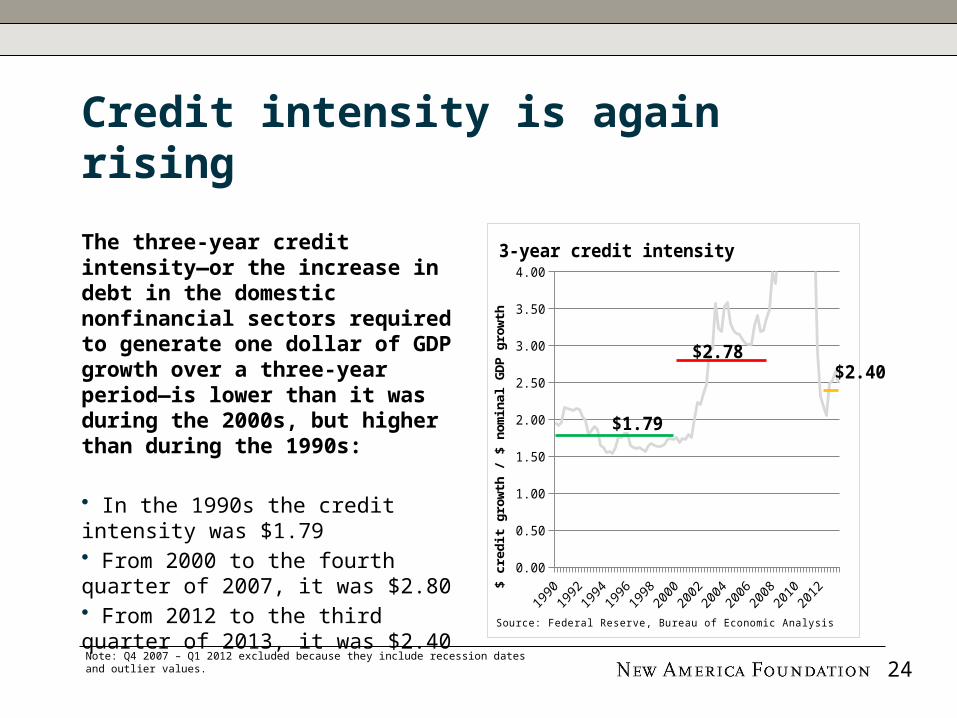

Credit intensity is again rising

The three-year credit intensity—or the increase in debt in the domestic nonfinancial sectors required to generate one dollar of GDP growth over a three-year period—is lower than it was during the 2000s, but higher than during the 1990s:

• In the 1990s the credit intensity was $1.79 • From 2000 to the fourth quarter of 2007, it was $2.80 • From 2012 to the third quarter of 2013, it was $2.40Note: Q4 2007 – Q1 2012 excluded because they include recession dates and outlier values. 24

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

$1.79

$2.78$2.40

3-year credit intensity

$ c

redit

gro

wth

/ $

nom

inal

GD

P g

row

th

Source: Federal Reserve, Bureau of Economic Analysis

A weak recovery in investment and capital expenditure

Fixed investment was $2.5T (2009 dollars) in the fourth quarter of 2013. This is $200B below the peak in the first quarter of 2006.

Fixed investment growth has slowed since the years immediately after the recession, growing 4.5% from 2012 to 2013. Business investment in equipment and software increased 3.1%.

Companies are sitting on cash rather than investing. The ratio of cash to net assets among U.S. non-financial non-utility companies is approximately 12%, double the rate during the 1990s.

2007

2007

2008

2008

2009

2009

2010

2010

2011

2011

2012

2012

2013

2013

1,500

1,700

1,900

2,100

2,300

2,500

2,700

Gross fixed investment

2009 $

B

Source: Bureau of Economic Analysis

25

Government investment has fallen

Net government investment has fallen from 1.4% of GDP in 2009 to 0.8% of GDP in 2012. State and local governments invested 0.6% of GDP in 2012, the lowest investment share since 1947.

Gross government investment, before accounting for depreciation, is currently 3.8% of GDP, the lowest rate since 1948.

The government invests 0.6% of GDP in structures, 0.1% of GDP in equipment, and 0.1% in intellectual property.

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Net government investment

State & Local Federal defense

% o

f G

DP

Source: Bureau of Economic Analysis

26

Private investment has only modestly rebounded

Net private nonresidential investment in fixed assets declined to 0.6% of GDP in 2009, its lowest level in six decades.

Since 2009, investment has rebounded to 1.8% of GDP, which is still lower than any level seen since World War II.

As a result of systemic under-investment in the economy, the age of private fixed assets has risen to 21.7 years, the highest rate since the late 1950s.

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Private nonresidential net investment

% o

f G

DP

Source: Bureau of Economic Analysis

27

Productivity growth has declined

Annual labor productivity growth was 1.7% at year-end 2013, 0.9% in 2012, and 0.4% in 2011.

During the current recovery, productivity growth has averaged 1.8% (red), while after the 1982 recession and 2001 recession productivity averaged 2.5% and 3.1%, respectively. 20

0820

0820

0920

1020

1120

1120

1220

13-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Productivity growth

productiv-ity growth

post-2007

post-2001

post-1982

Annual

% c

hange

Source: Bureau of Labor Statistics

The slow recovery has depressed the pace of capital accumulation, and it may also have hindered new business formation and innovation, developments that would have an adverse effect on structural productivity.

- Janet Yellen, Chair, Federal Reserve28

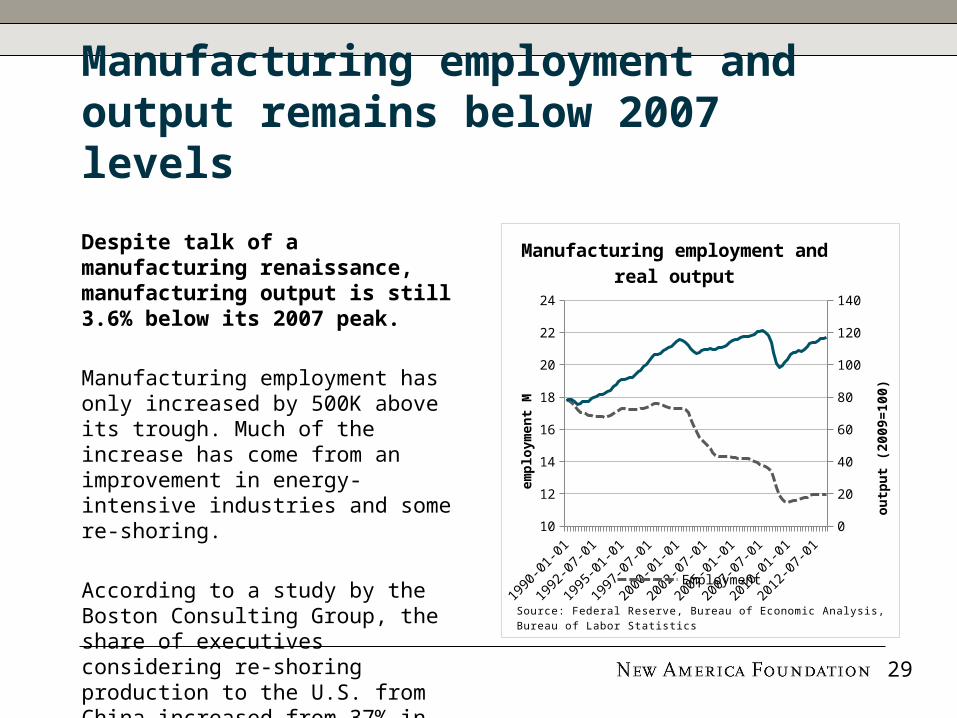

Manufacturing employment and output remains below 2007 levels

Despite talk of a manufacturing renaissance, manufacturing output is still 3.6% below its 2007 peak.

Manufacturing employment has only increased by 500K above its trough. Much of the increase has come from an improvement in energy-intensive industries and some re-shoring.

According to a study by the Boston Consulting Group, the share of executives considering re-shoring production to the U.S. from China increased from 37% in 2012 to 54% in 2013.

1990 1995 2000 2005 201010

12

14

16

18

20

22

24

0

20

40

60

80

100

120

140

Manufacturing employment and real output

Employment

em

plo

ym

ent

M

outp

ut

(2009=

100)

Source: Federal Reserve, Bureau of Economic Analysis, Bureau of Labor Statis-tics

29

A modest improvement in net exports

The trade deficit shrunk from 5.1% of GDP in 2008 to 2.6% of GDP today.

From the fourth quarter of 2007 to the fourth quarter of 2014, exports grew from 12.0% to 13.6% of GDP, while imports fell from 16.7% to 16.2% of GDP.

The decline in the trade deficit contributed to an increase in GDP in 2008-2009, but since has not contributed much.

30

2007

2007

2008

2008

2009

2009

2010

2010

2011

2011

2012

2012

2013

2013

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

Net export share of GDP

% o

f G

DP

Source: Bureau of Economic Analysis

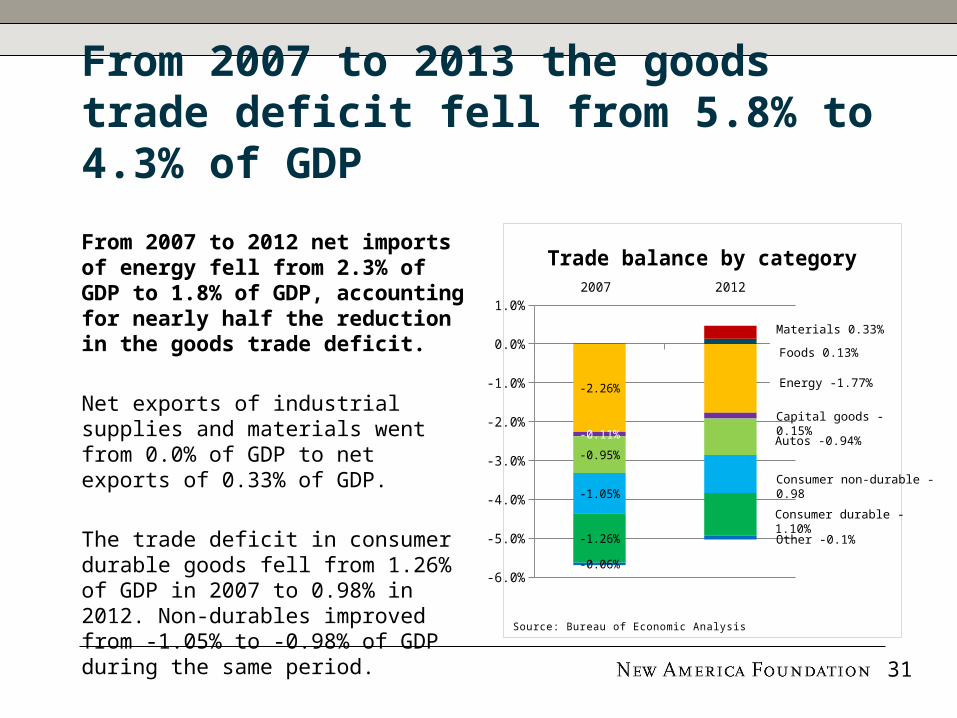

From 2007 to 2013 the goods trade deficit fell from 5.8% to 4.3% of GDP

From 2007 to 2012 net imports of energy fell from 2.3% of GDP to 1.8% of GDP, accounting for nearly half the reduction in the goods trade deficit.

Net exports of industrial supplies and materials went from 0.0% of GDP to net exports of 0.33% of GDP.

The trade deficit in consumer durable goods fell from 1.26% of GDP in 2007 to 0.98% in 2012. Non-durables improved from -1.05% to -0.98% of GDP during the same period.

2007 2012

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

-2.26%

-0.11%

-0.95%

-1.05%

-1.26%

-0.06%

Trade balance by category

Source: Bureau of Economic Analysis

31

Materials 0.33%

Foods 0.13%

Energy -1.77%

Capital goods -0.15%

Autos -0.94%

Consumer non-durable -0.98

Consumer durable -1.10%Other -0.1%

Energy has been a bright spot in the economic recovery

The oil and gas boom has lowered the cost of energy and increased American competitiveness in sectors from energy to manufacturing. The domestic energy boom is also inherently supportive of middle-class prosperity because it creates good-paying middle-class jobs and strengthens the tradable sector.

While total nonfarm employment has not surpassed its pre-recession levels, employment in oil and gas extraction increased 34% from 2007 to 2014 and support activities have increased 37%. 32

2007 2008 2009 2010 2011 2012 201380

90

100

110

120

130

140

Index of employment in oil and gas extraction and

support activities

Extraction Support activitiesTotal employment

Dec 2

007 =

100

Source: Bureau of Labor Statistics

An uneven and not yet sustainable housing recovery

Housing prices have rebounded 24% from the post-recession lows in March 2012, according to the Case-Shiller index.

Since reaching a high in November 2013 at 1.1M, housing starts have fallen to 880,000. The number of homes for sale, or inventories, has declined from a peak of 3.5M in 2007 to 1.9M in 2013.

The housing recovery has been held back by lack of first-time home buyers owing to high levels of unemployment and low rates of household formation.

0

50

100

150

200

250

Case-Shiller Index

Source: S&P

33

This has been a wealth-driven recovery

Household net worth increased $21.5T from $55.7T in the first quarter of 2009 to $77.3T in the third quarter of 2013.

$2.7T of the increase was due to the increase in real estate, while $18T, or 84% of the increase, was due to a rise in the value of financial assets, including deposits, stocks, and pensions.

The S&P peaked at 1565 in October 2007 and fell to 677 in March 2009. Since then, it has risen to 1859—170% above the trough and 17% above its previous peak.

1990 2000 20100

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Household net worth

$B

Source: Federal Reserve

34

In 2013, expansion of the trailing P/E multiple from 16.5x to 19.6x accounted for two thirds of the increase in the S&P.

Higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.

- Ben Bernanke

Low interest rates enable corporations to borrow cheaply and buy back shares. S&P 500 companies did $346B of buybacks in the first three quarters of 2013, effectively paying out 3% to shareholders.

Stock market recovery: multiple expansion, Fed Policy, and share buybacks

35

2009 2010 2011 2012 Q1 to Q3 2013

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

S&P share buybacks

Source: Standard & Poor’s

Inequality has increased

Income inequality is at all-time highs:• Top 10% earn 48.2% of total income• Top 1% earn 19.3% of total income• Top 0.1% earn 8.8% of income

From 2009 to 2012, the top 1% has captured 95% of the increase in national income.

In other words, the top 1% of incomes grew by 31.4% while bottom 99% incomes increased by 0.4%.

36

1922

1930

1938

1946

1954

1962

1970

1978

1986

1994

2002

2010

0

10

20

30

40

50

60

Income share of top earners

Top 10%

Top 1%

Top 0.1%

Top 0.01%

Source: Piketty and Saez

The rise of the American plutonomy: an economy driven by high-end consumption

Consumption growth by top-earners has driven the recovery: consumption for households in the top 5% of incomes increased 16% from 2007 to 2012, while consumption by the bottom 95% fell by 2%.

In 2012 the top 5% of earners were responsible for 38% of domestic consumption, up from 28% in 1995 and 34% in 2007.

37

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

0%

5%

10%

15%

20%

25%

30%

35%

40%

Consumption share of the top 5%

Source: Cynamon and Fazzari, “Inequality, the Great Recession, and Slow Recovery”

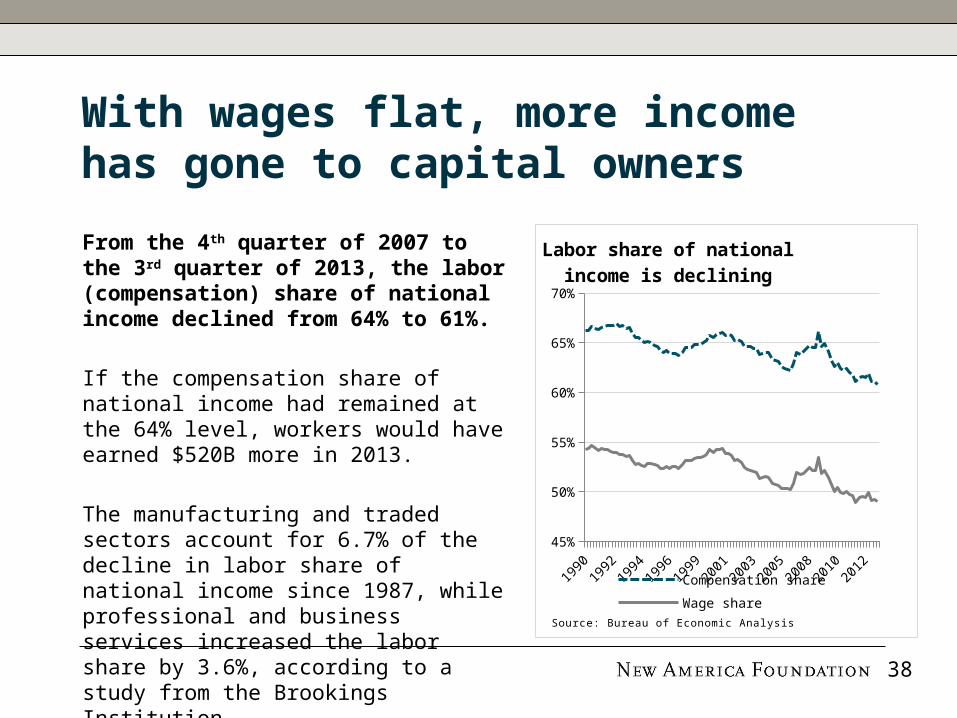

With wages flat, more income has gone to capital owners

From the 4th quarter of 2007 to the 3rd quarter of 2013, the labor (compensation) share of national income declined from 64% to 61%.

If the compensation share of national income had remained at the 64% level, workers would have earned $520B more in 2013.

The manufacturing and traded sectors account for 6.7% of the decline in labor share of national income since 1987, while professional and business services increased the labor share by 3.6%, according to a study from the Brookings Institution.

1990

1991

1993

1995

1997

1998

2000

2002

2004

2005

2007

2009

2011

2012

45%

50%

55%

60%

65%

70%

Labor share of national income is declining

Compensation share

Wage shareSource: Bureau of Economic Analysis

38

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

Households with head of household 25 years or

younger

House

hold

s ‘0

00s

Source: US Census

A tough start for younger Americans

Households with a head of household 25 years or younger declined from 6.6M in 2006 to 6.1M in 2012.

The 500,000 decline in households with heads of households 25 or younger indicates that many youth have moved back in with their parents.

In part due to the weak labor market, many youth have gone back to school. This and high tuition costs have burdened youth with $1.2T in student loans.

39

40

Part I: The Deleveraging Experience: Has America Fully De-Levered?

Part II: The Recovery: What Kind of Recovery?

Part III: Policy: Explaining the Deleveraging and Recovery We Got

Outcomes reflect policy decisions

Monetary reflation and Wall Street

bailout

Recovery of financial assets and profits

Tax cuts and unemployment

insurance

(Temporary) support of consumer spending

Modest infrastructure and

public works spending

Weak job creation and stagnant wages

Policy gridlock and weak demand

Weak private investment and slower productivity growth

Policy Choice Result

41

Monetary reflation and the wealth effect:QE is the ultimate trickle down

The Fed has expanded its balance sheet to more than $4 trillion (or 24% of GDP) by buying Treasuries and Mortgage-Backed Securities.

Quantitative easing is the ultimate trickle-down economic policy: it has caused huge gains in the stock market and boosted housing. But it has done little to create real wage growth.

Since the recession ended in 2009, the S&P has increased 90%, housing has gained 16%, and real wages have increased only 0.5%. 42

2009 2010 2011 2012 201380

100

120

140

160

180

200

2.0

2.5

3.0

3.5

4.0

4.5

5.0

QE pushes stocks up more than housing and housing

more than wages

Federal Reserve assets (right)S&P500 (left)Case-Shiller 20-city (left)Real Wages (left)

Index (

July

2009=

100)

$T

Source: Federal Reserve, Bureau of Labor Statistics, Standard and Poor’s

Transfer payments temporarily supported household income and consumption

Transfer payments temporarily supported household income during the recession, but unemployment insurance and other benefits have fallen $102B and $30B in real terms since the beginning of 2010.

The decline in temporary benefits has hit working-age and middle-class populations the hardest.

Transfer payments as a share of income have declined from 18.1% in the first quarter of 2010 to 17.0% today.

2000

2001

2003

2004

2006

2007

2009

2010

2012

2013

0

100

200

300

400

500

600

700

800

900

Government Benefits

Social se-curity

Medicare

Medicaid

Unem-ployment insurance

Veterans' benefits

Other

$B

Source: Bureau of Economic Analysis

43

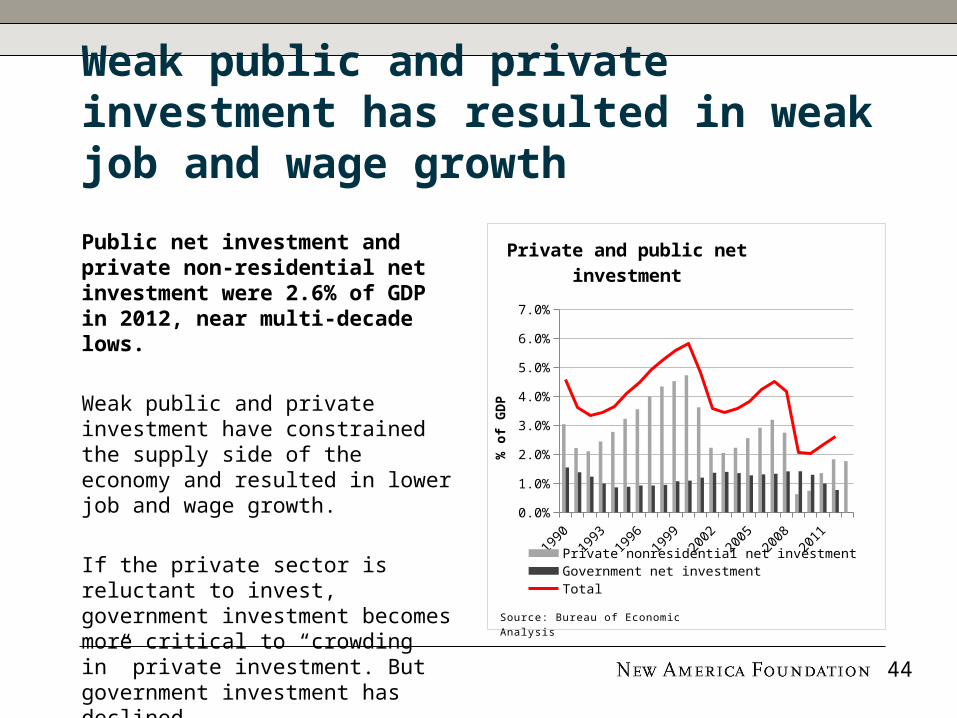

Weak public and private investment has resulted in weak job and wage growth

Public net investment and private non-residential net investment were 2.6% of GDP in 2012, near multi-decade lows.

Weak public and private investment have constrained the supply side of the economy and resulted in lower job and wage growth.

If the private sector is reluctant to invest, government investment becomes more critical to “crowding in” private investment. But government investment has declined.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Private and public net investment

Private nonresidential net investmentGovernment net investmentTotal

% o

f G

DP

Source: Bureau of Economic Analysis

44

Weak capital investment has also meant slower productivity growth

Weak investment has resulted in slower productivity growth, reducing the economy’s longer term growth potential.

The average age of fixed assets in the United States is 21.7 years—11% higher than the average during the 1990s.

If workers have permanently left the labor force and the capital stock has deteriorated and not been replaced by new investment, the supply side of the economy will be a constraint on growth when demand increases.

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

17

18

19

20

21

22

Age of private fixed assets

Age i

n y

ears

Source: Bureau of Economic Analysis

45

Weak global growth has meant limited improvement in net exports

The rest of the world has made it more difficult for the United States to adjust away from consumption toward greater investment and production.

The trade deficit with the euro area has recently expanded to 0.42% of GDP, from 0.2% of GDP in 2009 because the euro area has grown slowly and moved to a large current account surplus.

The trade deficit with China is 1.8% of GDP, and has begun to widen again to near its all-time high. 46

2001

2002

2003

2004

2006

2007

2008

2009

2011

2012

2013

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

Trade balance with the EU and China

EU

% o

f U

S G

DP

Source: Bureau of Economic Analysis

47

Visit New America’s Economic Growth Program online: growth.newamerica.org

For media inquiries, contact Jenny Mallamo at:[email protected]