The Politics of Tax Accounting in the US_ Evidence From Taxpayer Relief Act of 1997 - Roberts & B

26

The politics of tax accounting in the United States: evidence from the Taxpayer Relief Act of 1997 Robin W. Roberts*, Donna D. Bobek School of Accounting, University of Central Florida, PO Box 161400, Orlando, FL 32816, USA Abstract The purpose of this study is to utilize prior research in US Congressional politics, the accounting/state relationship, and corporate political activity to analyze corporations’ political activities during the development and passage of the United States’ Taxpayer Relief Act of 1997. Our study provides evidence consistent with the notion that large cor- porations exercise considerable political power during the state’s formulation of new tax accounting laws. These findings lead us to question the applicability of a strict pluralist model in accounting policy research and have implications for future research in corporate political activity, corporate tax accounting, and the political economy of accounting. # 2003 Elsevier Ltd. All rights reserved. A prominent debate continues over the extent to which business interests dominate politics and policymaking (Grier, Munger, & Roberts, 1994; Suarez, 1998). This debate occurs on multiple the- oretical levels (Quinn & Shapiro, 1991). In the accounting literature, some researchers argue that the heart of the debate rests on whether or not neoclassical state theory is the appropriate basis for accounting policy research (Cooper & Sherer 1984; Tinker, 1984; Tinker, Merino, & Nei- mark 1982). Of particular concern is the neoclassical assumption of political voluntarism, its linkage to the individualistic emphasis of interest group the- ory, and its reliance on the notion of equal access to the political marketplace. Tinker (1984, p. 62) argues that interest group theory’s pluralistic view of social relations is inadequate because, ‘‘while a recognition of the self-seeking of individuals may be necessary to understanding social behavior, it is not sufficient. It is also important to understand the type of social system in which individual self- interest is situated.’’ Research significance is attached to understanding the social system, at least in part, because the structure of the social system influences the manner in which interest groups develop and compete against each other for favored legislation. A significant result of the adoption of strict neoclassical assumptions in accounting policy research is a failure to recognize the social and political implications inherent in the public policy arena (Cooper & Sherer, 1984; Tinker et al., 1982). In this paper, we present a case study of US tax accounting law formation to investigate the extent to which tax policies are subject to the social and political powers of corporate interests. By examining the political activities of individual 0361-3682/$ - see front matter # 2003 Elsevier Ltd. All rights reserved. doi:10.1016/S0361-3682(03)00036-9 Accounting, Organizations and Society 29 (2004) 565–590 www.elsevier.com/locate/aos * Corresponding author. Tel.: +1-407-823-6727; fax: +1- 407-823-3881. E-mail addresses: [email protected] (R.W. Roberts), [email protected] (D.D. Bobek).

description

he politics of tax accounting in the US_ evidence from taxpayer relief act of 1997 - Roberts & B.pdf*

Transcript of The Politics of Tax Accounting in the US_ Evidence From Taxpayer Relief Act of 1997 - Roberts & B

The politics of tax accounting in the United States:evidence from the Taxpayer Relief Act of 1997

Robin W. Roberts*, Donna D. Bobek

School of Accounting, University of Central Florida, PO Box 161400, Orlando, FL 32816, USA

Abstract

The purpose of this study is to utilize prior research in US Congressional politics, the accounting/state relationship,and corporate political activity to analyze corporations’ political activities during the development and passage of theUnited States’ Taxpayer Relief Act of 1997. Our study provides evidence consistent with the notion that large cor-

porations exercise considerable political power during the state’s formulation of new tax accounting laws. Thesefindings lead us to question the applicability of a strict pluralist model in accounting policy research and haveimplications for future research in corporate political activity, corporate tax accounting, and the political economy ofaccounting.

# 2003 Elsevier Ltd. All rights reserved.

A prominent debate continues over the extent towhich business interests dominate politics andpolicymaking (Grier, Munger, & Roberts, 1994;Suarez, 1998). This debate occurs on multiple the-oretical levels (Quinn & Shapiro, 1991). In theaccounting literature, some researchers arguethat the heart of the debate rests on whether ornot neoclassical state theory is the appropriatebasis for accounting policy research (Cooper &Sherer 1984; Tinker, 1984; Tinker, Merino, & Nei-mark 1982). Of particular concern is the neoclassicalassumption of political voluntarism, its linkage tothe individualistic emphasis of interest group the-ory, and its reliance on the notion of equal accessto the political marketplace. Tinker (1984, p. 62)argues that interest group theory’s pluralistic view

of social relations is inadequate because, ‘‘while arecognition of the self-seeking of individuals maybe necessary to understanding social behavior, it isnot sufficient. It is also important to understandthe type of social system in which individual self-interest is situated.’’ Research significance isattached to understanding the social system, atleast in part, because the structure of the socialsystem influences the manner in which interestgroups develop and compete against each otherfor favored legislation.

A significant result of the adoption of strictneoclassical assumptions in accounting policyresearch is a failure to recognize the social andpolitical implications inherent in the public policyarena (Cooper & Sherer, 1984; Tinker et al., 1982).In this paper, we present a case study of US taxaccounting law formation to investigate the extentto which tax policies are subject to the socialand political powers of corporate interests. Byexamining the political activities of individual

0361-3682/$ - see front matter # 2003 Elsevier Ltd. All rights reserved.

doi:10.1016/S0361-3682(03)00036-9

Accounting, Organizations and Society 29 (2004) 565–590

www.elsevier.com/locate/aos

* Corresponding author. Tel.: +1-407-823-6727; fax: +1-

407-823-3881.

E-mail addresses: [email protected]

(R.W. Roberts), [email protected] (D.D. Bobek).

corporations and corporate coalitions we addressboth the collective political influence of corporateinterests at a societal level and the strategic poli-tical activities of corporations at the organiza-tional level. Even though there have been popularpress accounts of corporate influence on politicaldecisions (e.g., Birnbaum & Murray, 1987), thereis a strong need for academic research that exploresthe corporate/state relationship in this manner.Hillman and Hitt (1999) discuss the paucity ofacademic research on corporate political activityand strongly encourage new empirical work, stres-sing, ‘‘the specific behaviors that firms choose inorder to participate in the public policy processhave received relatively little attention’’ (Hillman& Hitt, 1999, p. 827).

Specifically, in this study we undertake a closeexamination of corporate political activitiesduring the development of the US TaxpayerRelief Act of 1997 (the 1997 Act). We studythree cases of corporate political activity con-cerning the 1997 Act, each examined within aspecific level of political competition or conflict(Epstein, 1969; Mitnick, 1993) during the 6-month public policy formulation stage (i.e.development) of the legislation (Mack, 1997).We analyze the insurance industry’s corporatepolitical activity concerning legislation thatbroadly affected their industry in order to demon-strate inter-social interest (e.g., business versusconsumers) political conflict. Our second caseinvolves the airline industry and examines thepolitical and economic debate surrounding revi-sions to an airline ticket tax. The industry’s frag-mented efforts, which pitted the major airlinesagainst smaller, low-fare carriers, provide anexample of intra-industry political conflict. In thelast case we illustrate individual corporationscompeting with others for favored legislation (i.e.,inter-firm political conflict). Our case of inter-firmpolitical conflict involves an examination of thepolitical activities of two corporations, AmwayCorporation and Sammons Enterprises, and thepassage of rifle-shot rules (i.e. tax law changestargeted to benefit a very specific set of taxpayers)that provided direct benefit to their shareholders.Although this classification of levels of politicalconflict is imperfect, it provides an effective way to

organize our study.1 We gathered data for eachcase by systematically examining relevant tax pro-visions, published articles, hearing transcripts,corporate lobbying reports, corporate annualreports, and campaign contribution data.

Our study is designed to accomplish two impor-tant goals. First, given the debate over the extentto which assumptions of pluralist theory can beused to completely describe how US accountingpolicy is formed, our study gathers empirical evi-dence as a basis from which to challenge the strictpluralist assumptions that support most account-ing policy research. Our purpose is not to disproveall variants of pluralist theory, but rather to shedlight on the presence of potential structuralinequities in the current system of US policy-making and to highlight its consequences. Theintensity and extent of corporate political activitythat we document during the act’s 6-month policyformulation stage raises significant concernsregarding pluralist assumptions. Specifically, plur-alist theory does not address the observed systemicinequities in participation and influence in thedevelopment of accounting and tax policy.

Second, our study was undertaken to advancethe use of corporate political activity frameworksin accounting research. By studying corporatepolitical activities in a tax accounting policy con-text, we highlight a void in empirical tax research.For example, a major segment of empirical taxaccounting research has been built upon the posi-tive approach embedded in the Scholes–Wolfsonparadigm (Shackelford & Shelvin, 2001). Thisparadigm utilizes a microeconomic-based, multi-lateral contracting perspective to examine corpo-rate tax planning activities as a part of overallbusiness strategy (Scholes & Wolfson, 1992).However, this paradigm fails to recognize thestate as a negotiable contracting party and thestructure of tax accounting laws as endogenous

1 We use the term political conflict to describe intense inter-

est group competition that may contain underlying structural

inequities (e.g., vastly different wealth endowments). This is not

equivalent to class conflict in a Marxist sense. However, later in

the paper we discuss Berg’s (1994) argument that many plural-

ist interpretations of US policy collapse into class structure

explanations because business interests hold such a dominating

power position during most policy debates.

566 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

to a corporation’s tax planning activities. Ourstudy shows that corporations not only structurebusiness transactions, they engage in politicalactivities in order to influence the structure of taxaccounting laws under which their corporationsmust operate.

Given the study’s goals, we selected the contextof tax legislation for two primary reasons. First,tax accounting is situated at a crucial intersectionof the accounting/state relationship. Cooper andSherer (1984, p. 218) purport, ‘‘The role of the stateis indeed central to an understanding of accountingpolicy, for the latter is strongly interrelated with atleast one obvious element of state activity, namelytaxation.’’ Second, we believe that a study of thedevelopment of tax accounting law provides acompelling setting from which to examine theinterface of accounting with the claims of pluralisttheory, the distributive dimensions of wealth andpower, and their resulting implications for socialwelfare. The social and political practice ofaccounting (Burchell et al., 1980) and the proble-matic nature inherent in the development ofaccounting policy is displayed prominently in atax setting. Again, we quote Cooper and Sherer(p. 208):

Not only is accounting policy political in thatit derives from the political struggle in societyas a whole but also the outcomes of account-ing policy are essentially political in that theyoperate for the benefits of some groups insociety and to the detriment of others.

We adopt multiple research methods in the hopeof providing convincing evidence to a broad audi-ence of accounting researchers. We utilize descrip-tive and inferential empirical analyses to aid in ourinterpretation of the case materials. This blendingof methods follows recent works that do not usestrict ontological-method pairings, but insteadadvocate multi-paradigm approaches as heuristicsbeneficial in developing an understanding of com-plex social topics (Bourdieu & Wacquant, 1992;Lewis & Grimes, 1999; Warsame, Neu, & Simmons2002).

The remainder of our paper is structured as fol-lows. First, we explain theories of US congres-

sional politics and the accounting/staterelationship and corporate political activity andrelate them to our study. Second, we explain ourmethod of analysis. Third, we present our threecase analyses of corporate political activity regardingselected provisions of the 1997 Act. Finally, wepresent our conclusions and offer suggestions forfuture research.

Theoretical development

In this section, we review and synthesize rele-vant literature on U.S. congressional politics, theaccounting/state relationship, and corporate poli-tical activity. We use this literature to guide ourexamination of corporate political activity and itprovides a theoretical perspective from which topartition and evaluate corporate activities duringthe US public policy-making process.

US Congressional politics and the accounting/staterelationship

Published theoretical work concerning US con-gressional politics reflects the broader debate con-cerning the construction of a civil society. Thus,research on interactions between corporations andthe state in the establishment of tax accountinglaws is rooted (in varying degrees of explicit andimplicit underpinnings) in variants of three grandtheories of American politics—pluralist, institu-tionalist, and Marxist (Berg, 1994). Our paper isconcerned with contrasting the manner in whichpluralist and Marxist theories may be utilized tostudy tax accounting policy.2

Pluralists hold that congressional outcomes arethe result of interest group pressures. These interest

2 Institutionalists argue that through years of customs and

practices members of Congress have attained a high degree of

autonomy (Berg, 1994) that insulates them from the pressures of

voters, other branches of government, interest groups, and

political parties (Berg, 1994). Institutionalists tend to focus on

the socialization processes used in congressional and bureau-

cratic settings to perpetuate the institution’s culture and/or gen-

erate self-protection (Berg, 1994). Because we focus on the

political activities of interest groups, we do not apply institu-

tional theory.

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 567

groups represent their constituencies before Con-gress in order to influence legislation (Berg, 1994).From a pluralist perspective, legislation and regula-tion exist within a ideal market characterized byself-interest motivated actors. Legislators seekre-election, regulators desire larger budgets, andinterest groups demand favorable legislation/reg-ulation. Legislation is determined as the outcomeof a ‘‘political marketplace’’ in which members ofCongress supply laws and regulations to con-stituencies and interest groups in exchange forpolitical re-election support. A relatively largebody of accounting policy research adopts thispluralist perspective through its embrace of neo-classical economics (e.g., Benston, 1982; Freed &Swenson, 1995; Watts & Zimmerman, 1978).Pluralist language used to characterize the socialand political interactions of members of societyreflects its assumption of political voluntarism andits corresponding view that state policy is derivedfrom an aggregation of individual utilities (Tinker,1984).

In contrast, Marxists characterize society by itsmode of production (e.g., capitalist, socialist). Themode of production leads to a class structure thatdetermines who benefits most from the processes ofproduction. The class that holds economic poweralso dictates the state’s dominant political ideologyand uses political power to further its own interests(Berg, 1994). Class structure theories generallyreject the pluralistic assumption of politicalvoluntarism.

A critical stream of accounting research arguesthat neoclassical economics-based accounting pol-icy studies ignore the role of societal-level interestsin the determination of laws and regulations gov-erning accounting (Armstrong, 1991; Burchell etal., 1980; Cooper & Sherer, 1984; Tinker, 1984;Tinker et al., 1982). This critical research ques-tions pluralist theory, political voluntarism, andthe concomitant positive approaches to account-ing policy research. As opposed to assuming thatinterest groups are ‘‘parachuted in’’ to staticresearch models such as is normally the case inaccounting policy studies, critical researcherscontend that policy research should include ananalysis of relevant historical and institutionalfactors. An understanding of these factors will

reveal the interest group conflict surroundingpotential policy outcomes and lead to a moreinformed analysis of the development and the con-sequences of policy decisions (Cooper & Sherer,1984; Tinker, 1984). Berg (1994) argues persuasivelythat many pluralist explanations of US policyhave class structure underpinnings. In essence,business interest groups possess such an imbalanceof power that the result is corporate hegemony.

The demarcation between pluralist and Marxistlines of research is rather clear in accountingpolicy research, principally due to accountingresearchers’ adherence to strict interpretations ofpluralist theory. Political scientists, on the otherhand, sometime develop theoretical perspectivesthat draw from pluralist theory yet acknowledgethe overwhelming power advantage of corporateinterests. These studies tend to investigate relativedifferentials in interest group strength, offer expla-nations why corporate interests do not always winpolitical contests, or explore how imbalances ininterest group power corrupt democratic processes(Clawson, Neustadtl, and Weller 1998; Quinn andShapiro 1991; Useem 1984). The theoretical fram-ing of these studies opens up a conceptual spacefrom which researchers can incorporate notions ofpower and the abuse of power into their empiricalanalyses yet retain the basic democratic notions ofgovernance.

Conceptual research on corporate political activity

Contemporary research streams concerning UScorporate political activity acknowledge the com-plexities in US interest group power relationshipsand recognize that corporate political conflictexists on several levels, occurs in a multitude oflegislative and regulatory arenas, and surfaceswith varying degrees of intensity. According tocorporate political activity theory, a corporationmay engage in political conflict at the inter-firmand/or inter-social interest level (Mitnick, 1993).3

Suarez (2000) views corporate political activity asa supplement to the structural power of business.

3 Mitnick (1993) presents a detailed description of levels of

corporate political competition. Inter-firm and inter-social

interests are most relevant to our study.

568 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

From her perspective, corporations tend tobecome engaged directly in state politics whenthey realize that their particular interests in thebusiness/state relationship are threatened byspecific policy deliberations. At this point corpora-tions may choose to compete with other firms fordesired policy outcomes and/or join other firms incollective action.

Inter-firm conflict may occur among firms in thesame industry (intra-industry) or among firms indifferent industries. For example, firms in the sameindustry may use corporate political activities as acompetitive strategy when attempting to securegovernmental contracts (Mitnick, 1993). Firms indifferent industries may compete for governmentsubsidies (Suarez, 1998). Inter-firm conflict mayalso occur directly between individual firms andall other taxpayers, as is the case when seekingrifle-shot legislation (Hulse, 1996). Inter-socialinterest conflict exists between corporations andother organized interests such as labor, consumer,or environmental advocacy groups (Mitnick,1993). This conflict may be regarding specific leg-islation (e.g., raising the minimum wage) or amore general conflict over the distribution of gov-ernment support (or taxation).

Numerous arenas for political conflict exist becauseof the complexity of the US federal public policy-making process. For this reason, public policy studiesoften examine issues through a life cycle model com-posed of three stages: public opinion formation, pub-lic policy formulation, and public policyimplementation (Buchholz, 1988; Mack, 1997).4 Thepublic opinion formation stage occurs when therebecomes a substantial difference between publicexpectations and institutional performance suchthat a definable issue is formed. A public policyissue enters the public policy formulation stagewhen the issue becomes politicized, is widely dis-cussed, becomes a concern for affected interestgroups, and is formally introduced as specific leg-islation. When legislation becomes public law thepublic policy issue becomes bureaucratized and

enters the public policy implementation stage(Buchholz, 1988).

Corporate political activity during the public policyformulation stage

Our study focuses on corporate political activityduring the policy formulation stage of the 1997Act. A federal tax policy issue typically enters thepublic policy formulation stage through commit-tee discussions within the US House of Repre-sentatives’ Ways and Means Committee or theSenate Finance Committee (Congressional Uni-verse, 2000) and ends when the final legislation ispassed (or defeated). The public policy formula-tion stage of the 1997 Act lasted approximately 6months (Congressional Universe, 2000).

Just as individual corporations develop strate-gies to enhance their economic power, they alsoselect and execute strategies designed to increasetheir political power, especially during the policyformulation stage (Suarez, 1998). Once a corpora-tion commits to political activity during this stage,its specific actions depend mainly upon the sub-stantive nature of the policy issue (Snyder, 1992)and the level of political conflict (Grier et al., 1994;Suarez, 1998).

During the public policy formulation stage,corporations advance their goals by undertakingactivities such as testifying at congressional hear-ings, lobbying public policymakers, and makingpolitical action committee (PAC) and individualcampaign contributions (Buchholz, 1988; Mack,1997). Corporations testify at congressional hear-ings and lobby public policymakers to communicatetheir views to legislators regarding proposed legis-lation. These activities provide a corporation withthe opportunity to provide legislators with theirreasons for adopting a particular position on pro-posed legislation and to try and influence policyoutcomes (Hillman and Hitt, 1999; Mack, 1997).Because legislators have limited amounts of time todevote to policymaking, corporate political activityresearch views campaign contributions as the pri-mary activity that can be used to gain the access tolegislators that is required to influence policy.

In inter-social interest and some types of inter-firm conflict, corporations may augment their

4 While the fluidity of actual policy-making raises questions

concerning the discreteness of each stage, the life cycle model is

viewed as a useful tool in the analysis of corporate political

activity (Getz, 1993, p. 247).

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 569

political activities through coordination with tradeassociations and/or advocacy coalitions (Hojnacki,1998; Mack, 1997; Mizruchi, 1992; Suarez, 1998).Trade associations typically represent a broadspectrum of industry membership. These types ofassociations (e.g., the American Institute of Certi-fied Public Accountants) are most likely to bepolitically active during policy formulation whenits members have similar concerns over proposedlegislation (Mack, 1997; Hillman & Hitt, 1999).Advocacy coalitions are most likely to form whenmultiple industries and/or firms reach agreementon the need for specific policies or legislation to bepassed (Mack, 1997; Suarez, 1998). For example,during the debate over private securities litigationreform both an inter-social interest and an intra-industry coalition were formed. Public accountingfirms, investment banking firms, and many cor-porations generally agreed on the need for secu-rities liability reform. Over 1400 organizationsjoined an inter social-interest coalition named theCoalition to End Abusive Securities Suits (Fritsch,1995). Similarly, public accounting firms agreed onthe need for reform and an intra-industry coalition,The Accountants Coalition, was also organized(Journal of Accountancy, 1996).

Researchers have been particularly interested inthe potential link between campaign financing andlegislative decision-making. The relationship isdifficult to untangle because of the complexitiesinherent in the campaign finance system and in thelegislative process (Grenzke, 1989a, 1989b). Priorresearch has studied PAC contributions madefrom a variety of industries including defense(Fleisher, 1993), financial services (Kroszner &Stratmann, 1998; Romano, 1997), and trucking(Frendreis & Waterman, 1985). These studiesmodel both legislators and interest groups usingpluralist assumptions. In this context, corpora-tions and coalitions use PAC contributions strate-gically in an attempt to influence the legislatorsmost important to them (Grier, Munger, & Tor-rent, 1990). Prior empirical work that is groundedin neoclassical economic theory has generallyfound that corporate PAC contributions are morelikely to be given to legislators of the majorityparty, higher-ranking legislators, and members ofcommittees with jurisdiction over the policy issues

of concern (Grier et al., 1990; Romano, 1997;Kroszner & Stratmann, 1998).

Taxation and corporate political activity

Prior research shows that tax policy affects thebusiness decisions of corporations (Vines & Moore,1996) and that corporations engage in inter-socialinterest (Jacobs 1987, 1988; Quinn & Shapiro,1991) intra-industry (Suarez, 1998), and inter-firm(Hulse, 1996; Suarez, 1998) political conflict inhopes of reducing their firms’ overall tax burden(Mizruchi, 1992).

Quinn and Shapiro (1991) examined severalhypothesized relationships among taxation, redis-tribution, politics, and business/class power. Usingfour alternative empirical models, they found strongsupport for the presence of inter-social interestpolitical conflict between business and labor. Ofparticular note, they found a significant relation-ship between increases in the general level of cam-paign financing from the corporate sector andlower overall corporate tax burdens.

Freed and Swenson (1995) investigated cam-paign contributions made by US corporations totax-writing members of the US Congress prior tothe passage of the Economic Tax Recovery Actof 1981 and the Tax Reform Act of 1986. Theirstudy, developed within a marginalist economicframework, hypothesized that a corporation’scampaign contributions to tax writing legislatorswas determined by the firm’s cost/benefit analysis.Using firm specific data for approximately 400 taxpaying firms for each tax act, Freed and Swensonregressed two related measures of firm campaigncontributions against measures of firm size,industry concentration, and expected benefits ofthe tax legislation. Their results were supportive ofthe model, with measures of industry specific taxaccounting rules related to the Tax Reform Act of1986 having the largest impact on contributions.

Although not using the framework of corporatepolitical activity theory, Hulse (1996) investigatedthe stock market reaction to firms’ successful taxcode restructuring efforts. Hulse utilized an eventsstudy methodology to estimate the stock marketreaction individual firms experienced when rifle-shot rules benefiting their firms were included in

570 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

the Tax Reform Act of 1986. While Hulse (1996)emphasized the secrecy surrounding these types ofprovisions and the efforts of lobbyists to obtaintax code restructuring for their clients, he did notinvestigate the political strategies used by cor-porations in their restructuring efforts.

Northcutt and Vines (1998) studied changes infinancial accounting methods used by corpora-tions that were characterized by advocacy groupsas ‘‘corporate freeloaders’’. Their sample con-sisted of corporations that were singled out andcriticized by the Citizens for Tax Justice becauseof the corporations’ extremely low effective taxrates. Northcutt and Vines (1998) found that cor-porations responded to this political scrutiny inlater reporting periods by choosing income-decreasing accruals with low book-tax conformity,thereby increasing their reported effective tax rate.By examining the interplay between advocacygroups and corporate interests, this study providesan example of inter-social interest level research.

Suarez (1998) reported the findings of her casestudy of the US possessions’ tax credit (e.g., creditsfor maintaining manufacturing facilities in PuertoRico). She analyzed relevant public informationregarding political action committee contribu-tions, congressional hearings, and company reports.Suarez argued that when a tax policy issue ismutually beneficial to a group of firms or indus-tries, coalitions and trade associations coordinatepolitical activities in order to maximize theireffectiveness. However, when a tax policy issueaffects these groups differently, coalition and tradeassociation alliances recede and fragmented lob-bying emerges. Suarez concluded from her casework that corporations used collective and frag-mented political alliances in attempts to protectthe possessions’ tax. In particular, she assertedthat the introduction of proposed changes that haddifferential impacts on the electronic and pharma-ceutical industries collapsed coalition efforts andresulted in an increase in inter-firm political conflict.

Implications for the case study

The two sections that follow describe our researchmethod and the results of our case analysis con-cerning corporate political activities during the

6-month policy formulation stage of the TaxpayerRelief Act of 1997. Our study of prior research onthe accounting/state relationship, corporate poli-tical activity, and tax accounting helped us iden-tify several contributions that our research canmake to our collective understanding of the devel-opment of US tax accounting laws. First, we areinterested in identifying and investigating cor-porations that undertook political activitiesregarding the 1997 Act. We argue that these cor-porations view the state as a contracting partyover which they can exert influence. Thus, con-trary to the microeconomic-based, strict pluralistassumptions common in empirical tax accountingresearch, tax accounting rules are not necessarilyexogenous to the firm. In other words, corporateinterests play a substantive role in the develop-ment of tax accounting policy.

Second, in addition to addressing pluralistassumptions, we also are able to extend researchon corporate political activity. As recommendedby Hillman and Hitt (1999), we investigate anddocument the specific behaviors that firms use toinfluence legislation. Further, we document andanalyze corporate behaviors at three differentlevels of political competition.

Third, evidence that corporations exert influencein the development of tax policy is not necessarilyinconsistent with pluralist theory. In order toassess the applicability of strict pluralist assump-tions, we must examine the intensity and extent ofcorporate political activities. Intense and extensivepolitical activities made by corporations duringthe six-month period bolster arguments that allinterest groups do not have similar opportunitiesto influence accounting policy. The more thatlobbying and campaign contributions allow cor-porate interests to dominate the public policy for-mulation process, the less applicable strictpluralist assumptions are in the study of policydevelopment (Clawson et al., 1998). Thus, this casestudy provides a basis from which to reflect on theappropriateness of any pluralist-based theory toaccounting policy research. The nature and levels ofpolitical conflict that we analyze can shed light onthe importance of incorporating political economymore prominently in the study of tax accountingpolicy.

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 571

Research method

Our study followed a four-step empirical case-based research approach (Ryan et al., 1992, pp. 113–129). First, we analyzed the provisions of the 1997Act, and publications, press releases and otherdocumentation associated with the 1997 Act.These data were gathered through a repetitivesearch of electronic databases (ABI-Inform, Busi-ness Index, Congressional Universe, Firstsearch,Wall Street Journal Index, and multiple searchengines for the World Wide Web). Our searchproduced a wide variety of public documentsrelated to the 1997 Act, including published tradearticles, transcripts of congressional hearings,legislative histories of the proposed law, popularpress articles, and newspaper columns.

From this search, we identified three sets oftaxpayers for further analysis. These taxpayerswere selected because each corresponded mostclosely with a specific level of political conflict(Buchholz, 1988; Mack, 1997). The insuranceindustry was concerned with numerous provisionsin the 1997 Act. Their unified efforts provided anexample of inter-social interest political conflictbecause the industry attempted to influence anumber of tax law changes within a constrainedresource setting. Thus, to the extent they weresuccessful, their efforts affected the overall dis-tribution of the tax burden. The airline industrydisplayed intra-industry political conflict overthe airline tax provisions. Major airline carriersand regional carriers strongly disagreed over thestructure of the tax. Amway Corporation andSammons Enterprises were selected as glaringexamples of inter-firm political conflict becausethese corporations sought specific, narrowly tar-geted, tax relief.

In the second step of our research process wegathered lobbying reports and political actioncommittee contribution data for the taxpayersunder study for the period relevant to the policyformulation stage of the 1997 Act. The data werecollected to provide additional primary sourceinformation regarding the political activities ofthese taxpayers and to corroborate the informa-tion we gathered from secondary sources. Thelobbying and political contribution activities rele-

vant to the public policy formulation stage of the1997 Act occurred between the times the 1997 Actwas originally introduced (as the Revenue Recon-ciliation Act) during January 1997 until its passageon August 5, 1997 (Congressional Universe, 2000).Lobbying reports are filed with the Clerk of theHouse of Representatives and the Secretary of theSenate on a semi-annual basis. Therefore, we gath-ered reports for Amway Corporation, SammonsEnterprises and for all insurance and airline rela-ted firms and associations for the January–June1997 reporting period. These mandatory filings arerequired of all organizations engaged in lobbyingefforts. The filings specify the legislation beinglobbied, the cost of lobbying activities, whether ornot the filing was made by a lobbying firm, andthe organization financing the lobbying activity.

Next we gathered PAC contribution data foreach firm that reported lobbying activity asso-ciated with the 1997 Act. Lobbying and makingfinancial contributions are firms’ and associations’most visible and effective activities during the pol-icy formulation stage of proposed legislation(Hillman & Hitt, 1999; Mack, 1997). Politicalaction committee contributions are reported to theFederal Election Commission and compiled by theCenter for Responsive Politics (2000). These con-tributions are reported by election cycle. Wegathered contribution data for the 105th Con-gressional election cycle because the 1997 Act waspassed by this congress.

The third step in our research was to use theframework provided by our theoretical work toanalyze and interpret the information that wasgathered in steps one and two (Grier et al., 1994;Mitnick, 1993; Suarez, 1998). This analysis pro-duced evidence of the taxpayers’ interests in the1997 Act and their motivation for undertakinglobbying and political campaign contributionactivities. Political campaign contribution datareported firms’ contribution amounts that weredonated to each senator and house member but,of course, did not provide direct information on thereason for the contribution. Therefore, we appealedto prior research on PAC contributions to guideour empirical work (Romer & Snyder, 1994;Snyder, 1992; Wright, 1985). In the two cases inwhich multiple firms were involved (insurance and

572 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

airlines), we developed and tested an empiricalmodel to explain the campaign contributionsmade to Senate and House members by thesefirms’ political action committees.

As we mentioned in the previous section, priorresearch models firms’ PAC contribution decisionsthrough a neoclassical economics perspective andhypothesizes that firms allocate contributions tolegislators who are in the best positions to leadefforts to have Congress adopt the corporation’sfavored legislation (Grier et al., 1994). According toprior studies, these are most likely to be legislatorswho hold leadership positions and/or who aremembers of committees with jurisdictional author-ity over relevant legislation. Thus, the political con-tributions that were particularly relevant to the1997 Act were contributions given to congres-sional leaders and/or members of the House Waysand Means Committee or the Senate FinanceCommittee.

Prior PAC research also states that legislatorswho hold influential positions may not be equallylikely to attempt to provide the desired legislation(Grier et al., 1994; Snyder, 1992). This differentialin legislators’ willingness to support a corporation’sspecific policy preferences is because legislators areultimately concerned with re-election. Therefore,their ability to support legislation that is importantto PAC contributors is constrained by their ownpolitical ideology and their voting constituents’legislative preferences (Grier et al., 1994; Snyder,1992).

Our PAC contribution regressions controlledfor political ideology, constituent preferences, andindustry-related committee membership in orderto improve the reliability of our tests of the rela-tionship between firm PAC contributions and leg-islator influence over tax policy. We performed fourregressions, two regressions for each of the caseswith multiple firms (insurance and airlines) for eachlegislative body (House and Senate). The generalspecifications of the empirical models we testedwere:

PAChouse ¼ b0 þ b1VOTE þ b2LEADTEAM

þ b3INDCOMM þ b4TAXCOMM

PACsenate ¼ b0 þ b1VOTE þ b2LEADTEAM

þ b3INDCOMM þ b4TAXCOMM

þ b5ELECT

þ b6ELECT�INDCOMM

þ b7ELECT� TAXCOMM

Where:

PAC= a

legislator’s total receipt of PACcontributions from eitherinsurance or airline industryPACs that lobbied the 1997Act (100 observations for theSenate and 437 for the Houseof Representatives).VOTE= t

he legislators’ cumulative votingrating by the U.S. Chamberof Commerce (range=0-100).The higher the rating, the morefavorable their view of thelegislator’s voting record.LEADTEAM=1

if the legislator holds aleadership position; 0 otherwise.INDCOMM= 1

if the legislator is a member ofa committee that has jurisdictionover legislation relatedspecifically to a firm’s industry(not tax-related); 0 otherwise.TAX COMM=1

if the legislator is a member ofthe legislative committee that hasjurisdiction over tax legislation.ELECT= 1

if the legislator is a Senator andis up for reelection during thenext election cycle; 0 otherwise.This variable is used only in theSenate regressions.TAX COMM is our primary test variablebecause its significance shows that a relationship

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 573

exists between corporate PAC contributions and alegislator’s ability to affect tax accounting changesthat are preferred by those corporations. All of theother variables controlled for non-tax-related fac-tors that may explain variance in contributionsmade by insurance or airlines firms to legislatorsduring the 105th congressional election cycle.VOTE was included in the model to control forpolitical ideology and constituent voting pre-ferences. As expected, VOTE is highly correlatedwith legislators’ political party membership (i.e.,Republican legislators possess higher pro-businessvoting ratings than Democrats). LEADTEAMand INDCOMM were included to control forother legislator attributes that could explain PACgiving. For LEADTEAM to be set equal to one, alegislator must have served the 105th Congress asMajority Leader, Minority Leader, MajorityWhip, Minority Whip or Chair of the applicabletax or industry committee.

For the House of Representatives, INDCOMMrepresented membership on the Commerce Com-mittee in the insurance regression and it repre-sented membership on the TransportationCommittee in the airline regression. For the Sen-ate, INDCOMM represented membership on theBanking, Housing, and Urban Affairs Committeein the insurance regression and it representedmembership on the Commerce, Science, andTransportation Committee in the airline regression.These committees have jurisdiction over legisla-tion that is most vital to each respective industry(Congressional Universe, 2000).5

The ELECT variable is added to the Senateregressions because US senators serve 6-year,staggered terms, resulting in only one-third of theSenate incumbents being up for reelection eachtwo-year election cycle. This variable is importantbecause PAC contributions to individual senatorstend to increase during their election year and,

-

-

therefore, should be controlled for in the regressions.All US House of Representatives incumbents areup for reelection every 2 years, thus the ELECTvariable is not needed. Because of the potentialinteraction between ELECT and TAXCOMM andbetween ELECT and INDCOMM, we includeinteraction terms in the Senate regressions.

We argue that a statistically significant relation-ship between PAC and TAXCOMM, after con-trolling for these other factors, provides evidencethat corporate interests view the state as a negoti-able contracting party when developing tax stra-tegies. In this particular case, statistical significanceof TAXCOMM will support our contention thatinsurance and airline firms used their resourceendowments to their advantage to make PACcontributions that enabled them to have access toand influence over the determination of taxaccounting law during the policy formulationstage of the 1997 Act. Statistical significance doesnot disprove pluralist theory, but it does providesupport for increasing the attention given to thepolitical economy aspects of accounting policy.We report parameter estimates to indicate thedollar effect of each independent variable on thedependent variable.6

5 Given our definitions for LEADTEAM, TAXCOMM and

INDCOMM, the chairs of TAXCOMM and INDCOMM were

included in the LEADTEAM variable. We performed sensitiv

ity analyses of our results leaving these chairs out of LEAD

TEAM. The results presented in the paper were not changed

when omitting committee chairs from the LEADTEAM

variables.

6 We recognize that the corporate taxpayers we are studying

could be lobbying Congress for reasons other than the 1997

Act. We thoroughly explored Congressional Universe for com-

mittee reports, testimony and bills of interest to the airline and

insurance industry before the House Ways and Means com-

mittee and/or the Senate Finance Committee during the time

period in question. Our search did not turn up any other bills

pertinent to the airline industry. However, Medicare legislation

was before the House Ways and Means committee at the same

time as the tax legislation. As a sensitivity check, we split the

House Ways and Means Committee into two variables. One

variable was coded ‘‘1’’ for House Ways and Means committee

members who were on the Health Subcommittee, the other

variable was coded ‘‘1’’ for House Ways and Means members

who were not on the Health Subcommittee. Our reasoning is

that if the PAC contributions were being made only to influ-

ence Medicare legislation, we would expect to see a significant

result for the members who were on the Health Subcommittee

versus. those House Ways and Means members who were not

on the Health subcommittee. This analysis showed that both

variables were highly significant (P-value=0.000), and the

parameter estimates were similar. We suggest that this is evi-

dence consistent with our argument that these PAC Contribu-

tions were made, at least in part, to influence the tax bill.

574 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

Fourth, after completion of all of our analyses,we organized our findings in order to present astructured examination of the corporate politicalactivities of each set of taxpayers. The analyses arepresented in the following section. First, we discussthe tax issues and provisions of interest to the setof taxpayers. Second, we discuss our findingsregarding lobbying and political campaign con-tribution activities.

Corporate political activity and the Taxpayer

Relief Act of 1997

Inter-social interest corporate political activity: theinsurance industry

Tax issuesThe insurance industry engaged in corporate

political activity on a number of complex tax issuesthat either directly affected the tax burden of theindustry or affected demand for their products. Oursearch of industry publications and press releasesenabled us to identify the major 1997 Act provisionsof interest to the industry as well as its position onthese provisions. Table 1 summarizes these issues.

The insurance industry favored a change in thetreatment of foreign sourced investment income.Subpart-F rules require financial services companies(e.g. insurance, banks and securities firms), but

not manufacturing firms, to immediately recognizeforeign-earned investment income even if thefunds have not been repatriated to the parent cor-poration (Brostoff, 1997b). The insurance indus-try, along with a coalition of the other affectedindustries argued that these rules impeded theirglobal competitiveness (Brostoff, 1997f).7

Insurance industry publications documented theireconomic and political interest in the highway taxprovisions included in the 1997 Act. A 4.3-cent-per-gallon tax had originally been enacted in 1993as a deficit reduction measure. However, a coalitionof industries (including insurance and construc-tion) lobbied to have the revenue re-directed to theHighway Trust Fund (Winston, 1997). Increasedfunding for federal highway programs wouldreduce automobile accidents and insured losses(Brostoff, 1997d).8 The insurance industry’s coali-tion strategies concerning the gasoline tax and the

Table 1

Insurance industry 1997 Tax Act provisions

Tax issue

Insuranceindustry position

1997 Act change

Sub-part F Rules required tax on non-repatriated foreign

source investment income for financial services firms

FAVORED

ELIMINATION OF TAX

Included one year reprieve

to the Sub Part F rules

Reallocation of 4.3 cent federal gas tax from deficit reduction

to the Highway Trust Fund

FAVORED THIS CHANGE

Provision was included in ActRestriction of general borrowing interest expense based on

the existence of unborrowed cash values on Corporate

Owned Life Insurance (COLI)

OPPOSED RULE, HOWEVER

SOUGHT CLARIFYING

LANGUAGE TO LIMIT

REACH OF RULE

Limitation on interest expense

from general borrowing was

restricted, but it only applied to

mortgage-owned life insurance

Proposed changes in NOL carryover rules from

3 back and 15 forward to 2 back and 20 forward

OPPOSED RULE

New NOL carryover rules wereenacted. Special exceptions were

allowed for presidentially declared

disaster areas

7 The 1997 Act passed by both houses of Congress included

a one-year reprieve from Subpart-F rules, however this provi-

sion was one of two vetoed by President Clinton under his line-

item veto privileges (Congressional Universe, 2000). The

Supreme Court later ruled the line-item veto law unconstitu-

tional; and the rule change was enacted (Congressional Uni-

verse, 2000).8 Their efforts were deemed successful because an amend-

ment to the 1997 Act was added to divert the 4.3-cent-per-gal-

lon fuel tax from deficit reduction to the Highway Trust Fund

(Brostoff, 1997d).

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 575

Subpart-F rules is consistent with expectationsderived from corporate political activity researchbecause of the inter-social interest nature of theseprovisions (Mack, 1997; Mizruchi, 1992; Suarez,1998).

The insurance industry was also concerned withthe 1997 Act provisions affecting corporate ownedlife insurance (Kerley, 1997b). While insurancepremiums are not deductible (if the payee is thebeneficiary) and death benefits are not taxable,any interest expense related to general borrowingof funds to purchase these policies was deductibleprior to the 1997 Act. Congress’ interest in closingthis loophole caused two major concerns. First,some insurance companies (along with FannieMae) were planning to exploit the interest deduct-ibility and opposed changes to the tax rule(Kerley, 1997b). Second, other companies fearedthat the rule changes would be drafted toobroadly.9

Finally, the insurance industry was also opposedto a change to the net operating loss (NOL) car-ryover rules. Prior to the 1997 Act, a NOL couldbe carried back 3 years and forward 15 years. The1997 Act changed the carry back period to only 2years, while the carry forward period was exten-ded to 20 years. The insurance industry, both theAlliance of American Insurers and the AmericanInsurance Association, argued that this changewould be particularly harmful to property andcasualty insurers that suffer catastrophic losses(Brostoff, 1997e). While the industry was unableto halt the rule change, an exception that allowedthe old rule to apply was made for losses thatoccurred in presidentially declared disaster areas.10

Lobbying and political action committee activitiesThrough a manual search of lobbying reports,

we found 112 reports associated with insurancelobbying activity regarding the 1997 Act. Thesereports were filed either by insurance corporations

or associations or by lobbying firms that repre-sented the insurance industry. Our analysis of thereports documents that the 50 insurance compa-nies that lobbied this bill spent approximately$15.2 million on lobbying expenses in the first 6months of 1997. In addition, 16 insurance industryassociations reported an additional $6.4 million oflobbying expenditures during this period.

These lobbying expenditures were supplementedby campaign contributions to legislators (Center forResponsive Politics, 2000) and ‘‘soft money’’ con-tributions made directly to political parties (Com-mon Cause, 2000). In total, the insurance industrymembers who lobbied during the formulation stageof the 1997 Act made PAC contributions of $5.0million to the campaigns of US House membersand $1.9 million to the campaigns of US Senators(Center for Responsive Politics, 2000). In addition,‘‘soft money’’ contributions of $2.8 million weremade by the insurance industry during this timeperiod (Common Cause, 2000). For this time per-iod, the insurance industry’s soft money contribu-tions were more than that of any other industry(Common Cause, 2000). Table 2 summarizes thecorporate political activities of the insurance indus-try. In total, we documented over $30 million ofcorporate political activity expenditures by thisindustry.

Although soft money contributions cannot bedirectly linked to individual legislators, PAC con-tributions are made to individual congressionalcampaigns. We examined the relationship betweeninsurance PAC contributions and legislator mem-bership on either the House Ways and MeansCommittee or the Senate Finance Committee bydeveloping and testing an empirical model thatcontrolled for other factors that could influence

-

-

10 The insurance industry also expressed concerns over pro

posed changes that affected individual taxpayers. This was

because the provisions, if adopted, could have business reper

cussions. These issues included privatization of social security

(Brostoff, 1997a), increased deductibility of health insurance

premiums for self-employed taxpayers (Kerley, 1997a), changes

in estate taxes (Kerley 1997a; Brostoff, 1997c; King, 1997), and

decreases in the capital gains tax rate (Kerley, 1997a). While

not explored further in our study, this further demonstrates the

extent to which tax-related issues affect corporate business and

tax-related political activities.

9 The industry was able to obtain clarifying language in the

provision that limited this provision to non-employees. Further

the tax rule was written such that it does not apply to coverage

of former employees, officers and directors (Brostoff, 1997b).

Thus, interest expense for general borrowing will not be dis-

allowed as a result of unborrowed policy cash values, except for

the case of mortgage-owned life insurance.

576 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

insurance PAC giving. The regression results for theHouse of Representatives are shown in Table 3and the results for the Senate are shown in Table 4.Each table provides descriptive statistics for eachvariable in the model and ordinary least squaresregression results.11 Panel A of each table presents

descriptive statistics as well as the t-test results ofthe differences in the mean PAC contribution foreach level of the dichotomous independent vari-ables. The reported means indicate the dollarimpact of each of the independent variables. PanelB of each table presents the multivariate OLSregression results for the PAC contribution model.We also present descriptive data regarding legisla-tors’ political party affiliation but this variable isnot included in the regressions because it is highlycorrelated with the legislators’ voting records. Theresults provide strong evidence that the insur-ance industry allocated its PAC contributions to

Table 2

Insurance industry summary of corporate political activities

1/1/97–6/30/97 1997 Tax Act lobbying expendituresa

Insurance Companies (n=50)

$ 15,189,740Insurance Industry Associations (n=16)

6,362,646Total Lobbying Expenditures by Insurance

Industry related to 1997 Tax Act, for first

Six months of 1997

$ 20,512,993PAC contributions to individual house and senate members by insurance companies and

insurance industry associations who lobbied for 1997 Tax Act: 1998 election cycleb

House Members

$ 5,005,851Senate Members

$ 1,942,667Total PAC Contributions

$ 6,948,518‘‘Soft money’’ contributions to political parties by insurance industryc

To the Democratic Party

$ 902,161To the Republican Party

$ 1,942,667Total ‘‘soft money’’ contributions

$ 2,841,860a Lobbying reports are filed with the Secretary of the Senate and the Clerk of the House of Representatives as required by the

Lobbying Disclosure Act. These reports include information about the specific bills that were being lobbied. We only included

amounts from lobbying reports that included the 1997 Tax Act as one of the lobbying targets. Note: in some cases the reported

amount was ‘‘<$10,000’’; because the act does not require the amount to be reported if it is less than $10,000. For these reports we

included the amount as $10,000. Therefore our totals are slightly overstated (there were 5 insurance companies that fell into this

category).b Reports filed with the Federal Election Commission and compiled by Federal Election Commission Information, Inc. for the

campaign cycle 1997–1998. Only PAC Contributions by insurance companies and industry associations who also reported lobbying on

the 1997 Tax Act are included.c Reported contributions are for the 12-month period ending 12/31/97. Source: Common Cause (2000).

11 There were a number of legislators who did not receive any

PAC contributions. Therefore, we also analyzed both the

insurance and airline data using a TOBIT model to take into

account the truncated nature of the dependent variable. The

TOBIT model results were virtually identical, therefore we have

only reported the OLS results here.

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 577

Table 3

Insurance industry PAC contributions to the US House of Representatives

578 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

Table 4

Insurance industry PAC contributions to the US Senate

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 579

legislators who held positions on the committeesresponsible for drafting and overseeing the revisionof the 1997 Act. In both House and Senate regres-sions, the test variable, TAXCOMM, is positiveand highly significant. In addition, all of the con-trol variables are both positive and significant.Thus, during the development of the 1997 Act, theinsurance industry appeared to allocate its PACcontributions to legislators who are responsiblefor developing economic and tax policies thatdirectly affect the corporate interests of insurancecompanies.

Intra-industry corporate political activity:the airline industry

Tax issuesOne of the major revenue increasing compo-

nents of the 1997 Act was the reinstatement of atax on airline tickets. This tax is used to fund theAirport and Airway Trust Fund, which providesmost of the funding for the Federal AviationAuthority (FAA). It was expected to raise $33billion over 5 years (Barker, 1997). The originaltax, a 10% surtax on domestic flights and a $6 perperson levy on international flights, expiredDecember 31, 1996. While the final structure ofthe tax was debated, the 10% surtax was tem-porarily reinstated for 6 months of 1997 (Prac-tical Accountant, 1997). Ultimately, the 1997 Actprovided a 10-year extension to a modified tax.The changes in the airline tax are depicted inTable 5.

This intra-industry conflict over whether andhow to fund the FAA pitted seven major airlines(American, Continental, Delta, Northwest, TWA,United and USAir) against smaller, low-fare car-riers (e.g. Southwest and Alaska Air). Even in thisintra-industry level of political conflict, the majorairlines were in agreement on the policy issues andorganized the Coalition for Fair FAA Funding.This coalition proposed that the tax be convertedto a ‘‘head’’ tax, with a per-passenger charge, asopposed to a percentage of the ticket price. TheCoalition’s proposal shifted approximately $600million of the tax burden from the major airlinesto the budget carriers (Phillips, 1997).

As theory predicts, the intra-industry nature ofthis conflict precluded the airline industry’s tradeassociation, the Air Transport Association, fromparticipating in the tax revision debate (Dono-ghue, 1997). However, hearings held by the HouseTransportation and Infrastructure Subcommitteeon Aviation on February 13, 1997, and the SenateFinance Committee on May 5, 1997, includedtestimonies by representatives of both coalitionairlines and low-cost air carriers.

The major airlines argued that their customerscurrently paid more than their fair share of FAAcosts, arguing that the costs were more related tothe number of passengers and segments flown(Congressional Universe, 2000). On the otherhand, lower fare airlines argued that a strictly userfee tax (as proposed by the major airlines) woulddevastate their business. Daniel Wolf, the pre-sident of a small, regional airline testified that the

Table 5

Airline tax proposals

Prior Tax (expired 12/31/96, reinstated until 9/30/97)

10% tax on airfaresMajor airline coalition proposal

$6/departure international flights$4.50/originating passenger

$2/seat on aircrafts with >70 seats

$1/seat on aircrafts with <71 seats

$.0005/nonstop passenger mile flown

1997 Taxpayer relief act

Fully phased-in tax7.5% tax on airfaresa

$12/departure and arrival on international flights

$3/flight segment

a Also applies to payments from credit card companies for frequent flyer miles.

580 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

proposed user-fee would increase the average tax/ticket for his customers by 54% in a highly fare-sensitive market. He also argued that the FAA’smost expensive equipment was located at large air-ports that were seldom, if ever, used by the smallregional carriers (Congressional Universe, 2000).12

Their fragmented intra-industry political activ-ity produced mixed results. This is often the casein intra-industry political conflict (Mizruchi, 1992).When corporations in an industry seek conflictinglegislative changes, the fragmentation of the lob-bying efforts can provide an opportunity for legis-lators to resist accommodating corporate demandsand adopt legislation that makes both sides of thelegislative debate worse off (Suarez, 1998). Whilethe major airlines were able to restructure the per-centage tax, with the ten percent tax being loweredto seven and one-half percent and a $3 per flight-segment added, overall the industry absorbed anadditional $4 billion in tax (over 5 years) com-pared to if no changes were made to the tax(Gatty & Blalock, 1997). Nevertheless, the WallStreet Journal’s cover story the day agreementon the 1997 Act was reached listed the coalitionairlines in its ‘‘big winners’’ category and smallairlines in its ‘‘big losers’’ category (Wessel &Georges, 1997).

Lobbying and political action committee activitiesIn our review of lobbying reports, we found

that the coalition airlines reported lobbyingexpenses of $4.96 million during the policy for-mulation stage of the 1997 Act, almost five timesthe amount reported by non-coalition airlines.13

The coalition airlines also made ‘‘soft money’’contributions during the 105th congressionalelection period that totaled $2.5 million while thenon-coalition airlines contributed $207,000 insoft money to the two major political parties(Common Cause, 2000). In total, the airlineindustry members who lobbied during the for-mulation stage of the 1997 Act made PAC con-tributions of approximately $566,000 to thecampaigns of House members and $375,000 tothe campaigns of Senators (Center for ResponsivePolitics, 2000). Table 6 summarizes the corporatepolitical activities of the airline industry. In total,we documented over $9.5 million in corporatepolitical activity expenditures by the airlineindustry.

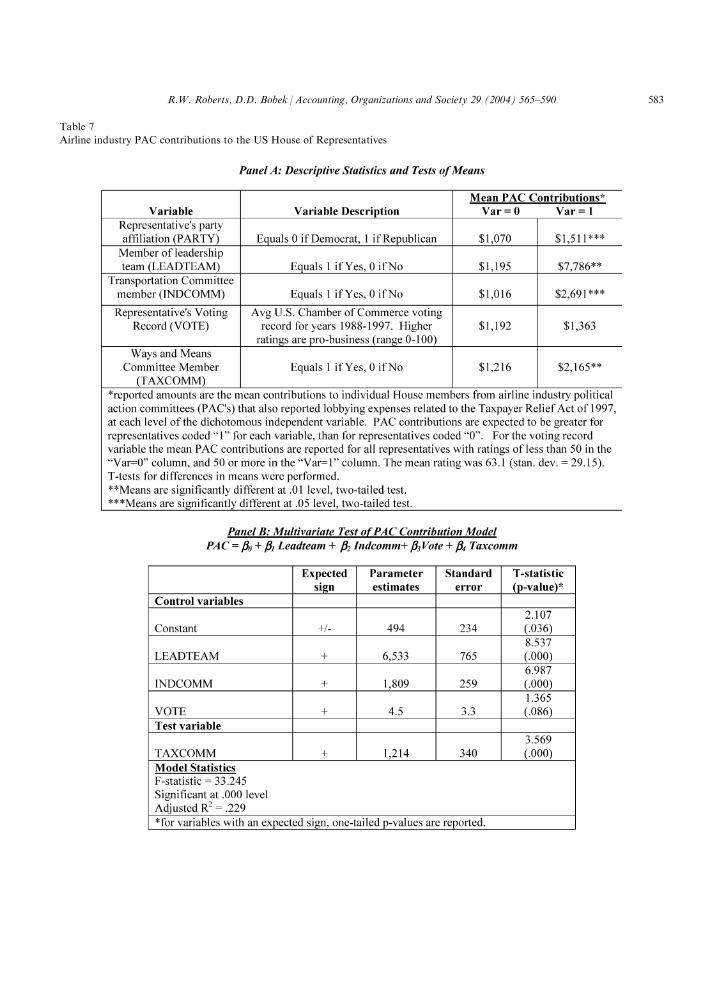

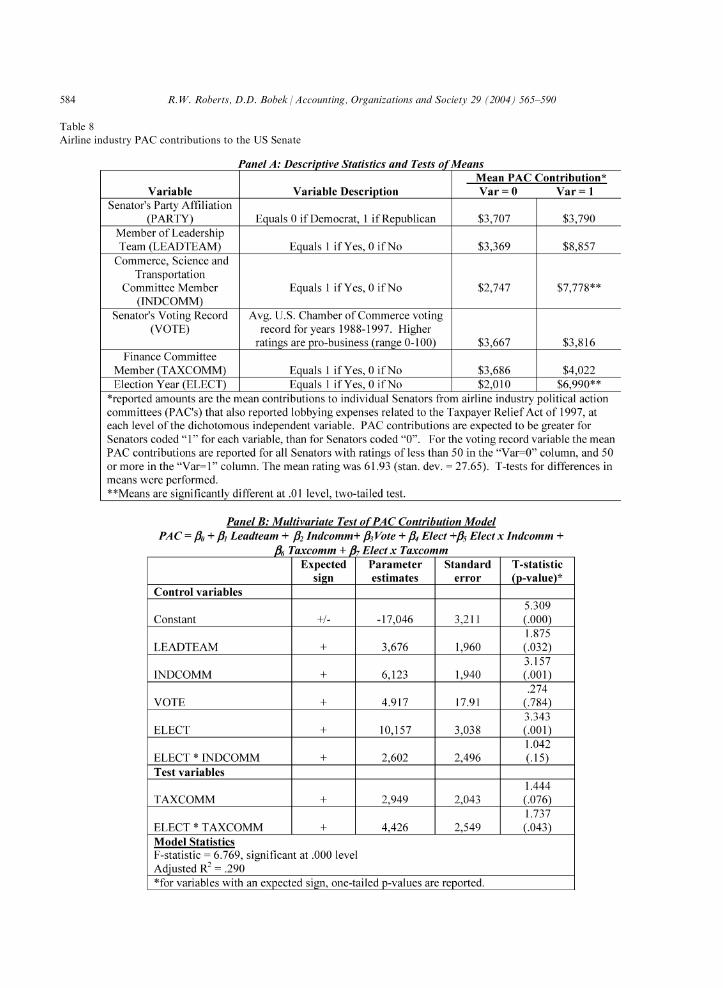

We tested the relationship between airline PACcontributions and legislator membership on eitherthe House Ways and Means Committee or theSenate Finance Committee using the same methodemployed for insurance contributions. The regres-sion results for the House of Representatives areshown in Table 7 and the results for the Senate areshown in Table 8. Panel A of each table presentsdescriptive statistics as well as the t-test results ofthe differences in the mean PAC contribution foreach level of the dichotomous independent vari-ables. The reported means indicate the dollarimpact of each of the independent variables. PanelB of each table presents the multivariate OLSregression results for the PAC contribution model.

As detailed in the tables, the results provideevidence that the airline industry allocated its PACcontributions to legislators who held positions onthe committees responsible for drafting and over-seeing the revision of the 1997 Act. In the Houseregression, Table 7, the test variable, TAXCOMM,is positive and highly significant. In addition, thecontrol variables INDCOMM and LEADTEAMare positive and significant. In the Senate regres-sion, Table 8, the test variable, TAXCOMM, ispositive and marginally significant, and theELECT*TAXCOMM interaction term is shownto be positive and significantly related to the allo-cation of airline industry PAC contributions.INDCOMM and LEADTEAM are both positiveand significant in the Senate airline industryregression.

12 One factor that intensified the lobbying efforts and poli-

tical debate was the fact that the FAA did not have adequate

cost accounting data to identify the actual costs generated by

specific users (Congressional Universe, 2000). Therefore, the

decision on how and if to modify the tax had to be made with-

out adequate data. The General Accounting Office (GAO)

issued a report on the tax and on the Coalition’s proposals in

early 1997. They concluded that the concept of ‘‘directly char-

ging users for the cost of the FAA services they consume’’ is

attractive but it should not come at the expense of industry

competitiveness (Phillips, 1997).13 Eight non-coalition airlines reported lobbying expenses

during this time period. The total amount was less than $1

million, with Southwest Airlines making up $880,000 of the

total.

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 581

We also examined the mean PAC contributionsto gain additional insight regarding the significantinteraction term. Senators who were up forreelection and were members of the FinanceCommittee averaged $8973 in airline PAC con-tributions, while senators who were up for reelec-tion but not on the Finance Committee averaged$6,495 in airline PAC contributions. Thus, boththe Senate and House of Representatives data areconsistent with the argument that airline corpora-tions strategically made PAC contributions in

order to influence tax accounting policy during thedevelopment of the 1997 Act.

Inter-firm political conflict: Amway Corporationand Sammons Enterprises

Prior research suggests that individual corpora-tions use corporate political activities to influencelegislation directly linked to their own economicbenefit (Hulse, 1996; Mitnick, 1993). As would beexpected, during the policy formation stage of the

Table 6

Airline industry summary of corporate political activities

1/1/97–6/30/97 1997 Tax Act lobbying expendituresa

Coalition Airlines (n=7)

$ 4,967,532Non-Coalition Airlines (n=8)

<1,000,000Total lobbying expenditures by airline

Industry related to 1997 Tax Act, for first

Six months of 1997

$<5,967,532PAC Contributions to Individual House and Senate Members by airline companies who

lobbied for 1997 Tax Act: 1998 election cycleb

House Members

$ 565,840Senate Members

$ 375,306Total PAC Contributions

$ 941,146‘‘Soft money’’ contributions to political parties by airline industryc

To the Democratic Party

$ 1,666,850To the Republican Party

$ 986,702Total ‘‘Soft Money’’ Contributions

$ 2,653,552a Lobbying reports are filed with the Secretary of the Senate and the Clerk of the House of Representatives as required by the

Lobbying Disclosure Act. These reports include information about the specific bills that were being lobbied. We only included

amounts from lobbying reports that included the 1997 Tax Act as one of the lobbying targets. Note: in some cases the reported

amount was ‘‘<$10,00000 because the act does not require the amount to be reported if it is less than $10,000. For these reports we

included the amount as $10,000. Therefore our totals are slightly overstated (all but Southwest Airlines in the non-coalition airline

category reported expenses in this way. Most of the non-coalition lobbying was done by Southwest. They reported $880,000 of

lobbying expenses).b Reports filed with the Federal Election Commission and compiled by Federal Election Commission Information, Inc. for the

campaign cycle 1997–1998. Only PAC Contributions by airline companies who also reported lobbying on the 1997 Tax Act are

included.c Reported contributions are for the 6-month period ending 6/30/97. Source: Common Cause (2000).

582 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

Table 7

Airline industry PAC contributions to the US House of Representatives

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 583

Table 8

Airline industry PAC contributions to the US Senate

584 R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590

1997 Act, there were a number of individual compa-nies that engaged in political activities in an effortto shape the Act, with varying degrees of success.14

We identified two corporations, Amway Corpora-tion and Sammons Enterprises, as particularlynoteworthy examples of successful participants ininter-firm political conflict. These two corpora-tions were able to gain ‘‘rifle-shot’’ tax breaks inthe final days of debate over the tax bill. Theinclusion of these tax breaks appeared to be atleast partly a result of a pattern of political activityby these corporations that allowed them to gainaccess to decision-makers at this critical time ofdebate.

Amway undertook corporate political activitiesto argue for changes to the Passive ForeignInvestment Corporation (PFIC) rules. Amway wasconcerned that their publicly traded Asian sub-sidiaries might be characterized as PFICs. As aresult, their US investors would face punitive taxconsequences when disposing of their shares orwhen receiving certain types of distributions.15

They sought a change in the method for deter-mining whether a corporation qualified as a PFIC.This law change16 reduced the potential for PFICstatus for a ‘‘very limited class of United Statesinvestors in foreign corporations’’ (O’Donnell,1997) and was estimated to save Amway share-

holders $19 million (Nelson, 1998).17 In the notesto the financial statements for Amway’s foreignsubsidiaries, the PFIC rule change was noted andthe corporations stated that they did not expect tobe classified as a PFIC in the future.

On April 2, 1997, during the policy formulationstage of the 1997 Act, Amway Corporation and itsaffiliated donors executed a $1 million soft-moneycontribution to the Republican Party (CommonCause, 2000). Amway also reported lobbying onthe 1997 Act and their total lobbying expenditureswere $60,000. Because Amway’s corporate poli-tical activities focused on soft-money donations,we cannot directly link the donations to theirconcern with the PFIC provisions of the 1997 Act.However, in a Wall Street Journal article a lobby-ist for Amway stated that they were the party whopushed for the change in PFIC rules (Hitt, 1997).18

Sammons Enterprises had been working foreight years (Rubin, 1997) to obtain estate tax reliefwhich would allow its founder, Charles Sammons(who died in 1988), to leave his holdings in thecorporation to an employee stock ownership plan(ESOP). Under current law, he could not receivean estate tax deduction for doing so; therefore hecreated a charitable remainder trust instead.However, he left instructions for at least some ofthe assets to be transferred to an ESOP if the ruleswere changed (Rubin, 1997).

The 1997 Act included a rifle-shot provisionthat allowed for an estate tax deduction for ‘‘limited

14 Estee Lauder, TIAA-CREF and U.S. West all unsuccess-fully fought provisions that increased their tax bills. While large

corporations do have significant resources that can be used to

gain access to lawmakers, they do not operate in a vacuum.

Senator Kerry, who was identified as sympathetic to US West,

was quoted in the Wall Street Journal (Rogers, 1997), ‘‘It looks

like a special plea. . . You have to do it as if it was on the six

o’clock news.’’15 Instead of gains being treated as long-term capital gains

that are subject to more favorable tax rates, the gains would be

treated as if the amounts were ordinary income received ratably

during the period the shareholders held the shares. Further, the

IRS would charge shareholders interest as if they had failed to

pay tax on the amounts allocated to prior years (Amway Asia

Pacific, 1998 Annual Report).16 This change appeared for the first time in the Conference

Report (after the House and Senate bills had already been

debated and voted on). The Wall Street Journal reported that

Senator Lott considered raising the proposal in the Finance

Committee, but waited for research that showed a few other

firms would benefit.

17 Some reports estimated the tax break at $280 million (for

example, Hohler, 1997), however in a 1998 letter to the editor

of Mother Jones magazine, an Amway representative argued

that neither figure was appropriate, and that the $19 million

figure included the savings of four other companies (Mother

Jones Magazine, 1998).18 Democrats criticized the provision because it was not lis-

ted as one of the tax breaks eligible for a presidential line-item

veto, ’’. . .noting a retired Amway president and his wife gave

$1 million to the GOP in April. One Democrat says: ‘For

$100,000, you get a tax break that makes the list; for $1 million,

you get a break that stays off the list.’’’ (Wall Street Journal, 8/

5/97). The reason the provision was not eligible for line-item

veto was because, although it helped a handful of corporations,

it also served to restrict the method for determining PFIC

status for all non-controlled foreign corporations (O’Donnell,

1997).

R.W. Roberts, D.D. Bobek /Accounting, Organizations and Society 29 (2004) 565–590 585

transfers of qualified employer securities bycharitable remainder trusts to ESOP’s’’ (Lear,1997).19 This provision was so narrow it was on theline-item veto list (Hitt, 1997). However, it hadsupport from both Democrats (namely, the minor-ity leader, Daschle) and Republicans (House Waysand Means member Sam Johnson who introducedthe provision). President Clinton received additionalpressure not to veto the provision from Sammons’employees in Hot Springs, Arkansas (Rubin,1997).

Sammons Enterprises’ corporate political activityassociated with the provision appeared to be limitedto lobbying, both by employees of the firm and paidlobbyists (one, a popular former Republican Con-gressman from Texas (Rogers, 1997)). Four firmsreported lobbying expenses related to the 1997 Acton behalf of Sammons Enterprises totaling $1.4million (Center for Responsive Politics, 2000).Sammons family members contributed smallamounts to both Johnson and Daschle ($2000 each),but no PAC contributions or soft money contribu-tions were reported by Sammons or relateddonors.20

These two corporations appear to view thestate as a negotiable party as they make strategicbusiness and tax planning decisions. Tax account-ing laws, therefore, are an endogenous part ofthese decisions. The extent to which the firms’relationships with members of the state and itspolitical activities (e.g., donations, the hiring offormer legislators as key lobbyists) are not avail-able to all citizens provides a basis for argumentsthat question the applicability of strict pluralistassumptions.

Limitations in our case analysis

Our empirical findings are subject to severallimitations. We are cautious in generalizing ourconclusions beyond the three cases that were exam-ined. Our findings would be strengthened if wecould further isolate campaign contributions andrefine our empirical tests. In addition, our inter-firm political conflict analysis could be criticized asanecdotal, as no statistical results were provided.We argue, however, that our descriptive analysisof Amway and Sammons provides compelling evi-dence against a strict adherence to pluralistassumptions when studying the formulation ofpublic policy in general, and tax policy in parti-cular. Thus, we believe its inclusion in this paper iswarranted.

Conclusions and future research