THE SHERWIN-WILLIAMS COMPANY SALARIED … · 5 WHO TO CONTACT Sherwin-Williams Retirement & Savings...

22

1 THE SHERWIN-WILLIAMS COMPANY SALARIED EMPLOYEES’ PENSION INVESTMENT PLAN SUMMARY PLAN DESCRIPTION (SPD) 2011 Edition TABLE OF CONTENTS

-

Upload

truongdung -

Category

Documents

-

view

342 -

download

1

Transcript of THE SHERWIN-WILLIAMS COMPANY SALARIED … · 5 WHO TO CONTACT Sherwin-Williams Retirement & Savings...

1

THE SHERWIN-WILLIAMS COMPANY SALARIED EMPLOYEES’

PENSION INVESTMENT PLAN

SUMMARY PLAN DESCRIPTION (SPD)

2011 Edition

TABLE OF CONTENTS

2

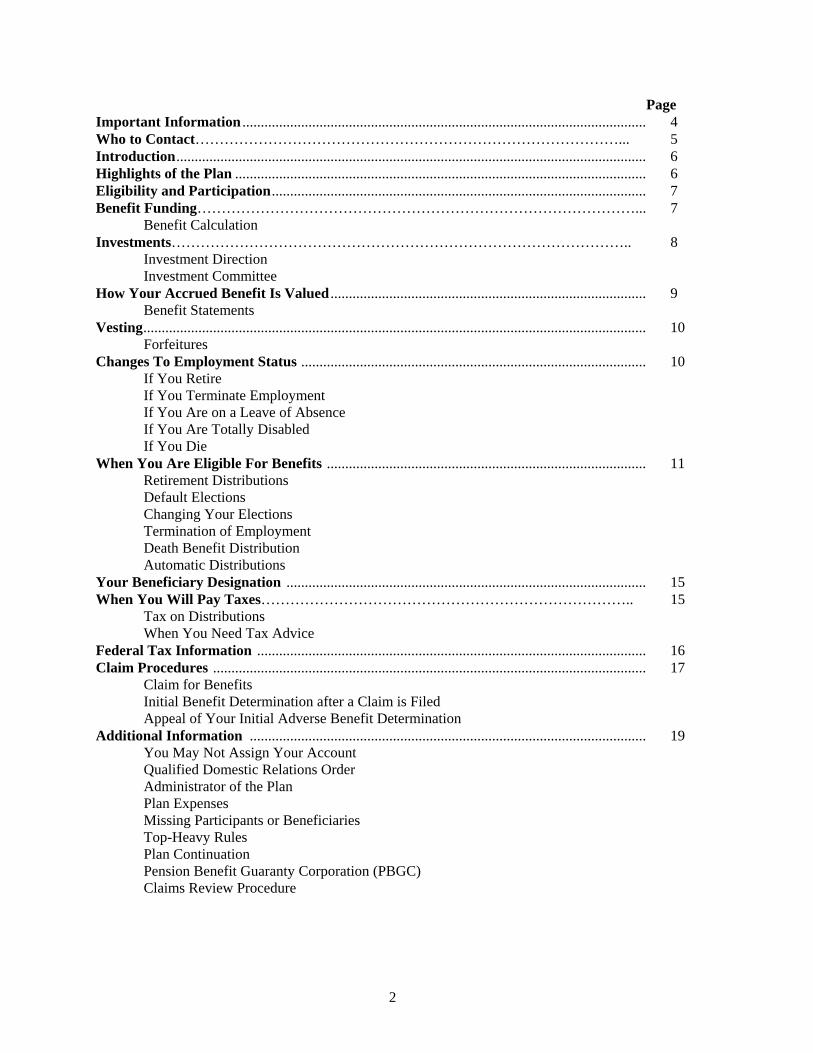

Page Important Information .............................................................................................................. 4 Who to Contact……………………………………………………………………………... 5 Introduction ................................................................................................................................ 6 Highlights of the Plan ................................................................................................................ 6 Eligibility and Participation ...................................................................................................... 7 Benefit Funding………………………………………………………………………………... 7 Benefit Calculation Investments………………………………………………………………………………….. 8 Investment Direction Investment Committee How Your Accrued Benefit Is Valued ...................................................................................... 9 Benefit Statements Vesting ......................................................................................................................................... 10 Forfeitures Changes To Employment Status .............................................................................................. 10 If You Retire If You Terminate Employment If You Are on a Leave of Absence If You Are Totally Disabled If You Die When You Are Eligible For Benefits ....................................................................................... 11 Retirement Distributions Default Elections Changing Your Elections Termination of Employment Death Benefit Distribution Automatic Distributions Your Beneficiary Designation .................................................................................................. 15 When You Will Pay Taxes………………………………………………………………….. 15 Tax on Distributions When You Need Tax Advice Federal Tax Information .......................................................................................................... 16 Claim Procedures ...................................................................................................................... 17 Claim for Benefits Initial Benefit Determination after a Claim is Filed Appeal of Your Initial Adverse Benefit Determination Additional Information ............................................................................................................ 19 You May Not Assign Your Account Qualified Domestic Relations Order Administrator of the Plan Plan Expenses Missing Participants or Beneficiaries Top-Heavy Rules Plan Continuation Pension Benefit Guaranty Corporation (PBGC) Claims Review Procedure

3

ERISA Rights ............................................................................................................................. 21 Receive Information about Your Plan and Benefits Prudent Action by Plan Fiduciaries Enforce Your Rights Assistance with Your Questions

4

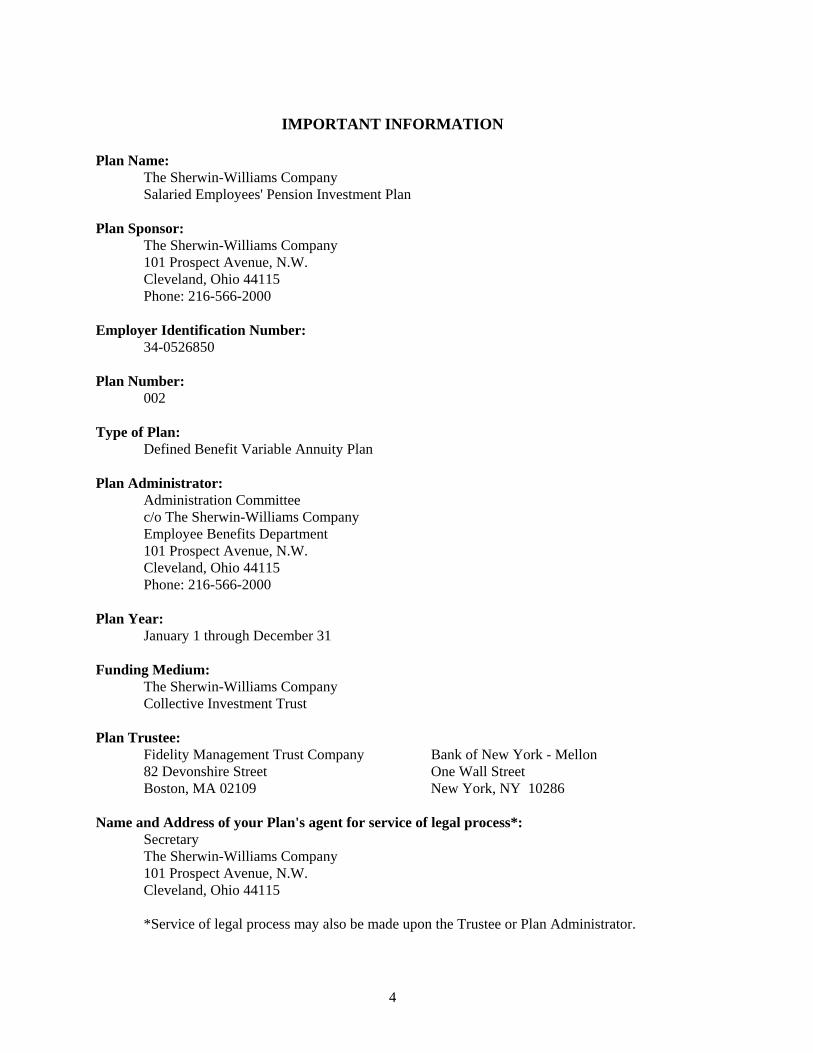

IMPORTANT INFORMATION

Plan Name: The Sherwin-Williams Company Salaried Employees' Pension Investment Plan Plan Sponsor: The Sherwin-Williams Company 101 Prospect Avenue, N.W. Cleveland, Ohio 44115 Phone: 216-566-2000 Employer Identification Number: 34-0526850 Plan Number: 002 Type of Plan: Defined Benefit Variable Annuity Plan Plan Administrator: Administration Committee c/o The Sherwin-Williams Company Employee Benefits Department 101 Prospect Avenue, N.W. Cleveland, Ohio 44115

Phone: 216-566-2000 Plan Year: January 1 through December 31 Funding Medium: The Sherwin-Williams Company Collective Investment Trust Plan Trustee:

Fidelity Management Trust Company Bank of New York - Mellon 82 Devonshire Street One Wall Street Boston, MA 02109 New York, NY 10286

Name and Address of your Plan's agent for service of legal process*: Secretary The Sherwin-Williams Company 101 Prospect Avenue, N.W. Cleveland, Ohio 44115 *Service of legal process may also be made upon the Trustee or Plan Administrator.

5

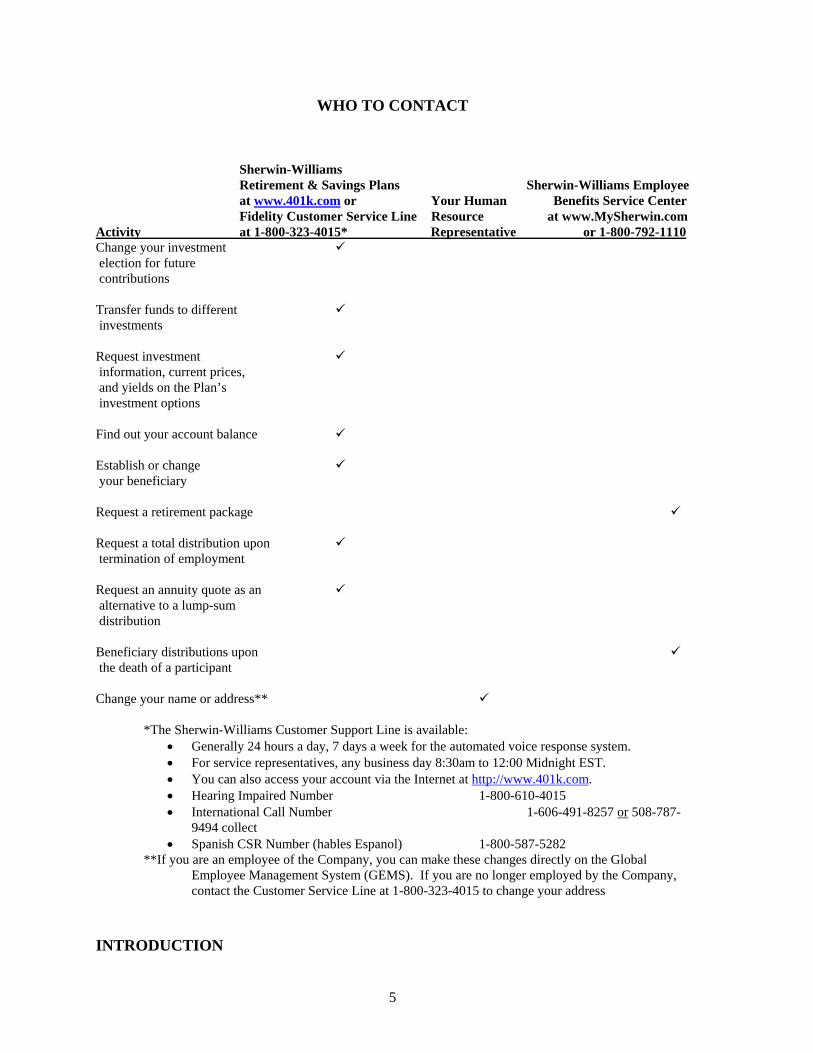

WHO TO CONTACT

Sherwin-Williams Retirement & Savings Plans Sherwin-Williams Employee at www.401k.com or Your Human Benefits Service Center Fidelity Customer Service Line Resource at www.MySherwin.com

Activity at 1-800-323-4015* Representative or 1-800-792-1110 Change your investment election for future contributions Transfer funds to different investments Request investment information, current prices, and yields on the Plan’s investment options Find out your account balance Establish or change your beneficiary Request a retirement package Request a total distribution upon termination of employment Request an annuity quote as an alternative to a lump-sum distribution Beneficiary distributions upon the death of a participant Change your name or address**

*The Sherwin-Williams Customer Support Line is available: Generally 24 hours a day, 7 days a week for the automated voice response system. For service representatives, any business day 8:30am to 12:00 Midnight EST. You can also access your account via the Internet at http://www.401k.com. Hearing Impaired Number 1-800-610-4015 International Call Number 1-606-491-8257 or 508-787-

9494 collect Spanish CSR Number (hables Espanol) 1-800-587-5282

**If you are an employee of the Company, you can make these changes directly on the Global Employee Management System (GEMS). If you are no longer employed by the Company, contact the Customer Service Line at 1-800-323-4015 to change your address

INTRODUCTION

6

Knowing your retirement will be financially secure and comfortable is important to you - - and to The Sherwin-Williams Company (“Company”). To help you reach your long term financial goals, the Company provides The Sherwin-Williams Company Salaried Employees' Pension Investment Plan (the “Plan”). The Plan works together with Social Security and your personal savings (including your 401(k) savings) to provide part of your retirement income. This summary highlights important provisions of the Plan document. Please take time to read it carefully. Keep in mind, however, that this summary does not attempt to cover all details of the Plan. More detailed information is contained in the Plan document, which governs in the event of any discrepancies. You may obtain a copy of the Plan document from the Employee Benefits Service Center at any time. This book summarizes the main features of the Plan effective October 1, 2011, for salaried employees employed by the Company on that date who were hired or rehired by the Company on or after January 1, 2002, and who are not covered by either the Company's Salaried Employees' Revised Pension Investment Plan or the prior Plan formula known as Appendix B after that date. In general, your benefit under the Plan is determined based on a formula that considers your combined age and time with the Company, your creditable earnings and various investment crediting rates that can be selected by you. Benefit details for persons who have separated from covered employment prior to October 1, 2011 may be different. In addition, the Plan provides benefits related to participants under the prior Plan formula, described in a separate summary plan description, and to employees and former employees whose plans have been merged into this Plan (these are determined based on the formula(s) set forth in the applicable acquired plan and are described in separate supplements to this summary plan description).

HIGHLIGHTS OF THE PLAN

Retirement benefits provided under the Plan are entirely funded by the Company. If you are eligible to participate, this Plan provides a retirement benefit when you become vested in your accrued benefit balance and retire or leave the Company for any reason. The Plan also provides a retirement benefit to your spouse or named beneficiary should you die before you retire or leave the Company. You may also select a retirement benefit payment option that in some cases provides continuing payments to your spouse or beneficiary following your death if you die after your payments begin. Plan benefits described in this booklet include:

Pension distribution flexibility in the form of a lump sum amount, or various forms of life annuities that include provisions for your spouse or other

7

beneficiary to receive a benefit, if you die before your spouse or named beneficiary.

A benefit payable to you if you leave the Company before retirement, and are vested in a benefit under the Plan.

The ability to select the allocation of investments on which your accrued benefit balance is determined, based on a variety of money market, fixed income and equity funds.

Daily access to your benefit via the Internet or by telephone. With this access you can get information on your accrued benefit balance, change your investment allocation for new and existing benefits, and request a total distribution from the Plan once you are eligible for such a distribution.

ELIGIBILITY AND PARTICIPATION Effective October 1, 2011, the Plan was frozen to new Participants, rehired employees, and transferred employees. For informational purposes only, the following sets forth the eligibility and participation criteria that were in place before the Plan was frozen.

If you were hired before October 1, 2011 you were eligible to participate in the Plan if:

You were an employee of the Company or a subsidiary of the Company which

had adopted the Plan, You were not a member of a collective bargaining unit unless eligibility for the

Plan was extended to such members through negotiation, You were a citizen of the United States if you were working abroad, under

certain circumstances described in the Plan, or a non-US citizen working in the United States,

You were not an active member of The Sherwin-Williams Company Salaried Employees’ Revised Pension Investment Plan, and

You had completed six (6) months of service.

BENEFIT FUNDING

The Company funds all benefits in this Plan - you do not make any contributions. You are eligible for a Company contribution each year if you meet the eligibility and participation requirements, and you have worked 1,000 hours of Service for the plan year. You may also be eligible for a Company contribution during the year in which you a) are eligible to retire, b) die, or c) cease to meet the eligibility requirements without terminating employment (i.e., change from salaried to a collective bargaining unit or are on an approved leave-of-absence). Contact the Employee Benefits Service Center if you have specific questions about these special circumstances.

8

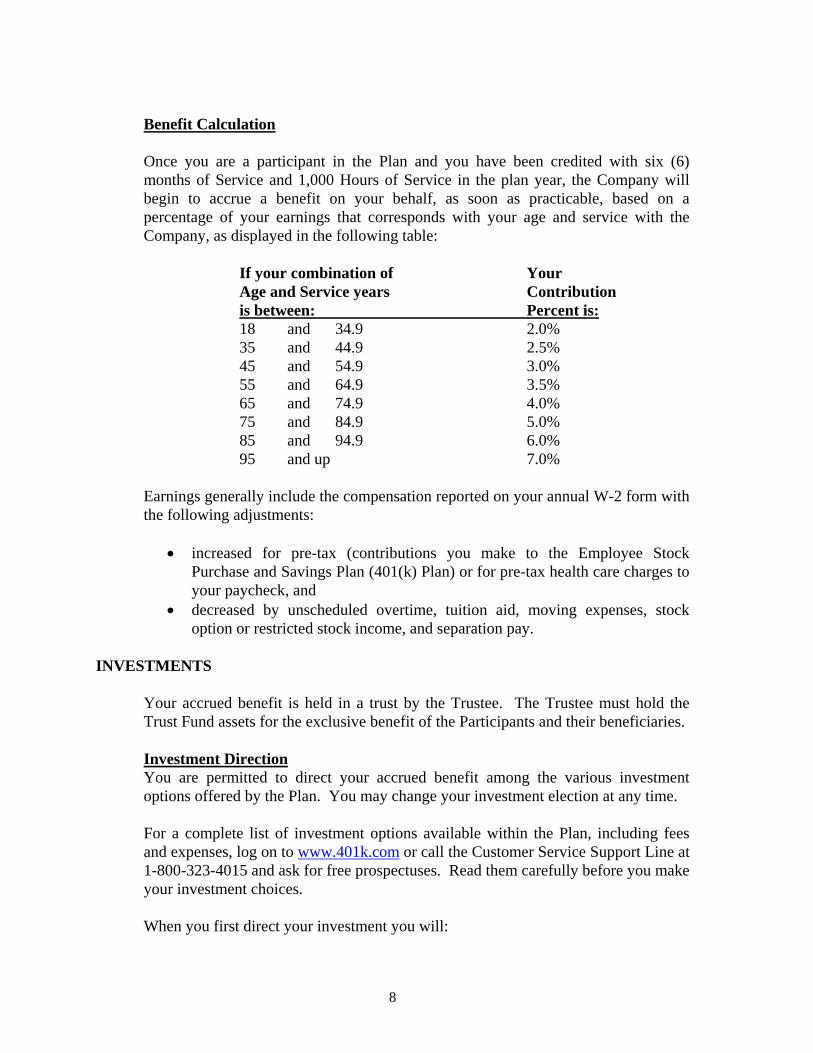

Benefit Calculation

Once you are a participant in the Plan and you have been credited with six (6) months of Service and 1,000 Hours of Service in the plan year, the Company will begin to accrue a benefit on your behalf, as soon as practicable, based on a percentage of your earnings that corresponds with your age and service with the Company, as displayed in the following table:

If your combination of Your Age and Service years Contribution is between: Percent is: 18 and 34.9 2.0% 35 and 44.9 2.5% 45 and 54.9 3.0% 55 and 64.9 3.5% 65 and 74.9 4.0% 75 and 84.9 5.0% 85 and 94.9 6.0% 95 and up 7.0%

Earnings generally include the compensation reported on your annual W-2 form with the following adjustments:

increased for pre-tax (contributions you make to the Employee Stock

Purchase and Savings Plan (401(k) Plan) or for pre-tax health care charges to your paycheck, and

decreased by unscheduled overtime, tuition aid, moving expenses, stock option or restricted stock income, and separation pay.

INVESTMENTS

Your accrued benefit is held in a trust by the Trustee. The Trustee must hold the Trust Fund assets for the exclusive benefit of the Participants and their beneficiaries. Investment Direction You are permitted to direct your accrued benefit among the various investment options offered by the Plan. You may change your investment election at any time. For a complete list of investment options available within the Plan, including fees and expenses, log on to www.401k.com or call the Customer Service Support Line at 1-800-323-4015 and ask for free prospectuses. Read them carefully before you make your investment choices. When you first direct your investment you will:

9

establish a Personal Identification Number (PIN) to be used to access your Account in the future, and

choose how you want to invest your own contributions.

You can direct your investment on a daily basis through the Plan’s Voice Response System, or by speaking directly to a service representative any business day between the hours of 8:30 A.M. and 12:00 Midnight, or by logging on to www.401k.com. Transaction requests received after 4 p.m. Eastern time or on weekends or holidays will receive the next business day’s closing price. If you do not direct your investment, your accrued benefit will be “defaulted”, or automatically invested, in a Fidelity Pyramis Fund that closely matches your retirement date based on a projected retirement age of 65. Sherwin-Williams’ makes no guarantees or assurances regarding the performance of any investment option. The value of your accrued benefit will ultimately be determined by the investment results of the investment fund(s) in which your investment have been invested. Investment Committee The Fund Review and Management Committee select and review the investment options from which you may choose. The members of the Committee are fiduciaries of the Plan.

HOW YOUR ACCRUED BENEFIT IS VALUED

Your accrued benefit is determined at the end of every business day. You can log on to the Company’s retirement plan website at www.401k.com, or call the Customer Service Support Line at 1-800-323-4015 virtually any time - day or night - to obtain the current lump sum value of your accrued benefit balance.

Benefit Statements Statements are always available on line at www.401k.com. If you choose not to access your account through the Internet, you will receive a statement at the end of each quarter showing your balance at the beginning of the quarter, the Account activity for the quarter and an ending balance for the quarter. Your statement will be sent to you within a reasonable time after the close of the quarter.

VESTING

10

Vesting gives you “ownership” of your Plan accrued benefit, which means that your benefits are non-forfeitable and you can take your accrued benefit account with you when you leave the Company. You become vested in your benefits under the Plan when you have completed three years of Service, or if you reach age 65 while still actively employed with the Company, or you die prior to your severance date (with exceptions).

For purposes of vesting, Service means at least 1,000 hours of service for a plan year.

Forfeitures The non-vested portion of your Company benefit will be forfeited after you leave the Company. If you leave the Company, then later become re-employed by the Company, you may be entitled to a reinstatement of the forfeited portion of your accrued benefit account, depending on several factors as outlined in the Plan document. Contact the Employee Benefits Service Center if you have questions relating to re-employment participation, and whether any previous forfeitures are eligible for reinstatement.

Once you meet the eligibility and participation requirements, membership in the Plan is automatic and the Company will mail you a participation package. This package provides you with additional information on the Plan and how to select investment allocations for your accrued benefit balance funded by the Company.

For Participants who terminate employment and are later re-employed, special rules (called “Break in Service Rules”) apply. Contact the Employee Benefits Service Center if you have questions relating to participation upon re-employment.

CHANGES TO EMPLOYMENT STATUS

Your level of participation in the Plan will depend on your employment status.

If You Retire If you retire from the Company, you will elect a benefit option offered by the Plan. Refer to the Retirement Distributions section of this summary plan description for further details.

If You Terminate Employment If you leave the Company for any reason other than retirement, the value of your vested account will automatically be distributed in accordance with the law if the total value is $1,000 or less. Vested account balances above $1,000 will remain in the Plan and will require your consent before your benefit can be paid. If you do not call the Customer Service Support Line at 1-800-323-4015 and request a distribution of your vested accrued benefit balance, you will continue to be a Plan Participant subject to the following:

You will be eligible to change investment accounts,

11

You can request a full distribution of your accrued benefit balance any time, You will be required to take a minimum distribution each year once you

attain age 70 ½, and Your accrued benefit balance will be paid to your named beneficiary should

you die before taking a full distribution.

If You Are on a Leave of Absence If you are on an authorized leave of absence, you will continue to accrue hours of service up to one year of vesting. While you are on leave of absence you cannot request a distribution of your vested accrued benefit balance. However, while you are on a leave of absence you can continue to direct Company contributions and transfer funds among the Plan’s investments.

If You Are Totally Disabled If you are considered totally disabled and you are collecting Long Term Disability (LTD) benefits, you will remain a Participant in the Plan. Totally disabled means you are unable to work at any gainful occupation for which you may be able to perform, or may reasonably become qualified to perform by education, training or experience. If you are considered totally disabled and continue to collect LTD from the Company, or you are still on an approved leave of absence, you will not be eligible for a distribution from the Plan of your accrued benefit balance without stopping all other benefits.

While on leave of absence or LTD you will continue to be a Plan Participant subject to the following:

You will be eligible to change investment accounts. You will be required to take a minimum distribution each year once you

attain age 70 ½. Your accrued benefit balance will be paid to your named beneficiary should

you die before taking a full distribution.

If You Die Please refer to the section titled, Death Benefit Distribution of this Summary Plan Description for payment of death benefits.

WHEN YOU ARE ELIGIBLE FOR BENEFITS

You can begin collecting benefits from the Plan after you terminate from employment with a vested benefit (including retirement after age 65 – Normal Retirement under the Plan), if you become disabled, or if you die.

Retirement Distributions You are eligible to retire from the Company if:

you are 55 through 59 years old, and you have at least 20 years of Service; OR

12

you are 60 years old or older, and the sum of your age and years of Service equal at least 75 (for example: you are 60 years old and you have 15 years of Service, or you are age 62 with 13 years of Service); OR

you are 65 years old (Normal Retirement).

To apply for retirement benefits (if you are eligible), you should contact the Employee Benefits Service Center and request a retirement package. The retirement package will include an “Application For Retirement” form which describes the distribution options that are available. These options are:

One Payment (Lump Sum); OR Variable Annuity (Joint & Survivor or Single Life Annuity)

One Payment:

If you elect the One Payment option, you have two choices of distribution: You can elect a direct rollover of your accrued benefit balance to another

employer retirement plan (or an individual retirement account -- IRA), OR

You can elect to have your accrued benefit balance paid directly to you. Variable Annuity:

Under the variable annuity option, you can select a Joint & Survivor or Single Life Variable Annuity option.

The “variable annuity” option will “vary” regarding the payment amount

each year. The variable annuity will be recalculated and re-established each year by the Plan Administrator. The annuity amount will increase or decrease as a result of several factors including prior-year returns, mortality, and interest rates.

If you elect the Variable Joint & Survivor Annuity option, estimates will

be provided to you as to the amount you (and your spouse) can expect to receive on a monthly basis from the annuity for your lifetimes. The Variable Joint & Survivor Annuity will be based on your accrued benefit balance at the time you retire, and may provide for survivor annuity payments to continue to your surviving spouse after your death in the amount of either 50% or 75% of the amount payable to you prior to your death (the annuity amount being subject to annual recalculation as described above).

Note that you may select a joint annuitant who is not your spouse for

purposes of the 50% option, but only if you are not married when benefit payments start or your spouse has otherwise consented to another beneficiary. If you wish to waive the Joint & Survivor Annuity option and choose one of the other retirement payment options available (and you are married at the time you retire), your spouse must consent to this waiver by signing the “Spouse Consent Statement” on the Application For Retirement

13

form. Your spouse’s signature must be witnessed by a Plan Representative or Notary Public.

If you elect the Variable Single Life Annuity option, you will receive

estimates of the amount that will be paid to you monthly for your lifetime. If you are married at the time of retirement and elect the Variable Single Life Annuity option, the “Spouse Consent Statement” on the Application For Retirement form must be completed and your spouse’s signature must be witnessed by a Plan Representative or Notary Public. As noted previously, your variable annuity can increase or decrease each year based on several factors used in calculating the annuity payment.

Default Elections

Single Participant If you are single and you do not make an election by your annuity starting date your payment option will be defaulted to the Variable Single Life Annuity. Married Participants If you are married and you do not make a payment election at your annuity starting date your payment option will be defaulted to the 50% Variable Joint and Survivor Annuity.

Changing Your Elections Before Retirement

Once you have elected a post-retirement payment option you are free to change your mind and either select another post-retirement option, or completely cancel the option. Remember however, your Spouse's written consent is always required to elect an option other than the post-retirement Joint & Survivor Variable Annuity. After Retirement You MAY NOT change or cancel the type of payment election you make once begin to receive your pension distributions.

Termination of Employment If you terminated your employment from The Sherwin-Williams Company for any reason (other than retirement or death) and you are not on a leave of absence, and you are 100% vested in your Plan benefit, you may call the Plan’s Customer Service Representatives at 1-800-323-4015 to request a full distribution of your accrued benefit balance from the Plan. The payment options described above for retirement are also available to you. To receive a full distribution in a single payment will require you to waive the Single Life Annuity, if you are not married, or the Joint and Survivor Annuity Option of distribution, if you are married, and your spouse will need to consent to this lump sum distribution by signing a distribution form and having his/her signature notarized.

When electing a lump sum distribution, you have two choices of distribution:

14

1. You can elect a direct rollover of a cash distribution to another employer retirement plan or an IRA arrangement. There will be no taxes deducted for this direct rollover, or

2. You can have the distribution paid directly to you. This type of distribution will require a mandatory 20% federal income tax to be deducted before the distribution is paid to you.

Prior to requesting a distribution from the Plan, please read the Federal Tax Information section of this Summary Plan Description.

Death Benefit Distribution If you should die before retirement, your accrued benefit balance will become fully vested and paid to your spouse (if you are married), or to your designated beneficiary(s). Your surviving spouse has the same distribution and/or payment options offered to a retiree. A beneficiary who is not your spouse will receive a single sum payment.

If you officially retire from the Company and later die, it will depend on the retirement option you elected as to whether there is any benefit to be paid to a beneficiary. For example, if you elected to receive the One Payment option, your full benefit will have already been paid out. However, if you selected one of the Variable Annuity options, there may be a continuation payment that will be paid to your joint annuitant.

Your spouse or beneficiary will need to submit to Employee Benefits an original

death certificate prior to the distribution of your accrued benefit balance.

Automatic Distributions If you terminate employment with the Company and your vested account balance is less than $1,000, such balance will be automatically distributed in accordance with the law. If you terminate employment with the Company and your vested benefit is greater than $1,000, you may leave your balance in the Plan until a later time. Notwithstanding the above, the Plan and the Internal Revenue Code provide that a distribution of your benefit must commence no later than April 1 of the year following the year in which you attain age 70 ½.

YOUR BENEFICIARY

It is absolutely essential that you establish one or more beneficiaries to receive your vested accrued benefit in the Plan in the event of your death. If you are married and you do not want to name your spouse as your only beneficiary, your spouse must consent in writing indicating his/her consent to your designating another beneficiary.

15

Your spouse’s signature must be witnessed by a notary public. Log on to www.401k.com, click on the “Your Profile” tab, and then locate the “Beneficiaries” link. Follow the step-by-step instructions to designate your beneficiary. If you do not have internet access, you can call the Customer Service Support Line at 1-800-323-4015 to obtain a beneficiary form.

As events in your life change over time, you can always update your beneficiary form by logging on to www.401k.com or by contacting the Customer Service Support Line at 1-800-323-4015.

WHEN YOU WILL PAY TAXES

Tax on Distributions Your pension is fully taxable as ordinary income when you receive it. If you receive a pension distribution before age 59½, your payout may be subject to an additional 10% penalty tax as well as ordinary income taxes. However, the penalty tax may not apply if your pension is distributed because of

retirement at age 55 or later death, or a qualified domestic relations order.

If you elect a lump sum distribution of your accrued benefit balance, government regulations require that 20% of your distribution be withheld automatically, unless you directly roll over the amount to an IRA or another employer retirement plan. The withheld amount will be applied toward your income taxes for the year in which you receive the distribution. You must provide your written election to the Pension Administration Committee to direct your distribution to be rolled over directly into an IRA (or another employer retirement plan that accepts rollovers) to avoid the 20% withholding. You will not pay taxes until you take the money out of the IRA or other employer retirement plan, at which time you will pay ordinary income tax (and, if applicable, the additional 10% penalty tax for premature distributions) on the money you receive. It should be noted that a rollover may also be made to a Roth IRA, which would mean that you pay ordinary income tax at the time of the rollover but may not owe additional income tax on future earnings. When You Need Tax Advice Because tax laws are complex and subject to change, this information is intended only as a general guideline based on our understanding of the federal income tax law in effect when this booklet was published. For your own protection, you should consult a tax specialist before you receive any Plan money that is subject to tax.

16

FEDERAL TAX INFORMATION

The Plan is intended to be qualified under the Internal Revenue Code of 1986 (the Code), as amended. The related trust is exempt from federal income tax under Section 501(a) of the Code. Contributions made by the Company on behalf of Participants in the Plan are deductible by the Company for federal income tax purposes. Employer Contributions: Company contributions on behalf of a participating employee are not includible in the employee’s gross income, and are not subject to federal income, Social Security or Medicare taxes at the time of contribution.

Plan Earnings: Earnings or appreciation on Company contributions are not subject to federal income tax until such amounts are withdrawn by the employee or are distributed to the employee upon termination of employment, or are distributed to a beneficiary in the event of the employee’s death.

Distribution of Employer (Company) Contributions: Distribution of employer contributions along with earnings and appreciation thereon will be subject to federal income tax as ordinary income and may be subject to additional taxes as described under the section Penalty and Excise Taxes.

Lump Sum Distributions upon Termination of Employment, including Retirement, Total Disability, and Death: The Plan provides that a distribution due to retirement, death, total disability, or other termination of employment may be made in a lump-sum distribution. The amount of the lump-sum distribution equal to the sum of after-tax contributions not previously withdrawn is not subject to federal income tax. The amount of the lump-sum distribution, including earnings and appreciation on company and employee contributions, is subject to federal income tax as ordinary income. However, a qualifying lump-sum distribution may be eligible for special ten-year income averaging (if you were born prior to January 1, 1936) for federal income tax purposes. A lump-sum distribution may be subject to penalty and excise taxes, as described under the section Penalty and Excise Taxes.

Rollover of Distributions: A Participant may defer federal income tax on all or any portion of a withdrawal (other than hardship distributions) or a lump-sum distribution that is rolled over to another employer retirement plan or to an IRA. A rollover can be made (1) by having the Plan trustee transfer all or a portion of the withdrawal or lump-sum distribution directly to another employer retirement plan or to the Participant’s IRA, or (2) by having the Trustee distribute the full amount of a withdrawal or lump-sum distribution to the Participant and the Participant transfers all or a portion of the withdrawal or lump-sum distribution to another employer retirement plan or to the Participant’s IRA within 60 days after the Participant receives the funds. If the Trustee transfers the funds to another employer retirement plan or the Participant’s IRA, the funds transferred are not subject to mandatory 20%

17

federal income tax withholding. However, if the Trustee transfers the funds to the Participant, the transferred funds are subject to mandatory federal income tax withholding. A subsequent distribution from an IRA will be subject to federal income tax as ordinary income and will not qualify for special ten-year income averaging. Generally, the amount of the lump-sum distribution rolled over to another employer retirement plan or IRA will not be subject to excise or penalty taxes, but a subsequent distribution of a rolled over amount from another employer retirement plan or IRA may be subject to excise or penalty taxes, as described under the section Penalty and Excise Taxes. Note, also, that if a rollover is made to the Participant's Roth IRA, income tax will be due at the time of the rollover.

Penalty and Excise Taxes: Unless certain exceptions apply, the taxable portion of any withdrawal, or the taxable portion of a lump-sum distribution that is not rolled over may be subject to a 10% penalty tax if the distribution is made before the Participant attains age 59 ½.

The federal tax information contained in this booklet briefly explains the federal tax aspects of participation in the Plan. The federal tax laws regarding participation in the Plan are extremely complex and no attempt has been made here to deal with the many special provisions that could be applicable to a particular situation or with the rules governing state, local or foreign taxes. Participants should consult their own counsel or other tax advisor to determine the specific tax consequences to them or their beneficiaries.

CLAIM PROCEDURES Claim for Benefits If you believe that you are being denied rights or benefits under the Plan, you may file a claim in writing with the Plan Administrator at:

Administration Committee c/o The Sherwin-Williams Company Employee Benefits Department 101 Prospect Avenue NW, 1300 Midland Cleveland, Ohio 44115

The Administration Committee will notify you of its decision in writing within 90 days after the claim is received (within 180 days if special circumstances require an extension – you will be notified of any extension within the initial 90-day period). Initial Benefit Determination after a Claim is Filed The Administration Committee will have full discretion to deny or grant a claim in whole or part. If your claim for benefits is wholly or partially denied, the Administration Committee will provide to you in writing:

18

specific reasons for the adverse determination; specific reference to the pertinent provision of the Plan document on which

the determination is based; a description of any additional material or information necessary for you to

perfect the claim and an explanation of why the material or information is necessary; and

a description of the plan’s review procedures and the time limits applicable to such procedures, including a statement of the claimant’s right to bring a civil action under section 502(a) of ERISA following an adverse benefit determination on review.

If notice of the adverse benefit determination is not furnished in a timely manner, your claim will be deemed denied and you will be permitted to exercise your of review as described in the paragraph below. Appeal of Your Initial Adverse Benefit Determination If your claim is denied, you may file a written request for review of the adverse determination within 60 days following receipt of an adverse determination. The Administration Committee will appoint a special review committee to review your appeal. If you do not request a review of the adverse determination within the 60-day timeframe, you may not challenge the adverse benefit determination. In making any appeal of an adverse benefits determination, you have the right to:

submit a written request for review by the Administration Committee at: Administration Committee c/o The Sherwin-Williams Company Employee Benefits Department 101 Prospect Avenue NW, 1300 Midland Cleveland, Ohio 44115

review or have reasonable access to or copies of, upon request and free of charge, all Plan documents, records or other information relevant to the your claim for benefits; and

submit any written comments, documents, records or other information relevant to the claim for benefits.

The Administration Committee will notify you of the special review committee’s

determination no later than 60 days after receiving your request for review (within 120 days if an extension is required due to special circumstances – you will be notified of any extension within the initial 60-day period). In the event of an adverse determination, you will be provided with a written explanation that will include the following information:

specific reasons for the adverse determination; specific reference to the pertinent provisions of the Plan document on which

the adverse determination is based;

19

a statement that the Claimant is entitled to receive, upon request and free of charge, reasonable access to, and copies of, all documents, records, and other information relevant to the Claimant’s claim for benefits; and

a statement of the Claimant’s right to bring a civil action under Section 502(a) of ERISA following an adverse determination on review.

If your claim is denied, you may bring legal action in court; provided, however, that you bring such action within one year of the mailing of the adverse benefit appeal determination. You must exhaust any and all administrative procedures set forth under the Plan before seeking relief in a court of law. Except where ERISA applies, the Plan is construed in accordance with the laws of the State of Ohio.

ADDITIONAL INFORMATION

You May Not Assign Your Account The Plan does not permit you or your beneficiary to assign, alienate, sell, transfer, or pledge the benefits under the Plan to a creditor or to anyone else, nor may any person create a lien on any funds, securities or other property held by the Plan. These provisions do not apply, however, in cases of certain qualified domestic relations court orders which create rights to Plan benefits for spouses, former spouses, children or other dependents of participants.

Qualified Domestic Relations Order If, as a result of a divorce, you are responsible for child support, alimony or marital property rights payments, all or part of your savings plan benefits may be assigned to meet these payments if a qualified domestic relations order, which the Plan Administrator determines complies with the terms of the Plan, has been issued by a court. Participants and beneficiaries can obtain, without a charge, copies of such procedures from the Plan Administrator.

Administrator of the Plan The Administration Committee (“Committee”) is the Plan Administrator of the Plan. The Administration Committee acts for the Company in administering the Plan. The Committee has the discretionary authority to interpret and apply the Plan’s provisions in its sole discretion. The Committee delegates the day-to-day Plan administration functions to the Employee Benefits Department. The Plan document, trust agreement and the annual report are available for review by Plan participants or their beneficiaries at the Employee Benefits Department of The Sherwin-Williams Company, 101 Prospect Avenue NW, Cleveland, Ohio 44115 during normal working hours. Upon written request addressed to the Employee Benefits Department, copies of these documents will be furnished, at a reasonable charge, to you as a Plan Participant or your beneficiary.

Plan Expenses

20

All reasonable costs, charges and expenses incurred in connection with the administration of the Plan, including but not limited to the fees of accountants, actuaries, counsel and other specialists and other costs of administration are paid from the Trust Fund, unless the Company elects to make such payments. The Plan Administrator has the discretion to direct payment of any administrative expenses attributable to a Participant’s Account to such Account, including such costs incident to the management of the assets of an investment fund. Missing Participants or Beneficiaries If you leave the employment of the Company, it is your responsibility to advise the Plan Trustee of any changes in your address. Address changes for terminated employees can be made by contacting the Plan’s Customer Service Support line at 1-800-323-4015. Neither the Administration Committee nor the Trustee shall be required to search for or locate a Participant or beneficiary. If you do not apply for benefits within 90 days of normal retirement date, your Account may be forfeited. It will be reinstated if you or your beneficiary request that your benefits be paid out.

Top-Heavy Rules The top-heavy rules impose additional legal restrictions on tax qualified employee benefit plans where more than 60% of the benefits go to “key employee” (certain officers and highly paid employees). If a plan is top-heavy, the special restrictions include provisions of certain minimum benefits and vesting. The Plan, like most other tax qualified employee benefit plans, must contain special top-heavy rules which apply if the Plan is top-heavy. Unless the Plan is top-heavy, the rules have not effect. The Plan is not top-heavy at this time. The Plan Administrator does not expect the Plan will become top-heavy.

Plan Continuation

The Company reserves the right to suspend, reduce, or discontinue contributions at any time in accordance with the Plan document. It may also amend, modify, merge or terminate the Plan. If the Plan terminates, Plan participants will become fully vested as of the date of such termination and you will receive your distribution according to the terms of the Plan

Pension Benefit Guaranty Corporation (PBGC) Your pension benefits under this Plan are insured by the Pension Benefit Guaranty Corporation (PBGC), a federal insurance agency. If the Plan terminates (ends) without enough money to pay all benefits, the PBGC will step in to pay pension benefits. Most people receive all of the pension benefits they would have received under their plan, but some people may lose certain benefits. For more information about the PBGC and the benefits it guarantees, ask your Plan Administrator or contact:

Pension Benefit Guarantee Corp.

21

Technical Assistance Branch 1200 K Street N.W., Suite 930 Washington, D.C. 20005-4026

or call 202-326-4040(not a toll-free number). TTY/TDD users may call the federal relay service toll-free at 1-800-877-8339

and ask to be connected to 202-326-4000. Additional information about the PBGC’s pension insurance program is available through the PBGC’s website on the Internet at http://www.pbgc.gov.

ERISA RIGHTS Receive Information about Your Plan and Benefits

In 1974, Congress passed the Employee Retirement Income Security Act of 1974 (“ERISA”) to safeguard the interests of participants and beneficiaries under employee benefit plans. As a Participant in the Plan, you are entitled to certain rights and protection under ERISA. ERISA provides that all Plan participants shall be entitled to:

examine, without charge, at the Plan Administrator’s office and at other specified locations, such as worksites, all documents governing the Plan and a copy of the latest annual report (Form 5500 Series) filed by the Plan with the U.S. Department of Labor and available at the Public Disclosure Room of the Employee Benefits Security Administration;

obtain copies, upon written request to the Plan Administrator, of all Plan documents governing the operation of the Plan, and copies of the latest annual report (Form 5500 Series) and updated SPD. These copies shall be subject to a reasonable charge;

receive a summary of the Plan’s annual financial report. The Plan Administrator is required by law to furnish each Participant with a copy of this summary annual report; and

receive annually a statement of your vested benefits or the earliest date on which benefits will become vested. This statement must be requested in writing and is not required to be given more than once every 12 months. The Plan must provide the state free of charge;

Prudent Action by Plan Fiduciaries In addition to creating rights for Plan participants, ERISA imposes duties upon the people who are responsible for the operation of the Plan. The people who operate your Plan, called “fiduciaries” of the Plan, have a duty to do so prudently and in the interest of you and other Plan Participants and beneficiaries. No one, including your employer, your union or any other person, may fire you or

22

otherwise discriminate against you in any way to prevent you from obtaining a benefit or exercising your rights under ERISA. Enforce Your Rights If your claim for a benefit is denied in whole or in part, you must receive a written explanation of the reason for the denial, you may obtain copies of documents relating to the decision without charge, and you have the right to have the Plan Administrator review and reconsider your claim, all within certain time schedules. Under ERISA, there are steps you can take to enforce the above rights. For instance, if you request, in writing, a copy of the Plan documents or the latest annual report from the Plan and do not receive it within 30 days, you may file suit in a federal court. In such a case, the court may require the Plan Administrator to provide you with the requested materials and pay you up to $110 a day until you receive such materials, unless materials were not sent because of reasons beyond the control of the Plan Administrator. If you have a claim for benefits that are denied or ignored, in whole or in part, you may file suit in a state or federal court. In addition, if you disagree with the Plan’s decision or lack thereof concerning the qualified status of a domestic relations order, you may file suit in federal court. If it should happen that Plan fiduciaries misuse the Plan’s money or if you are discriminated against for asserting your rights, you may seek assistance from the U.S. Department of Labor or you may file suit in a federal court. The court will decide who should pay court costs and legal fees. If you are successful, the court may order the person you have sued to pay these costs and fees. If you lose, the court may order you to pay these costs and fees; for example, if it finds your claim is frivolous. Assistance with Your Questions If you have any questions about the Plan, you should contact the Plan Administrator. If you have any questions about this statement or about your rights under ERISA, or if you need assistance in obtaining documents from the Plan Administrator, you should contact the nearest office of the Employee Benefits Security Administration, U.S. Department of Labor, listed in your telephone directory or the Division of Technical Assistance and Inquiries, Employee Benefits Security Administration, U.S. Department of Labor, 200 Constitution Avenue N.W., Washington, D.C. 20210. You may also obtain certain publications about your rights and responsibilities under ERISA by calling the publications hotline of the Employee Benefits Security Administration.