Markov and semi-Markov switching linear mixed models for ...

Economic Modelling 39 (2014) 213–220

Contents lists available at ScienceDirect

Economic Modelling

j ourna l homepage: www.e lsev ie r .com/ locate /ecmod

The non-linear impact of high and growing government external debt oneconomic growth: A Markov Regime-switching approach

İbrahim Doğan a,⁎, Faik Bilgili b

a Department of Economics, Faculty of Economics and Administrative Sciences, Bozok University, 66000 Yozgat, Turkeyb Department of Economics, Faculty of Economics and Administrative Sciences, Erciyes University, 38039 Kayseri, Turkey

⁎ Corresponding author. Tel.: +90 354 242 1042x2810E-mail addresses: [email protected], Ibrahim

[email protected], [email protected] (F. Bilgili).

http://dx.doi.org/10.1016/j.econmod.2014.02.0320264-9993/© 2014 Elsevier B.V. All rights reserved.

a b s t r a c t

a r t i c l e i n f oArticle history:Accepted 21 February 2014Available online 28 March 2014

Keywords:Economic growthExternal debtState-spaceMarkov Regime-switching model

Today, the major reason for external debt is to finance high public deficits. This study aims to examine the rela-tionship between external indebtedness and growth variables. In this context, Markov-switching model is usedbecause it allows the examination of unobservable variables in an observable model and provides steady algo-rithm to achieve robust optimization by iterations in a dynamic system, and is more flexible than prior models.This paper concentrates on the analysis of Turkey and utilizes the data set for the period of 1974 to 2009.Throughout the analyses, the relationship between growth and external borrowing is examined in terms of pub-lic and private external borrowing. Paper yields that, according to results of multivariate dynamic Markov-switching model, the main growth variables such as investment and human capital have positive impact ongrowth as expected. Findings can be summarized as follows; firstly, public and/or private external borrowinghas negative impact on growth both in regime at zero and regime at one. Secondly, the negative impact of publicborrowing on economic growth and development is higher than that of private borrowing on economic growthand development. Eventually, the conclusion reveals that the economic development and borrowing variables donot follow a linear path.

© 2014 Elsevier B.V. All rights reserved.

1. Introduction

External borrowing is considered as an important resource in the fi-nance for development in the developing countries. Since the currentdeficit of countries became unsustainable as of the 1950s, their tenden-cy to borrow from international organizations so as to nurture the eco-nomic development has increased. In the recent 50 years, foreign debtproblem has become one of the basic problems that have been facedby the developing countries. The debt crisis which occurred in theearly 1980s destabilized the economy of many developing countrieswith low income, and debt relief incentives were given to the saidcountries so as to relieve the bad impact of high borrowing on their de-velopment? High external borrowing received by the developing coun-tries since the second half of 1990s has become one of the mostimportant factors which have restricted the development of manypoor countries. The policy makers for this issue have been increasinglydrawing the attentions of public opinion all over the world.

In the recent years, borrowing has become an important economicproblem not only for the developing countries but for the developedcountries. In many countries, global crisis and expansionary publicpolicies have caused a rapid increase in the external borrowing, and

; fax: +90 354 242 [email protected] (İ. Doğan),

the unsustainable public debt in some European countries (especiallyGreece, Portuguese, Ireland, Spain, Italy etc.) have increased the atten-tion of politicians and academic members to excessive indebtedness.The Report of Bank for International Settlements for March, 2010 indi-cated that borrowing was unsustainable in many developed countries.Likewise, International Monetary Fund (IMF) updated that the externalborrowing received by the developed countries was unsustainable, andCarlo Cottarelli, Director of IMF's Fiscal Affairs Department, stated thatevenduring bigwars, the external borrowing received by the developedcountries had not been as high as it was (Cottarelli and IMF, 2010).

The final objective of the economic policies is to achieve a high andstable economic growth level. In the less developed or developing coun-tries, external borrowing is considered as an important resource forfinancing the economic growth. In the related literature, there is noconsensus about the way of impact of the external borrowing on theeconomic growth. There are study findings indicating that external bor-rowing can affect the economic growth either positively or negativelydepending on the level of borrowing. Because the negative impact of ex-ternal borrowing on the growth performance of the developed and de-veloping countries overweigh negatively in medium-term and longterm, the interest to this issue has increased. Especially governmentsand academic circles have increased their investigations for determin-ing and finding solution for this problem. Most of the studies in the lit-erature are linear but our estimates are non-linear and, unlike studies inthe literature, are considered regime changes. In this regard, first of all,

214 İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

the following the questions will be answered in this manuscript:(i) To what extent is the impact of external debt on the economicgrowth? (ii) Is the relationship between external debt and growthlinear? (iii) Does the impact of external debt on the economic growthchange depending on public borrowing and private sector borrowing?

2. Literature review

Paper first follows literature review of empirical relationship be-tween the external debt and economic growth. Basically, empiricalstudies are divided into two groups. The first group consists of the stud-ies which claim that external debt has a positive impact on the econom-ic growth; the second group comprises the studies which claim that ithas a negative effect on the economic growth. Such theoretical and em-pirical studies as Bakar and Hassan (2008), Umutlu et al. (2011), Çiçeket al. (2010), and Cohen (1991) put forward that low borrowing levelhas a positive relationship with growth. Such other studies as Tornelland Velasco (1992), Sachs (1989), Presbitero (2010), Uysal et al.(2009), Wijeweera et al. (2005), Pattillo et al. (2002) and Kumar andWoo (2010) indicate that the external debt, at high debt level, has anegative impact on the economic activities. Apart from the above-mentioned two types of researches, there are also researches in the lit-erature, indicating that the correlation between debt and economicgrowth is linear and non-linear. While Schclarek (2004), Blavy (2006)and Schclarek and Ramon-Ballester (2005) claim that they have a linearrelationship, some other studies such as Adam and Bevan (2005),Cordella et al. (2005), Pattillo et al. (2002), Smyth and Hsing (1995),and Cohen (1997) argue that they follow a non-linear pattern.

The theoretical literature about the correlation between growth andexternal borrowing extensively focuses on the adverse impact of thedebt burden. Krugman (1988) defines debt burden as the expected pay-back to be lower than the borrowed value. Cohen (1993), in his article,considers the relationship between the nominal values of investmentand borrowing as Laffer Curve. This curve asserts that the more in-creased the debt level after a threshold level is, the lower the expectedpayback. In the empirical study, debt burden hypothesis founded ourdifferent results? There are only a few studies which assess the directimpact of debt stock on the investment, in terms of econometrics. Inmany works, variables are employed by considering that the debtstock has both direct (by decreasing the incentives for the structural re-forms) and indirect impacts (through the impacts of investment) in theformof equations reduced for growth. AsWarner (1992) concludes thatdebt crisis decreases the investment in the middle income countries,Greene and Villanueva (1991), Serven and Solimano (1993), Elbadawiet al. (1997), Deshpande (1997), Fosu (1999) and Chowdhury (2001)support the debt burden hypothesis.

Pattillo et al. (2002) analyze 93 developing Sub-Saharan Africancountries and Latin American and Middle-Eastern Countries for the pe-riod covering 1969–1998. The article employs many different method-ologies (OLS, instrumental variables, fixed effects and GMM system)to show how there are different results in the econometric issues. It isasserted with empirical studies that the appropriate debt level has apositive impact on the growth, but high borrowing can prevent growth.The practical experiences of HIPCs (Heavily Indebted Poor Countries)agree with this idea. It concludes that although at the beginning theexternal borrowing aimed for financing the domestic investment op-portunities (to remedy the commercial shocks)? However, the factthat borrowing continued in the face of negative foreign conditionsand policies, it did not made a contribution to growth as it had been ex-pected. Cordella et al. (2005) look for the answer of the following ques-tions. Is the debt relief for supporting the growth? Is there any evidencefor HIPCs that suffer high debt problems and is there any need for fur-ther debt relief? The main question is to what extent and under whatconditions can borrowing become an obstacle before growth? To an-swer these questions, in thismanuscript, the impact of borrowing on in-vestment and growth in the last thirty years in HIPCs and non HIPCs as

well as what kind of impact the borrowing at different levels had on thepolicies or institutions of different qualities in these countries. To flattenthe short-term fluctuations, three-year averages of the series have beenused. This division has beenmade from1970 to 2002. Thismanuscript isdifferent from many studies in the literature in a few aspects. Firstly, ithas been controlled whether the relationship between growth and bor-rowing among the sub-samples is different as discussed or not (?). Afterdoing that, suchmethods asmany regression techniques which includesome threshold estimation and binding regressions. Secondly, whenborrowing is measured in the net present value method, this paper fol-lows the data set used in Kraay and Nehru (2004). Thirdly, contrary tosome related empirical studies, this manuscript employs official reliefand external debt service as the control variable with regard to the rela-tionship between external debt and growth. Fourthly, rather than usingproportion of GNP to external indebtedness, the proportion of GDP toexternal indebtedness has been used because GDP indicates the inde-pendent efficiency capacity of a country better. Analyses indicate thatthe relationship between growth and external borrowing depends onthe political and institutional quality of external borrowing. When theexternal indebtedness variables are considered, a concave relationshipseems to exist between growth and external debt only for the non-HIPCs.

Schclarek and Ramon-Ballester (2005) use data for seven periods,each of which consisting of five years between 1970 and 2002 (like1970–74; 1975–1979) for 20 Latin American and Caribbean countries.For the Latin American and Caribbean countries, the relationship be-tween the total external borrowing and economic growth level is tobe found significant and negative. As the total external borrowing con-sists of private external borrowing and public external borrowing, it isshown that the negative relationship between the foreign borrowingand growth is a negative relationship which results from the publicdebt and which does not result from the private debt. In other words,it is concluded that, while the high level of public external borrowingis relevant with low economic growth, the high level of private borrow-ing debt is not relevant with the low economic growth.

Emphasizing theways throughwhich external borrowing influencesgrowth in low-income countries, Clements and Krolzig (2003) yieldstrong supports for the debt burden hypothesis in their empirical esti-mates. They argue that, with the high external borrowing which isbeyond a definite threshold, the per capita income is related to lowgrowth rate. Depending on the variables used in the estimationmethod,they find the threshold value of 30–37% of GDP and 115–120% of export.All results have important estimates about the impact of debt relief ongrowth in HIPCs. Results explain a correlation stronger than the correla-tion between external borrowing and growth rate according to recentresearches focused on the developing countries. High borrowing ratedecreases the economic growth in the low-income countries.Moreover,asmentioned in the debt burden hypothesis, debt has a negative impacton growth after a definite threshold. Smyth and Hsing's (1995) study isa follow-up of Barro(1979), Eisner(1992), and Joines(1991) to analyzethe impact of debt on the economic growth and to test whether an op-timal debt ratewillmaximize the economic growth rate or not. It is con-cluded that, when public borrowing is used in the analysis of maximumdebt rate of economic growth, the threshold value will be 38.4% anddebt rate above this threshold will have a negative impact on economicgrowth.

Reinhart and Rogoff's (2010) annual observations on countries arecategorized into four groups according to the proportion of debt toGDP: the countries whose proportion of their external indebtedness totheir GDP is lower than 30% are the countries with low external indebt-edness; those with a proportion between 30 and 60% are the countrieswith medium external indebtedness rate; those with the said propor-tion between 60 and 90% are the countries with medium externalindebtedness rate and above 90% very high indebtedness. There is nocontradiction between foreign indebtment and growth until the debtrate reaches the threshold of 90%. High debt/GDP (of 90% and above)

215İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

is shown to be related with the low growth rate both in developed anddeveloping markets.

Testing the hypotheses regarding the causal relationship betweenthe growth rate of GDP and external borrowing accumulation rate,Chowdhury (1994) reaches consistent and efficient parameter esti-mates by means of applying three-stage least squares (3SLS) on annualobservations collected for the period between 1970 and 1988 in tenAsian and Pacific countries. That accounting the long-term impact ofGDP growth over the debt accumulation rate and statistical tests ofthe causal relationship between the foreign debt accumulation andGDP growth constitute one indication of the economic recessionshows that Bulow and Rogoff's (1988) proposal is rejected for all ofseven Asian countries. Structural model results show that all directand indirect impacts of private and public sectors' external borrowingon the GDP are positive.

Chen (2006) researches the common dynamics of external borrow-ing and growth. Although the impact of GPD growth on external bor-rowing is not linear, it is routinized (monotonous). Especially NearestNeighbor (NN) and Polynom Regression estimators are significantwhen the impact of external borrowing on growth and the impact ofgrowth on external borrowing are compared. Nadaraya–Watson Kernelestimator and Local Linear Estimator results are very similar. The resultsof these estimators are similar and show that the foreign debt may in-crease if the GDP increase is low compared to the previous periods butthat the foreign debt may decrease when GDP relatively increases inthe following periods. The results confirm that the Philippines needmore foreign debt because their GDP level, economic capacity andcapital accumulation are rather low.

Jayaraman and Lau (2009) use panel data for the empirical analysisof six Pacific countries during the period of 1988 to 2004. This paper ob-tains strong evidences to reject the null hypothesis of no co-integration.The panel results of GDP regression equation as a dependent variableconcludes that the external indebtedness coefficients and opennesscoefficients are positive and statistically significant but that the budgetdeficit variable is negatively significant.

Mariano and Villanueva (2006) provides the basic principles whichexplain the common interactions between the Neo-Classic GrowthModel, external debt and growth for a closed economy with the as-sumptions of learningmodel and globalizing capitalmarket by internal-izing the technology. External debt has influences on growth, which islinear with the interest rates and non-linear with the capital accumula-tion way. In the analysis of non-linear relations, as the GDP and exportare at the definite high level, they conclude that the increase of GDPand export have a positive influence on decreasing theburden of foreigndebt.

3. Methodology

Hamilton (1989) Markov-switching (MS) model which is alsoknown as Regime-switching model is one of the most popular non-linear time-series models in the literature. MS includes multiple-equations which can characterize the time-series behaviors in differentregimes. It is possible to have more complicated dynamic patterns withMS model by means of allowing switching between the equations. Aweird characteristic of MS model is the switching mechanism which iscontrolled with an unobservable state variable which follows first de-greeMarkov chain. EspeciallyMarkovian specialty regulates the currentstate which is affiliated to values of past without delay. Such a structurecan be effective for a random period of the time. This condition is in aclear contrary with Quandt (1972) random switch model in whichthose evident in the past are independent of time (Kuan, 2002).

The original Markov-switchingmodel focuses on themean behaviorof the variables. This model and its derivatives are widely applied to theanalysis of economic and financial time series (as is in Hamilton (1988,1989), Engel and Hamilton (1990), Garcia and Perron (1996), Goodwin(1993), Diebold et al. (1994), Engel (1994), Filardo (1994) and Kim and

Nelson (1998)). The greatest advantage of theMSmodel is its flexibilityin time-series models that are subject to change against regime shifts.All parameters of the theoretical conditional model can bemade depen-dent on the st state of the Markov model (Krolzig, 2000). State-spacemodels and MS parameters are widely used in the modeling of hetero-geneous dynamics of time series (Kang, 2010). In other words, the ad-vantages of the model can be expressed as follows: (i) the model'sfeatures regarding the number of regimes and connected regimesagainst the constancy of the parameters, (ii) the flexibility necessaryfor empirical research, and (iii) usefulness to the econometricians whowant to follow the co-integration systems which are dynamic, linearand non-stationary (Saltoğlu et al., 2003). According to the manuscriptof Anas et al. (2004) the basic advantage of the Markov-switchingprocess is the features such as the persistence of extreme observationsand the non-linearity and having the ability to take into account theasymmetry of time series. These features are considerable for theanalysis of business cycles.

A number of researchers worked in the modeling of economic andfinancial time series by having an interest in the discrete shifts ofparameters. Goldfeld and Quandt (1973) and Cosslett and Lee (1985)interpret the framework of Markov-switching regression as follows:when this framework is applied to a time series, its result is a modelwhich allows the sudden changes in variability of a series and non-linear dynamics. This approach has provided some new perspectivesover the long-term trend of GDP and the nature of business cycles. It ex-presses the regime 1 which is denoted by the state or st = 1 (e.g. con-traction period in cycle) and the regime 2 which is denoted by st = 2(expansion period in cycle). If there is a probable regime of differentK, it is assumed that the transition between the regimes is governedby a Markov chain with K state (Hamilton, 1996).

MS models are widely used to study the economic problems inwhich there are structural changes basically. In the approach that is ini-tiated by Hamilton (1989), the establishment of economic time series ismodeled as a vector auto-regression (VAR) in the process of parametersthat appears to be an output of the state of Markov process. A constantparameter which can be seen as a reduced form of forward lookingrational expectations is known as a vector auto-regression. In theliterature, several authors have recently started towork on the relation-ship between MS model and the forward looking MS Rational Expecta-tions models (MSRE). Some of the studies in this field are seen inLeeper and Zha (2003), Svensson and Williams (2005) and Blake andZampolli (2006). MSREmodels are more complex than the linear ratio-nal expectationsmodel because themodel should allow considering theprobability of future regime changes when the expectation occurs(Farmer Roger et al., 2009).

According to the manuscript of Hamilton (1990), the purpose of aneconometrician is to determine when shifts occur in order to estimatethe parameters that are defined in different regimes and to estimatethe rule of probability for the transition between regimes.

yt ¼

Xtβ1 þ ut utjstð Þ � NIDð0;X1

… st ¼ 1

: : :

Xtβ1 þ ut utjstð Þ � NIDð0;XM

… st ¼ M

8>>>><>>>>:

9>>>>=>>>>;

ð1Þ

More precisely, the auto-regressive model that Hamilton (1989)uses in his studies in order to analyze the GDP growth of USA, can begeneralized with the following equations:

Yt ¼ μst þXp

j¼1ϕjst− j Yt− j−μst− j

� �þ σstεt ð2Þ

ΔYt−μ stð Þ ¼ ϕ1 ΔYt−1−μ st−1ð Þð Þþ;…þ ϕpðΔYt−p−μ st−p

� �þ ut: ð3Þ

216 İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

The last equation above, the general form of MS model, is a form ofwriting of themultivariate Markov-switchingmodel just as in the stud-ies of Simon Van (1996), Frömmel et al. (2005), Liu andMümtaz (2010)and Bilgili et al. (2012). In this study, the relationship between growthand borrowing for Turkey will be analyzed by following a multivariatedynamic MS model.

4. Data and estimation outputs

The data are obtained from the CD of “World Development Indica-tors 2010” and the online web site of “World Development Indicators”.The data is composed of the annual data covering the years 1970–2009,but because of the problems encountered in the common data set andanalysis for Turkey, the data is covering the period that comprises theyears 1974–2009. The term (L) in some of the variables used in theanalysis indicates natural logarithm of the related variables.

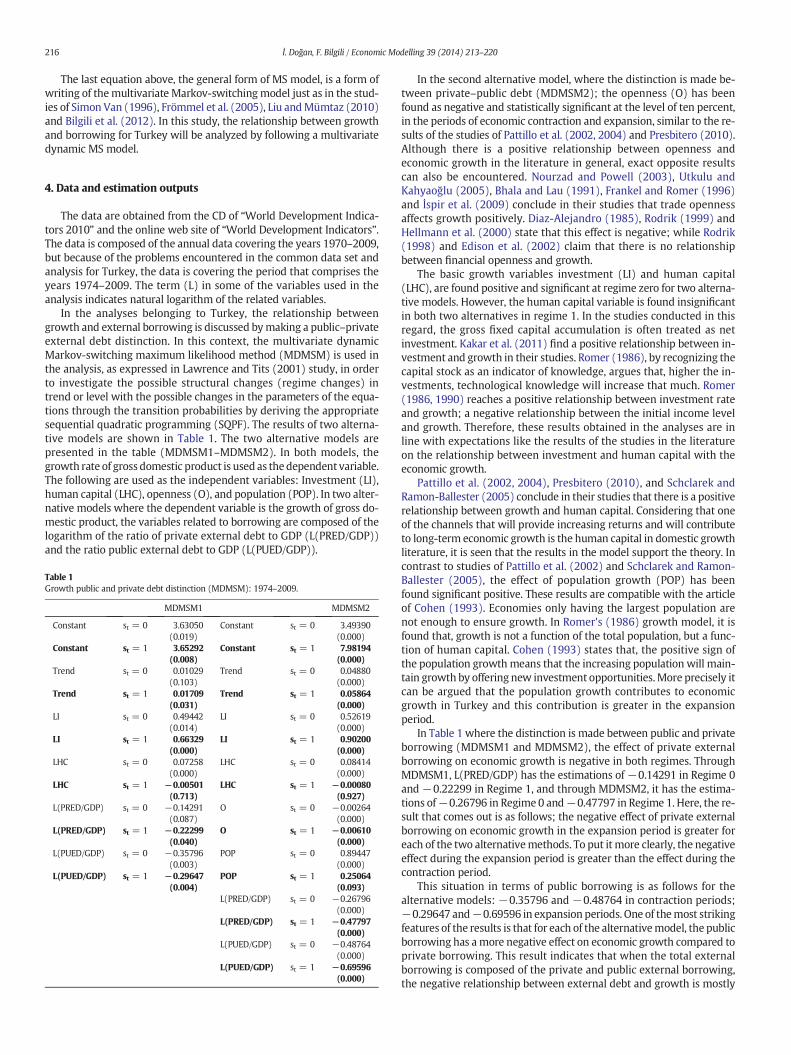

In the analyses belonging to Turkey, the relationship betweengrowth and external borrowing is discussed bymaking a public–privateexternal debt distinction. In this context, the multivariate dynamicMarkov-switching maximum likelihood method (MDMSM) is used inthe analysis, as expressed in Lawrence and Tits (2001) study, in orderto investigate the possible structural changes (regime changes) intrend or level with the possible changes in the parameters of the equa-tions through the transition probabilities by deriving the appropriatesequential quadratic programming (SQPF). The results of two alterna-tive models are shown in Table 1. The two alternative models arepresented in the table (MDMSM1–MDMSM2). In both models, thegrowth rate of gross domestic product is used as thedependent variable.The following are used as the independent variables: Investment (LI),human capital (LHC), openness (O), and population (POP). In two alter-native models where the dependent variable is the growth of gross do-mestic product, the variables related to borrowing are composed of thelogarithm of the ratio of private external debt to GDP (L(PRED/GDP))and the ratio public external debt to GDP (L(PUED/GDP)).

Table 1Growth public and private debt distinction (MDMSM): 1974–2009.

MDMSM1 MDMSM2

Constant st = 0 3.63050 Constant st = 0 3.49390(0.019) (0.000)

Constant st = 1 3.65292 Constant st = 1 7.98194(0.008) (0.000)

Trend st = 0 0.01029 Trend st = 0 0.04880(0.103) (0.000)

Trend st = 1 0.01709 Trend st = 1 0.05864(0.031) (0.000)

LI st = 0 0.49442 LI st = 0 0.52619(0.014) (0.000)

LI st = 1 0.66329 LI st = 1 0.90200(0.000) (0.000)

LHC st = 0 0.07258 LHC st = 0 0.08414(0.000) (0.000)

LHC st = 1 −0.00501 LHC st = 1 −0.00080(0.713) (0.927)

L(PRED/GDP) st = 0 −0.14291 O st = 0 −0.00264(0.087) (0.000)

L(PRED/GDP) st = 1 −0.22299 O st = 1 −0.00610(0.040) (0.000)

L(PUED/GDP) st = 0 −0.35796 POP st = 0 0.89447(0.003) (0.000)

L(PUED/GDP) st = 1 −0.29647 POP st = 1 0.25064(0.004) (0.093)

L(PRED/GDP) st = 0 −0.26796(0.000)

L(PRED/GDP) st = 1 −0.47797(0.000)

L(PUED/GDP) st = 0 −0.48764(0.000)

L(PUED/GDP) st = 1 −0.69596(0.000)

In the second alternative model, where the distinction is made be-tween private–public debt (MDMSM2); the openness (O) has beenfound as negative and statistically significant at the level of ten percent,in the periods of economic contraction and expansion, similar to the re-sults of the studies of Pattillo et al. (2002, 2004) and Presbitero (2010).Although there is a positive relationship between openness andeconomic growth in the literature in general, exact opposite resultscan also be encountered. Nourzad and Powell (2003), Utkulu andKahyaoğlu (2005), Bhala and Lau (1991), Frankel and Romer (1996)and İspir et al. (2009) conclude in their studies that trade opennessaffects growth positively. Diaz-Alejandro (1985), Rodrik (1999) andHellmann et al. (2000) state that this effect is negative; while Rodrik(1998) and Edison et al. (2002) claim that there is no relationshipbetween financial openness and growth.

The basic growth variables investment (LI) and human capital(LHC), are found positive and significant at regime zero for two alterna-tive models. However, the human capital variable is found insignificantin both two alternatives in regime 1. In the studies conducted in thisregard, the gross fixed capital accumulation is often treated as netinvestment. Kakar et al. (2011) find a positive relationship between in-vestment and growth in their studies. Romer (1986), by recognizing thecapital stock as an indicator of knowledge, argues that, higher the in-vestments, technological knowledge will increase that much. Romer(1986, 1990) reaches a positive relationship between investment rateand growth; a negative relationship between the initial income leveland growth. Therefore, these results obtained in the analyses are inline with expectations like the results of the studies in the literatureon the relationship between investment and human capital with theeconomic growth.

Pattillo et al. (2002, 2004), Presbitero (2010), and Schclarek andRamon-Ballester (2005) conclude in their studies that there is a positiverelationship between growth and human capital. Considering that oneof the channels that will provide increasing returns and will contributeto long-term economic growth is the human capital in domestic growthliterature, it is seen that the results in the model support the theory. Incontrast to studies of Pattillo et al. (2002) and Schclarek and Ramon-Ballester (2005), the effect of population growth (POP) has beenfound significant positive. These results are compatible with the articleof Cohen (1993). Economies only having the largest population arenot enough to ensure growth. In Romer's (1986) growth model, it isfound that, growth is not a function of the total population, but a func-tion of human capital. Cohen (1993) states that, the positive sign ofthe population growthmeans that the increasing population will main-tain growth by offering new investment opportunities.More precisely itcan be argued that the population growth contributes to economicgrowth in Turkey and this contribution is greater in the expansionperiod.

In Table 1 where the distinction is made between public and privateborrowing (MDMSM1 and MDMSM2), the effect of private externalborrowing on economic growth is negative in both regimes. ThroughMDMSM1, L(PRED/GDP) has the estimations of −0.14291 in Regime 0and −0.22299 in Regime 1, and through MDMSM2, it has the estima-tions of−0.26796 in Regime 0 and−0.47797 in Regime 1. Here, the re-sult that comes out is as follows; the negative effect of private externalborrowing on economic growth in the expansion period is greater foreach of the two alternativemethods. To put it more clearly, the negativeeffect during the expansion period is greater than the effect during thecontraction period.

This situation in terms of public borrowing is as follows for thealternative models: −0.35796 and −0.48764 in contraction periods;−0.29647 and−0.69596 in expansion periods. One of themost strikingfeatures of the results is that for each of the alternativemodel, the publicborrowing has amore negative effect on economic growth compared toprivate borrowing. This result indicates that when the total externalborrowing is composed of the private and public external borrowing,the negative relationship between external debt and growth is mostly

217İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

caused by thepublic debt. In otherwords, the high levels of public exter-nal borrowing seem to be associatedwith low economic growth, but thepresence of high levels of private external borrowing and its negativeeffect on economic growth are lower compared to the negative effectof public external borrowing.

In Table 2, in the models where the distinction is made betweenprivate–public external debt models (MDMSM1 and MDMSM2), com-pared to othermodels, the secondmodel (MDMSM2) is more appropri-ate due to the fact that it gives the lowest AIC value of−2.99820 and thehighest Log likelihood value of 73.96773. All MS models which makenon-linear estimations should be preferred against all opponents. Thelinearity test in Table 2 rejects the null hypotheses in one percentlevel of significance which suggests that two alternative models arelinear. In other words, the relationship between economic growth andborrowing variables is not linear. This result supports the studiesof Cordella et al. (2005), Adam and Bevan (2005), Chen (2006),Presbitero (2005), Kutivadze (2011), Pattillo et al. (2002) and Clementet al. (2004) which prove the existence of a non-linear relationship be-tween borrowing and economic growth. Each of the alternative model(the models of private–public external debt distinction) indicates thatwhen the current state of the relationship of growth and borrowing intime t is regime1, theprobability of the jumpof the growth and borrow-ing relationship from regime1 at time t+1 to regime zero is 0.34506onaverage.

During the transition probabilities, smoothed probabilitiesmay needto be observed over time (between regimes). Fig. 1 shows the smoothedprobabilities of contraction (regime 0) and expansion periods (regime1) for the two alternative models. Fig. 1a and b shows the transitionprobabilities of MDMSM1 alternative model in regime 0 and regime 1.The regime zero points cover the periods of 1974, 1977–1980, 1988–1991, 1994, 1998–1999, 2001 and 2008–2009. Regime 1 points coverthe periods of 1976, 1981–1987, 1992–1993, 1995–1997, 2000 and2002–2007. In Fig. 2a and b, the regime zero points for MDMSM2,which is considered best model in this paper, cover the periods of:1974, 1977–1978, 1980, 1985, 1988–1989, 1991, 1944, 1998–1999and 2001 and the regime zero points correspond the periods of:1975–1976, 1979, 1981–1984, 1986–1987, 1990, 1992–1993, 1995–1997, 2000 and 2002–2007. This is remarkable to observe the alterna-tive regimes in which there are periods of crisis and economic expan-sion that caused structural breaks in the conjuncture of the economiesof both the world and Turkey.

After the oil shocks of 1973 and 1979, there have been radical chang-es in economic policies throughout theworld.While the role of the statewas restricted in order to strengthen the free market economy, prioritywas given to liberalization of goods-service-financial markets. As thecrisis has been tried to be overcome by the economic policies thatwere put into effect on January 24, 1980, the transition into neo-liberal economic policies were being tried which were spread in theeconomy of Turkey and throughout the world. In Turkey, which startedfundamental changes in economic policies after 1980 by January 24decisions, the external shocks from time to time especially by the imple-mentation of open economy policies, have created a significant impact

Table 2Growth borrowing Markov-switching variance, transition probabilities smoothing andtest statistics: 1974–2009.

MDMSM1 MDMSM2

Sigma st = 0 0.03820 0.00357Sigma st = 1 0.04425 0.03862P{0|1} 0.28931 0.40082P{1|1} 0.71069 0.59918P{1|0} 0.42236 0.72818P{0|0} 0.57764 0.27182Log Likelihood 42.05741 73.96773AIC −1.44763 −2.99820Linearity test (Chi2) 40.875 (0.0000) 96.709 (0.0000)

on the Turkish economy. The purpose of the short-term decisions ofJanuary 24 decisions was to reduce the inflation in Turkey which wasaccelerated by the impact of oil shocks that occurred in the 1970s andfor the long-term, it was to make industrialization strategy outward-oriented.

The oil crisis in the years 1973–1974 had a negative impact onTurkey which is a major oil importer. Only for the year 1974, the exter-nal debt amounted to USD 359 million. In this period, Turkey has beenindebted to European Money Market for the first time, but due totheir short-term and high interest rates, it was ceased to borrow inthese markets. By the late 1970s, three separate external debtrescheduling agreements have been made as years 1978, 1979 and1980 and 5.5 billion dollars of debt was delayed. During this period, inorder to fix the rapidly deteriorating external balance, a $ 962 millionaid was pledged to Turkey by 16 OECD countries in 1979, and a$1 billion foreign debt suspension has been decided.

After January 24 decisions, the following occurred in the Turkisheconomy: the foundation of Capital Markets in 1981 and IstanbulStock Exchange in 1986; the permission of opening resident foreign cur-rency accounts, Central Bank is beginning to conduct government secu-rities auctions in 1985, great liberalization of foreign trade in 1983–84,partial liberalization of foreign exchange transactions in 1984, and theliberalization of capital movements in 1989. In 1989, after liberalizationof capital movements in 1989, as a result of political instability togetherwith inconsistencies in macroeconomic policies in 1990s, Turkey'seconomy has experienced fluctuations in domestic and foreign origin.The Gulf War in 1991, the economic crisis in 1994, the Asian crisis in1997, the Russian crisis in 1998 and the Marmara earthquake in 1999are the periods when the economy has serious problems.

After 1983 the external debt burden started to rise again, and then in1984, the growth rate increased to over 20%. Only between years 1984–1988 the external debts doubled. One of themost significant changes inTurkey's external borrowing was carried out since 1989. Starting fromthis date the external debt burden has started to withdraw fromthe dangerous point it reached and the “External Debt/GDP” ratio hasbeen started to reduce. In 1990, the amount of Turkey's debt was52.3 billion dollars. The ever-increasing external debt stock onlyshowed a decrease in 1994. But later that year, an upward trend contin-ued again and in 1995 it reached the level of 75.7 billion dollars. By theyear 1997, and it was foreseen for the consolidated budget to be equaland because of that it was aimed to shrink the expenditures in realterms, and to develop the budget revenues. The ratio of debt whichshowed a decrease between years 1996–1997, started to rise againbetween years 1998–2000.

The program of struggle with the exchange rate based inflationwas put into effect at the beginning of the year 2000. With this IMF-supported program, it was aimed to reduce inflation fast, to controlpublic deficit, and to restructure the financial sector. However, due tothe rigidity of this program, this program had to be abandoned by thecrisis of February 2001which is one of themost severe crises in history.After this crisis, Transition into the Strong Economy Program waslaunched in April. This program gave priority to structural reformsand regulations. With the program, the following were aimed: therestructuring of the financial sector, ensuring the independence of theCentral Bank, to increase transparency in governance, strengthening ofpublic finances and increasing the competition and efficiency in theeconomy. Transition into the Strong Economy Programhas been imple-mented successfully especially by the contribution of the abundance ofglobal liquidity and as a result the economy has achieved high growthrates. Besides, the inflation and interest rates were declined rapidly bycontrolling public deficits.

Justice and Development Party (AKP) which has been ruling Turkeysince the 2002General elections reached a period of stability around thediscourse that led to the new term, to expressing themselves to thevoters and to create a self-supporting block. These discourses are asfollows: “change”, “democracy”, “get rid of the military tutelage”,

1980 1990 2000 2010

0.25

0.50

0.75

1.00

a) Probability of Regime 0 Smoothed MDMSM1 b Probability of Regime 1 Smoothed MDMSM1

1980 1990 2000 2010

0.25

0.50

0.75

1.00

Fig. 1. The smoothed regime probabilities of alternative models. a: probability of Regime 0 Smoothed MDMSM1. b: probability of Regime 1 Smoothed MDMSM1.

218 İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

“becoming a member of the European Union”, and “solving the Kurdishproblem”. The annual average growth rate of the Turkish economyunder the administration of AKP between years 2003–2010 was 4.6%.

The credit bubble bursts by starting from the US housing market in2007 and led to a financial crisis. At the centers of the world economy,many executives, the U.S. Federal Reserve Chairman Greenspan, inparticular, expressed that they expect the markets to equilibrate them-selves and they were very surprised when they did not do so. The crisisthat began in theUSAwhich arose fromMortgage Loans has turned intoa global crisis starting from September 2008 and affected all countries.Many countries have relaxed their monetary policies and started to im-plement expansionary fiscal policies to mitigate the economic contrac-tion. Either the real economic indicators or the market related to theTurkish economy is showing that the economy has been dramaticallyadversely affected by the global crisis since the end of 2008. Therefore,all of these economic developments outlined one-to-one overlap withthe dates corresponding to the regime shifts shown in the analysis ofeach alternative model.

In general, the debt stock and thereby the increasing debt paymentsconstitute a major problem for less developed countries. The burden ofdebt payment limits the investment and capital accumulation, andnegatively affects economic growth from this aspect. The reasons ofthese can be stated as follows: (i) the use of the reserves in the country(the resource coming from the export) for debt payments, (ii) the neg-ative impact of high debt on the credit rating of the country, and (iii) asthe external debts created expectation of high taxes on production inthe future, this influenced negatively the stabilization programs thatwill be carried out by the government and also caused the productiveinvestments planned by the private sector to not to be carried outTherefore, the increase of the burden of the external debt means that

1980 1990 2000 2010

0.25

0.50

0.75

1.00

a) Probability of Regime 0 Smoothed MDMSM2

Fig. 2. a: probability of Regime 0 Smoothed MDMSM2

the returns caused by the improvement in the country's economy willgo to the external debt payments. In addition, the increasing debts cancause the finance of the debt by printing money by putting pressureon the government. In this case, the high amount of loan can be anincentive for the government to reduce the real value of the debt. How-ever, this may cause the inflation or even the hyperinflation. Therefore,the head of the most essential elements that is essential to ensuremacroeconomic stability is ensuring the sustainability of the debt andreducing the debt burden to reasonable levels and keeping at theselevels (Karagöl, 2010).

5. Summary and conclusion

The inadequate financial resources in the development process ofdeveloping countries such as Turkey caused these countries to head to-wards external resources through borrowing. In this case, the externaldebt becomes a highly important resource in the elimination of theinadequacy of the domestic capital accumulation, in the financing ofsome of the large investments and of the economic growth.

Turkey's debt structure in recent periods has been realized as a pri-vate sector dominated indebtedness from public dominated indebted-ness. This situation is also confirmed by the IMF's 2012 report onTurkey. MDMSM results support the hypotheses which state that theexternal debt affects economic growth negatively as in the studies ofPattillo et al. (2002), Schclarek and Ramon-Ballester (2005) and Uysalet al. (2009). Amore striking result is towards the following that the re-lationship between growth and borrowing is not linear for each of thealternative models. Another noteworthy point in the results is that thenegative impact of public borrowing is larger compared to privateborrowing for both periods of contraction and expansion. This may

1980 1990 2000 2010

0.25

0.50

0.75

1.00

b) Probability of Regime 1Smoothed MDMSM2

. b: probability of Regime 1 Smoothed MDMSM2.

219İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

mean that the public external debt is used more inefficiently. In devel-oping countries such as Turkey, public sector often resorts to externaldebt, in order to finance current expenditures.

MDMSM analysis reached conclusions which strongly support thedebt burden hypothesis. Accordingly, the negative effect of externalborrowing on growth requires taking steps towards reducing the exter-nal debt burden. And this can only be through an effective external debtmanagement. In order to achieve this; reducing the debt stock should beaimed by using the resources which were obtained from external bor-rowing, in more productive areas. In the Turkish economy wherethere is a serious problem such as lack of savings, channeling the foreignfunds in a way that will contribute to the achievement of productive in-vestment is of great importance. Using external debts in the areas thatincrease production is very important in terms of not encounteringpayment difficulties when the payment of the principal and interest ofthe external debt is due.

External borrowing means the resource that public and private sec-tor received fromoutside in return for interest.When the distribution ofthe private sector's long-term external debt of $130 billion according to2012 data of Undersecretaries of Turkish Treasury is observed, it is seenthat the 18% of this external borrowing ismade inmanufacturing indus-try. Non-industrial sector's share of external debt burden is around 73%.The banks' share is about one third only in the external debt stock. Thebanks make people use these resources that they provided mostly asconsumer loans. Therefore, for the private sector borrowing, theacquired borrowing should be primarily transferred to the industrialsector which directly increases production. The shocks in exchangerate are the nightmare of the firms that make external borrowing.Therefore, the firms should use the external debts that they receivedin the financing of investments in the export-oriented areas. The con-tractions that occur in international demand because of the reasons ofsuch as global economic crisis cause the reduction in export opportuni-ties. In this case, it makes the riskiness in the external debt even moreimportant. Therefore, it will be a very important and appropriatedecision to make country diversification in foreign trade because thenecessary resources for external debt payments are met from theproceeds in export.

References

Adam, Christopher S., Bevan, David L., 2005. Fiscal deficits and growth in developingcountries. J. Public Econ. 89, 571–597.

Anas, J., Billio, M., Ferrara, L., Duca, M.L., 2004. Business cycle analysis with multivariateMarkov switching models. University of Venice Department of Economics WorkingPapers, 04, 02.

Bakar, Abu Nor'aznin, Hassan, Sallahuddin, 2008. Empirical evaluation on external debt ofMalaysia. Int. Bus. Econ. Res. J. 7 (2), 95–108.

Barro, Robert J., 1979. On the determination of the public debt. J. Polit. Econ. 87 (5),940–971 (Part 1, October).

Bhala, S., Lau, L.J., 1991. Openness, technological progress, and economic growth indeveloping countries. Background Paper for World Development Report.

Bilgili, F., Tülüce, N.S.H., Doğan, İ., 2012. The determinants of FDI in Turkey: a MarkovRegime-switching approach. Econ. Model. 29, 1161–1169.

Blake, A.P., Zampolli, F., 2006. Optimal monetary policy in Markov-switching models withrational expectations agents. Bank of England Working Paper No. 298.

Blavy, Rodolphe, 2006. Public debt and productivity: the difficult quest for growth inJamaica. IMF Working Paper, 06/235, pp. 2–24.

Bulow, J., Rogoff, K., 1988. Sovereign debt: ıs to forgive to forget? NBERWorking Paper, No2623.

Chen, Si., 2006. External Debt and Growth Dynamics. Unpublished M.A. thesis, School ofEconomics and Social Sciences, Singapore Management University.

Chowdhury, Khorshed, 1994. A structural analysis of external debt and economic growth:some evidence from selected countries in Asia and the Pacific. Appl. Econ. 26,1121–1131.

Chowdhury, Abdur R., 2001. Foreign Debt and Growth in Developing Countries, PaperPresented at WIDER Conference on Debt Relief, Helsinki: United Nations University,August.

Çiçek, H., Gözegir, S., Çevik, E., 2010. Bir Maliye Politikası Aracı Olarak Borçlanma veEkonomik Büyüme İlişkisi: Türkiye Örneği (1990–2009). Cumhuriyet Üniv. İktisadive İdari Bilimler Derg. 11 (1), 141–153.

Clements, Michael P., Krolzig, Hans-Martin, 2003. Business cycle asymmetries: character-ization and testing based on Markov-switching autoregressions. J. Bus. Econ. Stat. 21(1), 196–211 (Jan).

Cohen, Daniel, 1991. Private Lending to Sovereign States: A Theoretical Autopsy. MITPress, Cambridge, MA (1991).

Cohen, Daniel, 1993. Low Investment and Large LDC Debt in the 1980s. Am. Econ. Rev. 83,437–449.

Cohen, Daniel, 1997. Growth and external debt: a new perspective on the African andLatin American tragedies. CEPR Discussion Papers 1753, C.E.P.R. Discussion Papers.

Cordella, T., Ricci, Luca A., Ruiz-Arranz, M., 2005. Debt overhang or debt ırrelevance?Revisiting the debt-growth link. IMF Working Paper, WP 05/223.

Cosslett, S.R., Lee, L.F., 1985. Serial correlation in discrete variable models. J. Econ. 27,79–97.

Cottarelli, C., IMF, 2010. Advanced economies need long-term efforts to tame public debt,IMF studies find. Press Release No. 10/322 (http://www.imf.org/external/np/sec/pr/2010/pr10322.htm (Accessed Date April, 2011)).

Deshpande, Ashwini, 1997. The debt overhang and the disincentive to ınvest. Dev. Econ.52, 169–187 (February).

Diaz-Alejandro, C., 1985. Goodbye financial repression, hello financial repression. J. Dev.Econ. 19.

Diebold, F.X., Lee, J.H., Weinbach, G., 1994. Regime switching with time-varying transitionprobabilities. In: Hargreaves, C., Granger, C.W.J., Mizon, G. (Eds.), Nonstationary TimeSeries Analysis and Cointegration (Advanced Texts in Econometrics). Oxford Univer-sity Press, Oxford, pp. 283–302.

Edison, H.J., Levine, R., Ricci, L.A., Slok, T., 2002. International financial ıntegration andeconomic growth. J. Int. Money Financ. 21, 749–776.

Eisner, Robert, 1992. Deficits: which, how much, and so what? Am. Econ. Rev. 295–298(May).

Elbadawi, I., Ndulu, B., Ndung'u, N., 1997. Debt Overhang and Economic Growth in Sub-Saharan Africa. IMF Institute, Washington DC.

Engel, Charles, 1994. Can the Markov switching model forecast exchange rates? J. Int.Econ. 36 (1–2), 151–165 (Elsevier).

Engel, C., Hamilton, J.D., 1990. Long swings in the dollar: are they in the data and domarkets know it? Am. Econ. Rev. 80 (4), 689–713.

Farmer Roger, E.A., Tao, Zha,Waggoner, Daniel F., 2009. UnderstandingMarkov-switchingrational expectations models. Nber Working Paper Series, Working Paper 14710.

Filardo, Andrew J., 1994. Business-cycle phases and their transitional dynamics. J. Bus.Econ. Stat. 12 (3), 299–308 (Juy).

Fosu, A.K., 1999. The External debt burden and economic growth in the 1980s: evidencefrom sub Saharan Africa. Can. J. Dev. Stud. 20 (2), 307–318.

Frankel, J., Romer, D., 1996. Trade and growth: an empirical investigation. National Bureauof Economic Research Working Paper (http://papers.nber.org/papers/w5476.,(Accessed Date October 2012)).

Frömmel,M., MacDonald, R., Menkhoff, L., 2005. Markov switching regimes in amonetaryexchange rate model. Econ. Model. 22 (3), 485–502 (Elsevier).

Garcia, Rene, Perron, Pierre, 1996. An analysis of the real interest rate under regime shifts.Rev. Econ. Stat. 78 (1), 111–125 (MIT Press).

Goldfeld, S.M., Quandt, R.E., 1973. A Markov model for switching regression. J. Econ. I,3–16.

Goodwin, T.H., 1993. Business-cycle analysis with a Markov-switchingmodel. J. Bus. Econ.Stat. 11 (3), 331–339.

Greene, J., Villanueva, D., 1991. Private investment in developing countries. IMF Staff Pa-pers. 38, pp. 33–58.

Hamilton, J.D., 1988. Rational-expectations econometric analysis of changes in regime: aninvestigation of the term structure of interest rates. J. Econ. Dyn. Control. 12, 385–423.

Hamilton, J.D., 1989. A new approach to the economic analysis of nonstationary timeseries and the business cycle. Econometrica 57 (2), 357–384.

Hamilton, J.D., 1990. Analysis of time series subject to changes in regime. J. Econ. 45,39–70.

Hamilton, J.D., 1996. Specification testing inMarkov switching time-seriesmodels. J. Econ.70, 127–157.

Hellmann, T., Murdock, K., Stiglitz, J.E., 2000. Liberalization, moral hazard in banking andprudential regulation: are capital requirements enough? Am. Econ. Rev. 90, 147–165.

İspir, M. Serdar, Ersoy, B. Açıkgöz, Yılmazer, Mine, 2009. Türkiye'nin BüyümeDinamiğinde İhracat mı İthalat mı Daha Etkin? Dokuz Eylül Üniv. İktisadi ve İdariBilimler Fak. Derg. 24 (1).

Jayaraman, T.K., Lau, Evan, 2009. Does external debt lead to economic growth in Pacificisland countries. J. Policy Model 31, 272–288.

Joines, Douglas H., 1991. How large a federal budget deficit can we sustain? Contemp.Policy Issues 1–11 (July).

Kakar, Z., Khan, K., Bashir, A., Khan, M.J., 2011. Relationship between education andeconomic growth in Pakistan: a time series analysis. J. Int. Acad. Res. 11 (1).

Kang, Kyu Ho, 2010. State-Space Models with Endogenous Markov Regime SwitchingParameters. (http://apps.olin.wustl.edu/MEGConference/Files/pdf/2010/4.pdf(Accessed Date December 2012)).

Erdal Tanas, Karagöl, 2010. Geçmişten Günümüze Türkiye'de Dış Borçlar, Siyaset,Ekonomi ve Toplum Araştırmaları Vakfı. 26 (Ağustos).

Kim, Chang-Jin, Nelson, Charles R., 1988. Business cycle turning points, a new coincidentindex, and tests of duration dependence based on a dynamic factor model withregime switching. Rev. Econ. Stat. 80 (2), 188–201 (May).

Kraay, Aart, Nehru, Vikram, 2004. When is debt sustainable? World Bank Policy ResearchWorking Paper No. 3200.

Krolzig, H.M., 2000. Predicting Markov-switching vector autoregressive process. NuffieldCollege Economics Working Papers W31.

Krugman, Paul, 1988. Financing vs. forgiving a debt overhang. J. Dev. Econ. 29, 253–268.Kuan, C.M., 2002. Lecture on TheMarkov Switching, Institute of Economics Academia Sinica.

(http://idv.sinica.edu.tw/ckuan/pdf/lecmarkn.pdf, (Accessed Date May 2012)).Kumar, Manmohan S., Woo, J., 2010. Public Debt and Growth. IMF Working Papers,

10/174. International Monetary Fund.

220 İ. Doğan, F. Bilgili / Economic Modelling 39 (2014) 213–220

Kutivadze, Natia, 2011. Public Debt, Domestic and External Financing, and EconomicGrowth, Dıpartımento Dı Scıenze Economıche Azıendalı E Statıstıche. WorkingPaper No. 12.

Leeper, E.M., Zha, T., 2003.Modest policy interventions. J.Monet. Econ. 50 (8), 1673–1700.Liu, P., Mümtaz, H., 2010. Evolving macroeconomic dynamics in a small open economy:

an estimated Markov switching DSGE model for the United Kingdom. WorkingPaper 397, Bank of England.

Mariano, Roberto S., Villanueva, Delano P., 2006. External Debt, Adjustment and Growth,Fiscal Policy and Management in East Asia. National Bureau of Economic Research,Cambridge, Massachusetts.

Nourzad, F., Powell, J.J., 2003. Openness, growth, and development: evidence from a panelof developing countries. Sci. J. Adm. Dev. 1 (1), 72–94.

Pattillo, C., Poirson, H., Ricci, L., 2002. External debt and growth. IMF Working Paper, WP02/69.

Pattillo, C., Poirson, H., Ricci, L., 2004. What are the channels through which external debtaffects growth. IMF Working Paper, WP 04/15.

Presbitero, Andrea F., 2005. The debt-growth nexus: a dynamic panel data estimation. 46Riunione Scientifica Annuale of the Società Italiana degli Economisti (SIE), Naples,October 21st–22nd.

Presbitero, Andrea F., 2010. Total public debt and growth in developing countries,Università Politecnica Delle Marche, Department Of Economics, Money FinanceResearch Group. Mofir Working Paper, No 44.

Quandt, Richard E., 1972. A new approach to estimating switching regressions. J. Am. Stat.Assoc. 67 (338), 306–310.

Reinhart, Carmen M., Rogoff, Kenneth S., 2010. Growth in a time of debt. Am. Econ. Rev.Pap. Proc. 1–25.

Rodrik, D., 1998. Why do more open economies have bigger governments? J. Polit. Econ.106, 997–1034.

Rodrik, D., 1999.Where did all the growth go? External shocks, social conflict, and growthcollapses. J. Econ. Growth 4, 358–412.

Romer, Paul M., 1986. Increasing returns and long-run growth. J. Polit. Econ. 94 (5),1002–1037 (October).

Romer, Paul M., 1990. Endogenous technological change. J. Polit. Econ. 98 (5), 71–102(October).

Sachs, Jeffrey, 1989. The debt overhang of developing countries. In: Calvo, Guillermo, et al.(Eds.), Debt Stabilization and Development: Essays in Memory of Carlos DiazAlejandro. Basil Blackwell, Oxford, pp. 80–102.

Saltoğlu, B., Şenyüz, Z., Yoldaş, E., 2003. Modeling Business Cycles with Markov SwitchingVAR Model: An Application On Turkish Business Cycles. (www.econturk.org/Turkisheconomy/msvar.doc, (Accessed Date October 2012)).

Schclarek, A., 2004. Debt and Economic Growth in Developing and Industrial Countries.(http://www.nek.lu.se/publications/workpap/Papers/WP05_34.pdf, (Accesseddate March 2012)).

Schclarek, A., Ramon-Ballester, F., 2005. External Debt and Economic Growth in LatinAmerica. (http://www.cbaeconomia.com/Debt-latin.pdf. (Accessed dateMay 2012)).

Serven, L., Solimano, A., 1993. Debt crisis adjustment policies and capital formation indeveloping countries: where do we stand? World Dev. 21, 127–140.

Simon Van, N., 1996. Regime Switching as a Test for Exchange Rate Bubbles. 11, 219–251.Smyth, David J., Hsing, Yu, 1995. In search of an optimal debt ratio for economic growth.

Contemp. Econ. Policy 13 (4), 51–59.Svensson, L.E., Williams, N., 2005. Monetary Policy with Model Uncertainty: Distribution

Forecast Targeting. Princeton University (Manuscript).Tornell, Aaron, Velasco, Andes, 1992. The tragedy of the commons and economic growth:

why does capital flow from poor to rich countries? J. Polit. Econ. 100 (6), 1208–1231(University of Chicago Press).

Umutlu, Goknur, Alizadeh, Neda, Erkilic, Ahmet, Yakup, 2011. Maliye PolitikasiAraçlarından Borclanma ve Vergilerin Ekonomik Buyumeye Etkileri. UludagUniversitesi İktisadi ve İdari Bilimler Fakultesi Dergisi No. 1, 75–93.

Utkulu, Utku, Kahyaoglu, Hakan, 2005. Ticari ve Finansal Aciklik Türkiye'de Buyumeyi NeYonde Etkiledi? Türkiye Ekonomi Kurumu Tartısma Metni No 13.

Uysal, D., Özer, H., Mucuk, M., 2009. Dış Borçlanma ve Ekonomik Büyüme İlişkisi:Türkiye Örneği (1965–2007). Atatürk Üniv. İktisadi ve İdari Bilimler Derg. 23(4), 161–178.

Warner, A., 1992. Did the debt crisis cause the investment crisis? Q. J. Econ. 1161–1186.Wijeweera, A., Brian, D., Palitha, P., 2005. Economic growth and external debt servicing: a

cointegration analysis of Sri Lanka, 1952 to 2002.Working Paper Series in Economics.University of New England School of Economics.