The Politics of Agribusiness Looking Forward Russia and...

40

The Politics of Agribusiness Looking Forward Russia and Ukraine Prof. Dick Farkas, DePaul University 1

Transcript of The Politics of Agribusiness Looking Forward Russia and...

The Politics of Agribusiness Looking Forward

Russia and Ukraine

Prof. Dick Farkas, DePaul University1

Generic ChallengesCommon to Russia and Ukraine

�“Transition” �Legitimacy of institutions �Relationship of the STATE to the Ag

sector �Minimal trajectory toward technology

2

Politics of Agriculture: Ukraine

�Institutional credibility was nearly destroyed by Maidan; integrity of political roles lost �Ukraine has been unable to re-

conceptualize itself; boundaries, relationships and leadership �All foreign relationships are problematic

3

Reform could …

�Attract financing and investment �Stimulate change to fight large scale

corruption �Secure constitutional property rights for 7 million small farm owners �Guarantee transparency & ensure buyers &

sellers have needed information �Reduce admin. costs of land transactions �Ensure equity, fairness, property rights through

appeal and dispute resolution mechanisms

4

Costs of No Reform

“The lack of transparency and the commitment to develop dynamic farmland markets reduces development perspectives for farmers, land owners, and local communities.” FT

�Limits financial instruments / mortgages �Fails to win over skeptical Ukrainian people

and international partners that the leaders are committed to reforms & the stimulation they generate.

5

Dimensions of Corruption

�Legacy: getting things was a function of who you knew � Was (is) corrosive because it is the antithesis

to a performance-based economy �The problem rests with the common citizen

and is particularly attributable to the middle level professional

�Goods, services, and data are all contaminated by gray area maneuvers

Corruption by Design

�Transition and privatization brought “corruption by design” �Those few who use power and position to

make themselves opulently wealthy by purposively manipulating the system �The normal focus of the “corruption”

discussion �Ultimately requires wrestling legislative

and judicial power from their control

Situational Corruption�An alternative is to focus on the massive

behaviors running through every tier of society and rationalized by common people. If common people simply choose to interact in ways they know are more respectful, fair and system supporting, change is possible.

�Without it, managers and investors can have no confidence in the production, distribution or marketing of products and services. �Corruption = current US explanation for

disengagement

8

UKR Strength: Economic Foundation?

� 2016, Ukrainian agricultural exports exceeded

$15B $4B increase over 2015

� Agrarian products = 42% of total exports � Fats and oils of animal or vegetable origin

demonstrated the most significant increase -- up 20%

� Exports of plant growing products -- over $8B � Food preparations at $2.45B � Live animals and animal products $0.78B 21.02.2017 Source: State Statistics Service of Ukraine

9

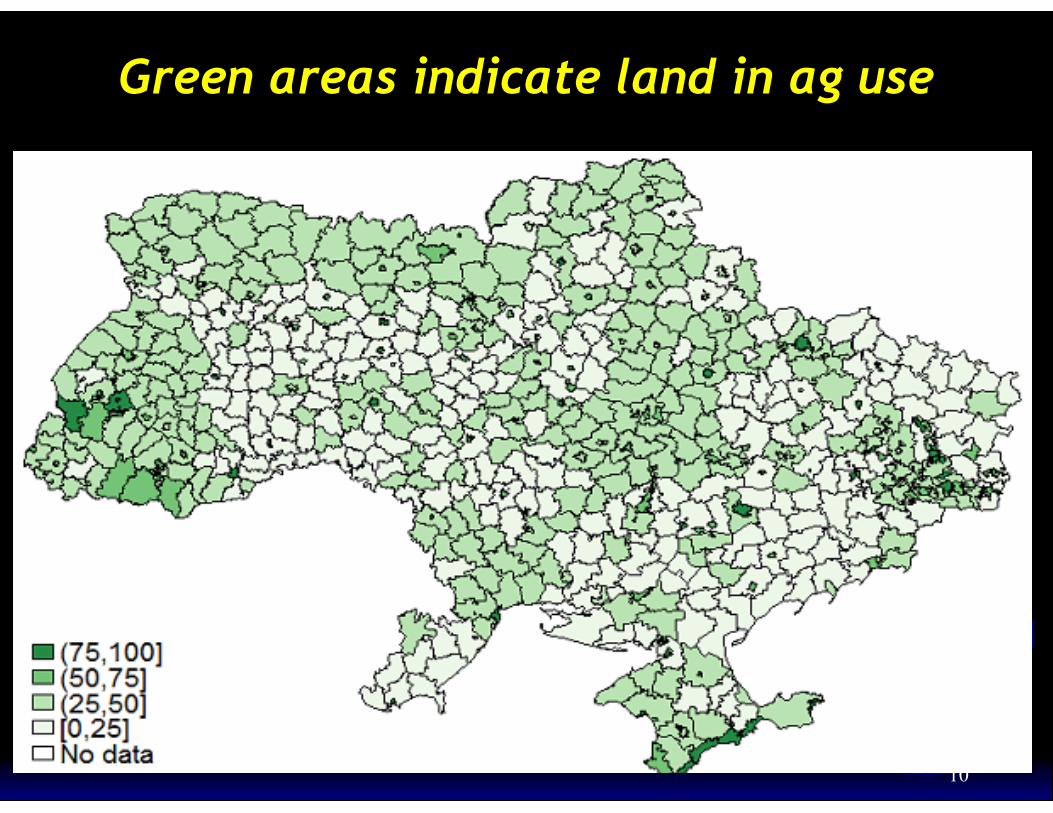

Green areas indicate land in ag use

10

Instability in the General Economy2014-2017

�In less than two years … �the Ukrainian currency lost 70% of its

value, �state deficits ran over 10%, �inflation was crushing at nearly 60%. �In two years, the economy contracted by

nearly 15%.

11

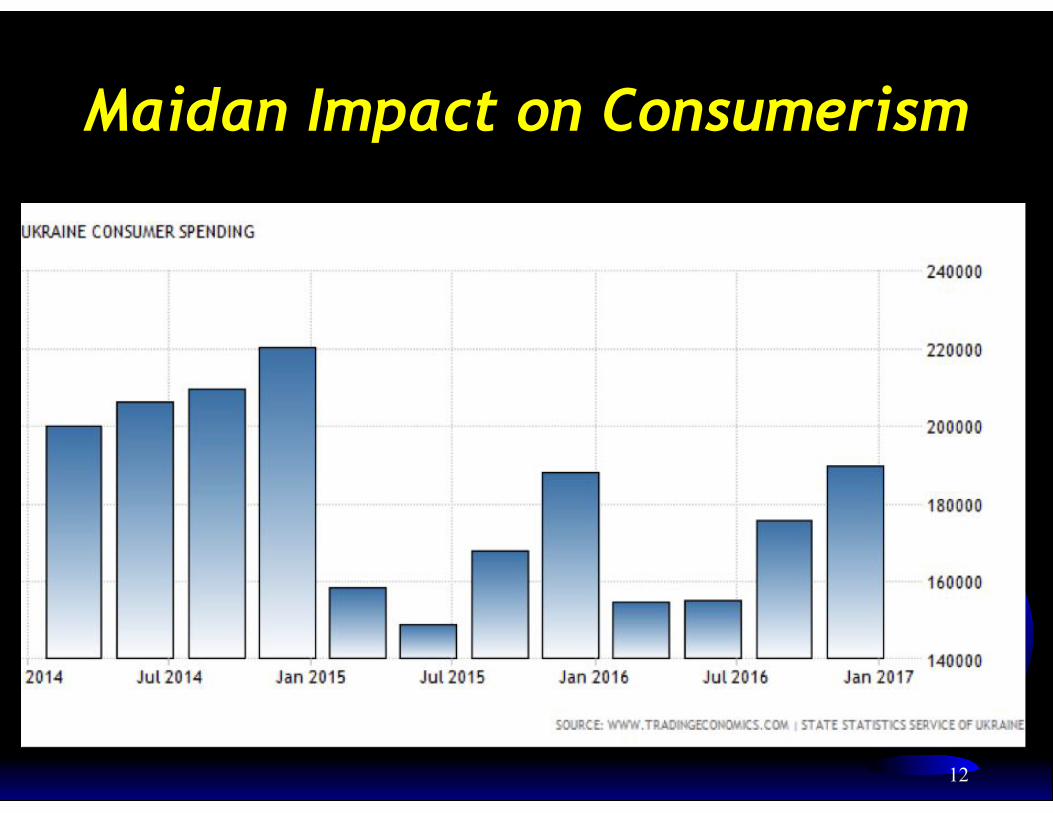

Maidan Impact on Consumerism

12

Livestock (typical example of issues)

�On average, 70% of technical equipment, feed ingredients and breeding material are imported. Hyrivna = soft currency

�In some product areas, the share of imported goods is at nearly 100%.

�Foreign reluctance: - absence of clear rules & legislation - reliable cooperation with state authorities agrofarm.org

13

Ukrainian Political SettingBrookings, “Why is Ukraine not leveraging its comparative advantage in agriculture? “The answer lies in the administration of the country’s farmland.” �An unstable and struggling political system �Deterioration of its political institutions �An ebb and flow of legitimacy �Three years torn by alternately violent and

frozen instability in eastern Ukraine. �Russian seizure of Crimea compounded the

sense of crisis and trauma for the Ukraine 14

Privatization of Collective Farms�UKR: collective farmland privatized more

than 15 years ago �Factors constraining growth: (a) moratorium on farmland sales (b) Belarus & Ukraine -- last countries in Europe where farmland sales are banned (c) low level of trust in goverment‘s commitment to competitive & transparent markets �Perception: gov is anti-reform & complacent about corruption

15

State “Control” of Non-Privatized Land

�UKR: 25% of farmland in the hands of the State 10.5 million hectares �Land set in reserve during privatization … 1 million hectares are used by state enterprises & state ag research institutions �8.9 million hectares are “unregistered” gov does not control use = income losses & corruption �Reform & state auctions could produce $1B

revenues & enable electronic registration

16

Foreign Ownership

� July 2014 following Maidan: major scramble by Monsanto, Cargill, DuPont

� January 2016: moratorium on foreign sales

�Implications: is there an alternative source of technological innovation? Clearly NOT

17

European Bank for Reconstruction & Development

�2014: ten private agribusinesses willing to invest $1 billion

� actual: small portion … because regulatory changes and tax breaks are necessary for

increases in investments and to stimulate economic growth

18

Foreign Investments in UKR Agriculture� Trigon Agri Denmark 52,679 � PIF Saudi Arabia

33,000 � Renaissance Group Russia 250,000 � MK Group Serbia 50,000 � Glencore PLC Switzerland 80,000 � Sintal Ag Cyprus 146,800 � Agrokultura AB Sweden 68,700 � AgroGeneration France 120,000 � Kernel Holding S.A. Luxembourg 405,000 � MCB Agricole Austria 96,000 � Mriya Agro Cyprus 298,000 Oakland Institute Total 1,600,179

19

Agrobarometer Assessment (2014)“Main Obstacles for Agribusiness” Survey

75% Market instability 55% Lack of adequate State support 50% Energy price increases 45% State regulation 35% Political instability 35% Lack of financing 30% Inflation 30% Shortage of skilled labor 10% Difficult introduction of new technology

20

Agricultural Leadership: UkraineTaras Kutovyi ?

� Ihor Shvaika, former agriculture minister (-2014) right-wing nationalist resigns under indictment (accepting bribe)

�Oleksiy Pavlenko replaces (resigns April 2016) �Taras Kutovyi 2016 – 41 “reformer” not ag specialist �Assumes office in April 2016 �Minister, Agrarian Policy and Food �Resigned May 2017 No replacement!

21

Russian Agriculture in Yeltsin Era�Yeltsin era: production down •privatization legalized •reforms focus on state & collective farms •95% “reorganized” •reforms met with farmers’ conservatism •gov retreats from role as guarantor of the market & reduces subsidies •‘90s -- overall ag production declined

22

Assessment … ‘90s

“Working with domestic producers calls for a specific approach. Russian agriculture lags behind developed countries in productivity, and requires high capital intensity and has experienced a long period of under investment following the collapse of the USSR which practically destroyed the production base of Russian agriculture.” Unilever Exec

23

“There are a lot of things which restrict Russian agricultural development.”

� local production lags behind the rest of the world in utilizing the latest practices and technology

� low levels of competitiveness of Russian ag producers � need for floating capital; long turnover period because of

seasonal harvests � in a region of marginal conditions -- conditions can vary

greatly from year to year -- significant impact on production. 10% of land useful 60% of that for crops 14% workforce

� number of qualified professionals in agriculture inadequate � significant migration from rural areas to urban ones -- rural areas not attractive to young people

24

Ag Intensive Regions of Russia

25

�high degree of state interference in agricultural prod

�uneven, irregular supply of inputs � insecure financial transaction systems �complicated regulatory environment

Summary: “Under current materials supply market and economic conditions, it’s clear that considerable time will be required to develop Russian agriculture. It will need to attract high levels of investments from state and foreign investors.”

26

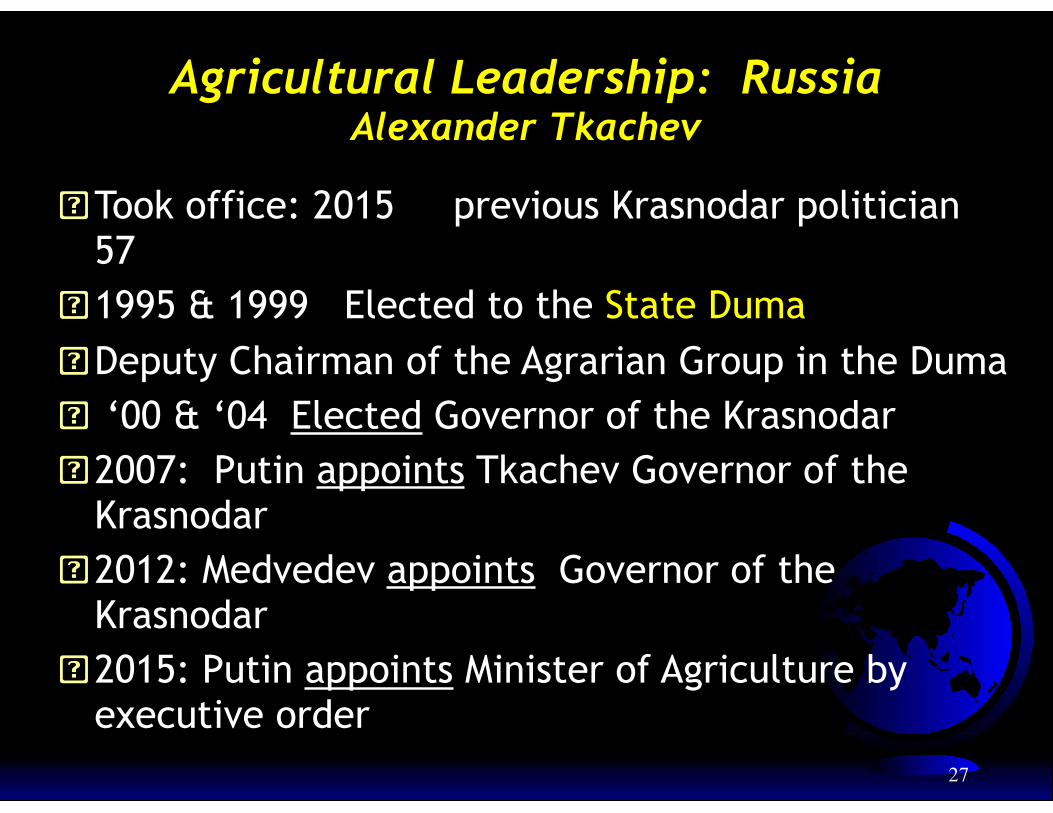

Agricultural Leadership: RussiaAlexander Tkachev

�Took office: 2015 previous Krasnodar politician 57

�1995 & 1999 Elected to the State Duma �Deputy Chairman of the Agrarian Group in the Duma � ‘00 & ‘04 Elected Governor of the Krasnodar �2007: Putin appoints Tkachev Governor of the

Krasnodar �2012: Medvedev appoints Governor of the

Krasnodar �2015: Putin appoints Minister of Agriculture by

executive order27

Tkachev

28

Sell pork to muslims in Indonesia

Agrocomplex

Sochi Olympic Games

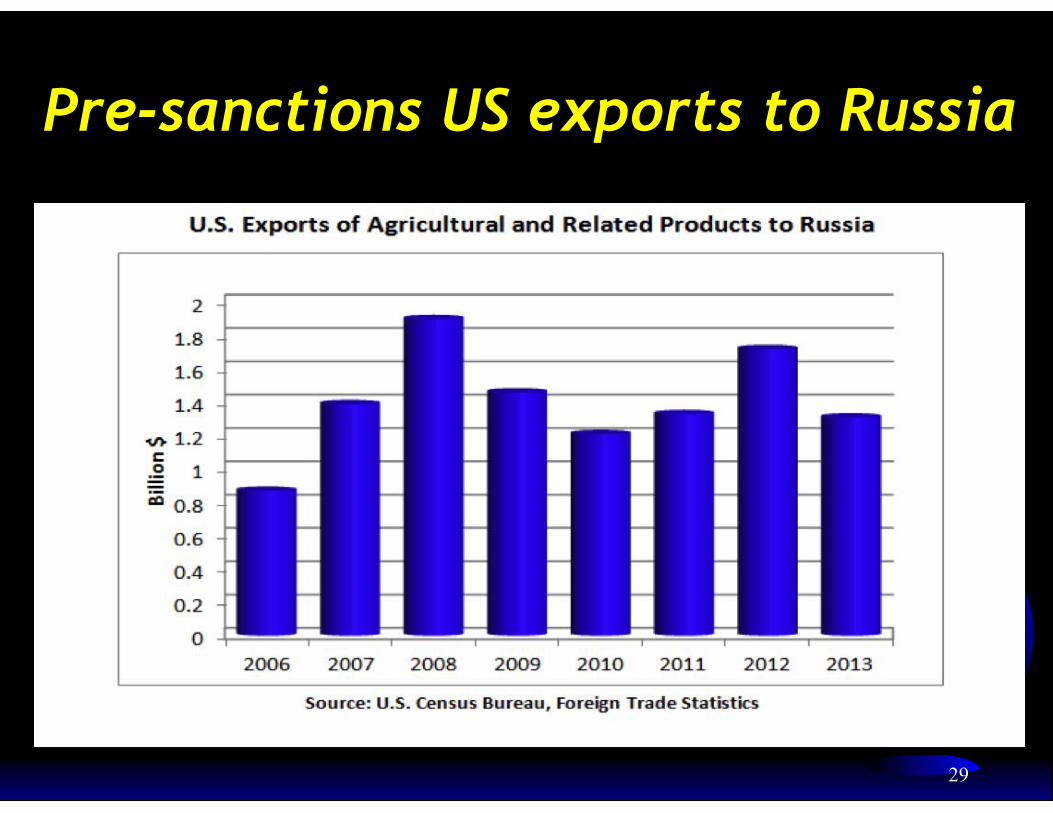

Pre-sanctions US exports to Russia

29

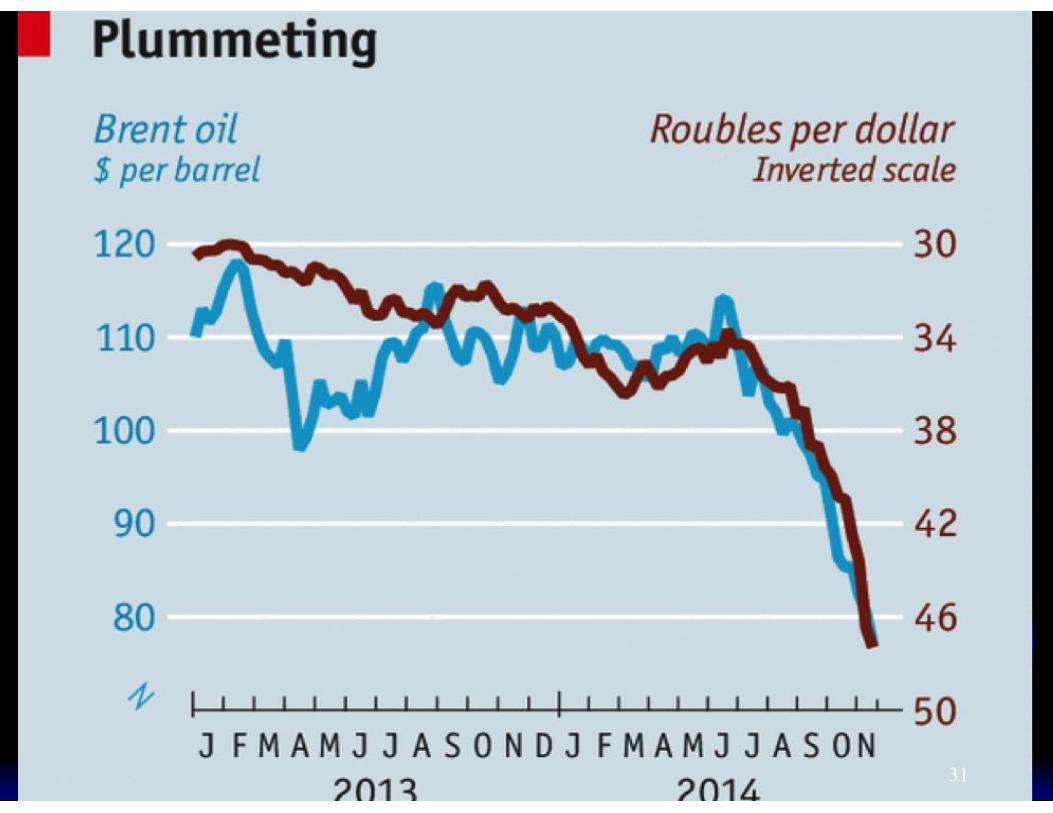

Russian Market Overview�Russia presents both significant challenges

and opportunities for experienced Am. exporters.

�2014-2016 economic downturn, driven by low oil prices and the lack of structural economic reform, squeezed both Russian corporations and the average consumer.

�targeted American and European economic sanctions remain in place; there is no overall trade embargo on Russia.

�Over 1,000 American firms of all sizes continued to do business in Russia

30

31

Sanctions

�US initiative; EU compliance �Reaction to Russian linkage to Ukrainian

civil war in Donbas �Focus: seed, commodities, software,

technology, equipment �Select policy-makers and entrepreneurs

are banned from business relationships

32

Counter-Sanctions

�Response: August 2014 �Impacting RU imports from US, EU,

Norway, Canada, Australia �Veg, meat, fish, milk, dairy �10% all RU imports come from EU �Over $1B in trade flow �Result: HIGHER food prices in RU �2015 recession

33

What Lies Ahead ?21st C Agriculture

�The next generation of agriculturalists are facing some of the greatest challenges we’ve seen thus far. They will need to produce more than ever, with less inputs, on less land, with increased regulations, at a competitive cost.

� In the future I see a farmer being able to plant his fields without even sitting in the cab of a tractor, and a rancher being able to simultaneously monitor the health of his cattle with just the click of a mouse.

34

“Farms, then, are becoming more like factories: tightly controlled operations for turning out reliable products, immune as far as possible from the vagaries of nature”

� Understanding a crop’s DNA sequence also means that breeding itself can be made more precise.

� Such technological changes, in hardware, software and “liveware”, are reaching beyond field, orchard and byre

� FAO by 2050 need ag prod up 70%

In sum, education, big data, robotics

35

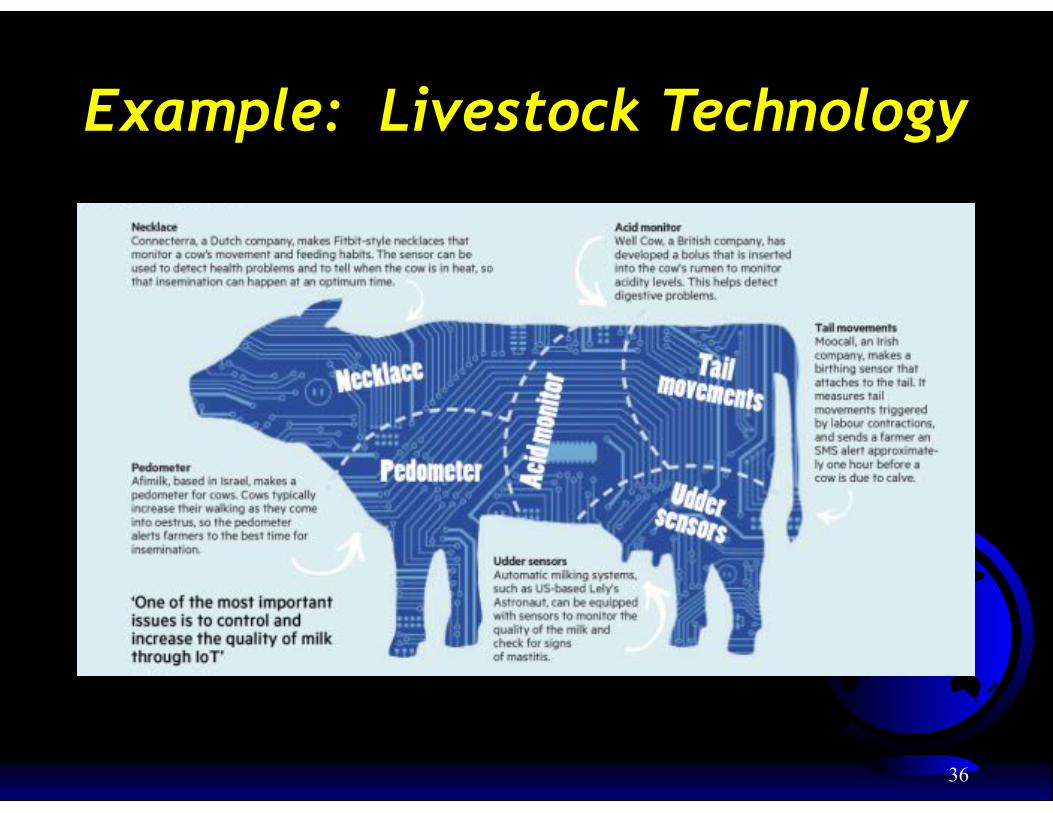

Example: Livestock Technology

36

In sum, education, big data, robotics

�Understanding the day-to-day logistics of a farm operation, education is paramount for success

�Productive decision-making will require “cloud” solutions

�Virtual field management; autonomous tractors, robots

37

The Most Optimistic Sign … UKR & RU “beginning to know what they don’t know”

�Farm managers are increasingly recognizing the dimensions of the challenges they are facing �In essence, they are learning what they

don’t know and the options for filling those voids �For most, needing information and

guidance that are not free; difficult options!

38

Generic ChallengesCommon to Russia and Ukraine

�“Transition” �Legitimacy of institutions �Relationship of the STATE to the Ag sector �Deteriorating foreign relationships

impacting markets & investment �Minimal trajectory toward technology

39

Meaning for the Ag Consultant

�Engaging RU & UKR projects will require a sophisticated understanding of the politics of the environment �American corporate clients also need to

adjust their anticipated time frames for results �Need to educate local farmers and

local politicians in the rationale for ethical behavior in the face of investment

40