The new norm: oil risk aversion, financial co-movements ... · Antonio Merino. Repsol Chief...

31

Antonio Merino. Repsol Chief Economist and Director Economic Research “The new norm: oil risk aversion, financial co-movements and fundamentals” London, UK May 13-14, 2013 6th Annual Crude Oil Summit New Supply, New Demand and the New World Order

-

Upload

truongdang -

Category

Documents

-

view

215 -

download

0

Transcript of The new norm: oil risk aversion, financial co-movements ... · Antonio Merino. Repsol Chief...

Antonio Merino. Repsol Chief Economist and Director Economic Research

“The new norm: oil risk aversion, financial co-movements and

fundamentals”

London, UK

May 13-14, 2013

6th Annual Crude Oil Summit

New Supply, New Demand and the New World Order

2

Discussion points

• A turning point in oil price formation: The break-up of the oil prices-

inventories relationship

• Explaining the 2004 changes: Surprises in the fundamentals and Oil as

an Asset Class

• The crisis 2008 – 2009: Tail events, co-movements and risk aversion

• 2013: Are we going back to fundamentals?

• Some final remarks

3

Discussion points

• A turning point in oil price formation: The break-up of the oil prices-

inventories relationship

• Explaining the 2004 changes: Surprises in the fundamentals and Oil as

an Asset Class

• The crisis 2008 – 2009: Tail events, co-movements and risk aversion

• 2013: Are we going back to fundamentals?

• Some final remarks

4 Source: EIA, NYMEX and Repsol Economic Research Department

A turning point in oil price formation Crude Oil Prices Evolution

Brent and WTI Crude Oil Prices Daily Evolution

0

20

40

60

80

100

120

140

160Jan-9

2

Oct-

92

Jul-9

3

Apr-

94

Jan-9

5

Oct-

95

Jul-9

6

Apr-

97

Jan-9

8

Oct-

98

Jul-9

9

Apr-

00

Jan-0

1

Oct-

01

Jul-0

2

Apr-

03

Jan-0

4

Oct-

04

Jul-0

5

Apr-

06

Jan-0

7

Oct-

07

Jul-0

8

Apr-

09

Jan-1

0

Oct-

10

Jul-1

1

Apr-

12

Jan-1

3

US

$ p

er

barr

el

Brent Crude Oil

WTI Crude Oil

0

20

40

60

80

100

120

140

160

2300 2400 2500 2600 2700 2800 2900

US

$/B

bl

Stocks in million barrels

Jan-92 → Dec-00

5 Source: EIA, NYMEX and Repsol Economic Research Department

A turning point in oil price formation The break-up of the oil prices-inventories relationship

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

0

20

40

60

80

100

120

140

160

2300 2400 2500 2600 2700 2800 2900

US

$/B

bl

Stocks in million barrels

Jan-01 → Jun-04

Jan-92 → Dec-00

6 Source: EIA, NYMEX and Repsol Economic Research Department

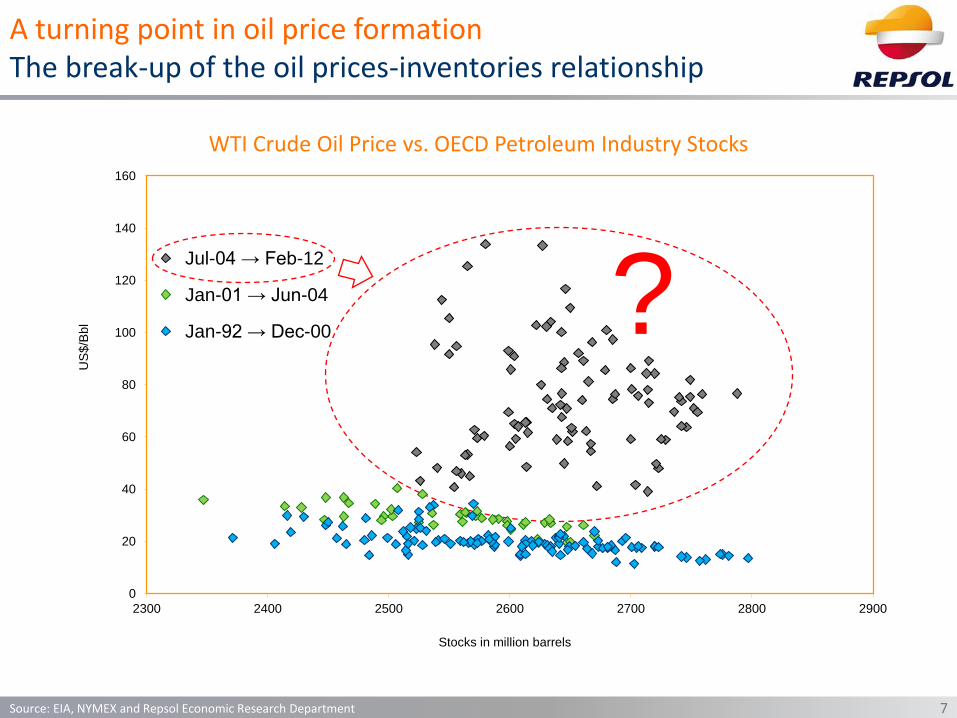

A turning point in oil price formation The break-up of the oil prices-inventories relationship

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

7 Source: EIA, NYMEX and Repsol Economic Research Department

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

A turning point in oil price formation The break-up of the oil prices-inventories relationship

?

0

20

40

60

80

100

120

140

160

2300 2400 2500 2600 2700 2800 2900

US

$/B

bl

Stocks in million barrels

Jul-04 → Feb-12

Jan-01 → Jun-04

Jan-92 → Dec-00

8

Discussion points

• A turning point in oil price formation: The break-up of the oil prices-

inventories relationship

• Explaining the 2004 changes: Surprises in the fundamentals and Oil as

an Asset Class

• The crisis 2008 – 2009: Tail events, co-movements and risk aversion

• 2013: Are we going back to fundamentals?

• Some final remarks

9 Source: EIA, NYMEX and Repsol Economic Research Department

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

Explaining the 2004 changes The break-up of the oil prices-inventories relationship

10

Non-OPEC Supply Annual Growth Surprises: Final Data - First Forecast

Explaining the 2004 changes: Surprises in the fundamentals Non-OPEC production → Unfulfilled expectations

Source: International Energy Agency (IEA) and Repsol Economic Research Department

0.50

0.30

-0.30

-1.10

-0.90

-1.20 -1.22

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Mill

ion B

arr

els

per

day

1.16 0.98 0.73 -0.08 0.35 0.22 -0.21

Actual YoY increment

Diference between final data and first forecast

10

14

18

22

26

30

341

97

11

97

21

97

31

97

41

97

51

97

61

97

71

97

81

97

91

98

01

98

11

98

21

98

31

98

41

98

51

98

61

98

71

98

819

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Mill

ion B

bl/d

Core OPEC Others OPEC

MAX OPEP-10 Production 2005 = 29.3 Million Bbl/d

11

OPEC Crude Oil Production: Core and not Core Countries

Explaining the 2004 changes: Surprises in the fundamentals OPEC Countries have not increased supply since the 70’s

Source: Enerdata, International Energy Agency (IEA) and Repsol Economic Research Department

Fuente: Thomson Reuters y Dirección de Estudios y Análisis del Entorno de Repsol

Profitability Index of different asset class

12

Explaining the 2004 changes: Oil as an asset class Oil began to be considered a financial asset

Source: Thomson Reuters and Repsol Economic Research Department

0

100

200

300

400

500

Jan-0

0

Jul-0

0

Jan-0

1

Jul-0

1

Jan-0

2

Jul-0

2

Jan-0

3

Jul-0

3

Jan-0

4

Jul-0

4

Jan-0

5

Jul-0

5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Jul-1

1

Jan-1

2

Jul-1

2

Jan-1

3

Index (

2000 =

100)

WTI

CRB

S&P 500 Total return

13

Discussion points

• A turning point in oil price formation: The break-up of the oil prices-

inventories relationship

• Explaining the 2004 changes: Surprises in the fundamentals and Oil as

an Asset Class

• The crisis 2008 – 2009: Tail events, co-movements and risk aversion

• 2013: Are we going back to fundamentals?

• Some final remarks

14 Source: EIA, NYMEX and Repsol Economic Research Department

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

The crisis 2008-2009: Tail events, co-movements and risk aversion The greatest economic downturn since 29’s crisis

65

70

75

80

85

90

95

100

105

110

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

meses desde el máximo

Crisis 2008 (índice abril 2008 = 100)

Crisis 1929 (índice junio 1929 = 100)

60

65

70

75

80

85

90

95

100

105

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

meses desde el máximo

Crisis 2008 (índice abril 2008 = 100)

Crisis 1929 (índice junio 1929 = 100)

2008 Crisis (Apr 2008 = 100)

1929 Crisis (Jun 1929 = 100)

Months from max

15 Source: Voxeu.org and Repsol Economic Research Department

Global Trade

The crisis 2008-2009: Tail events, co-movements and risk aversion The greatest economic downturn since 29’s crisis

The crisis 2008-2009: Tail events, co-movements and risk aversion The backstop to a worst economic crisis: Federal Reserve action

16

S&P 500 Index

Source: Datastream y Dirección de Estudios y Análisis del Entorno de Repsol

650

850

1,050

1,250

1,450

1,650

Ja

n-0

3

Ju

l-0

3

Ja

n-0

4

Ju

l-0

4

Ja

n-0

5

Ju

l-0

5

Ja

n-0

6

Ju

l-0

6

Ja

n-0

7

Ju

l-0

7

Ja

n-0

8

Ju

l-0

8

Ja

n-0

9

Ju

l-0

9

Ja

n-1

0

Ju

l-1

0

Ja

n-1

1

Ju

l-1

1

Ja

n-1

2

Ju

l-1

2

Ja

n-1

3

Ju

l-1

3

Po

ints

S&P 500

The crisis 2008-2009: Tail events, co-movements and risk aversion The backstop to a worst economic crisis: Federal Reserve action

17 Source: Datastream y Dirección de Estudios y Análisis del Entorno de Repsol

700

1,100

1,500

1,900

2,300

2,700

3,100

3,500

650

850

1,050

1,250

1,450

1,650

Ja

n-0

3

Ju

l-0

3

Ja

n-0

4

Ju

l-0

4

Ja

n-0

5

Ju

l-0

5

Ja

n-0

6

Ju

l-0

6

Ja

n-0

7

Ju

l-0

7

Ja

n-0

8

Ju

l-0

8

Ja

n-0

9

Ju

l-0

9

Ja

n-1

0

Ju

l-1

0

Ja

n-1

1

Ju

l-1

1

Ja

n-1

2

Ju

l-1

2

Ja

n-1

3

Ju

l-1

3

Bill

ion

US

D

Po

ints

S&P 500

FED total assets

S&P 500 Index and Federal Reserve total assets

18 Source: Thomson Reuters and Repsol Economic Research Department

250 Days Moving Correlation: Brent, S&P500 and Exchange Rate, daily changes

The crisis 2008-2009: Tail events, co-movements and risk aversion Systemic risk… everything is “co-movement” since Lehman

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Jan-9

4

Sep-9

4

Ma

y-9

5

Jan-9

6

Sep-9

6

Ma

y-9

7

Jan-9

8

Sep-9

8

Ma

y-9

9

Jan-0

0

Sep-0

0

Ma

y-0

1

Jan-0

2

Sep-0

2

Ma

y-0

3

Jan-0

4

Sep-0

4

Ma

y-0

5

Jan-0

6

Sep-0

6

Ma

y-0

7

Jan-0

8

Sep-0

8

Ma

y-0

9

Jan-1

0

Sep-1

0

Ma

y-1

1

Jan-1

2

Sep-1

2

Ma

y-1

3

S&P 500 and Exchange Rate EUR/USD

S&P 500 and Brent

19

Discussion points

• A turning point in oil price formation: The break-up of the oil prices-

inventories relationship

• Explaining the 2004 changes: Surprises in the fundamentals and Oil as

an Asset Class

• The crisis 2008 – 2009: Tail events, co-movements and risk aversion

• 2013: Are we going back to fundamentals?

• Some final remarks

20 Source: EIA, NYMEX and Repsol Economic Research Department

WTI Crude Oil Price vs. OECD Petroleum Industry Stocks

0

20

40

60

80

100

120

140

160

2300 2400 2500 2600 2700 2800 2900

US

$/B

bl

Stocks in million barrels

Apr-09 → Feb-12

Aug-08 → Mar-09

Jul-04 → Jul-08

Jan-01 → Jun-04

Jan-92 → Dec-00

2013: Are we going back to fundamentals? A new level for oil prices-inventories relationship

21 Source: International Energy Agency (IEA) and Repsol Economic Research Department

2013: Are we going back to fundamentals? Non-OPEC is delivering new production

Non-OPEC Supply Annual Growth Surprises: Final Data - First Forecast

0.50

0.30

-0.30

-1.10

-0.90

-1.20 -1.22

0.29

0.84

-0.24

-0.40

0.40

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Mill

ion B

arr

els

per

day

1.16 0.98 0.93 1.24 1.100.73 -0.08 0.35 0.22 -0.21 0.14 0.60

Actual YoY increment

2013: Are we going back to fundamentals? Ultimately technically recoverable resources are increasing

22

Ultimately technically recoverable resources and cumulative production

Source: IEA (WEO 2008 & WEO 2012) and Repsol Economic Research Department

-1222

-1128

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

-1222

-1128

1653

1241

1400

805

2840

2085

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

Cumulative Prod. @ t-1

P1 @ t-1

Conventional Oil

Unconventional

OTHER POTENTIALLY

RECOVERABLE VOLUMES

23 Source: IEA (WEO 2008 & WEO 2012) and Repsol Economic Research Department

Ultimately technically recoverable resources and cumulative production

2013: Are we going back to fundamentals? Ultimately technically recoverable resources are increasing

-1222

-1128

1653

1241

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

-1222

-1128

1653

1241

1400

805

2840

2085

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

Cumulative Prod. @ t-1

P1 @ t-1

Conventional Oil

Unconventional

OTHER POTENTIALLY

RECOVERABLE VOLUMES

24 Source: IEA (WEO 2008 & WEO 2012) and Repsol Economic Research Department

Ultimately technically recoverable resources and cumulative production

2013: Are we going back to fundamentals? Ultimately technically recoverable resources are increasing

-1222

-1128

1653

1241

1400

805

2840

2085

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

Cumulative Prod. @ t-1

P1 @ t-1

Conventional Oil

Unconventional

OTHER POTENTIALLY

RECOVERABLE VOLUMES

-1222

-1128

1653

1241

1400

805

2840

2085

-2000 -1000 0 1000 2000 3000 4000 5000 6000

WE

O 2

012

WE

O 2

008

Billion barrels

Cumulative Prod. @ t-1

P1 @ t-1

Conventional Oil

Unconventional

OTHER POTENTIALLY

RECOVERABLE VOLUMES

25 Source: Bloomberg and Repsol Economic Research Department

2013: Are we going back to fundamentals? Markets’ View: no so worried about the long term oil supply

Changes in the Future Market Crude Oil Price Perspectives

10

30

50

70

90

110

130

150

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

Ja

n-1

4

Ja

n-1

5

Ja

n-1

6

Ja

n-1

7

Ja

n-1

8

Ja

n-1

9

US

$ p

er

ba

rre

l

Historic Price

@ 7/5/2013

@ 7/1/2013

@ 7/5/2012

@ 7/5/2011

@ 1/5/2009

@ 1/6/2008

@ 1/1/2003

26 Source: IEA and Repsol Economic Research Department

Global Petroleum Demand Growth Rates Evolution by periods

2013: Are we going back to fundamentals? Global petroleum demand growing less

1.36%1.50%

-1.16%

0.95%0.80%

2000-2003 2004-2007 2008-2009 2010-2012 2013-2035

27 Source: IMF and Repsol Economic Research Department

2013: Are we going back to fundamentals? There are significant uncertainties about economic growth…

Global Economic Growth Revisions by IMF

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6A

pr-

11

Ma

y-1

1

Ju

n-1

1

Ju

l-1

1

Aug-1

1

Se

p-1

1

Oct-

11

No

v-1

1

De

c-1

1

Ja

n-1

2

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Ju

n-1

2

Ju

l-1

2

Aug-1

2

Se

p-1

2

Oct-

12

No

v-1

2

De

c-1

2

Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

% Y

oY

Gro

wth

Rate

2012 Global Economic Growth Forecast

2013 Global Economic Growth Forecast

28 Fuente: Thomson Reuters Datastream , Oxford Economics y Dirección de Estudios y Análisis del Entorno de Repsol

Central Bank Total Assets Evolution and Projections

? ?

0

10

20

30

40

50

60

70

De

c-0

8

Ma

r-0

9

Jun-0

9

Sep-0

9

De

c-0

9

Ma

r-1

0

Jun-1

0

Sep-1

0

De

c-1

0

Ma

r-1

1

Jun-1

1

Sep-1

1

De

c-1

1

Ma

r-1

2

Jun-1

2

Sep-1

2

De

c-1

2

Ma

r-1

3

Jun-1

3

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Sep-1

4

De

c-1

4

% P

IB

Fed

BCE

BOE

BOJ

2013: Are we going back to fundamentals? Growth and expectations are driven by Central Banks actions…

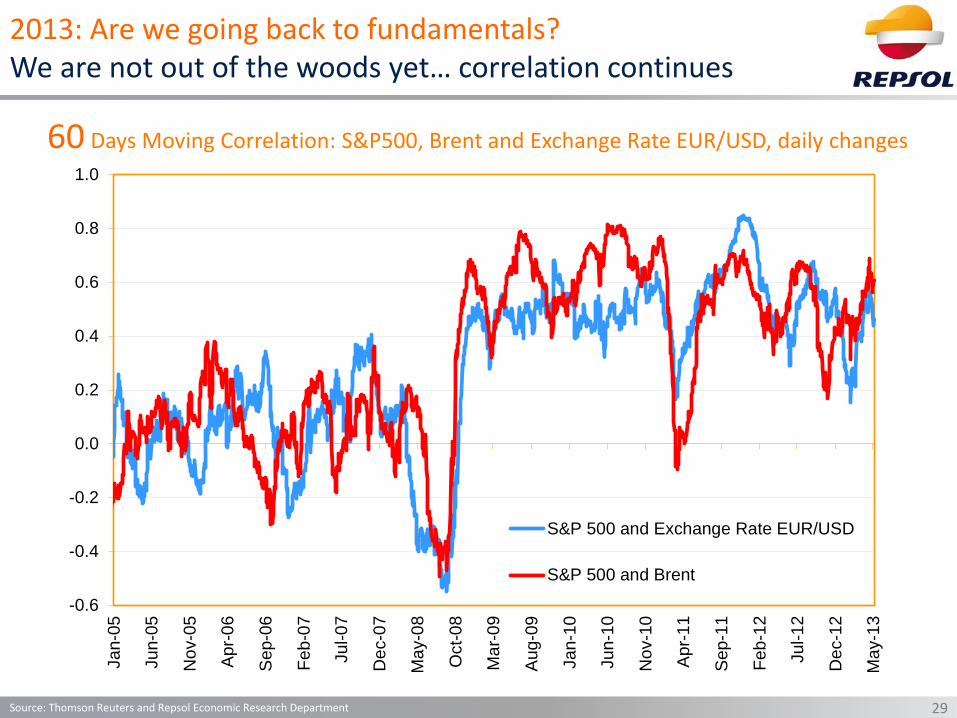

2013: Are we going back to fundamentals? We are not out of the woods yet… correlation continues

29 Source: Thomson Reuters and Repsol Economic Research Department

60 Days Moving Correlation: S&P500, Brent and Exchange Rate EUR/USD, daily changes

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Jan-0

5

Jun-0

5

No

v-0

5

Apr-

06

Sep-0

6

Feb

-07

Jul-0

7

De

c-0

7

Ma

y-0

8

Oct-

08

Ma

r-0

9

Aug-0

9

Jan-1

0

Jun-1

0

No

v-1

0

Apr-

11

Sep-1

1

Fe

b-1

2

Jul-1

2

De

c-1

2

Ma

y-1

3

S&P 500 and Exchange Rate EUR/USD

S&P 500 and Brent

30

Some final remarks

• Long term expectation about scarcity drove prices and investment in “Financial Oil” from 2004 to 2008

• After the 2008 crisis: Tail event fears and Co-movements ruled the scene and Quantitative Easing was the Central Banks prescription

• Are we going back to an oil price formation mechanism based on fundamentals, geopolitical and short term expectations?

• Long term supply worries have clearly been reduced although new production increases are limited to the US up to now.

• Regarding demand, less growth than before the crisis but big changes in sentiment link to tail event fears and monetary policy response…

• We continue living under the influence of increasing Central Bank balance-sheets, and market fears about when these expansionary measures are going to be reversed explain why we are still in a co-movements situation…