The Real Estate development Process - Daniel...

20

DRAFT FOR DISCUSSION AND COMMENT Page 1 of 20 The Real Estate Development Process: Is This A Value Creation Chain? The Potomac Yard Example Presented at, 2007 American Real Estate Society Annual Meeting San Francisco, California Presented by, Daniel B. Kohlhepp, Ph.D. President, Commercial Division Crescent Resources, LLC April 12, 2007

Transcript of The Real Estate development Process - Daniel...

DRAFT FOR DISCUSSION AND COMMENT

Page 1 of 20

The Real Estate Development Process:

Is This A Value Creation Chain?

The Potomac Yard Example

Presented at,

2007 American Real Estate Society Annual Meeting

San Francisco, California

Presented by,

Daniel B. Kohlhepp, Ph.D.

President, Commercial Division

Crescent Resources, LLC

April 12, 2007

DRAFT FOR DISCUSSION AND COMMENT

Page 2 of 20

The Real Estate Development Process:

Is This A Value Creation Chain?

The Potomac Yard Example

I. PERSONAL INTODUCTION

In 1973, Ohio State University Professor Ronald L. Racster invited University of

Wisconsin Professor James A. Grasskamp to Columbus, Ohio to address a group of real

estate practitioners about land development. Dr. Racster assigned me, his eager graduate

student, to be Dr. Graaskamp’s personal assistant for the day. I was unprepared for Dr

Graaskamp’s physical condition and totally unprepared for his presentation on land

development. His explanation of the land development process was a watershed day for

me, and his critical thinking about the stages of the process, the tasks involved, and the

skills required in each stage became an integral part of my real estate self-identity.

Through several panel discussions like this one, I became friends with Jim, and, in the

process, I became even more respectful of his critical thinking and its influence on my

future career. I have lost my notes from his lecture, but I think of him every day as I

thrash through the stages of land development and deal with the risks and returns on a

real-time basis. The real estate development process described in this paper is based on

Dr. Graaskamp’s lecture 33 years ago, but I have never been able to find an adequate

citation for his work in this area. Perhaps, my friends at ARES can help me with an

appropriate citation and recognition.

This paper addresses the questions: 1. Is the real estate development process a value

creation chain? And 2. If so, can the value creation be measured and observed in the

marketplace? This paper will focus on the Land Packaging, Land Development,

Building Development, and Building Operations stages of the development process. The

Potomac Yard Development, a mixed-use, urban-infill development in Northern Virginia

that Crescent Resources, LLC just completed, is used as an example to demonstrate the

real estate development process and the value created by it.

DRAFT FOR DISCUSSION AND COMMENT

Page 3 of 20

II. THE REAL ESTATE DEVELOPMENT PROCESS (a la Grasskamp)

Real estate development is a seven-stage process. Each stage has specific tasks which

require specific skills, and each stage has specific risks that must be accepted,

conditioned, reduced, or eliminated. Finally, each stage has profit opportunities that can

be captured. Participants and investors in the real estate development must be cognizant

of the characteristics of the stage or stages of development in which they participate.1

Failure to understand this process can lead to “getting in too early” or “getting out too

late” which, of course, leads to financial frustration and sometimes ruin

The seven stages in the real estate development process are listed below and presented

schematically in Figure 1.

DRAFT FOR DISCUSSION AND COMMENT

Page 4 of 20

Land Banking Stage

Sell? Stop YES

NO

Operating Stage

Sell? Stop YES

NO

Land Packaging Stage

Sell? Stop YES

NO

Building Development

Stage

Sell? Stop YES

NO

Land Development Stage

Sell? Stop YES

NO

Renovation Stage

Sell? Stop YES

NO

Redevelopment Stage

Sell? Stop YES

NO

DRAFT FOR DISCUSSION AND COMMENT

Page 5 of 20

1. Land Banking Stage: The “Land Banker” waits for general market forces to increase

the value of the land. This is a relatively passive investment position. The land banker

then sells the land to a “land packager.”

2. Land Packaging Stage: The “Land Packager” buys the raw land from the passive land

banker and then improves the value of the land through conceptual land planning, zoning

changes, financing schemes, or other “paper enhancements” like title insurance, accurate

surveys, or environmental studies. The packaged land is then sold to the “land

developer.”

3. Land Development Stage: The “Land Developer” buys the land with the paper

enhancements from the land packager and then improves the land so it can be sold as

finished building pads to the building developer. This usually involves the construction

of horizontal infrastructure such as roads and utilities as well as common improvements

such as water detention and recreational facilities.

4. Building Development Stage: The “Building Developer” buys the finished pad from

the land development and then does the vertical development by constructing the building

improvement. During construction, the building developer may also attempt to lease the

building so the finished building can be sold to the building operator.

5. Operating Stage: The “Building Operator” leases up the property, manages the

property, and develops a building operating history so it can be sold to other building

operators during its economic life or sold to a building renovator at the end of its

economic life.

6. Renovation Stage: The “Building Renovator” buys the property with substantial

economic and physical depreciation and creates value by curing these deficiencies and

continues to operate the building until the property is ready for redevelopment.

7. Redevelopment Stage: The “Building Re-developer” buys the property with such

serious physical or physical deficiencies that the building must be torn down or re-

developed for another use. This essentially begins the real estate development process all

over again.

The next sections of the paper will focus on the Land Packaging, Land Development,

Building Development, and Building Operations stages and will address the questions:

(1.) what is a value creation chain and

(2.) when or how does the real estate development process become a value

creation chain.

DRAFT FOR DISCUSSION AND COMMENT

Page 6 of 20

III. REAL ESTATE VALUE CHAIN (a la Roulac)

“The chain of property distribution traces those functions, tasks, and activities involved in

the conversion of land through planning and design processes, the manufacture via

building of physical forms and legal processes of property interests, through the

marketing and merchandising of physical forms and property interests. The producers

and providers of property goods and services elect business models which achieve

varying levels of prices in the resource markets and investment returns in the capital

markets.”2

“Value-added is the result of such unique contributions as:

1. perceiving an opportunity that others do not,

2. changing the use of a property, so that the new use has a value greater than costs

incurred in making the change,

3. doing what others say cannot be done,

4. doing what others are unwilling to do, and

5. taking on financial risks to make or guarantee payments in case others do not

perform and/or the project is unsuccessful.”3

“Real estate development services that can be put into five categories:

1. Creativity/ingenuity,

2. Reward for risk,

3. Provided service/resources,

4. Manage process, and

5. Advantageous purchase/negotiation.”4

DRAFT FOR DISCUSSION AND COMMENT

Page 7 of 20

IV. IS THE VALUE CREATION CHAIN OBSERVABLE AND MEASURABLE?

The value creation chain will focus on the Land Packaging, Land Development, Building

Development, and Building Operations stages of development. In each stage, the

developer buys the raw material and changes the input into a different product by adding

capital improvements so that the developer is selling a new product at the end the stage to

a participant in the next stage of development. In this process, I suggest the following

measurable and observable propositions:

Each successive stage of development has less risk and uncertainty that the earlier

stage of development e.g.,

o Land packaging has more risk than land development,

o Land development has more risk than building development, and

o Building development has more risk than building operations.

Each successive stage has a lower cost of capital than the earlier stage e.g.

o Land Packaging required rate of return – 25% and up,

o Land development required rate of return – 20%,

o Building development required rate of return – 15%, and

o Building operations required rate of return – 10%

Each successive stage requires more additional capital that the earlier stage e.g.

o Land Packaging – mostly fees to professionals,

o Land Development – fees, excavation costs and infrastructure materials,

o Building Development – fees, construction costs, and building materials,

and

o Building Operations -- building management and systems, (oops this one

doesn’t work).

The bad news is that more capital is required at each stage, and the good news is

that the cost of capital is lower at each stage.

Each successive stage creates value (or profit) by creating or manufacturing a new

product.

o Land Packaging produces “land with a plan”,

o Land Development produces “building pads”,

o Building Development produces “completed building”, and

o Building Operations produces “leased building with an operating history

and a cash flow” (an institutional investment).

With each successive stage of development, the developer attempts to create

additional value by incurring additional risks and increasing its capital exposure.

DRAFT FOR DISCUSSION AND COMMENT

Page 8 of 20

Most developers have neither the requisite skill set nor the appropriate capital

structure to complete all stages in the development process.

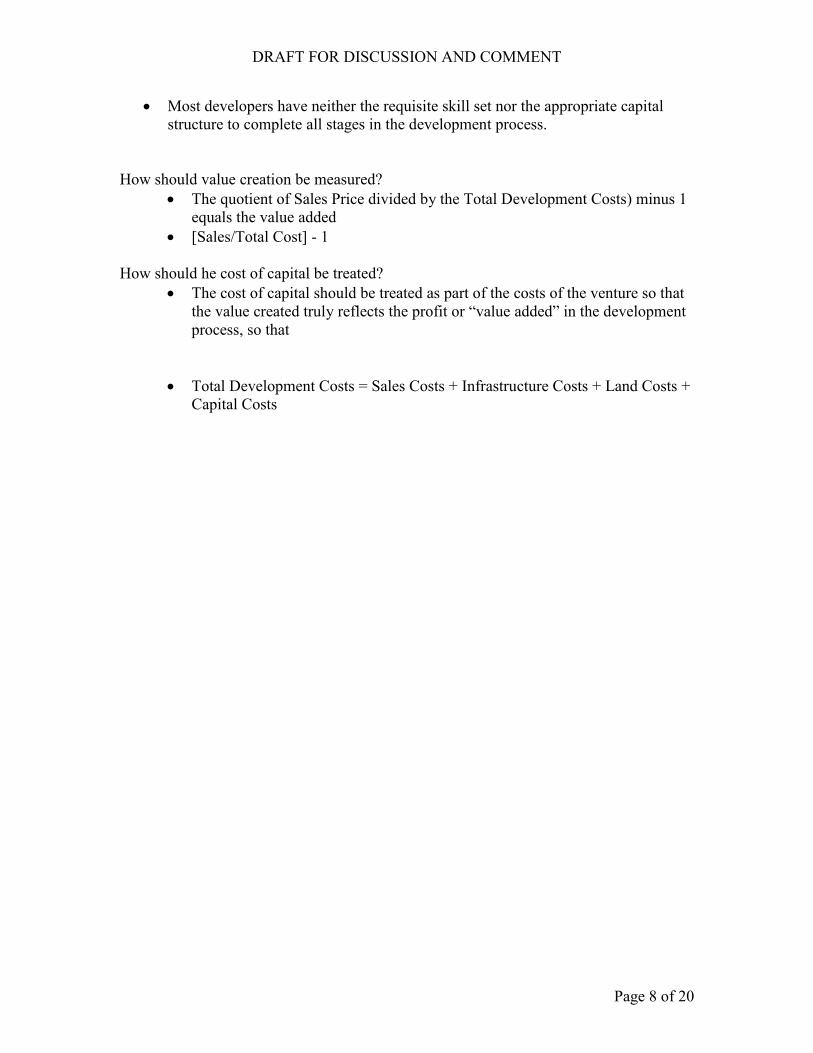

How should value creation be measured?

The quotient of Sales Price divided by the Total Development Costs) minus 1

equals the value added

[Sales/Total Cost] - 1

How should he cost of capital be treated?

The cost of capital should be treated as part of the costs of the venture so that

the value created truly reflects the profit or “value added” in the development

process, so that

Total Development Costs = Sales Costs + Infrastructure Costs + Land Costs +

Capital Costs

DRAFT FOR DISCUSSION AND COMMENT

Page 9 of 20

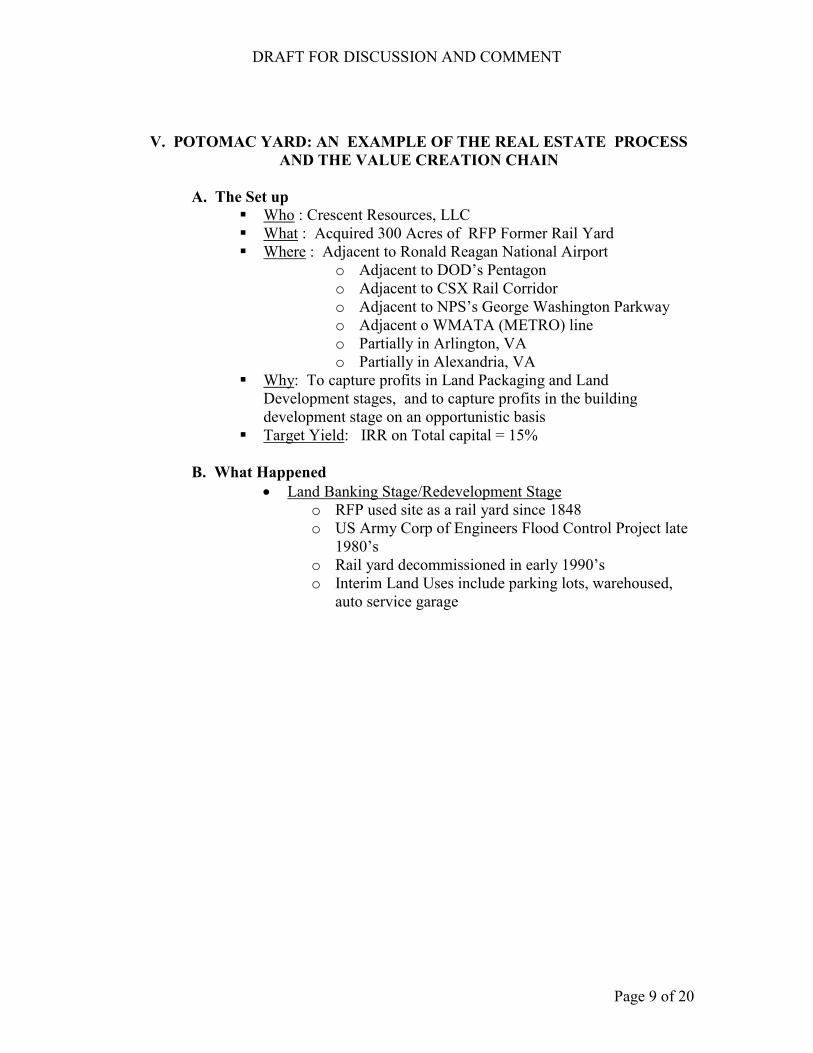

V. POTOMAC YARD: AN EXAMPLE OF THE REAL ESTATE PROCESS

AND THE VALUE CREATION CHAIN

A. The Set up

Who : Crescent Resources, LLC

What : Acquired 300 Acres of RFP Former Rail Yard

Where : Adjacent to Ronald Reagan National Airport

o Adjacent to DOD’s Pentagon

o Adjacent to CSX Rail Corridor

o Adjacent to NPS’s George Washington Parkway

o Adjacent o WMATA (METRO) line

o Partially in Arlington, VA

o Partially in Alexandria, VA

Why: To capture profits in Land Packaging and Land

Development stages, and to capture profits in the building

development stage on an opportunistic basis

Target Yield: IRR on Total capital = 15%

B. What Happened

Land Banking Stage/Redevelopment Stage

o RFP used site as a rail yard since 1848

o US Army Corp of Engineers Flood Control Project late

1980’s

o Rail yard decommissioned in early 1990’s

o Interim Land Uses include parking lots, warehoused,

auto service garage

DRAFT FOR DISCUSSION AND COMMENT

Page 10 of 20

Land Packaging Stage (Paper Infrastructure)

o Approved Conceptual Plans

Alexandria, CCD

Arlington, PDSP

o Alta Survey

o First Chicago Title Insurance

o Environmental Studies and Tests

o Environmental Remediation Plan

o Environmental Liability Insurance ($100,000,000)

o NEPA law suit resolved

o North Tract title issues resolved

o North Tract transfer to Arlington which included

environmental remediation plan and financial

guarantees

o Preliminary Phasing Plan in Alexandria – Infrastructure

Plan

o Preliminary Infrastructure Plan in Arlington

o Approved Soil Management Plan

o Community Outreach Program which resulted in

Neighborhood Approval of Off-site

Infrastructure

Monroe Avenue Bridge design and approval

o Development and approval of Arlington’s Public Art

Policy

o Arlington Park Approvals

Land Development Stage

o Off-Site Infrastructure

Alexandria --

Trunk Sewer construction

Outfall Construction and Enhancement

on Potomac River

Two water lines under CSX and

WAMTA rail lines

Sewer Lines under CSX and WMATA

rail lines

Play fields

US Route 1 Improvements

Haul road construction

DRAFT FOR DISCUSSION AND COMMENT

Page 11 of 20

Arlington

Pump Station

Outfall on Army Corps Flood Control

project

Water line under CSX to Regan National

Airport

Trunk Sewer line under US Route 1

US Route 1 Improvements

Crystal Drive Improvements

Glebe Road – US Route 1 Intersection

33rd

Street, Crystal Drive, and US

Route 1 Intersection

o On-Site Infrastructure

Alexandria

Rough Grade Potomac Avenue

Potomac Avenue Water Line (partial)

Potomac Avenue Sanitary Sewer (partial)

Potomac Avenue Storm Sewer (partial)

School Park Play Field

Soil Management Plan Execution (480

cu yds of land import and lay-down)

Dog Park Resolution

Pedestrian Bridge Resolution

Future WAMTA Station design and

reservation

DRAFT FOR DISCUSSION AND COMMENT

Page 12 of 20

Arlington

Potomac Avenue Construction

Glebe Road Extension Construction

33rd

Street Construction

35th

Street Partial Construction

Ball Street Construction

Storm Sewer Construction

Sanitary Sewer Construction

Water Line Construction

Communication and Power Duct Banks

Construction

Installed Traffic Signals with

communications and interconnection at

five intersections

Planted Potomac Avenue and Crystal

Drive Landscaping

Rough graded and Engineered transit

way

Managed excavation of soils in Land

bays F, E-East, and Land Bay A

Removed 40 tons of contaminated soils

and cinder ballast

DRAFT FOR DISCUSSION AND COMMENT

Page 13 of 20

o Building Development Stage

Municipal Site Plan Approvals

Arlington Land Bay F

Arlington land Bay E-East

Arlington Land Bay A

Alexandria Land Bay A

Alexandria Land Bay C

Building Permit

Arlington Land bay A

Arlington Land Bay E-East

Constructed land Bay A (1.1 million square

feet)

654,000 FAR SF in two, 12-story

Towers

Six stories of parking (3 above,3 below

grade)

Leased 420,000 SF to US Env.

Protection Agency

IAQ Implementation and Testing

Commissioned All Building Systems

Achieved USGBC’s Gold LEED Rating

Installed Public Art

Certificate of Occupancy permits

Federal protection Services level IV

Security

Build out EPA Tenant Improvements

Moved EPA into Space

Building monitoring systems for DOE’s

Energy Star Rating

DRAFT FOR DISCUSSION AND COMMENT

Page 14 of 20

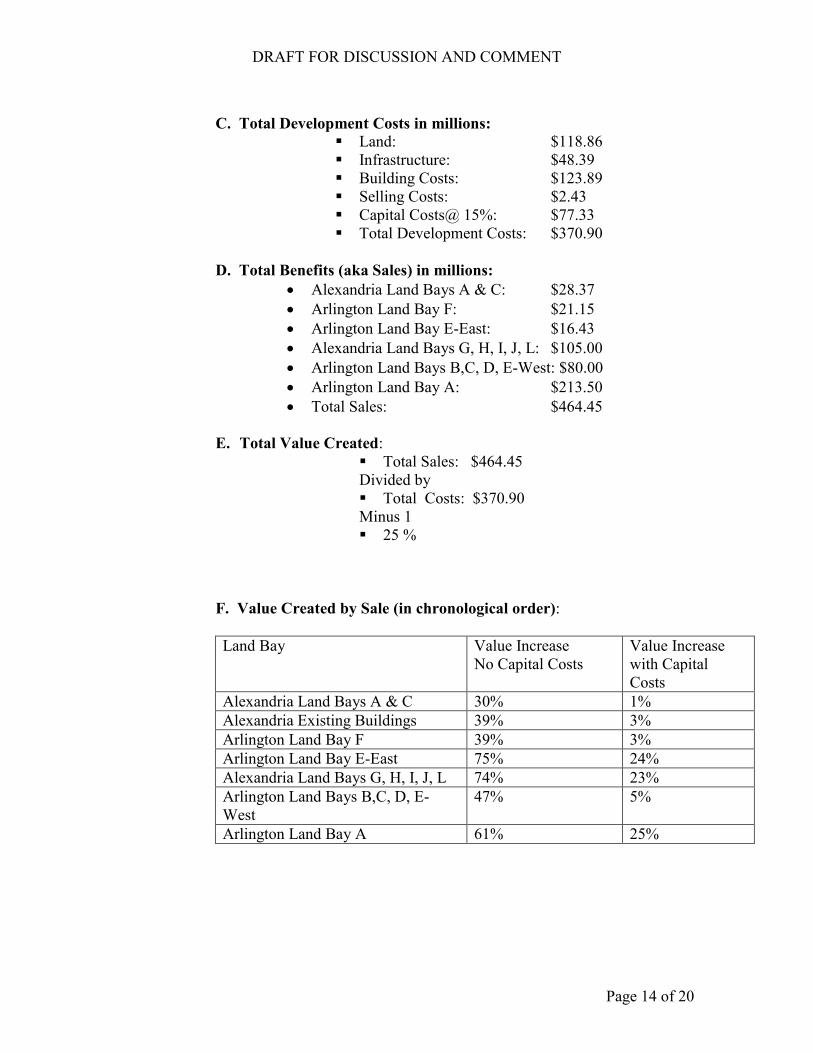

C. Total Development Costs in millions:

Land: $118.86

Infrastructure: $48.39

Building Costs: $123.89

Selling Costs: $2.43

Capital Costs@ 15%: $77.33

Total Development Costs: $370.90

D. Total Benefits (aka Sales) in millions:

Alexandria Land Bays A & C: $28.37

Arlington Land Bay F: $21.15

Arlington Land Bay E-East: $16.43

Alexandria Land Bays G, H, I, J, L: $105.00

Arlington Land Bays B,C, D, E-West: $80.00

Arlington Land Bay A: $213.50

Total Sales: $464.45

E. Total Value Created:

Total Sales: $464.45

Divided by

Total Costs: $370.90

Minus 1

25 %

F. Value Created by Sale (in chronological order):

Land Bay Value Increase

No Capital Costs

Value Increase

with Capital

Costs

Alexandria Land Bays A & C 30% 1%

Alexandria Existing Buildings 39% 3%

Arlington Land Bay F 39% 3%

Arlington Land Bay E-East 75% 24%

Alexandria Land Bays G, H, I, J, L 74% 23%

Arlington Land Bays B,C, D, E-

West

47% 5%

Arlington Land Bay A 61% 25%

DRAFT FOR DISCUSSION AND COMMENT

Page 15 of 20

G. How Value was Created (in chronological order):

Alexandria Land Bays A & C

Letter of Intent: October 31, 2001

Contract Execution: April 1, 2002

Sales Date: September 25, 2003

Conditions of Sale:

o Off-site Infrastructure (Trunk sewer)

o On-site Infrastructure ( Utilities to property line)

o Site Plan Approval (Special Use Permit)

o Executed Development Agreement

Value Created

o Sales Price: 28.37

o Total Costs:

Land: 16.235

Infrastructure: 5.44

Selling Expenses: .08

Capital Cost: 6.22

o Value Created: 1%

Arlington Land Bay F

Letter of Intent: April 2003

Contract Execution: June 2003

Sales Date: December 15, 2003

Conditions of Sale:

o Off-site Infrastructure (Pump station, Road

Improvements)

o On-site Infrastructure ( Utilities to property line)

o Soil Disposal

o Site Plan Approval (Regulation 4.1 approval)

o Executed Development Agreement

Value Created

o Sales Price: 21.15

o Total Costs:

Land: 11.356

Infrastructure: 3.8

Selling Expenses: .02

Capital Cost: 5.38

o Value Created: 3%

DRAFT FOR DISCUSSION AND COMMENT

Page 16 of 20

Arlington Land Bay E-East

Letter of Intent: May 2003

Contract Execution: August 2003

Sales Date: June 11, 2004

Conditions of Sale:

o Off-site Infrastructure (Pump station, Road

Improvements)

o On-site Infrastructure ( Utilities to property line)

o Soil Disposal

o Site Plan Approval (Regulation 4.1 approval)

o Building Permit.

o Executed Development Agreement

Value Created

o Sales Price: 16.43

o Total Costs:

Land: 6.897

Infrastructure: 2.31

Selling Expenses: .17

Capital Cost: 3.88

o Value Created: 24%

Alexandria Land Bays G, H, I, J, L

Letter of Intent: December 2003

Contract Execution: January 2004

Sales Date: June 30, 2004

Conditions of Sale:

o Off-site Infrastructure (Trunk sewer)

o On-site Infrastructure ( Utilities to property line)

o Executed Development Agreement

Value Created

o Sales Price: 105.

o Total Costs:

Land: 44.688

Infrastructure: 14.96

Selling Expenses: .66

Capital Cost: 25.15

o Value Created: 23%

DRAFT FOR DISCUSSION AND COMMENT

Page 17 of 20

Arlington Land Bays B, C, D, E-West

Letter of Intent: June 2004

Contract Execution: September 2004

Sales Date: October 28, 2004

Conditions of Sale:

o Off-site Infrastructure (Trunk sewer)

o On-site Infrastructure ( Utilities to property line)

o Executed Development Agreement

Value Created

o Sales Price: 80.

o Total Costs:

Land: 34.059

Infrastructure: 19.99

Selling Expenses: .28

Capital Cost: 21.29

o Value Created: 6%

Arlington Land Bay A

Letter of Intent: June 2005

Contract Execution: October 2005

Sales Date: November 15, 2005

Conditions of Sale:

o Off-site Infrastructure (Pump station, Road

Improvements)

o On-site Infrastructure ( Utilities to property line)

o Soil Disposal

o Site Plan Approval (Regulation 4.1 approval)

o Building Permit.

o Executed Development Agreement

o Constructed Buildings

o 66% Leased

o Occupancy Permits

o LEED Gold Rating

Value Created

o Sales Price: 213.5

o Total Costs:

Land: 5.6610

Infrastructure: 1.89

Selling Expenses: 1.23

Building Improvements: 123.89

Capital Cost: 15.42

o Value Created: 44%

DRAFT FOR DISCUSSION AND COMMENT

Page 18 of 20

H. Serendipity Value Creation

Existing Building Re-Sale

Purchase Option Sale

Falling Capitalization Rates

DRAFT FOR DISCUSSION AND COMMENT

Page 19 of 20

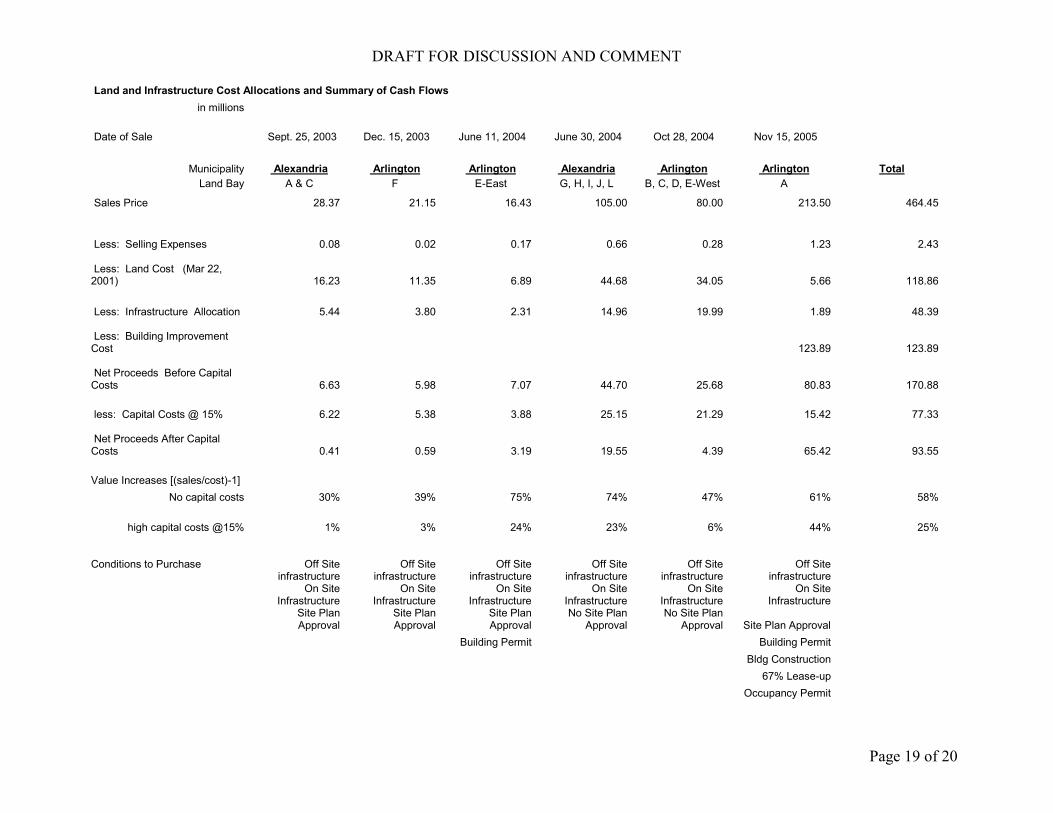

Land and Infrastructure Cost Allocations and Summary of Cash Flows

in millions

Date of Sale Sept. 25, 2003 Dec. 15, 2003 June 11, 2004 June 30, 2004 Oct 28, 2004 Nov 15, 2005

Municipality Alexandria Arlington Arlington Alexandria Arlington Arlington Total

Land Bay A & C F E-East G, H, I, J, L B, C, D, E-West A

Sales Price 28.37 21.15 16.43 105.00 80.00 213.50 464.45

Less: Selling Expenses 0.08 0.02 0.17 0.66 0.28 1.23 2.43 Less: Land Cost (Mar 22, 2001) 16.23 11.35 6.89 44.68 34.05 5.66 118.86

Less: Infrastructure Allocation 5.44 3.80 2.31 14.96 19.99 1.89 48.39 Less: Building Improvement Cost 123.89 123.89 Net Proceeds Before Capital Costs 6.63 5.98 7.07 44.70 25.68 80.83 170.88

less: Capital Costs @ 15% 6.22 5.38 3.88 25.15 21.29 15.42 77.33 Net Proceeds After Capital Costs 0.41 0.59 3.19 19.55 4.39 65.42 93.55

Value Increases [(sales/cost)-1]

No capital costs 30% 39% 75% 74% 47% 61% 58%

high capital costs @15% 1% 3% 24% 23% 6% 44% 25% Conditions to Purchase Off Site

infrastructure Off Site

infrastructure Off Site

infrastructure Off Site

infrastructure Off Site

infrastructure Off Site

infrastructure

On Site

Infrastructure On Site

Infrastructure On Site

Infrastructure On Site

Infrastructure On Site

Infrastructure On Site

Infrastructure

Site Plan Approval

Site Plan Approval

Site Plan Approval

No Site Plan Approval

No Site Plan Approval Site Plan Approval

Building Permit Building Permit

Bldg Construction

67% Lease-up

Occupancy Permit

DRAFT FOR DISCUSSION AND COMMENT

Page 20 of 20

END NOTES

1 James A. Graaskamp, Lecture Notes, 1973

2 Stephen Roulac, “Competitiveness of Business Models and the Chain of Property Distribution,” p

389. 3 Roulac, Adair, Allen, Berry, and McGreal, “Beyond Valuation Measurement to Value Creation,”

4 Ibid

5 FASB Statement 67 Real Estate: Accounting for Costs and Initial Rentals Operations of Real Estate

Projects Paragraph 11a. “Land cost and all other common costs (prior to construction) shall be

allocated to each land parcel benefited. Allocation shall be based on the fair value before

construction.” 6 Ibid

7 Ibid

8 Ibid

9 Ibid

10 Ibid