The Tax Cuts and Jobs Act - dhg.com · Corporate AMT much like individuals •AMT calculation could...

215

Welcome to DHG’s Tax Reform Briefing! The Tax Cuts and Jobs Act A Discussion of Key Provisions Impacting You FEBRUARY 7, 2018

Transcript of The Tax Cuts and Jobs Act - dhg.com · Corporate AMT much like individuals •AMT calculation could...

Welcome to DHG’s Tax Reform Briefing!

The Tax Cuts and Jobs ActA Discussion of Key Provisions Impacting You

FEBRUARY 7, 2018

• C Corporations

• Accounting Methods

• Impact on Financial Statements

• Other Changes Impacting Businesses

• Impact on Pass-through Entities

• Entity Selection Considerations: S Corp vs. C Corp

• Impact to Individuals

• Charitable Planning and Exempt Organizations

2

Tax Reform:

Impacts to CorporationsHaley Roberts, Tax Manager – Federal Tax Specialty Services

• Corporate tax rates

• Fiscal year end filers

• Dividends received deduction

• Corporate AMT

• Net operating losses

• Other miscellaneous corporate and business reforms

• Accounting methods

4

HISTORICAL REFORM FOR CORPORATIONS

Corporate Tax Rate

Tax Rate If taxable income is:

21% $0 and more

21% Personal Service Corporation

5

Tax Rate If taxable income is:

15% $0 - $50,000

25% $50,001 - $75,000

34% $75,001 - $10,000,000

35% $10,000,000+

35% Personal Service Corporation

2017 Tax Law Tax Reform Law

Return to Table of Contents

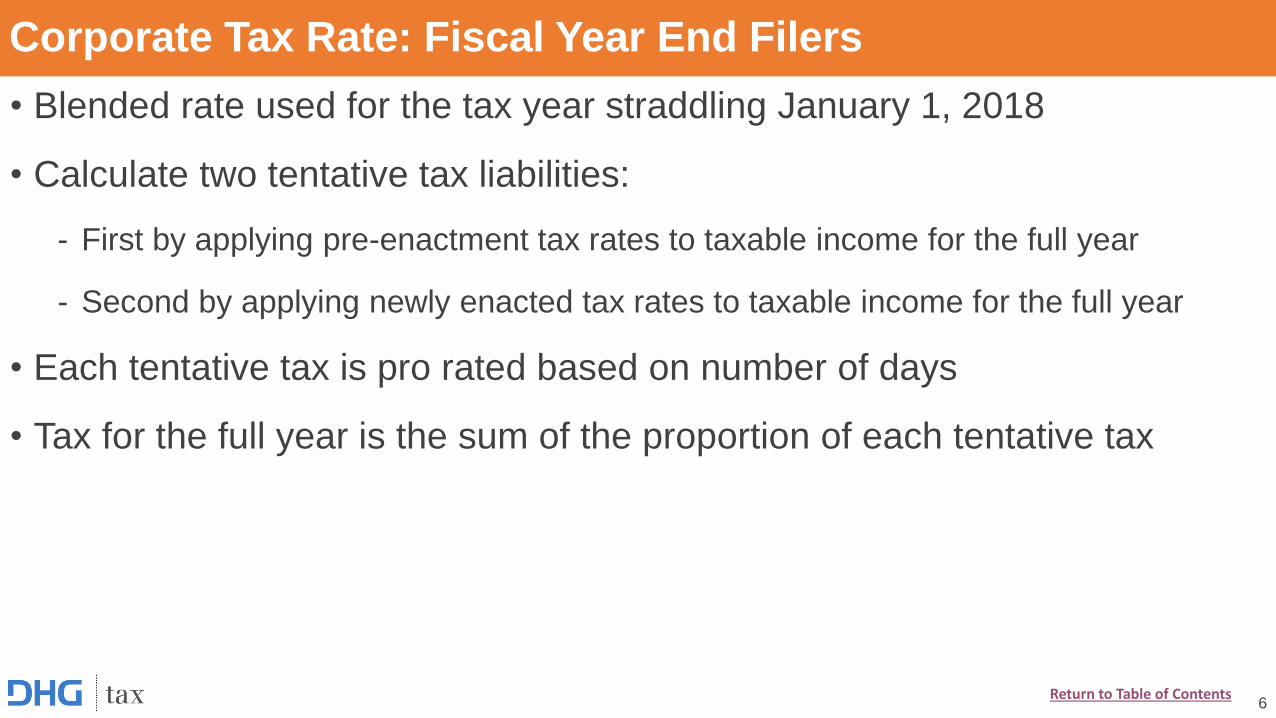

Corporate Tax Rate: Fiscal Year End Filers

• Blended rate used for the tax year straddling January 1, 2018

• Calculate two tentative tax liabilities:

- First by applying pre-enactment tax rates to taxable income for the full year

- Second by applying newly enacted tax rates to taxable income for the full year

• Each tentative tax is pro rated based on number of days

• Tax for the full year is the sum of the proportion of each tentative tax

6Return to Table of Contents

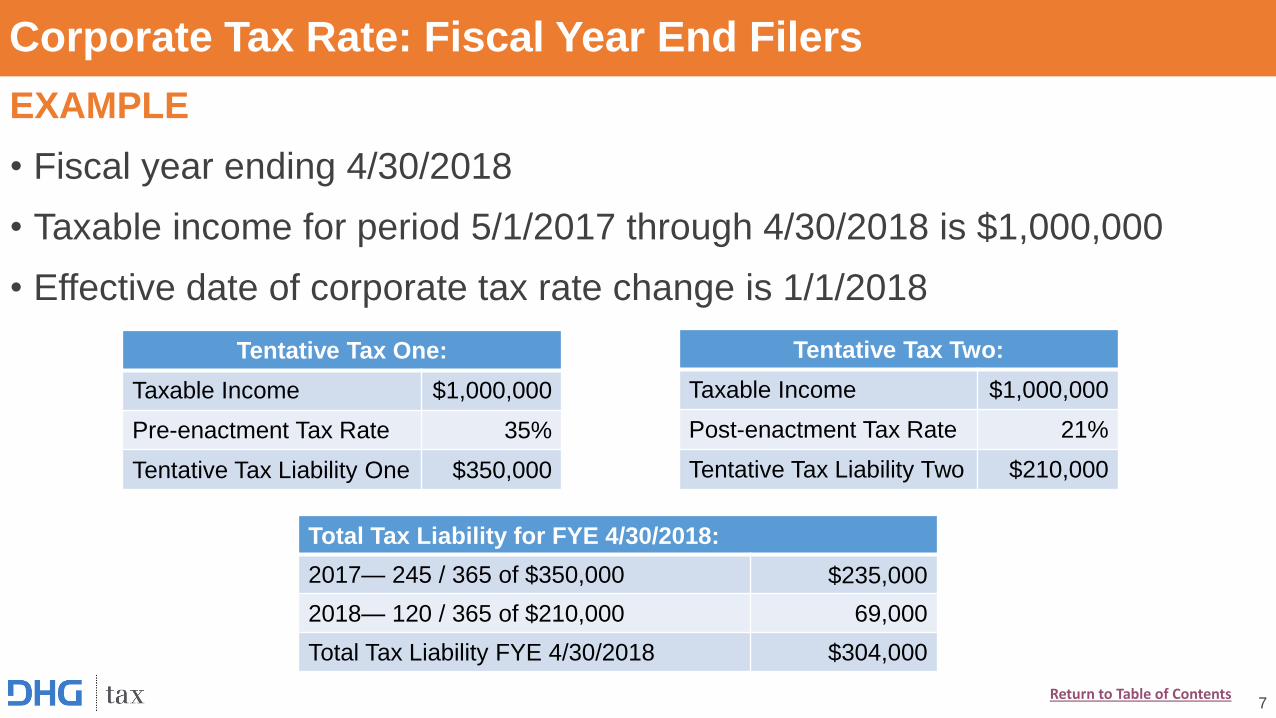

Corporate Tax Rate: Fiscal Year End Filers

EXAMPLE

• Fiscal year ending 4/30/2018

• Taxable income for period 5/1/2017 through 4/30/2018 is $1,000,000

• Effective date of corporate tax rate change is 1/1/2018

7

Tentative Tax One:

Taxable Income $1,000,000

Pre-enactment Tax Rate 35%

Tentative Tax Liability One $350,000

Tentative Tax Two:

Taxable Income $1,000,000

Post-enactment Tax Rate 21%

Tentative Tax Liability Two $210,000

Total Tax Liability for FYE 4/30/2018:

2017— 245 / 365 of $350,000 $235,000

2018— 120 / 365 of $210,000 69,000

Total Tax Liability FYE 4/30/2018 $304,000

Return to Table of Contents

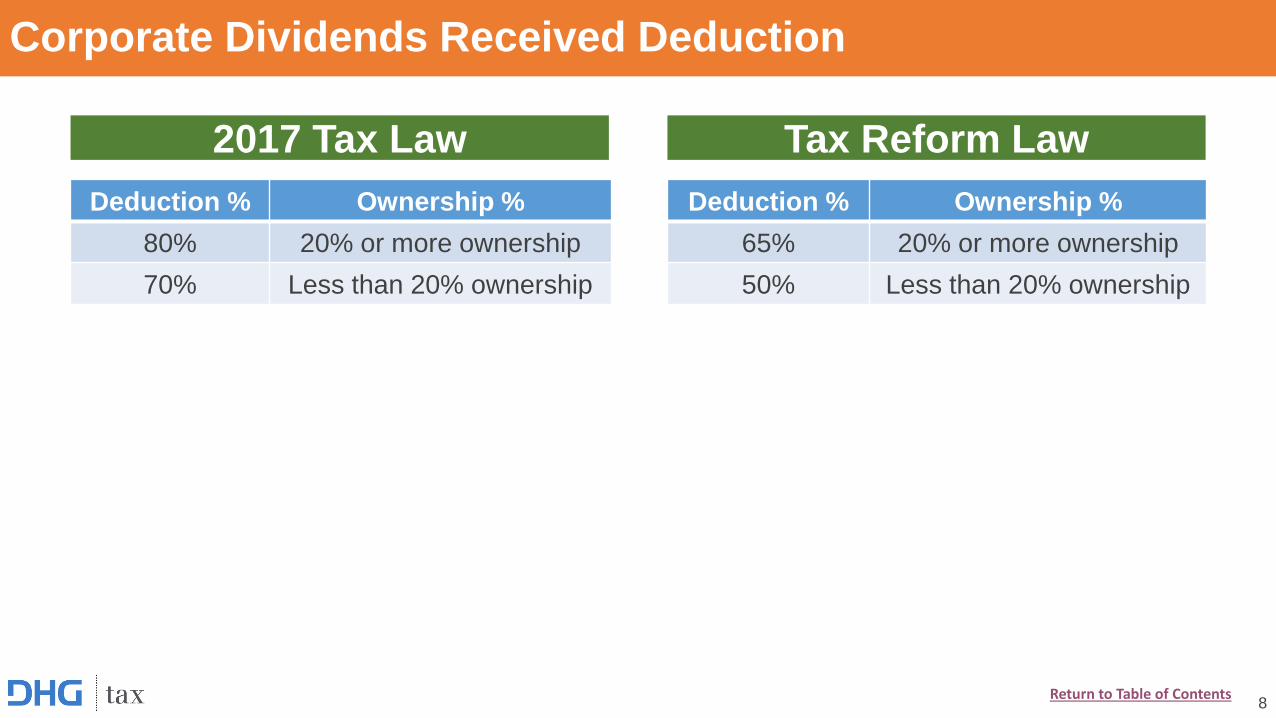

Corporate Dividends Received Deduction

Deduction % Ownership %

80% 20% or more ownership

70% Less than 20% ownership

8

Deduction % Ownership %

65% 20% or more ownership

50% Less than 20% ownership

2017 Tax Law Tax Reform Law

Return to Table of Contents

Corporate AMT

• Corporations subject to a

Corporate AMT much like

individuals

• AMT calculation could have

created credit carryovers

• Corporate AMT repealed

beginning after December 31,

2017

• Any remaining AMT credit

carryovers may be utilized to

the extent of regular tax liability

• For 2018, 2019 and 2020, to

the extent they exceed regular

tax, 50% of excess carryovers

are refundable, with the

balance refunded in 2021

9

2017 Tax Law Tax Reform Law

Return to Table of Contents

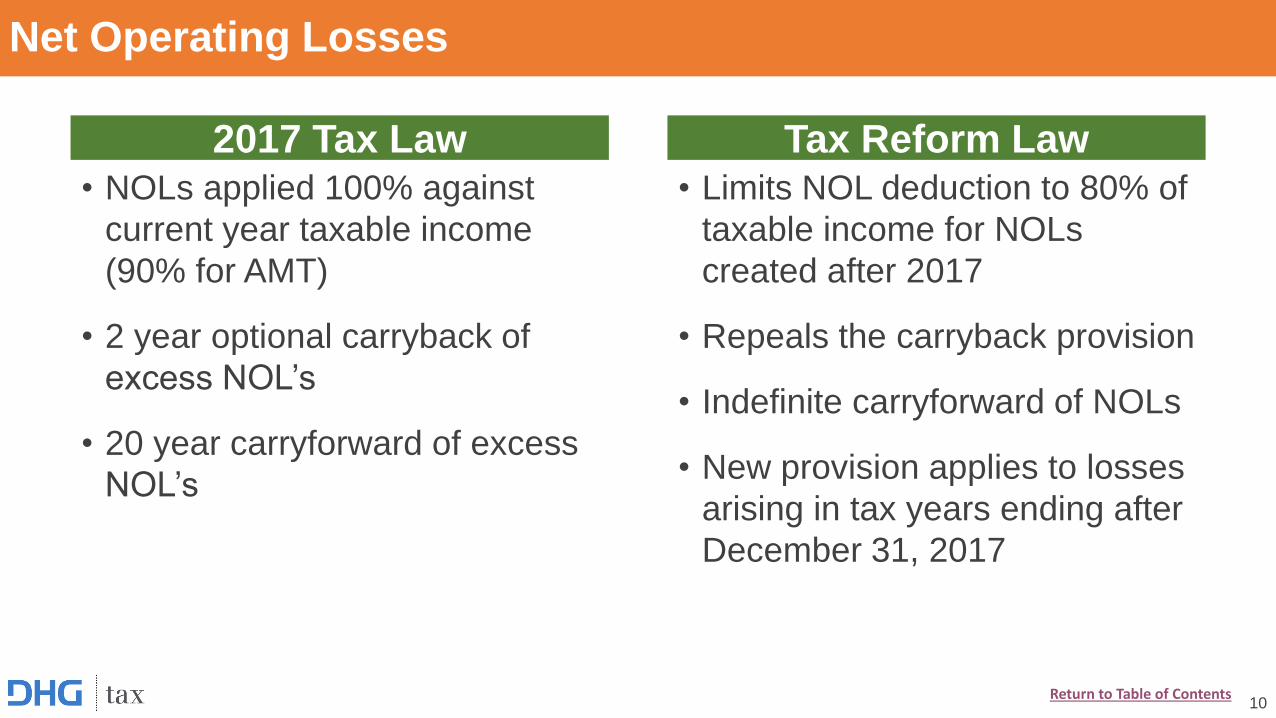

Net Operating Losses

• NOLs applied 100% against

current year taxable income

(90% for AMT)

• 2 year optional carryback of

excess NOL’s

• 20 year carryforward of excess

NOL’s

• Limits NOL deduction to 80% of

taxable income for NOLs

created after 2017

• Repeals the carryback provision

• Indefinite carryforward of NOLs

• New provision applies to losses

arising in tax years ending after

December 31, 2017

10

2017 Tax Law Tax Reform Law

Return to Table of Contents

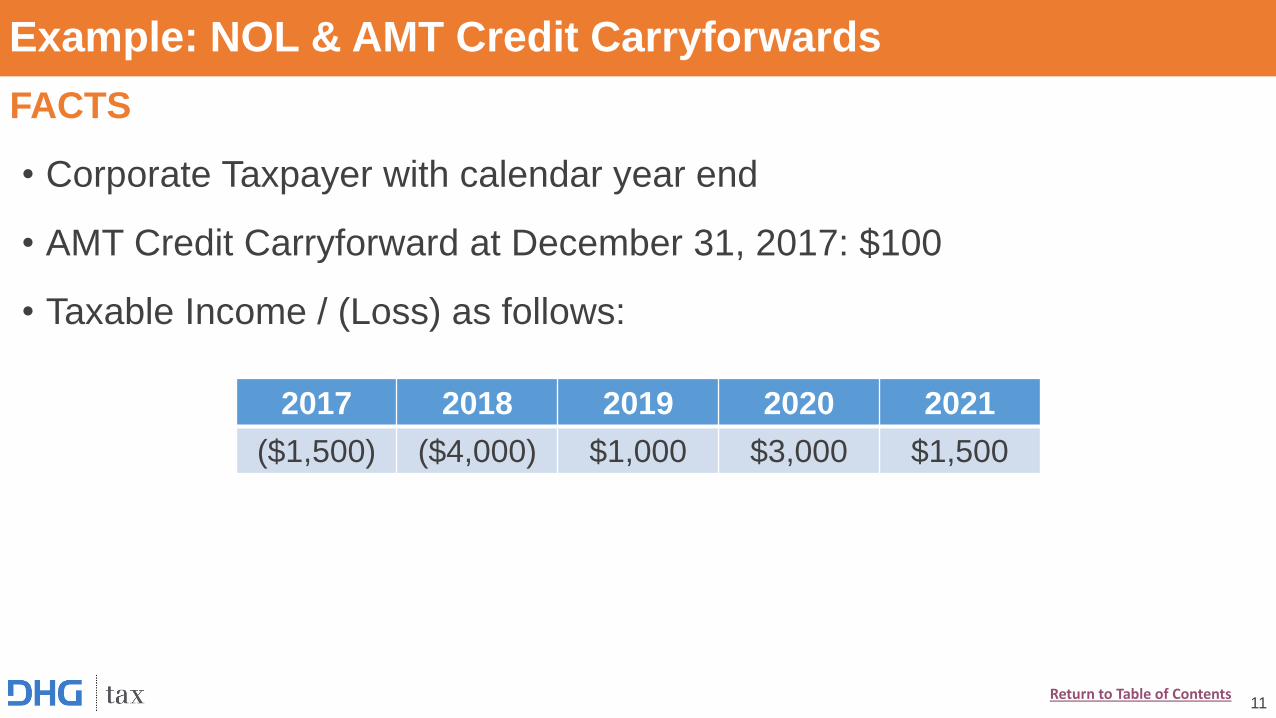

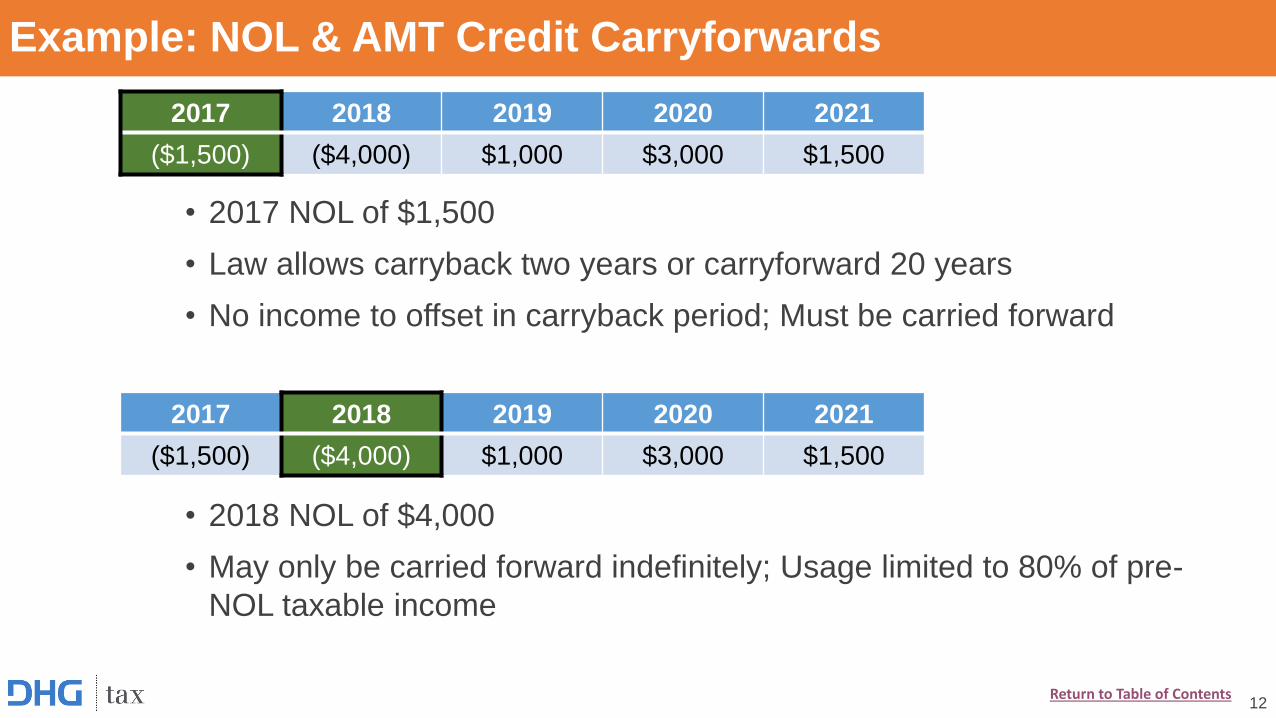

Example: NOL & AMT Credit Carryforwards

FACTS

• Corporate Taxpayer with calendar year end

• AMT Credit Carryforward at December 31, 2017: $100

• Taxable Income / (Loss) as follows:

11

2017 2018 2019 2020 2021

($1,500) ($4,000) $1,000 $3,000 $1,500

Return to Table of Contents

Example: NOL & AMT Credit Carryforwards

• 2017 NOL of $1,500

• Law allows carryback two years or carryforward 20 years

• No income to offset in carryback period; Must be carried forward

• 2018 NOL of $4,000

• May only be carried forward indefinitely; Usage limited to 80% of pre-

NOL taxable income

12

2017 2018 2019 2020 2021

($1,500) ($4,000) $1,000 $3,000 $1,500

2017 2018 2019 2020 2021

($1,500) ($4,000) $1,000 $3,000 $1,500

Return to Table of Contents

Example: NOL & AMT Credit Carryforwards

13

2017 2018 2019 2020 2021

Taxable Income ($1,500) ($4,000) $1,000 $3,000 $1,500

Pre-Reform NOL - - (1,000) (500) -

Post-Reform NOL - - - (2,400) (1,200)

Net Taxable Income ($1,500) ($4,000) - $100 $300

Tax Rate 35% 21% 21% 21% 21%

Tax Liability - - - $21 $63

AMT Credit C/F - - - (60) (40)

Net Tax Liability / (Refund) - - - ($39) $23

AMT Credit Usage 2020

Allowable Credit $21

50% of Excess $39 ($100 - $21 = $79 x 50%)

Total Allowable Credit $60

Return to Table of Contents

• Business interest expense

• Domestic production activity deduction (DPAD)

• Like-kind exchange

• Special rule for taxable year of inclusion

• Deduction for certain fines, penalties, and other amounts

• Local lobbying expense

• Business credits

• Other miscellaneous business provisions

14

MISCELLANEOUS CORPORATE AND BUSINESS PROVISIONS

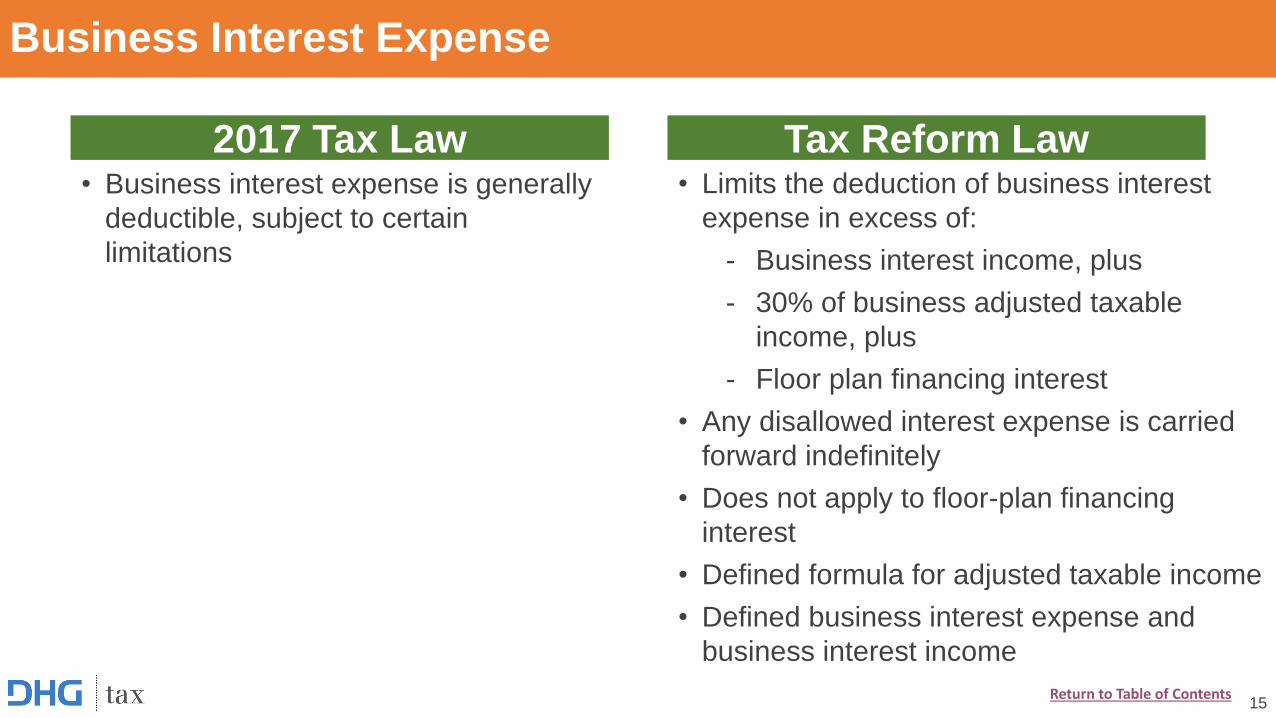

Business Interest Expense

• Business interest expense is generally

deductible, subject to certain

limitations

15

2017 Tax Law Tax Reform Law• Limits the deduction of business interest

expense in excess of:

- Business interest income, plus

- 30% of business adjusted taxable

income, plus

- Floor plan financing interest

• Any disallowed interest expense is carried

forward indefinitely

• Does not apply to floor-plan financing

interest

• Defined formula for adjusted taxable income

• Defined business interest expense and

business interest income

Return to Table of Contents

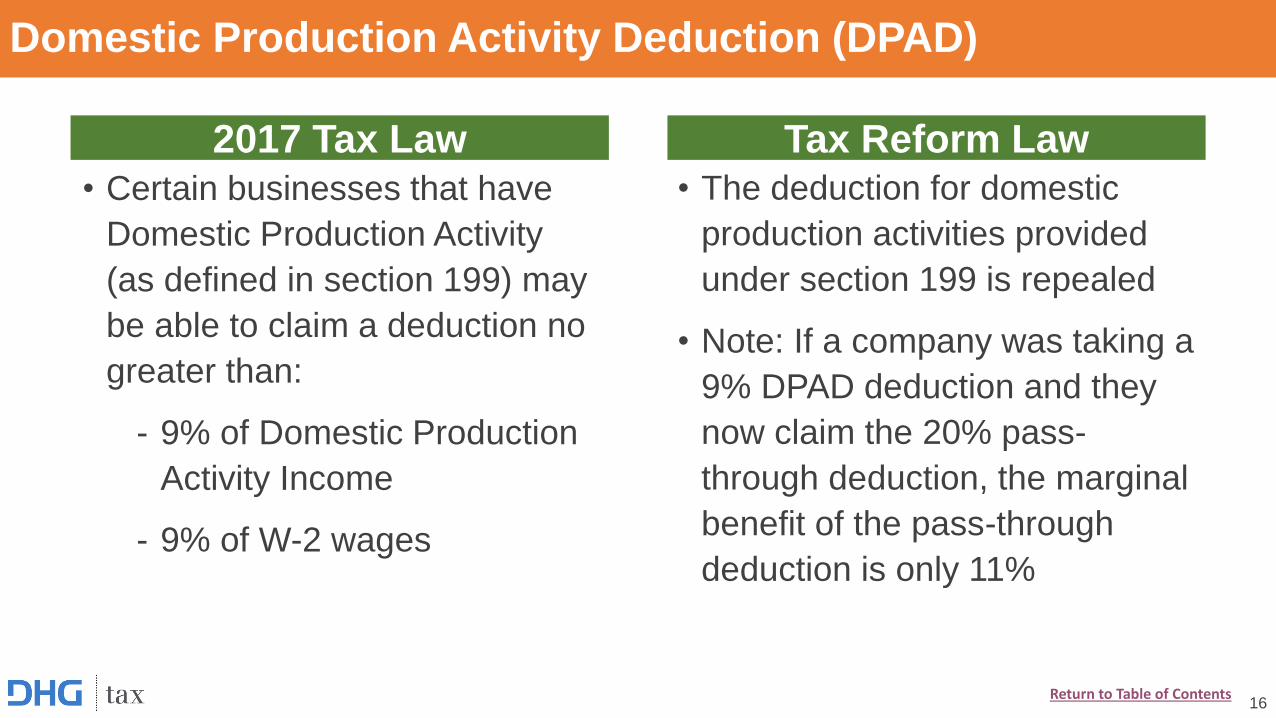

Domestic Production Activity Deduction (DPAD)

• Certain businesses that have

Domestic Production Activity

(as defined in section 199) may

be able to claim a deduction no

greater than:

- 9% of Domestic Production

Activity Income

- 9% of W-2 wages

16

2017 Tax Law Tax Reform Law

• The deduction for domestic

production activities provided

under section 199 is repealed

• Note: If a company was taking a

9% DPAD deduction and they

now claim the 20% pass-

through deduction, the marginal

benefit of the pass-through

deduction is only 11%

Return to Table of Contents

2017 Tax Law Tax Reform Law

Like-Kind Exchanges

• Section 1031 allows for the “roll-

over” exchange of like real

property, tangible personal

property, and intangible property

• Section 1031 still allowed for like-

kind real property

• Section 1031 disallowed for

tangible personal property and

intangible property

• Transition rules are applied and

still need to be defined by the

Secretary

17Return to Table of Contents

Special Rule for Taxable Year of Inclusion

• The “all events” test is satisfied no later

than when an amount is recognized as

revenue in the taxpayer’s applicable

financial statements

• Advance payments received must be

recognized as taxable revenue no later

than the end of the tax year following the

year of receipt

18

• Under §451, an accrual method taxpayer

includes an amount in taxable income when

“all events” have occurred which fix the

taxpayer’s right to receive the income and

the amount can be determined with

reasonable accuracy

• “All events” have occurred at the earliest

time when one of the following occurs:

- An amount is received;

- The taxpayer has the right to bill an

amount; or

- The amount is earned

• Possible that all events have not occurred

until after an amount is recognized for

financial reporting purposes

2017 Tax Law Tax Reform Law

Return to Table of Contents

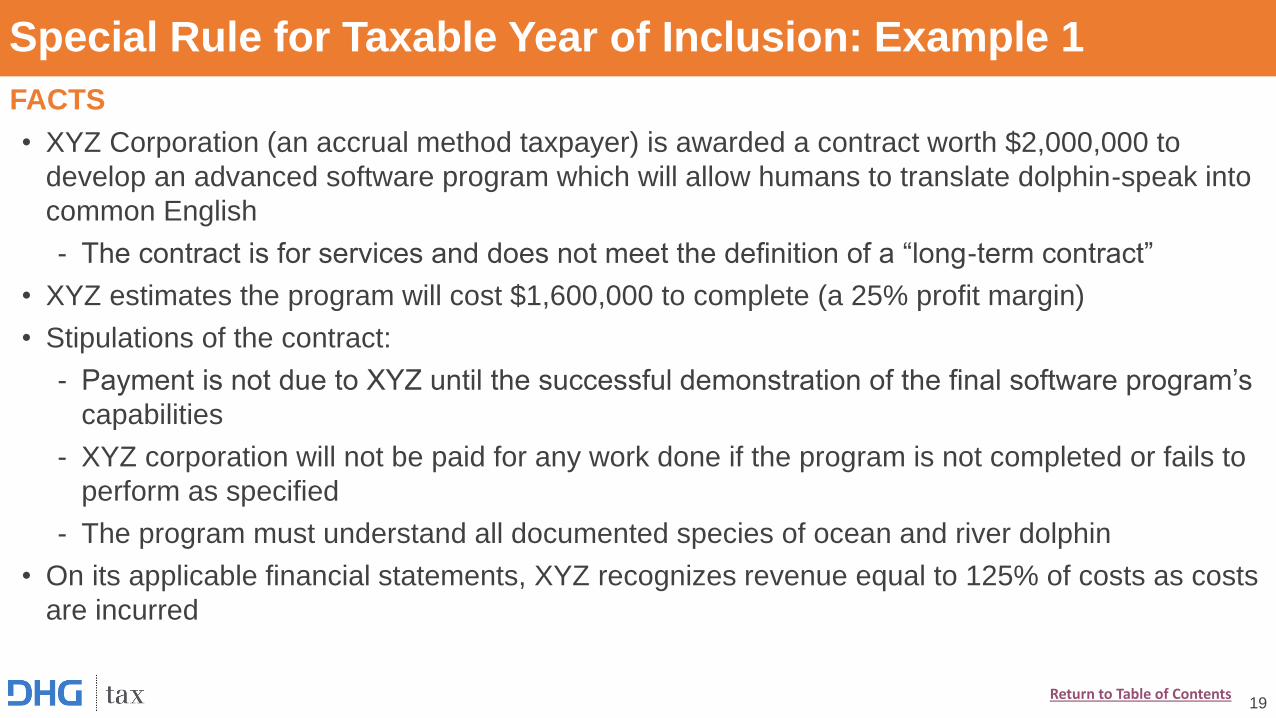

Special Rule for Taxable Year of Inclusion: Example 1

FACTS

• XYZ Corporation (an accrual method taxpayer) is awarded a contract worth $2,000,000 to

develop an advanced software program which will allow humans to translate dolphin-speak into

common English

- The contract is for services and does not meet the definition of a “long-term contract”

• XYZ estimates the program will cost $1,600,000 to complete (a 25% profit margin)

• Stipulations of the contract:

- Payment is not due to XYZ until the successful demonstration of the final software program’s

capabilities

- XYZ corporation will not be paid for any work done if the program is not completed or fails to

perform as specified

- The program must understand all documented species of ocean and river dolphin

• On its applicable financial statements, XYZ recognizes revenue equal to 125% of costs as costs

are incurred

19Return to Table of Contents

Special Rule for Taxable Year of Inclusion: Example 1

FACTS (cont.)

• The program is still in its nascent stages at the end of Year One and is

non-functional

• By the end of Year Two, the program understands common bottlenose

dolphins but not Amazon River dolphins

• The program is completed, successfully tested, and demonstrated to the

customer’s satisfaction during Year Three

• XYZ invoices the customer for the full contract price during Year Three but

does not receive payment until Year Four

20Return to Table of Contents

Special Rule for Taxable Year of Inclusion: Example 1

• Same as 2017 tax law with one

new addition…

• The “all events test” is met no later

than when the amount is

recognized as revenue in the

taxpayer’s applicable financial

statements

21

• Income is generally recognized

only when the “all events test” is

met – which occurs at the earliest

of:

(1) when payment is received,

(2) when entitled to invoice for

work done, or

(3) when the amount is earned

(e.g., when the work is

complete)

2017 Tax Law Tax Reform Law

Return to Table of Contents

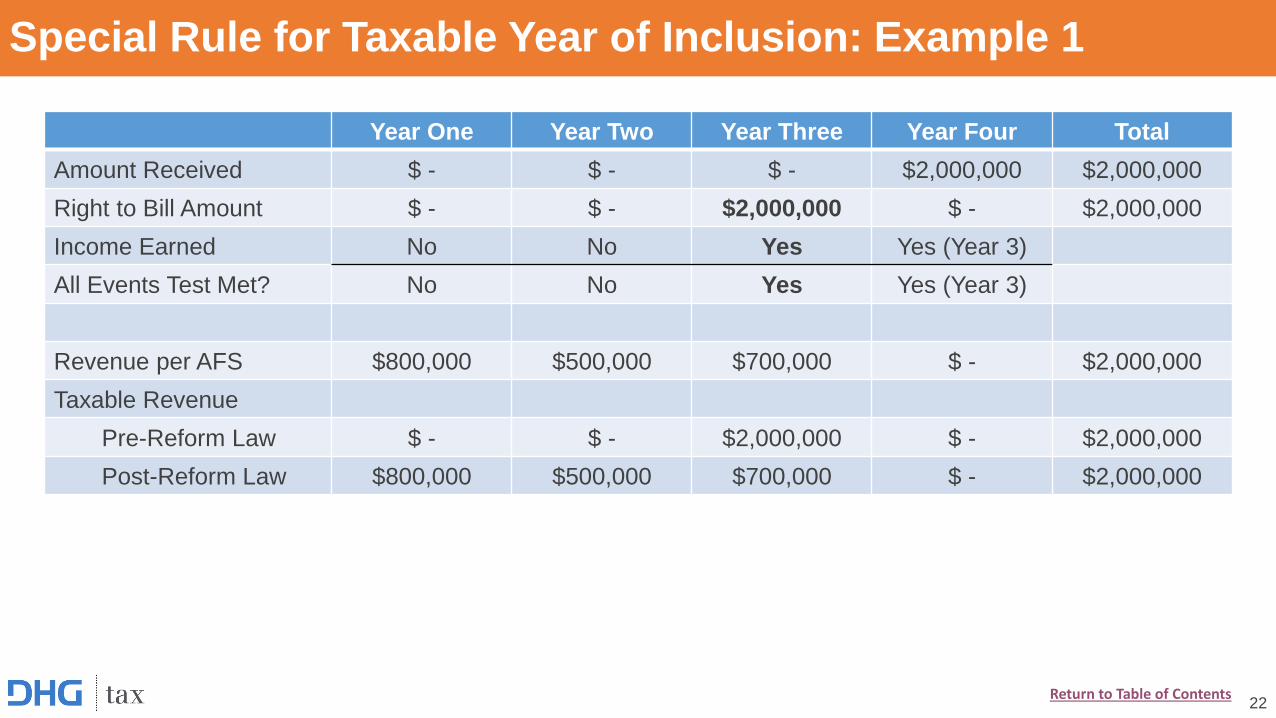

Special Rule for Taxable Year of Inclusion: Example 1

Year One Year Two Year Three Year Four Total

Amount Received $ - $ - $ - $2,000,000 $2,000,000

Right to Bill Amount $ - $ - $2,000,000 $ - $2,000,000

Income Earned No No Yes Yes (Year 3)

All Events Test Met? No No Yes Yes (Year 3)

Revenue per AFS $800,000 $500,000 $700,000 $ - $2,000,000

Taxable Revenue

Pre-Reform Law $ - $ - $2,000,000 $ - $2,000,000

Post-Reform Law $800,000 $500,000 $700,000 $ - $2,000,000

22Return to Table of Contents

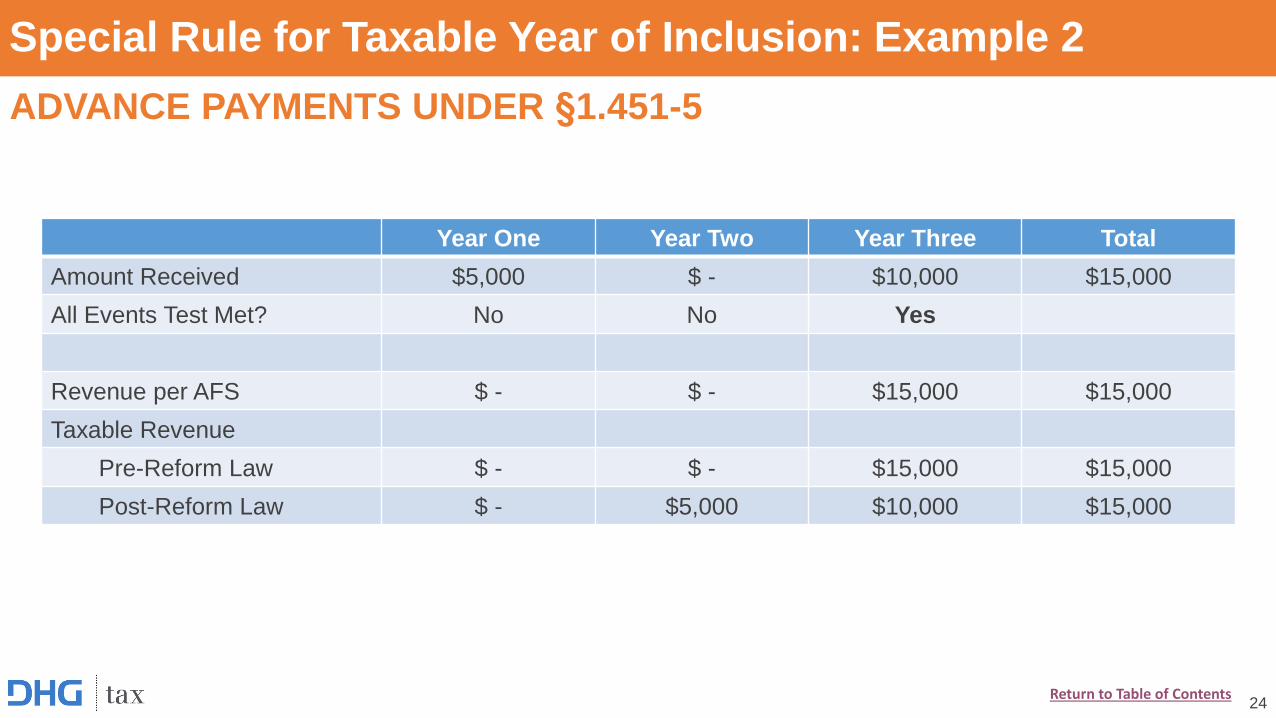

Special Rule for Taxable Year of Inclusion: Example 2

ADVANCE PAYMENTS UNDER §1.451-5

• ABC Co. is an accrual method taxpayer

• In Year 1, ABC receives a customer payment of $5,000 toward the

$15,000 purchase price for electric motors to be provided in Year 3

• ABC follows Treasury Regulation §1.451-5, which allows a taxpayer

to defer recognition of certain advance payments for goods until the

taxable year in which properly accruable under its method of

accounting

• ABC does not meet the all events test for this contract until Year 3

23Return to Table of Contents

Special Rule for Taxable Year of Inclusion: Example 2

Year One Year Two Year Three Total

Amount Received $5,000 $ - $10,000 $15,000

All Events Test Met? No No Yes

Revenue per AFS $ - $ - $15,000 $15,000

Taxable Revenue

Pre-Reform Law $ - $ - $15,000 $15,000

Post-Reform Law $ - $5,000 $10,000 $15,000

ADVANCE PAYMENTS UNDER §1.451-5

24Return to Table of Contents

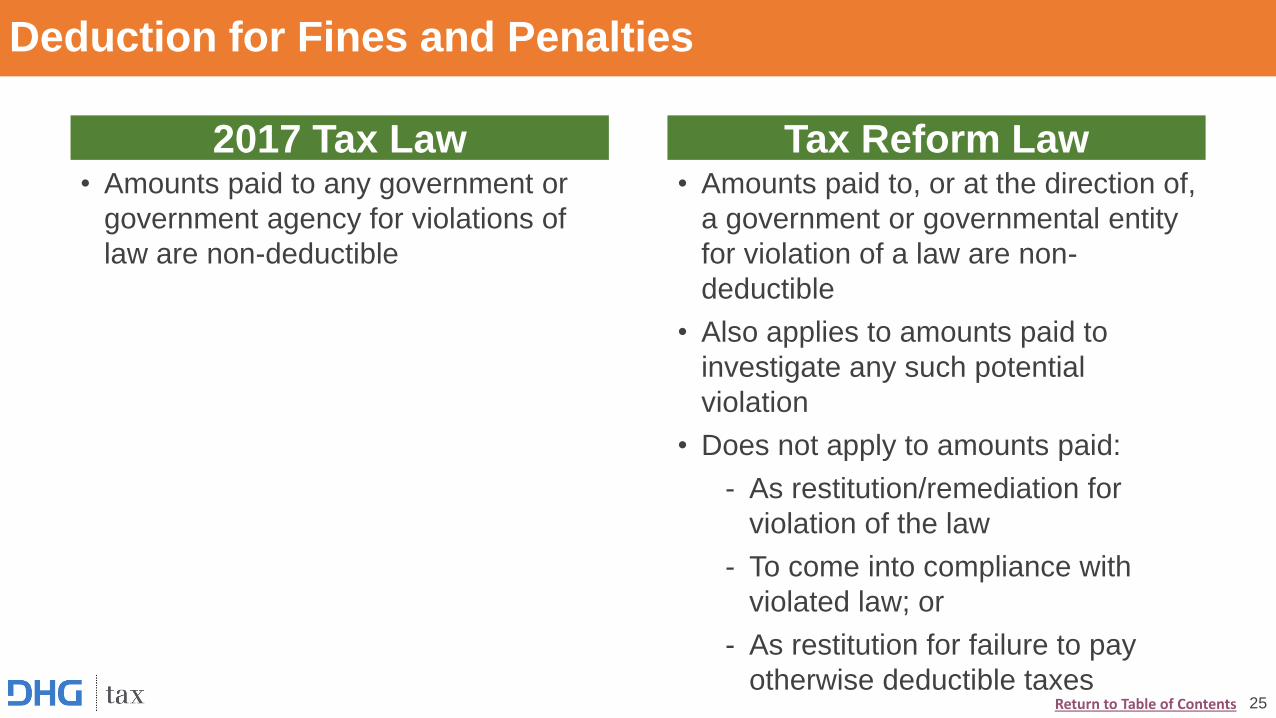

Deduction for Fines and Penalties

• Amounts paid to, or at the direction of,

a government or governmental entity

for violation of a law are non-

deductible

• Also applies to amounts paid to

investigate any such potential

violation

• Does not apply to amounts paid:

- As restitution/remediation for

violation of the law

- To come into compliance with

violated law; or

- As restitution for failure to pay

otherwise deductible taxes25

• Amounts paid to any government or

government agency for violations of

law are non-deductible

2017 Tax Law Tax Reform Law

Return to Table of Contents

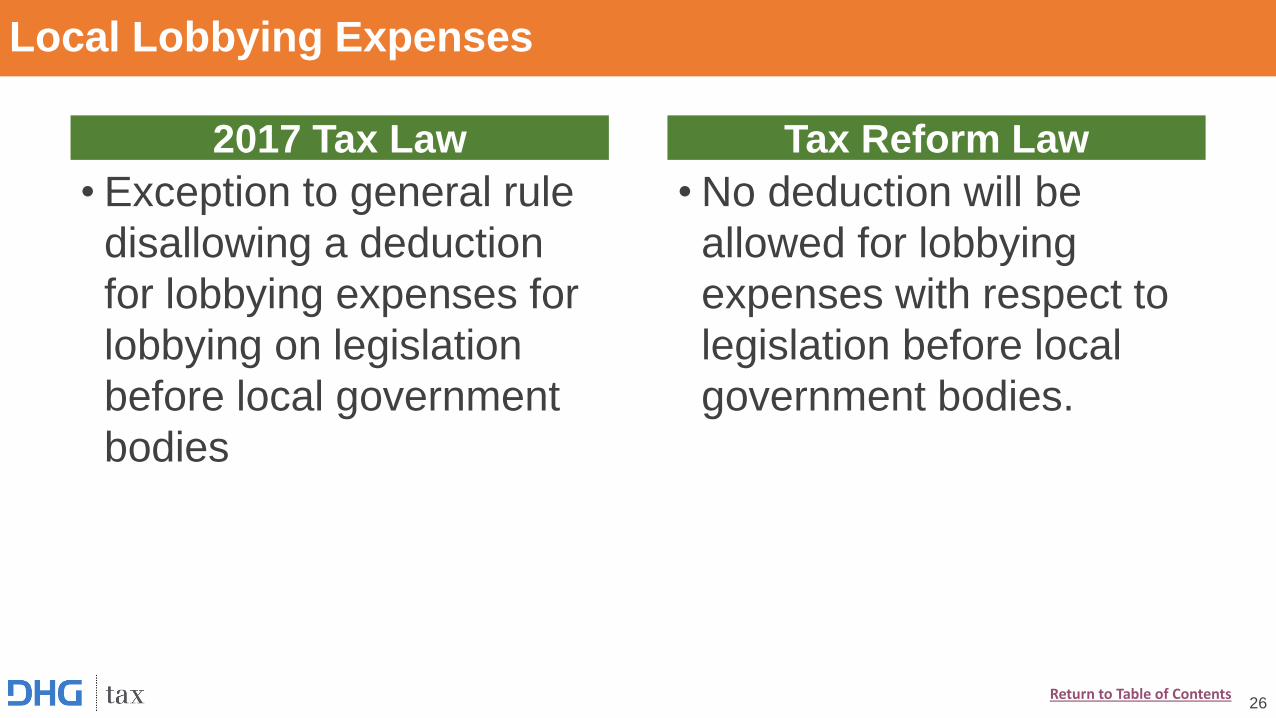

Local Lobbying Expenses

• No deduction will be

allowed for lobbying

expenses with respect to

legislation before local

government bodies.

26

• Exception to general rule

disallowing a deduction

for lobbying expenses for

lobbying on legislation

before local government

bodies

2017 Tax Law Tax Reform Law

Return to Table of Contents

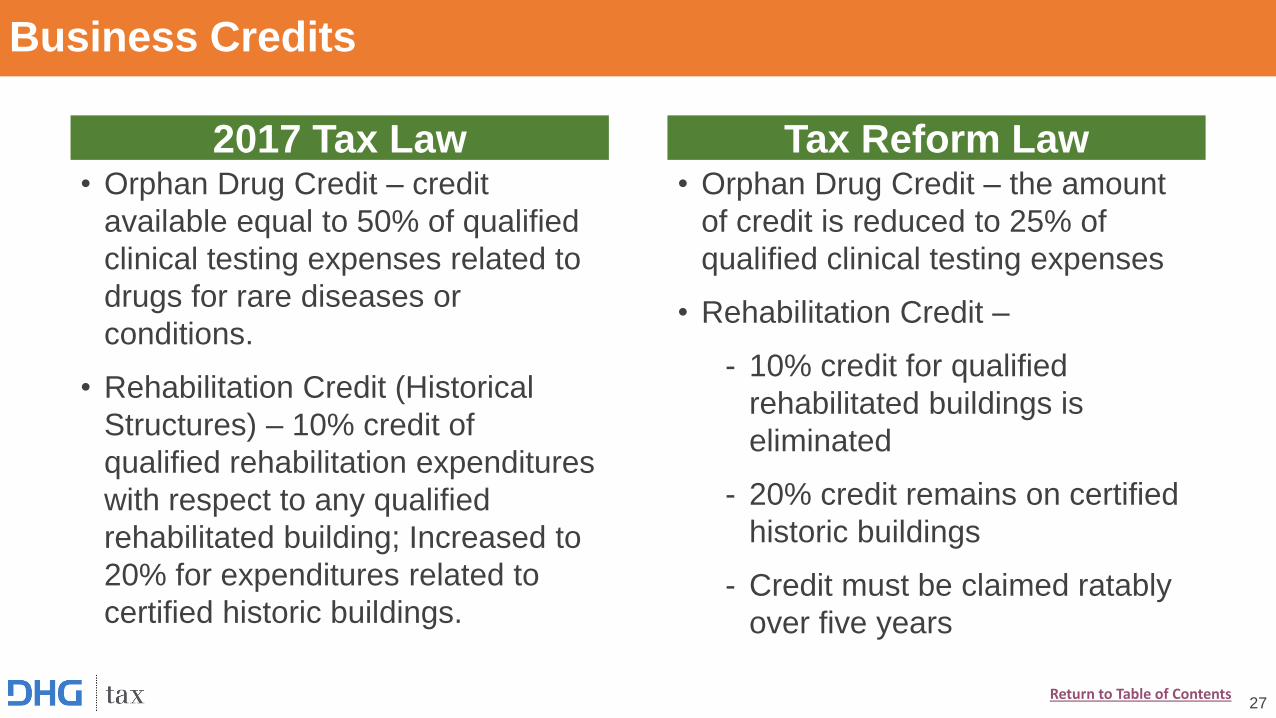

Business Credits

• Orphan Drug Credit – credit

available equal to 50% of qualified

clinical testing expenses related to

drugs for rare diseases or

conditions.

• Rehabilitation Credit (Historical

Structures) – 10% credit of

qualified rehabilitation expenditures

with respect to any qualified

rehabilitated building; Increased to

20% for expenditures related to

certified historic buildings.

• Orphan Drug Credit – the amount

of credit is reduced to 25% of

qualified clinical testing expenses

• Rehabilitation Credit –

- 10% credit for qualified

rehabilitated buildings is

eliminated

- 20% credit remains on certified

historic buildings

- Credit must be claimed ratably

over five years

27

2017 Tax Law Tax Reform Law

Return to Table of Contents

Business Credits (cont.)

• Employer credit for paid family and medical

leave – no credit existed in 2017

• Tax credit bonds – Taxpayers holding certain

bonds would receive tax credits in lieu of

interest payments from bond issuers.

• Employer credit for paid family and medical

leave –

- Eligible employers my claim a credit equal

to 12.5% of paid leave paid to qualifying

employees.

- Credit is increased by 0.25% for each

percentage point that wages paid during

qualifying leave exceeds 50% of the

wages normally paid to the employee.

- Maximum credit of 25%

• Tax credit bonds –

- Repealed; No new issuances after

12/31/2017

- Current holders of bonds issued prior to

12/31/2017 will continue to receive credits

2017 Tax Law Tax Reform Law

28Return to Table of Contents

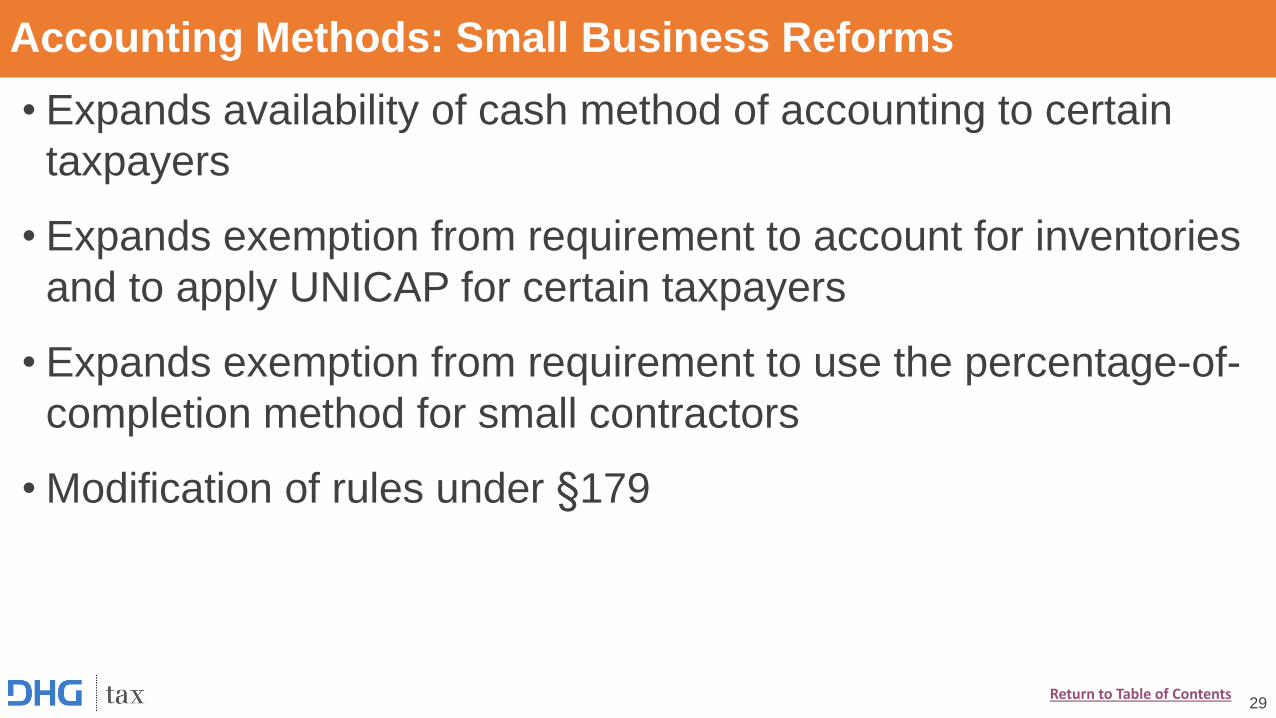

Accounting Methods: Small Business Reforms

• Expands availability of cash method of accounting to certain

taxpayers

• Expands exemption from requirement to account for inventories

and to apply UNICAP for certain taxpayers

• Expands exemption from requirement to use the percentage-of-

completion method for small contractors

• Modification of rules under §179

29Return to Table of Contents

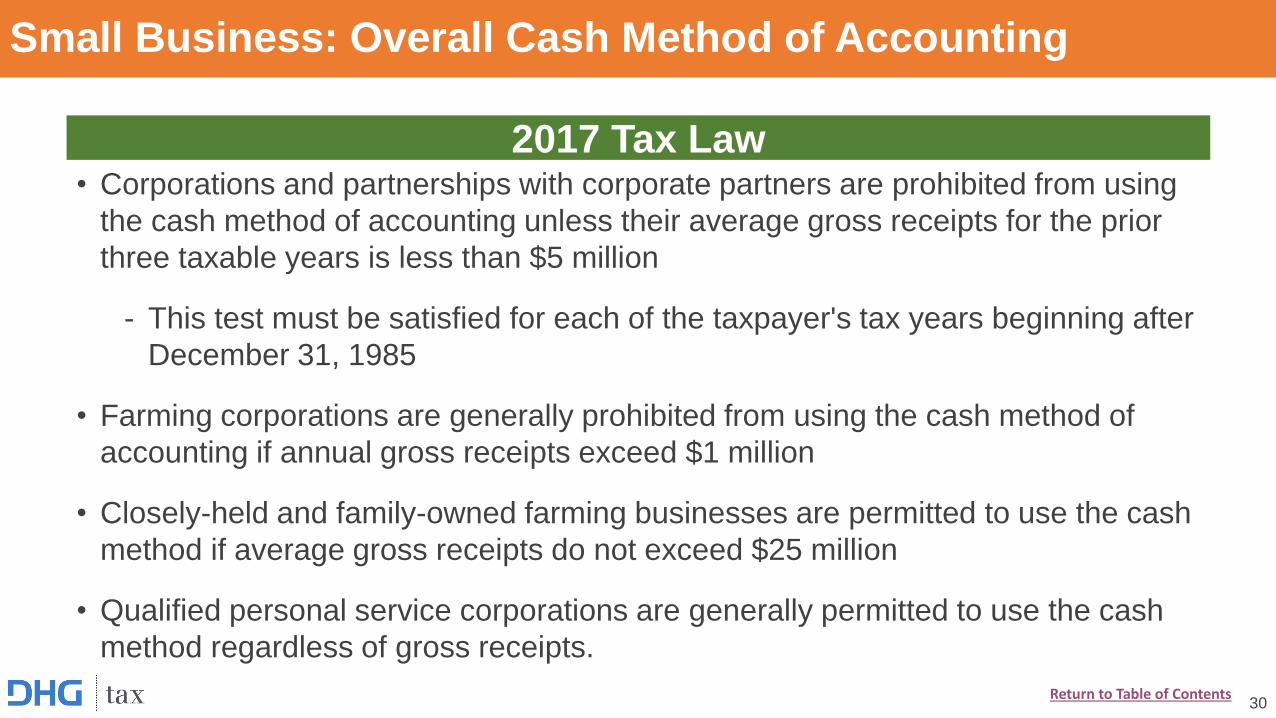

Small Business: Overall Cash Method of Accounting

30

• Corporations and partnerships with corporate partners are prohibited from using

the cash method of accounting unless their average gross receipts for the prior

three taxable years is less than $5 million

- This test must be satisfied for each of the taxpayer's tax years beginning after

December 31, 1985

• Farming corporations are generally prohibited from using the cash method of

accounting if annual gross receipts exceed $1 million

• Closely-held and family-owned farming businesses are permitted to use the cash

method if average gross receipts do not exceed $25 million

• Qualified personal service corporations are generally permitted to use the cash

method regardless of gross receipts.

2017 Tax Law

Return to Table of Contents

Tax Reform Law

Small Business: Overall Cash Method of Accounting (cont.)

31

• All taxpayers (other than tax shelters) with 3-year average gross receipts

less than $25 million (indexed for inflation) are permitted to use the cash

method of accounting

• Application of this provision constitutes a change in method of accounting

Return to Table of Contents

Small Business: Overall Cash Method of Accounting (cont.)

• Factors to consider when evaluating overall cash method:

- May be beneficial when Accounts Receivable are higher than Accounts

Payable (allows taxpayer to defer income)

- More flexibility with regard to timing of taxable income recognition

(taxpayer can write checks at end of the year or bill clients soon after

the close of the year to control expenses and income)

- Reduced administrative burden - assuming the taxpayer does not have

GAAP accrual-basis financial statements

- Gives a better indication of cash on hand

32Return to Table of Contents

2017 Tax Law

Small Business: Inventories

33

• Any business in which the production, purchase, or sale of merchandise is a

material income-producing factor must generally account for inventories at the

beginning and ending of each year

• Affected businesses must also use the accrual method of accounting for

purchases and sales of inventory

• Taxpayers in qualifying trades or businesses may account for inventory as

materials and supplies that are not incidental if average gross receipts for the

prior three taxable years does not exceed $10 million

- Must not otherwise be prohibited from using the cash method as overall

method of accounting under §448

Return to Table of Contents

Tax Reform Law

Small Business: Inventories (cont.)

34

• All taxpayers (other than tax shelters) with 3-year average gross

receipts less than $25 million (indexed for inflation) are exempt from the

requirement to account for inventories

• Eligible taxpayers may either treat inventories as materials and supplies

that are not incidental or conform to the taxpayer’s financial accounting

treatment

- Non-incidental materials and supplies are deducted as consumed or

utilized in the taxpayer’s operations

• Application of this provision constitutes a change in method of

accounting

Return to Table of Contents

Small Business: Inventories Example

FACTS

• Corporate Taxpayer producing wooden canoes

• Average annual gross receipts: $20M

• Annual purchases are fully consumed during the year of purchase – but

20% remains on-hand in the form of canoes in process

• Annual wood purchases as follows:

Year 1 Year 2 Year 3

$7,000,000 $9,000,000 $8,000,000

35Return to Table of Contents

Small Business: Inventories Example

• Accounting for inventory under accrual method:

• Accounting for inventory as non-incidental materials and supplies

Year 1 Year 2 Year 3

(A) Beginning Inventory $ - $1,400,000 $1,800,000

(B) Purchases 7,000,000 9,000,000 8,000,000

(C) Ending Inventory (20% of Purchases) 1,400,000 1,800,000 1,600,000

Cost of Goods Sold (A) + (B) – (C) $5,600,000 $8,600,000 $8,200,000

Year 1 Year 2 Year 3

Purchases $7,000,000 $9,000,000 $8,000,000

Consumed (100% of Purchases) 7,000,000 9,000,000 8,000,000

Cost of Goods Sold = Amount Consumed $7,000,000 $9,000,000 $8,000,000

Difference in Taxable Income

(Compared to accrual method)($1,400,000) ($400,000) $200,000

36Return to Table of Contents

Small Business: UNICAP

37

• Taxpayers must capitalize certain direct and indirect costs related

to real or tangible property, whether produced or acquired for

resale

• Qualifying resellers whose average annual gross receipts do not

exceed $10,000,000 are generally exempt from these

requirement with respect to personal property acquired for resale

• Other taxpayers may be exempt from the requirements of IRC

263A based on certain industry classification or other limited

exceptions

2017 Tax Law

Return to Table of Contents

Tax Reform Law

Small Business: UNICAP (cont.)

38

• All taxpayers (other than tax shelters) with 3-year

average gross receipts less than $25 million (indexed for

inflation) are exempt from the capitalization rules of IRC

263A

• Application of this provision constitutes a change in

method of accounting

Return to Table of Contents

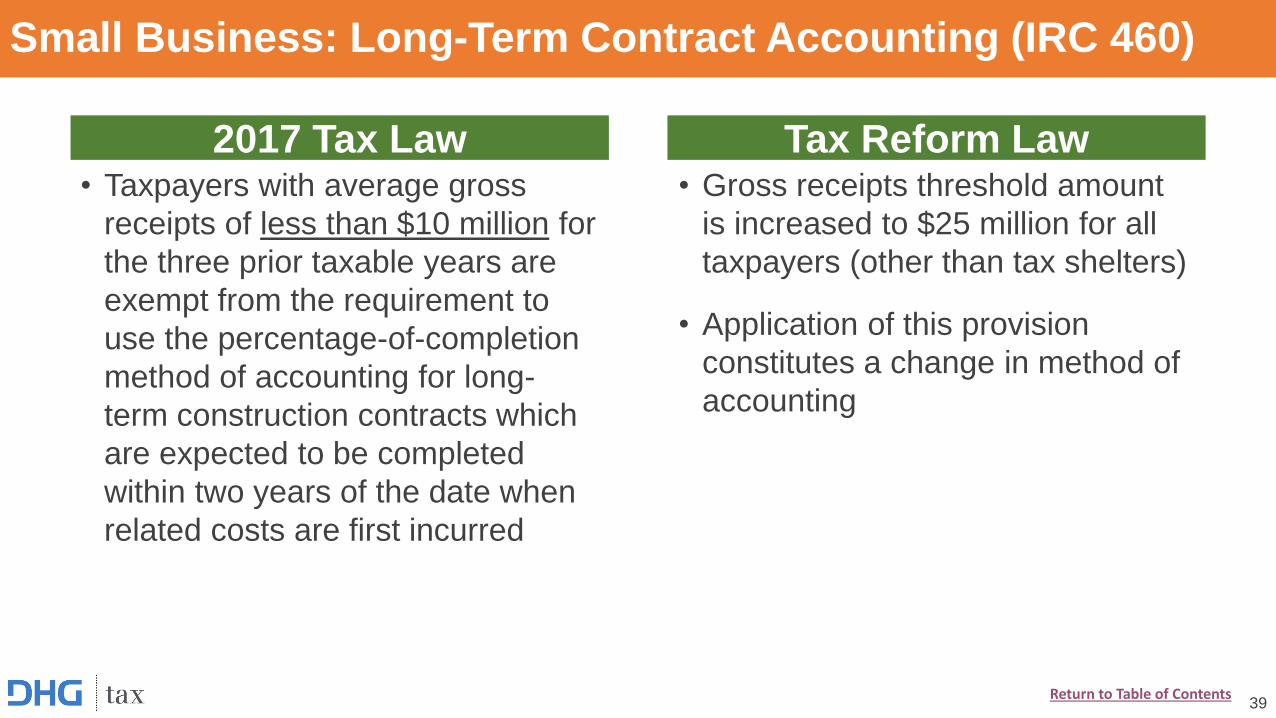

Small Business: Long-Term Contract Accounting (IRC 460)

• Gross receipts threshold amount

is increased to $25 million for all

taxpayers (other than tax shelters)

• Application of this provision

constitutes a change in method of

accounting

39

• Taxpayers with average gross

receipts of less than $10 million for

the three prior taxable years are

exempt from the requirement to

use the percentage-of-completion

method of accounting for long-

term construction contracts which

are expected to be completed

within two years of the date when

related costs are first incurred

2017 Tax Law Tax Reform Law

Return to Table of Contents

Other Accounting Methods Opportunities

• Even though many of these provisions are not effective

until 2018, taxpayers should explore opportunities to

accelerate deductions into to 2017 and defer income into

2018

• Not just timing! Will result in permanent tax savings

due to lowering of income tax rate

40Return to Table of Contents

Creating Value Through Deferral

EXAMPLE

Taxpayer recognizes revenue ratably as work is performed. Taxpayer changes its method to

recognize revenue when earned (e.g., when work is complete or product is delivered).

Taxpayer projects steady business activity and revenue going forward.

41

Year 1 Year 2 Year 3 Years 4-10 Total Final Year

Current Method 1,000 1,000 1,000 7,000 10,000 -

New Method 750 750 750 5,250 7,500 -

Recognize PY Deferral - 250 250 1,750 2,250 250

Total 750 1,000 1,000 7,000 9,750 250

Difference (250) - - - (250) 250

Tax Savings @ 35% (88) - - - (88) 88

Note: Example does not take into account IRR on cash tax savings. The

opportunity to generate significant benefit is greater than illustrated here! Return to Table of Contents

Creating Value Through Deferral

EXAMPLE

Same facts, but assume tax rate is 35% in Year 1 and is reduced to 21% in Year 2 and beyond.

42

Year 1 Year 2 Year 3 Years 4-10 Total Final Year

Current Method 1,000 1,000 1,000 7,000 10,000 -

35% 21% 21% 21% 21%

350 210 210 1,470 2,240 -

New Method 750 750 750 5,250 7,500 -

Recognize PY Deferral 0 250 250 1,750 2,250 250

Total 750 1,000 1,000 7,000 9,750 250

35% 21% 21% 21% 21%

263 210 210 1,470 2,153 53

Annual Tax Savings 88 - - - 88 (53)

Permanent Tax Savings 35

Note: Example does not take into account IRR on cash tax savings. The

opportunity to generate significant benefit is greater than illustrated here!Return to Table of Contents

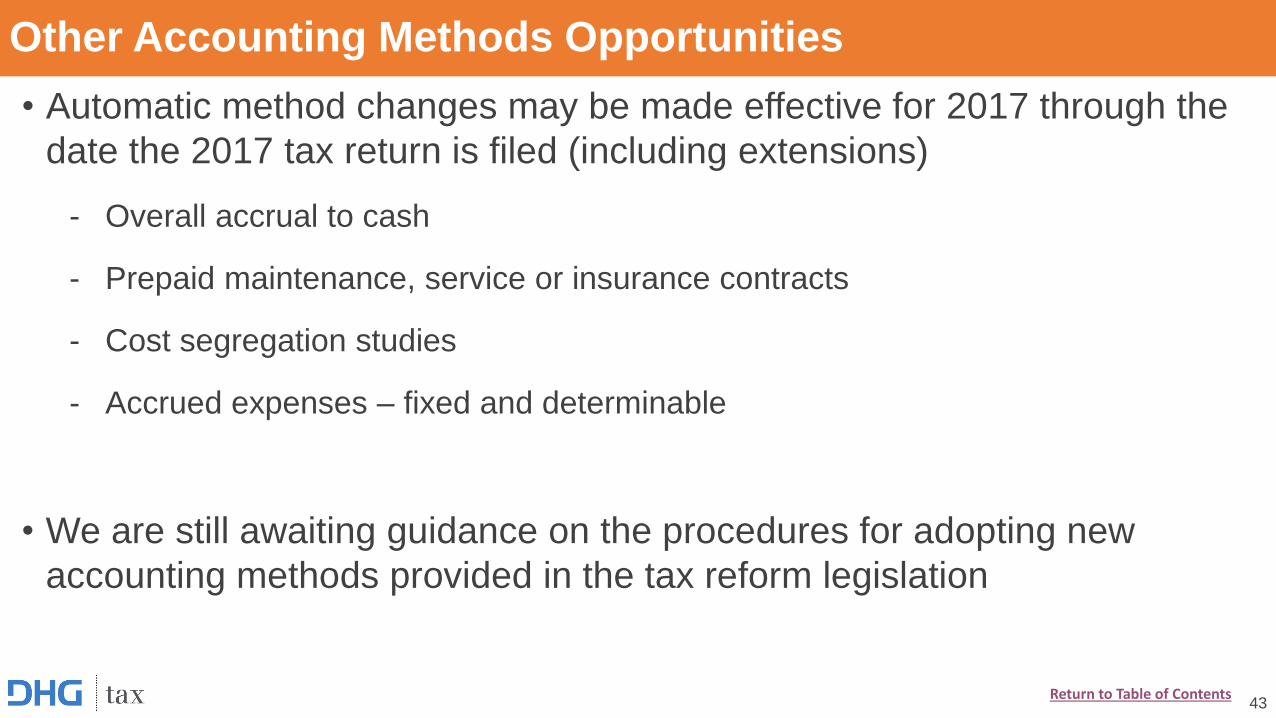

Other Accounting Methods Opportunities

• Automatic method changes may be made effective for 2017 through the

date the 2017 tax return is filed (including extensions)

- Overall accrual to cash

- Prepaid maintenance, service or insurance contracts

- Cost segregation studies

- Accrued expenses – fixed and determinable

• We are still awaiting guidance on the procedures for adopting new

accounting methods provided in the tax reform legislation

43Return to Table of Contents

Tax Reform: Impact on

Financial StatementsJeremy Betsill, Assurance Partner

Tax Reform Headlines

45Return to Table of Contents

Tax Reform Headlines

46Return to Table of Contents

• Enacted date vs. effective date

• Re-measurement of deferred taxes

• International tax considerations

FINANCIAL STATEMENT CONSIDERATIONS

Return to Table of Contents

Enacted Date vs Effective Date

DEFINITIONS

• Enacted

- The date the legislation is signed into law

• Effective

- The date the legislation (law) takes effect

48Return to Table of Contents

Enacted Date vs Effective Date

“The President signed the bill into law on December 22, 2017. The

new rates apply to tax years beginning on or after January 1, 2018.”

• Enacted Date: December 22, 2017

• Effective Date: January 1, 2018

49Return to Table of Contents

ASC 740: Enacted Date vs. Effective Date

• “The effect of a change in tax laws or rates shall be recognized at the

date of enactment.”

• Implications:

- Current taxes will remain under OLD tax regulations for 2017 since

new law not effective until January 1, 2018.

- However, deferred tax assets and liabilities shall be adjusted for the

effect of a change in tax laws or rates in the period enacted (i.e. 2017).

50Return to Table of Contents

Current vs Deferred Taxes

• Current Taxes –tax effects that are taxable or deductible in the

current reporting period.

• Deferred Taxes - tax effects that will lead to taxable income or

tax deductions in future periods.

- GAAP requires deferred tax liability or asset to be recognized for the estimated future tax effects attributable to temporary differences and carryforwards.

51Return to Table of Contents

Fiscal Year Ends (non-calendar)

• If a law is enacted subsequent to the balance sheet date but

prior to issuance of the financial statements, it is considered a

non-recognized subsequent event

• Example:

- Legislation enacted December 22, 2017 would be a non-

recognized subsequent event for a corporation with a

November 30th fiscal year end

52Return to Table of Contents

Re-measurement of Deferred Taxes

• Applies to C-corporations, pass-through entities (S-corps, LLC, etc.) are

generally not subject to tax at the entity level

• Corporate rate of 21% for deferred tax assets and liabilities expected to

reverse after 12/31/2017

• Blended statutory tax rate for fiscal year taxpayers

- Portion of year at 35%, portion at 21%

• Reduced federal benefit on state effective tax rates

• For U.S. GAAP purposes, all re-measurement effects of deferred tax

balances should be recorded to income from continuing operations as of

the enactment date

53Return to Table of Contents

Re-measurement of Deferred Taxes (cont.)

MECHANICS OF RE-MEASUREMENT AT DATE OF ENACTMENT

• Obtain U.S. deferred tax balances as of enactment date

- In practice, one may expect to use 12/31/2017 balances as

that may be the best information available

• Schedule the reversal of the deferred tax balances in the future

• Re-measure effect of temporary differences and carryforwards at

new corporate tax rate of 21%.

54Return to Table of Contents

Re-measurement of Deferred Taxes (cont.)

• Rate change may result in disproportionate tax effects being

lodged in OCI

- Could apply to various other items that are accounted for

through OCI, such as unrealized gains or losses derived from

pensions, currency translation, available-for-sale securities,

etc.

• FASB recently issued a proposed ASU that allows a reclass from

AOCI to retained earnings for the "lodged" tax effect that will

reside in AOCI.

55Return to Table of Contents

Re-measurement of Deferred Taxes – Example

Reduction of DTA = $140,000 charged to earnings through deferred tax expense

56

OLD Rate Tax Reform

NOL carryforward $1,000,000 $1,000,000

Tax rate 35% 21%

Deferred tax asset $350,000 $210,000

Return to Table of Contents

Net Operating Loss DTA Considerations

• Applicable for NOLs generated after 1/1/2018

• NOL utilization limited to 80% of taxable income

• NOL carrybacks eliminated

• NOL carryforward period is indefinite

• Note: NOL changes to be considered in ability to utilize NOL

carryforwards and need for valuation allowance

57Return to Table of Contents

Multinational Considerations

• New law creates one-time transition tax on undistributed foreign earnings (since 1986)

• “Unremitted Foreign Earnings” is a GAAP concept, based on book earnings

• “Earnings and Profits” (E&P) is a tax concept, based on U.S. tax rules

• Caution:

- In practice, the two above measures often vary by only an immaterial amount and differences between the two are often disregarded for ease of computation

58Return to Table of Contents

One-Time Transition Tax – Deemed Repatriation

• One-time transition tax on accumulated foreign earnings (E&P)

• Cash and Cash Equivalents taxed at 15.5%

• Operating Assets taxed at 8%

• Tax recorded in graduated installments over 8 years

- Record tax payable balance as of 12/31/2017

- Consider classification as current vs. non-current payable due

to 8-year payment period.

59Return to Table of Contents

SEC Implementation Guidance

• SEC guidance provides a “measurement period” for issuers to

evaluate the impacts of tax reform on their financial statements

• Measurement period not to extend beyond one year from the

enactment date

• During the measurement period, the SEC Staff expect that

entities will be acting in good faith to complete the accounting

under ASC Topic 740

• Applies to publicly traded companies, may be used as guideline

for privately-held companies

60Return to Table of Contents

Other Changes Impacting Businesses

• Cost Recovery

• Limitation on Deduction of Interest

• Meals and Entertainment Expenses

• State Tax Conformity

• International Implications

62

OTHER CHANGES IMPACTING BUSINESSES

Other Changes Impacting Businesses:

Cost RecoveryRachel Nightengale, Tax Manager

• Increased expensing

- Bonus depreciation

- Section 179 expensing

• Changes to recovery periods for real property

• Modifications to depreciation limitations on luxury automobiles and

personal use property

• Research and experimental expenses

• Planning considerations

64

COST RECOVERY

Bonus Depreciation

• Allows a 50% bonus depreciation deduction for first year placed in service

• Applies to new property only

• Not limited to taxable income of the entity

• Qualified property includes property with a MACRS life of 20 years or less

• Qualified property includes:

- Property with a MACRS life of 20 years or less

- Qualified leasehold improvement property

- Certain qualified restaurant property

- Certain qualified retail improvement property

- Limitations apply to self rental or owner occupied property

65

2017 Tax Law

Return to Table of Contents

Bonus Depreciation (cont.)

• Allows a 100% bonus depreciation deduction for first year placed in

service

• Applies to new and used property

• Not limited to taxable income of the entity

• Qualified property - Technical issues discussed later

• Applies to property acquired and placed in service after September 27,

2017, subject to binding contract rules

• Phased down by 20% each year beginning in 2023 until completely

phased on in 2027

66

Tax Reform Law

Return to Table of Contents

Bonus Depreciation – Binding Contracts

• Eligible property must be both acquired and placed in service after 9/27/2017

• Eligible property is considered acquired after 9/27/2017 only if there was not a written binding

contract prior to the acquisition date

• Requirements of a binding contract:

- Enforceable under state law

- Does not limit damages to a specified amount

- Any conditions are not within control of either party

- Any changes to conditions are insubstantial

- Supply agreements must include the amount and design specifications of the purchase to

be binding

- Purchasing a component or components of a larger asset is not considered a binding

agreement to purchase the larger asset

• Note: An option to buy property is not considered a binding contract

67Return to Table of Contents

Bonus Depreciation – Effective Dates and Allowances

68

Date Applicable Percentage

Acquired before Sept. 27, 2017 50%

Acquired and placed in service after Sept. 27, 2017, and before January 1, 2023 100%

Acquired and placed in service after Sept. 27, 2017, and before Dec. 31, 2022

with an election made to use 50% rather than 100%50%

Acquired after December 31, 2022, and PIS in before January 1, 2024 80%

Acquired after December 31, 2023, and PIS in before January 1, 2025 60%

Acquired after December 31, 2024, and PIS before January 1, 2026 40%

Acquired after December 31, 2025, and PIS before January 1, 2027 20%

PIS on or after January 1, 2027 0%

Return to Table of Contents

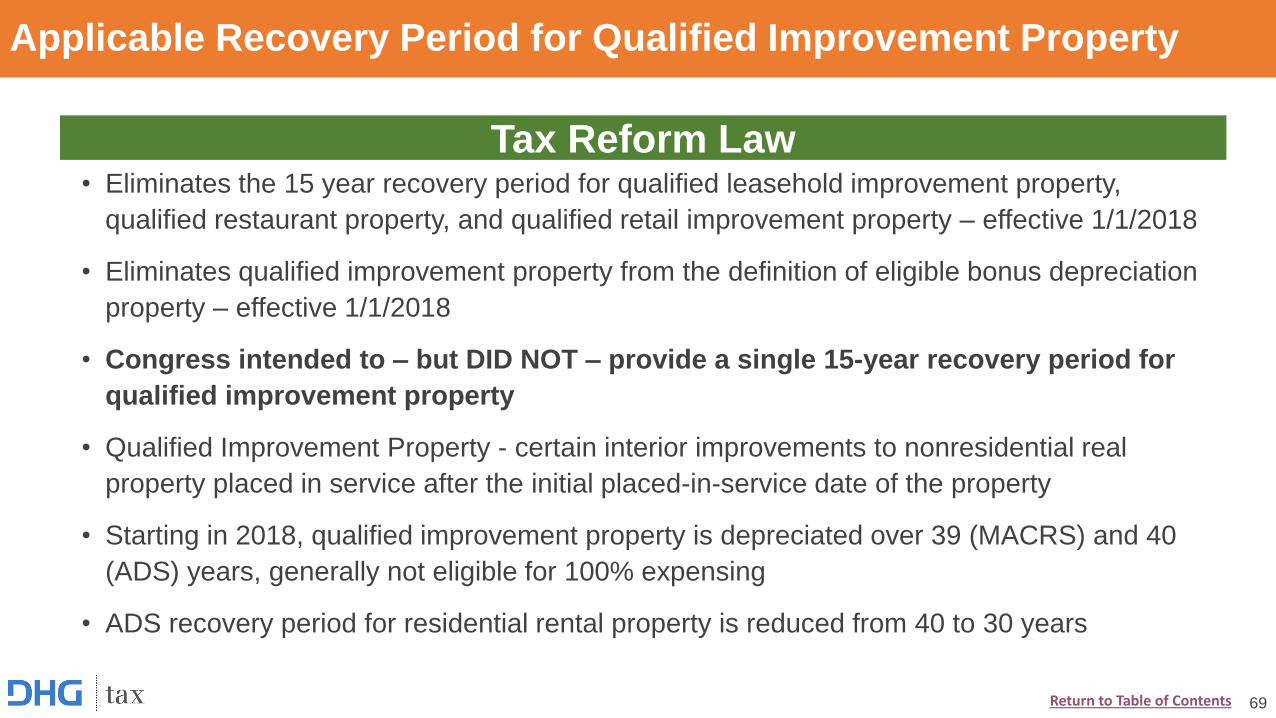

Applicable Recovery Period for Qualified Improvement Property

• Eliminates the 15 year recovery period for qualified leasehold improvement property,

qualified restaurant property, and qualified retail improvement property – effective 1/1/2018

• Eliminates qualified improvement property from the definition of eligible bonus depreciation

property – effective 1/1/2018

• Congress intended to – but DID NOT – provide a single 15-year recovery period for

qualified improvement property

• Qualified Improvement Property - certain interior improvements to nonresidential real

property placed in service after the initial placed-in-service date of the property

• Starting in 2018, qualified improvement property is depreciated over 39 (MACRS) and 40

(ADS) years, generally not eligible for 100% expensing

• ADS recovery period for residential rental property is reduced from 40 to 30 years

69

Tax Reform Law

Return to Table of Contents

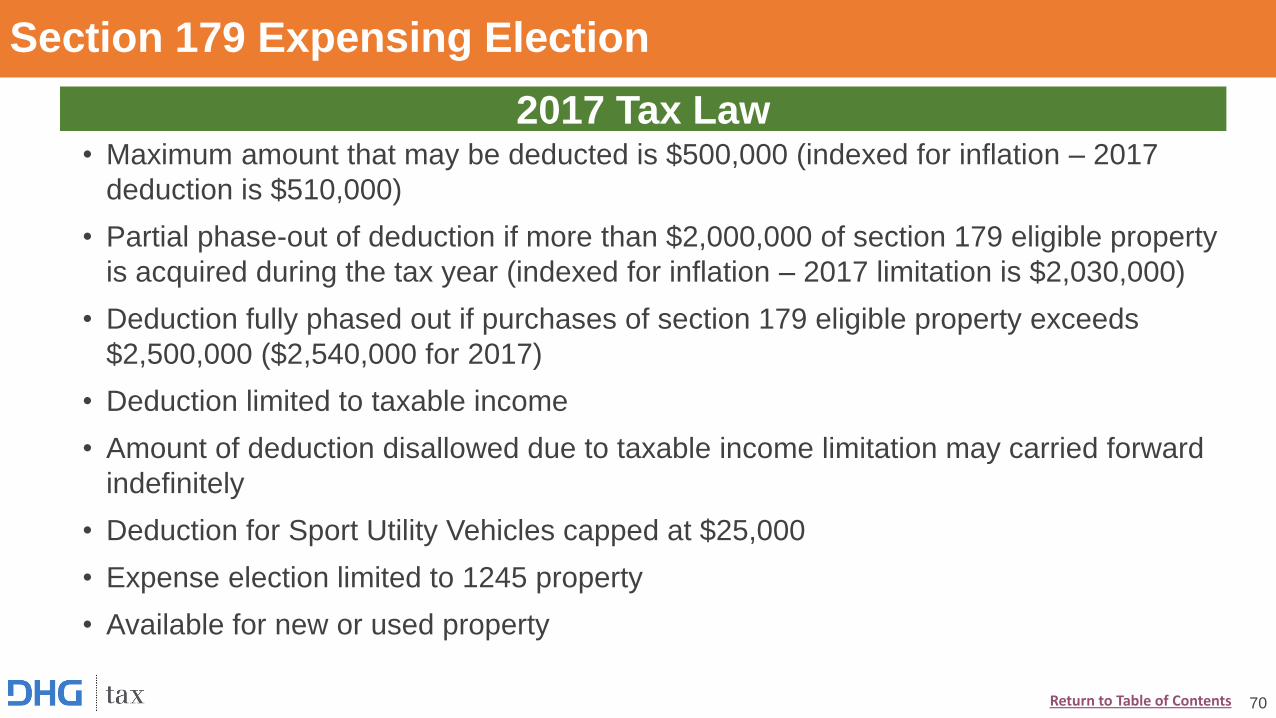

Section 179 Expensing Election

• Maximum amount that may be deducted is $500,000 (indexed for inflation – 2017

deduction is $510,000)

• Partial phase-out of deduction if more than $2,000,000 of section 179 eligible property

is acquired during the tax year (indexed for inflation – 2017 limitation is $2,030,000)

• Deduction fully phased out if purchases of section 179 eligible property exceeds

$2,500,000 ($2,540,000 for 2017)

• Deduction limited to taxable income

• Amount of deduction disallowed due to taxable income limitation may carried forward

indefinitely

• Deduction for Sport Utility Vehicles capped at $25,000

• Expense election limited to 1245 property

• Available for new or used property

70

2017 Tax Law

Return to Table of Contents

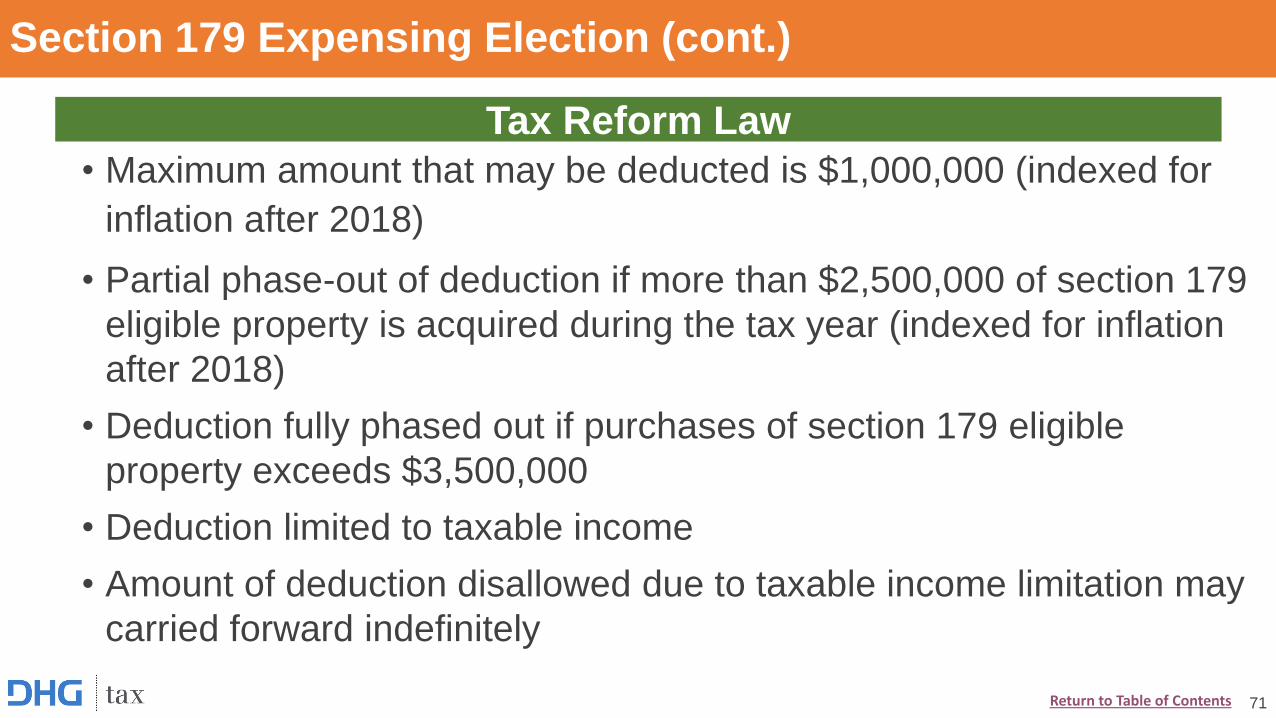

Section 179 Expensing Election (cont.)

• Maximum amount that may be deducted is $1,000,000 (indexed for

inflation after 2018)

• Partial phase-out of deduction if more than $2,500,000 of section 179

eligible property is acquired during the tax year (indexed for inflation

after 2018)

• Deduction fully phased out if purchases of section 179 eligible

property exceeds $3,500,000

• Deduction limited to taxable income

• Amount of deduction disallowed due to taxable income limitation may

carried forward indefinitely

71

Tax Reform Law

Return to Table of Contents

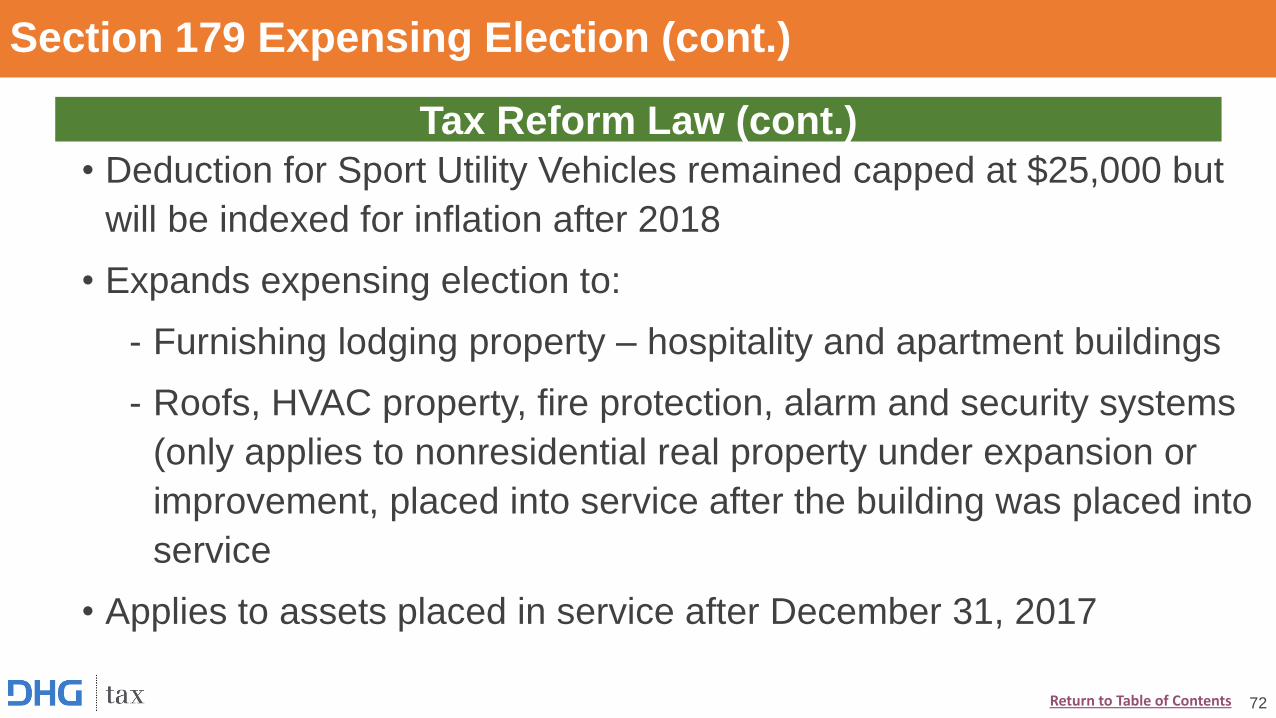

Section 179 Expensing Election (cont.)

• Deduction for Sport Utility Vehicles remained capped at $25,000 but

will be indexed for inflation after 2018

• Expands expensing election to:

- Furnishing lodging property – hospitality and apartment buildings

- Roofs, HVAC property, fire protection, alarm and security systems

(only applies to nonresidential real property under expansion or

improvement, placed into service after the building was placed into

service

• Applies to assets placed in service after December 31, 2017

72

Tax Reform Law (cont.)

Return to Table of Contents

Cost Recovery Life Comparison

Life Classification

27.5 Years Residential (MACRS)

40 Years Residential (ADS)

39 Years Nonresidential (MACRS)

40 Years Nonresidential (ADS)

15 years Qualified Leasehold Improvement

(MACRS)

15 Years Qualified Restaurant Property (MACRS)

15 Years Qualified Retail Improvement (MACRS)

39 Years Qualified Leasehold Improvement (ADS)

39 Years Qualified Restaurant Property (ADS)

39 Years Qualified Retail Improvement (ADS)

Life Classification

27.5 Years Residential (MACRS)

30 Years Residential (ADS)

39 Years Nonresidential (MACRS)

40 Years Nonresidential (ADS)

39 Years Qualified Improvement Property

(MACRS)

40 years Qualified Improvement Property (ADS)

Sec. 179 Roof, HVAC, Fire Protection, Security

and Alarm Systems – Not original UOP

73

2017 Tax Law 2018 Tax Law

Return to Table of Contents

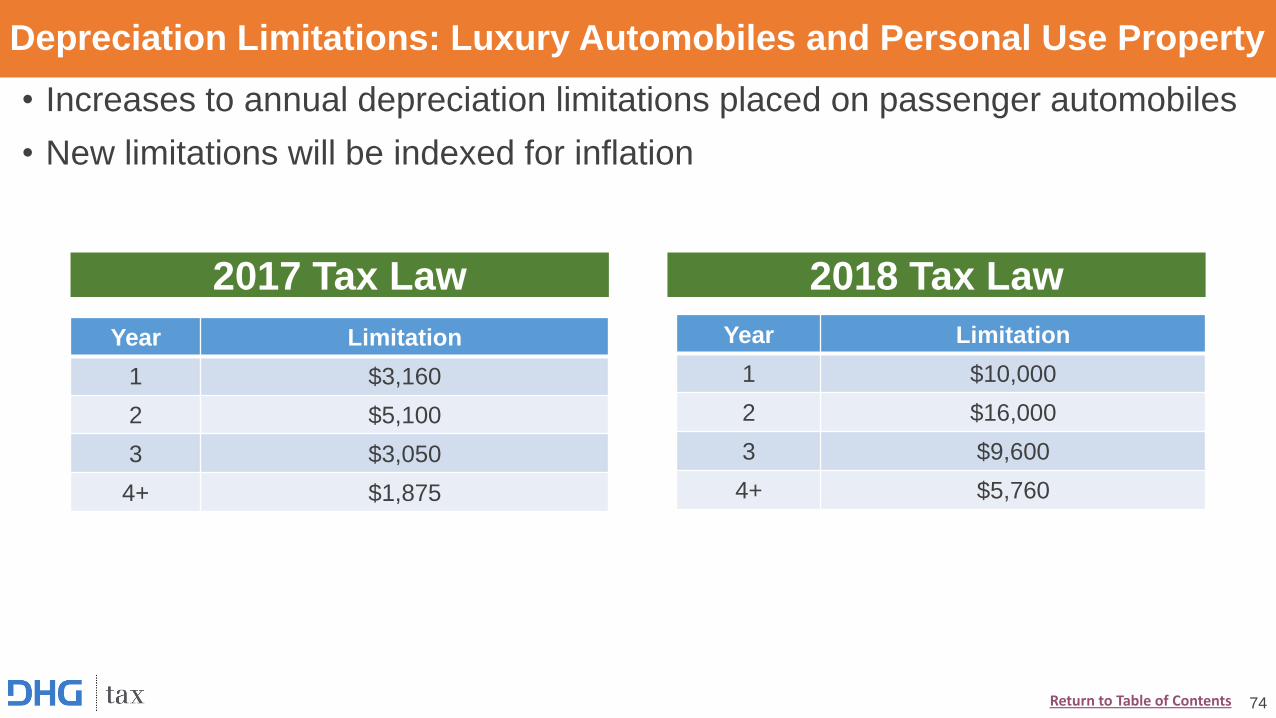

Depreciation Limitations: Luxury Automobiles and Personal Use Property

• Increases to annual depreciation limitations placed on passenger automobiles

• New limitations will be indexed for inflation

74

Year Limitation

1 $3,160

2 $5,100

3 $3,050

4+ $1,875

2017 Tax Law 2018 Tax Law

Year Limitation

1 $10,000

2 $16,000

3 $9,600

4+ $5,760

Return to Table of Contents

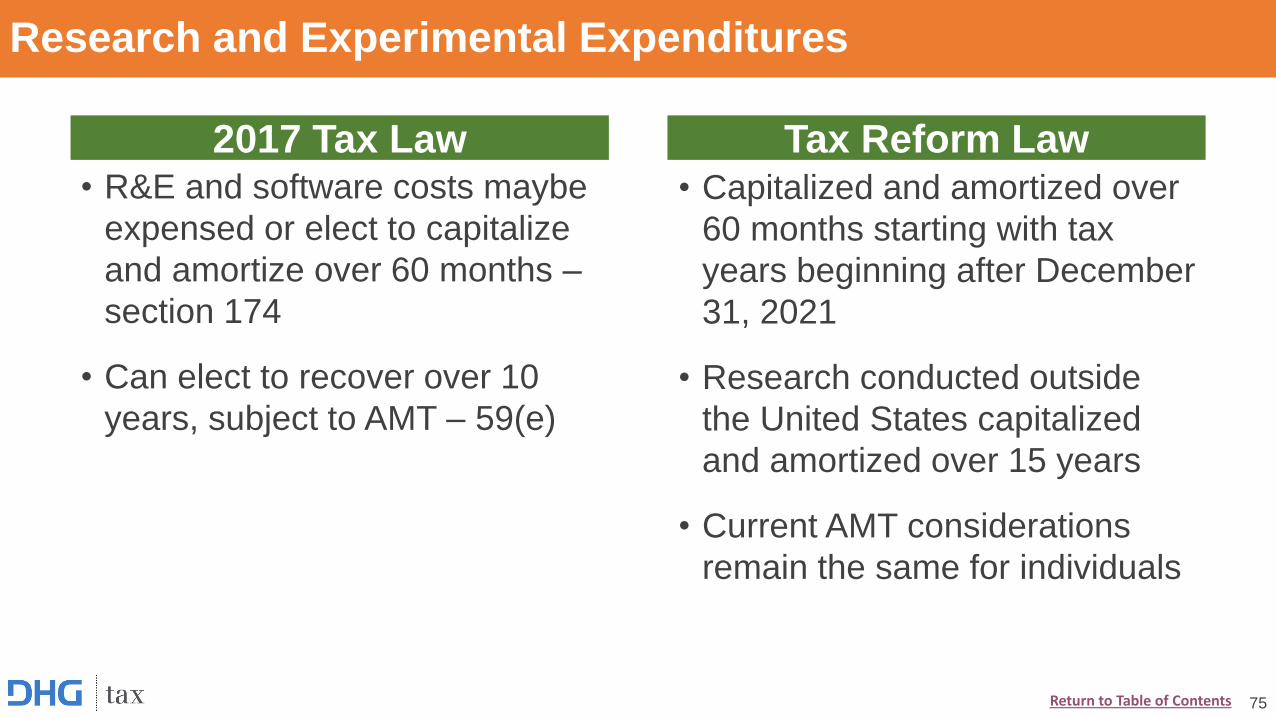

Research and Experimental Expenditures

• R&E and software costs maybe

expensed or elect to capitalize

and amortize over 60 months –

section 174

• Can elect to recover over 10

years, subject to AMT – 59(e)

75

2017 Tax Law Tax Reform Law• Capitalized and amortized over

60 months starting with tax

years beginning after December

31, 2021

• Research conducted outside

the United States capitalized

and amortized over 15 years

• Current AMT considerations

remain the same for individuals

Return to Table of Contents

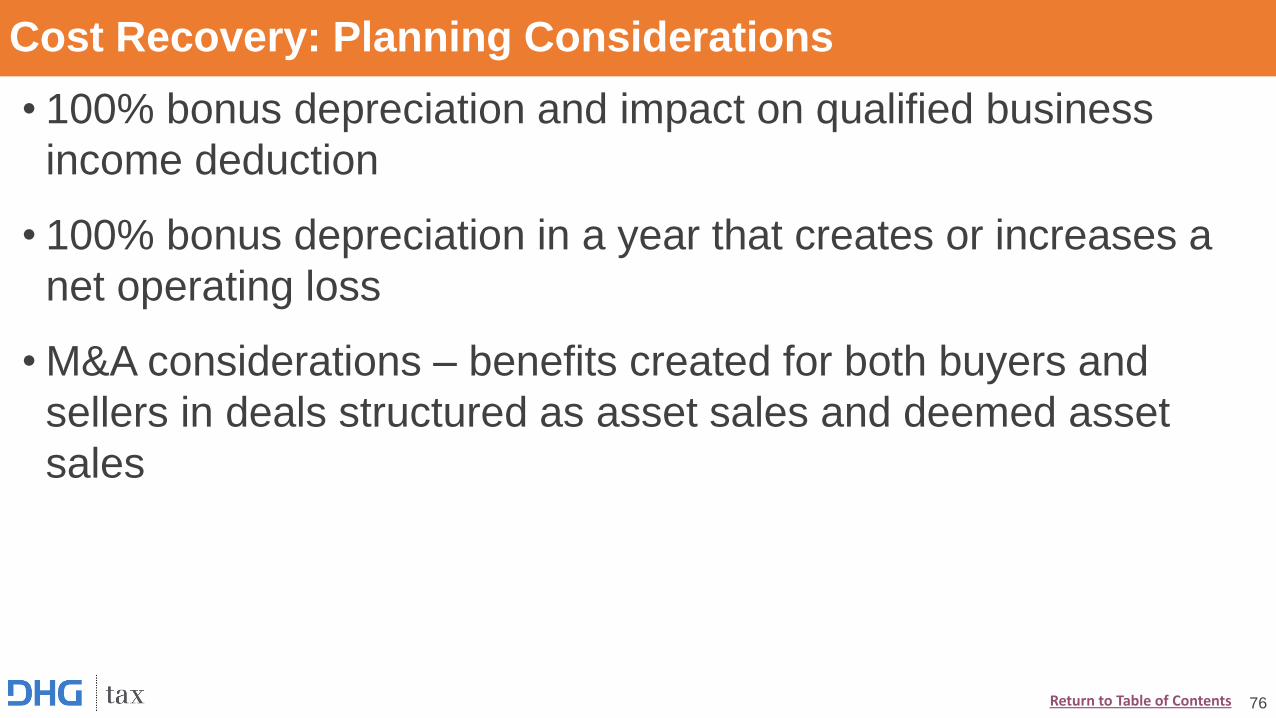

Cost Recovery: Planning Considerations

• 100% bonus depreciation and impact on qualified business

income deduction

• 100% bonus depreciation in a year that creates or increases a

net operating loss

• M&A considerations – benefits created for both buyers and

sellers in deals structured as asset sales and deemed asset

sales

76Return to Table of Contents

Other Changes Impacting Businesses:

Limitation on Deduction of InterestTracey Erbe, Tax Manager

Business Interest Expense

• Business interest expense is generally

deductible, subject to certain

limitations

78

2017 Tax Law Tax Reform Law• Limits the deduction of business interest

expense in excess of:

- Business interest income, plus

- 30% of business adjusted taxable

income, plus

- Floor plan financing interest

• Any disallowed interest expense is carried

forward indefinitely

• Does not apply to floor-plan financing

interest

• Defined formula for adjusted taxable income

• Defined business interest expense and

business interest income

Return to Table of Contents

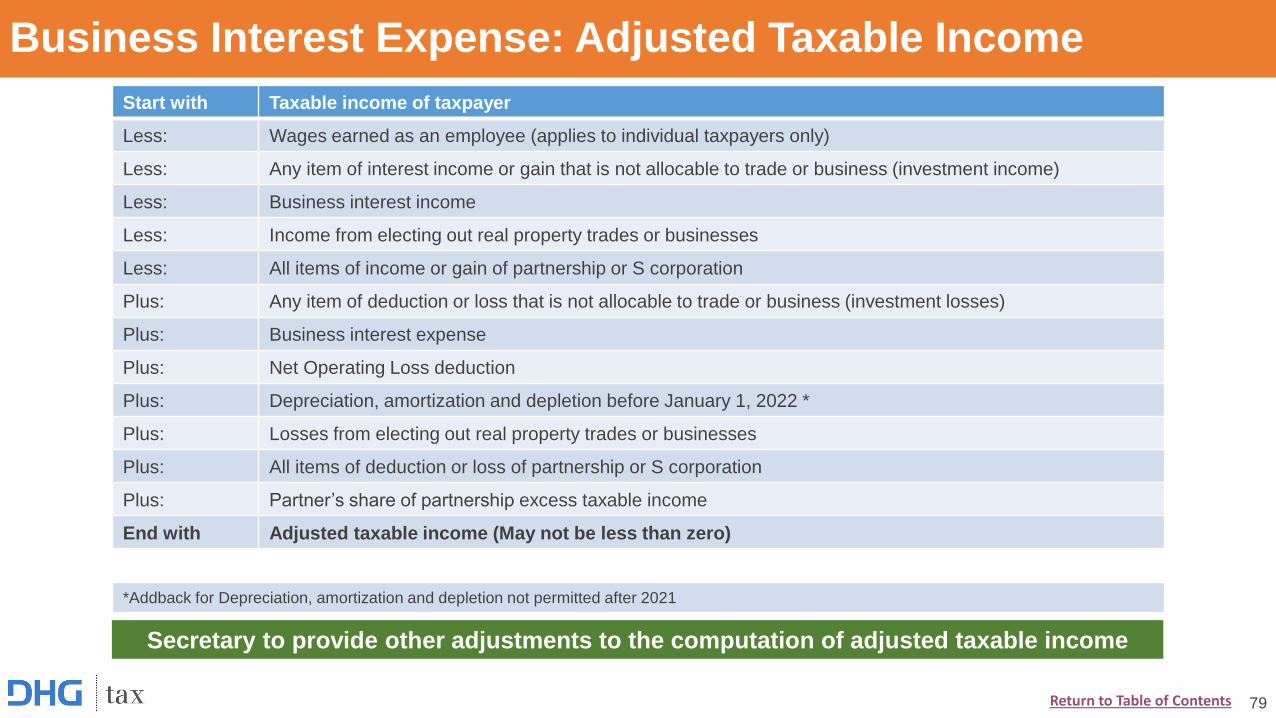

Business Interest Expense: Adjusted Taxable Income

Start with Taxable income of taxpayer

Less: Wages earned as an employee (applies to individual taxpayers only)

Less: Any item of interest income or gain that is not allocable to trade or business (investment income)

Less: Business interest income

Less: Income from electing out real property trades or businesses

Less: All items of income or gain of partnership or S corporation

Plus: Any item of deduction or loss that is not allocable to trade or business (investment losses)

Plus: Business interest expense

Plus: Net Operating Loss deduction

Plus: Depreciation, amortization and depletion before January 1, 2022 *

Plus: Losses from electing out real property trades or businesses

Plus: All items of deduction or loss of partnership or S corporation

Plus: Partner’s share of partnership excess taxable income

End with Adjusted taxable income (May not be less than zero)

*Addback for Depreciation, amortization and depletion not permitted after 2021

79

Secretary to provide other adjustments to the computation of adjusted taxable income

Return to Table of Contents

Business Interest

DEFINITION OF BUSINESS INTEREST

• Business Interest Income

- The amount of interest includible in the taxpayer's gross income and allocable to a

trade or business

• Business Interest Expense

- Any interest paid or accrued on indebtedness properly allocable to a trade or business

- Does not include investment interest

- “Floor plan financing interest” is excluded from limitation

Defined as interest associated with indebtedness to finance self-propelled vehicle,

boat, or farm machinery or equipment held for sale or lease

80Return to Table of Contents

Business Interest Expense

BUSINESS INTEREST EXPENSE LIMITATION DOES NOT APPLY TO:

• Small businesses with 3-year average annual gross receipts less than $25,000,000

• Real property trades or businesses may elect out, but are required to use alternative

depreciation system (ADS) to depreciate:

- Nonresidential real property

- Residential real property

- Qualified improvement property

• Farming businesses may elect out, but are required to use ADS to depreciate any

property with a recovery period of 10 years or more

• Certain regulated public utilities

• Floor plan financing interest

81Return to Table of Contents

Business Interest Expense: Does not apply to…

REAL PROPERTY TRADES OR BUSINESSES

• Includes any real property development, redevelopment, construction,

reconstruction, acquisition, conversion, rental, operation, management,

leasing or brokerage trades or businesses (IRC §469(c)(7)(C))

• Election out of interest limitation is irrevocable

• Requirement to use ADS system could include switch for existing property

in addition to any new and future acquisitions

82Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

• Interest deduction applies first at the entity level

- Any deduction is taken into account in determining the non-separately stated

taxable income or loss of pass-through entity

• Business interest not deducted can be carried forward indefinitely

- Special rules apply to partnerships

• Adjusted taxable income of each partner or shareholder is determined without

regard to partner’s or shareholder’s distributive share of income or deductions of

the entity

- This rule prevents double counting of same dollars used in computing the

adjusted taxable income of entity from generating additional interest deductions

from income passed through to the partners or shareholders

83Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

• “Excess taxable income” of a pass-through is passed through to partners or

shareholders

- If an entity has excess taxable income for purposes of deduction limit, such excess

is passed through to partners of shareholders

- Adjusted taxable income of each partner or shareholder is increased by its share of

the entity’s taxable income

• Excess taxable income from a pass-through increases the partner’s adjusted taxable

income, which can increase the interest deduction at the partner level

- It cannot be used to deduct disallowed interest from other pass-through entities

• Disallowed partnership interest is passed through to the partners and is carried

forward to the next year. It may only be deducted to the extent of 30% of excess

taxable income from that same partnership activity

84Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

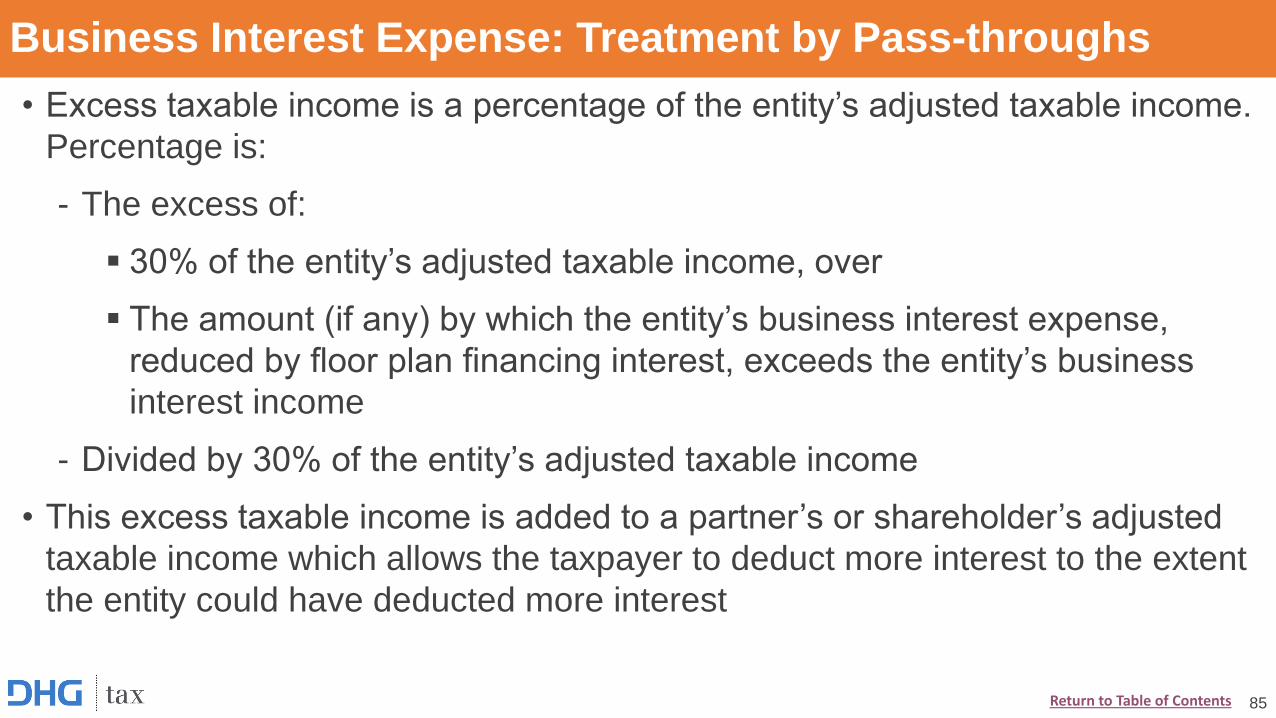

• Excess taxable income is a percentage of the entity’s adjusted taxable income.

Percentage is:

- The excess of:

30% of the entity’s adjusted taxable income, over

The amount (if any) by which the entity’s business interest expense,

reduced by floor plan financing interest, exceeds the entity’s business

interest income

- Divided by 30% of the entity’s adjusted taxable income

• This excess taxable income is added to a partner’s or shareholder’s adjusted

taxable income which allows the taxpayer to deduct more interest to the extent

the entity could have deducted more interest

85Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 1

• Roy is a 50% partner in ABC Partnership

• ABC Partnership has adjusted taxable income of $100,000 and business

interest expense of $20,000

• ABC Partnership deducts $20,000 of business interest because the amount

does not exceed its business interest expense limitation of $30,000 ($100,000 x

30%)

• Since ABC Partnership could have deducted an additional $10,000, Roy is

allocated $16,667 of excess taxable income [($10,000 / $30,000) x $100,000 x

50%]. This allows Roy to deduct an additional $5,000 of interest ($16,667 x

30%)

86Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

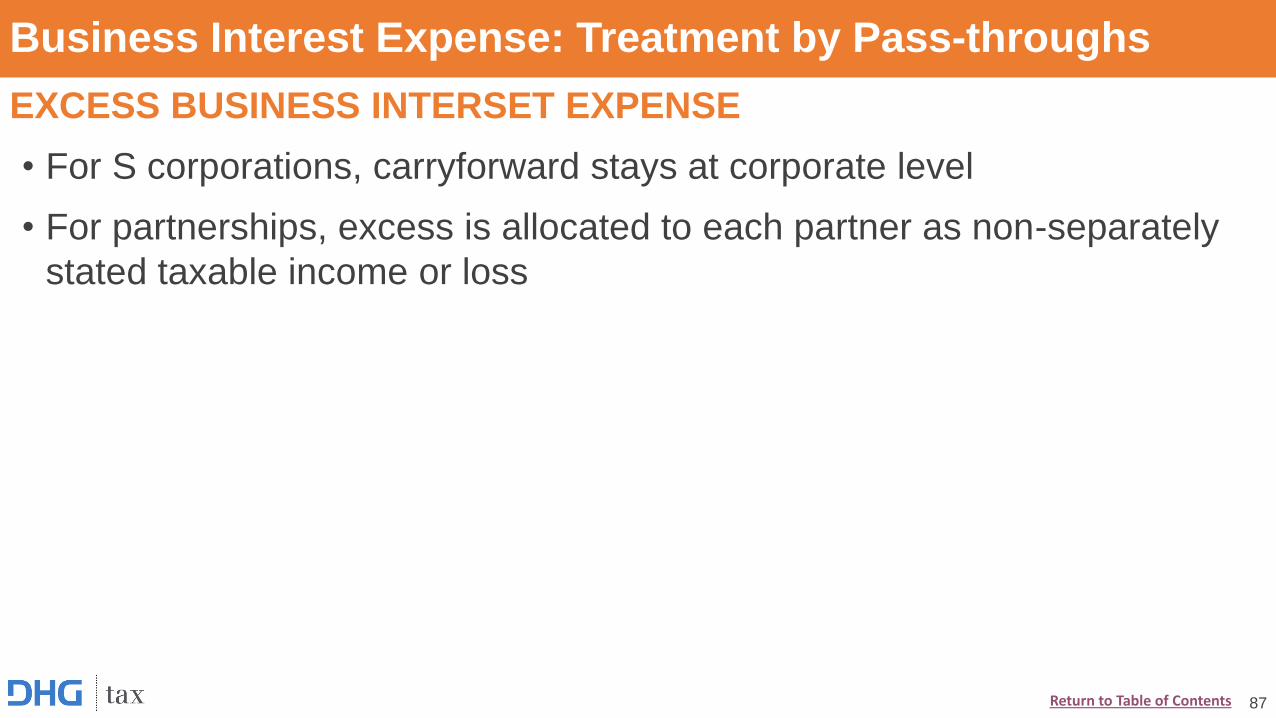

EXCESS BUSINESS INTERSET EXPENSE

• For S corporations, carryforward stays at corporate level

• For partnerships, excess is allocated to each partner as non-separately

stated taxable income or loss

87Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXCESS BUSINESS INTEREST EXPENSE FROM PARTNERSHIPS (NOT APPLICABLE TO S CORPS)

• Partners treat excess business interest as business interest in succeeding taxable year

• Allocated excess interest carried forward to a succeeding year by a partner is treated as paid or

incurred by such partner in succeeding year only to extent the partner is allocated “excess taxable

income” from such partnership in succeeding year

• If partner does have enough excess taxable income from the entity to offset excess business

interest carried forward to that year, excess becomes interest not deemed “paid” by partner in that

year. Therefore, excess business interest carried forward to succeeding tax years.

• Adjusted basis of partner’s interest in partnership is reduced in the year excess business interest is

allocated to partner (but not below zero)

• Excess business income does not carryforward

• Upon disposition of applicable partnership interest, remaining excess business interest is added to

partnership interest tax basis

88Return to Table of Contents

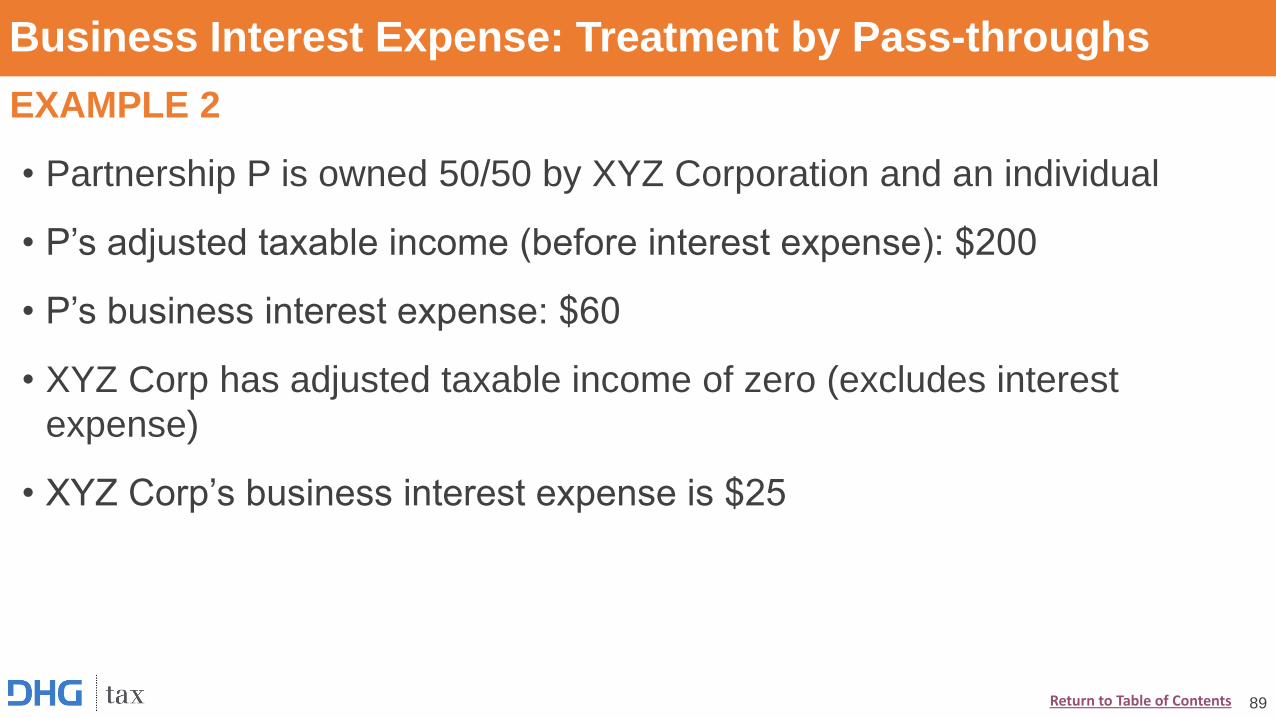

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 2

• Partnership P is owned 50/50 by XYZ Corporation and an individual

• P’s adjusted taxable income (before interest expense): $200

• P’s business interest expense: $60

• XYZ Corp has adjusted taxable income of zero (excludes interest

expense)

• XYZ Corp’s business interest expense is $25

89Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 2

Step One: Calculate limitation and income at Partnership level

• P’s interest deduction limit is $200 x 30% = $60

• P’s taxable income is $200 - $60 = $140

• XYZ Corp and the individual each receive $70 of taxable business

income

90Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 2

Step Two: Calculate limitation and income at XYZ Corp level

• Maximum interest deduction deducted at P level

- No interest deductions limited

- No excess business income

- P’s income is disregarded for XYZ adjusted taxable income calculation

• XYZ’s interest deduction limit: $0 x 30%

• XYZ’s $25 of business interest expense is limited

• XYZ has a $25 interest expense carryover (carryover is indefinite)

91Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

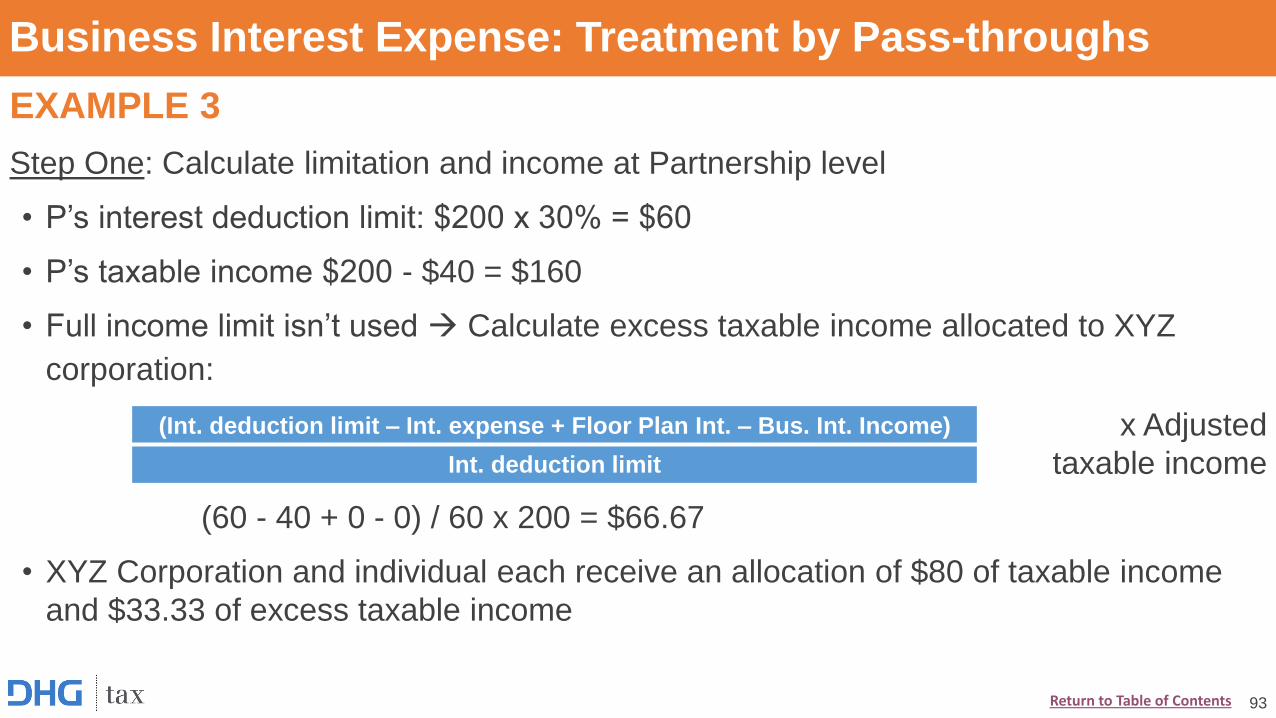

EXAMPLE 3

• Partnership P is owned 50/50 by XYZ Corporation and an individual

• P’s adjusted taxable (before interest income): $200

• P’s business interest expense: $40

• XYZ Corp has net taxable income of zero (Excludes interest expense)

• XYZ Corp’s business interest expense: $25

92Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 3

Step One: Calculate limitation and income at Partnership level

• P’s interest deduction limit: $200 x 30% = $60

• P’s taxable income $200 - $40 = $160

• Full income limit isn’t used Calculate excess taxable income allocated to XYZ

corporation:

x Adjusted

taxable income

(60 - 40 + 0 - 0) / 60 x 200 = $66.67

• XYZ Corporation and individual each receive an allocation of $80 of taxable income

and $33.33 of excess taxable income

(Int. deduction limit – Int. expense + Floor Plan Int. – Bus. Int. Income)

Int. deduction limit

93Return to Table of Contents

Business Interest Expense: Treatment by Pass-throughs

EXAMPLE 3

Step Two: Calculate limitation at XYZ Corp level

• Distributive share of excess taxable income from P is added to the adjusted taxable

income of XYZ

• XYZ’s deduction for business interest is limited to 30% of the sum of:

- Adjusted taxable income

- Allocation of excess taxable income from P

• XYZ’s interest deduction limit: 30% x ($0 + $33.33) = $10

• XYZ Corporation’s $25 of interest expense is limited to $10

• XYZ Corp has a $15 interest expense carryover (carryover is indefinite)

94Return to Table of Contents

Other Changes Impacting Businesses:

Meals & Entertainment ExpensesRudy Thomas, Tax Partner

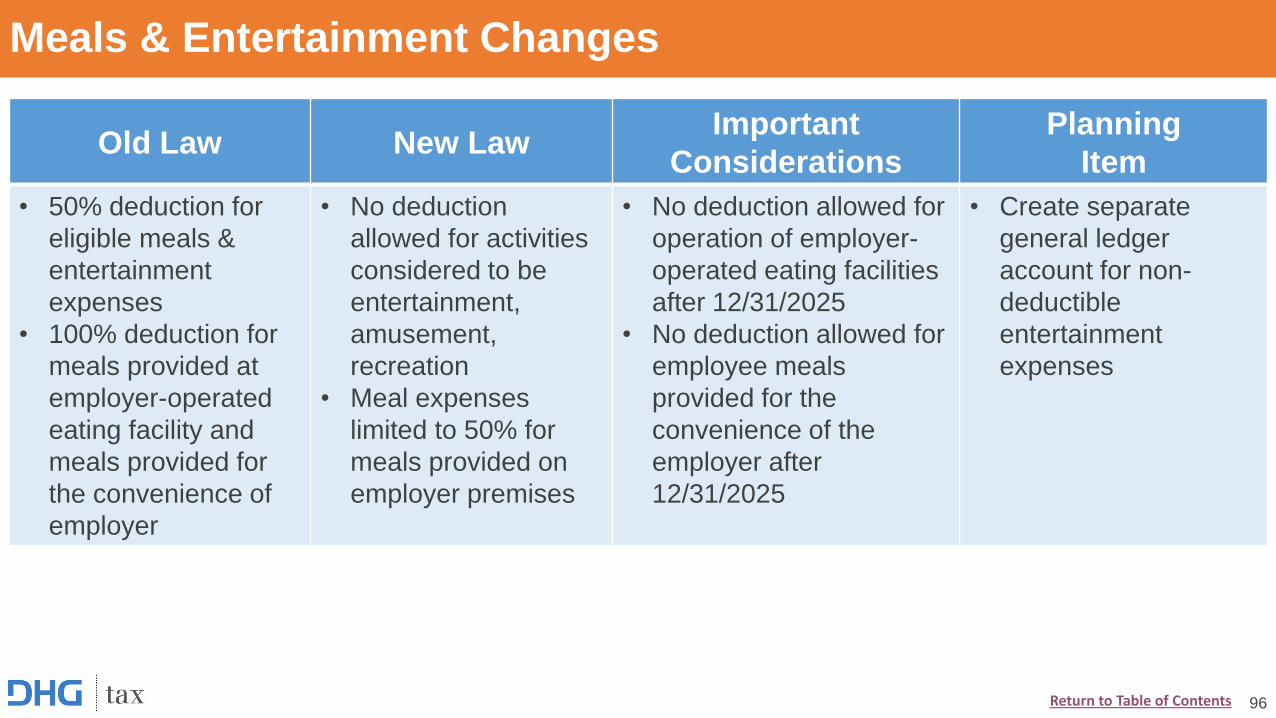

Meals & Entertainment Changes

Old Law New LawImportant

Considerations

Planning

Item

• 50% deduction for

eligible meals &

entertainment

expenses

• 100% deduction for

meals provided at

employer-operated

eating facility and

meals provided for

the convenience of

employer

• No deduction

allowed for activities

considered to be

entertainment,

amusement,

recreation

• Meal expenses

limited to 50% for

meals provided on

employer premises

• No deduction allowed for

operation of employer-

operated eating facilities

after 12/31/2025

• No deduction allowed for

employee meals

provided for the

convenience of the

employer after

12/31/2025

• Create separate

general ledger

account for non-

deductible

entertainment

expenses

96Return to Table of Contents

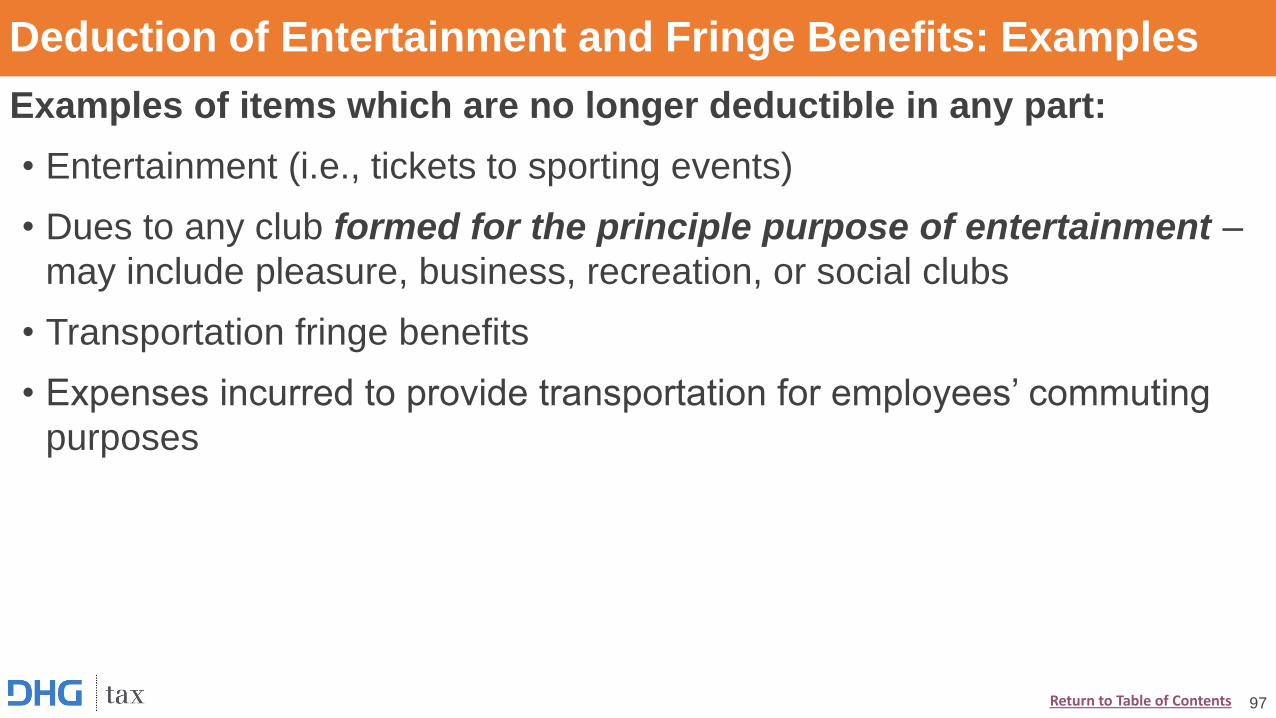

Deduction of Entertainment and Fringe Benefits: Examples

Examples of items which are no longer deductible in any part:

• Entertainment (i.e., tickets to sporting events)

• Dues to any club formed for the principle purpose of entertainment –

may include pleasure, business, recreation, or social clubs

• Transportation fringe benefits

• Expenses incurred to provide transportation for employees’ commuting

purposes

97Return to Table of Contents

Deduction of Entertainment: Dues

• Dues are deductible if the taxpayer is engaged in a trade or business, the dues are

incurred in carrying on that trade or business, and the payment is an ordinary and

necessary expense.

• Payments to the following organizations are deductible (unless the organization’s

principal purpose is providing entertainment to members):

- Business leagues

- Trade associations

- Chambers of commerce

- Boards of trade

- Real estate boards

- Profession organizations (e.g., bar and medical associations)

- Civic or public service organizations (e.g., Kiwanis, Lions, Rotary and Civitan)

98Return to Table of Contents

Other Changes Impacting Businesses:

State ConformityRudy Thomas, Tax Partner

State Conformity: Types of Conformity

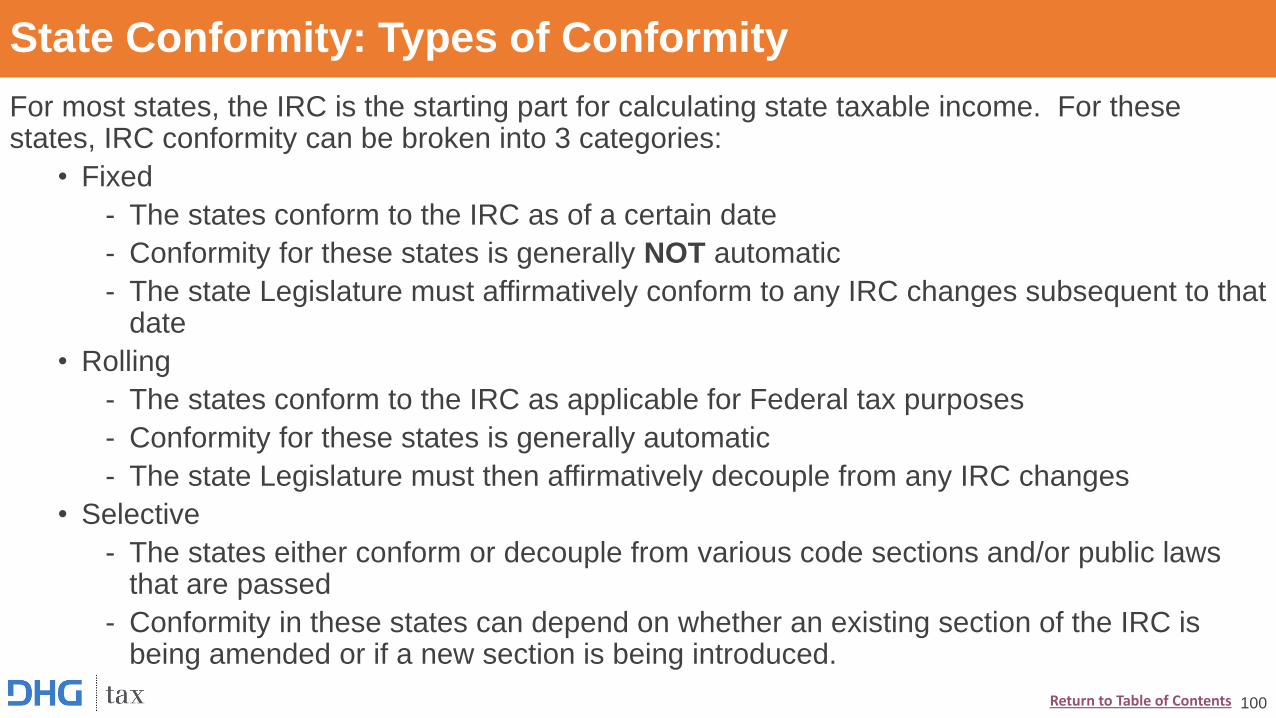

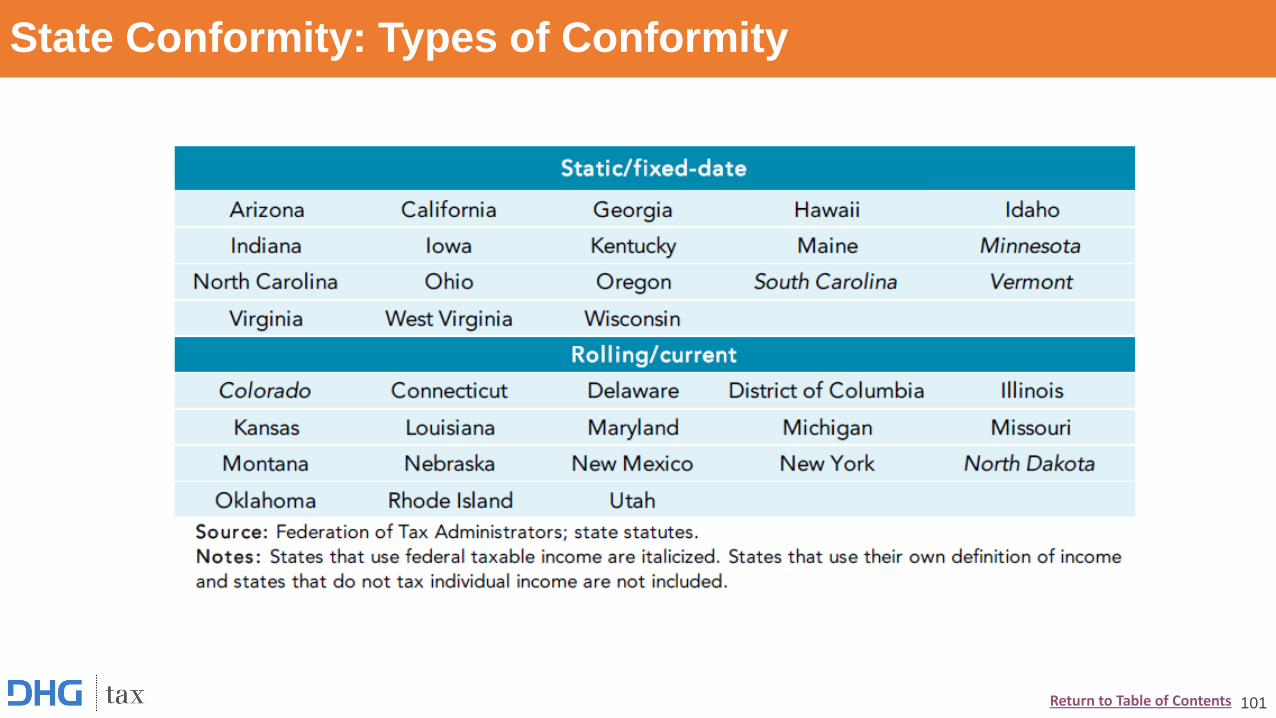

For most states, the IRC is the starting part for calculating state taxable income. For these states, IRC conformity can be broken into 3 categories:

• Fixed

- The states conform to the IRC as of a certain date

- Conformity for these states is generally NOT automatic

- The state Legislature must affirmatively conform to any IRC changes subsequent to that date

• Rolling

- The states conform to the IRC as applicable for Federal tax purposes

- Conformity for these states is generally automatic

- The state Legislature must then affirmatively decouple from any IRC changes

• Selective

- The states either conform or decouple from various code sections and/or public laws that are passed

- Conformity in these states can depend on whether an existing section of the IRC is being amended or if a new section is being introduced.

100Return to Table of Contents

State Conformity: Types of Conformity

101Return to Table of Contents

State Conformity: Items to be Addressed by States

Some of the items that will need to be addressed by states include:

• Bonus Depreciation

Will states continue to decouple from bonus depreciation and will more consider doing so?

• Interest Limitations

Will the states follow the Federal interest limitations, even if the state decouples from bonus depreciation?

• NOL Limitations

For states which require tracking state specific NOLs, will the new NOL limitations be applied?

102Return to Table of Contents

State Conformity: When Will We Know

• It will take time for the state impact of tax reform to become clear

- For the states with fixed and selective conformity, the Legislatures must meet and determine whether or not to conform

- For states with rolling conformity, the Legislatures still must meet and decide to decouple from specific provisions

• The current conformity for states will be unique for each particular state

103Return to Table of Contents

Tax Reform:

International ImplicationsStani Fowler, Tax Senior Manager

U.S. in a Global Tax Context

105Return to Table of Contents

Tax Competitiveness Rankings 2017

Country Overall Rank

Estonia 1

New Zealand 2

Switzerland 3

… …

United Kingdom 14

… …

Germany 23

… …

Mexico 25

… …

Greece 29

United States 30

… …

France 35

106Return to Table of Contents

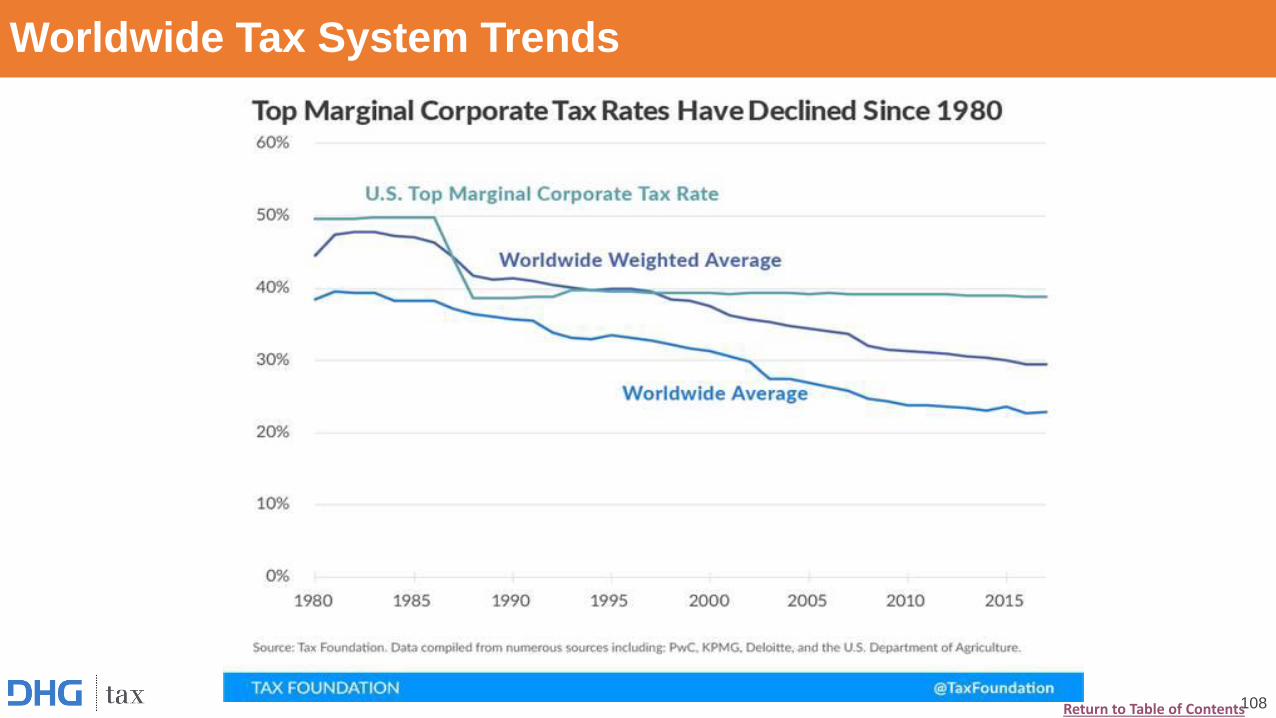

Worldwide Tax System Trends

107Return to Table of Contents

Worldwide Tax System Trends

108Return to Table of Contents

International provisions

Main purpose is to introduce a territorial system of taxation

• Includes introduction of participation exemption

• Transition rules for deferred income

• Strengthening of base erosion rules

109Return to Table of Contents

• Participation exemption for dividends (“DRD”)

• Deemed repatriation of Post 1986 Earnings and Profits

• Base Erosion Anti-Abuse Tax (“BEAT”)

• Global Intangible Low Taxed Income (“GILTI”)

• Deduction for Foreign Derived Intangible Income (“FDII”)

110

INTERNATIONAL TAX

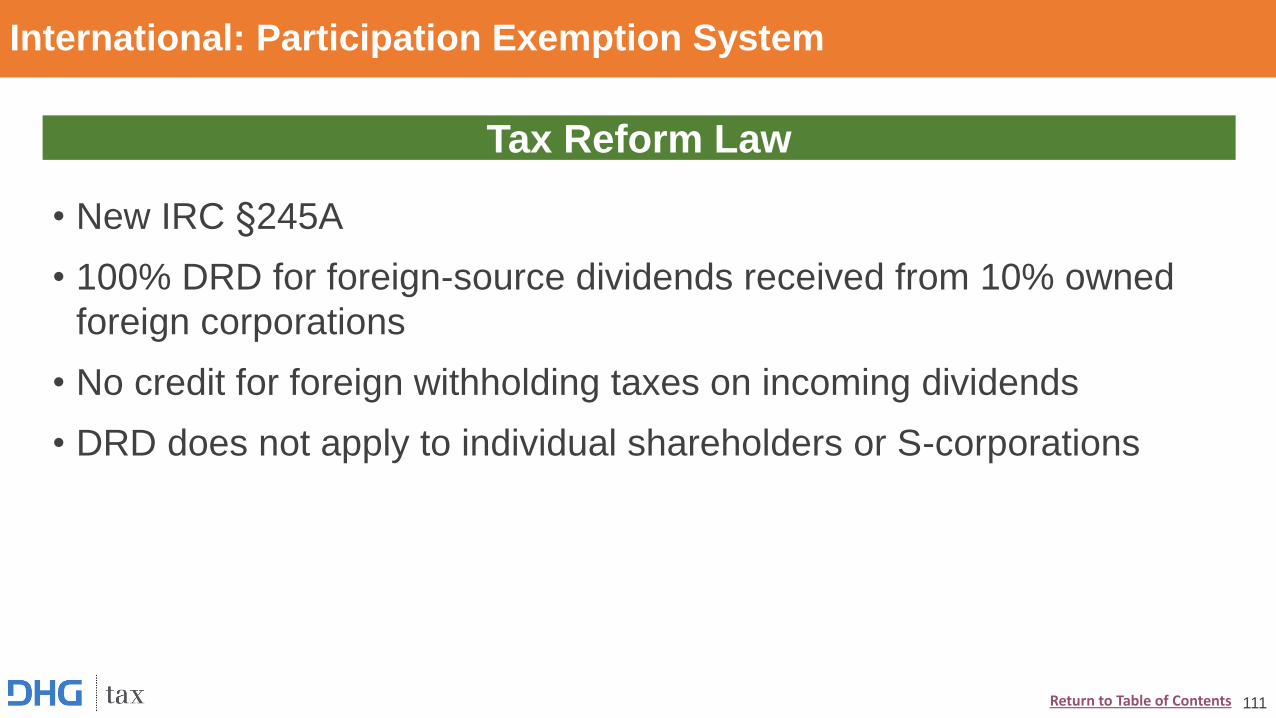

• New IRC §245A

• 100% DRD for foreign-source dividends received from 10% owned

foreign corporations

• No credit for foreign withholding taxes on incoming dividends

• DRD does not apply to individual shareholders or S-corporations

International: Participation Exemption System

111

Tax Reform Law

Return to Table of Contents

• Tax is assessed on accumulated earnings and profits (E&P) at rates of:

- 15.5% of E&P attributable to liquid assets (i.e., cash and cash equivalents)

- 8% of E&P attributable to illiquid assets (i.e., all other assets)

• Tax can be paid over 8 years

• Tax applies to “Specified Foreign Corporations” - CFC or foreign corporation

that has at least one domestic shareholder that is a US corporation.

• Foreign tax credits can be applied, subject to a “haircut” for the reduction in

US tax rate

International: Deemed Repatriation

112

Tax Reform Law

Return to Table of Contents

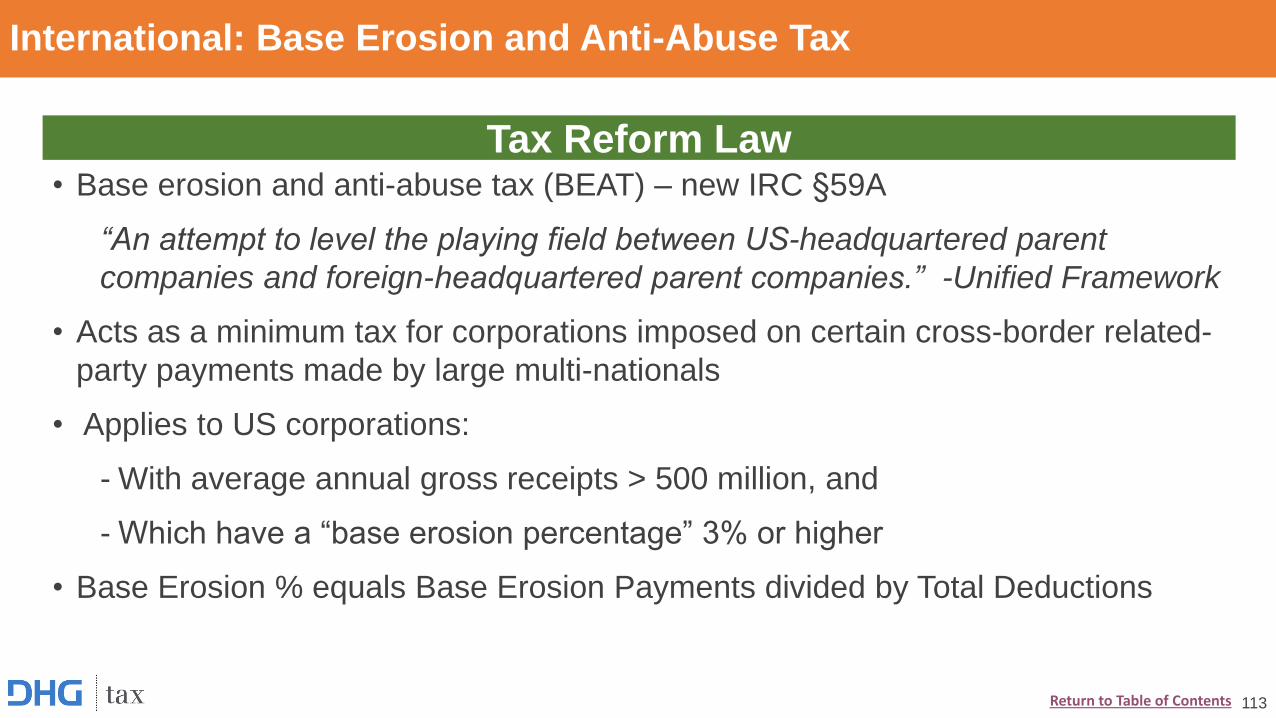

Tax Reform Law• Base erosion and anti-abuse tax (BEAT) – new IRC §59A

“An attempt to level the playing field between US-headquartered parent

companies and foreign-headquartered parent companies.” -Unified Framework

• Acts as a minimum tax for corporations imposed on certain cross-border related-

party payments made by large multi-nationals

• Applies to US corporations:

- With average annual gross receipts > 500 million, and

- Which have a “base erosion percentage” 3% or higher

• Base Erosion % equals Base Erosion Payments divided by Total Deductions

International: Base Erosion and Anti-Abuse Tax

113Return to Table of Contents

International: Base Erosion and Anti-Abuse Tax

DEFINITIONS

• Base Erosion Payment is any payment to a foreign related

person after 2017 for which a deduction is allowable

- Excludes amounts paid for costs of goods sold and eligible

services

• Total Deductions for purposes of calculating the BEAT

percentage means total deductions allowable for the year,

excluding NOLs, the participation exemption, the deduction

allowed under new IRC §250 for foreign intangible income, and

any amounts paid for costs of goods sold and eligible services

114Return to Table of Contents

International: Base Erosion and Anti-Abuse Tax

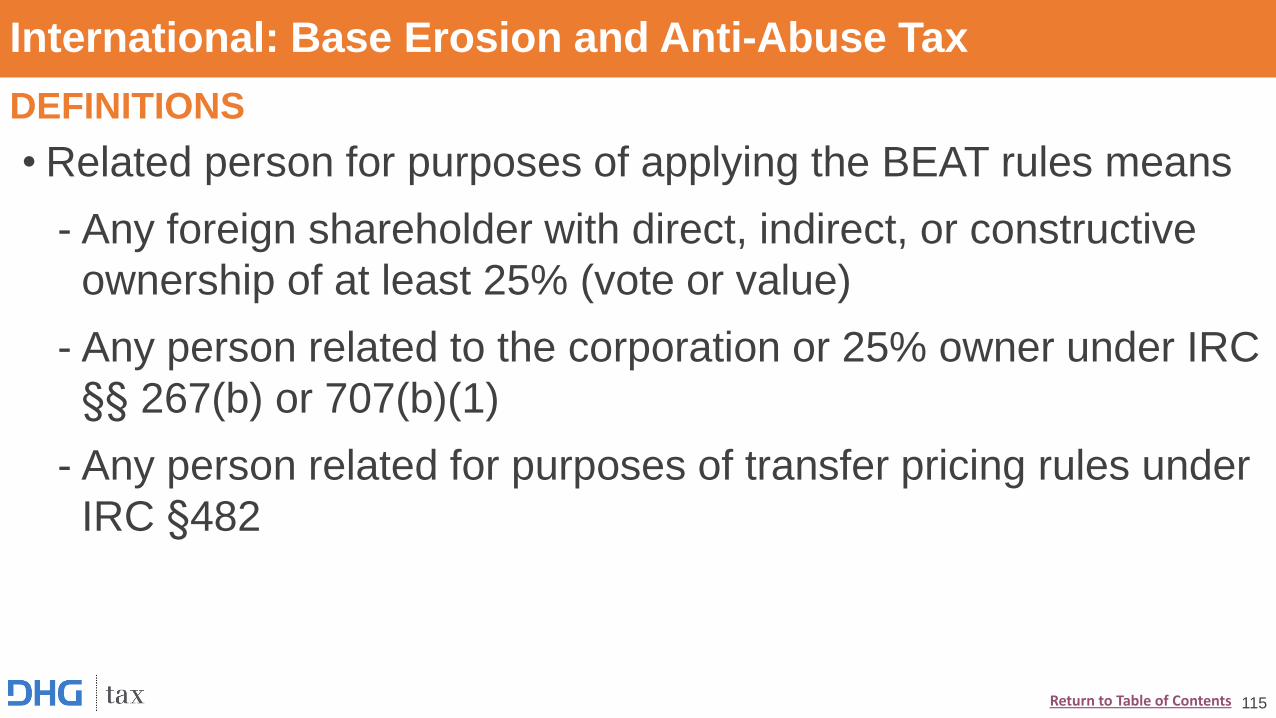

DEFINITIONS

• Related person for purposes of applying the BEAT rules means

- Any foreign shareholder with direct, indirect, or constructive

ownership of at least 25% (vote or value)

- Any person related to the corporation or 25% owner under IRC

§§ 267(b) or 707(b)(1)

- Any person related for purposes of transfer pricing rules under

IRC §482

115Return to Table of Contents

International: Base Erosion and Anti-Abuse Tax

COMPUTATION

• BEAT minimum tax amount is equal to excess of (a) over (b)

(a)10% x Modified Taxable Income

(b)Pre-credit regular income tax liability reduced by:

R&D credits

80% of applicable IRC §38 credits

• No FTCs or deductions

• In tax years beginning after 2025

- The percentage applied to modified taxable income in (a) above is increased from 10% to 12.5%

- R&D credits and applicable IRC §38 credits may no longer reduce the pre-credit regular income tax liability in (b) above

116Return to Table of Contents

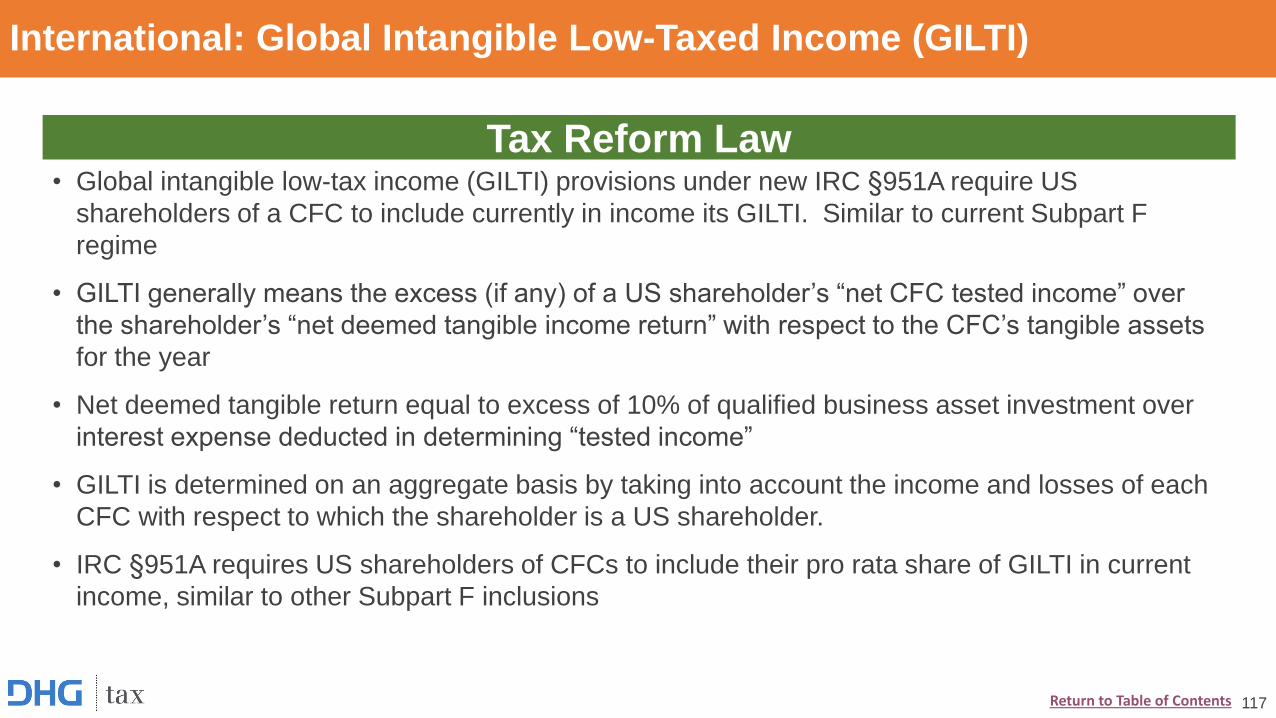

Tax Reform Law• Global intangible low-tax income (GILTI) provisions under new IRC §951A require US

shareholders of a CFC to include currently in income its GILTI. Similar to current Subpart F

regime

• GILTI generally means the excess (if any) of a US shareholder’s “net CFC tested income” over

the shareholder’s “net deemed tangible income return” with respect to the CFC’s tangible assets

for the year

• Net deemed tangible return equal to excess of 10% of qualified business asset investment over

interest expense deducted in determining “tested income”

• GILTI is determined on an aggregate basis by taking into account the income and losses of each

CFC with respect to which the shareholder is a US shareholder.

• IRC §951A requires US shareholders of CFCs to include their pro rata share of GILTI in current

income, similar to other Subpart F inclusions

International: Global Intangible Low-Taxed Income (GILTI)

117Return to Table of Contents

International: Global Intangible Low-Taxed Income (GILTI)

• US shareholders that are C Corporations are allowed a

deduction of up to 50% of the GILTI inclusion amount – resulting

in an ETR of 10.5%

• Non-corporate shareholders pay tax on GILTI at ordinary income

rates with no deduction

• A foreign tax credit is available to corporate shareholders, limited

to 80% of foreign taxes paid.

118Return to Table of Contents

International: Global Intangible Low-Taxed Income (GILTI)

EXAMPLE

• A CFC that is a qualified foreign corporation earns $1,000,000 of non-Subpart F income and pays $150,000 of foreign tax. The CFC has $500,000 of adjusted basis in its tangible personal property.

• The GILTI inclusion for the US shareholder is $800,000 ($850,000 of net CFC tested income less $50,000 of net deemed tangible income return).

119Return to Table of Contents

International: Global Intangible Low-Taxed Income (GILTI)

EXAMPLE

120

GILTI Inclusion (plus §78 gross up) $800,000

Less: 50% Deduction for GILTI (400,000

)

Equals: US Taxable Income Inclusion $400,000

US Tax on GILIT Inclusion at 20% $84,000

Less: Credit for Foreign Taxes (84,000)

Net US Tax Due $0

Implications for Corporate Shareholder

Return to Table of Contents

International: Global Intangible Low-Taxed Income (GILTI)

EXAMPLE

121

Implications for Individual Shareholder

GILTI Inclusion (plus §78 gross up) $800,000

No Deduction for GILTI (0)

Equals: US Taxable Income Inclusion $800,000

US Tax on GILIT Inclusion at 37% $296,000

Less: Credit for Foreign Taxes (0)

Net US Tax Due $296,000

Return to Table of Contents

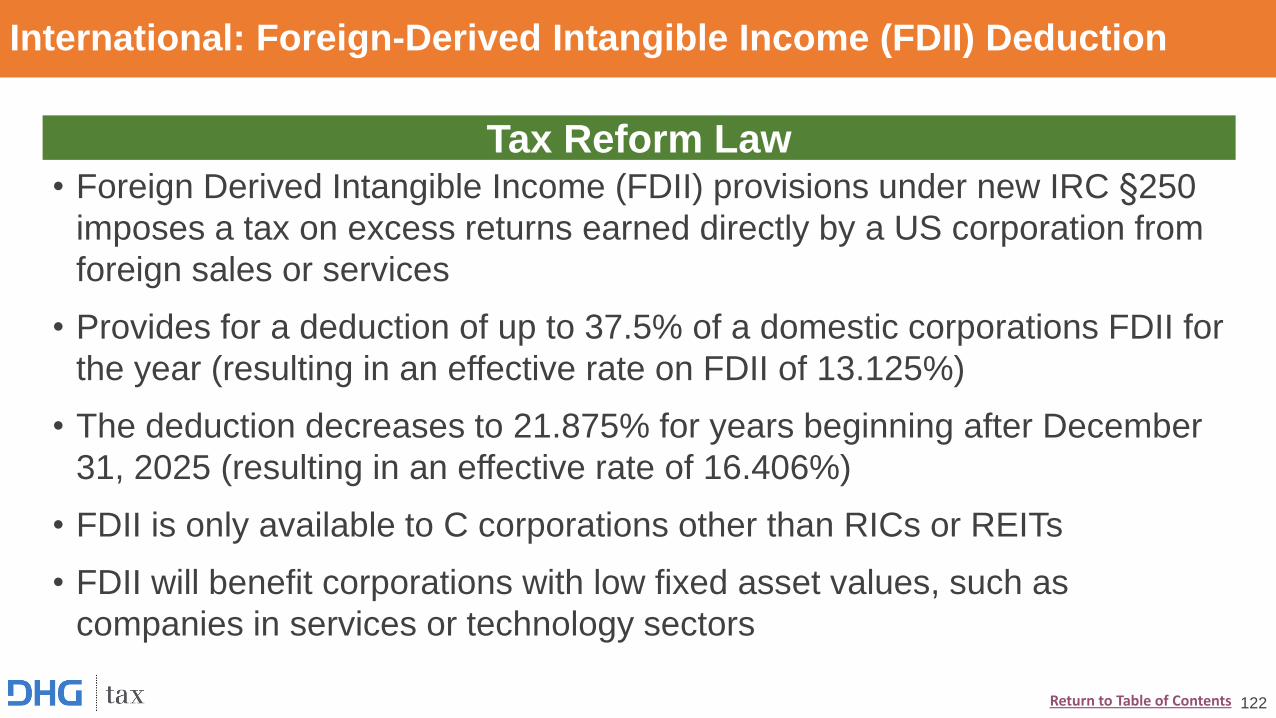

Tax Reform Law• Foreign Derived Intangible Income (FDII) provisions under new IRC §250

imposes a tax on excess returns earned directly by a US corporation from

foreign sales or services

• Provides for a deduction of up to 37.5% of a domestic corporations FDII for

the year (resulting in an effective rate on FDII of 13.125%)

• The deduction decreases to 21.875% for years beginning after December

31, 2025 (resulting in an effective rate of 16.406%)

• FDII is only available to C corporations other than RICs or REITs

• FDII will benefit corporations with low fixed asset values, such as

companies in services or technology sectors

International: Foreign-Derived Intangible Income (FDII) Deduction

122Return to Table of Contents

International: Foreign-Derived Intangible Income (FDII) Deduction

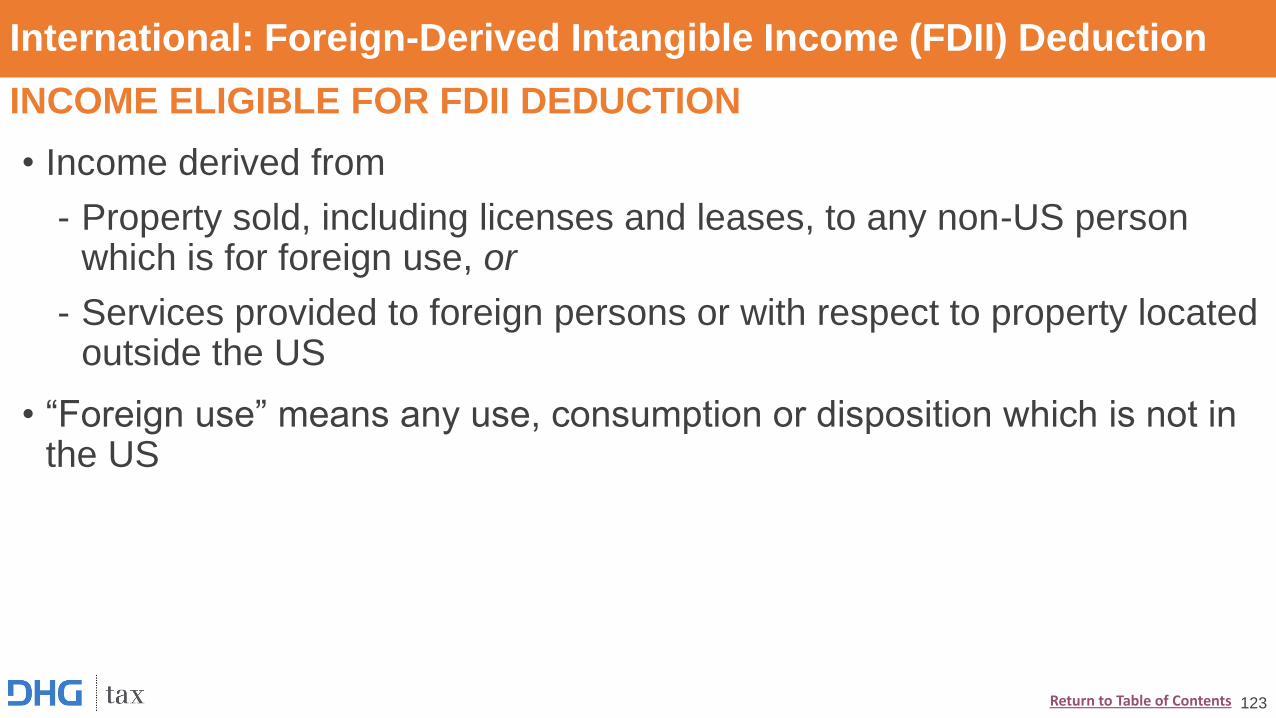

INCOME ELIGIBLE FOR FDII DEDUCTION

• Income derived from

- Property sold, including licenses and leases, to any non-US person which is for foreign use, or

- Services provided to foreign persons or with respect to property located outside the US

• “Foreign use” means any use, consumption or disposition which is not in the US

123Return to Table of Contents

International: Foreign-Derived Intangible Income (FDII) Deduction

COMPUTING THE DEDUCTION FOR FDII

• FDII is NOT deductible, rather it is used to determine the ratio of FDII to Gross income. This ratio is then applied to deemed intangible income

• Deemed intangible income is equal to net income less the deemed tangible income return

• Deemed tangible income return is equal to 10% of qualified business asset investments

124Return to Table of Contents

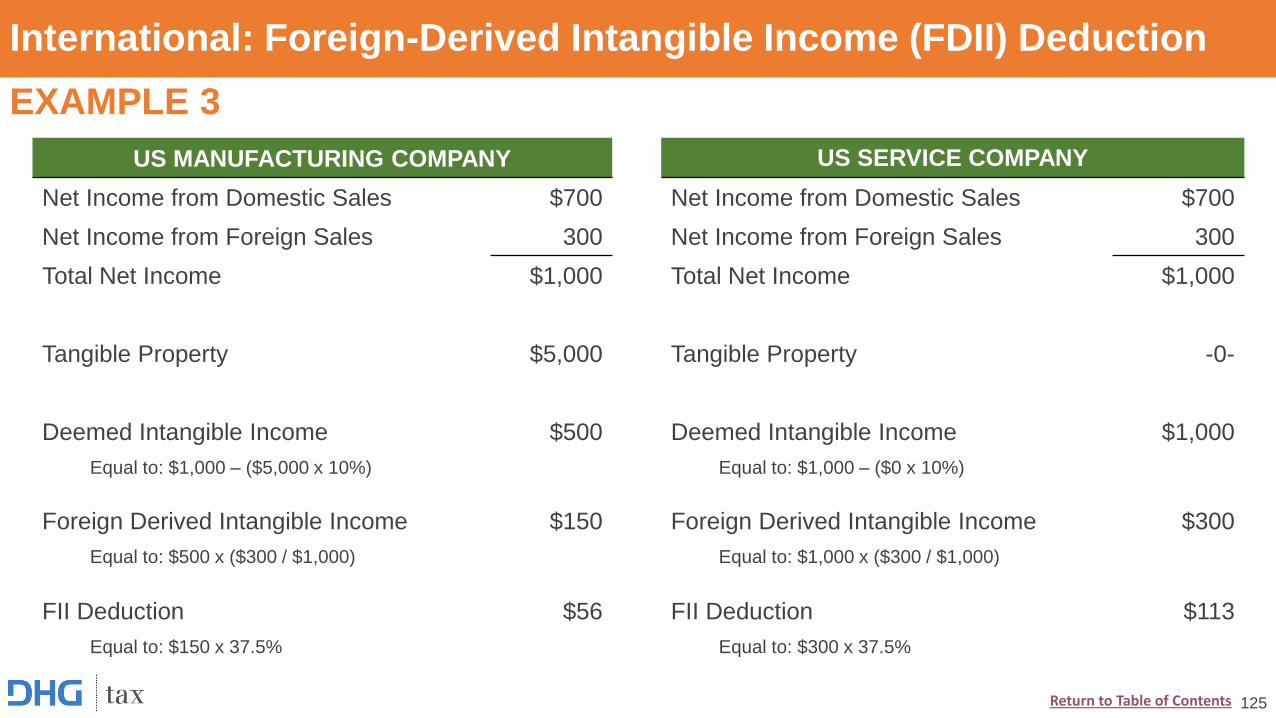

International: Foreign-Derived Intangible Income (FDII) Deduction

EXAMPLE 3

125

US MANUFACTURING COMPANY US SERVICE COMPANY

Net Income from Domestic Sales $700 Net Income from Domestic Sales $700

Net Income from Foreign Sales 300 Net Income from Foreign Sales 300

Total Net Income $1,000 Total Net Income $1,000

Tangible Property $5,000 Tangible Property -0-

Deemed Intangible Income $500 Deemed Intangible Income $1,000

Equal to: $1,000 – ($5,000 x 10%) Equal to: $1,000 – ($0 x 10%)

Foreign Derived Intangible Income $150 Foreign Derived Intangible Income $300

Equal to: $500 x ($300 / $1,000) Equal to: $1,000 x ($300 / $1,000)

FII Deduction $56 FII Deduction $113

Equal to: $150 x 37.5% Equal to: $300 x 37.5%

Return to Table of Contents

Tax Reform: Impact on Pass-Through Entities

Robert Bradham, Tax Partner Blair Clawson, Tax Manager

Pass-through: Qualified Business Income Deduction

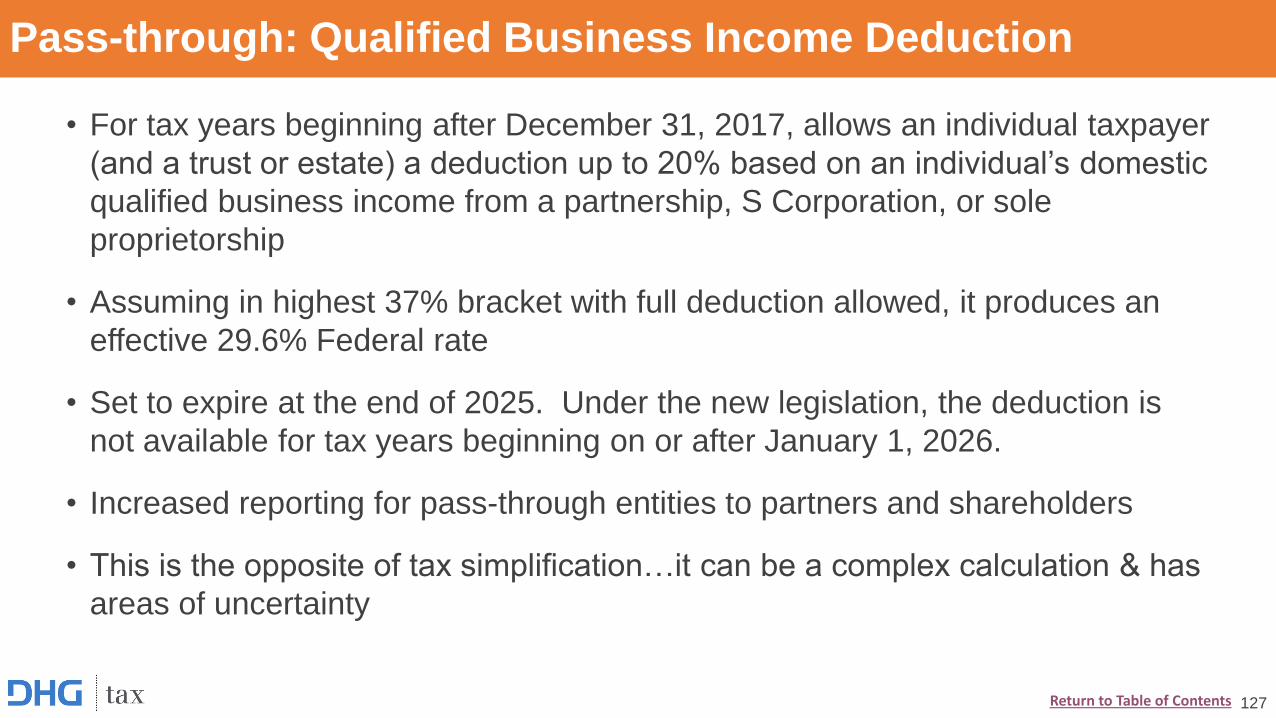

• For tax years beginning after December 31, 2017, allows an individual taxpayer

(and a trust or estate) a deduction up to 20% based on an individual’s domestic

qualified business income from a partnership, S Corporation, or sole

proprietorship

• Assuming in highest 37% bracket with full deduction allowed, it produces an

effective 29.6% Federal rate

• Set to expire at the end of 2025. Under the new legislation, the deduction is

not available for tax years beginning on or after January 1, 2026.

• Increased reporting for pass-through entities to partners and shareholders

• This is the opposite of tax simplification…it can be a complex calculation & has

areas of uncertainty

127Return to Table of Contents

Pass-through: Qualified Business Income Deduction

Items of consideration:

• What are “qualifying business activities”?

• What is “qualified business income” or “QBI”?

• Claiming the deduction (netting, overall TI, more limitations)

• Income limitation exception (AGI thresholds)

• Computations and complications

128Return to Table of Contents

Pass-through: Qualified Business Income Deduction

QUALIFYING BUSINESS ACTIVITIES

• Qualified trades or businesses that meets the following criteria:

- Generally must be U.S. domestic trade or business

- Based on qualified business income (includes both passive and non-passive)

- Excludes trade or businesses of performing services as an employee

- Excludes specified service trade or businesses:

Fields of health, accounting, law, actuarial science, performing arts, consulting,

athletics, financial services, and brokerage services (excludes engineers and

architecture)

Where the principal asset is the reputation or skill of the owners or employees

That involves the performance of services of investing and investment managing

trading or dealing in securities, partnership interests, or commodities

129Return to Table of Contents

Pass-through: Qualified Business Income Deduction

QUALIFYING INCOME

• Qualified business income

• Qualified cooperative dividends

• Qualified REIT dividends (excludes REIT capital gains)

• Qualified publicly traded partnership income

130Return to Table of Contents

Pass-through: Qualified Business Income Deduction

CLAIMING THE DEDUCTION

• Individuals, estates and trusts are eligible for the qualified business income deduction

• The deduction is calculated at the taxpayer level with information supplied by the

qualified trade or business

• The deduction is claimed on the taxpayer’s tax return

• For individuals, deduction claimed after taxable income is computed

- Below the line, not a deduction for AGI; not an itemized deduction

• Deduction available to taxpayers that itemize deductions, as well as those that do not

• Deduction does not reduce self-employment income

• Same for AMT and Regular Tax

131Return to Table of Contents

Pass-through: Qualified Business Income Deduction

INCOME LIMITATION EXCEPTION FOR SPECIFIED SERVICE TRADES OR

BUSINESSES

• Taxpayers with income from a specified service trade or business may

qualify for 20% deduction if taxable income is less than $315,000 (MFJ)

or $157,500 (all other filers)

• The 20% deduction is phased out as taxpayers’ taxable income increases

from $315,000 to $415,000 (MFJ) and $157,500 to $207,500 (all other

filers)

132Return to Table of Contents

Pass-through: Qualified Business Income Deduction

INCOME LIMITATION EXCEPTION

• If taxable income is less than $315,000 (MFJ) or $157,500 (all other

taxpayers), the limitation related to W-2 wages / capital does not apply

• If taxable income is between $315,000 and $415,000 (MFJ) or $157,500

and $207,500 (all other taxpayers), the limitation related to W-2 wages /

capital phases in

133Return to Table of Contents

Pass-through: Qualified Business Income Deduction

CALCULATING THE DEDUCTION

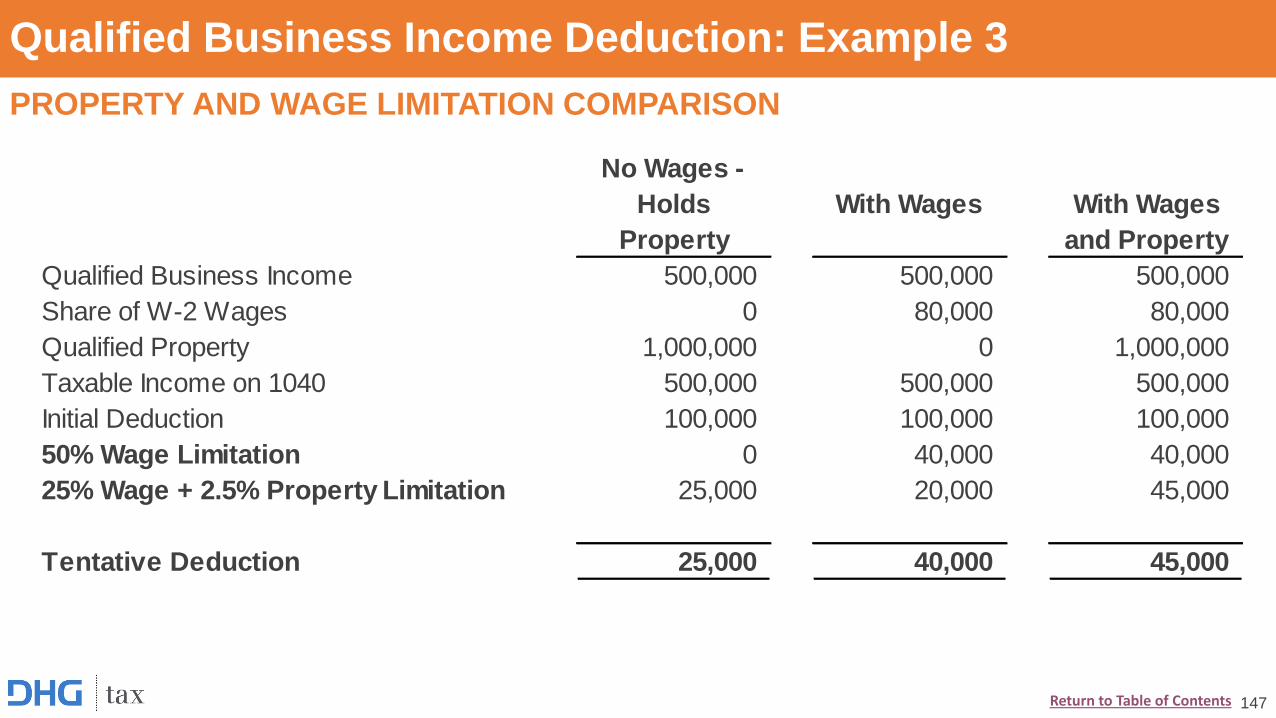

Equal to the lesser of (1) or (2):

(1) Combined Qualified Business Income = (a) + (b) + (c)

(a) The lesser of (i) or (ii)

(i) 20% of the business income of the qualified trade or business, or

(ii) The W-2 Wage / Capital Limitation, which is the greater of (A) or (B):

(A) 50% of W-2 wages paid with respect to the qualified trade or business, or

(B) 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property

(b) 20% of the aggregate REIT dividends and qualified publicly traded partnership income

(c) Lesser of (i) or (ii)

(i) 20% of qualified cooperative dividends, or

(ii) Taxable income reduced by net capital gain

(2) 20% of taxable income less net capital gain

134Return to Table of Contents

Pass-through: Qualified Business Income Deduction

MULTIPLE QUALIFIED BUSINESSES

• Compute the 20% Deduction for each qualified trade or business (Step 1) and add

them together

• Then apply the overall limitation (Step 2)

- The sum of the deductions cannot exceed 20% of the excess of taxable income

over net capital gains

135Return to Table of Contents

Pass-through: Qualified Business Income Deduction

DEFINITIONS

• W-2 wages are generally wages and deferred compensation reported to the Social

Security Administration

• Taxpayers’ wages derived from the Qualified Trade or Business are not added back to

determine Qualified Business Income

• For fiscal year partnerships and S corporations, W-2 wages are the calendar year

wages paid by the business during the calendar year ending during the taxable year

- Example: A partnership with a 5/31/2018 fiscal year end would use W-2 wages paid

for the calendar year ending 12/31/2017 for purposes of applying the wage

limitation

136Return to Table of Contents

Pass-through: Qualified Business Income Deduction

DEFINITION OF QUALIFIED PROPERTY

• The acquisition cost (unadjusted basis) of tangible and real property (excluding land)

• Held for use by the qualified trade or business at the close of the tax year

• Used at any point during the tax year

• Depreciable period for which has not ended before the close of the taxable year

- Depreciable period is the period beginning on date the property was first placed in

service and ending on the later of:

10 years after such date, or

The last day of the last full year in the applicable recovery period under section 168

(GDS recovery period)

- Example: A calendar year partnership acquires equipment with a 5 year GDS recovery

period on 7/1/2015. The equipment is considered qualified property through the 2025

tax year

137Return to Table of Contents

Pass-through: Qualified Business Income Deduction

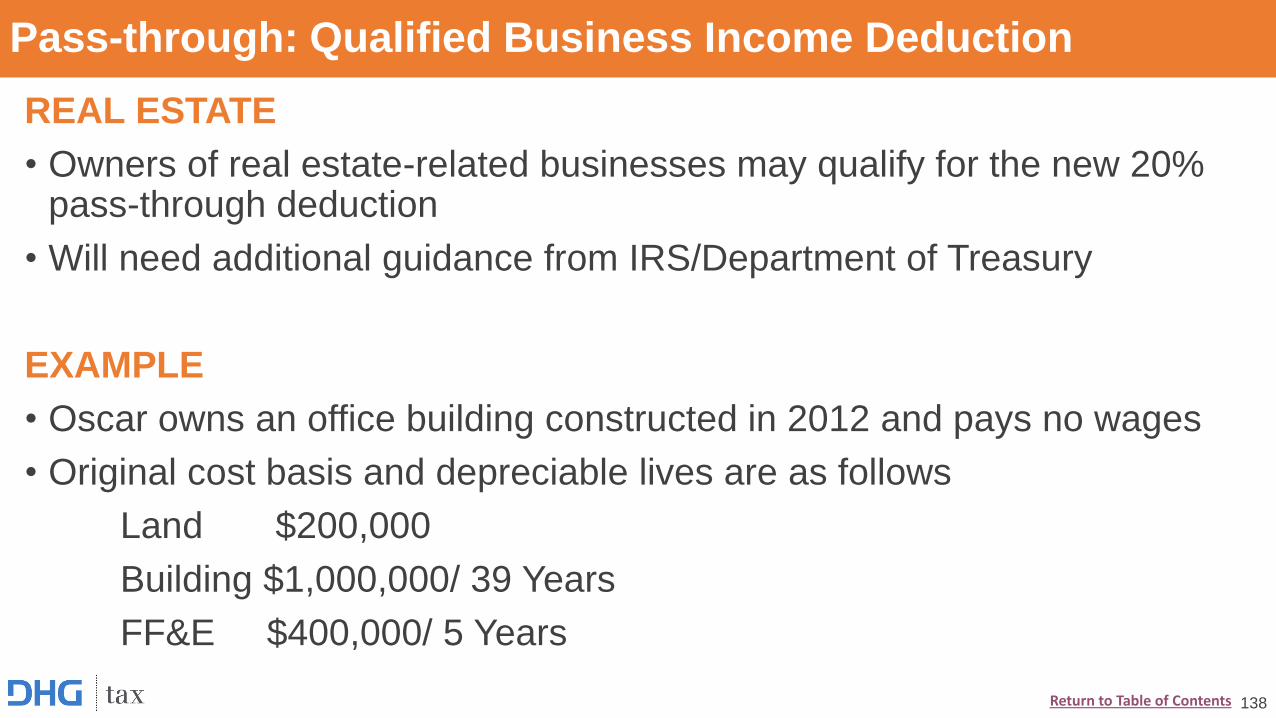

REAL ESTATE

• Owners of real estate-related businesses may qualify for the new 20% pass-through deduction

• Will need additional guidance from IRS/Department of Treasury

EXAMPLE

• Oscar owns an office building constructed in 2012 and pays no wages

• Original cost basis and depreciable lives are as follows

Land $200,000

Building $1,000,000/ 39 Years

FF&E $400,000/ 5 Years

138Return to Table of Contents

Pass-through: Qualified Business Income Deduction

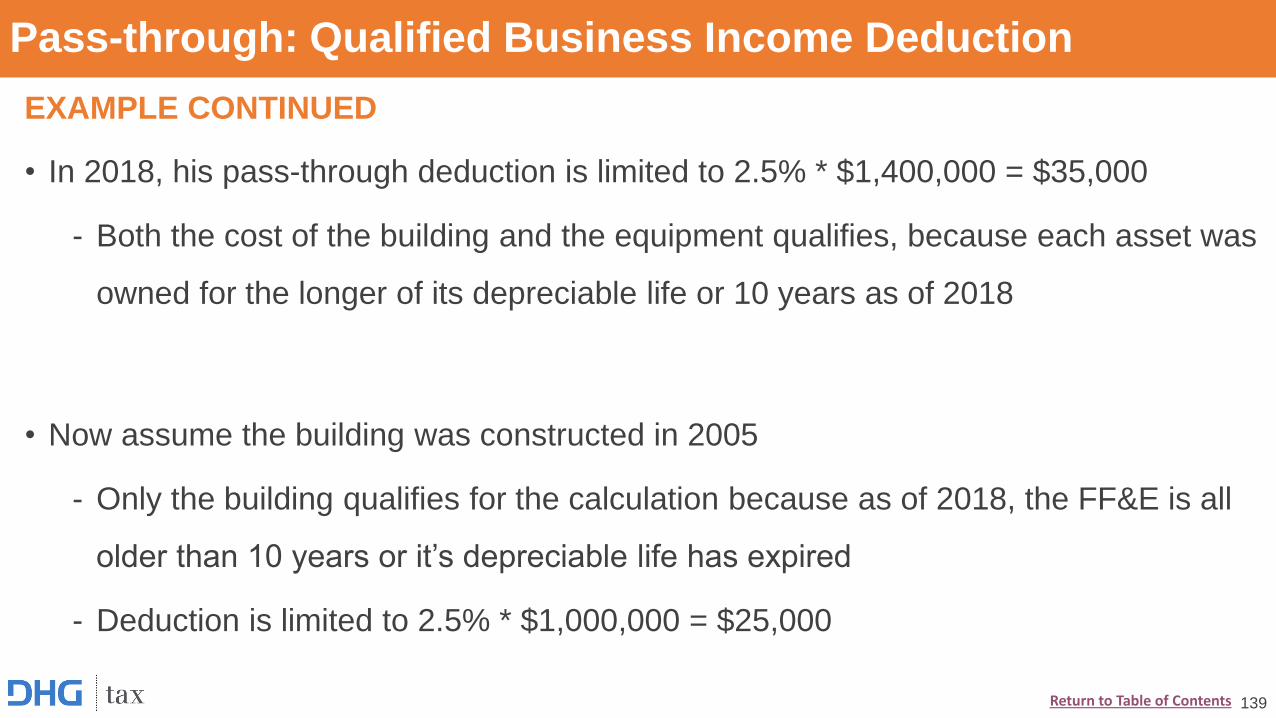

EXAMPLE CONTINUED

• In 2018, his pass-through deduction is limited to 2.5% * $1,400,000 = $35,000

- Both the cost of the building and the equipment qualifies, because each asset was

owned for the longer of its depreciable life or 10 years as of 2018

• Now assume the building was constructed in 2005

- Only the building qualifies for the calculation because as of 2018, the FF&E is all

older than 10 years or it’s depreciable life has expired

- Deduction is limited to 2.5% * $1,000,000 = $25,000

139Return to Table of Contents

Pass-through: Qualified Business Income Deduction

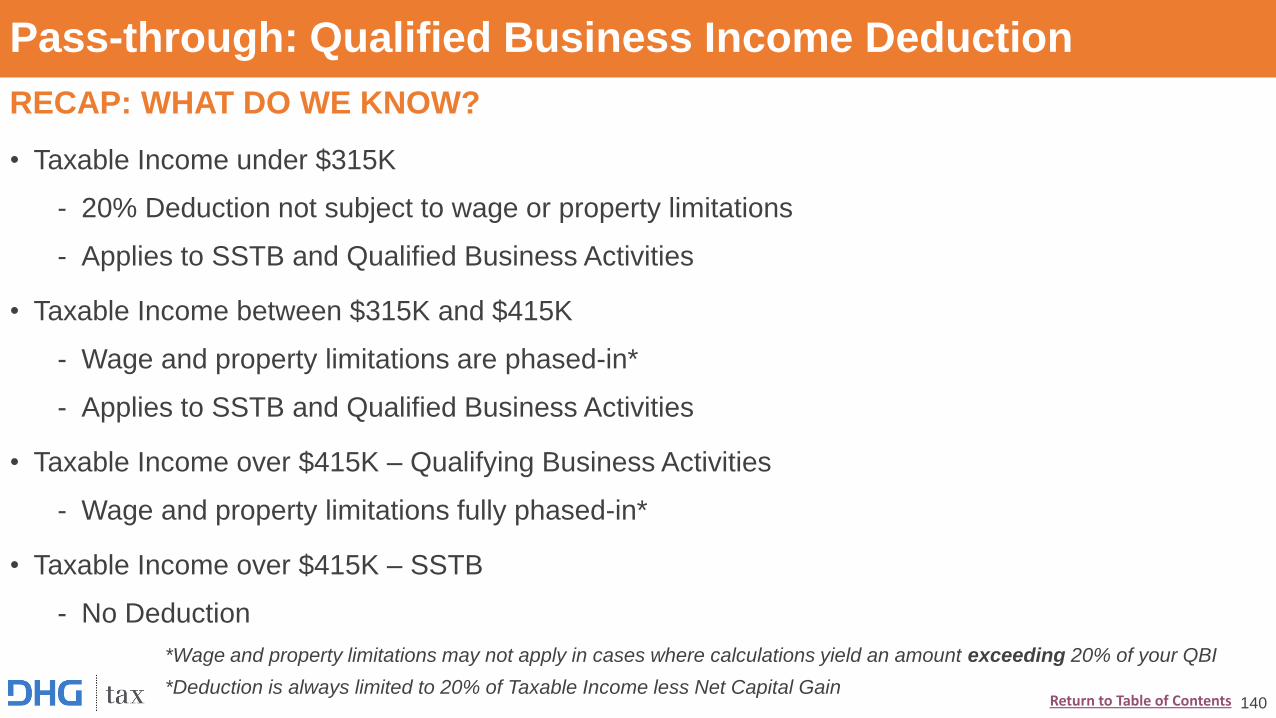

RECAP: WHAT DO WE KNOW?

• Taxable Income under $315K

- 20% Deduction not subject to wage or property limitations

- Applies to SSTB and Qualified Business Activities

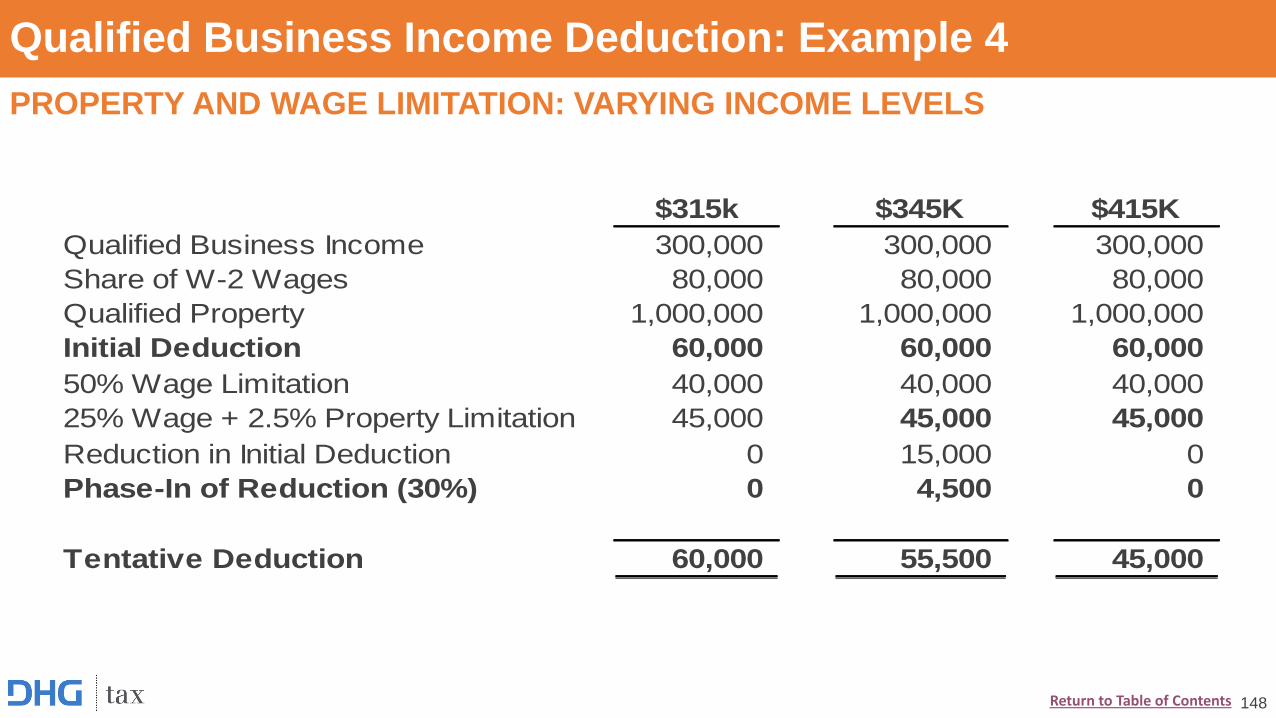

• Taxable Income between $315K and $415K

- Wage and property limitations are phased-in*

- Applies to SSTB and Qualified Business Activities

• Taxable Income over $415K – Qualifying Business Activities

- Wage and property limitations fully phased-in*

• Taxable Income over $415K – SSTB

- No Deduction

140

*Wage and property limitations may not apply in cases where calculations yield an amount exceeding 20% of your QBI

*Deduction is always limited to 20% of Taxable Income less Net Capital GainReturn to Table of Contents

Pass-through: Qualified Business Income Deduction

WHAT DON’T WE KNOW?

• Congress instructed the Secretary to issue regulations

• Awaiting guidance on:

- Application of provision to tiered entities

- Application of the rules in short tax years and in years of acquisition or disposition

of a major portion of a trade or business

- Anti-abuse rules for W-2s

- Determining unadjusted basis for like kind exchange or involuntary conversion

property

- Examples and instruction regarding activities “where the principal asset is the

reputation or skill of the owners or employees”

141Return to Table of Contents

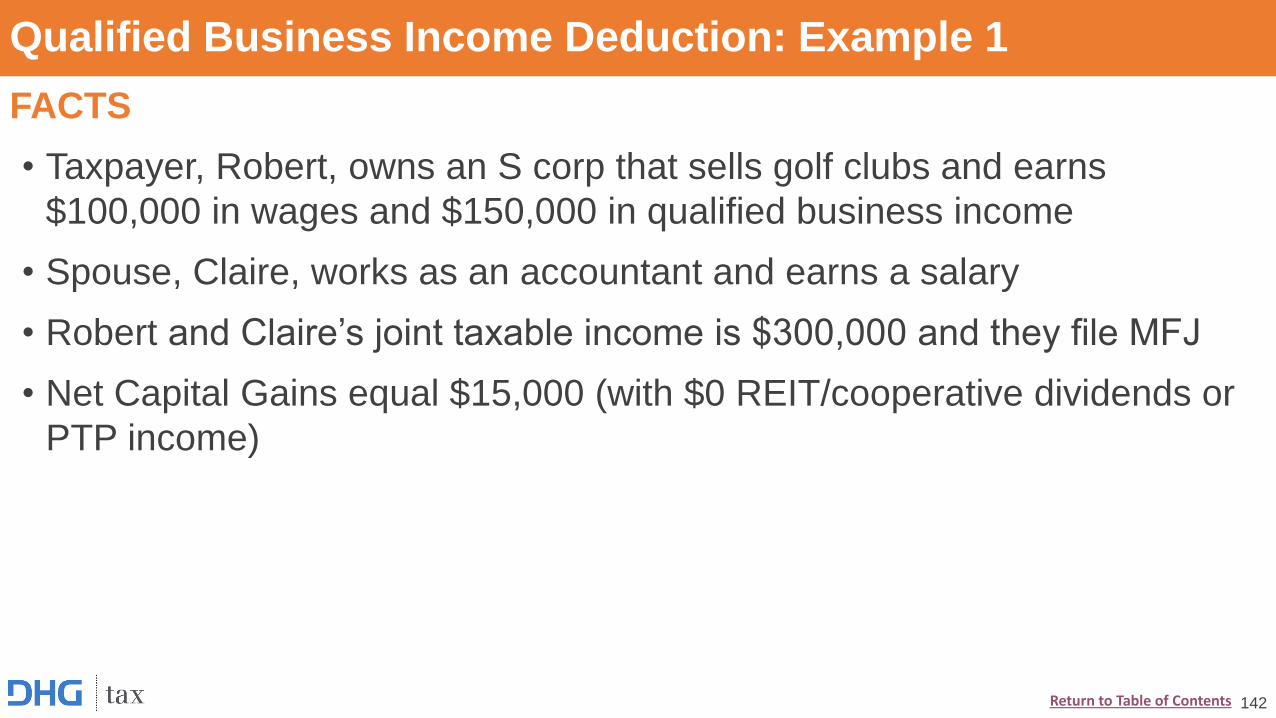

Qualified Business Income Deduction: Example 1

FACTS

• Taxpayer, Robert, owns an S corp that sells golf clubs and earns

$100,000 in wages and $150,000 in qualified business income

• Spouse, Claire, works as an accountant and earns a salary

• Robert and Claire’s joint taxable income is $300,000 and they file MFJ

• Net Capital Gains equal $15,000 (with $0 REIT/cooperative dividends or

PTP income)

142Return to Table of Contents

Qualified Business Income Deduction: Example 1

DEDUCTION

• Business income is not from an SSTB

• Taxable income before the deduction falls below $315,000 threshold, so there

are no wage or capital limitations

• Deduction is the lessor of:

1) 20% of Qualified Business Income

20% * $150,000 = $30,000

or

2) 20% of Taxable Income over Net Capital Gains

20% * (300,000-15,000) = 57,000

Total Deduction is $30,000

143Return to Table of Contents

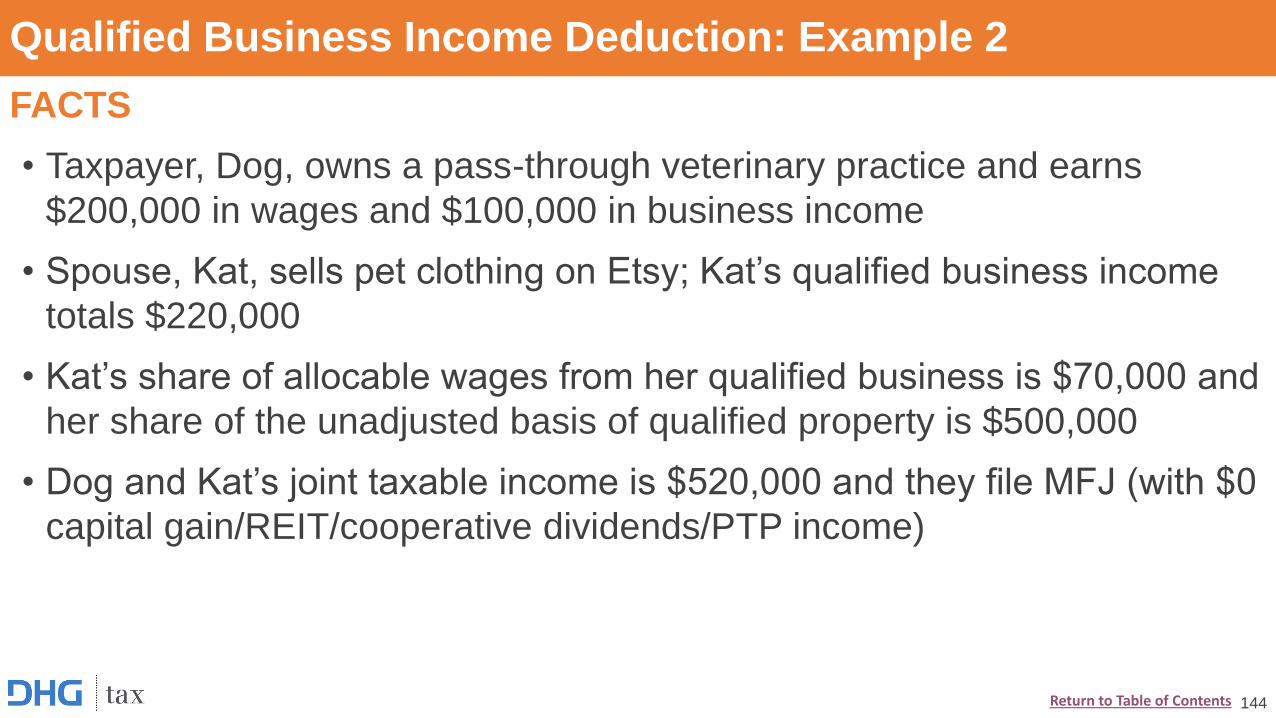

Qualified Business Income Deduction: Example 2

FACTS

• Taxpayer, Dog, owns a pass-through veterinary practice and earns

$200,000 in wages and $100,000 in business income

• Spouse, Kat, sells pet clothing on Etsy; Kat’s qualified business income

totals $220,000

• Kat’s share of allocable wages from her qualified business is $70,000 and

her share of the unadjusted basis of qualified property is $500,000

• Dog and Kat’s joint taxable income is $520,000 and they file MFJ (with $0

capital gain/REIT/cooperative dividends/PTP income)

144Return to Table of Contents

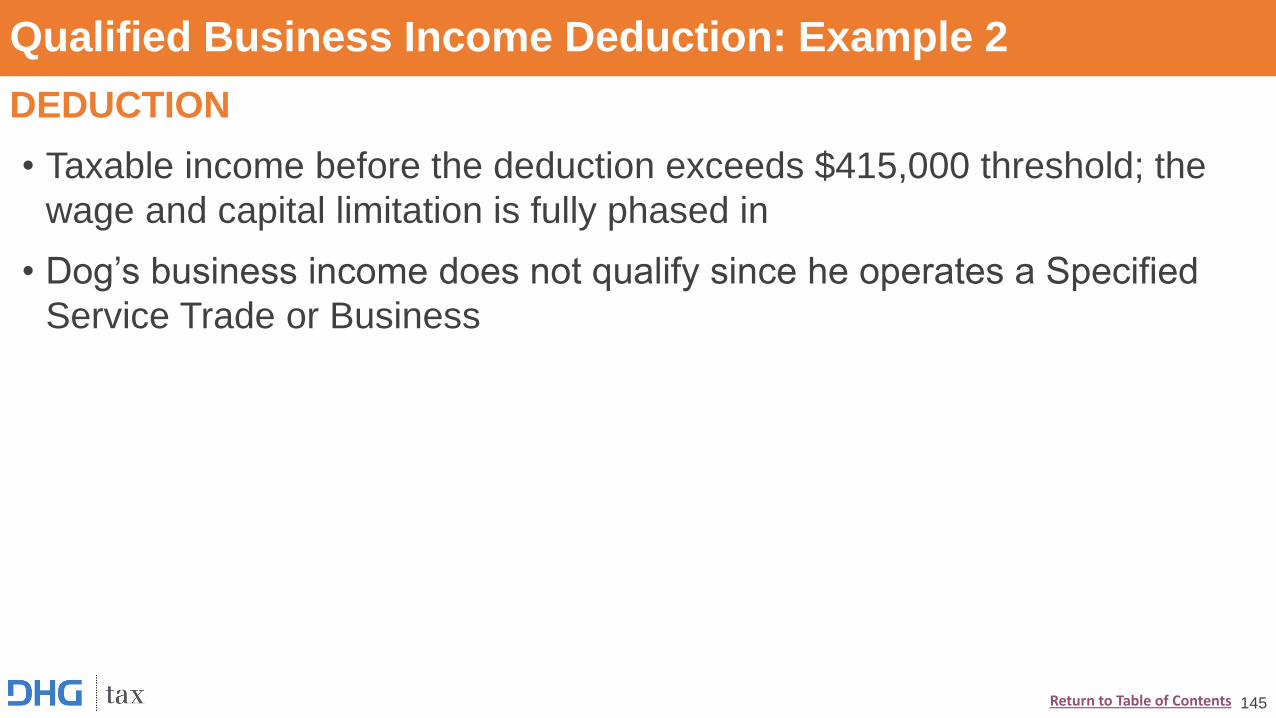

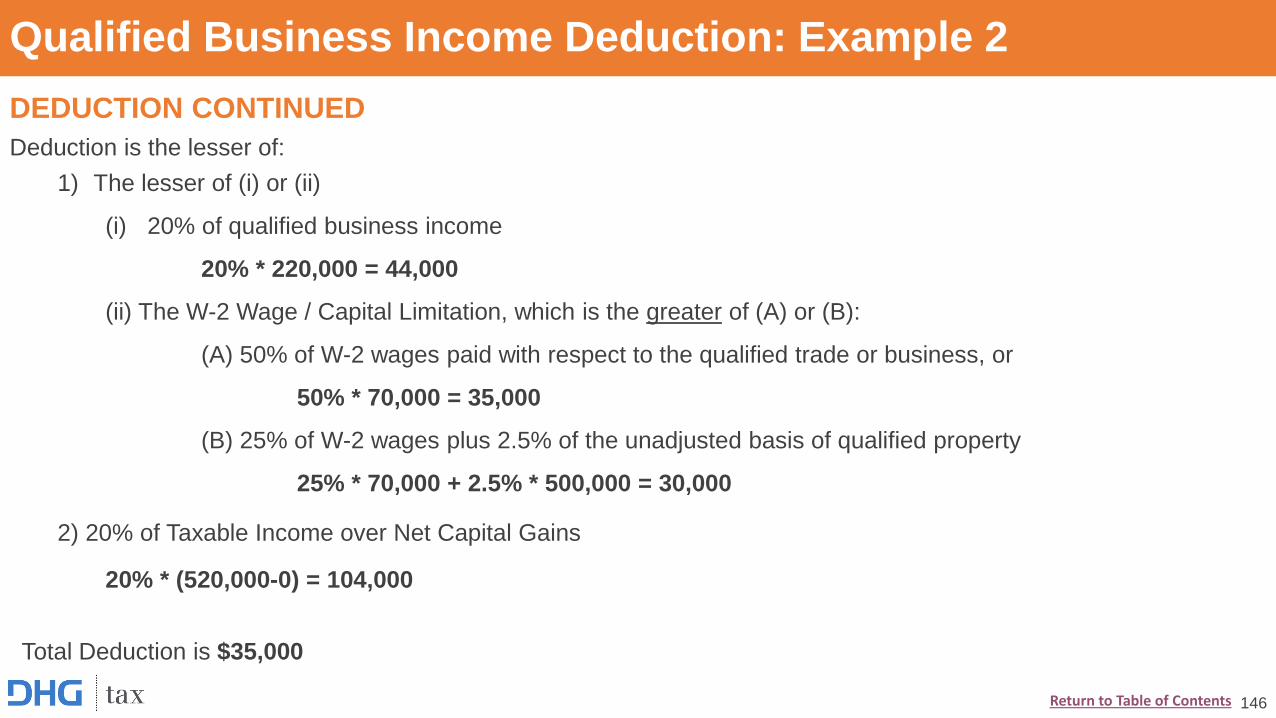

Qualified Business Income Deduction: Example 2

DEDUCTION

• Taxable income before the deduction exceeds $415,000 threshold; the

wage and capital limitation is fully phased in

• Dog’s business income does not qualify since he operates a Specified

Service Trade or Business

145Return to Table of Contents

Qualified Business Income Deduction: Example 2

DEDUCTION CONTINUED

Deduction is the lesser of:

1) The lesser of (i) or (ii)

(i) 20% of qualified business income

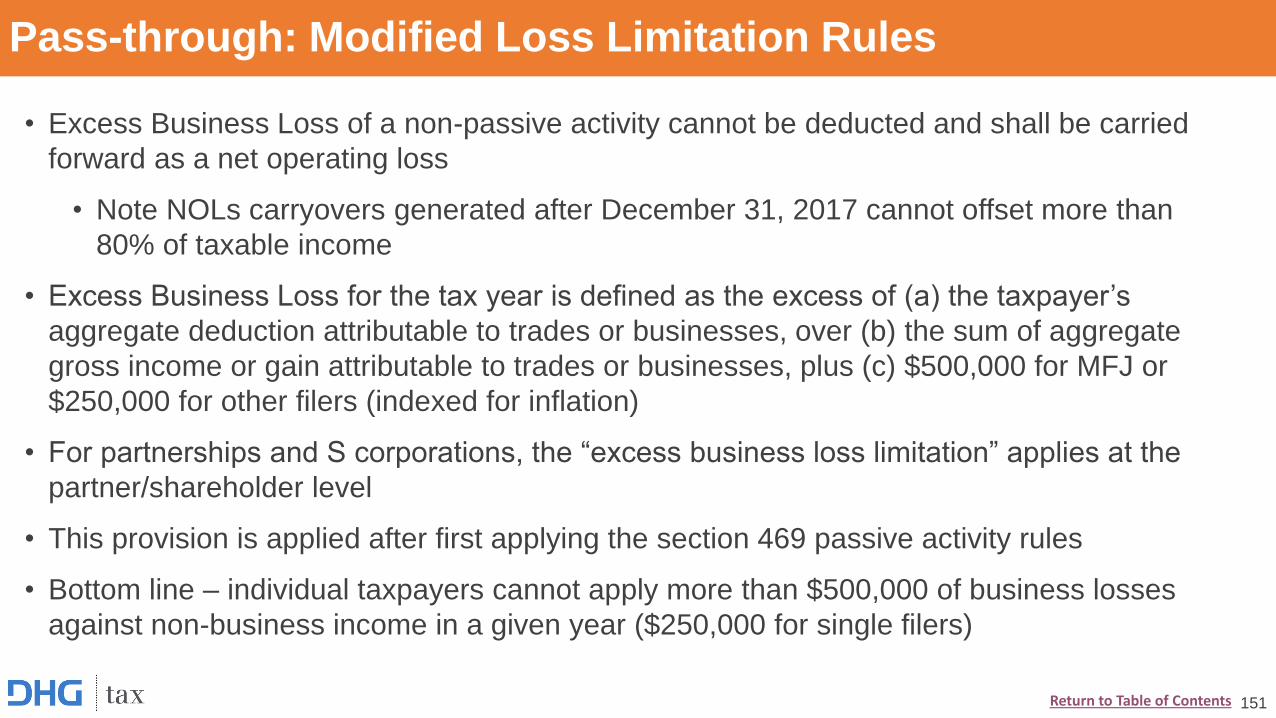

20% * 220,000 = 44,000