The Revised Standardised Approach - World...

32

October 19, 2015 Caio Ferreira The Revised Standardised Approach

Transcript of The Revised Standardised Approach - World...

October 19, 2015

Caio Ferreira

The Revised Standardised

Approach

Regulatory Reform:

2

Basel Committee 2008- 2015

(3Q):

79 Standards

52 Guidelines

15 Sound Practices

40 Implementation reports

37 Others

Capital Framework

3

K

RWACAR =

Basel III

Under

Discussion

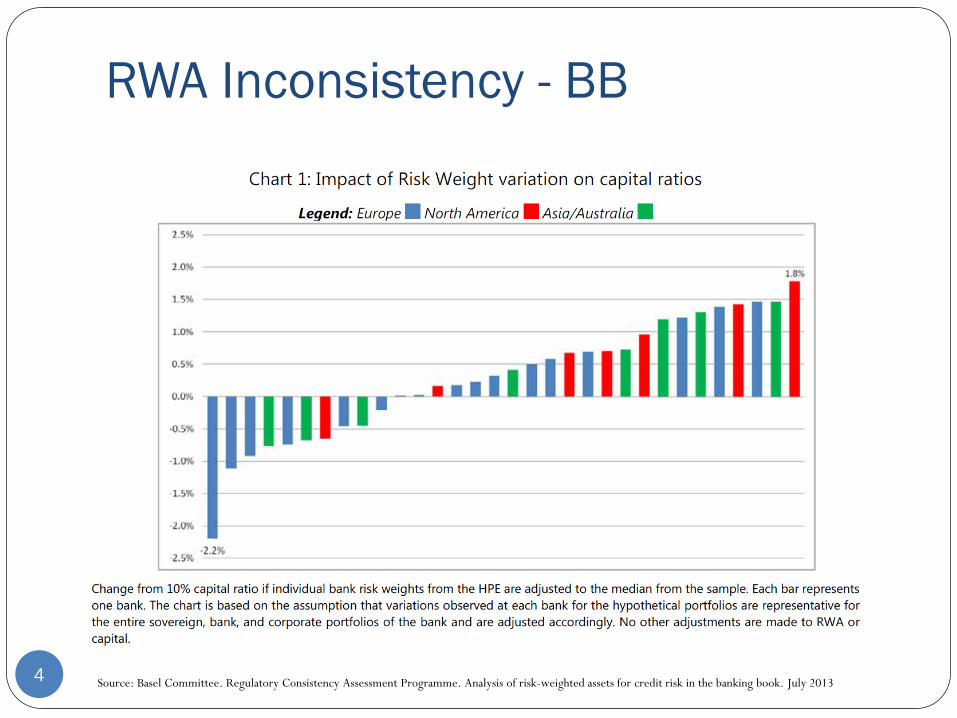

RWA Inconsistency - BB

4 Source: Basel Committee. Regulatory Consistency Assessment Programme. Analysis of risk-weighted assets for credit risk in the banking book. July 2013

RWA Inconsistency - TB

5 Source: Basel Committee. Regulatory Consistency Assessment Programme. Second report on risk-weighted assets for market risk in the trading book.

December 2013

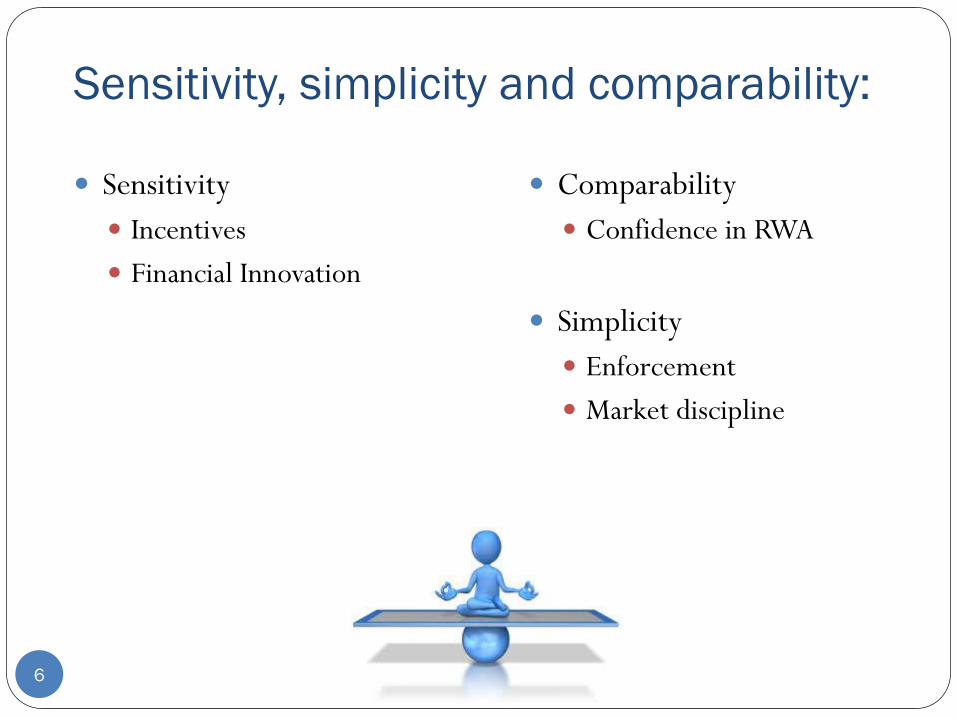

Sensitivity, simplicity and comparability:

6

Comparability

Confidence in RWA

Simplicity

Enforcement

Market discipline

Sensitivity

Incentives

Financial Innovation

RWA Approaches

7

Pillar 1

Charges

Credit risk

Market risk

Operational risk

FAIRB

AIRB

Internal Models Standardized

Cred. Standardized

IMM Market Standardized

BIA

TFSA / ASAAMA

Revisions underway:

8

Why to revised SA?

9

100% RW

Basel I Basel II

0%10%

20%30%

40%

50%80%

100%300%

900%

Risk

Sensitivity

Why to revised SA?

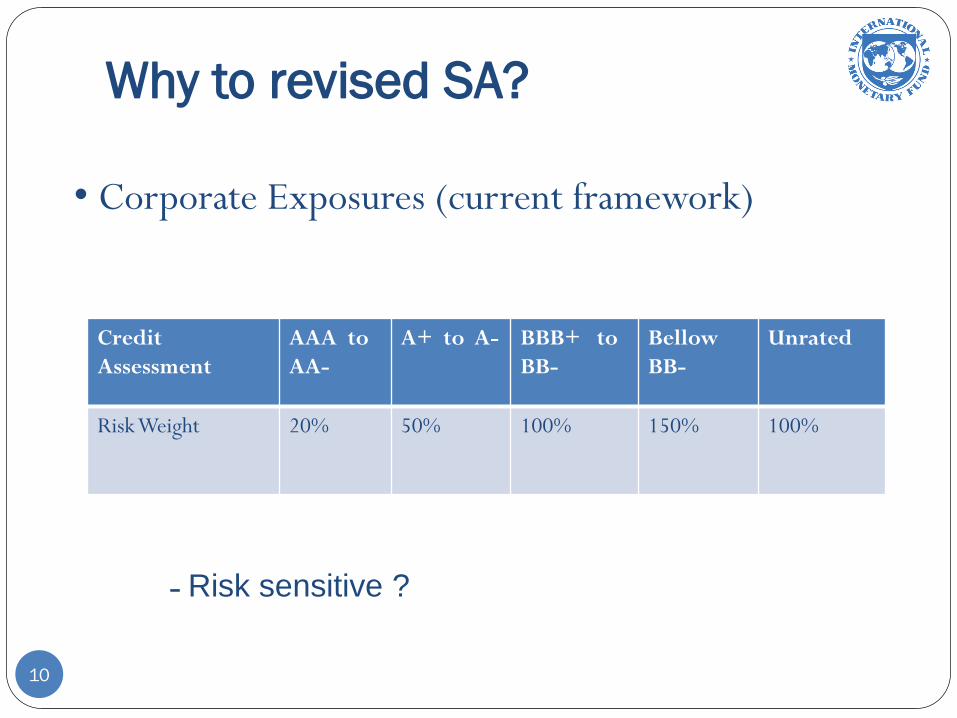

10

Credit

Assessment

AAA to

AA-

A+ to A- BBB+ to

BB-

Bellow

BB-

Unrated

Risk Weight 20% 50% 100% 150% 100%

• Corporate Exposures (current framework)

- Risk sensitive ?

Why to revised SA?

11

• Lack of risk sensitivity

Granularity

Unrated exposures

• Excessive use of ratings

mechanistic reliance

unrated exposures

• Miscalibration Out-of-date

relative terms

• Complexity lack of clarity

number of approaches

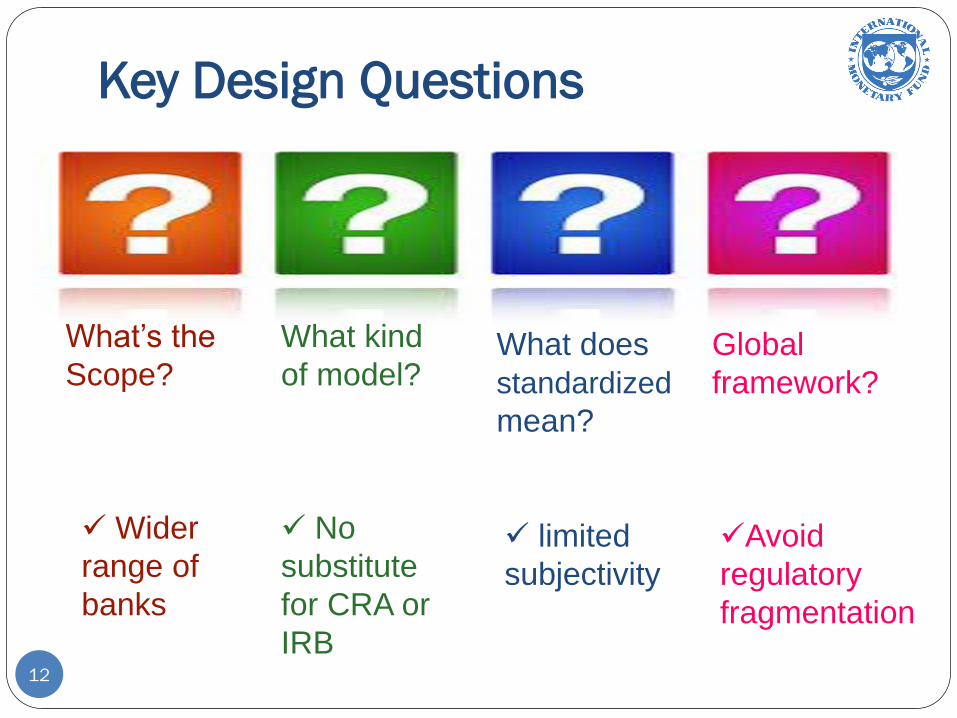

Key Design Questions

12

What’s the

Scope?

What kind

of model?What does

standardized

mean?

Global

framework?

Wider

range of

banks

No

substitute

for CRA or

IRB

limited

subjectivity

Avoid

regulatory

fragmentation

Road Map

13

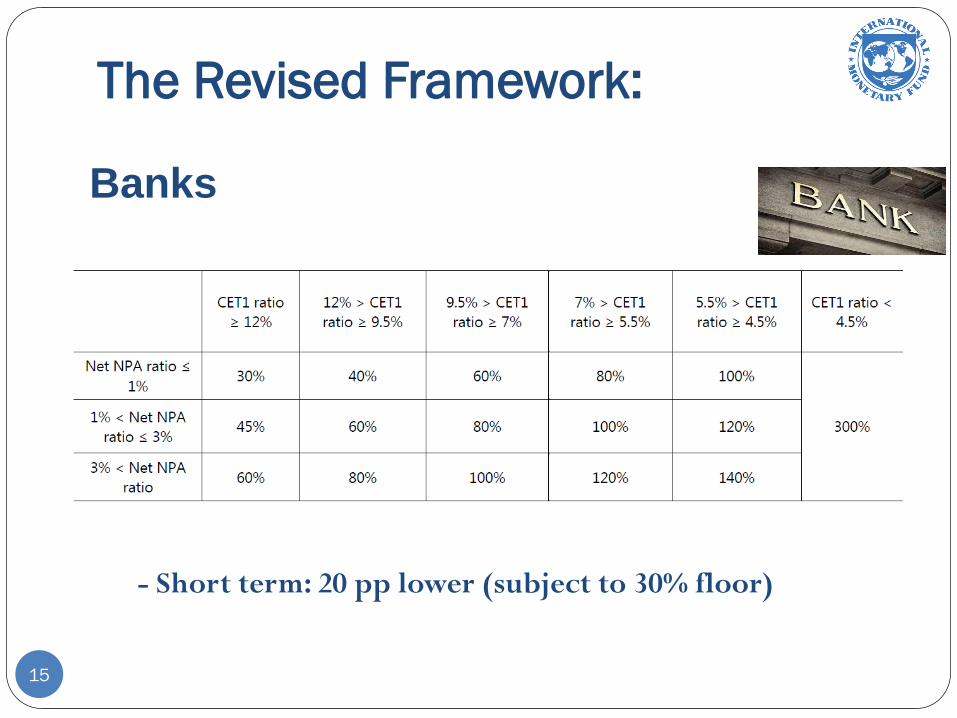

The Revised Framework:

14

• Sovereigns - not in the scope

• PSE – not in the scope

-National discretion: - PSE as sovereign

0% own sovereign

The Revised Framework:

15

Banks

- Short term: 20 pp lower (subject to 30% floor)

The Revised Framework:

16

Banks - Policy Issues

• Investment Banks

• Non Basel III countries

• Country risk

The Revised Framework:

17

Corporates

-Specialised Lending

- PF, OF, CF, IPRE : 120%

- ADC: 150%

- Equity / Subordinated debt : 300% or 400%

The Revised Framework:

18

Corporates - Policy Issues

• Very diverse class- low explanatory power

- risk drivers should be different

• SMEs “penalization”

• Specialized lending too punitive

The Revised Framework:

19

Residencial Real Estate

The Revised Framework:

20

RRE- Policy Issues

• Risk drivers thresholds

• Country specific?

• Pro-ciclicality•Monitoring?

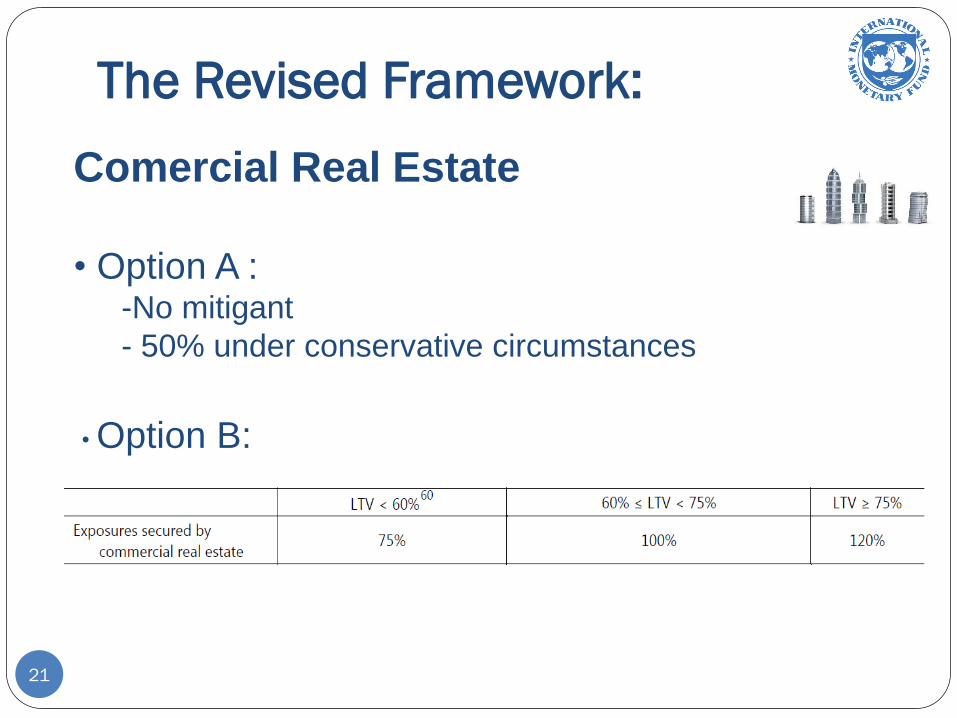

The Revised Framework:

21

Comercial Real Estate

• Option A : -No mitigant

- 50% under conservative circumstances

• Option B:

The Revised Framework:

22

CRE - Policy Issues

• collateral might increase risk weight

The Revised Framework:

23

Retail

• Risk weight 75%- Relevant asset class?

- Appropriate risk drivers?

• Objective Criteria- Exposure size: EUR $ 1 MM

- Diversification: 0,2%

The Revised Framework:

24

OFF Balance Exposures

The Revised Framework:

25

Credit Risk Mitigation

The Revised Framework:

26

Other Policy issues:

• Use of ratings

- No mechanistic reliance

- Limited role ?

• Calibration- current levels ?

The Revised Framework:

27

Country Implications

•Markets are different

• Certainly a lot of room for improvement- risk sensitivity

- economic reality

• Calibration issues

The Revised Framework:

28

Country Implications

• What is the best course of action for

jurisdictions that have not implemented BII?

- Case by case cost benefits analysis

The Revised Framework:

29

Basel II Implementation

Benefits• Better capitalization?

• Risk sensitivity?

• Risk Management?

• Alignment with International Standards ?

Implementation costs• Substantial for Banks and supervisors.

- Particularly for Mkt risk

The Revised Framework:

30

Country Implications

• BIII benefits are more tangible• Stronger definition of capital

• Liquidity requirement

• Macro dimension (buffers / SIBs)

• Most BIII features are independent from BII

• Some may be hard to implement• Need granular information (LCR)

• Institutional development (CCB)

The Revised Framework:

31

Country Implications

If not advanced in the process…• Postpone BII standardized implementation

• Prioritize:

- BIII definition of Capital;

- DSIBs surcharge;

-New PIII disclosure requirements;

Depending on the stage of development- LCR (or a simplified version)

- CCB

- PII surcharges