The Temenos guide to Real World RegTech - Banking … · 2017-05-18 · Real World RegTech The...

6

Real World RegTech The Temenos guide to Accounting IFRS 9 Adoption Key Changes Objectives Temenos Module • Published by the IASB in July 2014, effective from January 2018 • Worldwide more than 100 countries require, permit or are converging to IFRS • Will replace the earlier IAS 39 • Addresses the accounting for Financial Instruments. • IFRS 9 package includes: • A logical model for Classification & Measurement • A single forward looking ‘Expected Loss’ Impairment Model • A substantially reformed approach to Hedge Accounting • New guidance and rules: • Simplification of Classification & Measurement Categories • Move from Incurred Loss to Expected Loss Model • Improved Hedge Accounting Model • Replaces compliance for IAS39 • Provides a standardized solution for all three areas: Classification & Measurement, Impairment Accounting and Hedge Accounting Know Your Customer Common Reporting Standard (CRS) Adoption Key Changes Objectives Temenos Module • Released by OECD in July 2014, effective from January 2016 • 100 countries have currently committed to implement the CRS • 53 Jurisdictions Undertaking First Exchange of Information by 2017 and 47 by 2018 • Framework for the automatic exchange of information • FIs required to report financial account information on account holders that are tax residents in other participating jurisdictions • Automatic exchange of information from the source country to the residence country • Process to identify reportable accounts and obtain accurate, required information, a common standard with robust Due Diligence procedures • Reporting/Exchange of Information: • Basic Information/ Account Number • Name of Reporting FI • Account Balances • Income Details • Offers support for Client Identification and Due Diligence for new or existing individual or entity accounts • Provides exchange of information reporting using similar logic to IGA Model 1 or FATCA

Transcript of The Temenos guide to Real World RegTech - Banking … · 2017-05-18 · Real World RegTech The...

Real World RegTech

The Temenos guide to

AccountingIFRS 9

Adoption Key Changes Objectives Temenos Module

• Published by the IASB in July 2014, effective from January 2018

• Worldwide more than 100 countries require, permit or are converging to IFRS

• Will replace the earlier IAS 39

• Addresses the accounting for Financial Instruments.

• IFRS 9 package includes:

• A logical model for Classification & Measurement

• A single forward looking ‘Expected Loss’ Impairment Model

• A substantially reformed approach to Hedge Accounting

• New guidance and rules:

• Simplification of Classification & Measurement Categories

• Move from Incurred Loss to Expected Loss Model

• Improved Hedge Accounting Model

• Replaces compliance for IAS39

• Provides a standardized solution for all three areas: Classification & Measurement, Impairment Accounting and Hedge Accounting

Know Your CustomerCommon Reporting Standard (CRS)

Adoption Key Changes Objectives Temenos Module

• Released by OECD in July 2014, effective from January 2016

• 100 countries have currently committed to implement the CRS

• 53 Jurisdictions Undertaking First Exchange of Information by 2017 and 47 by 2018

• Framework for the automatic exchange of information

• FIs required to report financial account information on account holders that are tax residents in other participating jurisdictions

• Automatic exchange of information from the source country to the residence country

• Process to identify reportable accounts and obtain accurate, required information, a common standard with robust Due Diligence procedures

• Reporting/Exchange of Information:

• Basic Information/Account Number

• Name of Reporting FI

• Account Balances • Income Details

• Offers support for Client Identification and Due Diligence for new or existing individual or entity accounts

• Provides exchange of information reporting using similar logic to IGA Model 1 or FATCA

2

Foreign Account Tax Compliance Act (FATCA)

Adoption Key Changes Objectives Temenos Module

• Effective July 2014• In order to reduce

the administrative burden of complying with the US regulations, many countries have entered into Intergovernmental Agreement (IGA) with the US Government:

• IGA 1• IGA 2

• Financial institutions required to identify accounts held by US persons and report to IRS/local authorities

• The agreement imposes significant reporting and disclosure obligations

• Annual reporting on the identified US accounts to the tax authority

• FATCA aims to prevent tax evasion by US persons using foreign accounts

• Obtain and maintain necessary documentation for the determination of US accounts

• Offers support for Client Identification and Due Diligence for new or existing individual or entity accounts

• Identifies taxable income and applies 30% withholding tax

• Supports reporting based on xml schema V2.0 per the IRS

Risk ManagementBasel III

Adoption Key Changes Objectives Temenos Module

• Effective date extended from March 2018 to March 2019

• New framework for RWA and CAD

• New policies for portfolio leverage ratio

• Liquidity Requirements Introduction of LCR and NSFR intra-day and available liquidity

• Improve the banking sector’s ability to absorb shocks arising from financial and economic stress

• Improve risk management & governance

• Supports ALM & Liquidity Management

• Provides COREP/FINREP reporting

• Credit Risk, Exposure and Counterparty Management

3

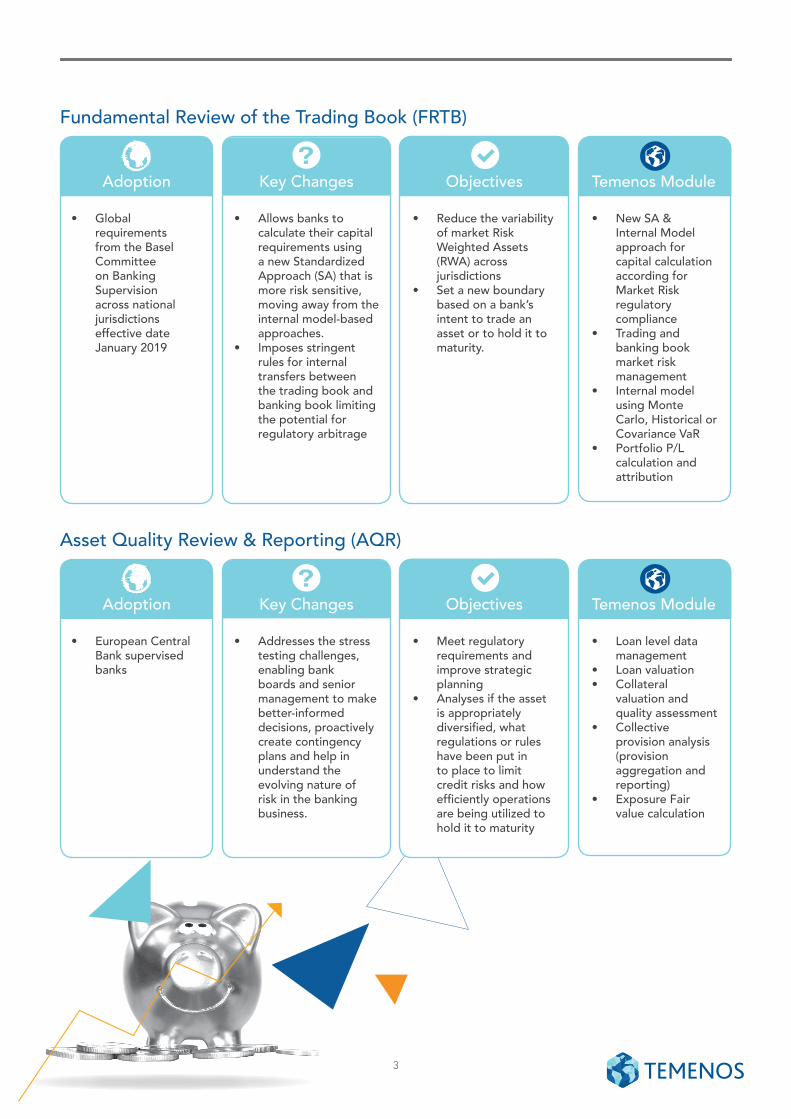

Fundamental Review of the Trading Book (FRTB)

Adoption Key Changes Objectives Temenos Module

• Global requirements from the Basel Committee on Banking Supervision across national jurisdictions effective date January 2019

• Allows banks to calculate their capital requirements using a new Standardized Approach (SA) that is more risk sensitive, moving away from the internal model-based approaches.

• Imposes stringent rules for internal transfers between the trading book and banking book limiting the potential for regulatory arbitrage

• Reduce the variability of market Risk Weighted Assets (RWA) across jurisdictions

• Set a new boundary based on a bank’s intent to trade an asset or to hold it to maturity.

• New SA & Internal Model approach for capital calculation according for Market Risk regulatory compliance

• Trading and banking book market risk management

• Internal model using Monte Carlo, Historical or Covariance VaR

• Portfolio P/L calculation and attribution

Asset Quality Review & Reporting (AQR)

Adoption Key Changes Objectives Temenos Module

• European Central Bank supervised banks

• Addresses the stress testing challenges, enabling bank boards and senior management to make better-informed decisions, proactively create contingency plans and help in understand the evolving nature of risk in the banking business.

• Meet regulatory requirements and improve strategic planning

• Analyses if the asset is appropriately diversified, what regulations or rules have been put in to place to limit credit risks and how efficiently operations are being utilized to hold it to maturity

• Loan level data management

• Loan valuation • Collateral

valuation and quality assessment

• Collective provision analysis (provision aggregation and reporting)

• Exposure Fair value calculation

4

Customer PrivacyGeneral Data Protection Regulation (GDPR)

Adoption Key Changes Objectives Temenos Module

• Effective from 2018 in all EU member states

• Replaces the existing Data Protection Directive

• Impacts any organization that gathers, processes and stores personal data

• Personal Data should be processed under the responsibility and liability of the Data Controller

• Establishes consent for use of personal data

• Non-compliance with the GDPR can result in reputational damage, litigation and major fines

• Covers non-EU companies holding data on EU citizens

• Personal Data are not made accessible to an indefinite number of individuals

• Only those Personal Data should be processed which are necessary for each specific purpose

• Personal Data should not be retained beyond the minimum necessary

• Personal Data should be processed lawfully, fairly and in a transparent manner in relation to the data subject

• Supports deletion of personal data

• Supports export of personal data

• Supports record of objections to the use of data

• Supports record of consent

• Analysis of personal data flows through Temenos software

Open Banking RegulationPSD 2

Adoption Key Changes Objectives Temenos Module

• All EU member states (28) plus Iceland, Liechtenstein and Norway to adopt an publish measures for PSD2 compliance by January 2018

• Revised European Union Payment Services Directive

• Establishes legal basis of Third Party Payment and Account Information Service Provider

• Regulatory requirement for Open API Access to Account Data – XS2A

• 2-factor authentication mandatory in all channels

• Introduces regulatory framework for Third Party Payment Providers and Account Information Services

• Open API Access to Account and Customer Information (XS2A)

• Increase in regulations in e-payments and m-payments

• Third party providers must itemise charges forwarded to payers

• Supports Payment Transparency

• Supports Payment Initiation via API

• Supports extension of Payment Services Directive

• Supports push of account information from Core banking and pull from API

5

Post TradeDerivative Regulatory Reporting (Dodd-Frank and EMIR)

Adoption Key Changes Objectives Temenos Module

• Dodd-Frank Wall Street Reform and Consumer Protection Act was signed into federal law in July 2010 in the US

• European Market Infrastructure (EMIR) Regulation became effective on August 2012

• Mandatory reporting of trades. Central clearing. Electronic Trading and Posting of Collateral

• Counterparties ensnared by EMIR must report exchange-traded derivatives, while Dodd-Frank requires only over-the-counter transactions to be reported

• Reporting formats; although essence the same, data fields and coverage also varies among regulators.

• Both Dodd-Frank and EMIR were implemented as a result of an international effort to increase stability in the financial markets especially after the financial crisis in 2008.

• New module “OC” introduced with reporting capabilities

• Framework able to handle multiple jurisdictions including EMIR and Dodd Frank

• Availability of Trade & Counterparty details

• User maintainability with configurable reporting rules, fields and csv reporting

Financial CrimeAnti-Money Laundering (AML) and Sanctions Screening

Adoption Key Changes Objectives Temenos Module

• Laws and regulations in US, EU and other major currencies jurisdictions administer economic sanctions

• 4th EU AML Directive effective June 2017

• FATF revision 2012

• Identify ultimate beneficial ownership (UBO) of legal persons

• Lower threshold for cash transactions

• Screen for domestic PEPs

• Enhanced and increased information sharing and global cooperation between enforcement units

• Increase transparency about real owners of companies and trusts

• Boost tax transparency and tackle tax abuse

• Combat more effectively terrorist financing and money laundering

• Banks should define and regularly re-assess risk-based approach in AML/CFT

• The Profile module creates alerts when current behavior differs from previous behavior or reference patterns

• The Screen module screens transactions and customers against sanctions and a bank’s own lists

6

Fraud

Adoption Key Changes Objectives Temenos Module

• Broadly among financial institutions globally

• Big data analytics and data clouds can help when faster payments are made, since data analytics collects and then analyses at a speed which was previously not possible, in order to identify behavioural patterns

• Use of advanced pattern detection techniques to reduce the risk of fraud

• As part of fraud prevention, these solutions monitor transactions in real time to identify gaps, issues and trends in financial crime.

• Detect and prevent insider fraud and external fraud

• The Profile module will detect and prevent external fraud attempts

• Build user, customer and transaction profiles of normal activities

• Detect abnormal activity with sophisticated techniques

• Stop fraudulent transactions before execution

About TememosTemenos Group AG (SIX: TEMN), headquartered in Geneva, is a market leading software provider, partnering with banks and other financial institutions to transform their businesses and stay ahead of a changing marketplace.

Over 2,000 firms across the globe, including 38 of the top 50 banks, rely on Temenos to process the daily transactions of more than 500 million banking customers.

Temenos customers are proven to be more profitable than their peers: in the period 2008-2014, they enjoyed on average a 31% higher return on assets, a 36% higher return on equity and an 8.6 percentage point lower cost/income ratio than banks running legacy applications.

Learn more

To find out how Temenos can help you, then contact [email protected] or visit us at www.temenos.com

Learn more and get involved atRegTech in Banking

https://www.linkedin.com/groups/12024766