The revised SGP: room to accommodate growth or structural reforms?

29

The revised SGP: room to The revised SGP: room to accommodate growth or accommodate growth or structural reforms? structural reforms? Catherine Mathieu and Henri Sterdyniak OFCE ETUC Conference, Brussels, 21 March 2006

description

The revised SGP: room to accommodate growth or structural reforms?. Catherine Mathieu and Henri Sterdyniak OFCE. ETUC Conference , Brussels, 21 March 2006. ‘I know very well that the Stability Pact is stupid, like all decisions that are rigid’, Romano Prodi, Le Monde , 18 October 2002. - PowerPoint PPT Presentation

Transcript of The revised SGP: room to accommodate growth or structural reforms?

The revised SGP: room to The revised SGP: room to accommodate growth or accommodate growth or

structural reforms?structural reforms?

Catherine Mathieu and Henri Sterdyniak

OFCE

ETUC Conference, Brussels, 21 March 2006

2

‘I know very well that the Stability Pact is stupid, like all decisions that are rigid’,

Romano Prodi, Le Monde, 18 October 2002.

1. Introduction2. The existing fiscal framework3. The SGP: an assessment 4. Some reform proposals from academics 5. March 2005 Council’s agreement6. The SGP and structural reforms7. The SGP and the NMS8. Our proposal

3

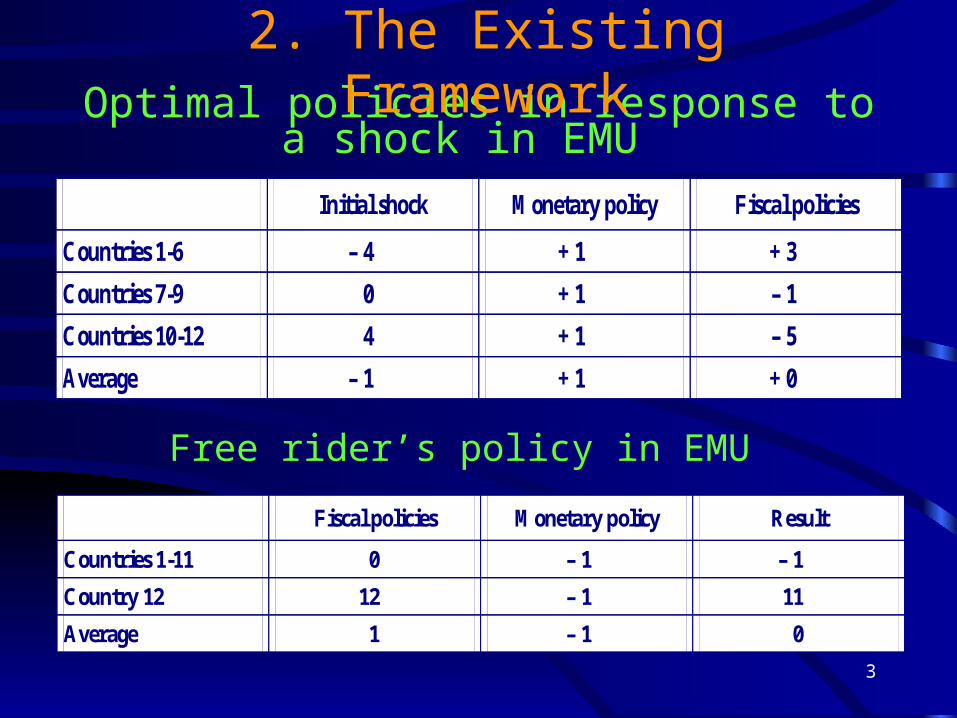

Optimal policies in response to a shock in EMU Initial shock Monetary policy Fiscal policies

Countries 1-6 – 4 + 1 + 3

Countries 7-9 0 + 1 – 1

Countries 10-12 4 + 1 – 5

Average – 1 + 1 + 0

Fiscal policies Monetary policy Result

Countries 1-11 0 – 1 – 1

Country 12 12 – 1 11

Average 1 – 1 0

Free rider’s policy in EMU

2. The Existing Framework

4

Interdependence and coordination

• Interdependence strengthened through: Interest rates, therefore inflation Public debt sustainability Exchange rate, therefore current account

• Choosing a framework

5

2.1. The Institutional Fiscal Framework

The 3% of GDP deficit thresholdSanctions to apply if the threshold is breached.

Debt to GDP ratios below 60%

The Stability and Growth Pact (1997) Stability programmes: 4-year budgetary plans Medium-term objective: budgetary positions ‘close-to-balance or in surplus’.

6

2.1. The Institutional Fiscal Framework: objective?

– Preventing negative externalities

– Economic policy co-ordination

– Setting a common economic policy

2.2. Rationale for the 3% of GDP reference value– Stabilising the debt level at 60% of GDP?

– Share of public investment in GDP?

A country hit by a specific shock may need a higher than 3% of GDP deficit, with monetary policy less reactive to growth and possibly not adequate for this country. No negative spillover effects will occur.

7

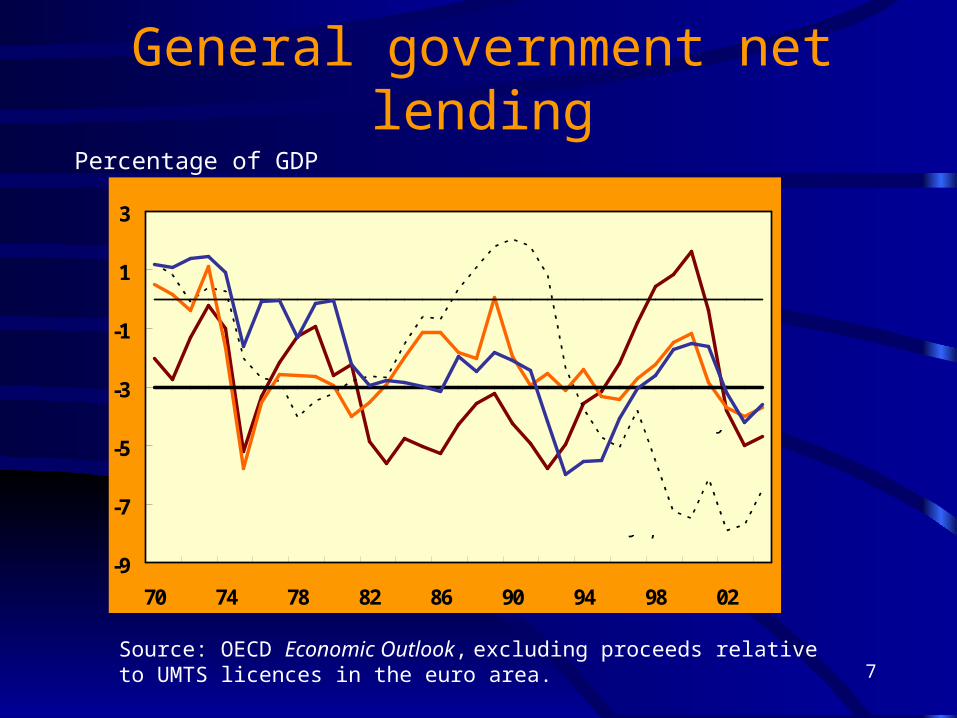

General government net lendingPercentage of GDP

Source: OECD Economic Outlook, excluding proceeds relative to UMTS licences in the euro area.

-9

-7

-5

-3

-1

1

3

70 74 78 82 86 90 94 98 02

USA

Japan

Germany

France

8

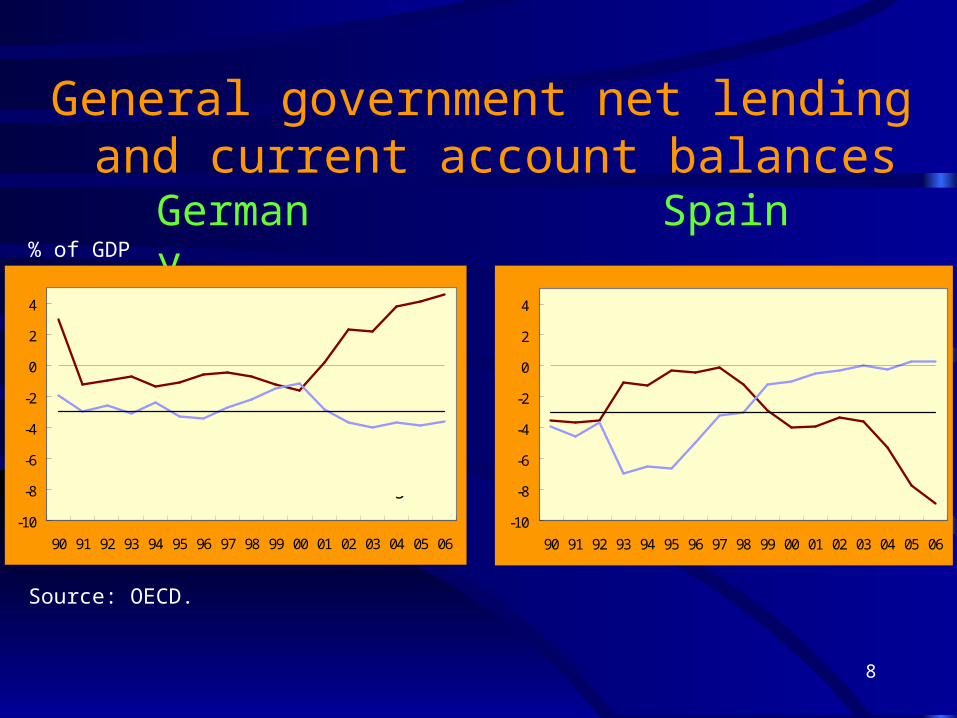

General government net lending and current account balances

% of GDP

Source: OECD.

Germany Spain

-10

-8

-6

-4

-2

0

2

4

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Current account

General Government net lending

-10

-8

-6

-4

-2

0

2

4

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Current account

General Government net lending

9

Interest Rates, GDP Growth and Inflation Forecasts, October 2005

(1) Differential between the short-term interest rate (2 per cent for the EA) and consumer price inflation plus real GDP growth forecasts for 2005/2006 (as of October 2005).(2) Defined as where g: potential output growth, inflation rate and: OECD’s output gap. Sources: Consensus Economics, OECD Economic Outlook, No. 77, June 2005, own calculations.

0.5( 2.0) 0.5( )r g y y ( )y y

GDP

growth, %

Consumer prices, %

Differential

(1) Output

gap

Interest rate target

(2) Germany 0.9 1.9 -0.8 -2.7 1.9 France 1.6 1.8 -1.4 -2.1 2.9 Italy 0.3 2.1 -0.4 -2.0 2.5 Spain 3.3 3.3 -4.5 -0.8 6.4 Netherlands 0.9 1.5 -0.4 -4.0 1.5 Belgium 1.6 2.5 -2.1 -1.5 4.0 Austria 2.0 2.2 -2.2 -2.2 3.6 Finland 2.1 1.3 -1.3 0.1 3.2 Portugal 0.9 2.3 -1.2 -4.4 2.7 Greece 3.3 3.3 -4.6 0.5 7.1 Ireland 4.9 2.4 -5.3 -0.6 7.3 Euro area 1.4 2.1 -1.5 -2.3 3.0

10

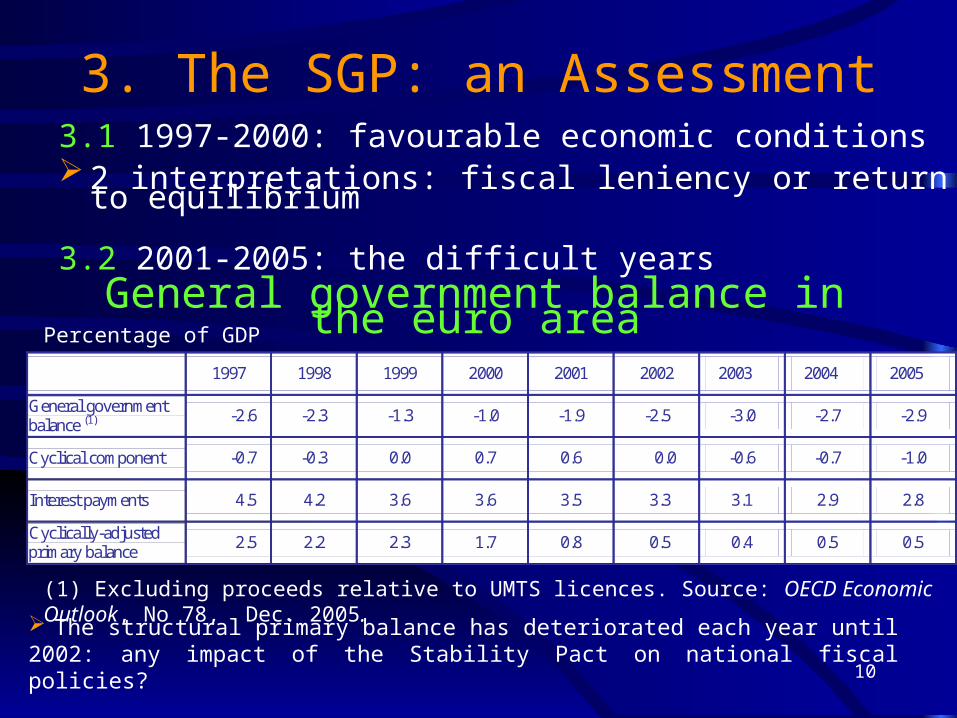

3. The SGP: an Assessment3.1 1997-2000: favourable economic conditions 2 interpretations: fiscal leniency or return to equilibrium

3.2 2001-2005: the difficult years

Percentage of GDP

General government balance in the euro area

The structural primary balance has deteriorated each year until 2002: any impact of the Stability Pact on national fiscal policies?

(1) Excluding proceeds relative to UMTS licences. Source: OECD Economic Outlook, No 78, Dec. 2005.

1997 1998 1999 2000 2001 2002 2003 2004 2005

General government balance (1)

-2.6 -2.3 -1.3 -1.0 -1.9 -2.5 -3.0 -2.7 -2.9

Cyclical component -0.7 -0.3 0.0 0.7 0.6 0.0 -0.6 -0.7 -1.0

Interest payments 4.5 4.2 3.6 3.6 3.5 3.3 3.1 2.9 2.8

Cyclically-adjusted primary balance

2.5 2.2 2.3 1.7 0.8 0.5 0.4 0.5 0.5

11

3. The EDP in practice: 12 countries under an EDPJan. 03: Portugal (01), Germany (02), early warning to France (03)June: France (02)25 November ‘crisis’: Council not endorsing Commission recommendations for France: structural deficit to be cut by 0.8 (instead of 1.0) in 2004 and 0.6 (instead of 0.5) in 2005;Germany: 0.6 (instead of 0.8) and 0.4 (instead of 0.5). Commission bringing an action before the ECJ. Pact held in abeyance

May 04: no early warning on Italy ‘renvoi d’ascenseur’

5 July: 8 new members under the EDP, although 5 (Malta, Poland and Slovakia, Czech Republic and Hungary) being given ‘delays’ due to ‘special circumstances’ (structural adjustment)

13 July: ruling of the ECJ: 25 Nov. Council’s conclusions annulled

Agreement needed between the Commission and Council

12

Structural budget, excluding public investment, should be permanently at least in balance.

Correct interpretation of the golden rule: the cyclically-adjusted borrowing, net of net public investment and of debt depreciation should be at least in balance.

Measurement difficulties.

The rule defines the neutrality of fiscal policy, cyclical neutrality (only automatic stabilisers are allowed to work) and structural neutrality (public savings equals public investment). But a government may choose not to be neutral.

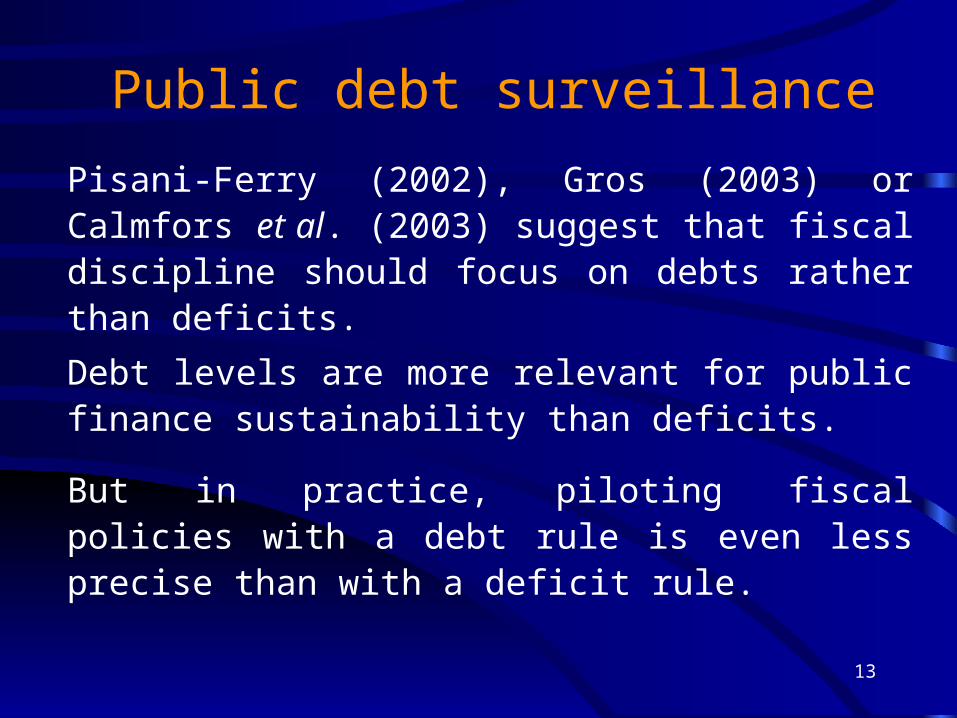

4. Some proposals by academicsThe golden rule for public finances

13

Pisani-Ferry (2002), Gros (2003) or Calmfors et al. (2003) suggest that fiscal discipline should focus on debts rather than deficits.

Debt levels are more relevant for public finance sustainability than deficits.

But in practice, piloting fiscal policies with a debt rule is even less precise than with a deficit rule.

Public debt surveillance

14

SGP remains essential

Nothing said on the reasons why the SGP did not work

3% and 60% remain the centrepiece of multilateral surveillance

Improving governance

MS to implement the policy of their choice within the limits of the Treaty

Commission guardian of the Treaty

- Showing continuity with former governments’ budgetary targets

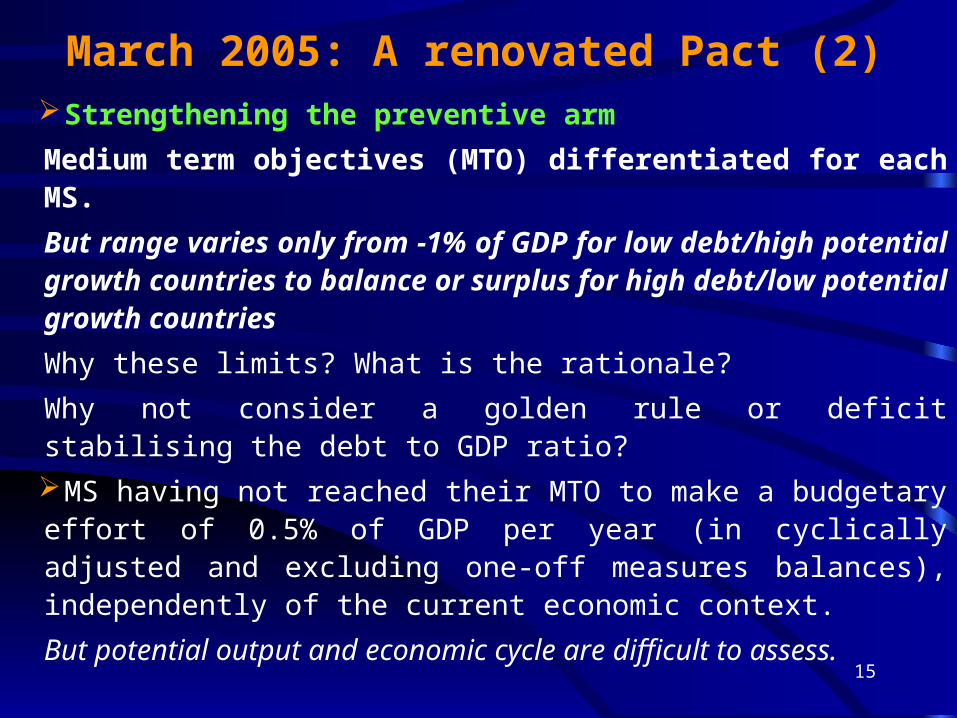

March 2005: A renovated Pact

15

Strengthening the preventive arm

Medium term objectives (MTO) differentiated for each MS.

But range varies only from -1% of GDP for low debt/high potential growth countries to balance or surplus for high debt/low potential growth countries

Why these limits? What is the rationale?

Why not consider a golden rule or deficit stabilising the debt to GDP ratio?

MS having not reached their MTO to make a budgetary effort of 0.5% of GDP per year (in cyclically adjusted and excluding one-off measures balances), independently of the current economic context.

But potential output and economic cycle are difficult to assess.

March 2005: A renovated Pact (2)

16

Commission’s report if deficit exceeds 3%; Small and temporary breaching allowed if due to negative growth or strong negative output gap.

Proposals made by France, Germany and Italy to automatically withdraw some categories of expenditure not accepted. But the Commission’s report will account for ‘all other relevant factors’: policies implemented in line with the Lisbon agenda, R&D spending, public investment, economic situation or debt sustainability, efforts for international solidarity, European goals or European unification, costs of the introduction of a compulsory, fully funded pension pillar. These elements may prevent the launch of an EDP, and could also allow for longer adjustment paths to bringing deficits below 3%.

The Council will take account of the speed of reduction in the debt to GDP ratio, for countries where they are above 60% of GDP.

March 2005: Improving the implementation of the EDP

17

Ageing of populations

Structural reforms, esp. pension reforms introducing a mandatory, fully funded pillar, will be taken into account if they raise potential growth and induce long-term savings in the long run. These elements may prevent the launch of an EDP, and could also allow for longer adjustment paths to bringing deficits below 3%.

But the design of the Social Security system is a national choice and there is no justification for a European rule to provide incentives for a fully funded system.

Implicit liabilities from ageing populations to be taken into account, but why not take account of social contributions people would be willing to pay?

How will the Commission address pensioner poverty risks in countries with low public pensions?

A Renovated Pact and structural reforms

18

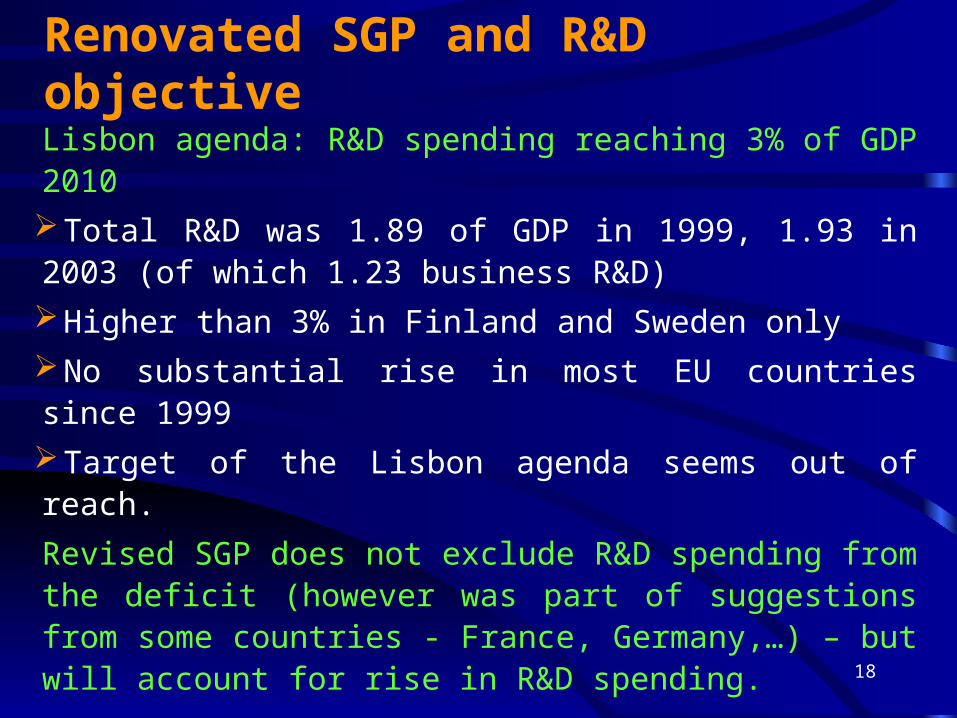

Lisbon agenda: R&D spending reaching 3% of GDP 2010

Total R&D was 1.89 of GDP in 1999, 1.93 in 2003 (of which 1.23 business R&D)

Higher than 3% in Finland and Sweden only

No substantial rise in most EU countries since 1999

Target of the Lisbon agenda seems out of reach.

Revised SGP does not exclude R&D spending from the deficit (however was part of suggestions from some countries - France, Germany,…) – but will account for rise in R&D spending.

Renovated SGP and R&D objective

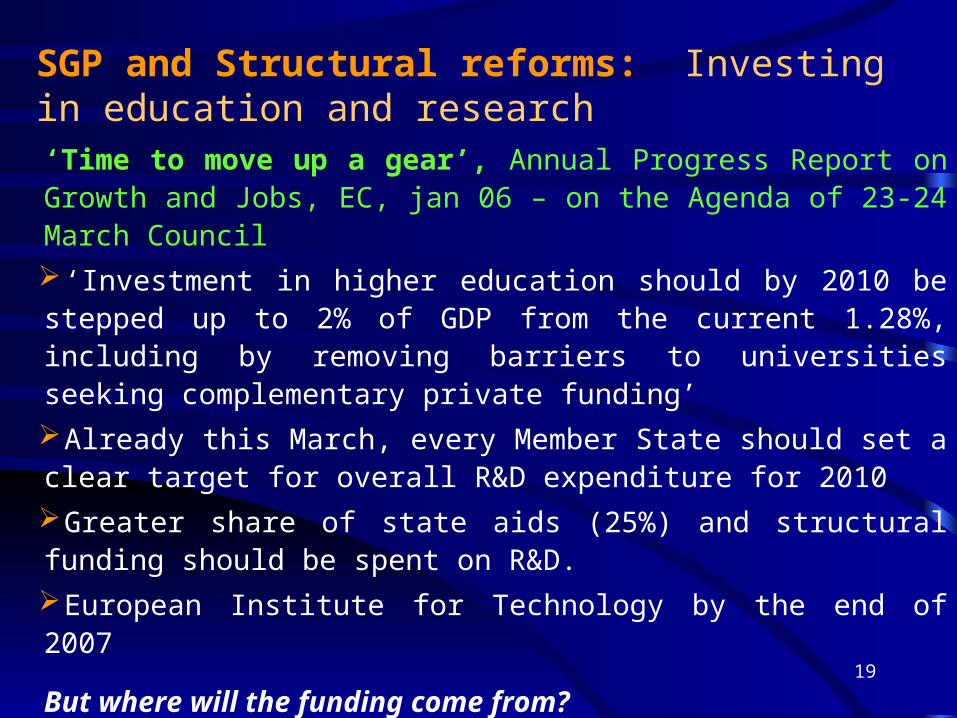

19

‘Time to move up a gear’, Annual Progress Report on Growth and Jobs, EC, jan 06 – on the Agenda of 23-24 March Council

‘Investment in higher education should by 2010 be stepped up to 2% of GDP from the current 1.28%, including by removing barriers to universities seeking complementary private funding’

Already this March, every Member State should set a clear target for overall R&D expenditure for 2010

Greater share of state aids (25%) and structural funding should be spent on R&D.

European Institute for Technology by the end of 2007

But where will the funding come from?

SGP and Structural reforms: Investing in education and research

20

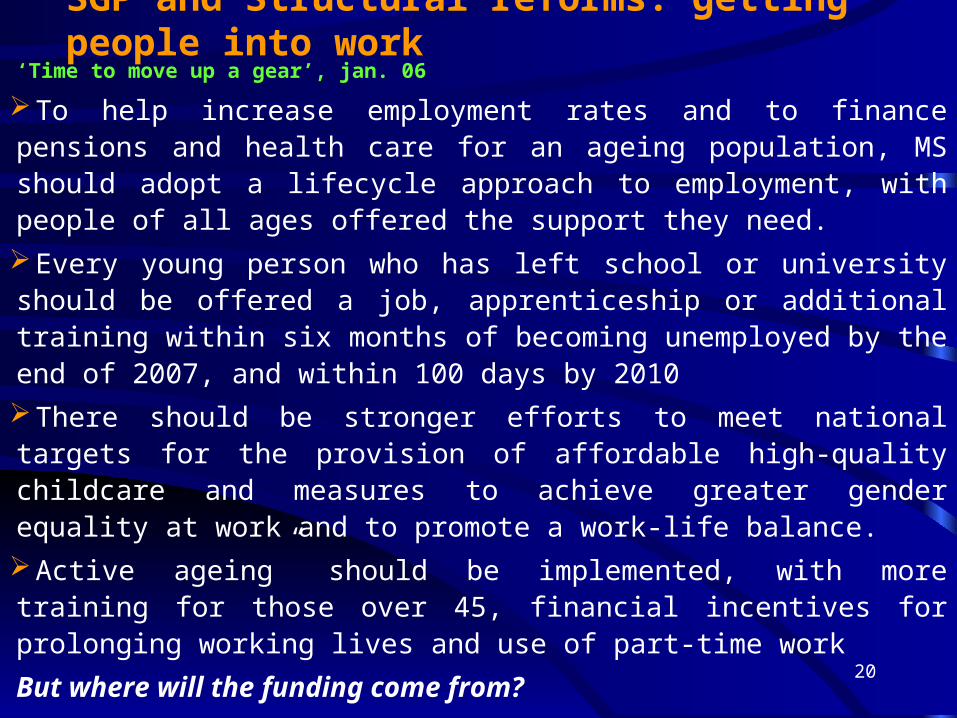

‘Time to move up a gear’, jan. 06

To help increase employment rates and to finance pensions and health care for an ageing population, MS should adopt a lifecycle approach to employment, with people of all ages offered the support they need.

Every young person who has left school or university should be offered a job, apprenticeship or additional training within six months of becoming unemployed by the end of 2007, and within 100 days by 2010

There should be stronger efforts to meet national targets for the provision of affordable high-quality childcare and measures to achieve greater gender equality at work and to promote a work-life balance.

Active ageing” should be implemented, with more training for those over 45, financial incentives for prolonging working lives and use of part-time work

But where will the funding come from?

SGP and Structural reforms: getting people into work

21

Reducing social benefits or job protection may increase social insecurity which will translate into higher saving rates and social tensions.

In a mass unemployment situation, it is difficult to induce young, low-skilled and senior people to work more.

Higher growth would allow for lower social contributions rates, without reducing social benefits.

Higher growth would allow for more job flexibility and would facilitate the rise the participation rate of young, female and senior workers.

Priority should be a growth-oriented policy mix.

SGP and the renewed Lisbon agenda, 2005: vicious and virtuous circles

22

The share of profit/VA has risen rapidly in recent past

The danger is not currently in too rapid wage increases but in high profits, not invested in the EU but saved or invested outside the EU.

Europe needs higher wages to support consumption, which will reduce unemployment and rise growth.

There is a need for coordinating wage bargaining in the EU in order to avoid social dumping.

SGP and the renewed Lisbon agenda, 2005: labour markets reforms

23

Public investment has declined as a share of GDP in a number of EU-12 countries

Germany (2.7% of GDP in 1991, 1.4 in 2004), Italy (3.2/2.6), France (3.6/3.3), Austria (3.1/1.2)

With the SGP rule: risk of public investment becoming too weak

While the golden rule has allowed UK public investment to rise from 1.3 in 1997 to 1.8 in 2004.

SGP and Structural reforms

24

Some facts in the current SGP debate

Deficits have not generated negative externalities and macroeconomic unbalances in the euro area:Public deficit at 2.7% of GDP in 2004, with CAPB surplus of 0.5% Current account: surplus of 0.2% of GDP expected for 2005Inflation: close to 2% Real long-term interest rates: 1.2%, slightly below real GDP growthAny effect of the SGP rules being breached by a growing number of members? No reaction of financial markets: no rise in interest rates no fall in the exchange rate of the euro

25

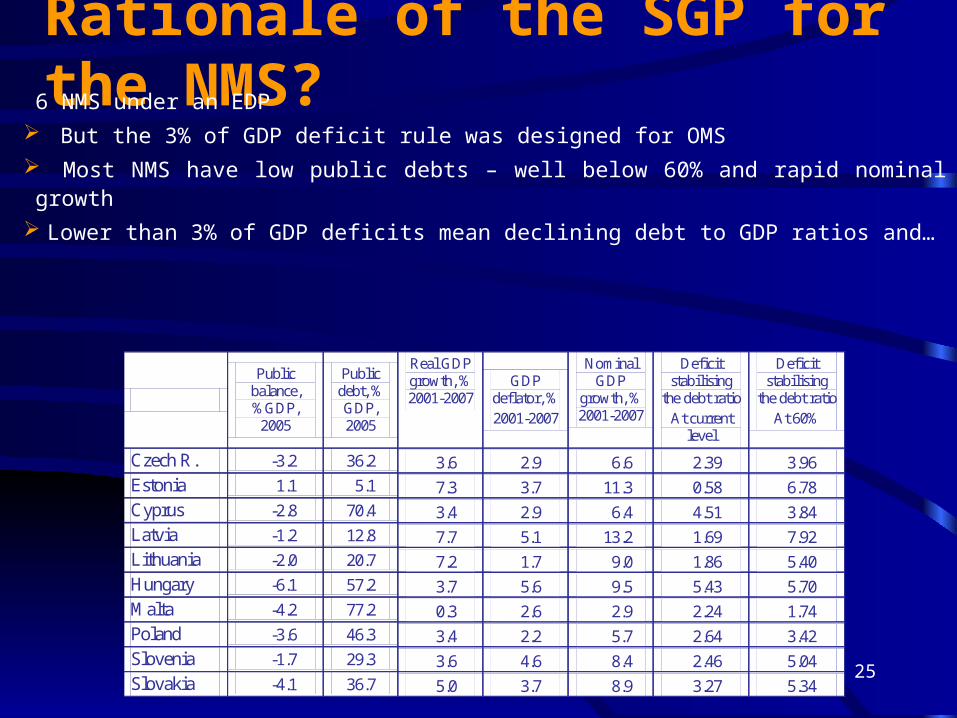

Rationale of the SGP for the NMS? 6 NMS under an EDP

But the 3% of GDP deficit rule was designed for OMS

Most NMS have low public debts – well below 60% and rapid nominal growth

Lower than 3% of GDP deficits mean declining debt to GDP ratios and…

Public balance, %GDP,

2005

Public debt, % GDP, 2005

Real GDP growth, % 2001-2007

GDP deflator, % 2001-2007

Nominal GDP

growth, % 2001-2007

Deficit stabilising

the debt ratio At current

level

Deficit stabilising

the debt ratio At 60%

Czech R. -3.2 36.2 3.6 2.9 6.6 2.39 3.96

Estonia 1.1 5.1 7.3 3.7 11.3 0.58 6.78

Cyprus -2.8 70.4 3.4 2.9 6.4 4.51 3.84

Latvia -1.2 12.8 7.7 5.1 13.2 1.69 7.92 Lithuania -2.0 20.7 7.2 1.7 9.0 1.86 5.40

Hungary -6.1 57.2 3.7 5.6 9.5 5.43 5.70

Malta -4.2 77.2 0.3 2.6 2.9 2.24 1.74

Poland -3.6 46.3 3.4 2.2 5.7 2.64 3.42

Slovenia -1.7 29.3 3.6 4.6 8.4 2.46 5.04

Slovakia -4.1 36.7 5.0 3.7 8.9 3.27 5.34

26

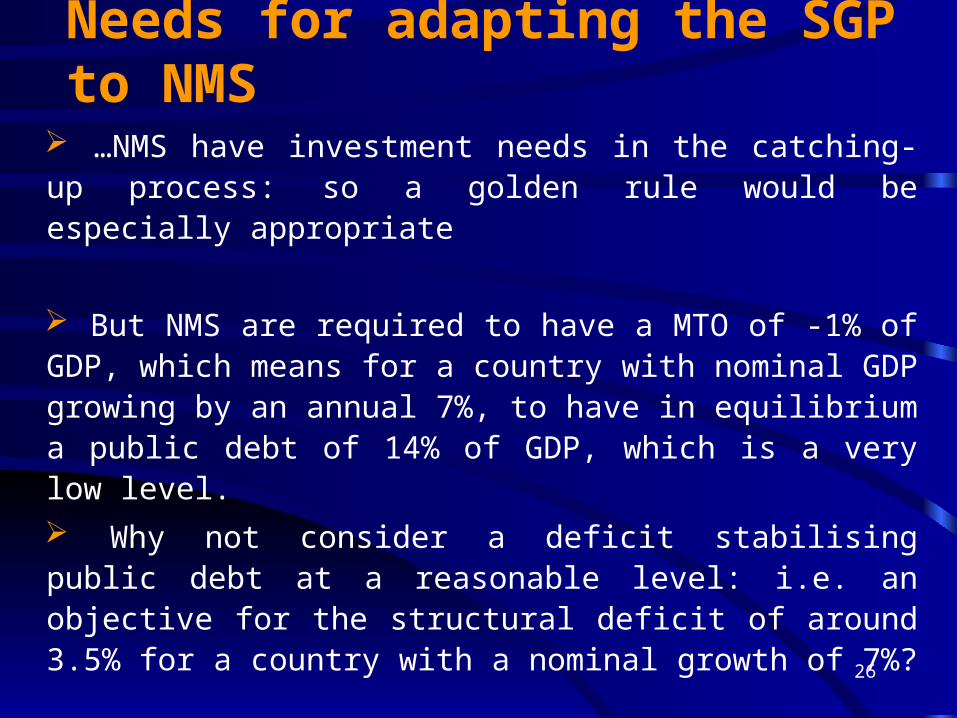

…NMS have investment needs in the catching-up process: so a golden rule would be especially appropriate

But NMS are required to have a MTO of -1% of GDP, which means for a country with nominal GDP growing by an annual 7%, to have in equilibrium a public debt of 14% of GDP, which is a very low level.

Why not consider a deficit stabilising public debt at a reasonable level: i.e. an objective for the structural deficit of around 3.5% for a country with a nominal growth of 7%?

Needs for adapting the SGP to NMS

27

Each country should be allowed to define its fiscal policy as long as it does not affect the macroeconomic equilibrium of the area, i.e as long as its inflation stays in line with the inflation target of the area. With an area inflation target set within 1.5 to 3.5%, ‘Northern’ countries would be given a target within 1 to 3%, countries in a catching-up process a target within 2 to 4%.

A country hit by a negative demand shock would be able to counterbalance it through temporary fiscal policy loosening. A country hit by a supply shock (inflationary pressures) would have to tighten its fiscal policy.

Our proposal

28

The Commission and the Ecofin council would

check that domestic inflation targets are fulfilled and

would possibly agree on deviations and delays for

common or asymmetric supply shocks.

They would also check the level of domestic public

debt does not endanger public finance sustainability

or that domestic current account deficits do not

depart too strongly from the aggregate level.

Avoiding externalities

29

Conclusions Lack of consensus in Europe on macroeconomic strategy: structural

reforms and fiscal consolidation versus active macroeconomic policies.

Close to balance budgetary positions should not be the main objective of the fiscal framework.

Each country could target the golden rule for public finances as a Medium Term Objective.

A surveillance based on true negative externalities would oblige the Council and the Commission to link fiscal policies and macroeconomic unbalances, which is not currently the case.

It would be desirable to set up real economic policy coordination in the framework of the Eurogroup, with whom the ECB would dialogue. This co-ordination should not focus on public finance balances, but should aim at supporting economic activity and achieving the 3% annual growth target of the Lisbon strategy