The Real Deal Webinar Series: Representation & Warranty ... · The Real Deal Webinar Series:...

41

© 2014 Winston & Strawn LLP The Real Deal Webinar Series: Representation & Warranty Insurance November 18, 2014

-

Upload

truongquynh -

Category

Documents

-

view

219 -

download

3

Transcript of The Real Deal Webinar Series: Representation & Warranty ... · The Real Deal Webinar Series:...

© 2014 Winston & Strawn LLP

The Real Deal Webinar Series: Representation & Warranty Insurance

November 18, 2014

©2014 Winston & Strawn LLP 2

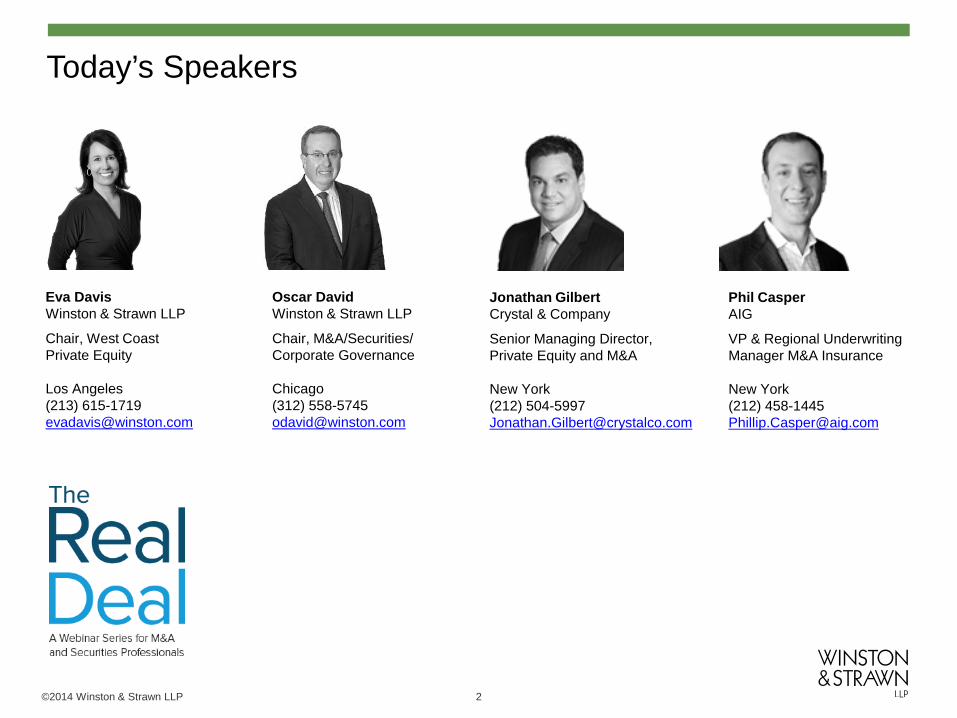

Today’s Speakers

Eva Davis Winston & Strawn LLP

Chair, West Coast Private Equity Los Angeles (213) 615-1719 [email protected]

Oscar David Winston & Strawn LLP

Chair, M&A/Securities/ Corporate Governance Chicago (312) 558-5745 [email protected]

Jonathan Gilbert Crystal & Company

Senior Managing Director, Private Equity and M&A New York (212) 504-5997 [email protected]

Phil Casper AIG

VP & Regional Underwriting Manager M&A Insurance New York (212) 458-1445 [email protected]

© 2014 Winston & Strawn LLP

Background

©2014 Winston & Strawn LLP 4

• The 2014 market for M&A deals in the U.S. remains strong, with the first three quarters of 2014 being some of the most active quarters since the 2008 financial collapse.

• Today’s M&A market is a heated “sellers’ market” fueled by: – Readily available acquisition financing – The largest overhang of private equity dry powder in US history – Excess cash on the balance sheets of US strategics

• With a strong sellers’ market, buyers, especially PE buyers, have embraced representation and warranty insurance to best position its bids.

• Use doubled in 2012 and may triple this year.

Background

© 2014 Winston & Strawn LLP

Overview

©2014 Winston & Strawn LLP 6

• Protects an insured from unanticipated and unknown losses that may arise subsequent to the closing

• Generally, covers all representations and warranties in the purchase agreement

• Either buyer or seller can be insured under the policy • Historically, designed to bridge gap between buyer and seller in the

face of specific dispute • More recently, used to provide insurance for breaches of certain or

all representations and warranties

R&W Insurance Overview

©2014 Winston & Strawn LLP 7

• Buyer-side policies more prevalent; generally viewed as providing greater protection

• Impact of exclusions, especially treatment of fraud and definition of “Knowledge”

• Difference in claim handling procedures and duty to defend – Seller-side policy structured as third-party liability policy—backstop – Buyer-side policy structured as first-party loss policy—step in Seller’s shoes

• If buyer-side policy is sole remedy for breach of reps and warranties, seller may want to include as a term in the purchase agreement

Buyer-side vs. Seller-side Policies

©2014 Winston & Strawn LLP 8

• Typically will not cover seller indemnity for breach of covenants or specifically-identified contingent liabilities

• Uncovered losses typically not counted against policy retention – May create unexpected gap for buyer

• Reps could be subject to another layer of negotiations • Changes in reps and warranties in purchase agreement may impact

coverage availability and premiums – Need to keep insurance carrier informed during negotiation process and be

responsive to carrier’s diligence requests

• Indemnification provisions in purchase agreement have to be negotiated side by side with insurance policy

Scope of Coverage

©2014 Winston & Strawn LLP 9

• Negotiated between Buyer and Seller • Party paying the premium not necessarily the insured • Both parties typically benefit, so premiums may be split • In addition to premium, insurance carrier may charge an underwriting

fee to cover due diligence and other legal costs (range of $15,000 to $50,000)

Who Pays?

©2014 Winston & Strawn LLP 10

• Potential Buyer benefits • Potential Seller benefits • Note costs/challenges to use of R&W insurance

– Cost of policy—adds to transaction costs – Introduction of 3rd party to negotiation – Potential credit risk of insurer – Potential coverage risk – Potential timing risk – No true off-the-shelf product—significant negotiation often present – Common policy exclusions

Buyer-side vs. Seller-side Policies

© 2014 Winston & Strawn LLP

Recent Surge in the Use of R&W Insurance

©2014 Winston & Strawn LLP 12

• Reports suggest that the sale of R&W insurance doubled in 2012 and is estimated to triple this year. This can be attributed to the following:

– Reduced costs (often 3 - 4% of the amount being insured) – Improved process (coverage can be bound in as quickly as a few days) – Better terms and conditions (after years of negotiations, policies can provide

narrower exclusions, longer policy periods and higher limits of liability) – Claims paying history (over the past 15 years, millions of dollars in claims have

been paid out for breaches of representations and warranties, with a number of clients with positive claims stories)

– Greater acceptance in the deal community (some sellers now include R&W insurance proposals in bid request packages when marketing their business for sale, and buyers are using R&W insurance as a tool to win auctions)

– Given “seller-friendly” market dynamics, sellers have in certain cases required or greatly encouraged the use of R&W insurance

Why the Increased Prevalence of R&W Insurance?

© 2014 Winston & Strawn LLP

Benefits of R&W Insurance to Buyers

©2014 Winston & Strawn LLP 14

• Can be obtained without the knowledge of the seller • Coverage for liabilities where creditworthiness of seller(s) or ability to

collect from multiple sellers a concern • May ease tension where buyer seeks indemnification from former

shareholder management members who are employed by buyer after the closing

• Coverage amounts, retention amounts (deductibles) and negotiated terms position the buyer to more easily accept indemnification terms from a seller on limited terms (e.g., modest survival periods, liability caps and escrow amounts)

• Increased protection against loss from breach of seller’s representations and warranties (dollar limit / policy terms exceed survival period)

• Buyer with added benefit of obtaining deal protection from a more financially viable entity (a AAA rated credit)

• Increase attractiveness of bid in competitive auction process

Benefits to Buyer

© 2014 Winston & Strawn LLP

Benefits of R&W Insurance to Sellers

©2014 Winston & Strawn LLP 16

• Reduce risk of lost dollars from unknown future losses (arising from breach)

• Ability to receive more purchase price upfront instead of tying it up in escrows and holdbacks

• Can ease tension among sellers related to the often contentious point of several and/or joint liability

• Ability to make a “cleaner exit” from the investment with limited (if any) indemnification obligations, providing greater certainty of deal proceeds

Benefits to Seller

© 2014 Winston & Strawn LLP

Differences in R&W Insurance from Other Insurance Policies Related to Transactions

©2014 Winston & Strawn LLP 18

• Just as a buyer can seek to negotiate indemnification terms with a seller, a buyer can negotiate insurance provisions with the insurance company.

• R&W insurance does not mirror what is or would customarily be contained in a seller’s indemnification covenant in a purchase in contract sale.

• Some policy provisions are more expansive thus providing the insured with more coverage while other provisions are narrower providing less coverage.

Overview

© 2014 Winston & Strawn LLP

R&W Insurance as a Potential Valuable Deal Solution

©2014 Winston & Strawn LLP 20

• Strategic Use By Buyer in Auctions: – Distinguish bid in auction by requiring seller to provide only limited (scope, time,

dollars) indemnification coverage – Effectively increases desired indemnification to buyer (scope, time, dollars)

• Strategic Use by Seller in Auctions: – Allows seller in auctions to specify exactly what it is willing to provide in terms of

indemnification (scope, time, dollars) – Message to buyer is to offer best purchase price given limited scope of

indemnification but knowing R&W insurance is available – “You’ll still get protection, but it’s not coming from me” – Similar to seller offering “stapled financing”

Strategic Use of R&W Insurance in Auctions

©2014 Winston & Strawn LLP 21

Provision M&A Agreement Coverage Insurance Coverage Fundamental Reps 5 years (less competitive deals would be

indefinite) 6 years

Operational Reps 15 months 2 years Intellectual Property Reps 15 months 3 years TAX, Environmental and ERISA Reps 3 years (less competitive deals would be

statute of limitations) 6 years (note that we may seek separate environmental insurance policy)

Dollar Thresholds

DeMinimus $50,000 $20,000 Deductible for Operational and Intellectual Property Reps

1% of purchase price 5% of purchase price (matches M&A indemnity cap) with step down in deductible to 1% of purchase price after 15 months (when indemnification for these items expires under the M&A agreement)

Deductible for Fundamental, TAX and ERISA Reps

None 1% of purchase price

Indemnity Cap on Operational and IP Reps (also matched the escrow)

5% of purchase price 20% of purchase price

Limitations

Consequential Damages, Lost Profit, Multiple of Earnings

Affirmatively disregarded Silent

Mitigation Duty to mitigate affirmatively stated Silent

Example of RWI from a Recent Transaction The policy may "layer in" above the coverage provided by a seller through indemnification. However, since the cost of the policy increases with coverage amounts and policy periods, an insured may choose coverage less than would typically be offered by a seller as indemnification for certain breaches.

© 2014 Winston & Strawn LLP

Policy Overview

©2014 Winston & Strawn LLP 23

• Cost: Premium range 3-4% of limits purchased • Limits Available: $10 million to $300 million + • Deductible: 1-2% of Purchase Price • Process:

– Step 1: <1 week to receive initial indications from market with basic information (draft transaction document, financials, summary of target)

• Parties should consider an NDA with the Insurance carrier before providing confidential information

– Step 2: 1-2 week underwriting process for insurance carrier to complete due diligence/underwriting

• Policy drafting typically done in tandem with buyer’s deal attorneys to ensure terms of policy align with transaction document

• Several provisions can be negotiated in a manner that would typically be considered "buyer favorable", including whether consequential damages, lost profit or multiple of earnings damages will be covered

Policy Overview

©2014 Winston & Strawn LLP 24

• Common Policy Exclusions – “Actual knowledge” of breach – Fines and penalties (uninsurable by law) – Asbestos – Environmental (varies by industry/target/

carrier) – Underfunded pension liabilities – Medicare/Medicaid exclusions – Purchase price or working capital

adjustments – Specific reserves on financial statements – Forward-looking statements

Policy Overview (continued)

• Common Policy Conditions – Defense expenses included as

covered cost/within definition of loss

– Subrogation against seller limited to fraud

– Policy assignable with consent – Buyer’s knowledge limited to

deal team members

© 2014 Winston & Strawn LLP

Underwriting Focus

©2014 Winston & Strawn LLP 26

• Industry/Deal Characteristic Specific Issues – Healthcare—regulatory and government billing issues – Financial – Technology – Adequacy of Due Diligence (third party due diligence)

• Heightened Areas of Concern: – Product Liability – Environmental – Healthcare—government billing – Tax – Labor Issues – Net Operating Loss

Underwriting Focus

© 2014 Winston & Strawn LLP

Claims History

©2014 Winston & Strawn LLP 28

• One out of every four policies have filed notice of claim • Between January 1998 and January 2013 –

– Claims notices were received on 28% of the policies issued in North America – Of the 71 claims received on the 253 W&I policies written since 1998, there have

been alleged breaches of 149 representations and warranties

Frequency of Claims Made – North America (AIG)

0

10

20

30

40

50

60

70

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Policies Written

Claims Made

Breaches

©2014 Winston & Strawn LLP 29

Global Overview: Claims by Industry Sector (2012)

0

1

2

3

4

5

6

7

8

9

10

©2014 Winston & Strawn LLP 30

Global Overview: Claims by Deal Size (2012)

36%

39%

25%

Deal Value under $50millionDeal Value between$50-$250 millionDeal Value above $250million

©2014 Winston & Strawn LLP 31

Types of Alleged Breaches – Global (2012)

0

5

10

15

20

25Pe

rcen

tage

of C

laim

s

©2014 Winston & Strawn LLP 32

Timing of Claims Reports – Global (2012)

64%

29%

7%

0-12 months frominception

12-24 monthsfrom inception

Over 24 monthsfrom inception

©2014 Winston & Strawn LLP 33

• Compliance with Laws Background: – Acquisition of a service company with over $400 million. – Claim brought by buyer under a buyer-side policy relating to a breach of

the compliance warranties resulting from several governmental investigations of the target company.

Claim Resolution: – The claim is still in the early stages and the amount of the potential

liability for the underlying matter cannot be quantified at this time. The amount of damages claimed are in excess of $25 million.

Claim Scenarios

©2014 Winston & Strawn LLP 34

• Accounts Receivable Background: – Acquisition of a restaurant chain by a strategic purchaser for over $78

million. – Seller-side policy responds to a claim brought by buyer for breach of,

among others, the financial statements and accounts receivable R&Ws in connection with the target's issuance of over $1 million of gift certificates which had not been recorded in the financial statements.

Claim Resolution: – The Buyer’s auditors presented sellers and insurer with a report

itemizing the alleged breaches and amount of damages resulting there from. AIG and its advisors reviewed the report and determined the claim was covered under the policy. As a result, AIG paid a significant sum in settlement and expenses to resolve the claim.

Claim Scenarios (continued)

©2014 Winston & Strawn LLP 35

• Material Adverse Change Background: – Acquisition of a horticulture business for over £10 million. Buyer-side

policy responds to a claim brought by the buyer against the RWI insurance policy for alleged breaches of the warranties regarding financial statements, operation of the business in the ordinary course, no MAC event between the date of the interim financial statements and the closing, title to assets, contracts and accounts receivable.

Claim Resolution: – Buyer and seller arbitrated their dispute, with AIG monitoring the

proceedings. While buyer and seller were still engaged in their dispute, AIG and the insured achieved resolution and settlement regarding several of the matters being disputed between the insured and seller. As a result of the settlement, AIG paid out a substantial sum in settlement and expenses.

Claim Scenarios (continued)

© 2014 Winston & Strawn LLP

Key Takeaways

©2014 Winston & Strawn LLP 37

• Carefully consider and negotiate your insurance policy just as you would negotiate an indemnification provision in a purchase agreement

• Indemnification provisions in purchase agreement have to be negotiated side by side with insurance policy

– Consider those areas that are likely to be excluded from the policy – Negotiate earlier in the process for greater indemnification of such excluded items – Can also seek alternative risk transfer vehicle (tax, environmental, other

contingent liability policy).

• “Actual Knowledge” Exclusion – R&W policies exclude matters of which the buyer has "actual knowledge" of (akin

to an "anti-sandbagging" provision in a purchase agreement). – If buyer’s due diligence has uncovered a matter that would constitute a breach of

the reps and warranties and the seller has not disclosed it, we recommend addressing the issue with the seller prior to signing (either via purchase price reduction, specific indemnity or other method).

Key Takeaways

©2014 Winston & Strawn LLP 38

• In a competitive auction, sellers should consider signaling from the outset that they intend to provide only limited indemnification, effectively forcing the buyer to purchase a R&W policy or, in the absence of one, be aware that other bidders may be doing so.

• While private equity funds are purchasing these policies more frequently (as buyers to better position bids and as sellers to provide for more certainty on the return on investment), strategic buyers are now more actively considering these policies.

• While R&W policies can be bound in a matter of days, an insured will be in a better position to negotiate the terms of a policy more favorable to the insured if it provides the underwriter with more time (preferably 2-3 weeks or more)

Key Takeaways

©2014 Winston & Strawn LLP 39

• While the insured under a R&W policy does have the backing of a AAA rated credit, the insurance company will expect proof of breach and loss, and to the extent that their interpretation of the amount of loss differs from the insured’s, there may be some negotiation as to the quantum of loss actually paid.

• Use of policies has doubled in 2012 and may triple in 2013 • Negotiation process if more efficient and this will continue • There are many benefits, but one must consider costs/challenges. • Policy terms and cost in the US are different than in Europe and other

regions of the world.

Key Takeaways

©2014 Winston & Strawn LLP 40

Questions?

Eva Davis Winston & Strawn LLP

Chair, West Coast Private Equity Los Angeles (213) 615-1719 [email protected]

Oscar David Winston & Strawn LLP

Chair, M&A/Securities/ Corporate Governance Chicago (312) 558-5745 [email protected]

Jonathan Gilbert Crystal & Company

Senior Managing Director, Private Equity and M&A New York (212) 504-5997 [email protected]

Phil Casper AIG

VP & Regional Underwriting Manager M&A Insurance New York (212) 458-1445 [email protected]

© 2014 Winston & Strawn LLP

Thank You