The SKF Group Nine-month result, 2005 Tom Johnstone, President and CEO.

24

-

Upload

basil-mcdowell -

Category

Documents

-

view

221 -

download

0

Transcript of The SKF Group Nine-month result, 2005 Tom Johnstone, President and CEO.

The SKF GroupNine-month result, 2005

Tom Johnstone, President and CEO

3

MSEK 2005 2004

Net sales 12 027 11 184

Operating profit 1 454 1 189

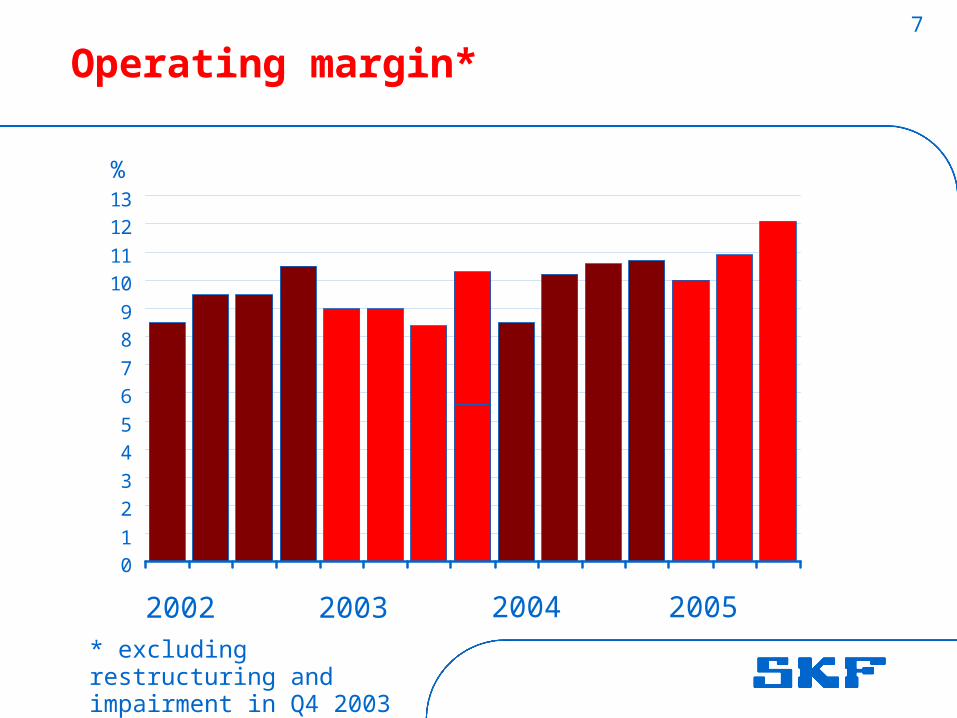

Operating margin 12.1% 10.6%

Profit before taxes 1 409 1 110

Net profit 974 729

Earnings per share, SEK 2.09 1.43

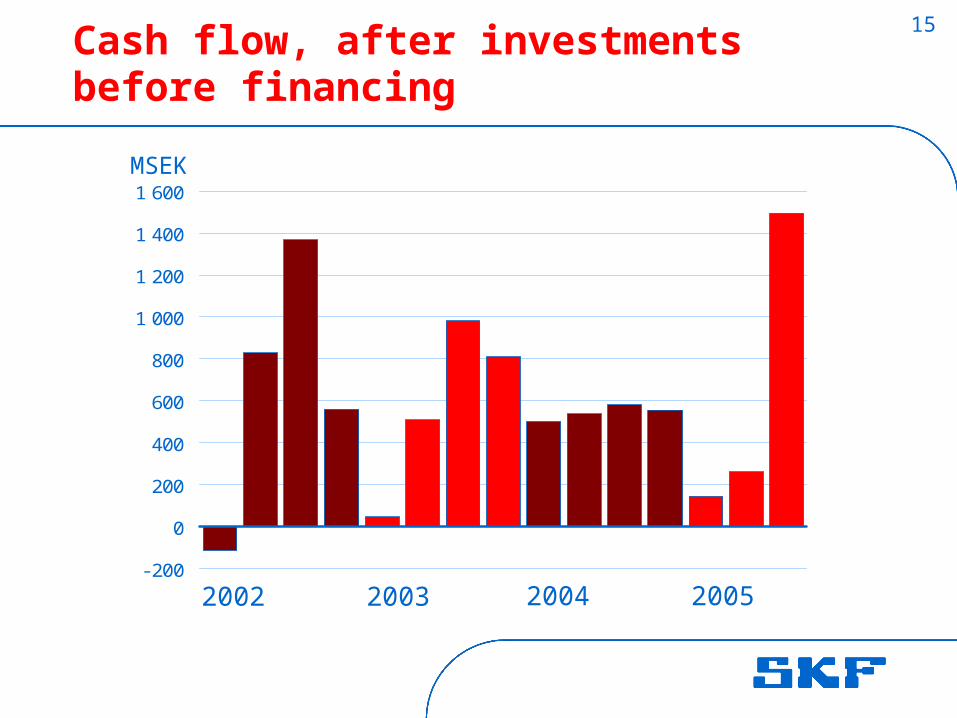

Cash flow after investments before

financing 1 495 516

Third quarter 2005

4

MSEK 2005 2004

Net sales 36 637 33 290

Operating profit 4 025 3 251

Operating margin 11.0% 9.8%

Profit before taxes 3 852 2 974

Net profit 2 658 2 131

Earnings per share, SEK 5.69 4.23

Cash flow after investments before

financing

1 901* 1 610

Nine-month result 2005

* MSEK 2 366 before the acquisitions and the purchase of minority shareholding in previously acquired companies.

5 Areas in focus 2005 Performance Q3 2005

• Operating margin level

Maintain a positive price/mix

Recovery of raw material cost increase

• Continued sales growth

Maintain organic growth pace

Structure (mainly Ovako)

• Strengthen the platform/segment offer

• Cash flow before financingand acquisitions

2.1%

Ongoing

7.2%

-2.9%

Ongoing

MSEK 1 495

6

Major events during the quarter

• Doubling of manufacturing capacity in Indonesia

• Locomotive axle boxes order from Alstom

• X-Tracker hub units for 2006 Cadillac STS-V

• Sustainability - For the sixth year: DJSI World and DJSI STOXX - For the fifth year: FTSE4Good

7

Operating margin*

%

2002 2003 2004

0

1

2

3

4

5

6

7

8

9

10

11

12

13

* excluding restructuring and impairment in Q4 2003

2005

8

0

2

4

6

8

10

12

14

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

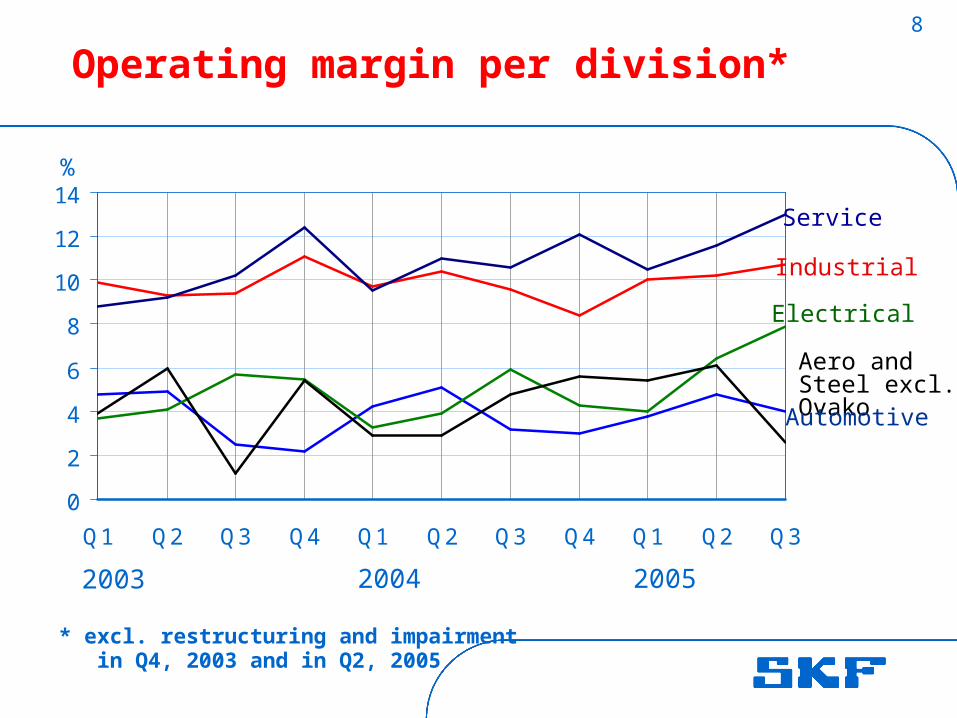

Operating margin per division*

Industrial

Service

Aero and Steel excl. Ovako

Electrical

Automotive

%

2003 2004

* excl. restructuring and impairment in Q4, 2003 and in Q2, 2005

2005

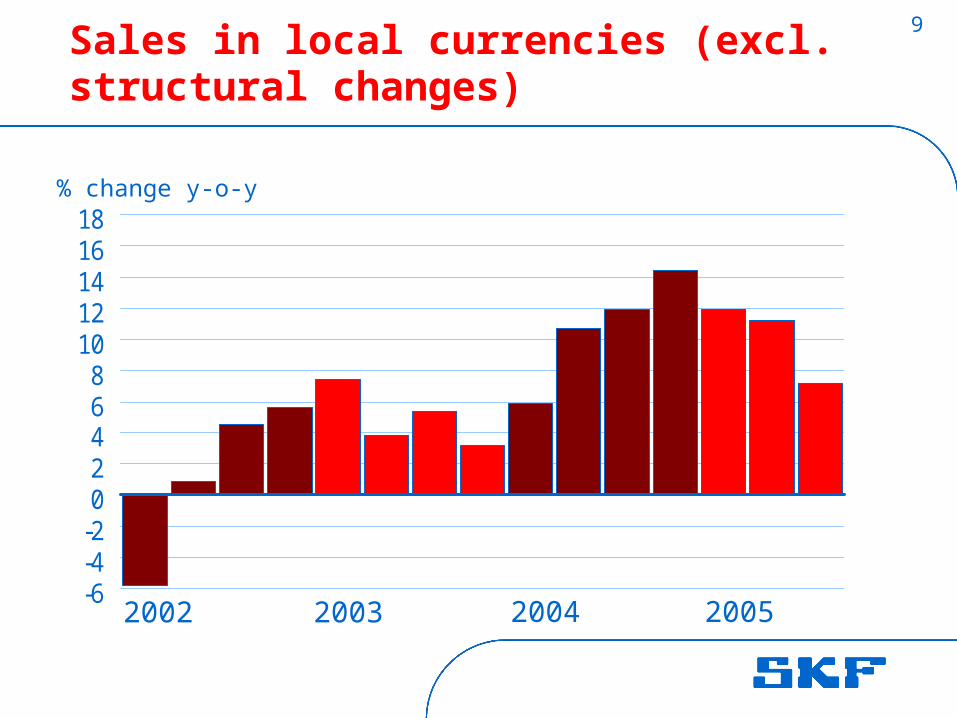

9Sales in local currencies (excl. structural changes)

-6-4-202468

1012141618

% change y-o-y

2002 2003 2004 2005

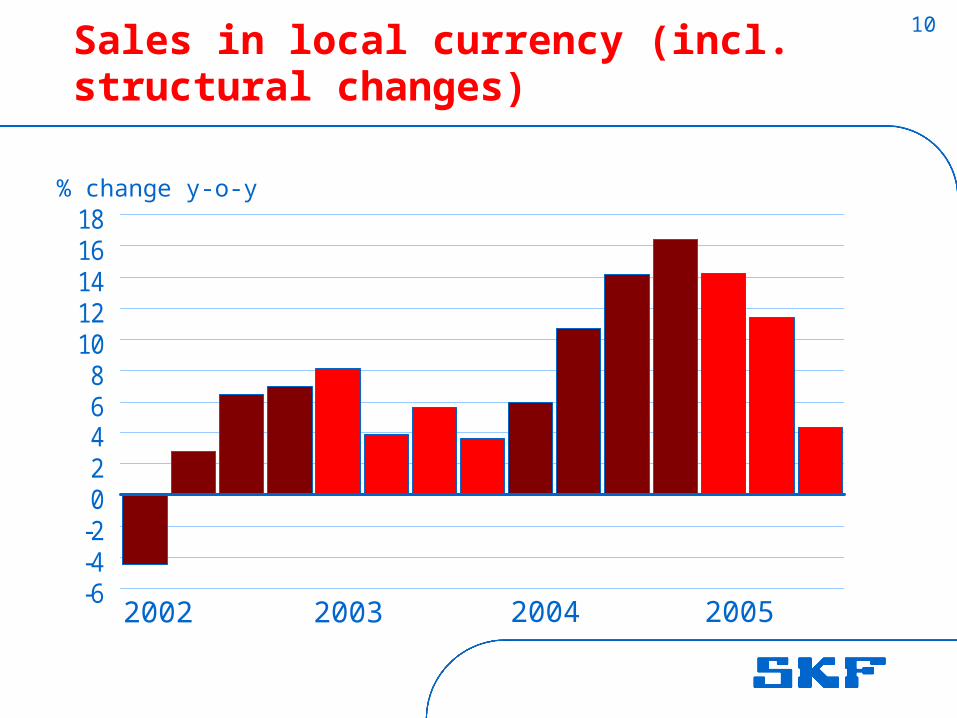

10Sales in local currency (incl. structural changes)

-6-4-202468

1012141618

% change y-o-y

2002 2003 2004 2005

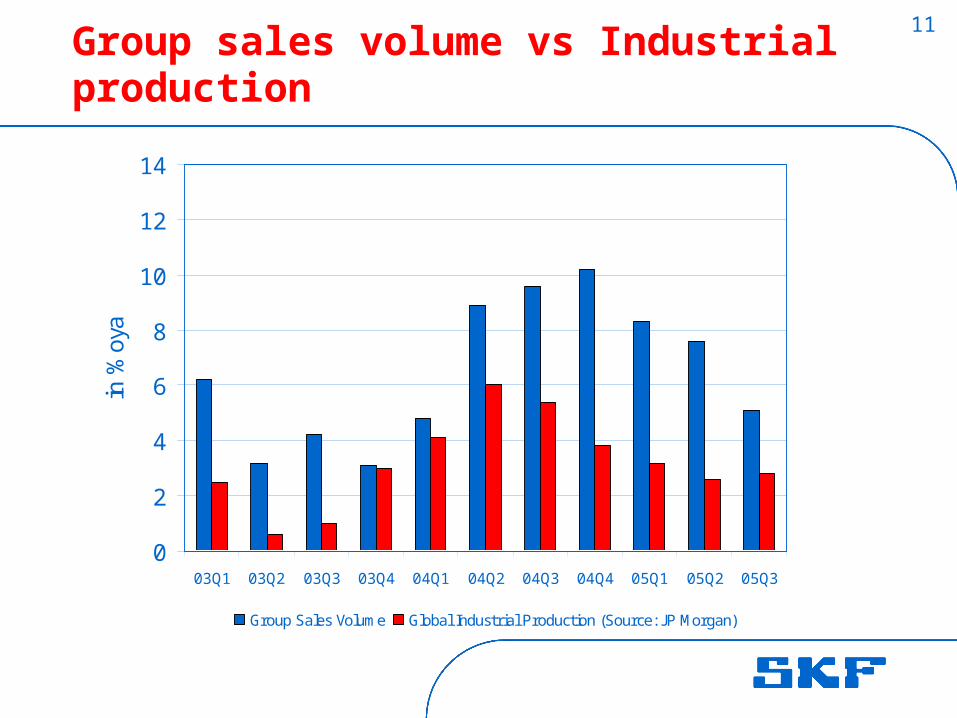

11Group sales volume vs Industrial production

0

2

4

6

8

10

12

14

03Q1 03Q2 03Q3 03Q4 04Q1 04Q2 04Q3 04Q4 05Q1 05Q2 05Q3

in %

oya

Group Sales Volume Global Industrial Production (Source: JP Morgan)

12

Growth development / local currency6% annual growth rate (whereof 4% organic)

% Y-o-Y

0

2

4

6

8

10

12

2002 2003 2004 2005

Acquisitions / Divestments

Organic growth

Up to September

(Organic 9.9, Net acq/div -0,2)

3.0

9.7

5.2

11.8

13

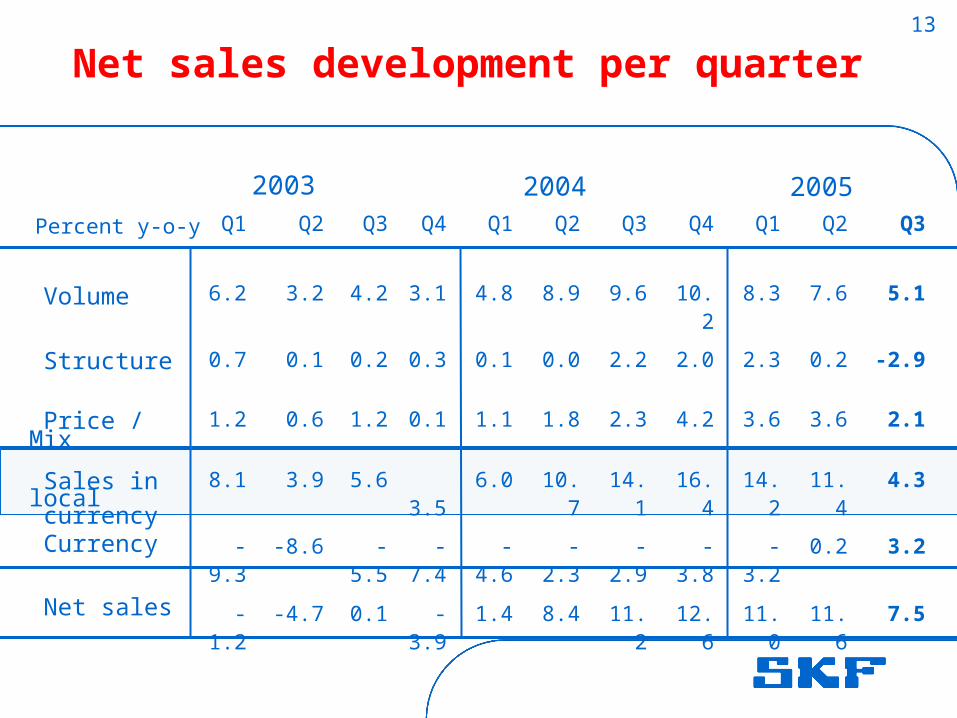

Net sales development per quarter

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

6.2 3.2 4.2 3.1 4.8 8.9 9.6 10.2 8.3 7.6 5.1

0.7 0.1 0.2 0.3 0.1 0.0 2.2 2.0 2.3 0.2 -2.9

1.2 0.6 1.2 0.1 1.1 1.8 2.3 4.2 3.6 3.6 2.1

8.1 3.9 5.6 3.5

6.0 10.7 14.1 16.4 14.2 11.4 4.3

-9.3 -8.6 -5.5 -7.4

-4.6 -2.3 -2.9 -3.8 -3.2 0.2 3.2

-1.2 -4.7 0.1 -3.9

1.4 8.4 11.2 12.6 11.0 11.6 7.5

Percent y-o-y

2003 2004

Volume

Structure

Price / Mix

Sales in local currency Currency

Net sales

2005

14

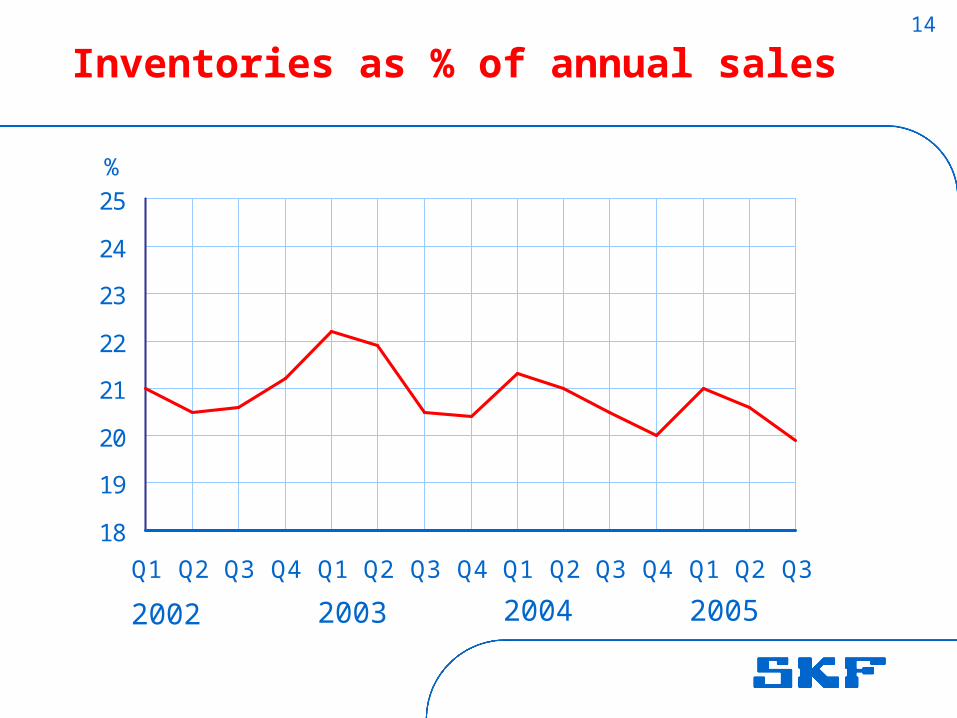

Inventories as % of annual sales

%

2002 2003 2004

18

19

20

21

22

23

24

25

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2005

15Cash flow, after investments before financing

-200

0

200

400

600

800

1 000

1 200

1 400

1 600MSEK

2002 2003 2004 2005

16

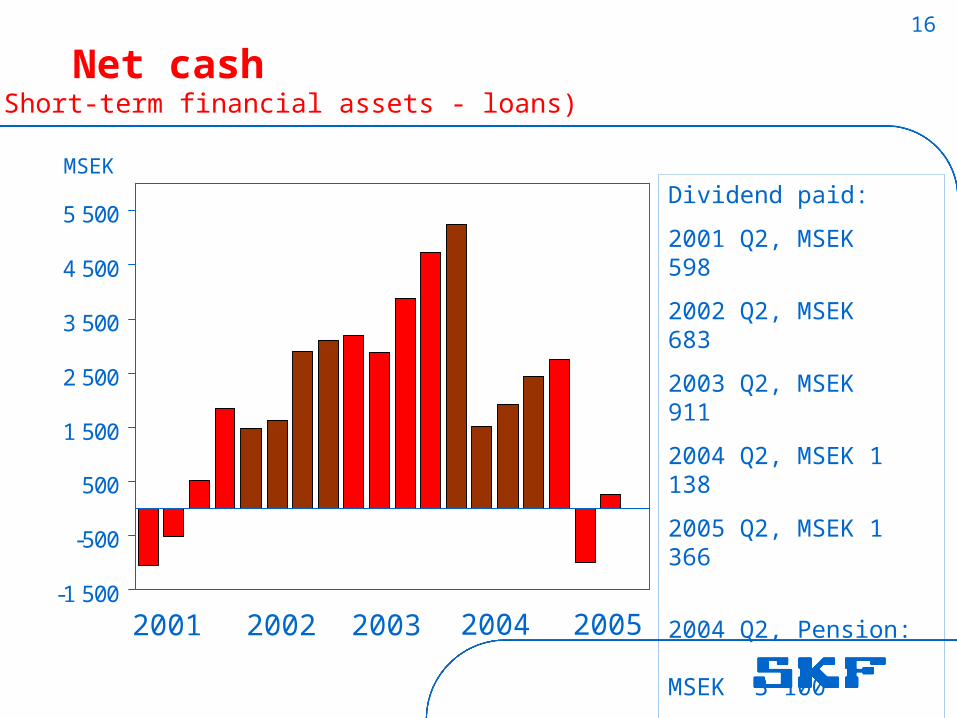

Net cash

-1 500

-500

500

1 500

2 500

3 500

4 500

5 500

MSEK

2001 2002 2003

Dividend paid:

2001 Q2, MSEK 598

2002 Q2, MSEK 683

2003 Q2, MSEK 911

2004 Q2, MSEK 1 138

2005 Q2, MSEK 1 366

2004 Q2, Pension: MSEK 3 100

2005 Q2, Redemption, MSEK 2 846

2004

(Short-term financial assets - loans)

2005

17

Net interest bearing liabilities

-6 000

-5 000

-4 000

-3 000

-2 000

-1 000

0

1 000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

MSEK

(Short-term financial assets - loans - net postemployment benefits)

2003 2004 2005

18

-8 000

-6 000

-4 000

-2 000

0

2 000

4 000

6 000

2000 2001

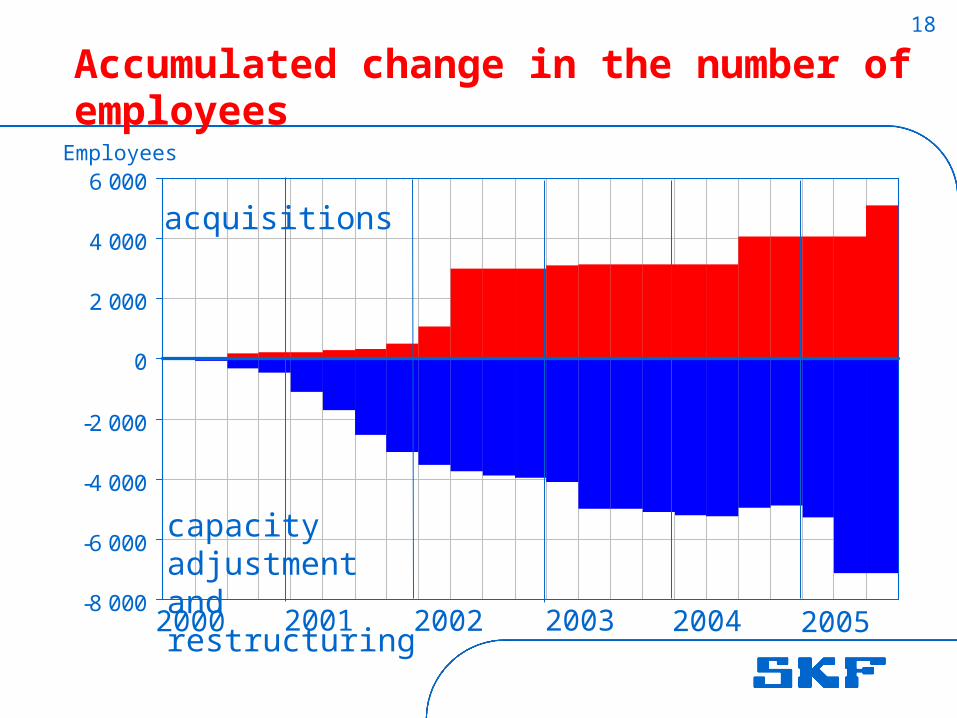

Accumulated change in the number of employees

2002

acquisitions

capacity adjustmentand restructuring

Employees

2003 2004 2005

19

Fixed assets / Sales

20

22

24

26

28

30

32

34

36

38

40

98 99 00 01 02 03 04 05

%%

Up to September

20

SKF Group targets

• 10% Operating margin level

• 6% Growth per annum

• 20% ROCE

• 18% Inventory / sales

2006

2007

21 October 2005: Outlook for the fourth quarter

The market demand for SKF's products and services in the fourth quarter, compared to the previous quarter, is expected to remain on a high level in Europe, to be slightly higher in North America, significantly higher in Asia and to remain on a high level in Latin America. This is in addition to normal seasonality.

The manufacturing level will be unchanged during the fourth quarter, compared to the third quarter, while higher in absolute terms due to normal seasonality.

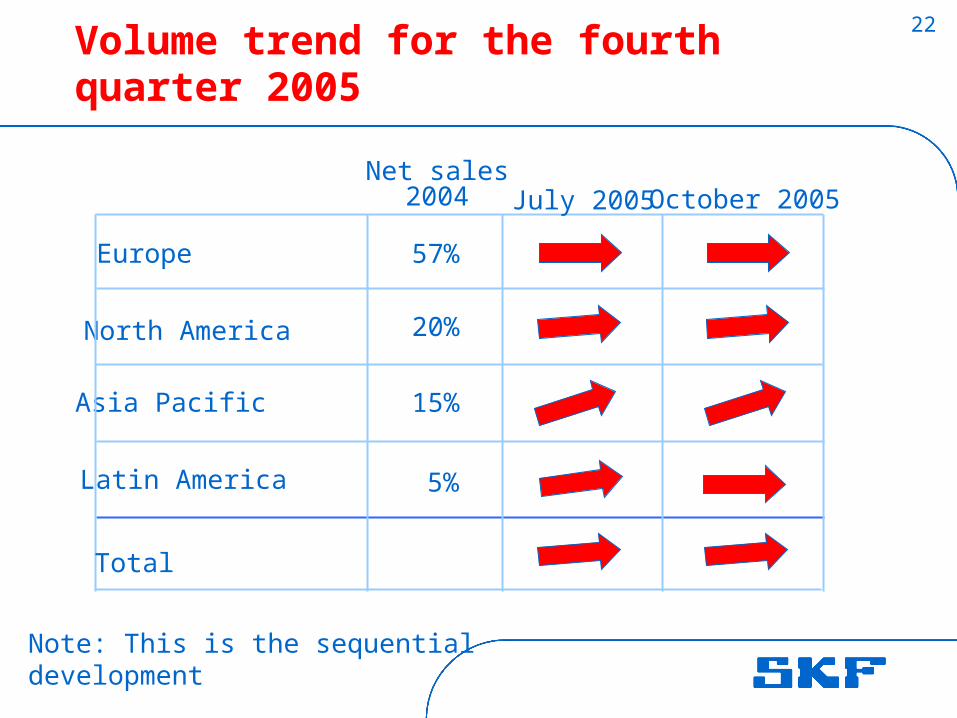

22Volume trend for the fourth quarter 2005

Europe 57%

20%

15%

5%

North America

Asia Pacific

Latin America

Net sales 2004 October 2005

Total

July 2005

Note: This is the sequentialdevelopment

23

Cautionary statement

This report contains forward-looking statements that are based on the current expectations of the management of SKF.

Although management believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those implied in the forward-looking statements as a result of, among other factors, changes in economic, market and competitive conditions, changes in the regulatory environment and other government actions, fluctuations in exchange rates and other factors mentioned in SKF's latest 20-F report on file with the SEC (United States Securities and Exchange Commission) under "Forward-Looking Statements" and "Risk Factors".