The Smart Homebuying Guide - Bobby Poth · The Smart . Homebuying . Guide. Contact us today!....

16

The Smart Homebuying Guide Contact us today! Helpful steps leading to your new front door. Loan Originator – Team Lead NMLS ID# 1121969 14497 North Dale Mabry Hwy Suite 235N, Tampa, FL 33618 Phone: 813-961-3900 Cell: 813-638-1840 Toll Free: 888-395-6065 [email protected] NMLS # 2893 The Smart Homebuying Guide is a tool that clarifies the loan process. Use this easy to follow guidebook to reach your goals and monitor your progress. When you choose Revolution Real Estate and NFM Lending, you gain a team of Real Estate and Mortgage professionals to find the right property and the right property and the right mortgage for you! Bryan Marx

Transcript of The Smart Homebuying Guide - Bobby Poth · The Smart . Homebuying . Guide. Contact us today!....

The Smart Homebuying Guide

Contact us today!

Helpful steps leading to your new front door.

The Smart Homebuying Guide is a tool that

clarifies the loan process. Use this easy-to-

follow guidebook to write down your goals,

understand your options and keep track of

your progress. When you choose

for homebuying, you gain a team of

mortgage professionals who are dedicated to

finding the right mortgage loan with the best

rates and terms to meet your financial

objectives.

Loan Originator – Team Lead NMLS ID# 1121969 14497 North Dale Mabry Hwy

Suite 235N, Tampa, FL 33618

Phone: 813-961-3900 Cell: 813-638-1840 Toll Free: 888-395-6065 [email protected]

NMLS # 2893

NFM Lending

The Smart Homebuying Guide is a tool that clarifiesthe loan process. Use this easy to follow guidebookto reach your goals and monitor your progress. When you choose Revolution Real Estate and NFM Lending,you gain a team of Real Estate and Mortgage professionals to find the right property and the rightproperty and the right mortgage for you!

mo

Bryan Marx Robert "Bobby" Poth

Realtor @

Revolution Real Estate, LLC352/[email protected]

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

dklimyentyev

Typewritten Text

ABOUT NFM Lending NFM Lending is a national, full service mortgage lender, offering a diverse portfolio of home loan products. Our knowledgeable and seasoned mortgage specialists are committed to delivering an innovative, high-touch, high-tech lending experience for consumers, brokers, and our industry partners across the country. At NFM Lending we do everything we can to put more knowledge, initiative, and power back into the borrower’s hands – where it belongs.

• FHA o • Veterans • Cash-out

refinance

• Fixed rate o • Jumbo • Plus much

more!

• Adjustable rate o • USDA

• Conventional o • Investor

ABOUT The MARX Team

Whether you are buying, selling, refinancing, or building your dream home, you have a lot riding on your Mortgage Loan Originator. Since market conditions and mortgage programs change frequently, you need to make sure you are dealing with a top professional who is able to give you quick and accurate financial advice. As an experienced Mortgage Loan Originator, I have the knowledge and expertise you need to explore the many financing options available. Ensuring that you make the right choice for you and your family is my ultimate goal. I am committed to providing my customers with mortgage services that exceed their expectations. I hope you will browse my website, check out the different loan programs I have available, use my decision-making tools and calculators, and use our secure online application to get started. After you have applied, I will call you to discuss the details of your loan, or you may choose to set up an appointment with me using my online form. As always, you may contact me anytime by phone, fax or email for personalized service and expert advice.

- Bryan Marx, Loan Originator

. THE SMART HOMEBUYING GUIDE PAGE 1

HOME FINANCING FAQs If you have a question, please feel free to call me. I’m here to make sure you understand the homebuying process and address any concerns you may have. As a start, here are answers to some frequently asked questions:

How long does it take for you to process and close my loan? For a home purchase, the time it takes between submitting your loan application to sitting at the closing table averages about 30 days.

What do I need to qualify for a home loan?

Guidelines vary from one loan to another, but to qualify, you must have a stable income and meet the minimum credit requirements. While some situations require a down payment, we have many options that require zero down or a very low down payment.

Does it cost anything to get pre-qualified? Obtaining pre-qualification is free. I will review and explain your options with you, and will provide you with a pre-approval letter at no charge. Also, there is no obligation to proceed if you change your mind.

Why is it better to finance with NFM Lending than my bank?

Although you may have banked with the same institution for years, you need something tailored to your unique needs when seeking a home loan. You may be surprised to learn that larger banks often have fewer lending options. We offer many options that other lenders don't.

What if I have already been pre-qualified by my bank and just want another option? Is that OK?

Yes! You need to feel good about your lending decision. If you have already spoken with another bank or lender, feel free to seek other options and opinions. Give me a call and I will look over your information and make sure you understand all options available to you. At NFM Lending, we want you to be as happy with your loan as you are with your home.

How do I decide if a 15-year mortgage is better for me than a 30-year mortgage?

We’ll sit down together or talk over the phone and review your financial situation and objectives. Then we’ll

crunch the numbers to see which option best suits your needs and comfortably fits within your budget. My ultimate goal is to make sure you feel great about your loan decision.

I’m ready to apply. What should I expect? First, you’ll need to gather several documents, including personal and financial information. Then we

will complete the application together. By having all the documents on hand at this meeting, the process can be fast and efficient. To help you, there’s a handy document checklist on the next page.

THE SMART HOMEBUYING GUIDE PAGE 2

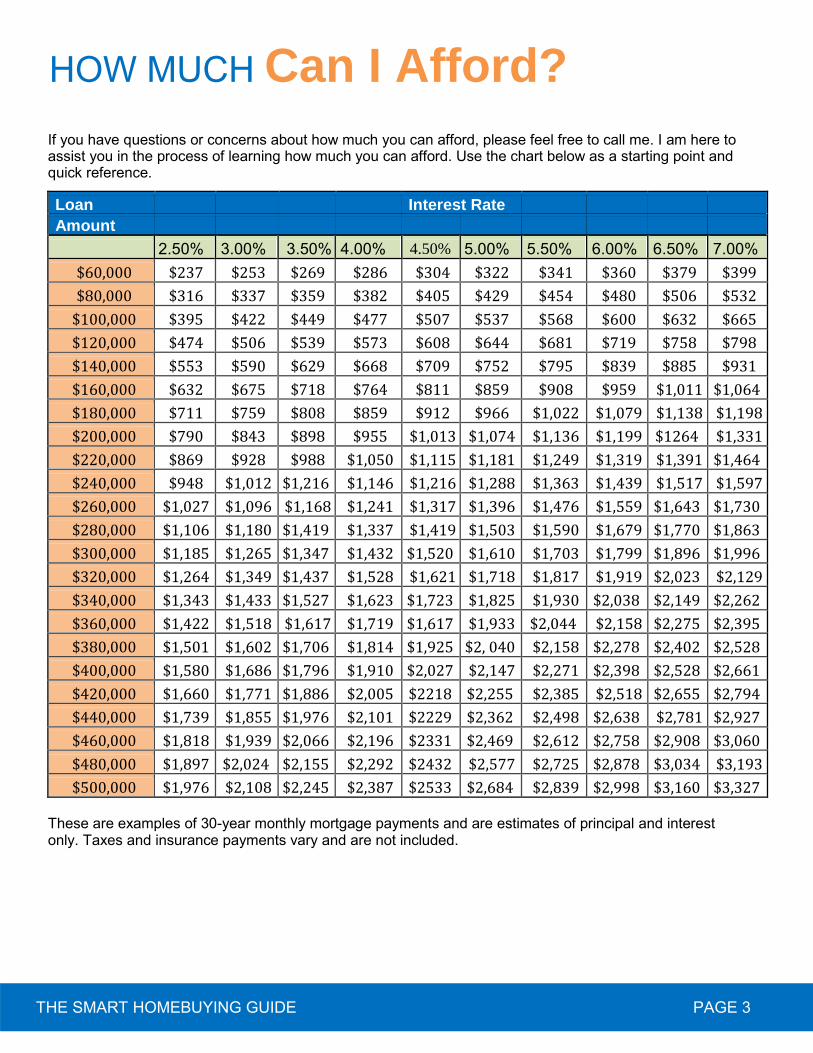

HOW MUCH Can I Afford?

If you have questions or concerns about how much you can afford, please feel free to call me. I am here to assist you in the process of learning how much you can afford. Use the chart below as a starting point and quick reference. Loan Interest Rate Amount

2.50% 3.00% 3.50% 4.00% 4.50% 5.00% 5.50% 6.00% 6.50% 7.00%

$60,000 $237 $253 $269 $286 $304 $322 $341 $360 $379 $399

$80,000 $316 $337 $359 $382 $405 $429 $454 $480 $506 $532

$100,000 $395 $422 $449 $477 $507 $537 $568 $600 $632 $665

$120,000 $474 $506 $539 $573 $608 $644 $681 $719 $758 $798

$140,000 $553 $590 $629 $668 $709 $752 $795 $839 $885 $931

$160,000 $632 $675 $718 $764 $811 $859 $908 $959 $1,011 $1,064

$180,000 $711 $759 $808 $859 $912 $966 $1,022 $1,079 $1,138 $1,198

$200,000 $790 $843 $898 $955 $1,013 $1,074 $1,136 $1,199 $1264 $1,331

$220,000 $869 $928 $988 $1,050 $1,115 $1,181 $1,249 $1,319 $1,391 $1,464

$240,000 $948 $1,012 $1,216 $1,146 $1,216 $1,288 $1,363 $1,439 $1,517 $1,597

$260,000 $1,027 $1,096 $1,168 $1,241 $1,317 $1,396 $1,476 $1,559 $1,643 $1,730

$280,000 $1,106 $1,180 $1,419 $1,337 $1,419 $1,503 $1,590 $1,679 $1,770 $1,863

$300,000 $1,185 $1,265 $1,347 $1,432 $1,520 $1,610 $1,703 $1,799 $1,896 $1,996

$320,000 $1,264 $1,349 $1,437 $1,528 $1,621 $1,718 $1,817 $1,919 $2,023 $2,129

$340,000 $1,343 $1,433 $1,527 $1,623 $1,723 $1,825 $1,930 $2,038 $2,149 $2,262

$360,000 $1,422 $1,518 $1,617 $1,719 $1,617 $1,933 $2,044 $2,158 $2,275 $2,395

$380,000 $1,501 $1,602 $1,706 $1,814 $1,925 $2, 040 $2,158 $2,278 $2,402 $2,528

$400,000 $1,580 $1,686 $1,796 $1,910 $2,027 $2,147 $2,271 $2,398 $2,528 $2,661

$420,000 $1,660 $1,771 $1,886 $2,005 $2218 $2,255 $2,385 $2,518 $2,655 $2,794

$440,000 $1,739 $1,855 $1,976 $2,101 $2229 $2,362 $2,498 $2,638 $2,781 $2,927

$460,000 $1,818 $1,939 $2,066 $2,196 $2331 $2,469 $2,612 $2,758 $2,908 $3,060

$480,000 $1,897 $2,024 $2,155 $2,292 $2432 $2,577 $2,725 $2,878 $3,034 $3,193

$500,000 $1,976 $2,108 $2,245 $2,387 $2533 $2,684 $2,839 $2,998 $3,160 $3,327 These are examples of 30-year monthly mortgage payments and are estimates of principal and interest only. Taxes and insurance payments vary and are not included.

THE SMART HOMEBUYING GUIDE PAGE 3

Document Worksheet ORGANIZE YOUR DOCUMENTATION A variety of personal and financial documents are needed to complete the loan application. To help you compile them, here’s a checklist of what you’ll need:

KEY DOCUMENTS: (Required for every application) W2s: For each job you’ve held over the last 2 years 1099s: For the last 2 years (Social Security, pension, etc.) Personal and business tax returns: For the last 2 years (all pages and schedules). Be sure to sign page 2 of Form 1040. Award letter: Most recent (Social Security, pension, etc.) Pay stubs: For the last 30 days Bank statements: For the last 2 months (all pages) Brokerage statements: Most recent (all pages) Driver's license: An enlarged copy for borrower and co-borrower Mortage statements: For all loans* Declarations page: Of your homeowners insurance* *If purchasing a second home.

ADDITIONAL DOCUMENTS: (Required for some situations only) ________________________________

________________________________

________________________________

________________________________

________________________________

________________________________

________________________________

THE SMART HOMEBUYING GUIDE PAGE 4

TIPS TO SELL Your Home If you currently own a home and are ready to sell and buy another, take a look at these tips. Maybe you’ll find a

few ideas that could make the difference for you to not only sell your house more quickly, but also to receive great offers.

Ramp up the curb appeal. To get folks inside the house, you need to first impress them with the outside. If your house and shutters have peeling paint, give them a fresh coat. Make sure your lawn is crisp, bushes trimmed, and mulch is fresh. Keep the walkway free of weeds, and put a pretty pot of flowers or greenery on your porch or front step. Sure, you’re investing

some money and time, but this is a key way to attract the eye of prospective buyers.

Clear the clutter. It’s common knowledge that staged homes sell faster. Buyers want to step into a place and see themselves living a great life in it, so remove “personality pieces” that can

distract them from seeing the home as their own. Pack away family and pet photos, knick knacks, trophies and mementos. Cull your books down. Hide toys and tikes. Your goal is for home shoppers to notice the house, not the things in it. Repair, replace and refresh. A dirty front door and grubby bathroom can be turn offs, but flaws that mean they might have to invest time and money on repairs can turn away move-in ready buyers. If you’ve got

broken shutters, leaky toilets, loose handles, outdated wall paper or stained carpets, then consider investing in elbow grease and a handyman. And it’s always a

good idea to paint a neutral color throughout.

Keep it clean. Make your home sparkle top to bottom. Clean windows inside and out. Sweep spider webs and leaves from the front steps. Keep only one appliance on each kitchen counter. Wipe down appliances. Polish furniture. Vacuum couches and chairs. Hide laundry in hampers. Put away shampoo bottles. Hang coordinating towels. Line up your shoes. Give the house a fresh fragrance by sprinkling carpets with freshener. Make it shine online. If you’re like a lot of homebuyers, you started your search for a new home online. So put this fact to your advantage: A study by trulia.com revealed that listings with more than six photos are twice as likely to be viewed by buyers as listings that had fewer than that amount. Choose to work with a real estate agency that has the ability to post photos on their site. Price it right. This is where the right real estate professional is key. You’ll want

someone who knows your market well, because house prices differ from one part of the country and one neighborhood to another. If you need help finding an agent, we can recommend top-notch professionals from coast to coast. Get a feel for the right asking price by looking on zillow.com at comparable homes for sale – and recently sold – in your area.

THE SMART HOMEBUYING GUIDE PAGE 5

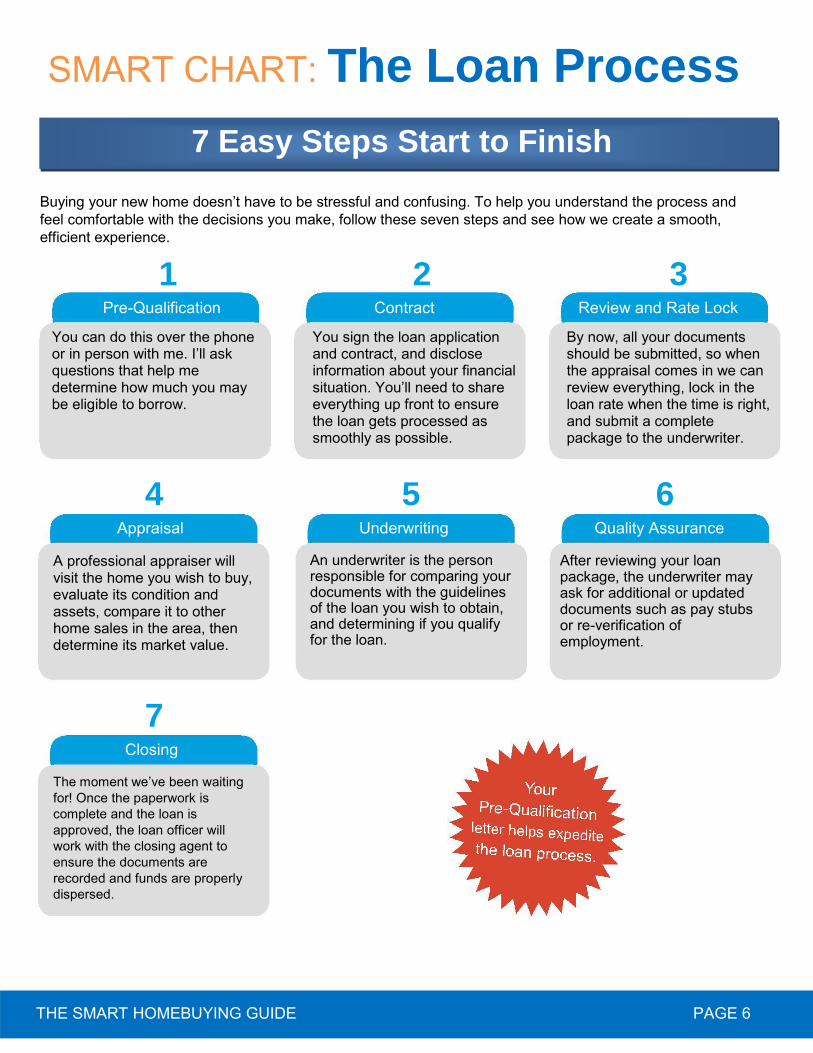

SMART CHART: The Loan Process

7 Easy Steps Start to Finish Buying your new home doesn’t have to be stressful and confusing. To help you understand the process and feel comfortable with the decisions you make, follow these seven steps and see how we create a smooth, efficient experience.

1 2 3

Pre-Qualification Contract Review and Rate Lock You can do this over the phone or in person with me. I’ll ask questions that help me determine how much you may be eligible to borrow.

You sign the loan application and contract, and disclose information about your financial situation. You’ll need to share everything up front to ensure the loan gets processed as smoothly as possible.

By now, all your documents should be submitted, so when the appraisal comes in we can review everything, lock in the loan rate when the time is right, and submit a complete package to the underwriter.

4

Appraisal A professional appraiser will visit the home you wish to buy, evaluate its condition and assets, compare it to other home sales in the area, then determine its market value.

5

Underwriting An underwriter is the person responsible for comparing your documents with the guidelines of the loan you wish to obtain, and determining if you qualify for the loan.

6

Quality Assurance After reviewing your loan package, the underwriter may ask for additional or updated documents such as pay stubs or re-verification of employment.

7

Closing The moment we’ve been waiting

for! Once the paperwork is complete and the loan is approved, the loan officer will work with the closing agent to ensure the documents are recorded and funds are properly dispersed.

THE SMART HOMEBUYING GUIDE PAGE 6

Step 1 Pre-Qualification We can do the loan pre-qualification process over the phone or in person. First, we’ll review your financial situation and objectives. Next, we’ll go over questions

about your employment, earnings, savings and other such information to help pre-approve you. I’ll also check your credit report. Rest assured that all your

information is kept confidential. I’ll use this information to see if you qualify for a mortgage and determine which loan options best suit your homebuying plans. Please conduct a thorough double-check of your paperwork for accuracy and legibility. Missing or incorrect information may delay the loan process.

Tasks:

Apply: Give us a clear picture of your financial situation so we can help you buy the home that’s

right for you.

Get Prepared: Gather the items on the Documents Worksheet, and get phone numbers for your human resources department and home-insurance agent, plus anything else you think would be helpful to process your application.

Step 2 Contract

Listen: We need to learn about your financial

situation, and your homebuying plans and goals. We'll look at your credit and discuss it with you.

Timeline: We'll review all the steps in the application process and estimate when it will be complete.

In this step, you sign your loan application and contract, and provide information that verifies your income and other assets. Please disclose everything at the beginning. Being up front from the start helps your loan process as quickly and smoothly as possible.

The initial paperwork does not finalize your loan. Rather, it is used to comply with government lending requirements. If anything on the application is not accurate, such as your work telephone number, just let us know and we will fix the inaccuracy before the closing.

Tasks:

Phone appointment: Ask questions. We Be available: Our most important duty in this want you to have a clear understanding of all step is to be ready and available to review all the paperwork you're signing, so let's cover paperwork with you and provide answers to any everything. questions you may have.

Return documents: The documents Double-check: Once your income documents in Step 1 should be returned as soon are received, we will review and update all

as you can gather them to ensure an accurate information to ensure your application can be pre-approval. approved.

THE SMART HOMEBUYING GUIDE PAGE 7

Step 3 Review & Rate Lock By now, all of your documents should be submitted. A rate lock is a guarantee to “lock in” the interest rate at which you will pay back your home loan. This protects

you from rate fluctuations in the market during the mortgage review period.

If mortgage rates climb after the rate lock is in place, you benefit by getting the lower interest rate once your loan is approved.

Tasks:

Lock: Locking in a loan rate can be completed at any stage after application. Feel free to consult with me on when is the right time to lock in your loan.

Review: Perform a final review of all options and make the most favorable decision. As always, I am available to answer your questions and offer advice.

Document: We will properly document everything

that goes into your loan file to ensure full transparency and an efficient approval process.

Copy of the appraisal: We'll send you a copy of your appraisal report for your records and review.

Step 4 Appraisal

The home appraisal is a key component of the loan process. Finance of America hires a certified professional appraiser to establish the market value of the property you’re interested in purchasing. The appraiser is licensed by the state with no

financial or personal connection to you or the seller.

The home’s value is calculated by reviewing factors that include the home's size, location, condition, structural integrity, proximity to neighborhood amenities, and sale and listings prices for comparable area homes.

Tasks:

Be patient: It typically takes about an hour Arrange appraisal: Our team will coordinate

for the appraiser to conduct a full analysis. The with the appraisal company to set up the

report is sent to Finance of America as soon as appraisal inspection of the home you are

it is completed by the appraiser, which can take interested in buying. The appraisal management

anywhere from three days to two weeks. company and the loan officer will discuss the

Be aware: It’s important to know what the expected timeline to receive your appraisal back.

home is worth. Think of the appraisal as an Finishing touches: We will communicate with

investment in your time, money and efforts. your title company, realtor and insurance.

THE SMART GUIDE TO HOMEBUYING PAGE 8

Step 5 Underwriting Conditions After the loan processor has compiled all your paperwork, it is handed over to the underwriter. An underwriter is responsible for comparing your documents with the guidelines of the loan you wish to obtain. The underwriter determines whether or not you meet all the conditions. It’s the underwriter’s job to double-check the processor’s work and compare your files

to the guidelines of the loan program to ensure that everything is in order. In some cases, the underwriter may approve your loan, but make the approval conditional upon you meeting additional criteria.

Tasks: Be ready for potential last-minute needs: During this part of the process, both you and your loan officer are eagerly awaiting the underwriting review. You can help the review proceed smoothly by quickly compiling any other information and documents requested by the underwriter. Make any and all payments: Missed or late

payments may affect your credit rating and lead to delays in approval.

Working with the loan processor: We'll meet with the loan processor at the time of submission to underwriting for guidance as to what may be needed moving forward. Income verification: Our processing staff will reach out to your employer and/or other entities as needed to verify your employment and income.

Step 6 Quality Assurance After reviewing your loan package, the underwriter may ask for updated documents, which you’ll need to submit at this time. For instance, you may be asked to provide

additional pay stubs or reverification of employment. We’ll go over the conditions so

you know exactly what is needed from you.

Tasks: Approve final disclosure: We strongly suggest you look over the final set of loan disclosures with your loan officer. Once you’ve had a chance to review and sign these documents, we will need them returned for compliance purposes. Prepare for settlement: Let us know days and times that work best to schedule the closing.

Double-check the final documents: We will thoroughly review all the final documents for accuracy and go over them with you. Await the final "Clear to Close": You've now passed underwriting with flying colors, and we await verification that all documents are compliant. Schedule the closing: Once we have the "Clear to Close," we will call you and celebrate the great news. Then we will verify the best time and location for settlement.

THE SMART HOMEBUYING GUIDE PAGE 9

Step 7 Closing This is exciting! The conditions of the loan have been met. The loan is approved by the underwriter and now proceeds to the closing table. You’ll be asked to sign closing documents, which can be done at the title company,

the real estate agent’s office, or various other locations. Once complete, I’ll

communicate with the closing agent to ensure your documents are recorded and funds are disbursed properly. The loan will close and the funds will be disbursed on the same day.

Tasks: Settlement: Attend the closing at the as-signed time and place. I.D. and payment: Please be sure to bring a valid form of photo identification (driver's license) and a certified bank check for the amount due. Performance review: After your loan has closed, you will receive a survey in the mail. Feedback is essential as we continually strive to improve our service. We truly care what you think; please take a few minutes to tell us how we did.

Gather all parties: We will confirm that all necessary parties — you, the seller, real estate agent and any lawyers — can sign the documents at an agreed-upon time and place. (Long-distance sellers may sign at another authorized location.) Answer closing questions: We remain ready and available to answer all questions you may have, either during closing or after. Return copies of documents: If you submitted any original documents, rest assured that we will return these documents to you now that the loan is complete.

THE SMART HOMEBUYING GUIDE PAGE 10

DO'S & DON'TS

During the Loan Process

1. Do consider having a professional home inspection performed. You need to learn as much as you can about the home, and a home inspection can help identify the need for major repairs or maintenance issues. 2. Do ensure that the person you hire to conduct the home inspection is reputable and certified. You can access a list of inspectors certified by the American Society of Home Inspectors at www.ashi.org. 3. Do ask questions. Turn to us to gain a better understanding of every detail and to get answers to your questions as they come up. 4. Do continue to collect pertinent information. Most recent pay stubs may be needed, so keep updated information on hand. 5. Do refer me, please. Our business is built on providing high-quality service and satisfaction. If we did an excellent job for you, we’d be happy to assist any friends, family or colleagues who you think could benefit from our loan products and services.

6. Don’t incur more debt! We cannot emphasize this enough. Hold off on that new car, boat or credit card. Any new debt could result in additional delays in the loan process.

7. Don’t open or close new credit accounts or change banks in the months prior to applying for your loan. Account changes can affect your credit rating. 8. Don’t consolidate credit cards or open new lines of credit. This may negatively affect your debt-to-credit ratio. 9. Don’t change jobs. Try not to make a career move until after your loan has closed. You want to demonstrate income stability. 10. Don’t spend the money you have in the bank. Many mortgages are approved on the condition that you have a certain amount of money on reserve after closing. Although you may be eager to purchase new furniture or accessories for your new home, please hold off.

THE SMART HOMEBUYING GUIDE PAGE 11

DO YOUR

Homework

Don’t wait until the last minute to prepare to move into your new home! Here are tips to help you plan ahead.

Schedule utilities stop/start: Create a list of all the utilities and services you will need to turn off and on so you will have power on your first day in your new home—gas, electric, cable, phone, alarm system, etc. Some services will transfer. Find utility providers at moving.com.

Change address: Make sure your mail delivery isn’t interrupted by visiting moversguide.usps.com. Let your magazine and newspaper providers know, too.

Hire a mover: Get recommendations from friends, colleagues and real estate agents. Check reputations at the Better Business Bureau’s site: bbb.org. Obtain an in-person, written estimate of how much your move will cost from at least three potential movers before you choose one.

Transfer schools: If you have children, collect the necessary paperwork from the district you’re

leaving, and then visit the new school(s) to enroll each child. Ask about bus routes, lunch costs, dress codes, and any immunizations required.

Source services: To find recommended dry cleaners, lawn service providers, roofers, remodelers or furnace technicians, check out angieslist.com or homeadvisor.com.

Choose caregivers: You can review the bios of housekeepers, babysitters, pet-care providers, elder-care providers and tutors at care.com or sittercity.com.

Discover best routes: Try different ways to get from your new house to your job, sitter, church, gas stations, grocery stores and other frequently visited locations to learn the best routes.

Find great food: Don’t fret about cooking the first night in your new house! Visit yelp.com or zagat.com to find popular pizza shops and dining destinations in your new neighborhood.

THE SMART HOMEBUYING GUIDE PAGE 12

IMPORTANT

Telephone Numbers Use this worksheet for quick reference.

LOAN OFFICER _____________________________________________

REAL ESTATE AGENT ____________________________________________

PROCESSOR _____________________________________________

TITLE COMPANY _____________________________________________

CLOSING AGENT ____________________________________________

HOUSE INSPECTOR ____________________________________________

OTHER _____________________________________________

OTHER _____________________________________________

OTHER ____________________________________________ OTHER _____________________________________________

OTHER _____________________________________________ THE SMART HOMEBUYING GUIDE PAGE 13

IMPORTANT

Notes Keep track of important notes and questions as they arise.

THE SMART HOMEBUYING GUIDE PAGE 14

*100% financing, no down payment is required. The loan amount may not exceed 100% of the appraised value, plus the guarantee fee may be included. Loan is limited to the appraised value without the pool, if applicable. To be eligible for a USDA RDHL: NFM Lending requires attending an approved on-line training seminar prior to taking any application. This is not a credit decision or a commitment to lend. Eligibility is subject to completion of an application and verification of home ownership, occupancy, title, income, employment, credit, home value, collateral and underwriting requirements. Not all programs are available in all areas. Offers may vary and are subject to change at anytime without notice. NFM, Inc. is an FHA-Approved Non-Supervised Mortgagee (19951-0018-0 and 19951-0000-7) and Veterans Affairs Automatic Lender (659985-00-00) under the trade name NFM Lending. NFM, Inc. is licensed as: Florida Mortgage Lender License (MLD174) and Florida Mortgage Lender Servicer License (MLD795) under the trade name NFM Lending. NFM, Inc.’s Nationwide Mortgage Licensing System (NMLS) Company Identifier Number is 2893. NFM, Inc. is not affiliated with, or an agent or division of, a governmental agency or a depository institution. Copyright © 2015.