The NEW HUD-1 - A Line by Line Walk-Through - IBAT · The NEW HUD-1 - A Line by Line Walk-Through...

79

The NEW HUD-1 - A Line by Line Walk-Through Webinar February 17, 2010 9-10 a.m. CST Presenter Ms. Christine Sisseck Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286 972.562.1966 [email protected] Panelists Mr. Alan Jackson Dennis Schwartz & Assoc., Attorneys At Law 106 Blue Sky Court Georgetown, TX 78633 512.863.6845 [email protected] Ms. Charlotte M. Meyer Robertson & Anschutz 10333 Richmond Ave., Suite 550 Houston, TX 77042 713.980.9520 [email protected] Ms. Janet S. Minke, CTIA Alliant National Title Insurance Company 7967 S FM 51 Boyd, TX 76023-3810 303.647.4047 [email protected] Mr. Charles H. Newman, III Beadles, Newman & Lawler 3500 Hulen Fort Worth, TX 76107 817.731.6469 [email protected] Mr. Dennis Schwartz Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286 972.562.1966 [email protected]

Transcript of The NEW HUD-1 - A Line by Line Walk-Through - IBAT · The NEW HUD-1 - A Line by Line Walk-Through...

The NEW HUD-1 - A Line by Line Walk-Through

Webinar

February 17, 2010 9-10 a.m. CST

Presenter Ms. Christine Sisseck Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286 972.562.1966 [email protected] Panelists Mr. Alan Jackson Dennis Schwartz & Assoc., Attorneys At Law 106 Blue Sky Court Georgetown, TX 78633 512.863.6845 [email protected] Ms. Charlotte M. Meyer Robertson & Anschutz 10333 Richmond Ave., Suite 550 Houston, TX 77042 713.980.9520 [email protected]

Ms. Janet S. Minke, CTIA Alliant National Title Insurance Company 7967 S FM 51 Boyd, TX 76023-3810 303.647.4047 [email protected] Mr. Charles H. Newman, III Beadles, Newman & Lawler 3500 Hulen Fort Worth, TX 76107 817.731.6469 [email protected] Mr. Dennis Schwartz Dennis Schwartz & Assoc., Attorneys At Law 1446 Heritage Dr Mc Kinney, TX 75069-3286 972.562.1966 [email protected]

Alan W. Jackson Compliance Administrator Schwartz and Associates Al has extensive experience in the residential mortgage business including loan production, loan servicing, regulatory compliance and government relations. Previously he served as Vice President of Government Relations at CitiMortgage, Inc. (St. Louis), and Vice President of Compliance and Government Issues at Principal Residential Mortgage, Inc. (Des Moines). Al has participated in various working groups of the Mortgage Bankers Association, Financial Services Roundtable, and the Consumer Mortgage Coalition, and is past chair of the Principal Financial Group Political Action Committee. Al obtained a Bachelor of Science degree in Mathematics & Business from Minnesota State University, and attended graduate school at the University of Colorado and Drake University Law School Christine Sisseck Operations Manager Schwartz and Associates Christine has been with Schwartz & Associates, a real estate document preparation Texas law firm, for 20 years. Employed in the mortgage industry since 1985, she has a broad and detail knowledge of residential real estate regulations and compliance matters, as well as experience in all phases of loan production, closing and operations. Prior to Schwartz & Associates, she worked at Merrill Lynch Mortgage, First Union Mortgage and Gregory Gregg & Associates. Christine attended Missouri Southern State College in Joplin, Missouri. Her expertise, attention to detail and commitment to accuracy in document preparation have been instrumental in taking Schwartz & Associates from a start-up operation to a national document preparation firm with a reputation for knowledge and quality.

CHARLOTTE M. MEYER Attorney at Law

Robertson & Anschutz 10333 Richmond Avenue

Suite 550 Houston, Texas 77042

713-980-9520 [email protected]

EDUCATION B.A. in Journalism, South West Texas State University - 1980 J.D., South Texas College of Law - 1986

PROFESSIONAL ACTIVITIES Texas Land Title Association – Education Committee Certification Committee Legal Issues Committee Texas Mortgage Bankers Association The College of the State Bar of Texas Texas Association of Mortgage Attorneys

LICENSURES AND CERTIFICATIONS State Bar of Texas United States – Southern, Eastern, Western and Northern Districts Courts of Texas Texas Board of Legal Specialization – Residential Real Estate Texas Board of Legal Specialization – Farm and Ranch Real Estate Certified Title Insurance Associate

PUBLICATIONS AND ARTICLES Tierra Grande Magazine – “Recognizing Mortgage Fraud” (January 2006) Co-Author State Bar of Texas 28th Annual Advanced Real Estate Law Course – “The Non-Borrowing Spouse in

Real Estate Transactions” (2006) Co-Author Texas Mortgage Lending Law & Practices Deskbook – Contributing Author Texas Mortgage Bankers Association Annual Education Seminars – “Fraud, Closing and Disclosing”

(2006) Author and Lecturer Texas Mortgage Bankers Association/Texas Land Title Association – “The New RESPA Road: Where

Lenders and Title Intersect” (2009) Panelist Texas Land Title Association Regional Seminars –

“The Legal Perspective – Deceased Real Property” (2004) Author and Lecturer “Advanced Title Examinations and Underwriting – Easements” (2006) Author and Lecturer “Liabilities and Responsibilities of a Notary Public” (2006) Author and Lecturer “Lost in Translation –Lender Lingo” (2007) Author and Lecturer “Ad Valorem Taxation” (2008) Lecturer “Foreclosure and Its Various Alternatives” (2009) Author and Lecturer “RESPA and the New HUD-1 – Hands On, How To Workshops” (2009) Lecturer

JANET S. MINKE Vice President, Underwriting Support Services

Alliant National Title Insurance Company Toll-free: 877-788-9800 x440

Direct: 303-647-4047 Mobile: 817-832-5656

EDUCATION • BA in Social Science from University of North Texas, 1970 • Texas Secondary Teaching Certificate

TITLE INSURANCE EXPERIENCE Ms. Minke entered the title insurance industry as an escrow assistant and conveyancer in a fee attorney office in Fort Worth, Texas, in 1970. Shortly thereafter, the attorney retired, selling his closing offices to Guardian Title Company, where Ms. Minke remained until 1994, progressing from escrow assistant to commercial escrow officer and eventually to Executive Vice President. Since that time, she has held various regional and national roles with major national title insurance companies where for the past 10 years she was a Business Process Manager and Corporate Trainer. She has recently moved into her current position with Alliant National, where she is available to respond to underwriting questions, as well as providing training and education for the company’s partner agents.

TEXAS LAND TITLE ASSOCIATION ACTIVITIES AND HONORS • Honors: Title Woman of the Year – 2006

Professional Excellence Award – Outstanding Underwriter Support, 2005 Peggy Hayes Teaching Excellence Award, 1995 President’s Award for Outstanding and Exemplary Contribution, 1992-93 Outstanding Young Title Person, 1985-86

• Current Chair: Education Committee • Current Member: Certification Task Force, Regulatory Committee

TEACHING AND TRAINING ACTIVITIES • TLTA and NMLTA Land Title School and Texas Land Title Institute • State Bar of Texas: Advanced R E Law Course – 2006; Agricultural Law Course – 2009 • TLTA, OLTA, NMLTA and NAPMW Conferences and Seminars • Underwriter Agency Seminars and Training in Texas, New Mexico and Oklahoma

PUBLICATIONS - Articles in TLTA News • Money-Saving Ideas That Everyone Can Use, 1988 • Proper Time Management Ensures Efficient Closings, 1989 • Tips Help Clarify Procedural Rules, 1991 • Training Today’s Workforce: Educating for Excellence, 1997

Charles H. Newman Biography Charles H. Newman is a founding partner and Chairman of the Board of Beadles, Newman & Lawler, P.C. Beadles, Newman & Lawler is a real estate law firm whose primary focus is the preparation of residential and commercial closing documents and is located in Fort Worth, Texas. The firm clients include national and regional banks, mortgage companies as well as title companies.

Mr. Newman’s career started in the title industry. From 1978 to 1999, he was Chairman of the Board and Chief Executive Officer for Trinity Western Title. Trinity Western Title was purchased by Alamo Title and ultimately by Fidelity National Title. He was honored as Title Man of the Year by the Texas Land Title Association in 1981 and he served as President of the Texas Land Title Association from 1982 to 1983. Mr. Newman is Board Certified in Commercial and Residential Real Estate Law by the Texas Board of Legal Specialization. He is a member of the State Bar of Texas, the Texas College of Real Estate Attorneys, the National Mortgage Bankers Association and the Texas Mortgage Bankers Association. He received his Bachelor of Arts from Washington & Lee University in Lexington, Virginia and his Juris Doctorate from the University of Texas School of Law in Austin, Texas. Charles is in high demand as a speaker. His presentations combine an informal style with humor and real world examples. His topics include Federal Regulatory Compliance, real estate and title related issues.

Executive Biography: Dennis P. Schwartz

Founder

DocsDirect (Schwartz & Associates)

Dennis P. Schwartz is founder of McKinney, Texas-

based Schwartz & Associates real estate law. Since 1989,

Schwartz & Associates has specialized in residential loan

document preparation for mortgage lenders of all sizes.

Under Schwartz’s leadership, Schwartz & Associates has developed DocsDirect

Online, a Web-based mortgage document solution that offers the flexibility

needed to handle the array of lender channels and loan programs offered by their

clients.

From 1996 to 2001, Mr. Schwartz was general counsel for the Texas

Mortgage Broker Association and is currently general counsel to the Tarrant

County Mortgage Broker Association and Dallas Association of Mortgage

Brokers. He was a member of the Board of Directors for the Texas Association of

Mortgage Brokers from 2002 - 2008.

Mr. Schwartz was a key participant in drafting legislation and

communicating with state political figures for the passage of the Texas mortgage

broker licensing and home equity constitutional amendment. He is an active

member of many other associations, including the State Bar of Texas, National

Mortgage Brokers Association and the Independent Bankers Association of

Texas.

Mr. Schwartz began practicing law in 1976 with the Tarrant County District

Attorney’s office. From 1977 until 1983, he was a litigator in a general practice

law firm. He began his focus on real estate law in 1983 representing numerous

savings and loan associations. Since 1989, he has limited his practice to

residential real estate lending document preparation representing banks,

mortgage brokers and wholesale lenders nationwide.

After receiving his Bachelor’s degree from Sarah Lawrence College in

1973, Mr. Schwartz received his Juris Doctor from Southern Methodist University

in 1976.

1

PresenterChristine Sisseck, Schwartz & Associates, McKinney

PanelistsAlan Jackson, Schwartz & Associates, McKinney

Charlotte M. Meyer, CTIA, Robertson & Anschutz, HoustonJanet S. Minke, CTIA, Alliant National Title Insurance Company, Dallas

Charles H. Newman, III, Beadles, Newman & Lawler, DallasDennis Schwartz, Schwartz & Associates, McKinney

Welcome to Today’s WebinarPresented by

Independent Bankers Association of Texas and

Texas Land Title AssociationFebruary 17, 2010

Purpose of this presentation is to provide a detailed line by line instruction on how to complete the HUD1 Settlement Statement.

Whether you are a loan originator, processor, underwriter, closer, doc prep attorney or closing agent, everyone needs to have an understanding of the GFE and HUD1 as they now go

hand in hand.

It is truly a collaborative effort for all parties.

RealEstateSettlementProceduresAct

1974RESPA Introduced

19961st RESPA Reform

2002Additional Reform Process began

March 14, 2008Proposed New Rule released

November 17, 2009Final New Rule published

January 1, 2009Portions Final New Rule effective

January 1, 2010Final New Rule effective

RealEstateSettlementProceduresAct

RESPA Reformimpacts all parties in

a real estate transaction

LendersTitle ProvidersSettlement AgentsMortgage BrokersRealtorsBuildersBuyers – BorrowersSellers

New RESPA Final RuleConsumer Protection Act

Greater Disclosure of Loan Terms and Settlement Fees

New standardized forms

Encourages consumer to shop for loan and service providers

Fees disclosed upfront must be closer to the actual fees collected at closing

Lender bound to settlement charges and terms disclosed in GFE, subject to certain tolerances

Goal was clarity, transparency and accuracy

5

New RESPA Final RuleNew Good Faith Estimate

New HUD‐1 Settlement Statement

Service Provider List

6

HUD‐1 Settlement StatementHUD‐1 Settlement Statement(HUD1) itemizes all the settlement charges

incurred with a federally related mortgage loan.

HUD‐1A is an abbreviated version of the HUD1 that can be used if there is no seller involved in the transaction, such as for refinances.

New Standardized HUD1 Settlement Statement – 3 pages

Re‐designed HUD1 Page 2 references GFE Block numbers

New Page 3 directly compares GFE estimated charges with final HUD1 charges

Tolerance Restrictions0% Bucket10% BucketUnlimited Bucket

7

HUD1 Settlement StatementLender’s Responsibility

Must provide all information from GFE and Loan Terms to Settlement Agent in order to complete HUD1 properly

Settlement Agent’s ResponsibilityMust properly prepare and complete HUD1

Borrower’s RightMay request review of HUD1 one day prior to settlement

8

Suggestions on what to provideLender is responsible for providing SettlementAgent with all the information from GFE and LoanTerms necessary to properly complete the HUD‐1

Suggested forms to provide to Settlement Agent:

Last Good Faith Estimate disclosed to consumerServicer Provider List disclosed to consumerComprehensive Closing InstructionsSample of items for HUD‐1 which reflect

800 series for Page 2 of HUD1Loan Summary Information for Page 3 of HUD‐1

HUD1 – Page OneSummary of Transaction

Identification of Loan and Parties to TransactionSummary of Borrower’s TransactionSummary of Seller’s TransactionBottom Line Amount Due from/to Borrower and Seller

10

HUD1 – Page One

11

HUD1 – Page TwoListing of All Settlement Charges

Same Series or Grouping of Fees

Line Items have been renamed or repositioned

Reference to corresponding GFE Block Number

“Inside” and “Outside” Column Line Items

Total of Borrower and Seller Column

12

HUD1 – Page Two

13

HUD1 – Page ThreeComparison Chart

Estimated GFE Fees vs. Actual HUD1 FeesCharges That Cannot Increase (0%) Charges That in Total Cannot Increase More Than 10%

Charges That Can Change (Unlimited)

Key Loan TermsInitial Loan Terms”Red Flag” Items

Adjustments in rate and paymentNegative AmortizationPrepayment PenaltiesBalloon Payments

Escrow Account SummaryTotal Monthly Payment

14

HUD1 – Page Three

15

HUD1 – Page One, Header Boxes

16

HUD1 – Page One, 200 series200. Amounts Paid by or in Behalf of Borrower

17

HUD1 – Page One, 200 series200. Amounts Paid by or in Behalf of Borrower

Credits to Borrower reflected in Lines 204 ‐ 209From Seller for Closing Costs (HUD‐1 Seller‐paid items FAQ 1 & 2)

From Lender for POC items or payment of Closing CostsFrom Third Party (HUD‐1 200 Series FAQ 4)

Credits to Cure Tolerance Violations may be reflected in Lines 204‐209 (Section 4 and 5 – Right to cure and tolerance violations FAQ 12)

Second Lien Proceeds (HUD‐1 200 Series FAQ 1)

18

HUD1 – Page One, 500 series500. Reductions in Amount Due to Seller

19

HUD1 – Page One, 500 series500. Reductions in Amount Due to Seller

Credits to Borrower reflected in Lines 504 – 509From Seller for Closing Costs

(HUD‐1‐Page 1, HUD‐1 Seller‐paid items FAQ 1 & 2)

20

HUD1 – Page TwoPre‐2010 (Old) HUD1

If Seller pays fee, listed in Seller ColumnIf Borrower pays fee, listed in Borrower Column

New 2010 HUD1If fee disclosed on GFE, no matter who pays fee, listed in Borrower ColumnIf Seller or Third Party pays fee that was disclosed on GFE

Charge must be shown inside Borrower Column on HUD1 Page 2Offset by reflecting Credit to Borrower on HUD1 Page 1 in Lines 204‐209 If paid by Seller, also a Charge to Seller must be reflected on HUD1 Page in Lines 506‐509

(HUD‐1‐General FAQ 6, HUD‐1 Seller‐paid items FAQ 1 & 2)

21

HUD1 – Page Two“Borrower Responsible Fees”

Fees that are typically Borrower Costs or normally paid by Borrower

Should have been disclosed on GFE, no matter who ultimately pays for the fees at closing

Will be reflected in Borrower Column on HUD1 Page 2, no matter who ultimately pays for the fees at closing

If fee is being paid by seller, lender or third party, shown in Borrower Column on HUD1 Page 2 and a credit is shown on HUD1 Page 1

22

HUD1 – Page Two“Seller Responsible Fees”

Fees that are typically Seller Costs or normally paid by Seller

Were not disclosed on GFEIf disclosed on GFE, then must be reflected in Borrower ColumnOn HUD1 Page 2 and show as seller credit on HUD1 Page 1

Will be reflected in Seller Column on HUD1 Page 2

Exception to above rule:On a purchase transaction, Owner’s Title Policy must always bedisclosed on GFE no matter if seller responsible fee, therefore mustalways be reflected inside Borrower column on HUD1 Page 2 andoffset by credit on HUD 1 Page 1 (HUD‐1 Seller‐paid items FAQ 1)

23

HUD1 – Page Two“Inside the Columns” ‐ Aggregate Totals, except 801, are reflected “inside the columns”

“Outside the Columns” – If fees are itemized, normally shown indented “outside the columns”

24

HUD1 – Page TwoGFE Block Number Reference ‐ HUD1 Lines on Page 2 have a cross reference to GFE Block Number*

*The dollar amount reflected should be the amount to be collected at closing not theamount disclosed on GFE.

25

HUD1 – Page TwoRoll‐up Lines ‐ Line item is a total of individual fees which may or may not be itemized in a particular series

Roll‐up Line – 703, 801, 803, 1001, 1101, 1201, 1203, 1301 are an aggregate total of individual feesTypically collected inside the column the Borrower column (except 801)Typically the first line item in a series (except 703, 803, 1203)

26

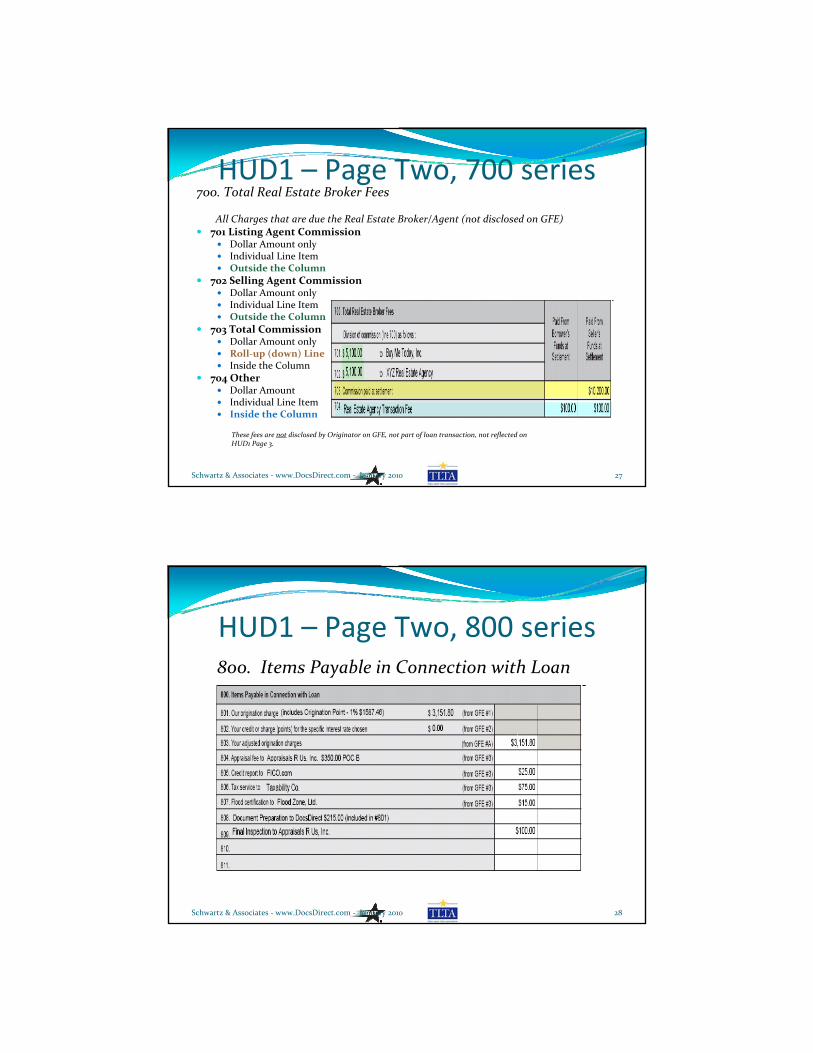

HUD1 – Page Two, 700 series700. Total Real Estate Broker Fees

All Charges that are due the Real Estate Broker/Agent (not disclosed on GFE)701 Listing Agent Commission

Dollar Amount onlyIndividual Line ItemOutside the Column

702 Selling Agent CommissionDollar Amount onlyIndividual Line ItemOutside the Column

703 Total CommissionDollar Amount onlyRoll‐up (down) LineInside the Column

704 OtherDollar AmountIndividual Line ItemInside the Column

These fees are not disclosed by Originator on GFE, not part of loan transaction, not reflected onHUD1 Page 3.

Schwartz & Associates ‐ www.DocsDirect.com ‐ January 2010 27

HUD1 – Page Two, 800 series800. Items Payable in Connection with Loan

Schwartz & Associates ‐ www.DocsDirect.com ‐ January 2010 28

HUD1 – Page Two, Line 801801. Our Origination Charge

Schwartz & Associates ‐ www.DocsDirect.com ‐ January 2010 29

HUD1 – Page Two, Line 801801. Our origination charge (HUD‐1 800 series FAQ 1)

All Charges that Originator will receive for compensationAdministrative FeeApplication FeeBroker FeesCommitment FeeCourier/Delivery FeeIn‐house AppraisalLender Inspection FeeDocument Preparation Fee (even if paid to third party) (HUD‐1 800 series FAQ 2)

MERS Fee (HUD‐1 800 series FAQ 9)

Origination FeeProcessing FeeUnderwriting FeeVerification FeeWire FeeService Fees paid directly to OriginatorMiscellaneous FeesYield Spread Premium (for table funding brokers)

Schwartz & Associates ‐ www.DocsDirect.com ‐ January 2010 30

HUD1 – Page Two, Line 801801. Our origination charge

Roll‐up Line“Outside the Columns”Does include YSP, but does not include Discount PointsNo POC items (HUD‐1 800 series FAQ 4)

If individual fee included in 801 was prepaid/POC, amount prepaid/POC must shown as credit or refunded to Borrower on HUD1Page 1 in 200s

Disclosed in Block 1 on GFEZero Tolerance BucketAny increase must be cured by Lender reimbursement

HUD Line 801 = GFE Block 1 = 0% Tolerance Bucket31

HUD1 – Page Two, Line 801801. Our origination chargeIRS 1098 Reporting of Actual Origination Points allowed(HUD‐1 800 series FAQ 10)

PercentageDollar AmountOutside the Columns

32

HUD1 – Page Two, Line 802802. Your Credit or Charge (Points) for the specific interest rate chosen

33

HUD1 – Page Two, Line 802802. Your Credit or Charge (Points) for the specific interest rate chosen

Zero, if no credit and no chargeCredit (HUD‐1 800 series FAQ 5)

Charge

A credit and charge cannot occur together in same transaction

34

HUD1 – Page Two, Line 802802. Your Credit or Charge (Points) for the specific interest rate chosen

CreditMust be equal to or greater than credit disclosed on GFEYield Spread Premium for Table Funding Brokers“No cost” Loan Credit

Fees being paid through interest rateCredit given used to offset all fees

35

HUD1 – Page Two, Line 802802. Your Credit or Charge (Points) for the specific interest rate chosen

ChargeMust be equal to or less than charge disclosed on GFEDiscountEscrow Waiver FeeBuydown

36

HUD1 – Page Two, Line 802802. Your Credit or Charge (Points) for the specific interest rate chosen

Individual Fee Line“Outside the Columns”No POC items

No longer reflect YSP payment from lender to broker on HUD1No Percentage shown

Disclosed in Block 2 on GFEZero Tolerance BucketAmount should match amount disclosed in GFE Block 2

Any credit for rate chosen cannot decreaseCredit can increase since it would benefit borrower

Any charge for rate chosen cannot increaseCharge can decrease since it would benefit borrower

HUD Line 802 = GFE Block 2 = 0% Tolerance Bucket

37

HUD1 – Page Two, Line 803803. Your Adjusted Origination Charges

Schwartz & Associates ‐ www.DocsDirect.com ‐ January 2010 38

HUD1 – Page Two, Line 803803. Your Adjusted Origination Charges

Line 801 +/‐ Line 802 = Line 803

May be a negative number if Credit in Line 802 exceeds Charge in Line 801

39

HUD1 – Page Two, Line 803803. Your Adjusted Origination Charge

Roll‐up (down) Line of 801 and 802“Inside the Columns”No POC items

Disclosed in Block A on GFEZero Tolerance BucketAmount should match amount disclosed in GFEBlock A

HUD Line 803 = GFE Block A = 0% Tolerance Bucket

40

HUD1 – Page Two, Line 804 ‐ 807

41

HUD1 – Page Two, Line 804 ‐ 807

Individual Fee Lines ( Appraisal Fee: HUD‐1 800 series FAQ 6, 8 & 11)“Inside the Columns”POC items are reflected “outside the columns”Payable to the appropriate service providerLines cannot be renamed or used for any other item

Disclosed in Block 3 on GFE10% Tolerance Bucket – aggregate total, even if POCFees payable to third party other than Originator

HUD Line 804, 805, 806, 807, 800s inside the column fees =GFE Block 3 = 10% Tolerance Bucket

42

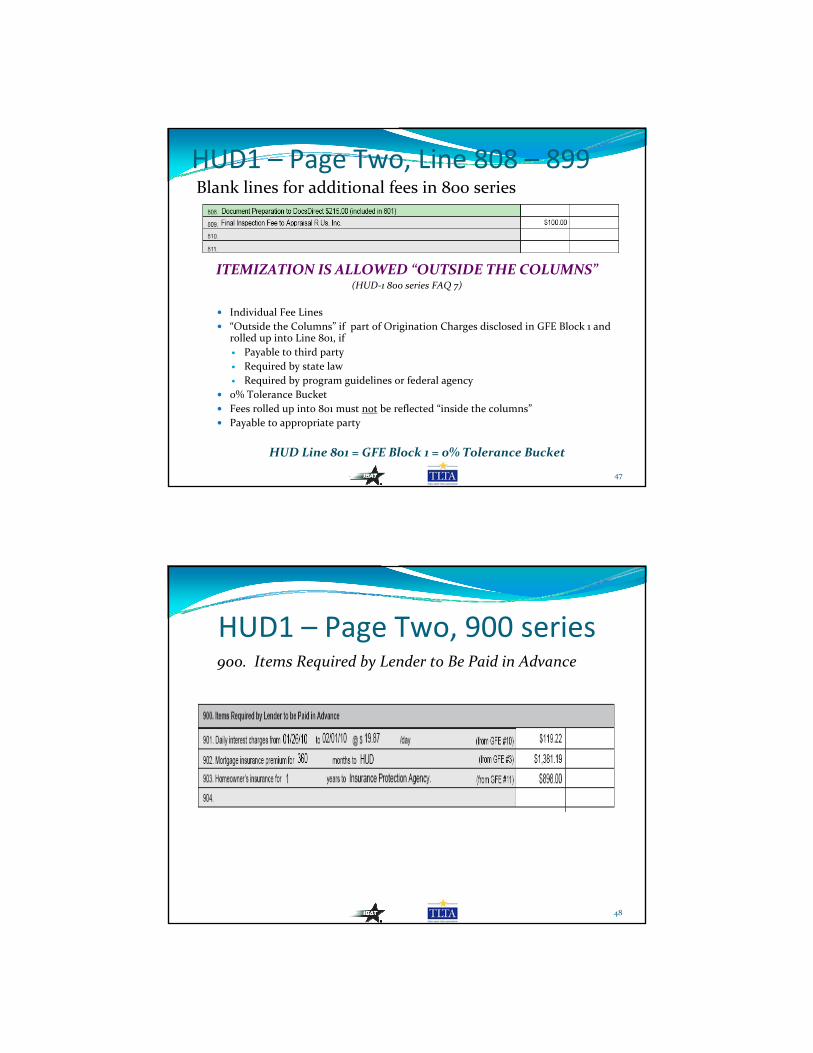

HUD1 – Page Two, Line 808 ‐899Blank lines for additional fees in 800 series

43

HUD1 – Page Two, Line 808 ‐ 899Blank lines for additional fees in 800 series

Any Charges for services that Originator requires use of a particular provider, that do not have a specific line item and disclosed in GFE Block 3

Final Inspection FeeMCC Fee

44

HUD1 – Page Two, Line 808 – 899

Individual Fee Lines“Inside the Columns” if Required Services Lender Selects and disclosed in GFE Block 3POC items are reflected “outside the columns”, if Required Services Lender Selects and disclosed in GFE Block 3Payable to the appropriate service providerAdditional lines can be added if necessary by separate page

Disclosed on Block 3 on GFE10% Tolerance Bucket – aggregate total, even if POCFees payable to third party other than Originator

HUD Line 804, 805, 806, 807, 800s inside the column fees =GFE Block 3 = 10% Tolerance Bucket

45

HUD1 – Page Two, Line 808 ‐ 899Blank lines for additional fees in 800 series

Any Charges for services that Originator rolled into Line 801 payable to a third party

Document Preparation FeeIRS Transcript FeeVerification of Employment Service Fee

46

HUD1 – Page Two, Line 808 – 899Blank lines for additional fees in 800 series

ITEMIZATION IS ALLOWED “OUTSIDE THE COLUMNS”(HUD‐1 800 series FAQ 7)

Individual Fee Lines“Outside the Columns” if part of Origination Charges disclosed in GFE Block 1 and rolled up into Line 801, if

Payable to third partyRequired by state lawRequired by program guidelines or federal agency

0% Tolerance BucketFees rolled up into 801 must not be reflected “inside the columns”Payable to appropriate party

HUD Line 801 = GFE Block 1 = 0% Tolerance Bucket

47

HUD1 – Page Two, 900 series900. Items Required by Lender to Be Paid in Advance

48

HUD1 – Page Two, Line 901901. Daily Interest Charges

The charge for the amount of interest on new loan due from date of settlement until first day of next month or first day of normal payment cycle

Date of Disbursement/Funding

First Day of the Coming Month

Amount of Interest to be collected Daily(Loan Amount x Interest Rate divided by Per Diem Factor [360, 365 or 366] = Amount of Daily Interest)

Total Amount of Interest to be collected or credited at Closing(Number of Days of Interest Due at Closing x Amount of Daily Interest = Total Interest Due at Closing)*

(If interest credit: Number of Days of Interest Credit Due at Closing x Amount of Daily Interest = Total InterestCredit Due at Closing*) (HUD1 900 series FAQ 2)

*Interest credit is shown as a negative number

49

HUD1 – Page Two, Line 901901. Daily Interest Charges

Individual Fee Line“Inside the Columns”Line cannot be renamed or used for any other item

Disclosed in Block 10 on GFEUnlimited Tolerance BucketCredit reflected if short pay/interest credit applies

HUD Line 901 = GFE Block 10 = Unlimited Tolerance Bucket

50

HUD1 – Page Two, Line 902902. Mortgage Insurance Premium

Number of months Premium coversConventional = 1 month – Loan Term, depends on coverage plan required by loan program and/or selected by LenderFHA = Loan Term

Payable to Conventional = MI CompanyFHA = FHA

Total Amount of MI Premium due at closing

51

HUD1 – Page Two, Line 902902. Mortgage Insurance Premium

Individual Fee Line“Inside the Columns”Line cannot be renamed or used for any other item

Disclosed in Block 3 on GFE10% Tolerance Bucket – aggregate totalPayable to appropriate entity

HUD Line 902 = GFE Block 3 = 10% Tolerance Bucket

52

HUD1 – Page Two, Line 903903. Homeowner’s Insurance

Number of years Premium coversPurchase = 1 Year is usually collected at closingRefinance = 0 – 1 Year, depends on if additional payment or coverage is necessary to meet investor guidelines

Payable to insurance company/agentTotal Amount of Insurance Premium due at closing or collected outside of closing, as appropriate

53

HUD1 – Page Two, Line 903903. Homeowner’s Insurance

Individual Fee Line“Inside the Columns”POC items are reflected “outside the columns”Line cannot be renamed or used for any other item

Disclosed in Block 11 on GFEUnlimited Tolerance BucketPayable to insurance company

HUD Line 903 = GFE Block 11 = Unlimited Tolerance Bucket

54

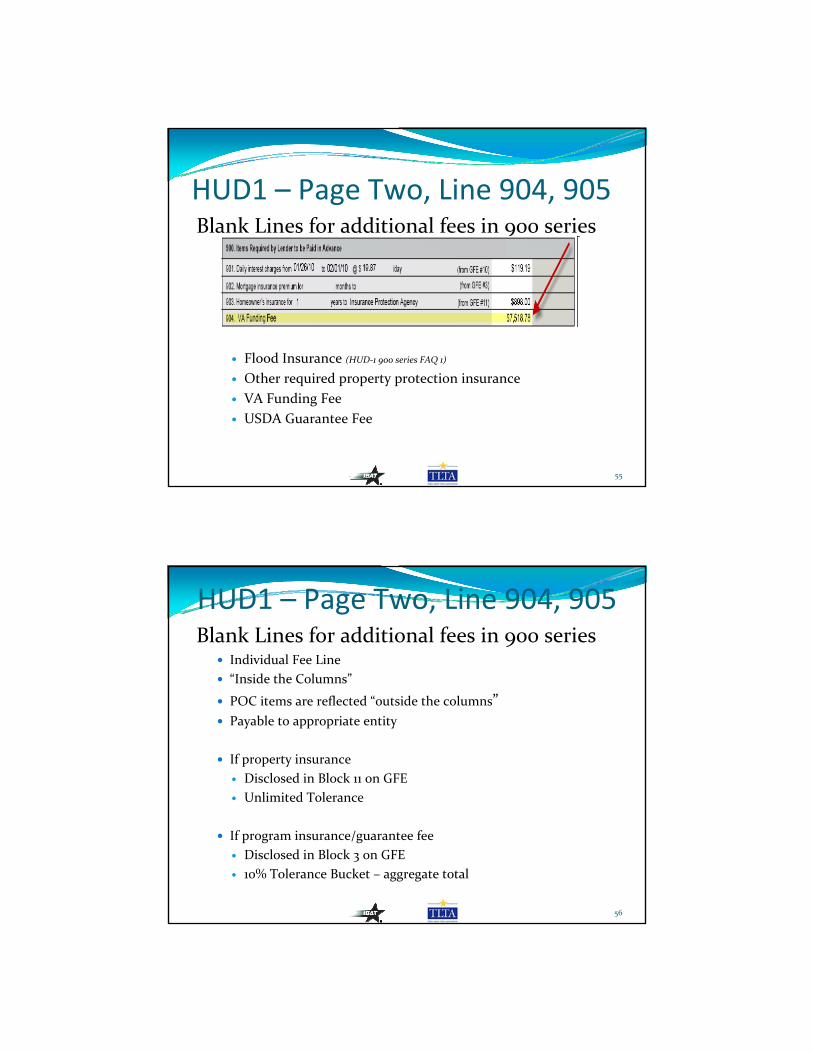

HUD1 – Page Two, Line 904, 905Blank Lines for additional fees in 900 series

Flood Insurance (HUD‐1 900 series FAQ 1)

Other required property protection insuranceVA Funding FeeUSDA Guarantee Fee

55

HUD1 – Page Two, Line 904, 905Blank Lines for additional fees in 900 series

Individual Fee Line“Inside the Columns”

POC items are reflected “outside the columns”Payable to appropriate entity

If property insuranceDisclosed in Block 11 on GFEUnlimited Tolerance

If program insurance/guarantee feeDisclosed in Block 3 on GFE10% Tolerance Bucket – aggregate total

56

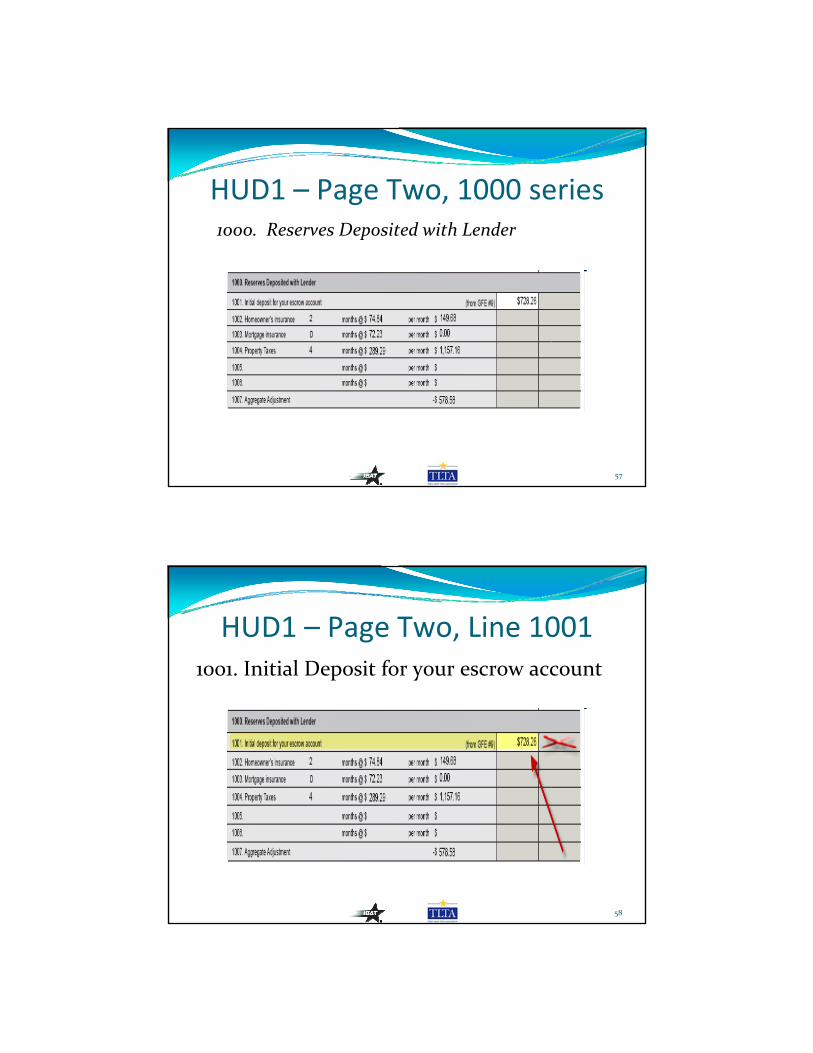

HUD1 – Page Two, 1000 series1000. Reserves Deposited with Lender

57

HUD1 – Page Two, Line 10011001. Initial Deposit for your escrow account

58

HUD1 – Page Two, Line 10011001. Initial Deposit for your escrow account

All Charges that lender requires borrower to place into a reserve or escrow account at settlement to be applied to recurring charges that lender pays on behalf of borrower (HUD1 1000 series FAQ 1)

Condo Content InsuranceEarthquake InsuranceHomeowner’s InsuranceFlood InsuranceMortgage InsuranceProperty TaxesWindstorm/Hail Insurance

59

HUD1 – Page Two, Line 10011001. Initial Deposit for your escrow account

Total Amount to be collected at closing to begin the borrower’s escrow/impound account for the loan

Includes Line 1002 – 1006 (and additional 1000s items if applicable)Less Aggregate Adjustment (typically 1007 or last line in 1000s)

Roll‐up Line“Inside the Columns”Disclosed in Block 9 of GFEUnlimited Tolerance BucketLine cannot be renamed or used for any other itemDoes not include amount to bring property taxes current at closing

HUD Line 1001 = GFE Block 9 = Unlimited Tolerance Bucket

60

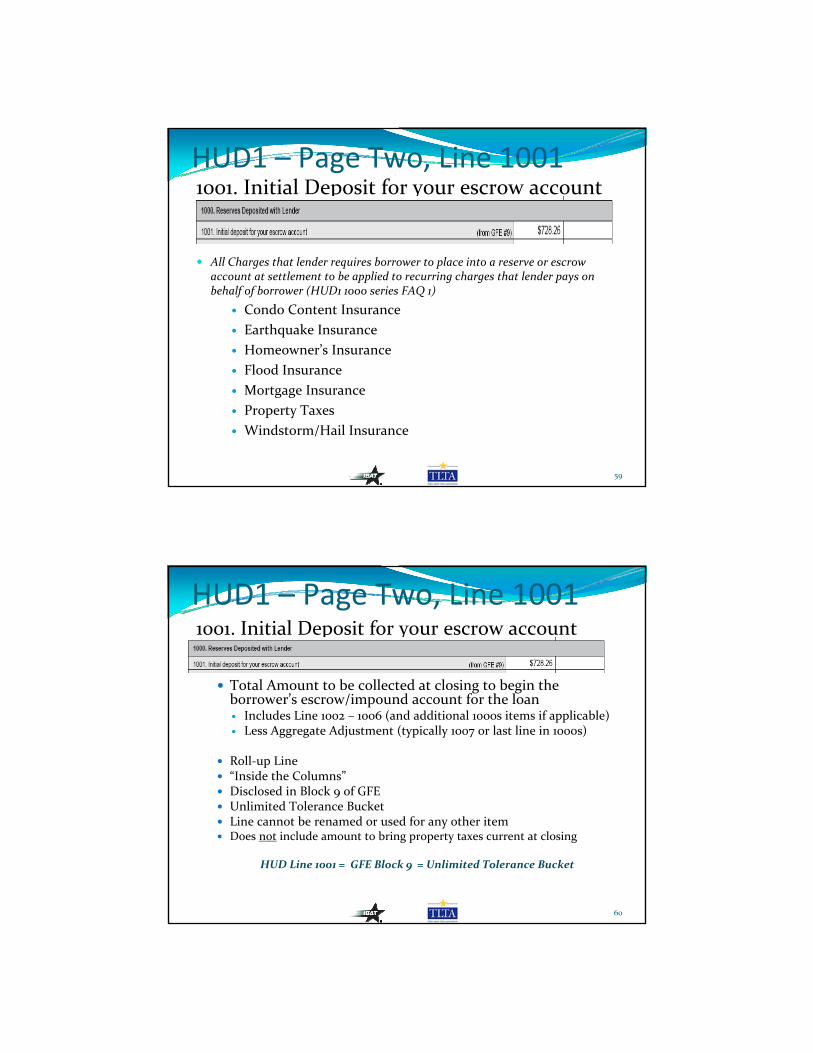

HUD1 – Page Two, Line 1002 ‐ 1006

61

HUD1 – Page Two, Line 1002 ‐ 1006Individual Escrow Line Items to be collected at closing to begin the borrower’s escrow/impound account for the loan

1002. Homeowner’s Insurance1003. Mortgage Insurance1004. Property Taxes (itemization of individual taxes, such as city, county and school is no longer required on HUD1) (HUD‐1 – 1000 series FAQ 3)

1005. – 1006. Blank lines to be used if needed for other property insurance

Each applicable escrow item must reflectNumber of months to be collected at closingMonthly amount of escrow item (Total divided by 12)Total amount for individual escrow item to be collected at closing

“Outside the Columns”Individual lines “roll up” into Line 1001

Lines cannot be renamed or used for any other itemAdditional lines can be added if necessary, but Aggregate Adjustment line must always be last line in 1000s (HUD1 1000 series FAQ 2)

62

HUD1 – Page Two, Line 10071007. Aggregate Adjustment

63

HUD1 – Page Two, Line 10071007. Aggregate Adjustment

Amount that must be credited back to borrower from establishment of escrow account through aggregate accounting method

__________________________________________________________Individual Line Item“Outside the Columns”Shown on 1007, but must always be last line in 1000s(HUD‐1 1000 series FAQ 2)

64

HUD1 – Page Two, 1100 Series1100. Title Charges

65

HUD1 – Page Two, Line 11011101. Title services and lender’s title insurance

66

HUD1 – Page Two, Line 11011101. Title services and lender’s title insurance

All Charges for services that Title/Settlement Agent requires and Title Insurance Costs to protect the Lender (HUD‐1 – 1100 series FAQ 1 – 5 , 15 & 23)

Attorney Fee representing title companyClosing FeeCourier FeeE‐Doc FeeEscrow FeeHandling FeeLender’s Title Insurance Premium (HUD‐1 – 1100 series FAQ 7 & 10)Lender’s Title Endorsement PremiumNotary FeeSettlement FeeTax Certificate Fee on non‐purchase transactionsTexas Guaranty Fee for Lender’s Loan PolicyTitle Binder/Commitment Fee (HUD‐1 – 1100 series FAQ 14)Title Examination FeeWire Fee

67

HUD1 – Page Two, Line 11011101. Title services and lender’s title insurance

Roll‐up Line“Inside the Columns”Does include 1102 Settlement or Closing Fee and 1104 Lender’s Title Insurance PremiumDoes NOT include 1103 Owner’s Title Insurance Premium

Disclosed in Block 4 on GFE10% Tolerance Bucket – aggregate totalUnlimited Tolerance Bucket – if Borrower chooses a title/settlement agent not on the listIf Originator permits Borrower to shop for a title/settlement agent, must provide at least one option on the service provider list given to Borrower at time GFE is disclosedFees payable to title/settlement agentFees payable to third parties must be itemized “outside the columns” in 1100s

HUD Line 1101, 1102, 1104, 1100s= GFE Block 4= 10% Tolerance Bucket

68

HUD1 – Page Two, Line 11021102. Settlement or closing fee

69

HUD1 – Page Two, Line 11021102. Settlement or Closing Fee

Individual Fee Line“Borrower Responsible” Fee – typical borrower costs

“Outside the Columns”, no matter who is actually paying fee“Rolls up” into Line 1101

“Seller Responsible” Fee – typical seller cost“Inside the Columns” on 1102 in Seller column

if paid by seller and not disclosed on GFE

Reflect payable to third party, if applicable (not the Settlement Agent)

(HUD‐1 1100 series FAQ 13, 15 & 16)

70

HUD1 – Page Two, Line 11031103. Owner’s Title Insurance

All Charges for Title Insurance to protect the BorrowerOwner’s Title Insurance PremiumOwner’s Title Endorsement PremiumTexas Guaranty Fee for Owner’s Policy

Owner’s Title Policy Premium must be disclosed on GFE on purchase transactions. If there is a charge for Owner’s Title Insurance Premium at closing, it must be collected from Borrower regardless of who has agreed to pay. If agreed to be paid by seller or other party, a credit will be reflected on HUD1 Page 1.

71

HUD1 – Page Two, Line 11031103. Owner’s Title Insurance

Individual Fee Lines (HUD‐1 1100 series FAQ 12)

“Inside the Columns”Lines cannot be renamed or used for any other item

Disclosed in Block 5 on GFE10% Tolerance Bucket – aggregate totalUnlimited Tolerance Bucket – if Borrower chooses a title/settlement agent not on the listIf Originator permits Borrower to shop for a title/settlement agent, must provide at least one option on the service provider list given to Borrower at time GFE is disclosedFees payable to third party other than Title/Settlement Agent

HUD Line 1103 = GFE Block 5 = 10% Tolerance Bucket

72

HUD1 – Page Two, Line 11041104. Lender’s Title Insurance

73

HUD1 – Page Two, Line 11041104. Lender’s Title Insurance

All Charges for Title Insurance Costs to protect the LenderLender’s Title Insurance PremiumLender’s Title Endorsement PremiumTexas Guaranty Fee for Lender’s Policy

Please note: RESPA does not require itemization of endorsements

74

HUD1 – Page Two, Line 11041104. Lender’s Title Insurance

Individual Fee Lines“Rolls up” into Line 1101 (HUD‐1 1100 series FAQ 7, 10 & 21)

“Outside the Columns”Lines cannot be renamed or used for any other item

Disclosed in Block 4 on GFEIf Originator permits Borrower to shop for a title/settlement agent, must provide at least one option on the service provider list given to Borrower at time GFE is disclosedFees payable to third party other than Title/Settlement Agent

HUD Line 1101 = GFE Block 4 = 10% Tolerance Bucket

75

HUD1 – Page Two, Line 1105, 1106Title Policy Limits

76

HUD1 – Page Two, Line 1105, 11061105. Lender’s Title Policy Limit (HUD‐1 1100 series FAQ 6)

Loan AmountIf negative amortization loan, maximum loan amountIf reverse mortgage loan, maximum claim amount

1106. Owner’s Title Policy LimitPurchase Price

Individual Line Items (not a fee)“Outside the Columns”Lines cannot be renamed or used for any other item

77

HUD1 – Page Two, Line 1107, 1108Agent and Underwriter portion of Title Insurance Premium

78

HUD1 – Page Two, Line 1107, 11081107. Agent’s portion of the total title insurance premium1108. Underwriter’s portion of the total title insurance premium (HUD‐1 ‐1100 series FAQ 8, 9, 19 , 20 & 22)

Individual Line Items“Outside the Columns”Lines cannot be renamed or used for any other itemPayable to appropriate partyTotal of 1107 and 1108 is equal to

Owner’s title premium, Line 1103, minus $5.00 TX Guaranty FeeLender’s title premium, Line 1104

HUD Line 1107 + 1108 = HUD Line 1103 ‐ $5.00 TX Guaranty Fee + HUD Line 1104

79

HUD1 – Page Two, Line 1109 ‐ 1199Blank lines for additional fees in 1100 series

80

HUD1 – Page Two, Line 1109 ‐ 1199Blank lines for additional fees in 1100 series

Any Charges for title or settlement related services that do not have a specific line item

Attorney Fees for Seller representationAttorney Fees for Borrower representation (HUD‐1 – 1100 series FAQ 11)

___________________________________________Individual Fee Lines“Inside the Columns” if not part of Line 1101Payable to the appropriate service providerAdditional lines can be added if necessary by separate pageNot Disclosed on GFE, if not required by Lender or Title as a part of the loan or settlement transaction

81

HUD1 – Page Two, Line 1109 ‐1199Blank lines for additional fees in 1100 series

ITEMIZATION IS ALLOWED “OUTSIDE THE COLUMNS”(HUD‐1 800 series FAQ 17 & 18)

Individual Fee Lines“Outside the Columns” if part of Title services and Lender’s Title Insurance disclosed in GFE Block 4 and rolled up into Line 1101, if

Payable to third partyRequired by state law

Fees rolled up into 1101 must not be reflected “inside the columns”Payable to appropriate party

HUD Line 1101 = GFE Block 1 = 0% Tolerance Bucket

82

TDI Requirements & Audit Guidelines700 Series – TDI Bulletin 160 requires settlement agent to itemize “outsideof column” names of any third parties who will receive a portion of the realestate commission from settlement.

Line 1107 – TDI Audit Guidelines require settlement agent to itemize“outside of column” on an additional line any amount of title insurance premiumbeing paid to a third party for “title examination” or “closing the transaction” andamount should be subtracted from amount shown in Line 1107.(HUD‐1 – 1100 series FAQ #22)

HUD1 – Page Two, 1200 series1200. Government Recording and Transfer Charges

84

HUD1 – Page Two, Line 12011201. Government recording charges

85

HUD1 – Page Two, Line 12011201. Government Recording Charges (HUD‐1 – 1200 series FAQ 1 & 2)

All Charges for recording loan and title documents upon settlement that are normal borrower costs

Assignment Recording FeeCounty Recording FeeDeed Recording FeeGovernment RecordingDeed of Trust/Mortgage/Security Instrument Recording FeePower of Attorney Recording FeeRelease Recording FeeState Recording Fee

86

HUD1 – Page Two, Line 12011201. Government recording charges

Roll‐up Line“Inside the Columns”Does include 1202 Itemized Document Recording Fees

Disclosed in Block 7 on GFE10% Tolerance Bucket – aggregate totalFees payable to title company or government agencyAdditional specific recording fees may be itemized “outside the columns” in 1200s

HUD Line 1201 = GFE Block 7= 10% Tolerance Bucket87

HUD1 – Page Two, Line 12021202. Deed/Mortgage/Release recording charges

88

HUD1 – Page Two, Line 12021202. Deed/Mortgage/Release recording charges

Itemized Charges for recording specific documents uponsettlement

Deed Recording Fee*Deed of Trust/Mortgage/Security Instrument Recording FeeRelease Recording Fee*

*Deed and Release Recording Fees, if seller responsibleFees and are not required to be disclosed on the GFE(HUD‐1 – 1200 series FAQ 5)

89

HUD1 – Page Two, Line 12021202. Deed/Mortgage/Release recording charges

Individual Fee Line“Borrower Responsible” Fee – typical borrower costs

“Outside the Columns”, no matter who is actually paying fee“Rolls up” into Line 1201

“Seller Responsible” Fee – typical seller cost“Inside the Columns” on 1202 in Seller column

if paid by seller and not disclosed on GFE(HUD‐1 – 1200 series FAQ 5)

90

HUD1 – Page Two, Line 12031203. Transfer Taxes

Roll‐up Line“Inside the Columns”Does include 1205 Itemized Document Tax/Stamps

Disclosed in Block 8 on GFE0% Tolerance BucketFees payable to government agency or departmentAdditional specific state/transfer fees/taxes may be itemized “outside the columns” in 1200s

HUD Line 1203 = GFE Block 8= 0% Tolerance Bucket

91

HUD1 – Page Two, Line 1204, 12051204. City/County tax/stamps1205. State tax/stamps

Itemized Charges for recording specific documents upon settlement

Deed Tax/Stamp*Deed of Trust/Mortgage/Security Instrument Tax/Stamp

*Deed tax/stamp, if seller responsible fees and are not required tobe disclosed on the GFE(HUD‐1 – 1200 series FAQ 6)

92

HUD1 – Page Two, Line 1204,12051204. City/County tax/stamps1205. State tax/stamps

Individual Fee Line“Borrower Responsible” Fee – typical borrower costs

“Outside the Columns”, no matter who is actually paying fee“Rolls up” into Line 1203

“Seller Responsible” Fee – typical seller cost“Inside the Columns” on 1203 in Seller column

if paid by seller and not disclosed on GFE(HUD‐1 – 1200 series FAQ 6)

93

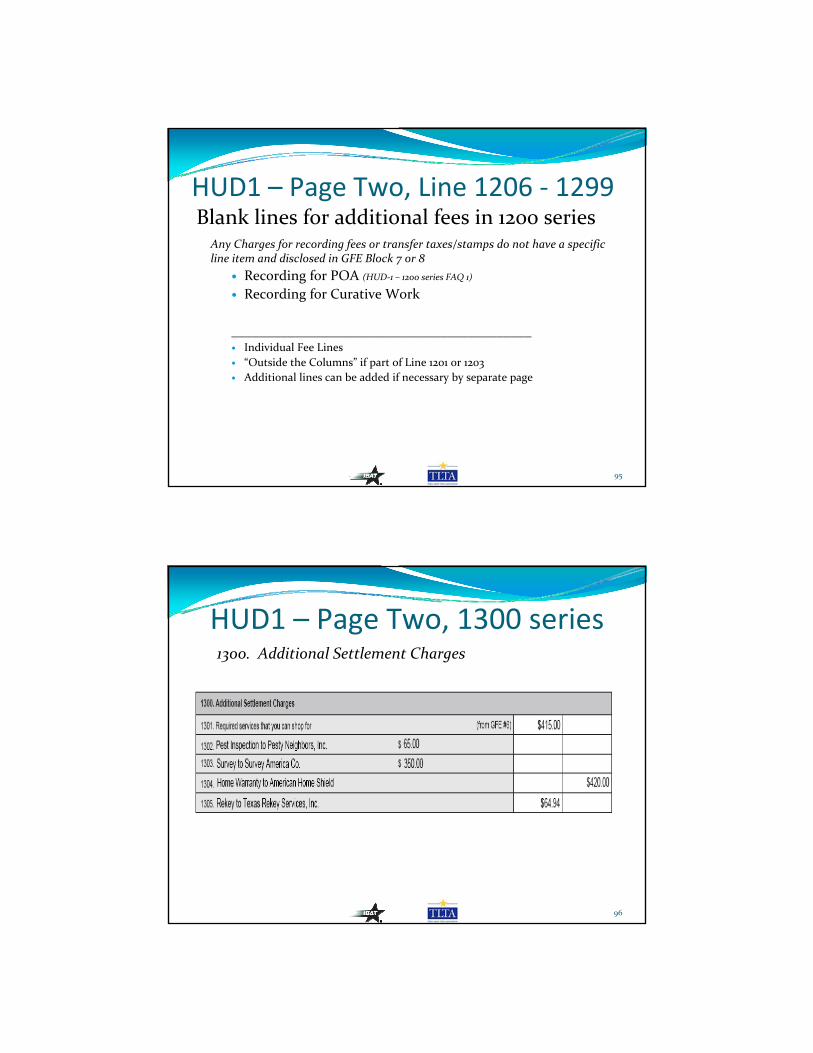

HUD1 – Page Two, Line 1206 ‐ 1299Blank lines for additional fees in 1200 series

94

HUD1 – Page Two, Line 1206 ‐ 1299Blank lines for additional fees in 1200 series

Any Charges for recording fees or transfer taxes/stamps do not have a specific line item and disclosed in GFE Block 7 or 8

Recording for POA (HUD‐1 – 1200 series FAQ 1)

Recording for Curative Work

___________________________________________Individual Fee Lines“Outside the Columns” if part of Line 1201 or 1203Additional lines can be added if necessary by separate page

95

HUD1 – Page Two, 1300 series1300. Additional Settlement Charges

96

HUD1 – Page Two, Line 13011301. Required Services that You can shop for(HUD‐1 – 1300 series FAQ 1, 2 & 4)

All Charges for services that Originator requires but that Borrower can chose the service provider (except title services and title insurance)

Pest InspectionSurvey

97

HUD1 – Page Two, Line 13011301. Required Services that You can shop for

Roll‐up Line“Inside the Columns”Does include Itemized Required Services disclosed “outside the columns”in Lines 1302, 1303 and 1300s

Disclosed in Block 6 on GFE10% Tolerance Bucket – aggregate totalUnlimited Tolerance Bucket – if Borrower chooses a title/settlement agent not on the listIf Originator permits Borrower to shop for a service provider, must provide at least one option on the service provider list given to Borrower at time GFE is disclosedFees payable to service provider

HUD Line 1301 = GFE Block 6= 10% Tolerance Bucket

98

HUD1 – Page Two, Line 1302, 13031302, 1303 – Blank lines for Required Services that You can shop for

Itemization of each Charge for services that Originator requires but that Borrower can chose the service provider(HUD‐1 – 1300 series FAQ 3)

Pest InspectionSurvey

99

HUD1 – Page Two, Line 1302, 13031302, 1303 – Blank Lines for Required Servicesthat You can shop for

Individual Fee Line“Borrower Responsible” Fee – typical borrower costs

“Outside the Columns”, no matter who is actually paying fee“Rolls up” into Line 1301

“Seller Responsible” Fee – typical seller cost“Inside the Columns” on 1302 & 1303 in Seller column

if paid by seller and not disclosed on GFE

100

HUD1 – Page Two, Line 1304‐1399Blank lines for additional fees in 1300 series

101

HUD1 – Page Two, Line 1304‐1399Blank lines for additional fees in 1300 series

Any Charges for additional fees that are not included in a specific category and were not required to be disclosed on GFE (HUD‐1 – 1300 series FAQ 1 & 5)

Home Warranty FeeHOA Transfer FeePre‐sale Inspections________________________________________________________

Individual Fee Lines“Inside the Columns” if not part of Line 1301Payable to the appropriate service providerAdditional lines can be added if necessary by separate pageNot Disclosed on GFE, if not required by Lender or Title as a part of the loan or settlement transaction

102

HUD1 – Page Two, Line 14001400. Total Settlement Charges

Total of all fees in Borrower’s columnAmount is carried forward to HUD1 Page 1 Line 103

Total of all fees in Seller’s columnAmount is carried forward to HUD1 Page 1 Line 502

103

HUD1 Roll‐up LinesROLL‐UP FEE

HUD LINE NUMBER(INSIDE COLUMN)

INDIVIDUAL FEES THAT ROLL‐UP

(OUTSIDE COLUMN)

703 701, 702

801 808 – 899 feesoutside column

1001 1001 ‐ 1099

1101 1102, 1104,1109 – 1199 feesoutside column

1201 1202,1206 – 1299 recording fees

outside column

1203 1204, 12051206 – 1299 transfer taxes

outside column

1301 1302, 13031304 – 1399

outside column104

HUD1, Page ThreeComparison Charts =Tolerance Buckets

105

HUD1, Page ThreeComparison Charts =Tolerance Buckets

Estimated Feesdisclosed at application on GFE Page 2

vs.Actual Fees

collected at closing on HUD1 Page 2

(HUD‐1 – Page 3 FAQ 3 , 4, 8 & 14)

106

HUD1 – Page ThreeCharges that Cannot Increase

O% Tolerance‐ Estimated Fees disclosed on GFE cannot increase at settlement on

HUD1

‐ Origination Fees (GFE 1/801)‐ Credit/Charge (GFE 2/802)‐ Adjusted Origination (GFE A/803)‐ Transfer Taxes (GFE 8/1203)

‐ Individual Block tolerance, not an aggregate total (Section 4 and 5 –Right to cure and tolerance violations FAQ 10)

‐ Dollar for Dollar Cure required if tolerance violation and must be reflected on HUD1

‐ Must be done at closing or no more than 30 calendar days after closing

HUD1 – Page ThreeCharges that Cannot Increase

O% Tolerance

HUD1 – Page ThreeCharges That in Total Cannot Increase More Than 10%

1O% Tolerance‐ Total of Estimated Fees disclosed on GFE cannot increase at

settlement on HUD1 more than 10% (HUD‐1 – Page 3 FAQ 2 & 8 )

‐ Required Services that Lender selects (GFE 3/804, 805, 806, 800s)‐ Title Services (GFE 4/1101)‐ Owner’s Title Policy (GFE 5/1103)‐ Required Services that Borrower can shop for (GFE 6/1301)‐ Recording Fees (GFE 7/1201)

‐ Aggregate Total‐ Individual Line Items must be reflected‐ Cure required if tolerance violation only for amount over 10%‐ Cure must be reflected on HUD1‐ Must be done at closing or no more than 30 calendar days after closing

HUD1 – Page ThreeCharges That in Total Cannot Increase More Than 10%

10% Tolerance

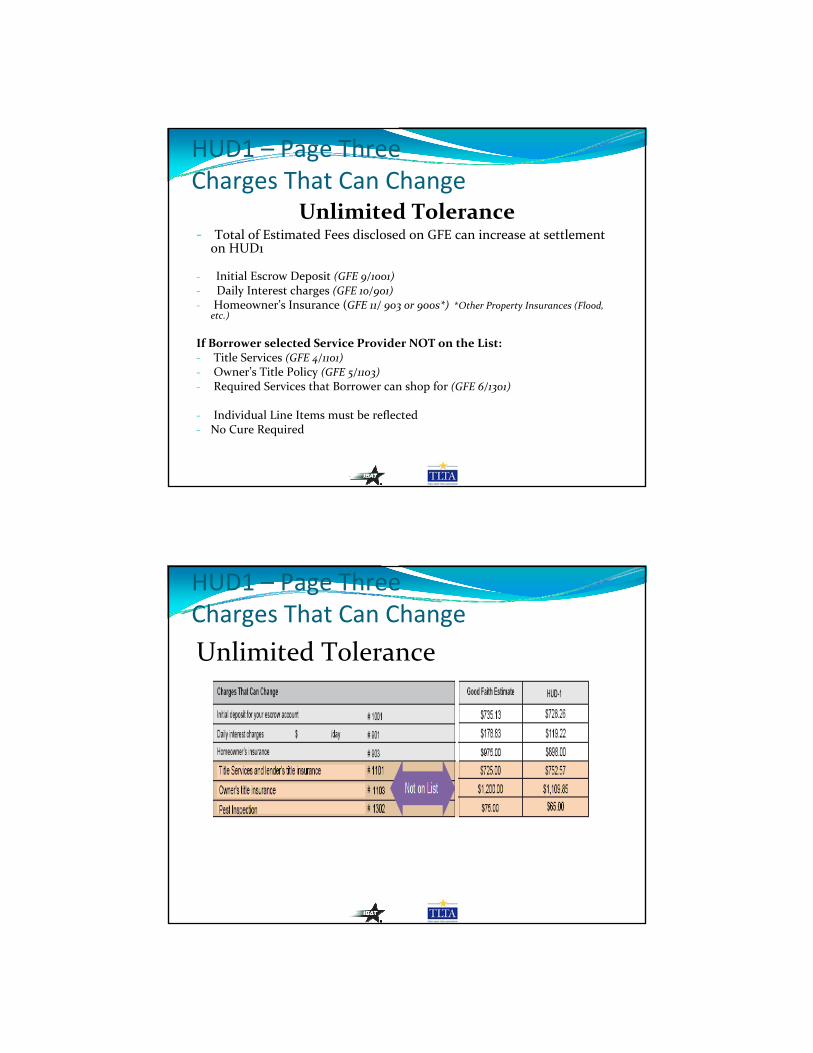

HUD1 – Page ThreeCharges That Can Change

Unlimited Tolerance‐ Total of Estimated Fees disclosed on GFE can increase at settlement

on HUD1

‐ Initial Escrow Deposit (GFE 9/1001)‐ Daily Interest charges (GFE 10/901)‐ Homeowner’s Insurance (GFE 11/ 903 or 900s*) *Other Property Insurances (Flood,

etc.)

If Borrower selected Service Provider NOT on the List:‐ Title Services (GFE 4/1101)‐ Owner’s Title Policy (GFE 5/1103)‐ Required Services that Borrower can shop for (GFE 6/1301)

‐ Individual Line Items must be reflected ‐ No Cure Required

HUD1 – Page ThreeCharges That Can Change

Unlimited Tolerance

Service Provider ListIf Borrower chooses a Service Provider

On the List ‐ 10% Tolerance Bucket – aggregate totalNOT on the List – Unlimited Bucket

If List not provided or no provider listed for services in Block 4, 5 or 6

Subject to 10% Tolerance Bucket – aggregate totalOriginator does not get benefit of Unlimited Bucket if they have not allowed Borrower to shop for services

Provider must beQualified service provider or Originator can rejectAble to provide service in Borrower’s area

113

The Bucket ListGFE BLOCK NUMBER HUD LINE NUMBER

or HUD SERIESTOLERANCE BUCKET

Block 1 801 0%

Block 2 802 0%

Block A 803 0%

Block 3 804, 805, 806, 807, 800s902, 900s

10%

Block 4* 1101, 1102, 1104, 1100s 10%

Block 5* 1103 10%

Block 6* 1301, 1300s 10%

Block 7 1201, 1202, 1200s 10%

Block 8 1203, 1204, 1205, 1200s 10%

Block 9 1001 Unlimited

Block 10 901 Unlimited

Block 11 903, 900s Unlimited*If provider not on the List *Unlimited

114

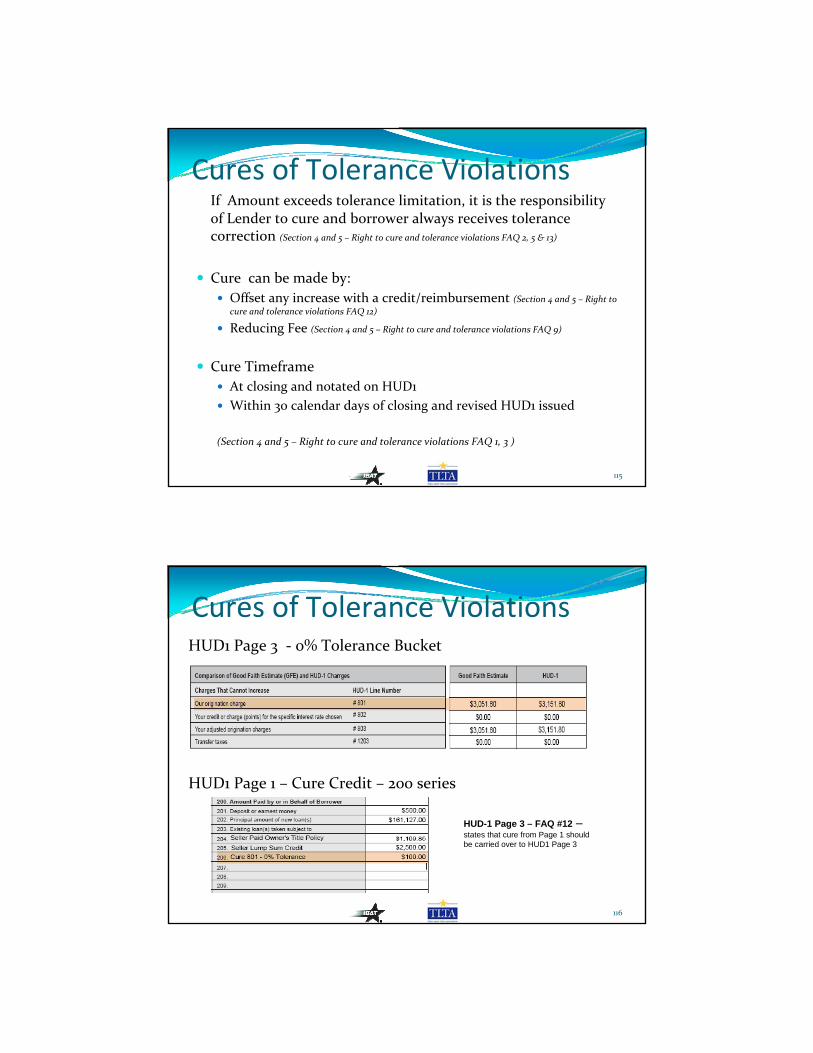

Cures of Tolerance ViolationsIf Amount exceeds tolerance limitation, it is the responsibility of Lender to cure and borrower always receives tolerance correction (Section 4 and 5 – Right to cure and tolerance violations FAQ 2, 5 & 13)

Cure can be made by:Offset any increase with a credit/reimbursement (Section 4 and 5 – Right to cure and tolerance violations FAQ 12)

Reducing Fee (Section 4 and 5 – Right to cure and tolerance violations FAQ 9)

Cure TimeframeAt closing and notated on HUD1Within 30 calendar days of closing and revised HUD1 issued

(Section 4 and 5 – Right to cure and tolerance violations FAQ 1, 3 )

115

Cures of Tolerance ViolationsHUD1 Page 3 ‐ 0% Tolerance Bucket

HUD1 Page 1 – Cure Credit – 200 series

116

HUD-1 Page 3 – FAQ #12 –states that cure from Page 1 should be carried over to HUD1 Page 3

Cures of Tolerance ViolationsHUD1 Page 3 ‐ 10% Tolerance Bucket

HUD1 Page 1 – Cure Credit – 200 series

117

HUD-1 Page 3 – FAQ #12 –states that cure from Page 1 should be carried over to HUD1 Page 3

HUD1 – Page Three, Loan Terms

118

HUD1 – Page Three, Loan TermsLender must provide this information in a format that permits theSettlement Agent to simply enter the necessary information in theappropriate spaces, without the Settlement Agent having to refer to

loan documents. (HUD‐1 – Page 3 FAQ 1 & 13)

Suggestions:1. Provide Sample or Pro forma HUD12. Provide an Addendum to Closing Instructions with this specific loan term information in similar format

HUD1 Page 3 does not need to be given to the Seller. (HUD1

General FAQ 4 & HUD‐1 – Page 3 FAQ 7)

119

HUD1 – Page Three, Loan Terms

120

HUD1 – Page Three, Loan Terms

121

HUD1 – Page Three, Loan Terms

122

HUD1 – Important Things to KnowTo properly complete the HUD1, Lender and Settlement Agent must know the following:

Is the fee a “borrower responsible” or “seller responsible” fee?

Was the fee disclosed on the GFE?

What Block Number was fee disclosed in on GFE?

What was the estimated amount of fee disclosed on GFE?

Did Lender fail to disclose on GFE as required?

123

HUD1 – Important Things to KnowTo properly complete the HUD1, Lender and Settlement Agent must know the following:

What Line Number should fee be disclosed in on HUD1?

What is the actual amount of fee to be collected/disclosed on HUD1?

Is it an individual line item fee or is it a part of a roll‐up line item fee?

Did the Borrower choose a Service Provider NOT on the List?

124

HUD1 – Important Things to KnowCannot change any Line Item label

Two loans – Two HUD1s

Old GFE – Old HUD1, New GFE – New HUD1

Settlement Agent does not have to stop closing if tolerance is violated; however, it is recommended that any violation be curedat closing.

Lender cannot pressure Settlement Agent or any Service Provider to reduce their charges to “cover the difference” in order to bring costs into compliance with tolerance limitations (RESPA Section 8a) (Section 4 and 5 – Right to cure and tolerance violations FAQ 6)

125

HUD1 – Items that can be Added to FormDate or Signature linesAdditional Pages (HUD1‐General FAQ 5 & 10)

Additional Lines

126

HELP?

Refer to RESPA Final Rule

Refer to RESPA Frequent Asked Questions (FAQs)

www.HUD.govwww.HUD.gov/RESPA/RESPA

127

A. Settlement Statement (HUD-1)

HUD-1Previous editions are obsolete Page 1 of 3

OMB Approval No. 2502-0265

( )

B. Type of Loan

6. File Number: 7. Loan Number: 8. Mortgage Insurance Case Number:1. FHA 2. RHS 3. Conv. Unins.

4. VA 5. Conv. Ins.

C. Note: This form is furnished to give you a statement of actual settlement costs. Amounts paid to and by the settlement agent are shown. Items marked“(p.o.c.)“ were paid outside the closing; they are shown here for informational purposes and are not included in the totals.

D. Name & Address of Borrower: E. Name & Address of Seller: F. Name & Address of Lender:

G. Property Location: H. Settlement Agent: I. Settlement Date:

Place of Settlement:

The Public Reporting Burden for this collection of information is estimated at 35 minutes per response for collecting, reviewing, andreporting the data. This agency may not collect this information, and you are not required to complete this form, unless it displays acurrently valid OMB control number. No confidentiality is assured; this disclosure is mandatory. This is designed to provide the parties toa RESPA covered transaction with information during the settlement process.

J. Summary of Borrower’s Transaction K. Summary of Seller’s Transaction

100. Gross Amount Due from Borrower 400. Gross Amount Due to Seller

101. Contract sales price 401. Contract sales price

102. Personal property 402. Personal property

103. Settlement charges to borrower (line 1400) 403.

104. 404.

105. 405.

Adjustment for items paid by seller in advance Adjustments for items paid by seller in advance106. City/town taxes to 406. City/town taxes to

107. County taxes to 407. County taxes to

108. Assessments to 408. Assessments to

109. 409.

110. 410.

111. 411.

112. 412.

120. Gross Amount Due from Borrower 420. Gross Amount Due to Seller

200. Amounts Paid by or in Behalf of Borrower 500. Reductions In Amount Due to Seller201. Deposit or earnest money 501. Excess deposit (see instructions)

202. Principal amount of new loan(s) 502. Settlement charges to seller (line 1400)

203. Existing loan(s) taken subject to 503. Existing loan(s) taken subject to

204. 504. Payoff of first mortgage loan

205. 505. Payoff of second mortgage loan

206. 506.

207. 507.

208. 508.

209. 509.

Adjustments for items unpaid by seller Adjustments for items unpaid by seller210. City/town taxes to 510. City/town taxes to

211. County taxes to 511. County taxes to

212. Assessments to 512. Assessments to

213. 513.

214. 514.

215. 515.

216. 516.

217. 517.

218. 518.

219. 519.

220. Total Paid by/for Borrower 520. Total Reduction Amount Due Seller

300. Cash at Settlement from/to Borrower 600. Cash at Settlement to/from Seller301. Gross amount due from borrower (line 120) 601. Gross amount due to seller (line 420)

302. Less amounts paid by/for borrower (line 220) ( ) 602. Less reductions in amount due seller (line 520)

303. Cash From To Borrower 603. Cash To From Seller

HUD-1Previous editions are obsolete Page 2 of 3

L. Settlement Charges

700. Total Real Estate Broker Fees

Division of commission (line 700) as follows:

701. $ to

702. $ to

703. Commission paid at settlement

704.

800. Items Payable in Connection with Loan

801. Our origination charge $ (fromGFE #1)

802. Your credit or charge (points) for the specific interest rate chosen $ (fromGFE #2)

803. Your adjusted origination charges (fromGFE A)

804. Appraisal fee to (fromGFE #3)

805. Credit report to (fromGFE #3)

806. Tax service to (fromGFE #3)

807. Flood certification (fromGFE #3)

808.

900. Items Required by Lender to Be Paid in Advance

901. Daily interest charges from to @ $ /day (fromGFE #10)

902. Mortgage insurance premium for months to (fromGFE #3)

903. Homeowner’s insurance for years to (fromGFE #11)

904.

1000. Reserves Deposited with Lender

1001. Initial deposit for your escrow account (fromGFE #9)

1002. Homeowner’s insurance months @ $ per month $

1003. Mortgage insurance months @ $ per month $

1004. Property taxes months @ $ per month $

1005. months @ $ per month $

1006. months @ $ per month $

1007. Aggregate Adjustment –$

1100. Title Charges1101. Title services and lender’s title insurance (fromGFE #4)

1102. Settlement or closing fee $

1103. Owner’s title insurance (fromGFE #5)

1104. Lender’s title insurance $

1105. Lender’s title policy limit $

1106. Owner’s title policy limit $

1107. Agent’s portion of the total title insurance premium $

1108. Underwriter’s portion of the total title insurance premium $

1200. Government Recording and Transfer Charges

1201. Government recording charges (fromGFE #7)

1202. Deed $ Mortgage $ Releases $

1203. Transfer taxes (fromGFE #8)

1204. City/County tax/stamps Deed $ Mortgage $

1205. State tax/stamps Deed $ Mortgage $

1206.

1300. Additional Settlement Charges

1301. Required services that you can shop for (fromGFE #6)

1302. $

1303. $

1304.

1305.

1400. Total Settlement Charges (enter on lines 103, Section J and 502, Section K)

Paid FromBorrower’sFunds atSettlement

Paid FromSeller’sFunds atSettlement

HUD-1Previous editions are obsolete Page 3 of 3

$123456 or %

NNoottee:: If you have any questions about the Settlement Charges and Loan Terms listed on this form, please contact your lender.

Comparison of Good Faith Estimate (GFE) and HUD-1 Charges Good Faith Estimate HUD-1

Charges That Cannot Increase HUD-1 Line Number

Our origination charge # 801

Your credit or charge (points) for the specific interest rate chosen # 802

Your adjusted origination charges # 803

Transfer taxes #1203

Charges That in Total Cannot Increase More Than 10% Good Faith Estimate HUD-1

Government recording charges # 1201

#1201

#1201

#1201

#1201

#1201

#1201

#____

Total

Increase between GFE and HUD-1 Charges

Charges That Can Change Good Faith Estimate HUD-1

Initial deposit for your escrow account #1001

Daily interest charges # 901 $ 2 /day

Homeowner’s insurance # 903

#1201

#1201

#1201

Loan Terms

YYoouurr iinniittiiaall llooaann aammoouunntt iiss $

YYoouurr llooaann tteerrmm iiss years

YYoouurr iinniittiiaall iinntteerreesstt rraattee iiss %

YYoouurr iinniittiiaall mmoonntthhllyy aammoouunntt oowweedd ffoorr pprriinncciippaall,, iinntteerreesstt,, aanndd $ includes

aanndd aannyy mmoorrttggaaggee iinnssuurraannccee iiss Principal

Interest

Mortgage Insurance

CCaann yyoouurr iinntteerreesstt rraattee rriissee?? No. Yes, it can rise to a maximum of XXX%. The first change will be

on [DATEDATE] and can change again every [DATEDATE] after

[DATEDATE] . Every change date, your interest rate can increase or decrease

by XXX%. Over the life of the loan, your interest rate is guaranteed to never be

lloowweerr than XXX% or hhiigghheerr than XXX%.

EEvveenn iiff yyoouu mmaakkee ppaayymmeennttss oonn ttiimmee,, ccaann yyoouurr llooaann bbaallaannccee rriissee?? No. Yes, it can rise to a maximum of $[AMOUNT].

EEvveenn iiff yyoouu mmaakkee ppaayymmeennttss oonn ttiimmee,, ccaann yyoouurr mmoonntthhllyy No. Yes, the first increase can be on and the monthly amount

aammoouunntt oowweedd ffoorr pprriinncciippaall,, iinntteerreesstt,, aanndd mmoorrttggaaggee iinnssuurraannccee rriissee?? owed can rise to $[DATEDATE].

The maximum it can ever rise to is $[DATEDATE].

DDooeess yyoouurr llooaann hhaavvee aa pprreeppaayymmeenntt ppeennaallttyy?? No. Yes, your maximum prepayment penalty is $[AMOUNT .

DDooeess yyoouurr llooaann hhaavvee aa bbaalllloooonn ppaayymmeenntt?? No. Yes, you have a balloon payment of $[AMOUNT] due in

XXX years on [DATEDATE].

TToottaall mmoonntthhllyy aammoouunntt oowweedd iinncclluuddiinngg eessccrrooww aaccccoouunntt ppaayymmeennttss You do not have a monthly escrow payment for items, such as property

taxes and homeowner’s insurance. You must pay these items directly yourself.

You have an additional monthly escrow payment of $[AMOUNT]

that results in a total initial monthly amount owed of $[AMOUNT]. This includes

principal, interest, any mortgage insurance and any items checked below:

Property taxes Homeowner’s insurance

Flood insurance

Good Faith Estimate (GFE)

Good Faith Estimate (HUD-GFE) 1

This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us.

Purpose

Summary of your settlement charges

AYour Charges for All Other Settlement Services (See page 2.) $ BYour Adjusted Origination Charges (See page 2.) $

Summary of your loan

Important dates

Total Estimated Settlement Charges $

OMB Approval No. 2502-0265

Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find the best loan. Use the shopping chart on page 3 to compare all the offers you receive.

Shopping for your loan

Your initial loan amount is Your loan term is Your initial interest rate is Your initial monthly amount owed for principal, interest, and any mortgage insurance is

$ years % $ per month

Can your interest rate rise?

Even if you make payments on time, can your loan balance rise?Even if you make payments on time, can your monthly amount owed for principal, interest, and any mortgage insurance rise?

Does your loan have a prepayment penalty?

Does your loan have a balloon payment?

c No c Yes, it can rise to a maximum of %. The first change will be inc No c Yes, it can rise to a maximum of $

c No c Yes, the first increase can be in and the monthly amount owed can rise to $ . The maximum it can ever rise to is $ . c No c Yes, your maximum prepayment penalty is $

Some lenders require an escrow account to hold funds for paying property taxes or other property-related charges in addition to your monthly amount owed of $ . Do we require you to have an escrow account for your loan?c No, you do not have an escrow account. You must pay these charges directly when due.c Yes, you have an escrow account. It may or may not cover all of these charges. Ask us.

Escrow account information

Borrower

Property Address

Date of GFE

Name of Originator

Originator Address

Originator Phone Number

Originator Email

1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate.

2. This estimate for all other settlement charges is available through .

3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate.

4. You must lock the interest rate at least days before settlement.

A B+

c No c Yes, you have a balloon payment of $ due in years.

Understanding your estimated settlement charges

Good Faith Estimate (HUD-GFE) 2

Your Adjusted Origination Charges

Your Adjusted Origination Charges

Total Estimated Settlement ChargesA B+

3. Required services that we selectThese charges are for services we require to complete your settlement. We will choose the providers of these services.Service Charge

B Your Charges for All Other Settlement Services

9. Initial deposit for your escrow accountThis charge is held in an escrow account to pay future recurring charges on your property and includes all property taxes, all insurance, and other .

Your Charges for All Other Settlement Services

10. Daily interest chargesThis charge is for the daily interest on your loan from the day of your settlement until the fi rst day of the next month or the fi rst day of your normal mortgage payment cycle. This amount is $ per day for days (if your settlement is ).

A

1. Our origination charge This charge is for getting this loan for you. 2. Your credit or charge (points) for the specifi c interest rate chosen c The credit or charge for the interest rate of % is included in

“Our origination charge.” (See item 1 above.) c You receive a credit of $ for this interest rate of %. This credit reduces your settlement charges. c You pay a charge of $ for this interest rate of %. This charge (points) increases your total settlement charges. The tradeoff table on page 3 shows that you can change your total settlement charges by choosing a different interest rate for this loan.

11. Homeowner’s insurance This charge is for the insurance you must buy for the property to protect from a loss, such as fi re.

Policy Charge

Some of these charges can change at settlement. See the top of page 3 for more information.

4. Title services and lender’s title insuranceThis charge includes the services of a title or settlement agent, for example, and title insurance to protect the lender, if required.

5. Owner’s title insurance You may purchase an owner’s title insurance policy to protect your interest in the property.6. Required services that you can shop for

These charges are for other services that are required to complete your settlement. We can identify providers of these services or you can shop for them yourself. Our estimates for providing these services are below.Service Charge

7. Government recording chargesThese charges are for state and local fees to record your loan and title documents.

8. Transfer taxesThese charges are for state and local fees on mortgages and home sales.

$

$

$

These charges cannot increase at settlement:

Our origination charge

Your credit or charge (points) for the specifi c interest rate chosen (after you lock in your interest rate)

Your adjusted origination charges (after you lock in your interest rate)

Transfer taxes

The total of these charges can increase up to 10% at settlement:

Required services that we select

Title services and lender’s title insurance (if we select them or you use companies we identify)

Owner’s title insurance (if you use companies we identify)

Required services that you can shop for (if you use companies we identify)

Government recording charges

These charges can change at settlement:

Required services that you can shop for (if you do not use companies we identify)

Title services and lender’s title insurance (if you do not use companies we identify)

Owner’s title insurance (if you do not use companies we identify)

Initial deposit for your escrow account

Daily interest charges

Homeowner’s insurance

Using the tradeoff table

Good Faith Estimate (HUD-GFE) 3

InstructionsThis GFE estimates your settlement charges. At your settlement, you will receive a HUD-1, a form that lists your actual costs. Compare the charges on the HUD-1 with the charges on this GFE. Charges can change if you select your own provider and do not use the companies we identify. (See below for details.)

Understanding which charges can change at settlement

In this GFE, we offered you this loan with a particular interest rate and estimated settlement charges. However:

• If you want to choose this same loan with lower settlement charges, then you will have a higher interest rate.• If you want to choose this same loan with a lower interest rate, then you will have higher settlement charges. If you would like to choose an available option, you must ask us for a new GFE. Loan originators have the option to complete this table. Please ask for additional information if the table is not completed.

Your initial loan amount

Your initial interest rate 1

Your initial monthly amount owed

Change in the monthly amount owed from this GFE

Change in the amount you will pay at settlement with this interest rate

How much your total estimated settlement charges will be

The loan in this GFE

You will pay $ less every month

You will pay $ more every month

The same loan with lower settlement charges

The same loan with a lower interest rate

1For an adjustable rate loan, the comparisons above are for the initial interest rate before adjustments are made.

Use this chart to compare GFEs from different loan originators. Fill in the information by using a different column for each GFE you receive. By comparing loan offers, you can shop for the best loan.

Using the shopping chart

This loan Loan 2 Loan 3 Loan 4

Loan originator name

Initial loan amount

Loan term

Initial interest rate

Initial monthly amount owed

Rate lock period

Can interest rate rise?

Can loan balance rise?

Can monthly amount owed rise?

Prepayment penalty?

Balloon payment?

Total Estimated Settlement Charges

Some lenders may sell your loan after settlement. Any fees lenders receive in the future cannot change the loan you receive or the charges you paid at settlement.

If your loan is sold in the future

Your settlement charges will increase by $

Your settlement charges will be reduced by $$$

$

$

$

$

$

$

$

No change

No change

%%%

A. Settlement Statement (HUD-1)

HUD-1Page 1 of 3Previous edition are obsolete

B. Type of Loan

J. Summary of Borrower’s Transaction

100. Gross Amount Due from Borrower

C. Note:

400. Gross Amount Due to Seller

This form is furnished to give you a statement of actual settlement costs. Amounts paid to and by the settlement agent are shown. Items marked “(p.o.c.)” were paid outside the closing; they are shown here for informational purposes and are not included in the totals.

401. Contract sales price

106. City/town taxes to

to

to

to

to

to

to

to

to

to

to

to

406. City/town taxes

203. Existing loan(s) taken subject to 503. Existing loan(s) taken subject to

212. Assessments 512. Assessments

302. Less amounts paid by/for borrower (line 220) 602. Less reductions in amounts due seller (line 520)( ) ( )

213. 513.

214. 514. 215. 515. 216. 516.

218. 518.

217. 517.

219. 519.

102. Personal property

101. Contract sales price

402. Personal property

107. County taxes 407. County taxes

204. 504. Payoff of first mortgage loan

103. Settlement charges to borrower (line 1400) 403.

108. Assessments 408. Assessments

205. 505. Payoff of second mortgage loan

104. 404.

109. 409.

206. 506.

201. Deposit or earnest money 501. Excess deposit (see instructions)

210. City/town taxes 510. City/town taxes

105.

1.

D. Name & Address of Borrower:

G. Property Location:

E. Name & Address of Seller: F. Name & Address of Lender:

I. Settlement Date:H. Settlement Agent:

Place of Settlement:

2. 3.FHA RHS Conv. Unins. 6. File Number: 7. Loan Number: 8. Mortgage Insurance Case Number:

VA Conv. Ins.4. 5.

405.

110. 410.

207. 507.

202. Principal amount of new loan(s) 502. Settlement charges to seller (line 1400)

211. County taxes 511. County taxes

301. Gross amount due from borrower (line 120) 601. Gross amount due to seller (line 420)

111. 411.

208. 508.

112. 412.

209. 509.

120. Gross Amount Due from Borrower 420. Gross Amount Due to Seller200. Amount Paid by or in Behalf of Borrower 500. Reductions In Amount Due to seller

Adjustments for items unpaid by seller Adjustments for items unpaid by seller

220. Total Paid by/for Borrower 520. Total Reduction Amount Due Seller

303. Cash 603. CashFrom ToTo Borrower From Seller

300. Cash at Settlement from/to Borrower 600. Cash at Settlement to/from Seller

Adjustment for items paid by seller in advance Adjustment for items paid by seller in advance

K. Summary of Seller’s Transaction

OMB Approval No. 2502-0265

The Public Reporting Burden for this collection of information is estimated at 35 minutes per response for collecting, reviewing, and reporting the data. This agency may not collect this information, and you are not required to complete this form, unless it displays a currently valid OMB control number. No confidentiality is assured; this disclosure is mandatory. This is designed to provide the parties to a RESPA covered transaction with information during the settlement process.

HUD-1Page 2 of 3Previous edition are obsolete

L. Settlement Charges

700. Total Real Estate Broker Fees

800. Items Payable in Connection with Loan

900. Items Required by Lender to be Paid in Advance

1000. Reserves Deposited with Lender

1100. Title Charges

1200. Government Recording and Transfer Charges

1300. Additional Settlement Charges

702. $ to

to

802. Your credit or charge (points) for the specific interest rate chosen

902. Mortgage insurance premium for months to

1002. Homeowner’s insurance months @ $ per month $

1102. Settlement or closing fee

1202. Deed $ Mortgage $ Release $

1302.

701. $

801. Our origination charge

901. Daily interest charges from to @ $ /day

1001. Initial deposit for your escrow account

1101. Title services and lender’s title insurance

1201. Government recording charges

1301. Required services that you can shop for

703. Commission paid at settlement

Division of commission (line 700) as follows :

803. Your adjusted origination charges

903. Homeowner’s insurance for years to

1003. Mortgage insurance months @ $ per month $

1103. Owner’s title insurance

1203. Transfer taxes

1303.

704.

804. Appraisal fee to

904.

1004. Property Taxes months @ $ per month $

1104. Lender’s title insurance

1204. City/County tax/stamps Deed $ Mortgage $

1304.

1005. months @ $ per month $

1105. Lender’s title policy limit $

1205. State tax/stamps Deed $ Mortgage $

1305.

1006. months @ $ per month $

1106. Owner’s title policy limit $

1206.

1007. Aggregate Adjustment -$

1107. Agent’s portion of the total title insurance premium to

1108. Underwriter’s portion of the total title insurance premium to

1109.

1110.

1111.

805. Credit report to

806. Tax service to

807. Flood certification to

808.

809.

810.

811.

Paid FromBorrower’sFunds at

Settlement

Paid FromSeller’s

Funds atSettlement

$

$

$

$

$

$

1400. Total Settlement Charges (enter on lines 103, Section J and 502, Section K)

(from GFE #1)

(from GFE #3)

(from GFE #2)

(from GFE #3)

(from GFE #10)

(from GFE #4)

(from GFE #3)

(from GFE #11)

(from GFE #9)

(from GFE #5)

(from GFE #7)

(from GFE #8)

(from GFE #6)

(from GFE #A)

(from GFE #3)

(from GFE #3)

$

$

HUD-1Page 3 of 3Previous edition are obsolete

Comparison of Good Faith Estimate (GFE) and HUD-1 Charrges

% $ or

Charges That In Total Cannot Increase More Than 10%

Good Faith Estimate

Good Faith Estimate

Good Faith Estimate

Total

Increase between GFE and HUD-1 Charges

HUD-1

HUD-1

HUD-1

Charges That Cannot Increase HUD-1 Line Number

Government recording charges

Charges That Can Change

Your initial loan amount is

Loan Terms

Note: If you have any questions about the Settlement Charges and Loan Terms listed on this form, please contact your lender.

Daily interest charges

Your initial interest rate is

Initial deposit for your escrow account

Your loan term is years

No

No

No

No

Property taxes Homeowner’s insurance

Flood insurance

No

Yes, it can rise to a maximum of %. The first change will be on

Yes, the first increase can be on and the monthly amount

Yes, it can rise to a maximum of $

Yes, your maximum prepayment penalty is $

Yes, you have a balloon payment of $ due in yearson .

You do not have a monthly escrow payment for items, such as property taxes and

You have an additional monthly escrow payment of $

that results in a total initial monthly amount owed of $ . This includes

principal, interest, any mortagage insurance and any items checked below:

homeowner’s insurance. You must pay these items directly yourself.

Principal

Interest

Mortgage Insurance

includes

%

Our origination charge

Your credit or charge (points) for the specific interest rate chosen

Your adjusted origination charges

Transfer taxes

Homeowner’s insurance

Your initial monthly amount owed for principal, interest, and any

mortgage insurance is

Can your interest rate rise?

Even if you make payments on time, can your loan balance rise?

Does your loan have a prepayment penalty?

Does your loan have a balloon payment?

Total monthly amount owed including escrow account payments

Even if you make payments on time, can your monthly

amount owed for principal, interest, and mortgage insurance rise?

$

# 1001

#

# 1201

# 901

#

# 903

#

# 801

#

#

# 802

#

#

# 803

#

#

#

# 1203