The Phosphate Outlook - FIRT · The Phosphate Outlook Corey Giasson, MBA Manager, Market Research...

44

The Phosphate Outlook The Phosphate Outlook Corey Corey Giasson Giasson , MBA , MBA Manager, Market Research Manager, Market Research PotashCorp PotashCorp 2007 Fertilizer Outlook and Technology Conference 2007 Fertilizer Outlook and Technology Conference Arlington, Virginia Arlington, Virginia November 7, 2006 November 7, 2006

Transcript of The Phosphate Outlook - FIRT · The Phosphate Outlook Corey Giasson, MBA Manager, Market Research...

The Phosphate OutlookThe Phosphate Outlook

Corey Corey GiassonGiasson, MBA, MBAManager, Market ResearchManager, Market Research

PotashCorpPotashCorp

2007 Fertilizer Outlook and Technology Conference2007 Fertilizer Outlook and Technology ConferenceArlington, VirginiaArlington, VirginiaNovember 7, 2006November 7, 2006

ForwardForward--Looking StatementsLooking StatementsThis presentation contains forwardThis presentation contains forward--looking statements. These statements are based on looking statements. These statements are based on certain factors and assumptions as set forth in this release inccertain factors and assumptions as set forth in this release including foreign exchange luding foreign exchange rates, expected growth, results of operations, performance and brates, expected growth, results of operations, performance and business prospects and usiness prospects and opportunities. While the company considers these factors and assopportunities. While the company considers these factors and assumptions to be umptions to be reasonable based on information currently available, they may prreasonable based on information currently available, they may prove to be incorrect. A ove to be incorrect. A number of factors could cause actual results to differ materiallnumber of factors could cause actual results to differ materially from those in the forwardy from those in the forward--looking statements, including, but not limited to: fluctuationslooking statements, including, but not limited to: fluctuations in supply and demand in in supply and demand in fertilizer, sulfur, transportation and petrochemical markets; chfertilizer, sulfur, transportation and petrochemical markets; changes in competitive anges in competitive pressures, including pricing pressures; risks associated with napressures, including pricing pressures; risks associated with natural gas and other hedging tural gas and other hedging activities; changes in capital markets; changes in currency and activities; changes in capital markets; changes in currency and exchange rates; exchange rates; unexpected geological or environmental conditions; and governmenunexpected geological or environmental conditions; and government policy changes. t policy changes. Additional risks and uncertainties can be found in our 2005 annuAdditional risks and uncertainties can be found in our 2005 annual report to shareholders al report to shareholders and in filings with the U.S. Securities and Exchange Commission and in filings with the U.S. Securities and Exchange Commission and Canadian provincial and Canadian provincial securities commissions. Forwardsecurities commissions. Forward--looking statements are given only as at the date of this looking statements are given only as at the date of this presentation and the company disclaims any obligation to update presentation and the company disclaims any obligation to update or revise the forwardor revise the forward--looking statements, whether as a result of new information, futulooking statements, whether as a result of new information, future events or otherwise. re events or otherwise.

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplyConclusionConclusion

AgendaAgenda

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplyConclusionConclusion

AgendaAgenda

Source: FerteconSource: Fertecon

FOB Tampa DAP PriceFOB Tampa DAP Price

100

150

200

250

300

Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

FOB Tampa DAP Adjusted for Inflation

$US/Tonne FOB

$256*$256*

* Average for the month* Average for the month--toto--datedate

$212*$212*

Source: TFI, Fertecon, PotashCorpSource: TFI, Fertecon, PotashCorp

0

50

100

150

200

250

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-060

50

100

150

200

250

US DAP Cost US DAP Cost vsvs DAP PriceDAP Price

Cost ($US/Short Ton)Cost ($US/Short Ton)

Estimate for an AverageEstimate for an Average--Cost ProducerCost ProducerDAP FOB Tampa Price ($US/Short Ton)DAP FOB Tampa Price ($US/Short Ton)

Sulfur

Rock

Ammonia

Other

* Average for the month* Average for the month--toto--datedate

Source: TFI, Fertecon, PotashCorpSource: TFI, Fertecon, PotashCorp

US DAP Yearly Average DAP MarginUS DAP Yearly Average DAP Margin

-15

-10

-5

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 YTD 2006 7-YearAverage

-$12

+$32

+$4.7

$US/Short Ton

+$10

+$24

-$8 -$9

$0$0

Estimate for an AverageEstimate for an Average--Cost ProducerCost Producer

Source: TFI, Fertecon, PotashCorpSource: TFI, Fertecon, PotashCorp

DAP ROI at the Top of the CycleDAP ROI at the Top of the Cycle

1mmt of new P1mmt of new P22OO5 5 capacity (2.2mmt of DAP) capacity (2.2mmt of DAP) $1 Billion$1 BillionCost of New CapacityCost of New Capacity $ 460/mt$ 460/mt

Average Margin (JanAverage Margin (Jan--00 to present)00 to present) $ 5/mt$ 5/mtPayback Period Payback Period 92 years92 yearsROIROI 1%1%

Current Margin ($35/st)Current Margin ($35/st) $ 40/mt$ 40/mtPayback PeriodPayback Period ~12 years~12 yearsROIROI ~9%~9%

And it is currently considered the top of the market !?!And it is currently considered the top of the market !?!

DAP Price at a 15DAP Price at a 15--20% Return20% Return $293$293--320/mt320/mt

Source: British Sulphur, FerteconSource: British Sulphur, Fertecon

Global Net Change DAP/MAP CapacityGlobal Net Change DAP/MAP Capacity

Morocco Morocco +1.7M TPY+1.7M TPY

Other Asia Other Asia 0.0M TPY0.0M TPY

20002000--2006E 2006E

North America North America --5.8M TPY5.8M TPY

FSU FSU +2.0M TPY+2.0M TPY

Central America Central America --1.5M TPY1.5M TPY India India

+2.5M TPY+2.5M TPY

China China +9.8M TPY+9.8M TPY

Oceania Oceania +0.3M TPY+0.3M TPY

Other Africa Other Africa +0.3M TPY+0.3M TPYSouth America South America

--0.1M TPY0.1M TPY

Europe Europe --0.1M TPY0.1M TPY

Global Net Change in DAP/MAP Capacity Global Net Change in DAP/MAP Capacity +9.0M TPY+9.0M TPY

Global Net Change in DAP/MAP Consumption Global Net Change in DAP/MAP Consumption +7.4M TPY+7.4M TPY

Middle East Middle East --0.1M TPY0.1M TPY

Source: British Sulphur, PotashCorpSource: British Sulphur, PotashCorp

2

4

6

8

10

12

14

16

18

20

22

2005 2006E

Million Tonnes Product

US Phosphate Fertilizer CapacityUS Phosphate Fertilizer Capacity

-16%

EstimatedEstimated

Source: TFISource: TFI

US ProducersUS Producers’’ DAP/MAP Ending InventoryDAP/MAP Ending Inventory

0.8

1.0

1.2

1.4

1.6

1.8

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005 2006 3-Year Average

Million Tons ProductMillion Tons Product

SeptSept--06 DAP/MAP ending inventory 06 DAP/MAP ending inventory was 1% above the 3was 1% above the 3--yr yr AvgAvg

Source: TFISource: TFI

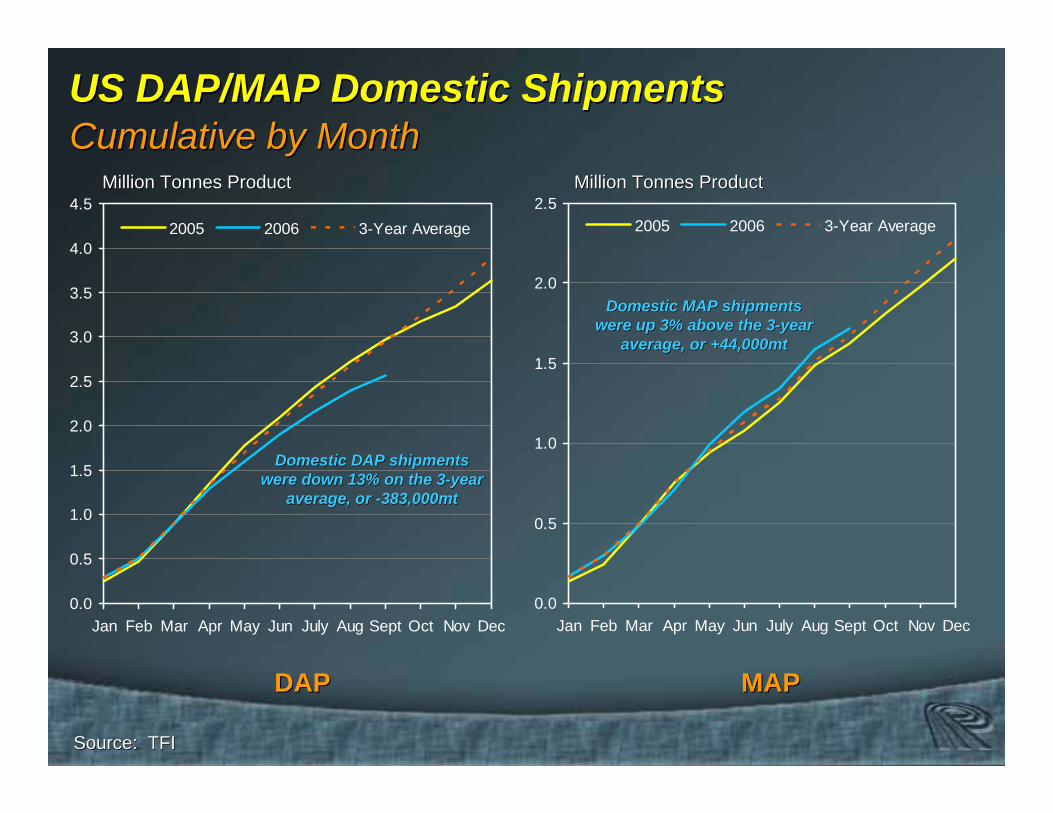

US DAP/MAP Domestic ShipmentsUS DAP/MAP Domestic Shipments

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

2005 2006 3-Year Average

Million Tonnes ProductMillion Tonnes Product

Cumulative by MonthCumulative by Month

0.0

0.5

1.0

1.5

2.0

2.5

Jan Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

2005 2006 3-Year Average

Million Tonnes ProductMillion Tonnes Product

DAPDAP MAPMAP

Domestic DAP shipments Domestic DAP shipments were down 13% on the 3were down 13% on the 3--year year

average, or average, or --383,000mt383,000mt

Domestic MAP shipments Domestic MAP shipments were up 3% above the 3were up 3% above the 3--year year

average, or +44,000mtaverage, or +44,000mt

Source: TFISource: TFI

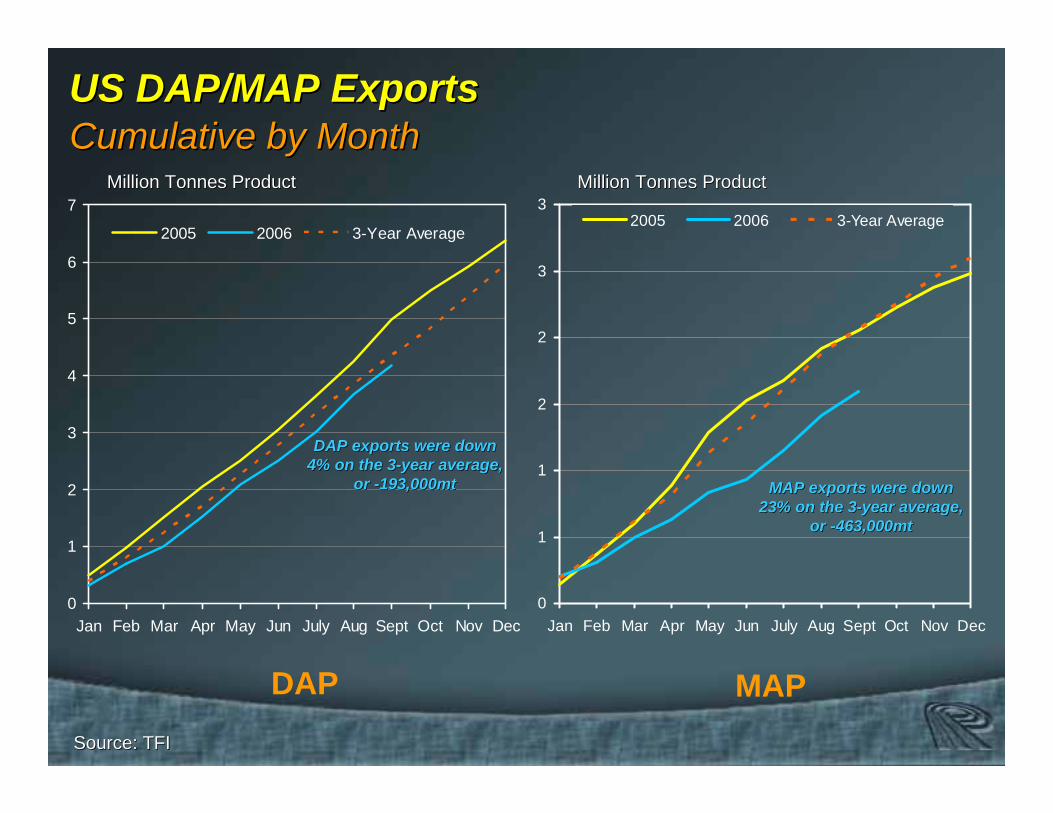

US DAP/MAP ExportsUS DAP/MAP Exports

0

1

2

3

4

5

6

7

Jan Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

2005 2006 3-Year Average

0

1

1

2

2

3

3

Jan Feb Mar Apr May Jun July Aug Sept Oct Nov Dec

2005 2006 3-Year Average

Million Tonnes ProductMillion Tonnes Product Million Tonnes ProductMillion Tonnes Product

DAP MAP

DAP exports were down DAP exports were down 4% on the 34% on the 3--year average, year average,

or or --193,000mt193,000mt MAP exports were down MAP exports were down 23% on the 323% on the 3--year average, year average,

or or --463,000mt463,000mt

Cumulative by MonthCumulative by Month

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplyConclusionConclusion

AgendaAgenda

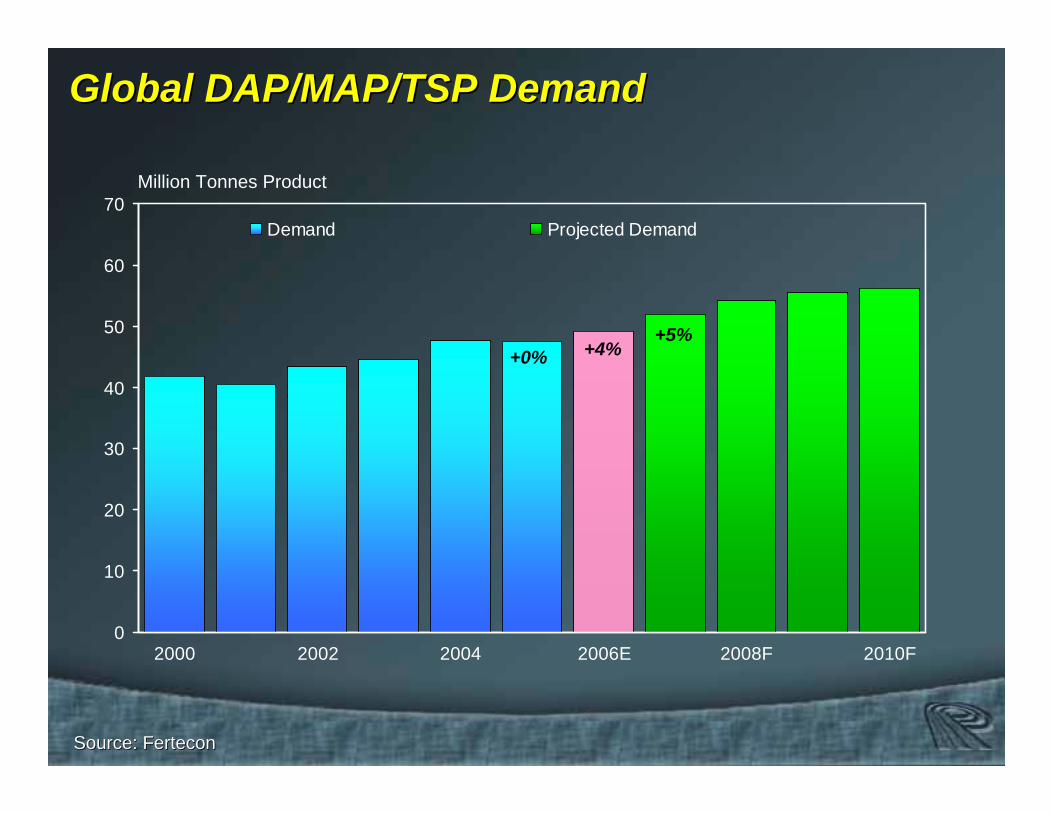

Source: FerteconSource: Fertecon

Global DAP/MAP/TSP DemandGlobal DAP/MAP/TSP Demand

0

10

20

30

40

50

60

70

2000 2002 2004 2006E 2008F 2010F

Demand Projected Demand

Million Tonnes Product

+4%+5%

+0%

Source: FerteconSource: Fertecon

Global DAP/MAP/TSP Demand and TradeGlobal DAP/MAP/TSP Demand and Trade

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F0

10

20

30

40

50

60

70

80

90

100Demand Projected Demand Imports Imports as a % of Demand

Million Tonnes Product

--1%1% +3%+3%--2%2%

+4%+5%

+0%

-5% -1%-2%

Percent

Source: FerteconSource: Fertecon

China DAP/MAP/TSP DemandChina DAP/MAP/TSP Demand

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Demand Projected Demand Imports Net Exports

Million Tonnes Product

--21%21% +6%+6%--23%23%

+4% +4%+14%

Source: British Suolphur, FerteconSource: British Suolphur, Fertecon

5+ Million Tonnes

1-5 Million Tonnes< 1 Million TonnesNo Phosphate Reserves

ChinaChina’’s Phosphate Rock Productions Phosphate Rock ProductionBy Province in Million TonnesBy Province in Million Tonnes

Source: Fertecon, PotashCorpSource: Fertecon, PotashCorp

India DAP/MAP DemandIndia DAP/MAP Demand

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Demand Projected Demand Imports

Million Tonnes Product

0%0% --2%2%+313%+313%

+8%+7%

+19%

Source: FerteconSource: Fertecon

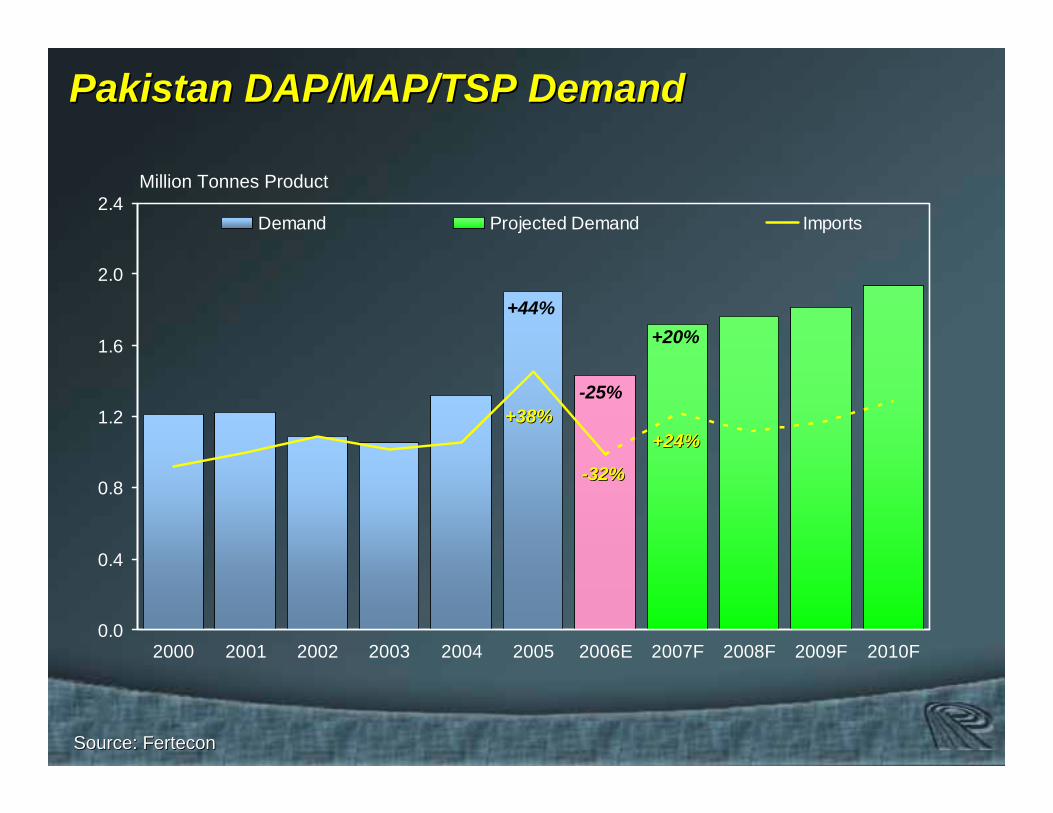

Pakistan DAP/MAP/TSP DemandPakistan DAP/MAP/TSP Demand

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Demand Projected Demand Imports

Million Tonnes Product

--32%32%

+24%+24%+38%+38%

-25%

+20%+44%

Source: FerteconSource: Fertecon

Brazil DAP/MAP/TSP DemandBrazil DAP/MAP/TSP Demand

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Demand Projected Demand Imports

Million Tonnes Product

--9%9% +6%+6%--28%28%

-3%

+12%-20%

Source: FerteconSource: Fertecon

Australia DAP/MAP/TSP Demand Australia DAP/MAP/TSP Demand

0.0

0.5

1.0

1.5

2.0

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Demand Projected Demand Imports

Million Tonnes Product

--16%16%+20%+20%--18%18%

-10%

+12%-13%

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplyConclusionConclusion

AgendaAgenda

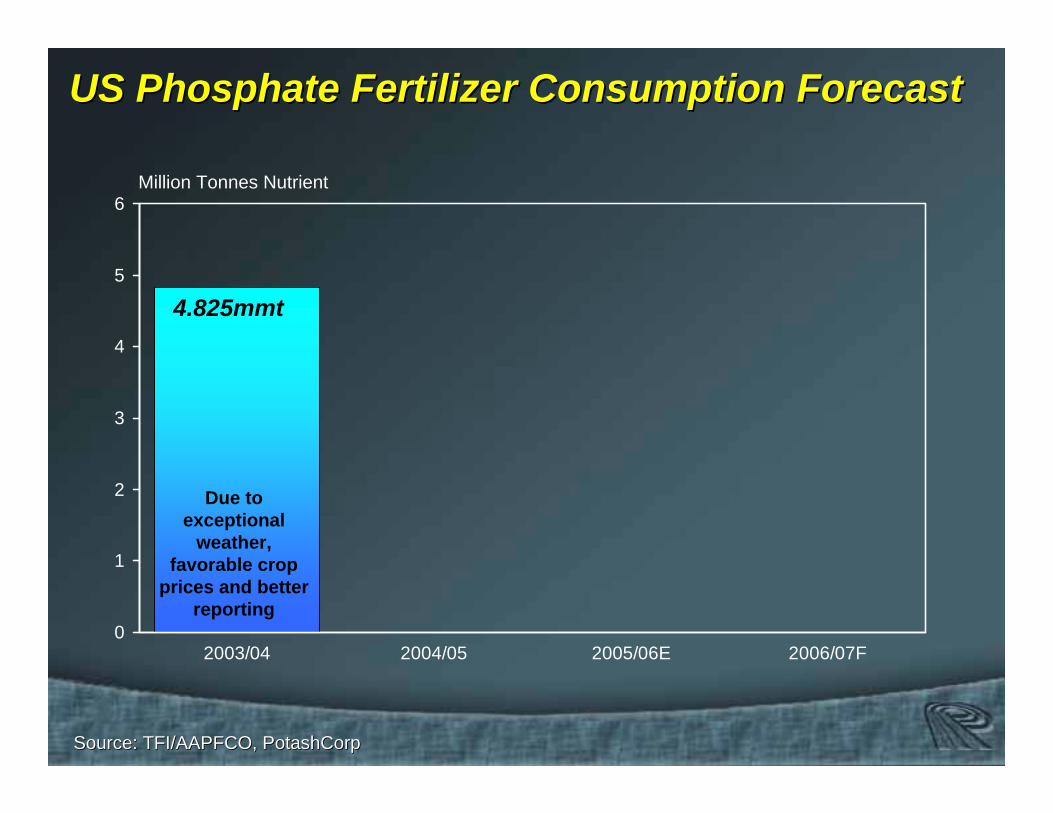

Source: TFI/AAPFCO, PotashCorpSource: TFI/AAPFCO, PotashCorp

0

1

2

3

4

5

6

2003/04 2004/05 2005/06E 2006/07F

Million Tonnes Nutrient

US Phosphate Fertilizer Consumption ForecastUS Phosphate Fertilizer Consumption Forecast

4.825mmt

Due to exceptional

weather, favorable crop

prices and better reporting

Source: TFI/AAPFCO, PotashCorpSource: TFI/AAPFCO, PotashCorp

0

1

2

3

4

5

6

2003/04 2004/05 2005/06E 2006/07F

4.638mmt-3.9%

4.825mmt

Million Tonnes Nutrient

US Phosphate Fertilizer Consumption ForecastUS Phosphate Fertilizer Consumption Forecast

Due to more normal weather and a decline in

commodity prices

Source: TFI/AAPFCO, PotashCorpSource: TFI/AAPFCO, PotashCorp

0

1

2

3

4

5

6

2003/04 2004/05 2005/06E 2006/07F

Million Tonnes Nutrient

US Phosphate Fertilizer Consumption ForecastUS Phosphate Fertilizer Consumption Forecast

Due to continued weakness in commodity

prices, higher energy input

costs and uncertainty about

planting decisions

4.050mmt-10 to -15%

4.638mmt-3.9%

4.825mmt

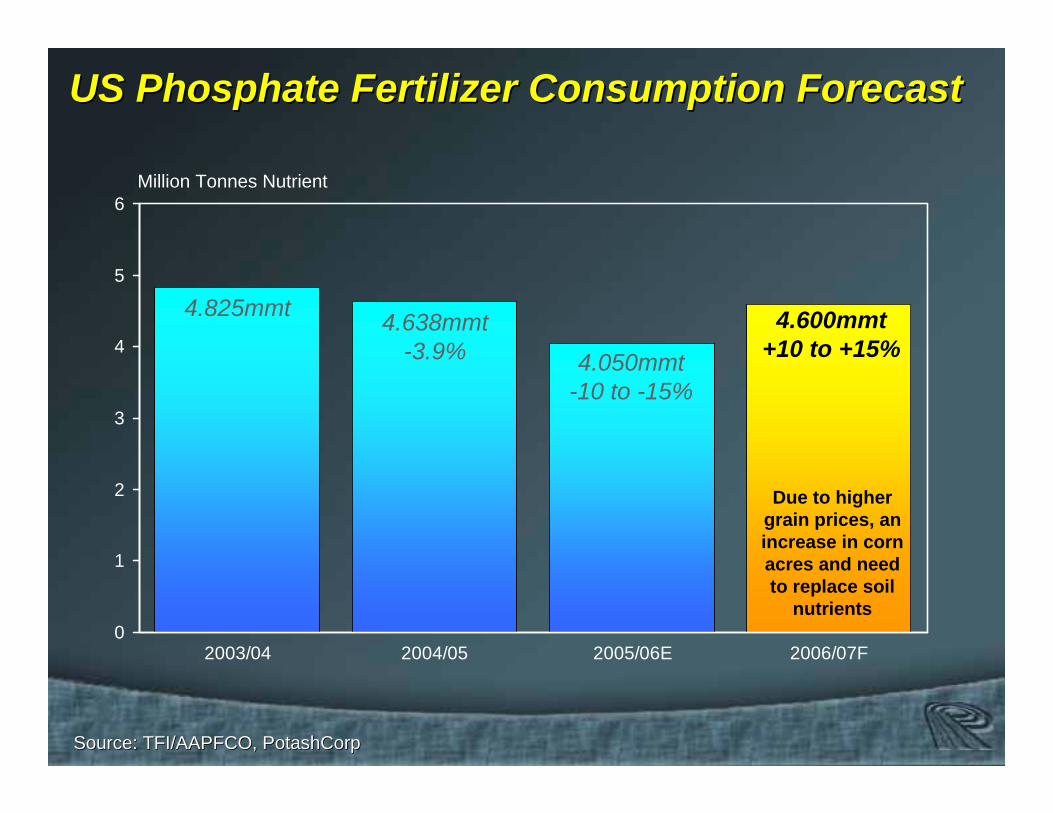

Source: TFI/AAPFCO, PotashCorpSource: TFI/AAPFCO, PotashCorp

0

1

2

3

4

5

6

2003/04 2004/05 2005/06E 2006/07F

Million Tonnes Nutrient

4.600mmt+10 to +15%4.050mmt

-10 to -15%

US Phosphate Fertilizer Consumption ForecastUS Phosphate Fertilizer Consumption Forecast

4.638mmt-3.9%

4.825mmt

Due to higher grain prices, an increase in corn acres and need to replace soil

nutrients

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplySummarySummary

AgendaAgenda

Source: FerteconSource: Fertecon

Global DAP/MAP/TSP Production GrowthGlobal DAP/MAP/TSP Production Growth

Africa / Middle East Africa / Middle East +9% to 8.0mmt+9% to 8.0mmt

Asia Asia +11% to 19.8mmt+11% to 19.8mmt

2007E (Million Tonnes)2007E (Million Tonnes)

Europe Europe +8% to 1.9mmt+8% to 1.9mmtNorth America North America

+1% to 14.5mmt +1% to 14.5mmt

FSU FSU +4% to 5.2mmt+4% to 5.2mmt

South America South America +16% to 2.2mmt+16% to 2.2mmt Oceania Oceania

0% to 0.9mmt0% to 0.9mmt

Global Production GrowthGlobal Production Growth+5% to 51.9 Million Tonnes+5% to 51.9 Million Tonnes

Source: Fertecon, PotashCorpSource: Fertecon, PotashCorp

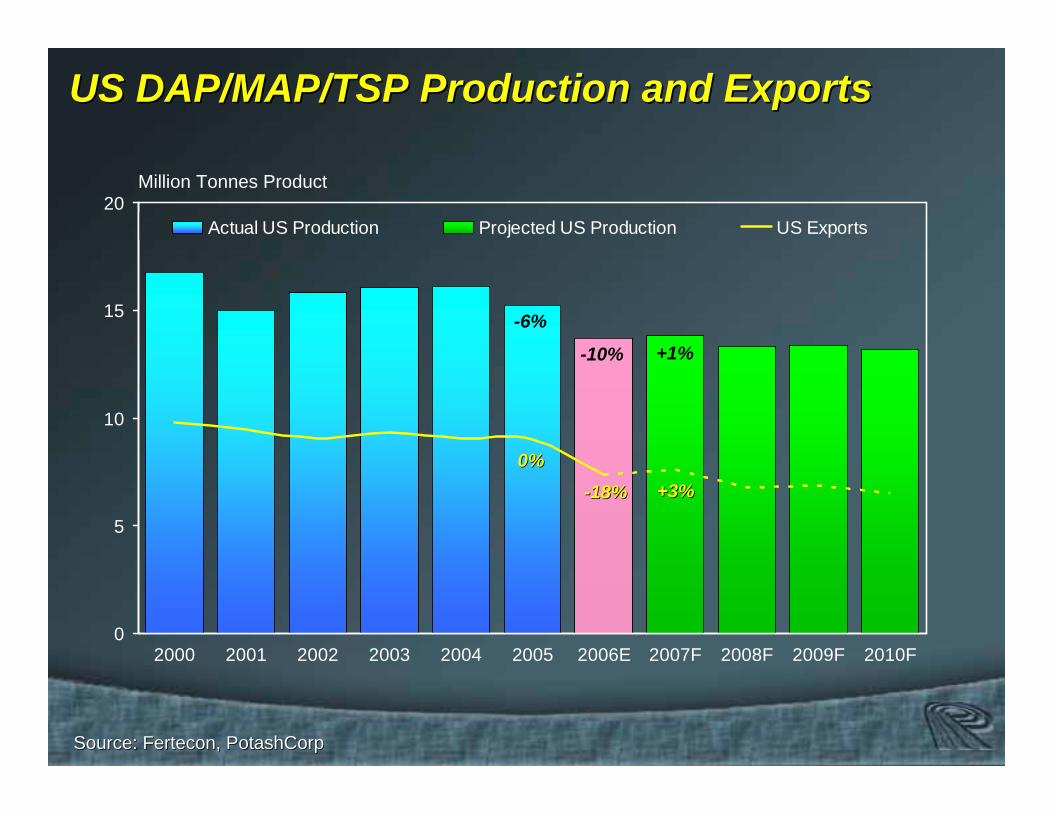

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Actual US Production Projected US Production US Exports

Million Tonnes Product

US DAP/MAP/TSP Production and ExportsUS DAP/MAP/TSP Production and Exports

--18%18% +3%+3%0%0%

-10% +1%-6%

Source: FerteconSource: Fertecon

India DAP ProductionIndia DAP Production

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Production Projected Production

Million Tonnes Product

+13%

+14%

-16%

Source: FerteconSource: Fertecon

Morocco DAP/MAP/TSP ProductionMorocco DAP/MAP/TSP Production

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F0

10

20

30

40

50

60

70

80

90

100Production Projected Production Share of World Trade

Million Tonnes Product

+31%+31% +16%+16%--5%5%

+26%

+16%

0%

PercentPercent

Source: FerteconSource: Fertecon

China DAP/MAP/TSP ProductionChina DAP/MAP/TSP Production

0

2

4

6

8

10

12

14

16

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F

Production Projected Production

Million Tonnes Product

+10%+6%

+19%

Source: British Sulphur, PotashCorpSource: British Sulphur, PotashCorp

Projected DAP/MAP/TSP Capacity ChangesProjected DAP/MAP/TSP Capacity Changes

Africa Africa 1.21.2

East Asia East Asia 6.06.0

Estimated 2006Estimated 2006--2010 (Million Tonnes Product)2010 (Million Tonnes Product)

Middle East Middle East 3.03.0

Net Capacity Additions = 10.9 Million TonnesNet Capacity Additions = 10.9 Million Tonnes

North America North America --3.23.2

South Asia South Asia 1.21.2

South East Asia South East Asia 0.20.2

South America South America 1.91.9

Oceania Oceania 0.00.0

Europe Europe 0.00.0

FSU FSU 0.10.1

Source: British Sulphur, PotashCorpSource: British Sulphur, PotashCorp

China DAP/MAP ProjectsChina DAP/MAP Projects

6.0 MillionTotal

2007-2010DAP/MAP3.5 MillionMiscellaneous

2006DAP0.9 MillionHubei - Yangfeng & Dayukouu

2008DAP/MAP0.8 MillionYunnan - NG Chemical Comples

2007MAP0.5 MillionGuizhou - Kaiyang

2008DAP0.3 Million Hubei - Yihua Group Corp

OperationalProductProductionLocation

Estimated 2006Estimated 2006--2010 (Million Tonnes Product)2010 (Million Tonnes Product)

Source: FerteconSource: Fertecon

ChinaChina’’s Low Analysis Phosphate Productions Low Analysis Phosphate Production

0

1

2

3

4

5

1980 1985 1990 1995 2000 2005 2010

SSP FMP

Million Tonnes PMillion Tonnes P22OO55

SSP & Fused Magnesium PhosphateSSP & Fused Magnesium Phosphate

Total reduction 2005Total reduction 2005--2010 = .5 million tonnes P2010 = .5 million tonnes P22OO55

Source: Ma'adenSource: Ma'aden

MaMa’’adenaden Phosphate ProjectPhosphate Project

JeddahJeddah

JawfJawf

HailHail

EshidiyaEshidiya

RiyadhRiyadh

DammanDammanRasRas AzAz ZawrZawr

AzAz ZabirahZabirah3.5 Mt/y3.5 Mt/y

Al Al JalamidJalamid4.5 Mt/y4.5 Mt/y

QurayyatQurayyat

BuraydaBurayda

CurrentCurrent

FutureFuture

Saudi ArabiaSaudi Arabia

Source: Ma'adenSource: Ma'aden

MaMa’’adenaden Phosphate Project Proposed MarketPhosphate Project Proposed Market

IranIran

IndiaIndia

PakistanPakistanChinaChina JapanJapan

Saudi ArabiaSaudi Arabia

IndonesiaIndonesia

Source: British Sulphur, Fertecon, PotashCorpSource: British Sulphur, Fertecon, PotashCorp

0

2

4

6

8

10

12

2006E 2007F 2008F 2009F 2010F

China S.Arabia Morocco Bangladesh India Other Demand

Million Tonnes ProductMillion Tonnes Product

New DAP Capacity* vs Demand**New DAP Capacity* vs Demand**

*Several projects uncertain, unlikely projects excluded*Several projects uncertain, unlikely projects excluded**Adjustments made to net out North American capacity curtailmen**Adjustments made to net out North American capacity curtailmentsts

Cumulative Growth Cumulative Growth –– Net CapacityNet Capacity

3.2

The Phosphate Outlook The Phosphate Outlook

Summary of Previous YearSummary of Previous YearOffshore DemandOffshore DemandDomestic ConsumptionDomestic ConsumptionSupplySupplyConclusionConclusion

AgendaAgenda

Source: FerteconSource: Fertecon

Global DAP/MAP/TSP Demand and TradeGlobal DAP/MAP/TSP Demand and Trade

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006E 2007F 2008F 2009F 2010F0

10

20

30

40

50

60

70

80

90

100

Demand Projected Demand Imports Imports as a % of Demand

Million Tonnes ProductMillion Tonnes Product

--1%1% +3%+3%--2%2%

+4%+5%

+0%

-5% -1%-2%

PercentPercent

Source: TFI/AAPFCO, PotashCorpSource: TFI/AAPFCO, PotashCorp

0

1

2

3

4

5

6

2003/04 2004/05 2005/06E 2006/07F

Million Tonnes NutrientMillion Tonnes Nutrient

4.600mmt+10 to +15%4.050mmt

-10 to -15%

US Phosphate Fertilizer Consumption ForecastUS Phosphate Fertilizer Consumption Forecast

4.638mmt-3.9%

4.825mmt

Due to higher grain prices, an increase in corn acres and need to replace soil

nutrients

Source: British Sulphur, Fertecon, PotashCorpSource: British Sulphur, Fertecon, PotashCorp

0

2

4

6

8

10

12

2006E 2007F 2008F 2009F 2010F

China S.Arabia Morocco Bangladesh India Other Demand

Million Tonnes ProductMillion Tonnes Product

New DAP Capacity* vs Demand**New DAP Capacity* vs Demand**

*Several projects uncertain, unlikely projects excluded*Several projects uncertain, unlikely projects excluded**Adjustments made to net out North American capacity curtailmen**Adjustments made to net out North American capacity curtailmentsts

Cumulative Growth Cumulative Growth –– Net CapacityNet Capacity

3.2

ThankThank--YouYou