The nickel market outlook - can the laterite revolution continue?

34

The nickel market outlook – can the laterite revolution continue? July 2013 Jim Lennon Consultant to: Macquarie Capital Securities (Europe) Ltd +44 203 037 4271 [email protected] In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. Please see disclaimer. Page 1

-

Upload

informa-australia -

Category

Business

-

view

4.899 -

download

0

Transcript of The nickel market outlook - can the laterite revolution continue?

The nickel market outlook – can the laterite

revolution continue?

July 2013

Jim Lennon

Consultant to:

Macquarie Capital Securities (Europe) Ltd

+44 203 037 4271

In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an investment decision on the basis of this research,

the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. Please see

disclaimer.

Page 1

The changing face of the nickel market

Huge needs for new capacity driven by explosion in Chinese demand since 2000

Nickel shortage up to 2006/07 led to three responses:

Growth in 200-series stainless steel (1-2% Ni) as a substitute for 300-series (8-9% Ni)

Processing of low-grade laterite nickel ores into nickel pig iron in China

$30bn+ spent by non-Chinese industry to expand production (including New Caledonia)

In the face of declining sulphide reserves, solution to growth was mainly from using low-grade laterites (limonites) by pressure acid leach processes (PAL) or from higher-grade laterites (saprolites) using conventional ferronickel smelting.

Soaring capex and major technical challenges have made this “solution” economically unviable in the eyes of the industry.

The “new” solution has been the development of low-capex/high opex nickel pig iron (NPI) in China.

Main questions for the market are: Economics of NPI now and into the future – when does this end?; What are the economics of the alternatives? Will we revert back to PAL/FeNi “solution” or there alternatives (e.g., low grade sulphides?).

Page 2

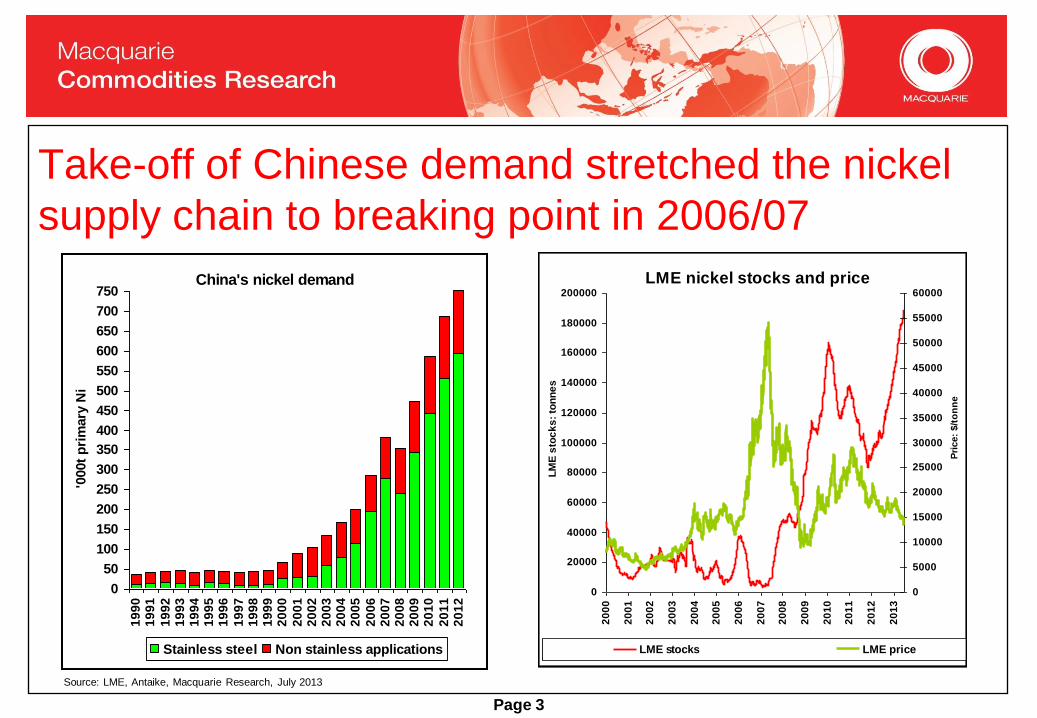

Take-off of Chinese demand stretched the nickel

supply chain to breaking point in 2006/07

China's nickel demand

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

'000t

pri

mary

Ni

Stainless steel Non stainless applications

Page 3

Source: LME, Antaike, Macquarie Research, July 2013

LME nickel stocks and price

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

LM

E s

toc

ks

: to

nn

es

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

55000

60000

Pri

ce:

$/t

on

ne

LME stocks LME price

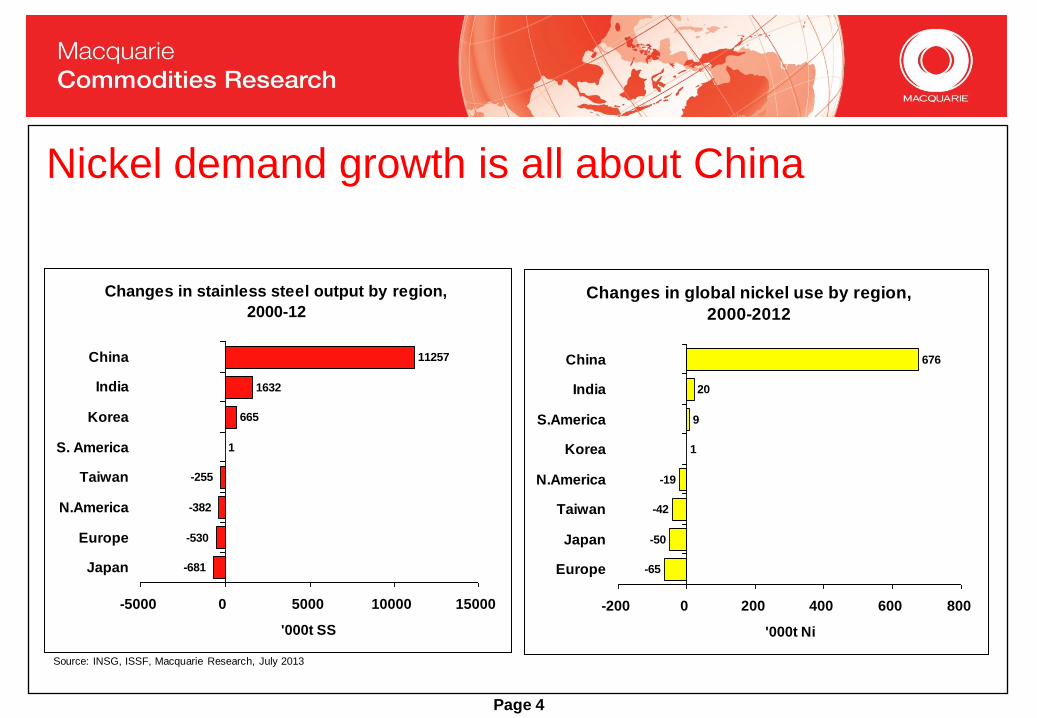

Nickel demand growth is all about China

Changes in stainless steel output by region,

2000-12

-681

-530

-382

-255

1

665

1632

11257

-5000 0 5000 10000 15000

Japan

Europe

N.America

Taiwan

S. America

Korea

India

China

'000t SS

Changes in global nickel use by region,

2000-2012

-65

-50

-42

-19

1

9

20

676

-200 0 200 400 600 800

Europe

Japan

Taiwan

N.America

Korea

S.America

India

China

'000t Ni

Source: INSG, ISSF, Macquarie Research, July 2013

Page 4

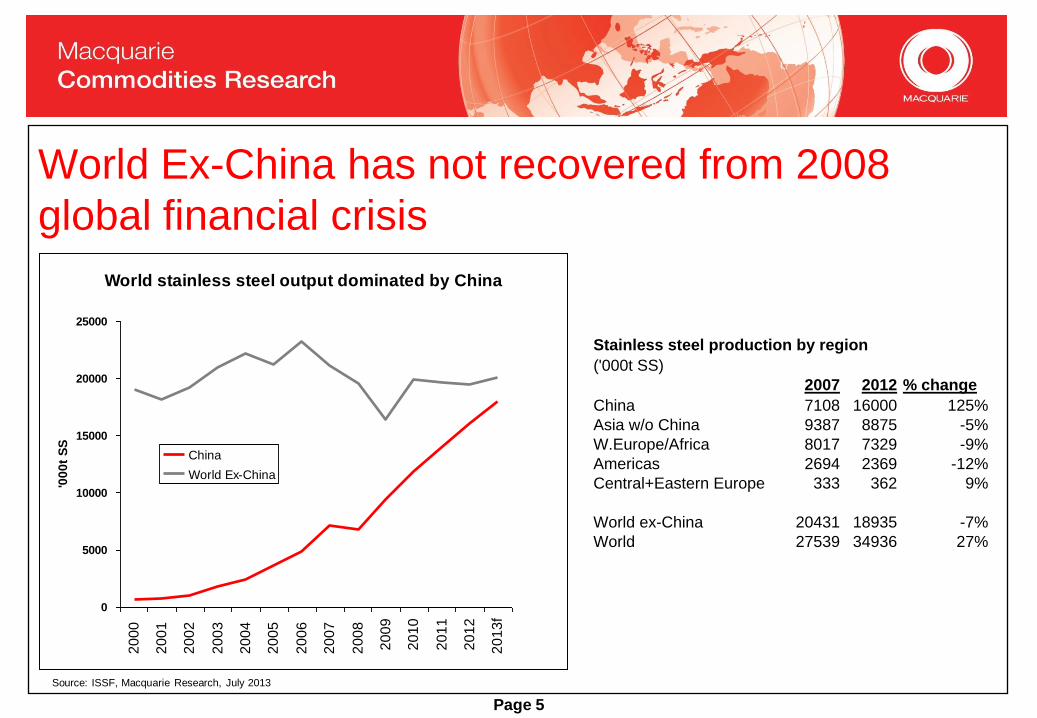

World Ex-China has not recovered from 2008

global financial crisis

World stainless steel output dominated by China

0

5000

10000

15000

20000

25000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

f

'00

0t

SS

China

World Ex-China

Stainless steel production by region

('000t SS)

2007 2012 % change

China 7108 16000 125%

Asia w/o China 9387 8875 -5%

W.Europe/Africa 8017 7329 -9%

Americas 2694 2369 -12%

Central+Eastern Europe 333 362 9%

World ex-China 20431 18935 -7%

World 27539 34936 27%

Source: ISSF, Macquarie Research, July 2013

Page 5

Primary nickel supply has also been all about China since

2008 – surge in supply too much for market

7 -1 3 12 13 18 7 8

103

62 64

102 86 926850

1820

49

1 256

-37

-103

27

76

55

-7

-110

-90

-70

-50

-30

-10

10

30

50

70

90

110

130

150

170

190

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

'000t

ni

China Rest of world Total

YoY growth in nickel production

Source: INSG, Macquarie Research, July 2013

Page 6

The short term – still awful with more cuts needed – LME

stocks up 51kt in 2012 and 46kt in 2013 YTD

LME nickel stocks and prices over the past year -

surplus!

13000

14000

15000

16000

17000

18000

19000

Ju

l-1

2

Au

g-1

2

Sep

-12

Oc

t-1

2

No

v-1

2

Dec

-12

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

Ju

n-1

3

LM

E c

as

h p

ric

e:

$/t

100000

110000

120000

130000

140000

150000

160000

170000

180000

190000

LM

E s

toc

ks

: to

nn

es

LME price LME stocks

Page 7

Source: LME, Antaike, Macquarie Research, July 2013

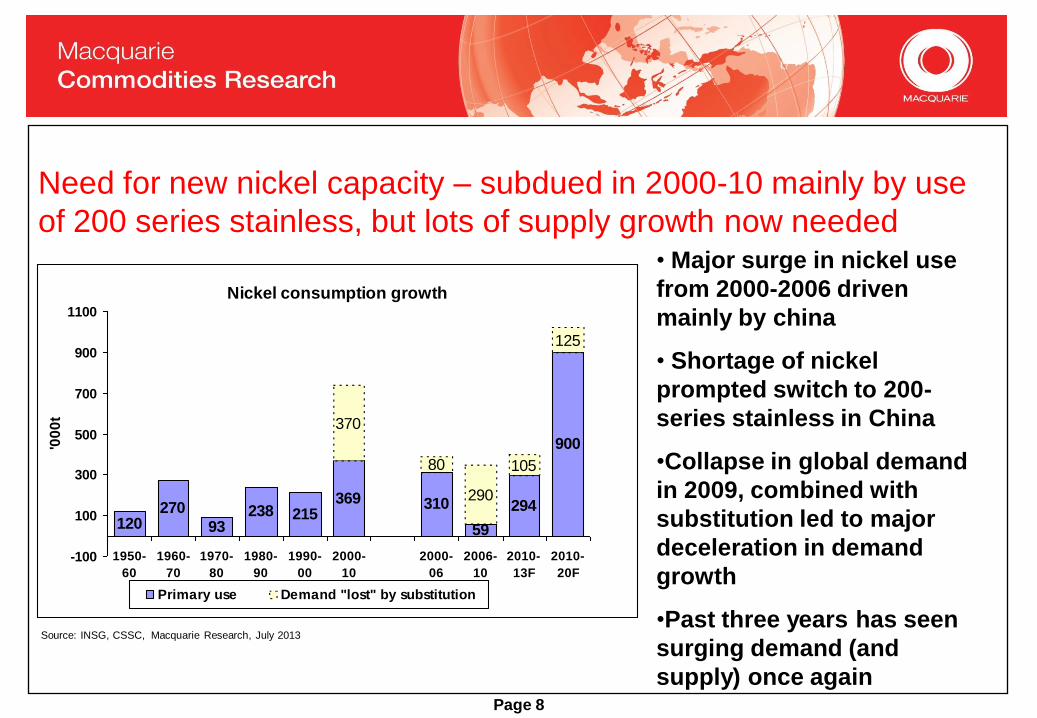

Need for new nickel capacity – subdued in 2000-10 mainly by use

of 200 series stainless, but lots of supply growth now needed • Major surge in nickel use

from 2000-2006 driven

mainly by china

• Shortage of nickel

prompted switch to 200-

series stainless in China

•Collapse in global demand

in 2009, combined with

substitution led to major

deceleration in demand

growth

•Past three years has seen

surging demand (and

supply) once again

Source: INSG, CSSC, Macquarie Research, July 2013

Nickel consumption growth

120270

93238 215

369 310

59

294

900

370

80

290

105

125

-100

100

300

500

700

900

1100

1950-

60

1960-

70

1970-

80

1980-

90

1990-

00

2000-

10

2000-

06

2006-

10

2010-

13F

2010-

20F

'00

0t

Primary use Demand "lost" by substitution

Page 8

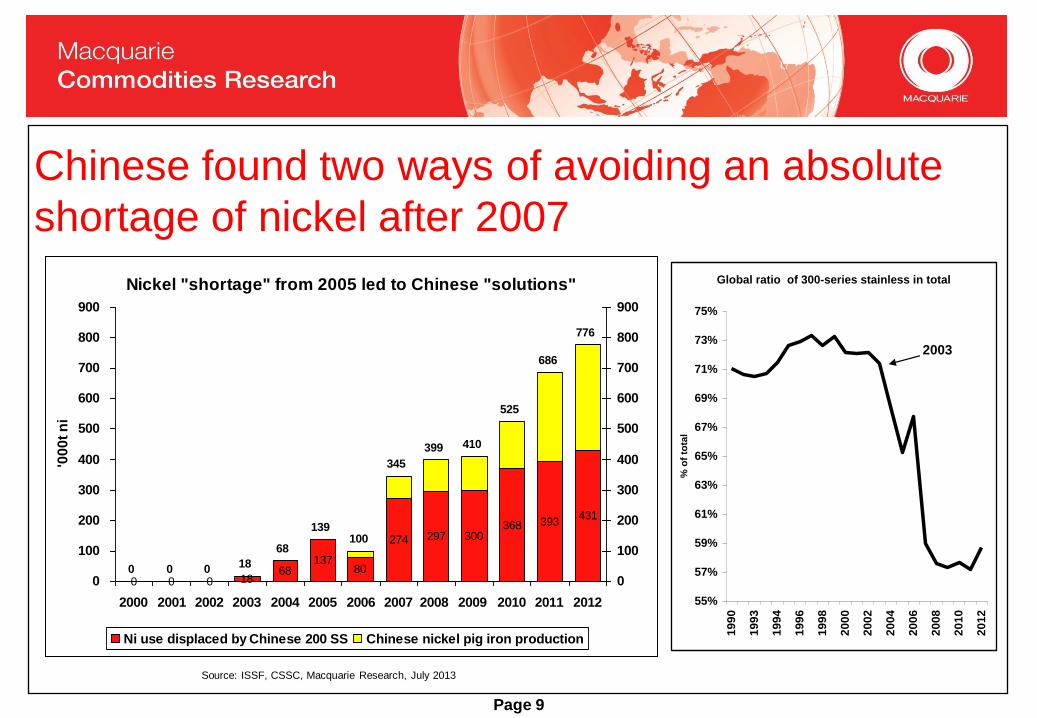

Chinese found two ways of avoiding an absolute

shortage of nickel after 2007

Source: ISSF, CSSC, Macquarie Research, July 2013

Nickel "shortage" from 2005 led to Chinese "solutions"

0 0 0 1868

13780

274 297 300368 393

431

0 0 0 18

68

139100

345

399 410

525

686

776

0

100

200

300

400

500

600

700

800

900

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

'00

0t

ni

0

100

200

300

400

500

600

700

800

900

Ni use displaced by Chinese 200 SS Chinese nickel pig iron production

Page 9

Global ratio of 300-series stainless in total

55%

57%

59%

61%

63%

65%

67%

69%

71%

73%

75%

19

90

19

93

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

% o

f to

tal

2003

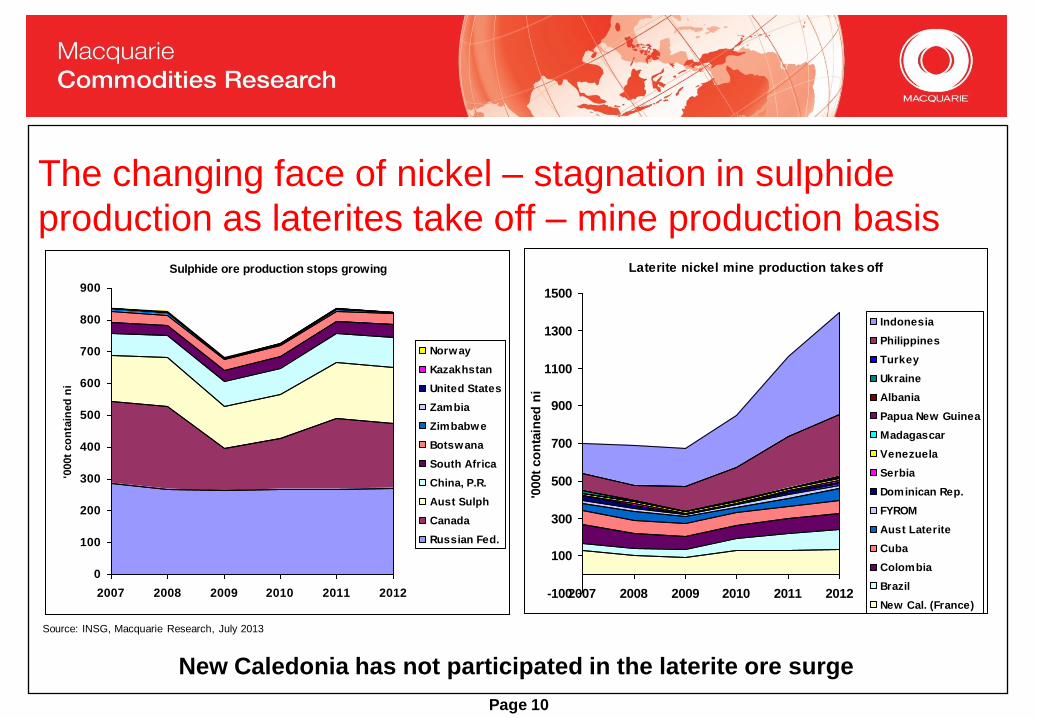

The changing face of nickel – stagnation in sulphide

production as laterites take off – mine production basis

Page 10

Source: INSG, Macquarie Research, July 2013

Laterite nickel mine production takes off

-100

100

300

500

700

900

1100

1300

1500

2007 2008 2009 2010 2011 2012

'000t

co

nta

ined

ni

Indonesia

Philippines

Turkey

Ukraine

Albania

Papua New Guinea

Madagascar

Venezuela

Serbia

Dominican Rep.

FYROM

Aust Laterite

Cuba

Colombia

Brazil

New Cal. (France)

Sulphide ore production stops growing

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012

'000t

co

nta

ined

ni

Norway

Kazakhstan

United States

Zambia

Zimbabwe

Botswana

South Africa

China, P.R.

Aust Sulph

Canada

Russian Fed.

New Caledonia has not participated in the laterite ore surge

The growing role of Indonesia and the Philippines

Source: Philippines Mines and Geosciences Bureau, INSG, GTIS, Macquarie Research, July 2013

Mine production overstates the actual impact due to massive ore stocking in China and

also >50% of ore from Philippines not being used as nickel, but iron ore

Page 11

Indonesia and Philippines share in global mine

production

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012

% o

f w

orl

d m

ine p

rod

ucti

on

Nickel ore production in Indonesia and the

Philippines

-100

100

300

500

700

900

1100

2007 2008 2009 2010 2011 2012'0

00t

co

nta

ined

nic

kel

New Caledonia Indonesia Philippines

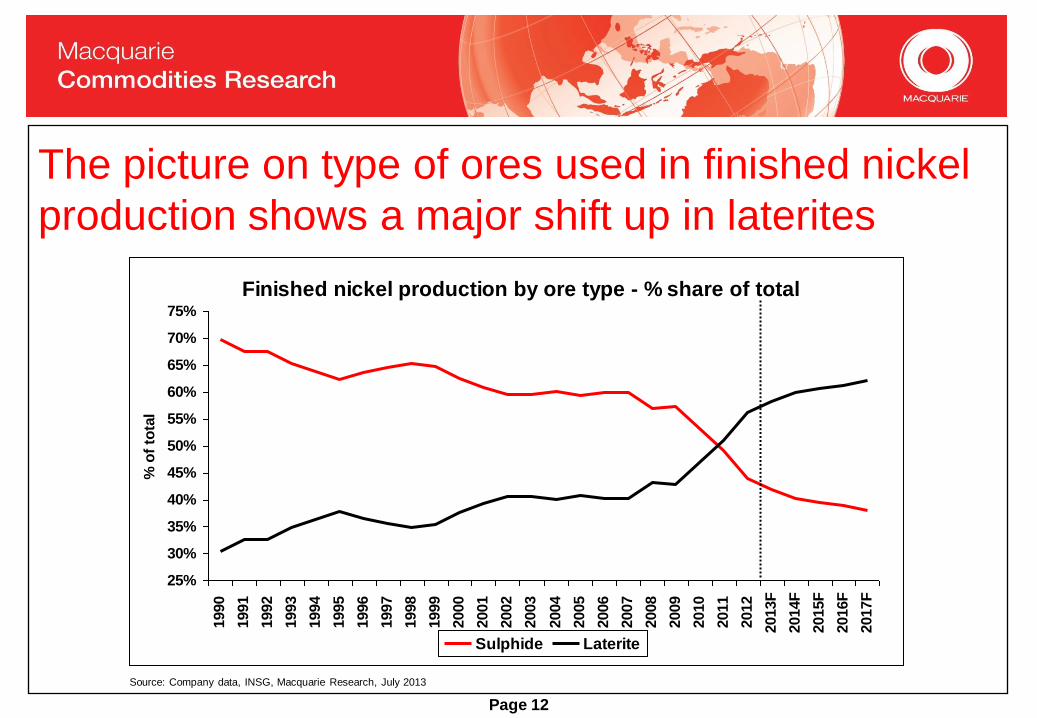

The picture on type of ores used in finished nickel

production shows a major shift up in laterites

Finished nickel production by ore type - % share of total

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

2014F

2015F

2016F

2017F

% o

f to

tal

Sulphide Laterite

Page 12

Source: Company data, INSG, Macquarie Research, July 2013

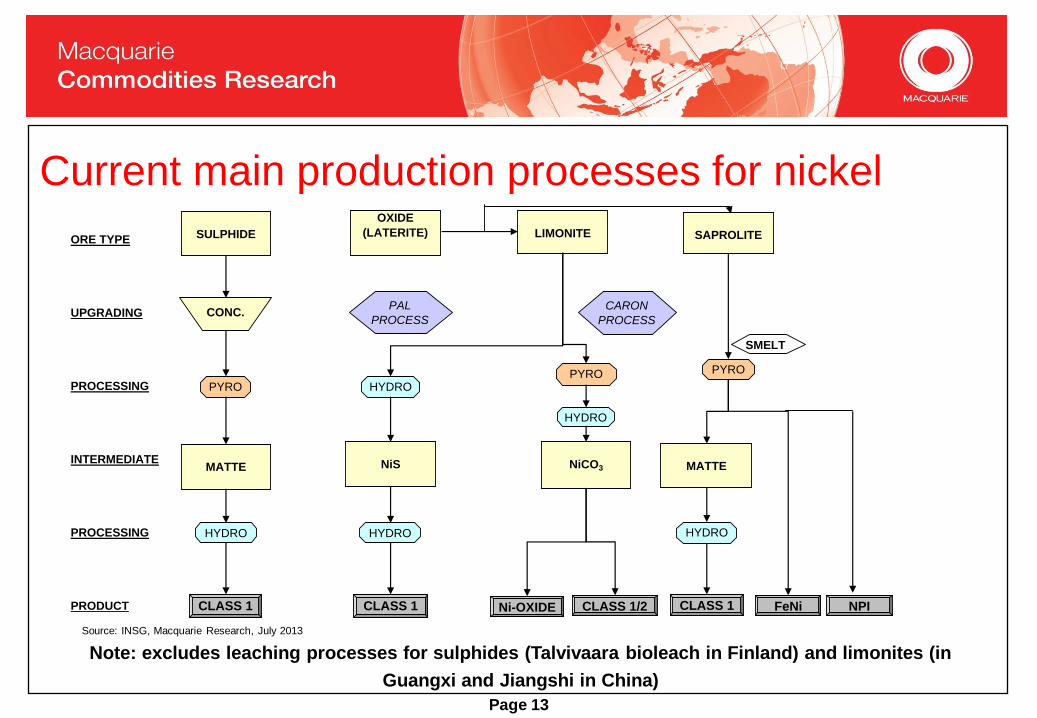

Current main production processes for nickel

Note: excludes leaching processes for sulphides (Talvivaara bioleach in Finland) and limonites (in

Guangxi and Jiangshi in China) Page 13

ORE TYPE

UPGRADING

PROCESSING

INTERMEDIATE

PROCESSING

PRODUCT

SULPHIDE

OXIDE

(LATERITE) LIMONITE SAPROLITE

CONC.

PYRO HYDROPYRO

HYDRO

PYRO

MATTE NiS NiCO3 MATTE

HYDRO HYDRO HYDRO

CLASS 1 FeNiCLASS 1 CLASS 1 Ni-OXIDE CLASS 1/2

SMELT

PAL

PROCESS

CARON

PROCESS

NPI

Source: INSG, Macquarie Research, July 2013

Our estimates and forecasts of nickel production

by process route

Finished nickel production by main process

0

500

1000

1500

2000

2500

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

2014F

2015F

2016F

2017F

'000t

Ni

Sulphide - conventional Sulphide bioheapleach Laterite - ferronickel Laterite - Caron

Laterite - PAL Other laterite Laterite - nickel pig iron

Page 14

Source: Company data, INSG, Macquarie Research, July 2013

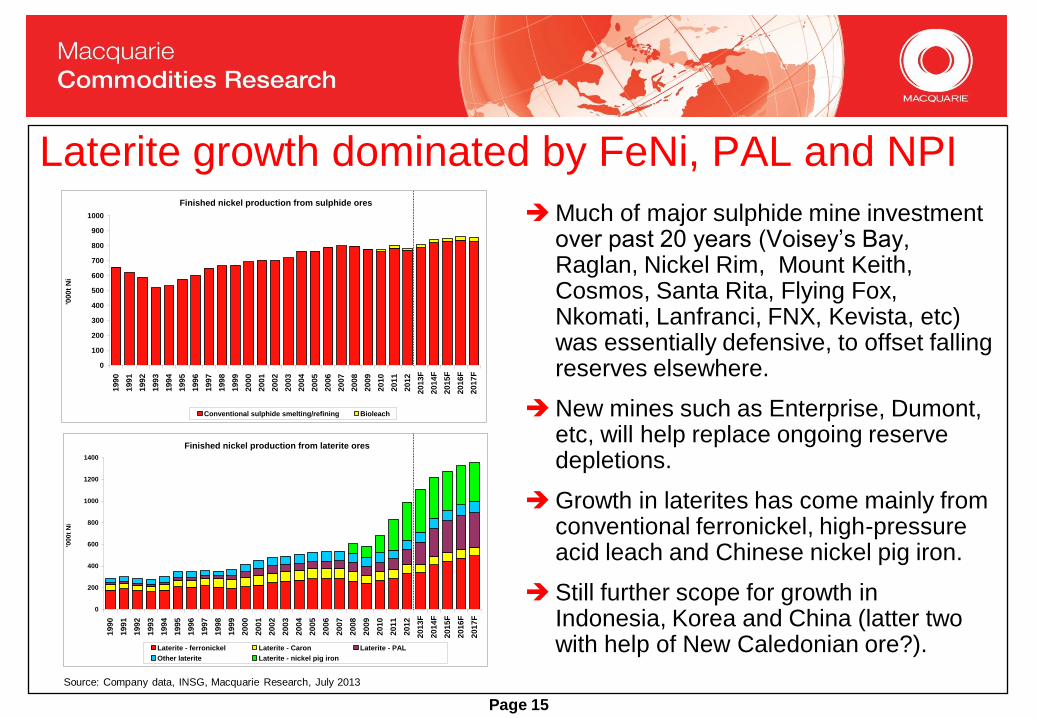

Laterite growth dominated by FeNi, PAL and NPI

Much of major sulphide mine investment over past 20 years (Voisey’s Bay, Raglan, Nickel Rim, Mount Keith, Cosmos, Santa Rita, Flying Fox, Nkomati, Lanfranci, FNX, Kevista, etc) was essentially defensive, to offset falling reserves elsewhere.

New mines such as Enterprise, Dumont, etc, will help replace ongoing reserve depletions.

Growth in laterites has come mainly from conventional ferronickel, high-pressure acid leach and Chinese nickel pig iron.

Still further scope for growth in Indonesia, Korea and China (latter two with help of New Caledonian ore?).

Page 15

Source: Company data, INSG, Macquarie Research, July 2013

Finished nickel production from sulphide ores

0

100

200

300

400

500

600

700

800

900

1000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

F

20

14

F

20

15

F

20

16

F

20

17

F

'000

t N

i

Conventional sulphide smelting/refining Bioleach

Finished nickel production from laterite ores

0

200

400

600

800

1000

1200

1400

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

F

20

14

F

20

15

F

20

16

F

20

17

F

'00

0t

Ni

Laterite - ferronickel Laterite - Caron Laterite - PAL

Other laterite Laterite - nickel pig iron

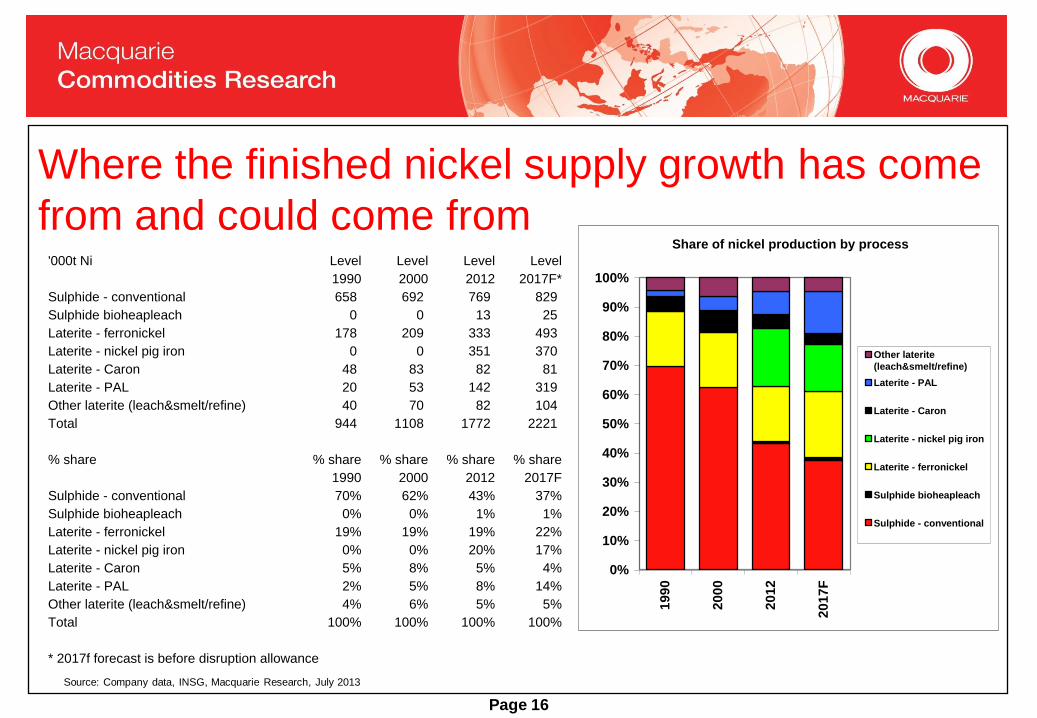

Where the finished nickel supply growth has come

from and could come from

Page 16

Source: Company data, INSG, Macquarie Research, July 2013

'000t Ni Level Level Level Level

1990 2000 2012 2017F*

Sulphide - conventional 658 692 769 829

Sulphide bioheapleach 0 0 13 25

Laterite - ferronickel 178 209 333 493

Laterite - nickel pig iron 0 0 351 370

Laterite - Caron 48 83 82 81

Laterite - PAL 20 53 142 319

Other laterite (leach&smelt/refine) 40 70 82 104

Total 944 1108 1772 2221

% share % share % share % share % share

1990 2000 2012 2017F

Sulphide - conventional 70% 62% 43% 37%

Sulphide bioheapleach 0% 0% 1% 1%

Laterite - ferronickel 19% 19% 19% 22%

Laterite - nickel pig iron 0% 0% 20% 17%

Laterite - Caron 5% 8% 5% 4%

Laterite - PAL 2% 5% 8% 14%

Other laterite (leach&smelt/refine) 4% 6% 5% 5%

Total 100% 100% 100% 100%

* 2017f forecast is before disruption allowance

Share of nickel production by process

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

90

20

00

20

12

20

17

F

Other laterite

(leach&smelt/refine)

Laterite - PAL

Laterite - Caron

Laterite - nickel pig iron

Laterite - ferronickel

Sulphide bioheapleach

Sulphide - conventional

Strong growth ahead for FeNi and PAL…but that

has been the case for some time now!

Ferronickel production by producer

-50

50

150

250

350

450

550

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

2014F

2015F

2016F

2017F

'000t

Ni

0%

5%

10%

15%

20%

25%

Onca P uma

B arro A lto

Ko niambo

Kwangyang

P rist ina

Kavadarci

Laryma

P o bugsko ye

Lo mo do N iquel

P rato po lis

N iqualandia

P o malaa

Oheyama

H achino he

H yuga

C erro M ato so

D o niambo

F alco ndo

% o f wo rld to tal

PAL production by producer

0

50

100

150

200

250

300

350

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

2014F

2015F

2016F

2017F

'000t

Ni

0%

2%

4%

6%

8%

10%

12%

14%

16%

% s

hare

of

wo

rld

pro

du

cti

on

Moa Bay*

Ambatovy

Ramu River*

Taganito*

Coral Bay*

Ravensthorpe*

Cawse*

Bulong

Murrin Murrin

VNC

% of world supply

* intermediate

product only

Page 17

Source: Company data, INSG, Macquarie Research, July 2013

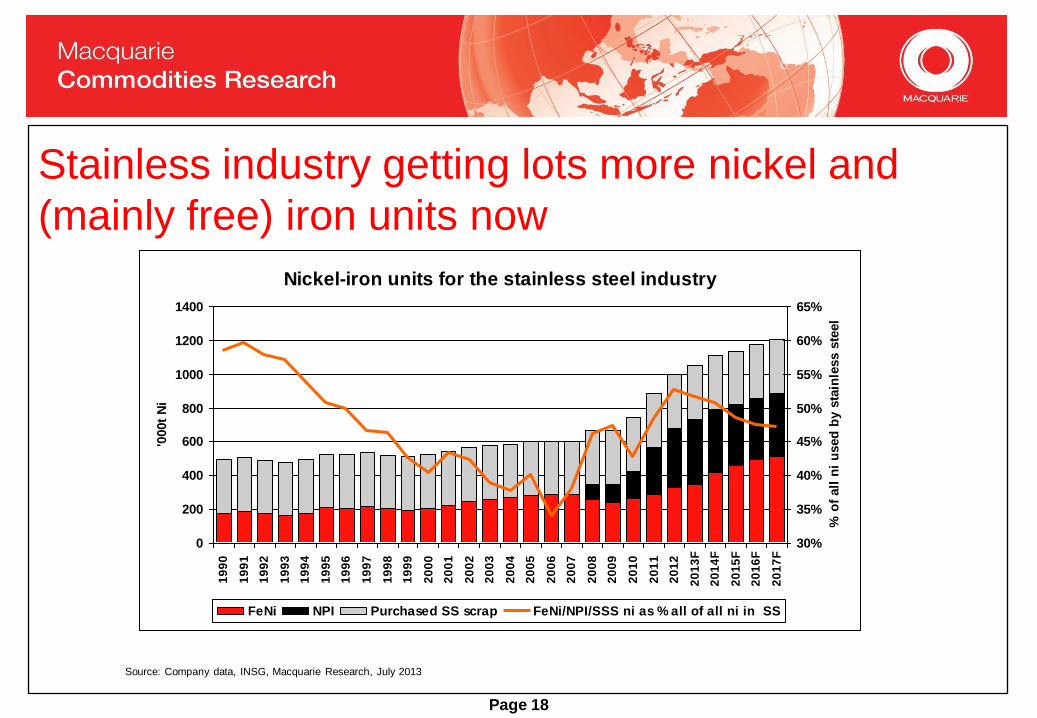

Stainless industry getting lots more nickel and

(mainly free) iron units now

Source: Company data, INSG, Macquarie Research, July 2013

Page 18

Nickel-iron units for the stainless steel industry

0

200

400

600

800

1000

1200

1400

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

F

20

14

F

20

15

F

20

16

F

20

17

F

'000t

Ni

30%

35%

40%

45%

50%

55%

60%

65%

% o

f all

ni

used

by s

tain

less s

teel

FeNi NPI Purchased SS scrap FeNi/NPI/SSS ni as % all of all ni in SS

NPI accounted for major share of nickel used in China in

2012 – replacement for scrap use in ROW

Chinese nickel use by type

17%

38%

7%

38%Ni in scrap

NPI

FeNi

Metal/utility/oxide

Nickel use ex-China by type

40%

0%

18%

42%

Ni in scrap

NPI

FeNi

Metal/utility/oxide

Source: INSG, Macquarie Research, July 2013

Page 19

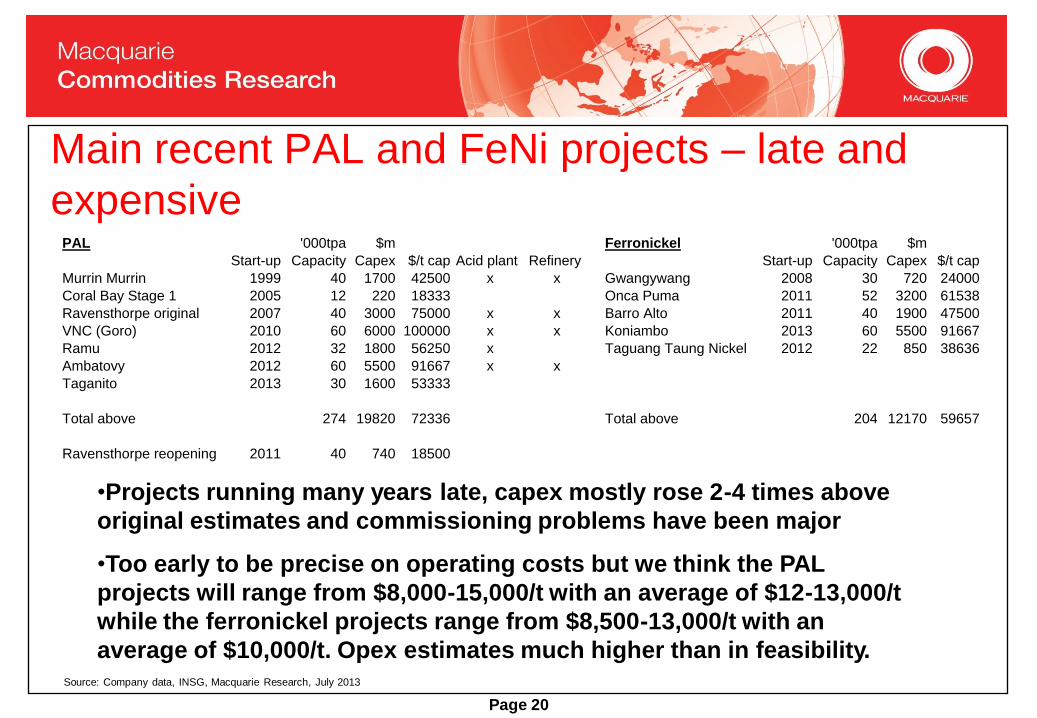

Main recent PAL and FeNi projects – late and

expensive PAL '000tpa $m Ferronickel '000tpa $m

Start-up Capacity Capex $/t cap Acid plant Refinery Start-up Capacity Capex $/t cap

Murrin Murrin 1999 40 1700 42500 x x Gwangywang 2008 30 720 24000

Coral Bay Stage 1 2005 12 220 18333 Onca Puma 2011 52 3200 61538

Ravensthorpe original 2007 40 3000 75000 x x Barro Alto 2011 40 1900 47500

VNC (Goro) 2010 60 6000 100000 x x Koniambo 2013 60 5500 91667

Ramu 2012 32 1800 56250 x Taguang Taung Nickel 2012 22 850 38636

Ambatovy 2012 60 5500 91667 x x

Taganito 2013 30 1600 53333

Total above 274 19820 72336 Total above 204 12170 59657

Ravensthorpe reopening 2011 40 740 18500

•Projects running many years late, capex mostly rose 2-4 times above

original estimates and commissioning problems have been major

•Too early to be precise on operating costs but we think the PAL

projects will range from $8,000-15,000/t with an average of $12-13,000/t

while the ferronickel projects range from $8,500-13,000/t with an

average of $10,000/t. Opex estimates much higher than in feasibility.

Page 20

Source: Company data, INSG, Macquarie Research, July 2013

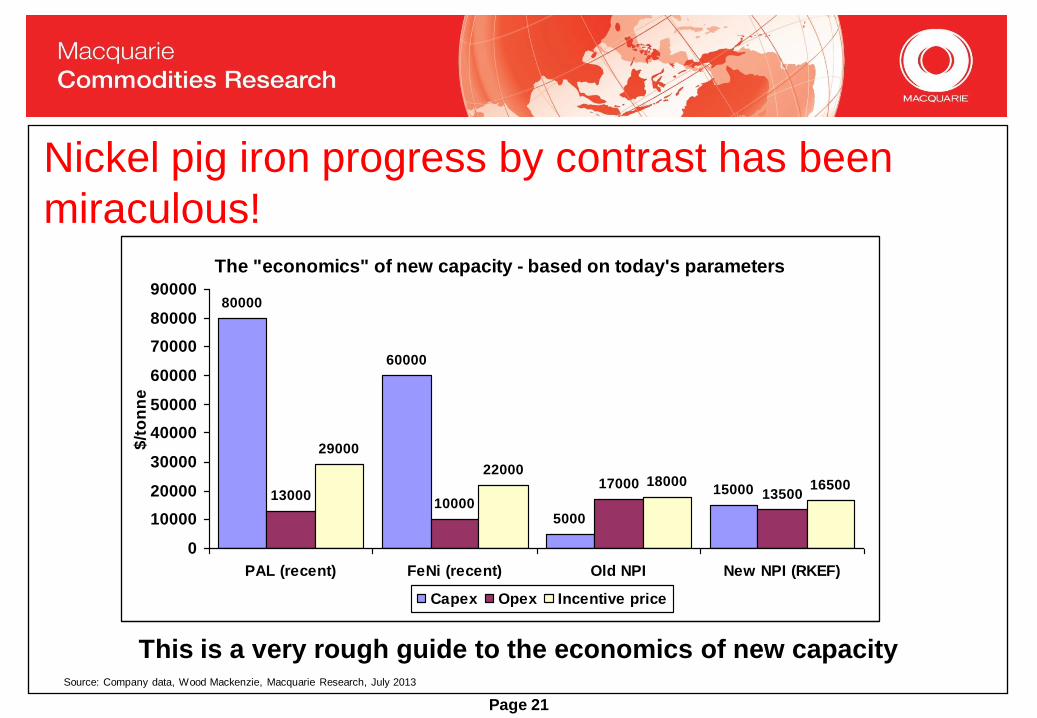

Nickel pig iron progress by contrast has been

miraculous! The "economics" of new capacity - based on today's parameters

80000

60000

5000

150001300010000

1700013500

29000

2200018000 16500

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

PAL (recent) FeNi (recent) Old NPI New NPI (RKEF)

$/t

on

ne

Capex Opex Incentive price

This is a very rough guide to the economics of new capacity

Page 21

Source: Company data, Wood Mackenzie, Macquarie Research, July 2013

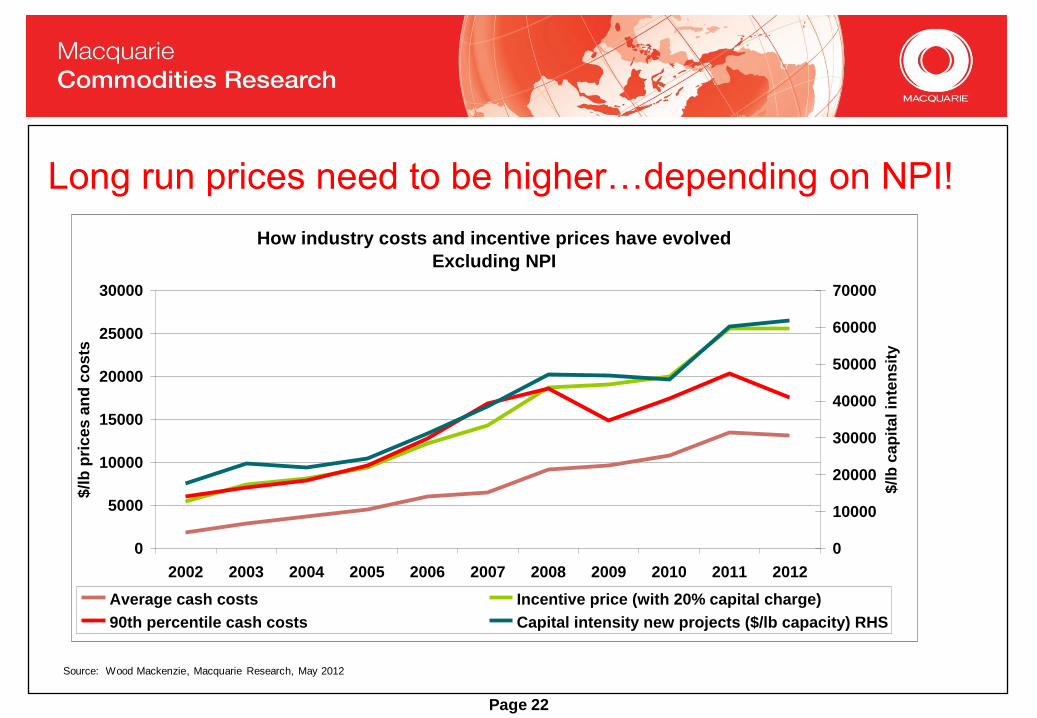

Long run prices need to be higher…depending on NPI!

Page 22

Source: Wood Mackenzie, Macquarie Research, May 2012

How industry costs and incentive prices have evolved

Excluding NPI

0

5000

10000

15000

20000

25000

30000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$/l

b p

rices a

nd

co

sts

0

10000

20000

30000

40000

50000

60000

70000

$/lb

ca

pit

al in

ten

sit

y

Average cash costs Incentive price (with 20% capital charge)

90th percentile cash costs Capital intensity new projects ($/lb capacity) RHS

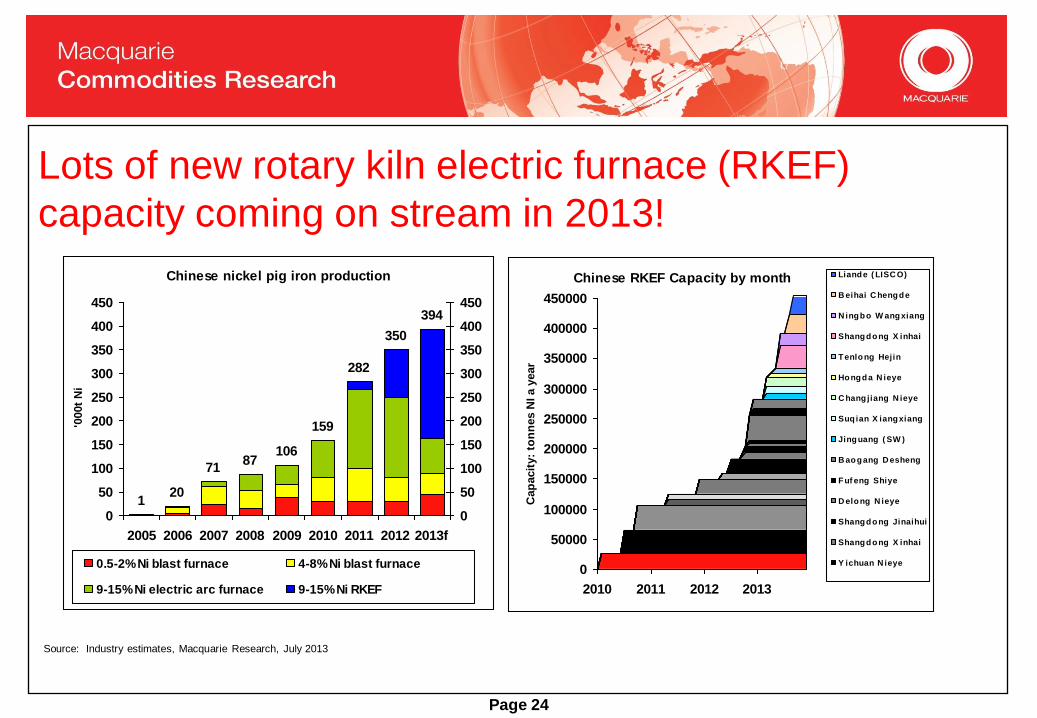

Nickel pig iron – the big unknown Estimates for 2012 output (still!) vary from 290kt to 370kt – very little reporting, lots of

guessing.

Cash costs range from $12-20,000/tonne ($5.45-9/lb) depending on process and location. Costs vary widely.

Costs do vary with nickel price so there is no single price below which supply shuts – indeed costs have fallen sharply (15-20%) since March 2012 (lower carbon and ore prices and new power rebates in Inner Mongolia).

Capacity potential is massive – OVER 400,000 tpa NEW capacity due, mostly Greenfield rotary kiln/electric arc furnace and integrated with stainless mills. Costs will rise as energy prices rise and RMB appreciates but new plants have 30-50% less energy consumption and stainless mills get significant energy and iron credit benefits.

Ore supplies from Philippines and Indonesia are critical in determining the future output limits. Many Chinese producers trying to backwardly integrate into ore.

If new supply outside China comes on successfully, capping prices, NPI production will be limited – if new supply fails, there will be more NPI.

Page 23

Lots of new rotary kiln electric furnace (RKEF)

capacity coming on stream in 2013!

Source: Industry estimates, Macquarie Research, July 2013

Page 24

Chinese RKEF Capacity by month

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

2010 2011 2012 2013

Cap

acit

y:

ton

nes N

I a y

ear

Liande ( LISC O)

B eihai C hengde

N ingbo W angxiang

Shangdong X inhai

Tenlong Hejin

Hongda N ieye

C hang jiang N ieye

Suq ian X iangxiang

Jinguang ( SW )

B aogang D esheng

Fuf eng Shiye

D elong N ieye

Shangdong Jinaihui

Shangdong X inhai

Y ichuan N ieye

Haigan Keji

Tsingshan Sij i

Shangai Haihe

Tsingshan

C hangq ing

B eihai C hengde

N ingbo W anxiang

D elong N ieye

Shangdong Jinaihui

Shangdong X inhai

Tsingshan D ingxin

Chinese nickel pig iron production

120

7187

106

159

282

350

394

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011 2012 2013f

'000t

Ni

0

50

100

150

200

250

300

350

400

450

0.5-2% Ni blast furnace 4-8% Ni blast furnace

9-15% Ni electric arc furnace 9-15% Ni RKEF

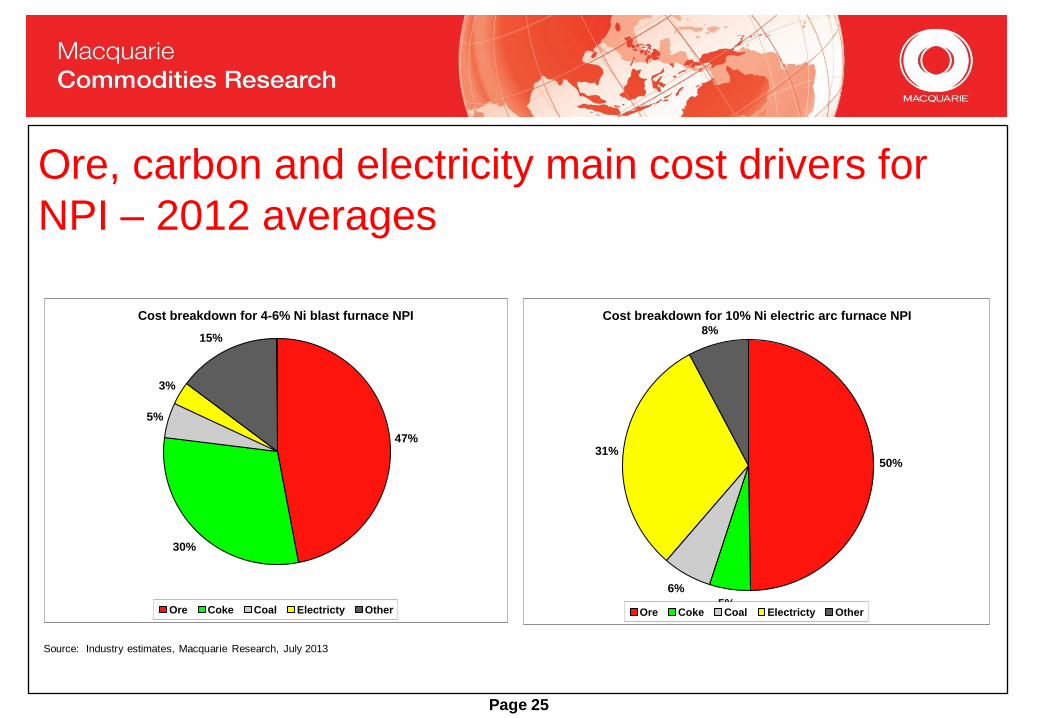

Ore, carbon and electricity main cost drivers for

NPI – 2012 averages

Cost breakdown for 4-6% Ni blast furnace NPI

47%

30%

5%

3%

15%

Ore Coke Coal Electricty Other

Cost breakdown for 10% Ni electric arc furnace NPI

50%

5%

6%

31%

8%

Ore Coke Coal Electricty Other

Source: Industry estimates, Macquarie Research, July 2013

Page 25

NPI costs for electric furnace producers – big differences in costs

according to location and furnace types – costs fall as raw material

and power costs fall

Page 26

Source: SMM, Macquarie Research, July 2013

12000

14000

16000

18000

20000

22000

24000

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

May-1

1

Ju

l-11

Sep

-11

No

v-1

1

Jan

-12

Mar-

12

May-1

2

Ju

l-12

Sep

-12

No

v-1

2

Jan

-13

Mar-

13

May-1

3

$/lb

ex-V

At

Price: 8-13% NPICosts: 10% Ni - CoastalCosts: 10% Ni - Inner Mongolia

12000

14000

16000

18000

20000

22000

24000

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

May-1

1

Ju

l-11

Sep

-11

No

v-1

1

Jan

-12

Mar-

12

May-1

2

Ju

l-12

Sep

-12

No

v-1

2

Jan

-13

Mar-

13

May-1

3

$/lb

ex-V

AT

Price: 8-13% NPICosts: 12% Ni - ConventionalCosts: 12% Ni - RKEF

Low Ni NPI blast furnace producers still profitable

12000

14000

16000

18000

20000

22000

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

May-1

1

Ju

l-11

Sep

-11

No

v-1

1

Jan

-12

Mar-

12

May-1

2

Ju

l-12

Sep

-12

No

v-1

2

Jan

-13

Mar-

13

May-1

3

$/lb

ex-V

AT

Price: 4-6% NPI

Costs: 6% Ni in blast furnace

20000

22000

24000

26000

28000

30000

32000

Jan

-10

Mar-

10

May-1

0

Ju

l-10

Sep

-10

No

v-1

0

Jan

-11

Mar-

11

May-1

1

Ju

l-11

Sep

-11

No

v-1

1

Jan

-12

Mar-

12

May-1

2

Ju

l-12

Sep

-12

No

v-1

2

Jan

-13

Mar-

13

May-1

3

$/lb

ex-V

AT

Price: 1.5-2% NPI

Costs: 1.7% Ni in blast furnace

Source: SMM, Macquarie Research, July 2013

Page 27

Cost of ore from Indonesia has plunged in 2013

Indonesia ore price plunges in 2013

$/ wet tonne for 1.8% Ni in dry ore

25

30

35

40

45

50

55

60

Oc

t-1

2

No

v-1

2

De

c-1

2

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

$/t

on

ne

CIF FOB

Ore cost in making one tonne of nickel in 10%

Ni pig iron

2500

3000

3500

4000

4500

5000

5500

Oc

t-1

2

No

v-1

2

De

c-1

2

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

$/t

on

ne

CIF FOB

Source: NPI producers, Macquarie Research, July 2013

Page 28

Key factors in NPI Indonesian ore ban planned for end-2013. No-one thinks this will happen!

Quotas and taxes more likely? 20% export tax (adds 35-40c/lb to costs if

passed on…but it was not!) from May 2012…maybe higher?

Longer term cost pressures – breakeven for NPI could rise from $12,000-

17,000/t currently to $19,000-25,000/lb over next 4-5 years as ore costs,

electricity costs rise and RMB appreciates?

Competition for higher-grade ore (1.8%+Ni) will intensify as more RKEF

comes on and high grade reserves deplete – price of these ores could

rise sharply.

Still unclear how long the resources can last at current rates.

We don’t think ore supply from Indonesia to China will stop in 2014 – it will

become (a lot) more expensive and there will probably be some NPI capacity

built in Indonesia from 2015 onwards.

Page 29

Page 30

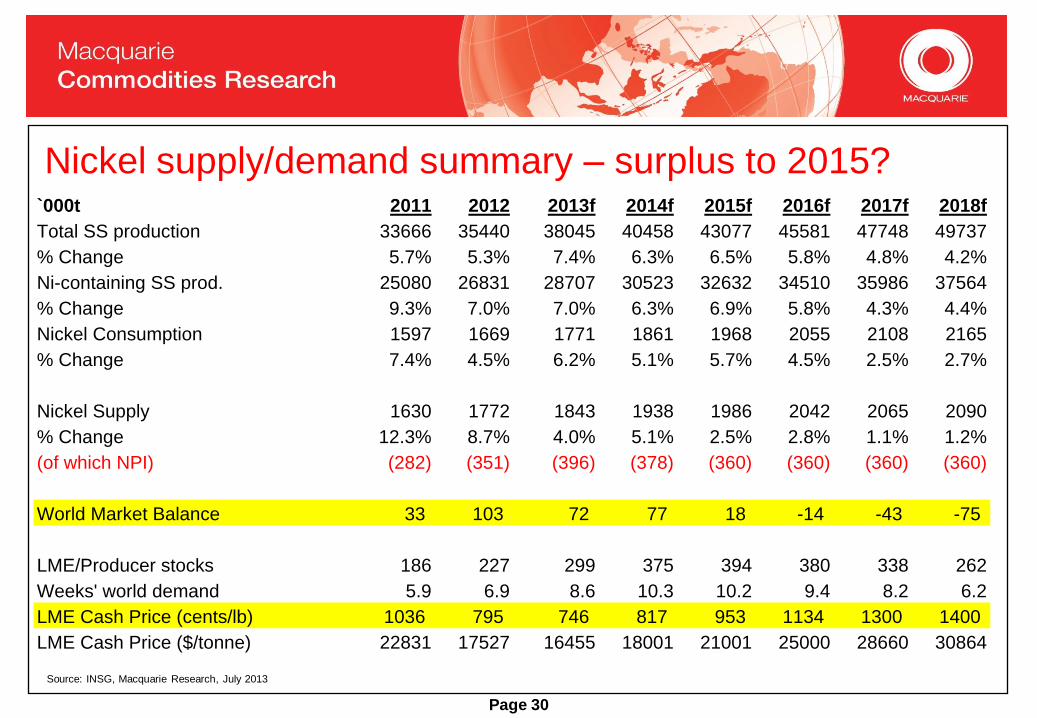

Nickel supply/demand summary – surplus to 2015?

Source: INSG, Macquarie Research, July 2013

`000t 2011 2012 2013f 2014f 2015f 2016f 2017f 2018f

Total SS production 33666 35440 38045 40458 43077 45581 47748 49737

% Change 5.7% 5.3% 7.4% 6.3% 6.5% 5.8% 4.8% 4.2%

Ni-containing SS prod. 25080 26831 28707 30523 32632 34510 35986 37564

% Change 9.3% 7.0% 7.0% 6.3% 6.9% 5.8% 4.3% 4.4%

Nickel Consumption 1597 1669 1771 1861 1968 2055 2108 2165

% Change 7.4% 4.5% 6.2% 5.1% 5.7% 4.5% 2.5% 2.7%

Nickel Supply 1630 1772 1843 1938 1986 2042 2065 2090

% Change 12.3% 8.7% 4.0% 5.1% 2.5% 2.8% 1.1% 1.2%

(of which NPI) (282) (351) (396) (378) (360) (360) (360) (360)

World Market Balance 33 103 72 77 18 -14 -43 -75

LME/Producer stocks 186 227 299 375 394 380 338 262

Weeks' world demand 5.9 6.9 8.6 10.3 10.2 9.4 8.2 6.2

LME Cash Price (cents/lb) 1036 795 746 817 953 1134 1300 1400

LME Cash Price ($/tonne) 22831 17527 16455 18001 21001 25000 28660 30864

In conclusion – on the medium term

The laterite “revolution” has arrived – it is built on the shaky ground of low-cost

Indonesian ore/Chinese NPI and VERY high-cost non-Chinese PAL/FeNi

capacity

Failure of major Greenfield projects outside China and massive rises in

construction costs of non-Chinese Greenfield projects likely to deter future

investment

Next two years will be challenging for the nickel industry – unless the

Indonesians ban ore exports in 2014

Growing deficits by mid-decade will lead to need for new capacity…new

capacity needs prices significantly above $22,000/t ($10/lb)

Huge reliance on Indonesian ore to feed RFEF plants in China – unlikely to

stay as “cheap” as it is today?

Page 31

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand

Outperform – return > 3% in excess of benchmark return

Neutral – return within 3% of benchmark return

Underperform – return > 3% below benchmark return

Benchmark return is determined by long term nominal GDP growth plus 12

month forward market dividend yield

Macquarie – Asia/Europe

Outperform – expected return >+10%

Neutral – expected return from -10% to +10%

Underperform – expected <-10%

Macquarie First South - South Africa

Outperform – return > 10% in excess of benchmark return

Neutral – return within 10% of benchmark return

Underperform – return > 10% below benchmark return

Macquarie - Canada

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Macquarie - USA

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Volatility index definition* This is calculated from the volatility of historic price

movements.

Very high–highest risk – Stock should be expected

to move up or down 60-100% in a year – investors

should be aware this stock is highly speculative.

High – stock should be expected to move up or down

at least 40-60% in a year – investors should be aware

this stock could be speculative.

Medium – stock should be expected to move up or

down at least 30-40% in a year.

Low–medium – stock should be expected to move up

or down at least 25-30% in a year.

Low – stock should be expected to move up or down

at least 15-25% in a year.

* Applicable to Australian/NZ stocks only

Recommendation – 12 months

Note: Quant recommendations may differ from

Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments

made:

Added back: goodwill amortisation, provision for catastrophe

reserves, IFRS derivatives & hedging, IFRS impairments &

IFRS interest expense

Excluded: non recurring items, asset revals, property revals,

appraisal value uplift, preference dividends & minority

interests

EPS = adjusted net profit /efpowa*

ROA = adjusted ebit / average total assets

ROA Banks/Insurance = adjusted net profit /average total

assets

ROE = adjusted net profit / average shareholders funds

Gross cashflow = adjusted net profit + depreciation

*equivalent fully paid ordinary weighted average number of

shares

All Reported numbers for Australian/NZ listed stocks are

modelled under IFRS (International Financial Reporting

Standards).

Recommendation proportions – For quarter ending 31 March 2013

AU/NZ Asia RSA USA CA EUR

Outperform 45.12% 53.24% 50.00% 40.70% 62.98% 43.30% (for US coverage by MCUSA, 10.55% of stocks covered are investment banking clients)

Neutral 41.52% 28.01% 41.43% 55.01% 32.60% 34.10% (for US coverage by MCUSA, 9.05% of stocks covered are investment banking clients)

Underperform 13.36% 18.74% 8.57% 4.29% 4.42% 22.60% (for US coverage by MCUSA, 0.00% of stocks covered are investment banking clients)

Page 32

Page 33

Company Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst Certification:

The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be

directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research receives compensation based on

overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken reasonable care to achieve and maintain

independence and objectivity in making any recommendations.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA) Inc; Macquarie

Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; and Macquarie First South Securities (Pty) Limited; Macquarie Capital

Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for

the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL.

MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect

of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale clients of the

Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the information in this research in

any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any

changes made to them by any other person. MGL has established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant

to regulatory requirements (including the FSA Rules) which sets out how we must seek to identify and manage all material conf licts of interest. Nothing in this research shall be construed as a solicitation

to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or

particular needs. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of your

particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even

become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions,

which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is

accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie

Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should

contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise.

Disclaimer: The information contained in this e-mail is confidential and has been furnished to you solely for your use. You may not disclose, reproduce or distribute the information in any way. Macquarie

does not guarantee the integrity of this e-mail or attached files.

Macquarie Capital (USA) Inc. affiliate research reports and affiliate employees are not subject to the disclosure requirements of FINRA rules. Any persons receiving this report directly from Macquarie

Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. In Germany, this research is issued and/or distributed by Macquarie

Capital (Europe) Limited, Niederlassung Deutschland, which is authorised and regulated by the UK Financial Services Authority and in Germany by BaFin.

Macquarie salespeople, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the opinions

expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis, quantitative analysis, and trade

ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of research, whether as a result of differing time horizons, methodologies,

or otherwise.

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange. New Zealand: In

New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada

Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-dealer and

member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States and sent to US persons. Any person wishing to effect

transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so with Macquarie Capital Markets North America Ltd. The Research Distribution Policy of

Macquarie Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and distributed by

Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Services Authority (No. 193905). Germany: In Germany, research is issued and distributed by Macquarie Capital

(Europe) Ltd, Niederlassung Deutschland, which is authorised and regulated in the United Kingdom by the Financial Services Authority (No. 193905). France: In France, research is issued and distributed

by Macquarie Capital (Europe) Ltd, which is authorised and regulated in the United Kingdom by the Financial Services Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is

issued and distributed by Macquarie Capital Securities Ltd, which is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited

Shanghai Representative Office only engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie

Capital Securities Ltd. Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc., Osaka Securities Exchange Co.

Ltd. (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association and The Financial Futures Association of Japan and Japan Investment

Advisers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pty Ltd., 92, Level 9, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East),

Mumbai – 400 051, India, which is a SEBI registered Stock Broker having membership with National Stock Exchange of India Limited (INB231246738) and Bombay Stock Exchange Limited

(INB011246734). Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 463469-W) which is a Participating

Organisation of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: Information on securities/instruments that are traded in Taiwan

is distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of the report may be reproduced or quoted by the

press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any security or product. Research Associate(s) in this report who

are registered as Clerks only assist in the preparation of research and are not engaged in writing the research. Thailand: In Thailand, research is produced with the contribution of Kasikorn Securities

Public Company Limited, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities (Thailand) Ltd. is a licensed securities company that is authorized by the Ministry of Finance,

regulated by the Securities and Exchange Commission of Thailand and is an exchange member of the Stock Exchange of Thailand. Macquarie Securities (Thailand) Limited and Kasikorn Securities Public

Company Limited have entered into an exclusive strategic alliance agreement to broaden and deepen the scope of services provided to each parties respective clients. The strategic alliance does not

constitute a joint venture. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange

Commission of Thailand. Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at:

http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited , which is

regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at http://dis.kofia.or.kr/fs/dis2/fundMgr/DISFundMgrAnalystPop.jsp?companyCd2=A03053&pageDiv=02.

South Africa: In South Africa, research is issued and distributed by Macquarie First South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and

distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in

securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt from complying with

sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie First

South Securities (Pty) Limited and Macquarie Capital (USA) Inc. represent and warrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States,

research is issued and distributed by Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each

research report prepared by one of its non-US affiliates when the research report is distributed in the United States by Macquar ie Capital (USA) Inc. Macquarie Capital (USA) Inc.’s affiliate’s analysts are

not registered as research analysts with FINRA, may not be associated persons of Macquarie Capital (USA) Inc., and therefore may not be subject to FINRA rule restrictions on communications with a

subject company, public appearances, and trading securities held by a research analyst account. Information regarding futures is provided for reference purposes only and is not a solicitation for purchases

or sales of futures. Any persons receiving this report directly from Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital

(USA) Inc. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures, or contact your registered representative at 1-

888-MAC-STOCK, or write to the Supervisory Analysts, Research Department, Macquarie Securities, 125 W.55th Street, New York, NY 10019.

© Macquarie Group

Page 34