The Timing of Macroprudential Intervention: The Central Bank’s new LTV and LTI regulations Lars...

10

The Timing of Macroprudential Intervention: The Central Bank’s new LTV and LTI regulations Lars Frisell, Central Bank of Ireland

-

Upload

joanna-hunt -

Category

Documents

-

view

214 -

download

0

Transcript of The Timing of Macroprudential Intervention: The Central Bank’s new LTV and LTI regulations Lars...

The Timing of Macroprudential Intervention: The Central Bank’s new LTV and LTI regulations

Lars Frisell, Central Bank of Ireland

2

Main Messages

• The effect of the regulations on house prices and housing supply is expected to be small and temporary:

– International experience

– CBI simulation

– Straightforward intuition

• Some shift towards rental accommodation is probable - both supply and demand

• The timing is right:

– Regulations and tight credit conditions are not additive

– Worst mistake is to wait too long

3

Loan to Value (LTV) for principal dwelling houses (PDH)PDH mortgages for non-first time buyers are subject to a limit of 80 per cent LTV.

For first time buyers of properties valued up to €220,000, a maximum LTV of 90 per cent will apply. For first time buyers of properties over €220,000 a 90 per cent limit will apply on the first €220,000 value of a property and an 80 per cent limit will apply on any excess value over this amount.

The cumulative monetary value of loans for principal dwelling purposes which breach either of these limits should not exceed 15 per cent of the euro value of all PDH loans on an annual basis.

Housing loans for borrowers in negative equity who wish to obtain a mortgage for a new property are not within the scope of the LTV limits.

Loan to Value (LTV) for Buy to Let mortgages (BTLs)BTL mortgages are subject to a limit of 70 per cent LTV.

This limit can only be exceeded by no more than 10 per cent of the euro value of all housing loans for non PDH purposes during an annual period.

Loan to Income (LTI) for PDH mortgagesPDH mortgage loans are subject to a limit of 3.5 times loan to gross income.

This limit should not be exceeded by more than 20 per cent of the euro value of all housing loans for PDH purposes during an annual period.

Switcher mortgages and housing loans for the restructuring of mortgages in arrears or pre-arrears are not in the scope of the Regulations.

The Regulations

4

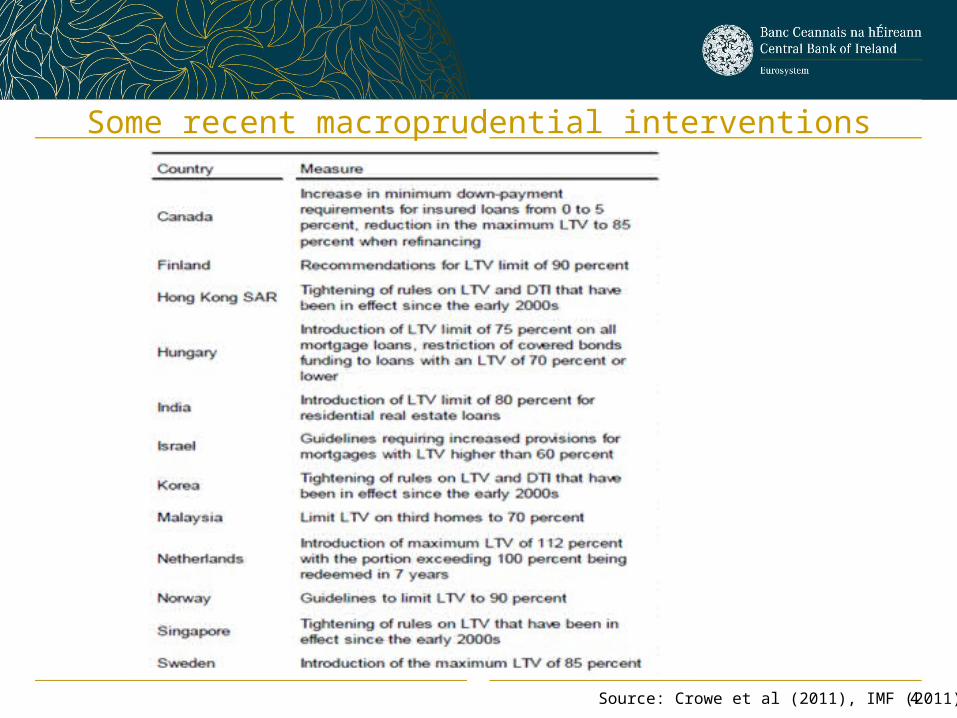

Some recent macroprudential interventions

Source: Crowe et al (2011), IMF (2011)

5

Before vs. after LTI/DTI-rules in Korea

Source: Igan and Kang (2011)

6

Actual against counterfactual scenario after LTV-restriction in New Zealand

Source: Price (2014)

7

Simulation results of potential effects of the CBI regulations

Source: Cussen, O’Brien, Onorante and O’Reilly (2015)

8

Examples of potential price falls and sellers’ gain from waiting

Note: Rent is assumed equal to user cost of buying

Available deposit: 30,000 30,000

Amortisation period: 30 30

Maximum LTV before regulation: 90% 95%

Maximum price before regulation: 300,000 600,000

Maximum price after regulation: 260,000 260,000

Solve: 30.000 = 0.1 * 220,000 + 0.2* (price - 220,000)

Potential price fall: 13% 57%

Deposit required after regulation for original price: 38000 98000Solve: 0.1 * 220,000 + 0.2* (price - 220,000)

New LTV: 87% 84%

Annual amortisation at original price: 9000 19000

Years required to accumulate new deposit: 0.9 3.6

Seller's total return from waiting: 15% 131%

9

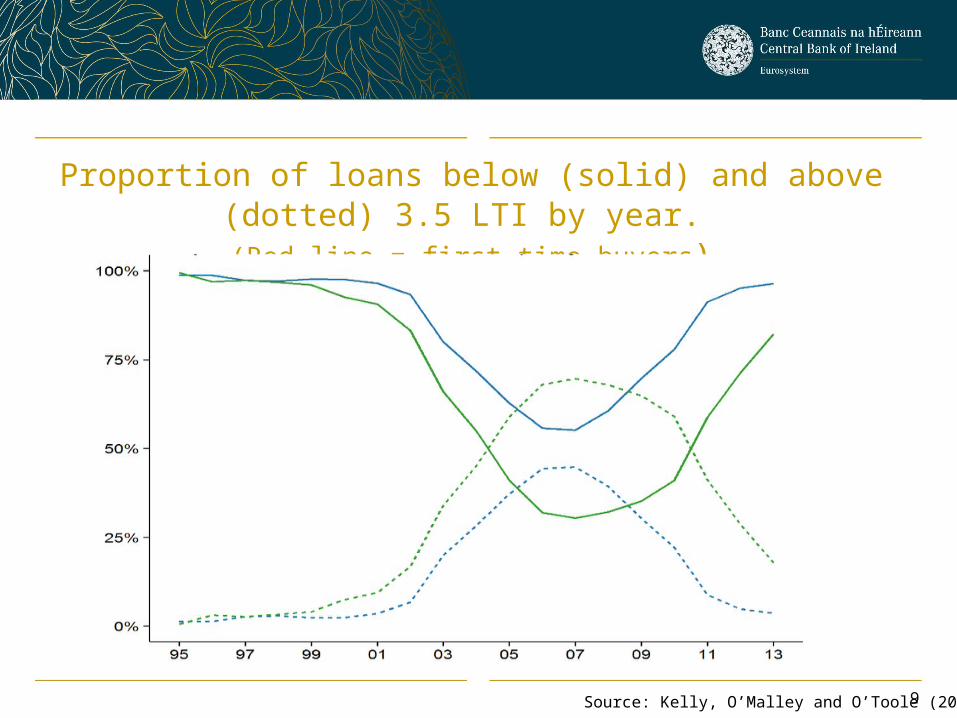

Proportion of loans below (solid) and above (dotted) 3.5 LTI by year.

(Red line = first-time-buyers)

Source: Kelly, O’Malley and O’Toole (2014)

10

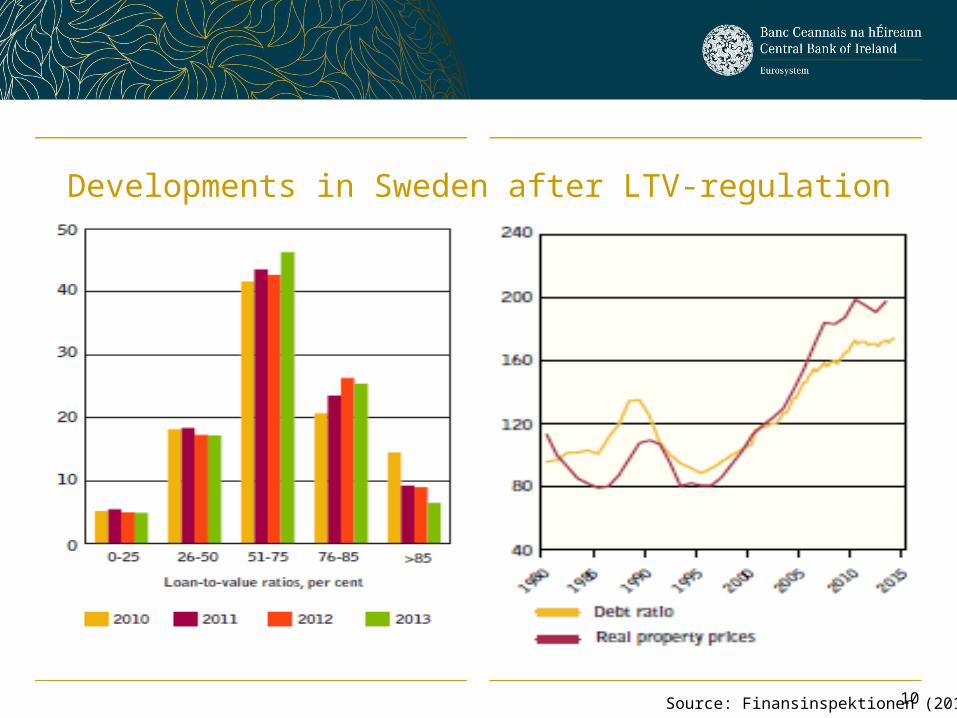

Developments in Sweden after LTV-regulation

Source: Finansinspektionen (2014)