The “Unconventional” O&G Revolution: Another Look Under ...

23

The “Unconventional” O&G Revolution: Another Look Under the Hood Pete Stark, Senior Research Director and Advisor IHS CERA RCP Sponsors Meeting Colorado School of Mines October 25, 2013 CONFIDENTIAL © 2012, All rights reserved, Cambridge Energy Research Associates, Inc., 55 Cambridge Parkway, Cambridge, Massachusetts 02142 No portion of this presentation may be reproduced, reused or otherwise distributed in any form without prior written consent.

Transcript of The “Unconventional” O&G Revolution: Another Look Under ...

The “Unconventional” O&G Revolution: Another Look Under the Hood

Pete Stark,

Senior Research Director and Advisor

IHS CERA

RCP Sponsors Meeting

Colorado School of Mines

October 25, 2013

CONFIDENTIAL

© 2012, All rights reserved, Cambridge Energy Research Associates, Inc., 55 Cambridge Parkway, Cambridge, Massachusetts 02142

No portion of this presentation may be reproduced, reused or otherwise distributed in any form without prior written consent.

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013 1

Terms of Use

• CERA content and information, including but not limited to graphs, charts, tables, figures,

and data, are not to be disseminated outside of a client organization to any third party,

including a client’s customers, financial institutions, consultants, or the public.

• Content distributed within the client organization must display CERA’s legal notices and

attributions of authorship.

The accompanying materials were prepared by Cambridge Energy Research Associates, Inc. (CERA),

and are not to be redistributed or reused in any manner without prior written consent, with the exception

of client internal distribution as described below.

CERA strives to be supportive of client internal distribution of CERA content but requires that

Some information supplied by CERA may be obtained from sources that CERA believes to be reliable

but are in no way warranted by CERA as to accuracy or completeness. Absent a specific agreement to

the contrary, CERA has no obligation to update any content or information provided to a client.

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

What if the Unconventional Revolution - - -

Did Not Happen?

• Avg. annual household disposable income would be $1,200 less

• Your natural gas and power bills would be 2X to 3X higher

• US would import 14-16 Bcfd, cost ~ $12/Mcf or $70 billion/year

• US would import >10.5 Mmbod, cost ~ $140/bbl or $127 billion/yr

• Gasoline would cost ~ $5 / gallon

• 2.1 million additional Americans would not have jobs; rate ~ 8.6%

• Loss of $2.4 trillion in O&G capital investment through 2025

• No US manufacturing renaissance (+3.9% to 2025)

• Loss of ~ $3.3 trillion to US GDP 2010-2020

US 2013 GDP would be 3% less – in recession?

• 12% drop in 2012 US GHG emissions would not have happened

2

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013 3

The Market Environment

• Multi-speed global recovery

• 2012 U.S. GDP 2.2%

• 2012 (Sept) Henry Hub at

$2.82 per Mcf

• Storage = 3,715 bcf

• WTI oil price at $91.08 / bbl

• Rigs: Oil Gas Horiz %

1410 427 1114 61%

• U.S. only moderate growth

• 2013 U.S. GDP ~ 1.5%

• 2013 (Sept) Henry Hub at

$3.62 per Mcf

• Storage = 3,577 bcf (- 3.7%)

• WTI oil price at $102.49 / bbl

• Rigs: Oil Gas Horiz %

1361 372 1099 63%

What has changed since 2012?

Source: IHS Cambridge Energy Research Associates.

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

U.S. 2012 Completions with Resource Plays

4

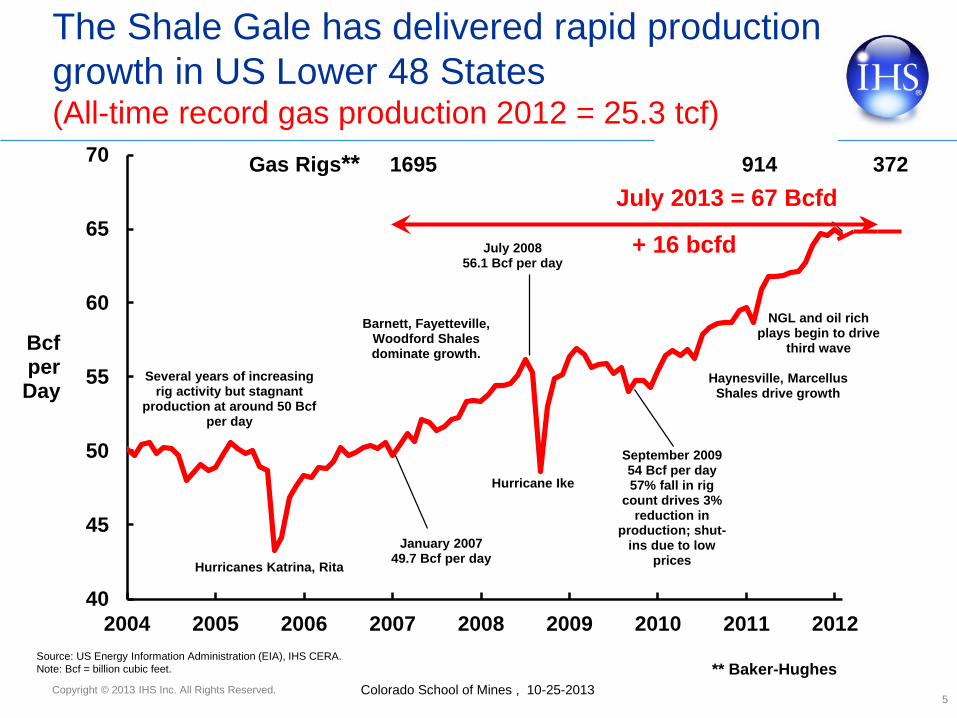

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

40

45

50

55

60

65

70

2004 2005 2006 2007 2008 2009 2010 2011 2012

BcfperDay

Several years of increasing rig activity but stagnant

production at around 50 Bcf per day

Hurricanes Katrina, Rita

Barnett, Fayetteville, Woodford Shales dominate growth.

January 200749.7 Bcf per day

Hurricane Ike

July 200856.1 Bcf per day

September 200954 Bcf per day57% fall in rig

count drives 3% reduction in

production; shut-ins due to low

prices

Haynesville, Marcellus Shales drive growth

NGL and oil rich plays begin to drive

third wave

February 201264.5 Bcf per day

Source: US Energy Information Administration (EIA), IHS CERA.

The Shale Gale has delivered rapid production

growth in US Lower 48 States (All-time record gas production 2012 = 25.3 tcf)

5

Source: US Energy Information Administration (EIA), IHS CERA.

Note: Bcf = billion cubic feet.

July 2013 = 67 Bcfd

+ 16 bcfd

Gas Rigs** 1695 914 372

** Baker-Hughes

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

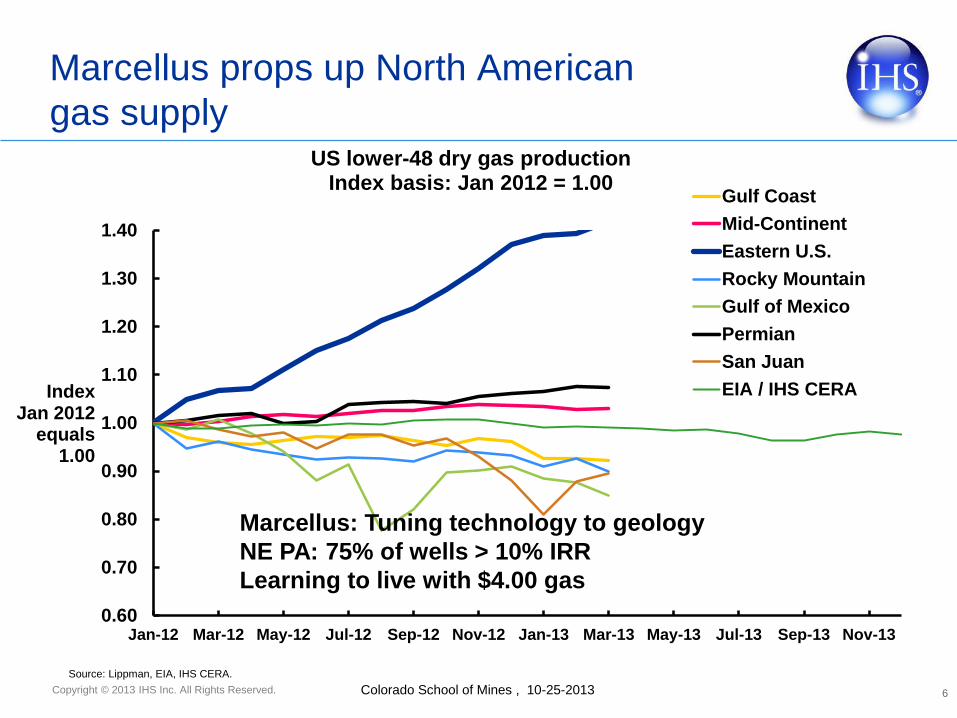

Marcellus props up North American

gas supply

6

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Nov-13

Index Jan 2012

equals 1.00

US lower-48 dry gas production Index basis: Jan 2012 = 1.00

Gulf Coast

Mid-Continent

Eastern U.S.

Rocky Mountain

Gulf of Mexico

Permian

San Juan

EIA / IHS CERA

Source: Lippman, EIA, IHS CERA.

Marcellus: Tuning technology to geology

NE PA: 75% of wells > 10% IRR

Learning to live with $4.00 gas

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

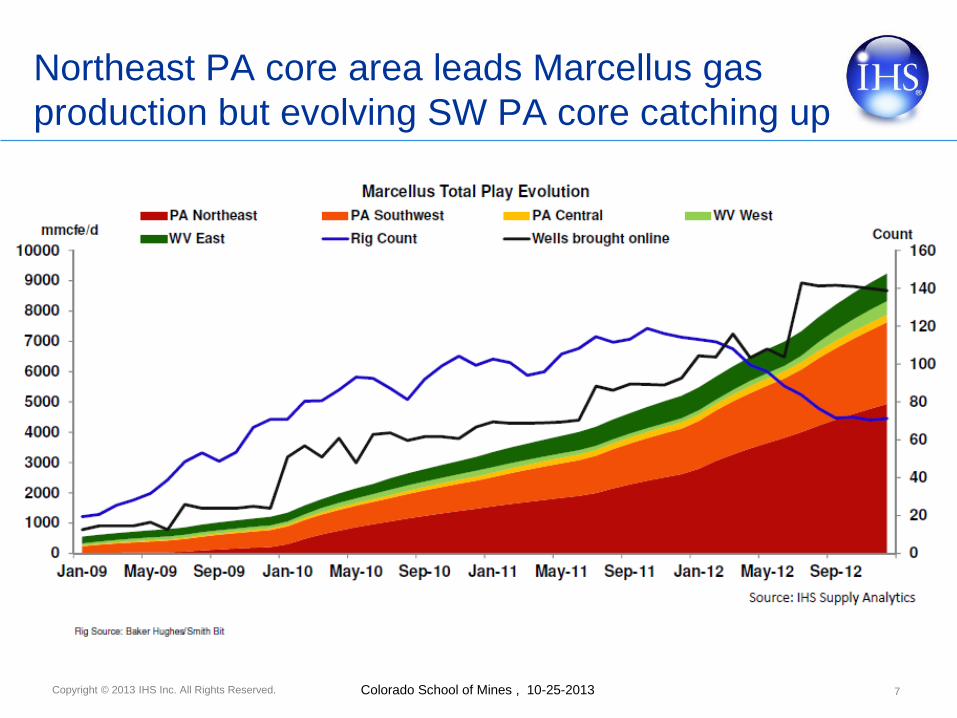

Northeast PA core area leads Marcellus gas

production but evolving SW PA core catching up

7

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

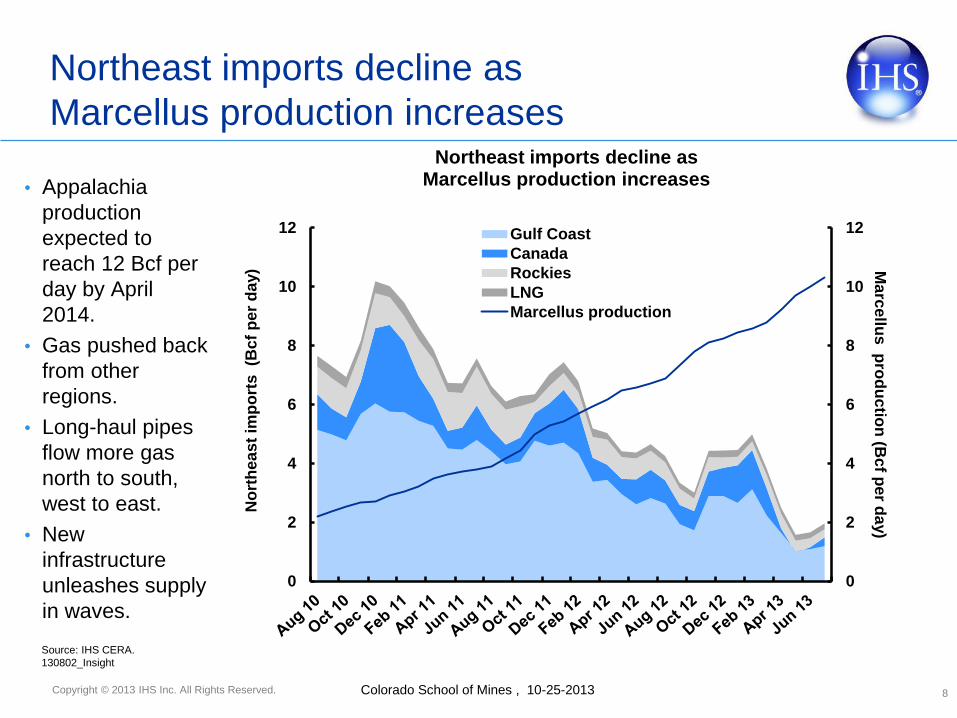

• Appalachia

production

expected to

reach 12 Bcf per

day by April

2014.

• Gas pushed back

from other

regions.

• Long-haul pipes

flow more gas

north to south,

west to east.

• New

infrastructure

unleashes supply

in waves.

Northeast imports decline as

Marcellus production increases

8

0

2

4

6

8

10

12

0

2

4

6

8

10

12

Ma

rce

llus p

rod

uc

tion

(Bcf p

er d

ay)

No

rth

ea

st

imp

ort

s (B

cf

pe

r d

ay)

Northeast imports decline as Marcellus production increases

Gulf Coast

Canada

Rockies

LNG

Marcellus production

Source: IHS CERA.

130802_Insight

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

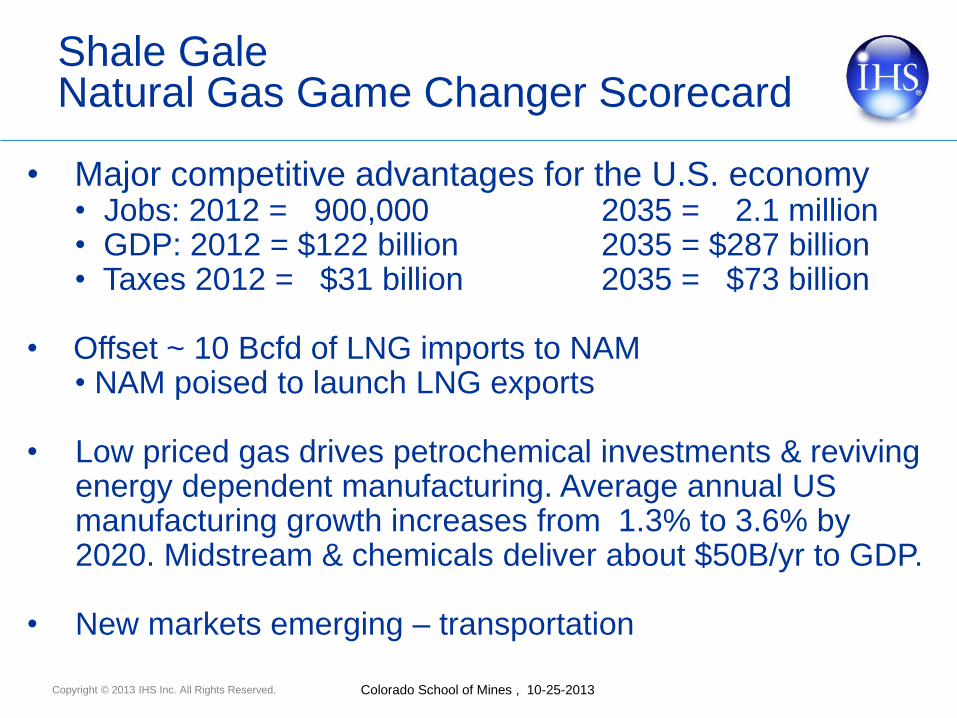

Shale Gale Natural Gas Game Changer Scorecard

• Major competitive advantages for the U.S. economy • Jobs: 2012 = 900,000 2035 = 2.1 million • GDP: 2012 = $122 billion 2035 = $287 billion • Taxes 2012 = $31 billion 2035 = $73 billion

• Offset ~ 10 Bcfd of LNG imports to NAM • NAM poised to launch LNG exports

• Low priced gas drives petrochemical investments & reviving energy dependent manufacturing. Average annual US manufacturing growth increases from 1.3% to 3.6% by 2020. Midstream & chemicals deliver about $50B/yr to GDP.

• New markets emerging – transportation

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

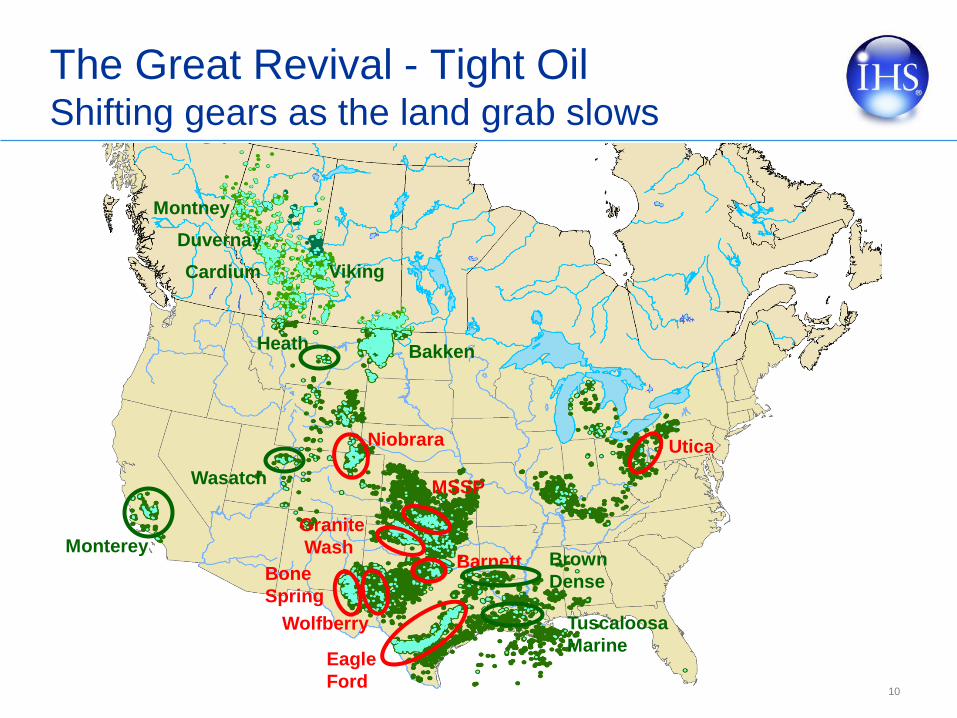

The Great Revival - Tight Oil Shifting gears as the land grab slows

10

Niobrara Utica

MSSP

Granite

Wash

Wolfberry

Eagle

Ford

Barnett Bone

Spring

Brown

Dense

Tuscaloosa

Marine

Wasatch

Monterey

Heath Bakken

Montney

Viking Cardium

Duvernay

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

U.S. liquids production could exceed 1970’s

peak, and reverse four decades of decline. 2012 record ~ 1 MMb/d liquids production growth!

• Reversing a trend that spanned

the previous four decades, U.S.

liquids production is expected to

regain and overtake its 1970

peak by 2020.

• Driven solely by the growth in

tight oil and wet gas plays, total

liquids production could

potentially reach >11.5

mmboe/d by the end of this

decade.

0

2

4

6

8

10

12

1960 1970 1980 1990 2000 2010 2020

mmboe/d U.S. Oil and NGL Production: 1960 – 2020

Conventional Oil NGLs Tight Oil

Source: Supply Analytics, North American Crude Oil Markets

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

Outside of the Bakken – Three Forks and Eagle Ford

plays, there is more gas and lower IP rates

12

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

200

400

600

800

1,000

1,200

1,400

% Gas boe/d

Avg. Peak Mo. Oil Rate (bbl/d) Avg. Peak Mo. Gas Rate (boe/d) % Gas

Source: Supply Analytics

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

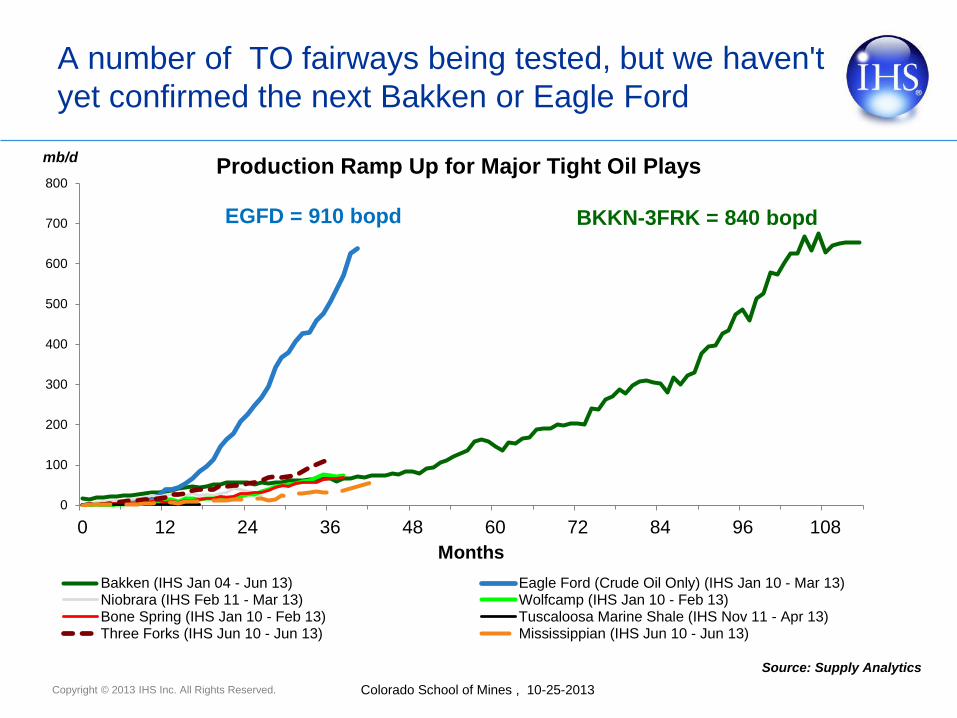

A number of TO fairways being tested, but we haven't

yet confirmed the next Bakken or Eagle Ford

0

100

200

300

400

500

600

700

800

0 12 24 36 48 60 72 84 96 108

mb/d

Months

Production Ramp Up for Major Tight Oil Plays

Bakken (IHS Jan 04 - Jun 13) Eagle Ford (Crude Oil Only) (IHS Jan 10 - Mar 13)Niobrara (IHS Feb 11 - Mar 13) Wolfcamp (IHS Jan 10 - Feb 13)Bone Spring (IHS Jan 10 - Feb 13) Tuscaloosa Marine Shale (IHS Nov 11 - Apr 13)Three Forks (IHS Jun 10 - Jun 13) Mississippian (IHS Jun 10 - Jun 13)

Source: Supply Analytics

EGFD = 910 bopd BKKN-3FRK = 840 bopd

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

Bakken sub-plays based on

peak production / 1000 lateral ft.

14

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

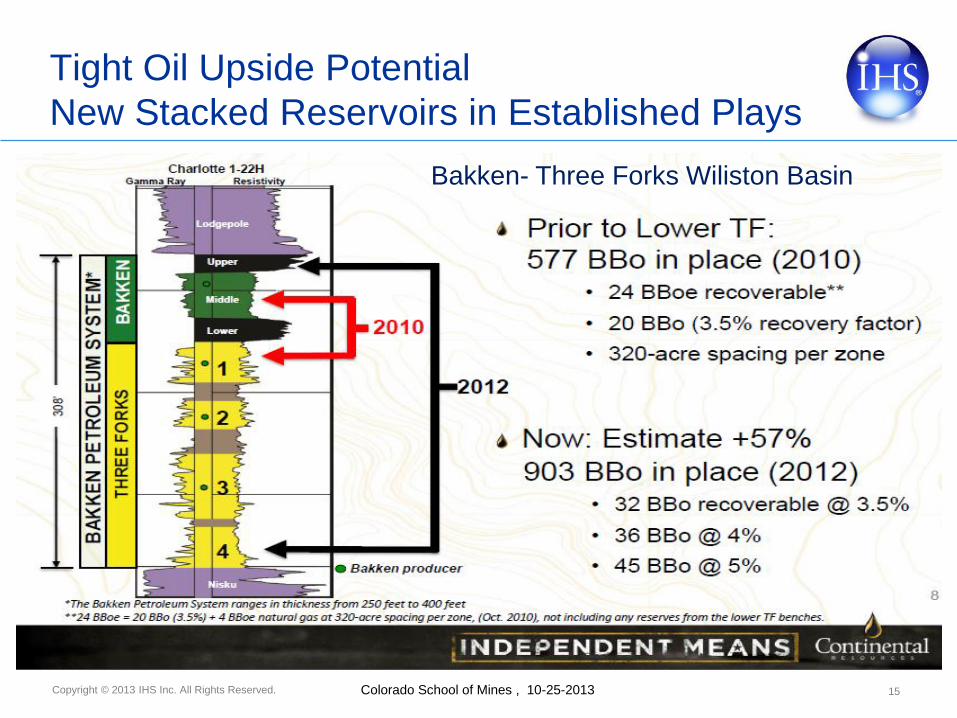

Tight Oil Upside Potential

New Stacked Reservoirs in Established Plays

15

Bakken- Three Forks Wiliston Basin

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

The Tight Oil Revolution Scorecard

•What does this mean to the U.S. economy?

• Jobs: 2012 = 800,000 2035 = 1.4 million

• GDP: 2012 = $116 billion 2035 = $188 billion

• Taxes: 2012 = $ 30 billion 2035 = $ 51 billion

• Dramatic decrease in US oil imports

• In 2005 US net oil imports = 12.2 mbd or 58% of demand. By

2020 US net import requirement will shrink to 30% of demand.

• Huge implications for energy security and the economy

• The learning curve is alive and well

The rest of the story:

Towards a Manufacturing Renaissance – How the Rise

of Unconventional Oil and Natural Gas is Transforming

the US Economy and Changing US Global

Competitiveness

17

Estimate > $125 billion in direct capital investment

to build out the U.S. midstream infrastructure to

Incremental increases in unconventional oil and gas

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

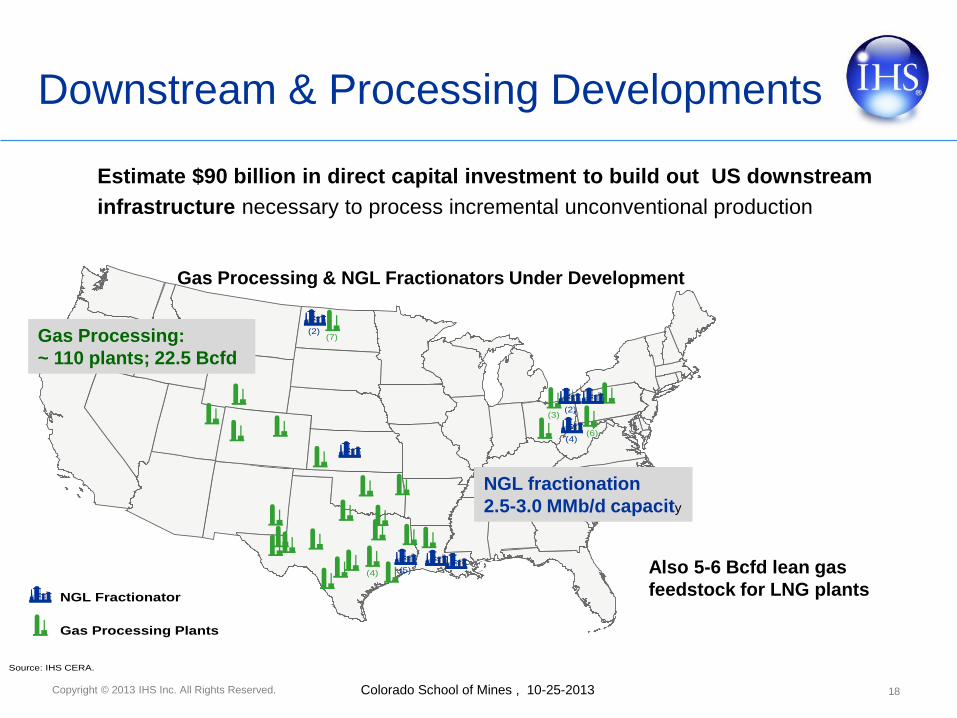

Downstream & Processing Developments

18 1

Source: IHS CERA.

Gas Processing Plants

NGL Fractionator

(5)(4)

(2)(7)

(3)(2)

(6)(4)

Estimate $90 billion in direct capital investment to build out US downstream

infrastructure necessary to process incremental unconventional production

Gas Processing & NGL Fractionators Under Development

Gas Processing:

~ 110 plants; 22.5 Bcfd

NGL fractionation

2.5-3.0 MMb/d capacity

Also 5-6 Bcfd lean gas

feedstock for LNG plants

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

90 95 00 05 10 15 20

Million Metric Tons

North America

West Europe

A Renewal of the US Chemical Industry Basic Chemicals & Plastics Production Change

(1990 Base)

US > $100 Billion in new investment

Copyright © 2013 IHS Inc. All Rights Reserved. Colorado School of Mines , 10-25-2013

The Climate Change Benefit

US Total Energy Related GHG Emissions

20

© 2013 IHS

• Unconventional oil and natural gas activity is reshaping America’s energy future &

bringing significant benefits to the US economy in terms of jobs, government

revenues, and GDP.

• A new era of affordable and abundant energy is creating significant competitive

advantages for the US in both energy-intensive industries and industries that rely on

natural gas derivatives as critical production feedstock.

Summary: Measuring the Transformative Contribution

of Unconventional Energy to the US Economy

21

2012

$1,200

2015

$2,000

2025

$3,500

2012

2.1M

2020: 3.3M

2025: 3.9M

• Jobs: 2.1 million jobs in 2012, 3.3

million in 2020 and 3.9 million in 2025.

• GDP: annual contributions will nearly

double from $284 billion in 2012 to

$533 billion in 2025.

• Government revenues: average $115

billion annually, totaling over $1.6

trillion from 2012 to 2025.

• Real household disposable income:

increase of more than $1,200 in 2012,

$2,000 in 2015 to more than $3,500 in

2025

Employment Contribution

Contribution to Household Income

The “Unconventional” O&G Revolution: Another Look Under the Hood

Pete Stark,

Senior Research Director and Advisor

IHS CERA

RCP Sponsors Meeting

Colorado School of Mines

October 25, 2013

CONFIDENTIAL

© 2012, All rights reserved, Cambridge Energy Research Associates, Inc., 55 Cambridge Parkway, Cambridge, Massachusetts 02142

No portion of this presentation may be reproduced, reused or otherwise distributed in any form without prior written consent.