The next 15 years Is there a

57

The next 15 years – Is there a “New Normal” ahead? Delaware Investments Presentation © Richard C Marston Wharton School, University of Pennsylvania

Transcript of The next 15 years Is there a

The next 15 years – Is there a “New Normal” ahead? Delaware Investments Presentation

© Richard C Marston

Wharton School, University of Pennsylvania

Outline

1. Is there a “New Normal” ahead for stocks?

2. Is the thirty-year bull market in bonds finally over?

3. Is it possible to avoid the New Normal by diversifying beyond U.S. stocks and bonds?

– Diversifying into fast growing economies

– Diversifying into alternative investments

Bill Gross introduced the “New Normal” too soon – in May 2009

• S&P 500 reached its bottom on March 9, 2009 – just six months after Lehman failed.

• It has been a great cyclical rally ever since then.

• Through September 2016, the S&P 500 is up by 220%

• After a recession, we always experience a sharp cyclical rally

S&P 500 in Last 15 Years, 1999-2016 Source: S&P

600

1000

1400

1800

2200

2000 2004 2009 2014

S&P

50

0 In

dex

Returns after Recession: S&P 500 return in 1st 12 months Source: Investing for a Lifetime (2014), Table 3.3

46.0%

43.4%

32.6%

41.9%

37.3%

59.3%

33.5%

38.5%

49.8%

0% 10% 20% 30% 40% 50% 60% 70%

Jul 53-May 54

Aug 57-Apr 58

Apr 60-Feb 61

Dec 69-Nov 70

Nov 73-Mar 75

Jul 81-Nov 82

Jul 90-Mar 91

Mar 01-Nov 01

Dec 07-Jun 09

Dat

es

of

Re

cess

ion

The true “New Normal”

• Yet Bill Gross may be right that stock returns in the future will not what they have been in the past.

• Future stock returns may not be as high as in the past because growth in the industrial world has slowed down.

Real GDP Growth in Japan Source: IMF, international Financial Statistics

BRICs

4.6% 4.7%

1.0%0.7%

0%

2%

4%

6%

1971-1980 1981-1990 1991-2000 2001-2015

The collapse in growth occurred in Japan 25 years ago

Real GDP Growth in Europe Source: IMF, International Financial Statistics

3.2%

2.5%

2.1%

1.0%

2.7%

2.3%

2.9%

1.1%

0%

1%

2%

3%

4%

1971-1980 1981-1990 1991-2000 2001-2015

Gro

wth

pe

r A

nn

um

France Germany

Real GDP Growth in United States Source: Bureau of Economic Analysis

3.2%3.4%

3.4%

1.8%

0%

1%

2%

3%

4%

1971-1980 1981-1990 1991-2000 2001-2015

Gro

wth

pe

r A

nn

um

Long view of U.S. growth

• U.S. economy grew rapidly in the 19th century – but never as fast as China!

• Slowdown in 1930s depression, then postwar boom that extended until 2000.

U.S. GDP growth since 1870 Source: NIPA, Table 1.1.6 and F 10-16

4.2%

3.1%

1.7%

3.2% 3.2%

1.8%

0%

1%

2%

3%

4%

5%

1870-1913 1913-1929 1930-1940 1946-1972 1972-2000 2001-2015

Perc

ent

per

an

nu

m

Postwar boom

Long view of U.S. growth

• Growth in industrial countries is slowing partly because productivity growth is slowing.

• A major reason for the slowdown in the growth in output per hour is the shift of the economy towards services and away from manufacturing.

• Productivity in most service sectors is way below that in manufacturing or agriculture or mining

Annual Growth in Productivity in Services, 1987-2014 Source: Brookings Institution (WSJ, 10-31-16)

-1.0% -0.5% 0.0% 0.5% 1.0% 1.5%

Legal Services

Hospitals/Residential Care

Eduational Services

Social Assistance

Food Services

Computer Systems/Services

Administrative Services

Accomodation/Hospitality

Two Trends in Manufacturing

• Will examine two trends in manufacturing since 1980:

1. Growth in manufacturing output (adjusted for inflation)

2. Growth in employment in manufacturing

Production and Employment in Manufacturing

Bureau of Labor Statistics and Council of Economic Advisors

50

100

150

200

250

300

1980. 1985. 1990. 1995. 2000. 2005. 2010. 2015

Ind

ex (

19

80

= 1

00

)

Manufacturing Output

Manufacturing Jobs

18.6 million jobs

12.3 million jobs

The true “New Normal”

• Another reason growth is slowing is that the industrial countries are aging.

• That’s particularly true of Japan, Germany and Italy.

• Look at share of population that is 65 years or older.

Share of Population 65 Years or Older Source: Pew Research Center using United Nations data

0% 10% 20% 30% 40%

U.S.

U.K.

France

Italy

Germany

Japan

2050

2010

Stock returns in developed markets

• Stock returns in the developed (or industrial) countries over the last 45 years or the last 30 years have been quite impressive.

• But the last 15 years have been a different story.

• Let’s divide developed markets into three sets of markets: 1. U.S. market represented by the S&P 500 index

2. European portion of the MSCI EAFE index

3. Pacific portion of the EAFE index (Japan, Australasia, Hong Kong, and Singapore)

Stocks in developed markets Sources: S&P and MSCI

Last 15 years

Last 30 years

10.3%

11.4%

4.3%

9.5% 9.4%

2.9%

10.0%

11.5%

3.4%

9.2%

6.9%

1.9%

0%

2%

4%

6%

8%

10%

12%

14%

1970-2015 1986-2015 2001-2015

Ret

urn

pe

r an

nu

m

S&P 500 EAFE Europe Pacific

Last 30 years

Last 15 years

Stock returns in real terms

• Investors in the long run are interested in real (or inflation-adjusted) returns.

• Let’s look at the same returns adjusted by the U.S. inflation rate (since the returns are measured in dollars).

• This chart shows how miserable stock returns have been over the last 15 years.

Stocks in developed markets: real returns Sources: S&P and MSCI

Last 15 years

5.9%

8.4%

2.0%

5.2%

6.5%

0.6%

5.7%

8.5%

1.1%

4.9%

4.0%

-0.4%

-2%

0%

2%

4%

6%

8%

10%

1970-2015 1986-2015 2001-2015

Ret

urn

pe

r an

nu

m

S&P 500 EAFE Europe Pacific

Last 15 years

2) A “New Normal” for bonds?

• Bill Gross talked about a New Normal for stocks.

• But what about bonds? Surely, there is a New Normal ahead for bonds.

• The bull market for bonds has lasted for 30 years.

Figure 3-3 U.S. Inflation and Bond Yields, 1954-2015 Data Source: IMF, International Financial Statistics and Bureau of Labor Statistics

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1954 1964 1974 1984 1994 2004 2014

Pe

r A

nn

um

CPI Inflation 10 yr Treas Yield

Factors influencing interest rates

A. Fiscal deficits

B. Monetary overhang

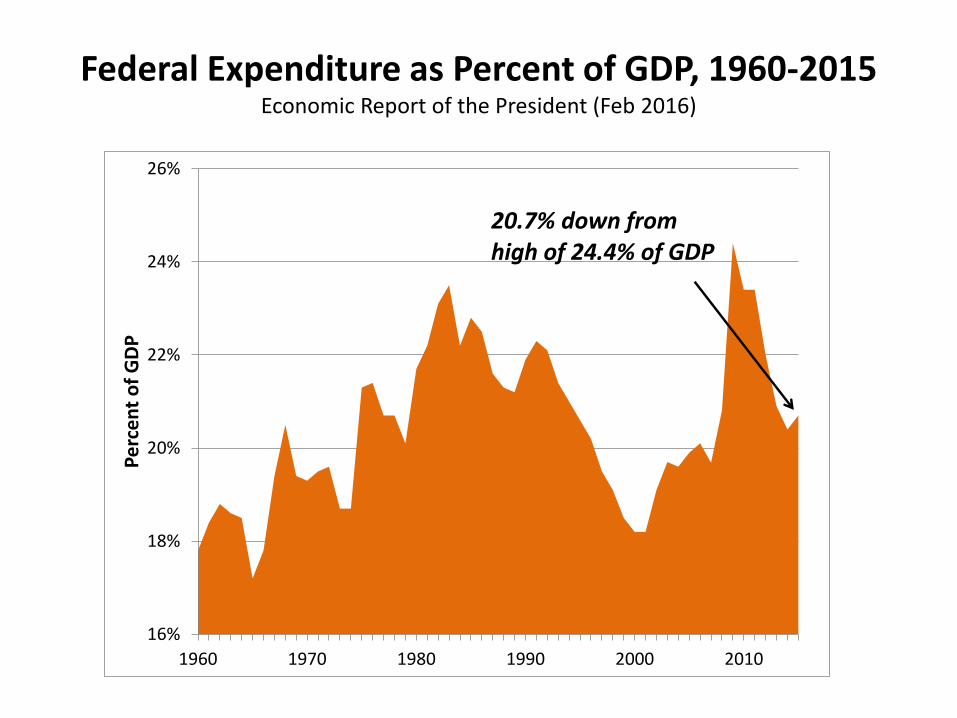

• Fiscal deficits have been reduced dramatically in last few years.

Federal Expenditure as Percent of GDP, 1960-2015 Economic Report of the President (Feb 2016)

16%

18%

20%

22%

24%

26%

1960 1970 1980 1990 2000 2010

Pe

rce

nt

of

GD

P

20.7% down fromhigh of 24.4% of GDP

U.S. Tax Receipts as Percent of GDP, 1960-2015 Economic Report of the President (Feb 2016)

14%

16%

18%

20%

22%

1960 1970 1980 1990 2000 2010

Pe

rce

nt

of

GD

P

18.3% up fromlow of 14.6% of GDP

U.S. Fiscal Deficit as Percent of GDP, 1960-2015 Economic Report of the President (Feb 2016)

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

1960 1970 1980 1990 2000 2010

Pe

rce

nt

of

GD

P

-2.5% up fromlow of -9.8% of GDP

Factors influencing interest rates

• The election results promise that this favorable trend will not continue.

– Infrastructure spending

– Large tax cuts

B. Monetary overhang

• Federal reserve did heroic work during the financial system – providing massive liquidity to save banking system and bolster economy.

• But legacies:

1. Fed balance sheet has ballooned.

2. So has cash at commercial banks.

Assets on Fed’s Balance Sheet Source: Federal Reserve Board

Federal Reserve H.4.1 Release

Start of QE2

Start of QE3

Start of QE1

$0

$1,000

$2,000

$3,000

$4,000

$5,000

1/5/2005 1/5/2008 1/5/2011 1/5/2014

$ B

illio

ns Other Assets

Loans

Other Securities

U.S. Treasuries

QE2

QE3

QE1

Cash assets at commercial banks

Source: FRB H8 Series

Start of QE2

Start of QE3

Start of QE1

$-

$1,000

$2,000

$3,000

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

$ B

illio

ns

Start of QE1

Start of QE2

Start of QE3

A “New Normal” for bonds

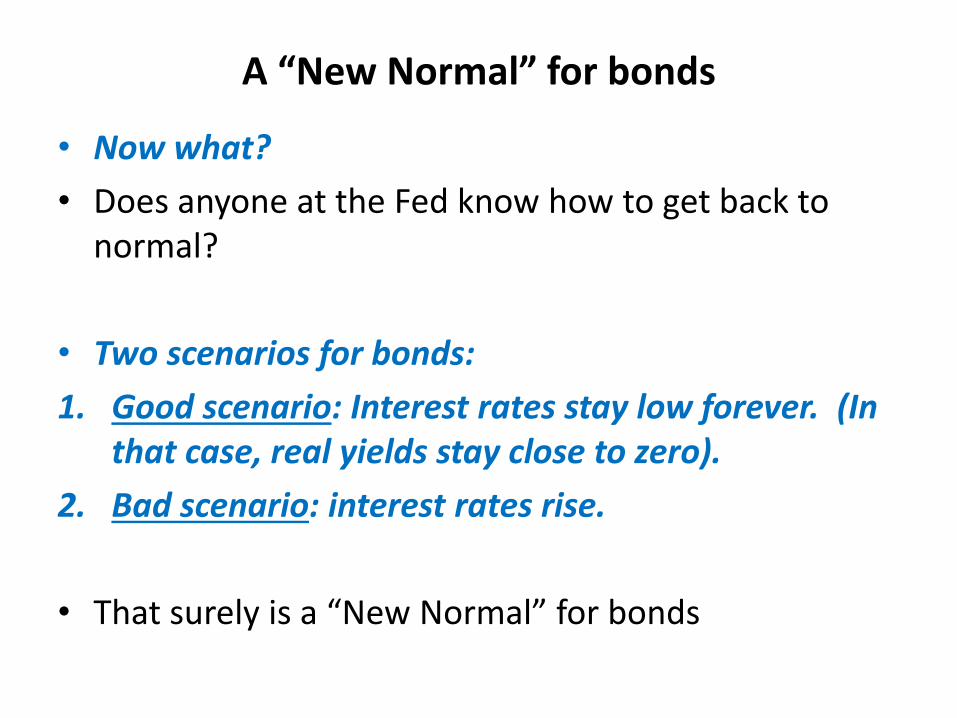

• Now what?

• Does anyone at the Fed know how to get back to normal?

• Two scenarios for bonds:

1. Good scenario: Interest rates stay low forever. (In that case, real yields stay close to zero).

2. Bad scenario: interest rates rise.

• That surely is a “New Normal” for bonds

3. Is it possible to escape the “New Normal” by diversifying?

• If U.S. stock and bond markets promise lower returns, will diversification help?

1. One possibility is to diversify into countries that are growing much faster than the United States – the emerging markets.

2. Another possibility is to diversify into alternative investments.

• Let’s explore each possibility.

A. Diversifying into emerging markets

• Since 2001, emerging markets have earned the highest stock returns, easily beating the U.S. and other developed stock markets.

• Maybe emerging markets will help investors to escape the New Normal.

• In November 2001, Jim O’Neill of Goldman Sachs introduced the BRICs

• Heralded an impressive decade of high stock returns not only in the BRICs, but emerging markets as a whole.

Figure 9-6 Returns in the BRIC Countries and Emerging Markets as a Whole

Data Source: MSCI

1.2%

14.1%

-5.0%

-16.8%

-4.1%

8.2%6.7%

14.1%12.6%

9.7%

-20%

-10%

0%

10%

20%

Brazil Russia India China MSCI EM

Ret

urn

/An

nu

m

1995-2001 2002-2015

Decade of the “BRICs”

• But then in December 2013, Goldman Sachs published “Emerging Markets: As the Tide Goes Out” which forecast a prolonged slowdown in stock returns in the emerging markets.

• Is it wise to look for salvation there?

Stock Returns in Emerging Markets Source: MSCI EM Index

Emerging markets have faltered over last 5 years

8.3%

16.2%

-4.5%

-10%

-6%

-2%

2%

6%

10%

14%

18%

1991-2000 2001-2010 2011-2015

Ret

urn

pe

r A

nn

um

China has led all emerging markets in growth

• China has grown rapidly for over three and ½ decades.

Real GDP Growth in China, 1979-2013 Source: IMF, international Financial Statistics

BRICs

9.9%

9.0%

10.4%10.0% 9.7%

0%

2%

4%

6%

8%

10%

12%

1979-85 1986-92 1993-99 2000-06 2007-13

Gro

wth

Pe

r A

nn

um

Share of Employment by Sector in China Source: China Statistical Yearbook, 2013

0%

30%

60%

90%

1952 1982 1992 2002 2012

Emp

loym

en

t in

Se

cto

r (%

of

GD

P)

Agriculture

Industry

Services

Key: lots of labor available

Wage Increases in China Source: China Statistical Yearbook, 2013

¥0

¥20,000

¥40,000

¥60,000

¥80,000

1995 2000 2005 2010

Total Wage Bill

Average Wage

Average wage increase = 13.6% per annum

But now wages are rising rapidly

Will China slow down?

• China also confronts an aging problem almost as bad as in Japan, Germany and Italy.

• Consider United Nations projections through 2050.

China’s Working Age Population Relative to Non-Working Age Population

Source: United Nations

1

1.5

2

2.5

3

1980 1990 2000 2010 2020 2030 2040 2050

Wo

rkin

g A

ge/N

on

Wo

rkin

g A

ge

Will China slow down?

• China is beginning to slow down.

– That’s bad news for everyone.

– China has been the growth engine for the world.

• With China slowing, two other BRICs are in even worse shape, Brazil and Russia.

Economic forecasts for emerging markets Source: IMF, July 2016

2015 2016f 2017f

China

India

Brazil

Russia

6.9%

7.6%

-3.8%

-3.7%

6.6%

7.5%

-3.3%

-1.2%

6.2%

7.4%

0.5%

1.0%

Three of the BRICs have slowed down

B. Diversifying into alternative investments

• Hedge funds:

• Surely hedge funds provide an escape from the low returns offered by U.S. stock and bonds.

• Let’s consider how well they have performed in the last 15 years.

Hedge Fund Returns – Too Many Cooks Spoiling the Returns?

HFRI Fund Weighted Hedge Fund Index

Decline in average

returns over time Decline in average

returns over time Decline in average

returns over time

18.2% 18.3%

7.1%

5.7%

3.6%

0%

5%

10%

15%

20%

1990-1994 1995-1999 2000-2004 2005-2009 2010-2015

Ret

urn

pe

r A

nn

um

Decline in average

returns over time

Diversifying into alternative investments

• Hedge funds:

• The increasingly poor performance of hedge funds in last 15 years is perhaps expected.

• After all, the space has been flooded by the influx of new funds. Are there that many arbitrage opportunities to keep 10,000 managers in business?

Diversifying into alternative investments

• Real Estate:

– Over last 20+ years as well as over the last 40+ years, real estate has outperformed U.S. equity.

– Look at REIT index relative to the S&P 500

Table 12-1 NAREIT and stock returns compared

Average Return Standard deviation

1972-2015

NAREIT

S&P 500

12.0%

10.3%

17.1%

15.2%

1992-2015

NAREIT

S&P 500

11.2%

9.0%

19.1%

14.4% Sources: NAREIT and Standard and Poor’s.

Diversifying into alternative investments

• Two caveats about real estate:

1. Real estate is as cyclically sensitive as stocks are.

– It’s true that in the 2000-2001 recession, real estate did not fall with stocks.

– But in the financial crisis, the drop in REITs (65%) was more severe than in stocks (50%).

2. Current values in real estate (“Cap rates”) are high. It’s not a great time to add to this sector.

– On other hand, the outlook is not great in any sector.

Figure 11-4. NAREIT and S&P 500 Returns, 1992-2015 Data Sources: Ibbotson Associates and Zephyr Database

Crushed in financial crisis, but have come back fully

0

500

1000

1500

Dec-91 Dec-97 Dec-03 Dec-09 Dec-15

Ind

ex (

De

c 1

99

1 =

10

0)

NAREIT

S&P 500

Diversifying into alternative investments

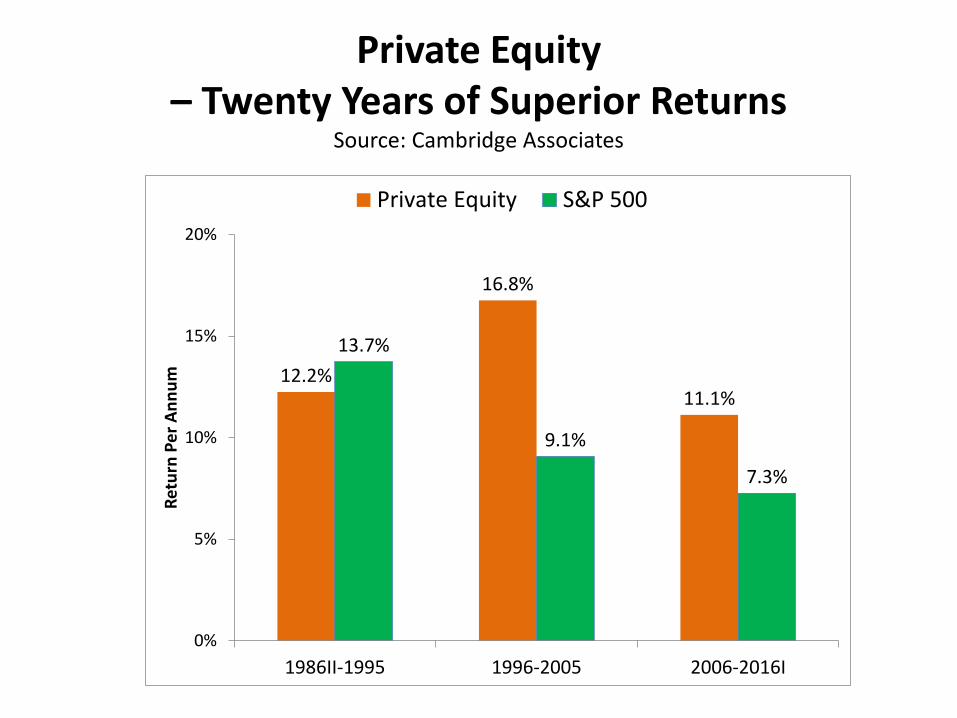

• Private equity: – Here we have an alternative investment that has proved

itself time and again.

– Cambridge Associates has reported its private equity series since 1986.

– Returns have been consistently above those of the private equity markets.

• My advice to endowments (and wealthy families) wealthy enough to invest in PE:

Take advantage of excess returns to buck the New Normal in public markets

Private Equity – Twenty Years of Superior Returns

Source: Cambridge Associates

12.2%

16.8%

11.1%

13.7%

9.1%

7.3%

0%

5%

10%

15%

20%

1986II-1995 1996-2005 2006-2016I

Ret

urn

Pe

r A

nn

um

Private Equity S&P 500

Diversifying into alternative investments

• So private equity provides an alternative to the New Normal only for large endowments – not for the rest of us.

The bottom line

• Investors face a “New Normal” of diminished returns.

• Economic growth has slowed throughout much of the world, so investment returns are likely to be lower than in the past.

My latest book published by Wiley

Investing for a Lifetime Managing Wealth for the “New Normal”

1) Saving and Investing

2) Choosing a Portfolio

3) Wealth Management

Also see my website

richardcmarston.com