THE STATE OF THE ART IN FINANCE - CBS MoneyWatchi.bnet.com/whitepapers/SAP_State_of_Finance.pdf ·...

16

THE STATE OF THE ART IN FINANCE SAP INSIGHT

Transcript of THE STATE OF THE ART IN FINANCE - CBS MoneyWatchi.bnet.com/whitepapers/SAP_State_of_Finance.pdf ·...

THE STATE OF THEART IN FINANCE

SAP INSIGHT

Table of Contents

CEO Notes 1

Introduction 2

Is Cost all That Matters? 3

Conclusion 10

THE STATE OF THEART IN FINANCEBy Katharina Muellers-Patel

1

CEO NOTES

In the wake of recent accounting scandals and theincreasingly competitive business environment,many CFOs and the finance organizations they leadhave started to take on new strategic roles within theenterprise. They are aiming at enforcing strictercontrol processes to ensure legal and regulatorycompliance, offering strategic insights into theinternal and external business environment, andconnecting the business strategy with dailyoperations through performance tracking.

The trend toward a more strategic role is echoed bythe responses of participants in recent APQC surveys(formerly known as The American Productivity andQuality Center). Respondents indicated that, threeyears down the road, they would spend 30% moretime on decision support and management.According to the same surveys, however, theserespondents have not made much progress toward agreater strategic role. Finance organizations, nomatter what their size, report to APQC that they stillspend almost two-thirds of their time on transactionprocessing and controls and only one-third ondecision support and management.

The difficulty lies in bridging the current gapbetween the finance function that emphasizesgreater efficiency and the finance function thatbecomes a partner in managing the business. Thebest companies have found that reaching the goal ofa more strategic finance function warrants a two-step approach, as follows.

1. These companies deal with the complexity ofthe various functions that come under thefinance umbrella, making them as efficient aspossible and, in the process, freeing up corporateresources for other activities. As one globaltreasury manager put it, “We must develop afinance function that is as efficient as it can be,

replicate it globally, and then use it effectively tohelp us quickly establish brands and enter newmarkets.” Companies like this one choose avariety of approaches to streamline andautomate finance functions while ensuring thatthey keep customers happy (in the case ofshared-services arrangements).

2. With the efficiency of the transaction andcontrol functions assured, they can turn todevising a more strategic approach for finance -not only giving finance more of a decision-making responsibility in risk management andcompliance, but also a proactive role inmanaging the daily cash position to helpincrease resources for quick strategic moves.

One global consumer products company took thefollowing approach to a more strategic path forfinance. In the first step, the company developed amore efficient cash management, accounts payable,and accounts receivable group of functions in itsworldwide operations, based on greater transparencyof information. In the second step, the companydeveloped “straight-through processing” along everylevel of the finance function, leveraging its globalreach to maximize cash management efficiency,foreign-exchange exposure, and the global supplychain to help fund growth, participate in newmarketing and distribution arrangements, andcomply with worldwide regulations. The followingpoint of view will discuss the results of the APQCsurvey, as well as research performed by SAP, in lightof the current state of the finance function in U.S.companies, the challenges to that function, and theroad map to increasing its strategic capabilities.

2

The research group encompasses a wide samplingof organization size. Although the majority of respondents are billion dollar-plus organizations (inU.S. dollars ), their size in terms of revenue and number of employees covers a complete spectrum.

INTRODUCTION

Benchmarking is an important tool that financeorganizations use to stay competitive. It allows themto determine the value of adopting best practices andchanging business processes. To assess the trends inthe finance function and identify best practices,APQC has evaluated the performance of over 130finance organizations. The study included thefollowing key processes:

� Financial strategy and planning� Internal controls� Treasury� Revenue accounting (order to cash)� General accounting� Fixed assets and project accounting� Accounts payable and expense reporting� Tax� Payroll

This SAP Insight will discuss recent trends and bestpractices, as well as provide examples for those com-panies with best-practice processes, models, andtechnologies.

Study Demographics

Providing a Complete Picture

1As of August 20052All monetary amounts cited herein are in U.S. dollars.

Figure 1

39%

19%

13%29%

$ 1 billion-$10 billion

$ 100 million-$1 billion

<$ 100 million>$ 10 billion

Business UnitRevenue

SMB50k

Medium500k

Large5b

EnterpriseRevenue

Average 5.4% 5.7% 1.1% 1.0%

Median 2.7% 0.7% 0.6% 0.8%

3

Figure 3

Finance Costs as aPercentage of Revenue

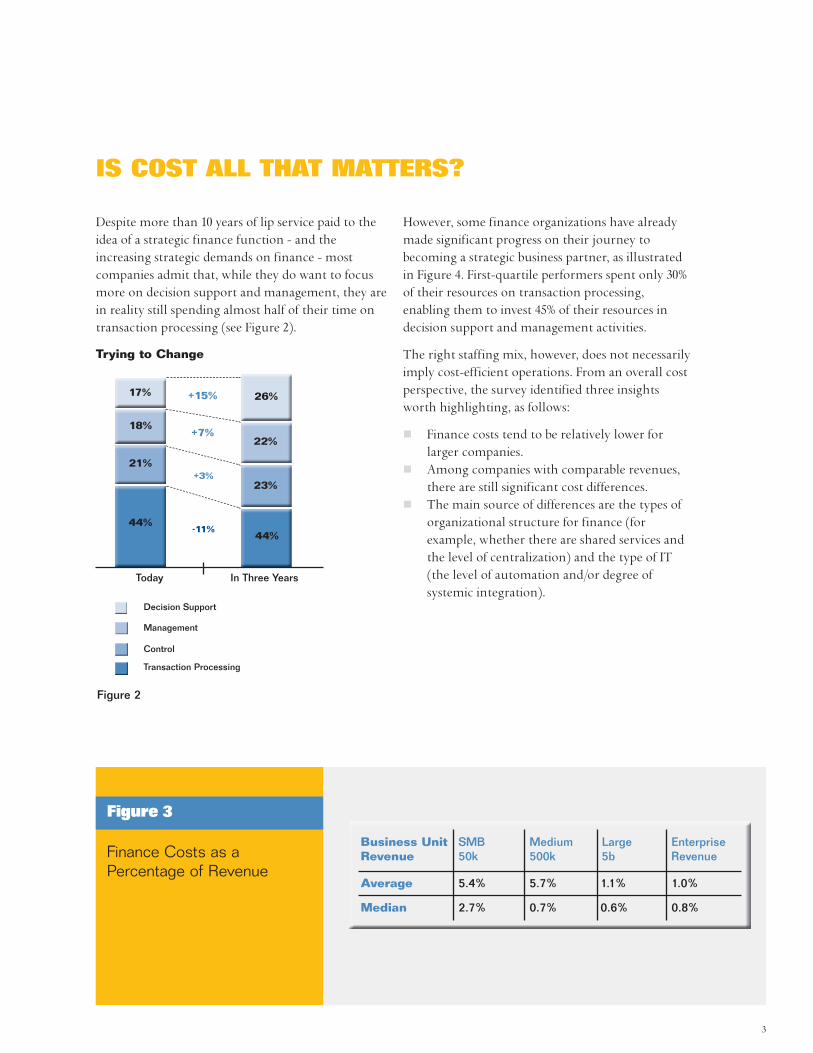

IS COST ALL THAT MATTERS?

Despite more than 10 years of lip service paid to theidea of a strategic finance function - and theincreasing strategic demands on finance - mostcompanies admit that, while they do want to focusmore on decision support and management, they arein reality still spending almost half of their time ontransaction processing (see Figure 2).

However, some finance organizations have alreadymade significant progress on their journey tobecoming a strategic business partner, as illustratedin Figure 4. First-quartile performers spent only 30%of their resources on transaction processing,enabling them to invest 45% of their resources indecision support and management activities.

The right staffing mix, however, does not necessarilyimply cost-efficient operations. From an overall costperspective, the survey identified three insightsworth highlighting, as follows:

� Finance costs tend to be relatively lower forlarger companies.

� Among companies with comparable revenues,there are still significant cost differences.

� The main source of differences are the types oforganizational structure for finance (forexample, whether there are shared services andthe level of centralization) and the type of IT(the level of automation and/or degree ofsystemic integration).

Figure 2

Trying to Change

Today In Three Years

44%44%

21%

18%

17%

23%

22%

26%

-11%

+3%

+7%

+15%

Decision Support

Management

Control

Transaction Processing

4

The first insight is not surprising, as largercompanies will be able to leverage economies of scale(see Figure 4 below).

However, within each revenue band, somecompanies had as much as 16 times relative higherfinance costs than other companies withapproximately the same revenues (see Figure 4).Among all the cost drivers discussed above, theextent to which the company established sharedservices was the strongest driver for cost efficiency(apart from revenues). In fact, the survey showedthat, given the average company revenue of $4.7billion, each additional shared service saves anaverage of $3.4 million!

It is logical that, in line with the focus on transactionprocessing, personnel represent the largest costelement, on average, comprising more than 65% ofall finance function costs.

SAP research has shown that leading companiesmaximize the efficiency of transactional activities asa first step on the road to a more strategic approach.One globally diversified industrial manufacturer, forexample, which considers itself world-class in everystrategic respect, has been coping with thecomplexities inherent in an acquisition growthstrategy that resulted in more than 60 acquisitionsand an almost equal number of divestitures (55 inall). The CEO wished to hone in on the segments

where the company’s product line leads the marketand exit those where it had no competitiveadvantage. While the strategy succeeded and growthwas maintained, operational difficulties began toshow up in the early 2000s. Each of the acquisitionsbrought along its own type of IT system; each had itsown finance function and its own approach. Theresult was a nightmare for the CFO. Working with abenchmarking firm to determine which financefunctions were not in the top quartile ofproductivity, he found that finance transactionprocesses clearly needed to be changed.

Shared services seemed to be an obvious target,especially for transaction-based functions. The firstchosen was payroll, which suffered from inefficientprocesses and lack of automation. Now the financialcenter operates so effectively that it has begun toshow a profit when employees ask for extra processes(cash advances, stop payments, manual checks, andso forth). The internal customers whose staffmembers use direct deposit and the self-serviceportal are charged less than those whose employeesprefer paper transactions. The keys to success are theuse of service-level agreements and a well thought-out performance management process to establishand track productivity goals with customers.

WHETHER TO OUTSOURCE OR SHARESERVICES

If you want to reduce costs or improve service levels,should you move to outsourcing - or is sharedservices the answer? Outsourcing is becomingincreasingly prevalent as a way to decrease costs. Forexample, the APQC survey found that when three ormore functions are outsourced, average costs offinance as a percent of revenue are only one-fourthof those costs without outsourcing.

Companies normally approach outsourcing inwaves, with payroll and tax among the first to beoutsourced, and fixed assets, general accounting andaccounts payable and expense as part of a second

10.00%

1.00%

0.10%0.10%

0.01%

Figure 4

Size Means Little to Costs

Revenue

5

wave. Finance strategy and planning, internalcontrols, and treasury are not typically outsourced;revenue accounting and order to cash might emergeas another outsourcing application in the future.

The outsourcing strategy varies among industries.While order-to-cash functions are not widelyoutsourced today, public utilities and energy are anotable exception. In these industries, where thenumber of customer payments is high andcustomers tend to get behind in their payments,many companies outsource both their accountsreceivable and credit functions, checking allcustomers through outside services. At that point,when collection becomes critical, the utility canconcentrate on enforcing collection rules wherenecessary, while the outsourcing service deals withthe majority of customers who do not overstep therules.

Companies also like to use shared services; whenmanaged well, shared services can improve processeffectiveness while helping decrease costs. APQCresearch found that the lowest-performingcompanies most often had not implemented sharedservices for any function and as a result, incurred thehighest cost of the finance function as a percentageof revenue (see Figure 5).

One consumer products company made the movetoward shared services and gradually improved theperformance of the finance function. The companyoptimized both IT systems and organization. Theperson in charge of finance shared servicesconsistently improves the function by measuringand tracking improvements. Its transaction centerhas become largely automated, freeing up financeemployees to perform more value-added, customer-oriented financial work.

Another example is a global pharmaceuticalcompany that has used shared services for more than15 years and simply changed the technologicalfoundation. The company had developed aphilosophy of centralization as part of its long-termstrategy to standardize, reduce costs, and increasecontrol and economies of scale as it embarked on apath of growth through acquisitions in the 1990s.Accounts payable has been a shared service eversince. The process was run on various legacysystems, but then upgraded to an overall enterpriseresource planning (ERP) system that handled theparent company’s transactions. Now, however, thecompany realizes that processes cannot be mademore efficient without changing the technologyagain. The company is experimenting with a fullyintegrated procure-to-pay approach, which willrequire integrating systems and developing theomnibus measurement system necessary to tracktransactions.

In another case, a large utility turned to sharedservices with the initial intent of increasing cost-efficiency. The utility, which serves a largemetropolitan area, is diverse and decentralized. Costsfrom shared services are shared by its customers;performance measures are based on the results ofshared services from other utilities around thecountry. The flexibility of the payroll shared-servicesystem has helped the company streamline processesand dramatically reduce cycle time. The unit morequickly isolates problems (such as employees who do

Figure 5

Shared Services Holds Down Costs

6

Companies that had automated more than 66% oftheir finance processes had average finance costsof 1.2% of revenues, while companies with lessautomation had average finance costs of 3.0% perrevenue.

not enter the required number of hours) andaddresses them before a payroll run. Continualbenchmarking against other companies in the sameindustry helps the utility firm find places toconsolidate and eliminate duplication of effort.

Besides the cost-efficiency inherent in theseimprovements, an unforeseen benefit of sharedservices is that employees in the payroll function cantake on other responsibilities with a longer-termimpact, such as developing new-hire orientationprograms and providing training programs infinancial management. As the finance function takeson more strategic roles, it has been able to provide anew level of incentives for its employees and has seenits historically high turnover rate moderate overtime.

MORE EFFECTIVE IT LEADS TO MOREEFFICIENT FINANCE FUNCTIONS

The APQC survey reaffirmed that more effective useof technology helps companies achieve greater levelsof efficiency and gradually frees up personnel formore strategic tasks requiring more thought andmanagerial capacity. Let’s first discuss how the rightuse of information technology leads to greaterefficiency and lower costs.

First, the APQC survey showed that companies witha higher degree of automation have lower overallfinance costs. Companies that had automated morethan 66% of their finance processes had averagefinance costs of 1.2% of revenues, while companieswith less automation had average finance costs of3.0% per revenue. For example, companies that reliedon manual techniques or spreadsheets for costaccounting and cost management had average coststhree times as high for that process ($2.21 per $1,000of revenue) than companies with an automatedprocess (only $0.72 per $1,000 of revenue).

Even more interesting, the APQC survey found thatwhile more automation means decreased costs, littleautomation even impedes reporting. APQC foundthat more than two-thirds of companies with lessthan 33% automated processes were unable toprovide process cost data. Only 32% of companieswith more highly automated processes were unableto provide detailed process cost data.

Looking further into the impact of automation,APQC found that packaged financial software (versuscustom applications or spreadsheets combined withmanual processes) is used in most core financeprocesses, including accounts receivable and payable,payroll, general accounting, and fixed-assetaccounting. As a result, companies have succeeded in

Planning/Budgeting/Forecasting

Cost Accounting/Cost Management

Evaluating andManagingFinancialPerformance

Single-instance accountingsoftware/ERP, commonchart of accounts

$1.60 $1.69 $1.87

Multiple instances or multiple accounting software applications

$2.62 $3.55 $3.21

7

reducing staffing levels in these areas (see Figure 6).On the other hand, less than 40% of the companiessurveyed had off-the-shelf software implemented inthe areas of cash management and planning,budgeting, and forecasting. These areas were amongthe most staff-intensive processes within the financefunction.

The research also found a correlation between thelevel of cost decrease and the lack of IT complexity.Companies in the APQC survey reported that theiraverage costs decreased dramatically when they useda single instance of ERP software and a common

chart of accounts (see Figure 7). When they usedmultiple instances or even multiple applications, thecost was more than 50% higher than with the singleinstance and common chart of accounts.

MORE EFFECTIVE IT ENABLES MORESTRATEGIC FINANCE FUNCTIONS

The use of an integrated ERP system by the financefunction also paves the way to a more strategicapproach. If a company establishes a more integratedprocess, planning and reporting cycle times aremuch reduced, providing data for critical decisionsmuch sooner and enabling improved decisionmaking by company executives. For example,looking at budget preparation cycle time or closingof monthly accounts, the APQC survey revealed thatcompanies relying heavily on manual processes orspreadsheets took an average of 90 days to preparetheir annual budgets, versus an average of 62 days forcompanies relying on an ERP system. The surveyshowed that companies with a rolling forecastreduced annual budget preparation time to 60 daysfrom 85 days on average. The average surveyparticipant generated $330,000 in cost savings eachadditional day the budget cycle time was reduced(through technology and improved processes).

Vendor Package

Manual/Spreadsheet

Custom

Figure 6

Reducing Staff at the Core

Figure 7

Comparison of Single-Instance ERP versusMultiple/Applications

8

Finance professionals echoed the fact that, movingforward, IT would take over more of thetransactional aspects of the function, while theythemselves will take over decision support andfinancial management activities, helping to make thefinance function more strategic. This forwardthinking is revealed in the APQC survey: despite thecurrent focus on processing transactions, APQCrespondents all indicated that, three years hence,they would be more involved with decision supportand management activities, underscoring the basicimportance of these more strategic capabilities

These respondents reflect the fact that CFOs andfinance functions must deal with a wealth of newdifficulties, including many that are at the heart ofthe company’s strategic goals - such as increasingshareholder wealth. The CFO’s function has becomepivotal to a company’s health in the following ways:

� Balancing revenue generation against costefficiency

� Assessing risk daily� Siphoning off risk into the future through

sophisticated use of derivatives� Managing earnings expectations and the need to

create shareholder value � Mitigating the deleterious effects of exchange

rate fluctuations

Yet it is difficult for the finance function to managethe earnings flow and shareholder expectations forthose earnings, given increasing global competitionand regulatory constraints. To achieve excellence infinance requires a greater attention to a balancing actbetween operational efficiency and strategiceffectiveness. The foundation for both is a great dealof analysis, data, and management time devoted toeach, as well as more automation of nonstrategic,more operational processes, freeing up manpower toperform the data collection

AN EXAMPLE OF A STRATEGICFINANCE FUNCTION

A global consumer products company has createdhighly successful strategic finance functions based ona four-phase approach and using software from SAP.The end point: complete transparency of financialdata across all global divisions. The CFO believes thatcash generation is the lifeblood of a consumerproducts company, affecting all parts of theorganization. Cash, in fact, is the barometer of thesuccess of the company’s brand-building exercises;sales indicate the strength of the brand, and salesgenerate the cash that allows the company to fundits brand-building activities in new regions and newproduct areas. To develop the capability to monitorand understand the company’s cash flow, however,

To achieve excellence in finance requires agreater attention to a balancing act betweenoperational efficiency and strategic effectiveness.

9

the CFO realized he had to take care of four endemicand chronic inefficiencies and data difficulties in thefollowing areas:

� Cash management� Foreign exchange processes� Funds transfers� Month-end closing and accounts receivable

The problems with cash management were symbolicfor the CFO as the root of all other evils. The processwas essentially manual, took most of the day, andresulted in many mistakes. That led to missedfunding opportunities in the commercial papermarket, whose rates rise during the day; seizingopportunities required understanding the cashposition immediately at the start of the day. Fromthere, according to the CFO, the finance functioncould achieve all other strategic objectives.

In Phase One, the company standardized andestablished new processes to reconcile bank accountsdaily, concentrate cash, determine a final number toborrow or invest each day, improve control, enhanceaccuracy, and pare down the number of full-timeequivalents (FTEs) involved in the function. Inanother development, global vendor payments wereintegrated with the bank payment systems, andcustomer receipts posted to the general ledger. Eachday, the company could then reconcile all global

account information. Contracts in the ERP systemwere linked to the daily cash position, providingperformance reporting and investment calculation.

In Phase Two, the CFO integrated the systems of theoffshore divisions into the main system. That tacticassures that he can see the state of cash managementin operations around the world.

Phase Three involved implementation of straight-through processing, whereby payments aretransmitted directly to the bank from payment data.A single platform uses payment files extracted fromthe SAP® accounts payable and treasury applicationsfor all types of payment. In effect the centraltreasury department has become the house bank forall of the company’s far-flung subsidiaries. Thecompany believes straight-through processingeliminates costly errors caused by processingdifferent payments in different countries. Inaddition, the straight-through processing of foreignexchange has cut down on difficulties in reconcilingpayments and revenues in the 30 or more currenciesin which the company operated.

Phase Four completed the process of developing thisstrategic approach. This final step entailed enteringall foreign exchange and commodities hedgingcontracts into the system, enabling the company toreconcile them itself without going through a third-

The company went so far as to do away with allmanual processing in accounting for derivativecontracts, as well. Not only did the companyreduce costs; it also created the type oftransparency and audit trail necessary to trulycomply with the U.S. Sarbanes-Oxley Act.

CONCLUSION

party processor. The company went so far as to doaway with all manual processing in accounting forderivative contracts, as well. Not only did thecompany reduce costs; it also created the type oftransparency and audit trail necessary to trulycomply with the U.S. Sarbanes-Oxley Act.

As a result, of the joint research between SAP andAPQC, we found that the best companies, and theirCFOs, recognize the importance of ready access tothe right information to drive the right choicesbetween different variables. Achieving this accessrequires the right system that will deliver thefollowing benefits:

� Accelerate closing processes throughautomation, workflow, and collaboration

� Improve business analysis and decision supportby providing historical and forward-lookingviews

� Deploy performance management tools thatanalyze the company and its resources

� Maximize cash flow through improved billing,receivables, collections, payments, and treasurymanagement

� Increase effectiveness of compliance effortsthrough comprehensive auditing, deeperreporting, and management of internal controls(Sarbanes-Oxley)

In addition, the integrated systemic foundation willhelp companies meet the following objectives:

� Structure strategy and communicate goalsthroughout the entire organization

� Monitor the performance of strategic keysuccess factors using external and internalbenchmarks

� Use tools that support a financial planningprocess that integrates global strategic planningand specific operational planning problems in aclosed-loop process

10

© 2006 by SAP AG. All rights reserved. SAP, R/3, mySAP, mySAP.com, xApps, xApp, SAP NetWeaver, and other SAP products and servicesmentioned herein as well as their respective logos are trademarks or registered trademarks of SAP AG in Germany and in several othercountries all over the world. All other product and service names mentioned are the trademarks of their respective companies. Data con-tained in this document serves informational purposes only. National product specifications may vary.

These materials are subject to change without notice. These materials are provided by SAP AG and its affiliated companies (“SAP Group”)for informational purposes only, without representation or warranty of any kind, and SAP Group shall not be liable for errors or omissionswith respect to the materials. The only warranties for SAP Group products and services are those that are set forth in the express warrantystatements accompanying such products and services, if any. Nothing herein should be construed as constituting an additional warranty.

www.sap.com

January 2006