The Murray Ohio Manufacturing Company Presented by: Vincent, Shaoying, Mary, Yuting, and Feny.

36

The Murray Ohio Manufacturing Company Presented by: Vincent, Shaoying, Mary, Yuting, and Feny

-

Upload

cheyanne-cayson -

Category

Documents

-

view

222 -

download

0

Transcript of The Murray Ohio Manufacturing Company Presented by: Vincent, Shaoying, Mary, Yuting, and Feny.

The Murray Ohio Manufacturing Company

Presented by:

Vincent, Shaoying, Mary, Yuting, and Feny

Agenda

Strategy Analysis Accounting Analysis Financial Analysis Prospective Analysis Conclusion Subsequent Developments

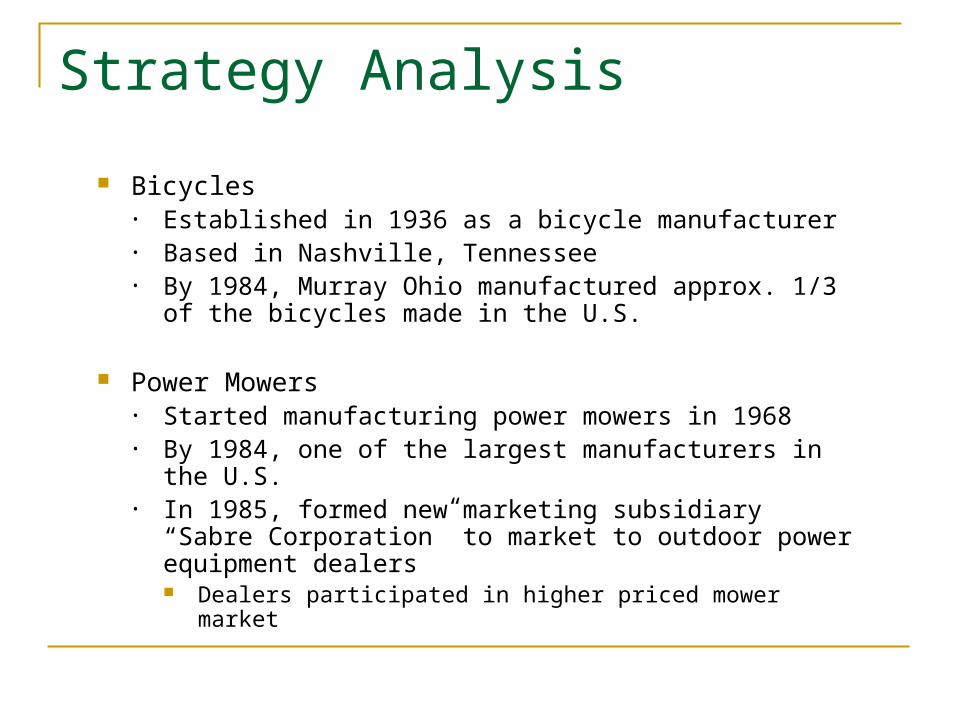

Strategy Analysis

Bicycles• Established in 1936 as a bicycle manufacturer• Based in Nashville, Tennessee• By 1984, Murray Ohio manufactured approx. 1/3 of the

bicycles made in the U.S.

Power Mowers• Started manufacturing power mowers in 1968• By 1984, one of the largest manufacturers in the U.S.• In 1985, formed new marketing subsidiary “Sabre

Corporation” to market to outdoor power equipment dealers Dealers participated in higher priced mower market

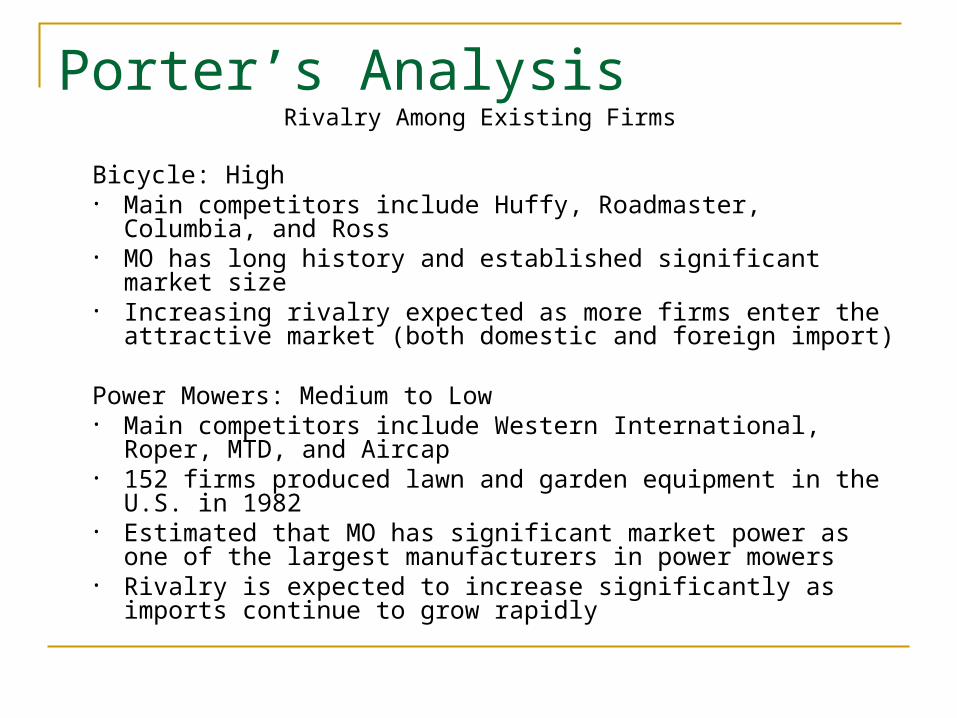

Porter’s AnalysisRivalry Among Existing Firms

Bicycle: High• Main competitors include Huffy, Roadmaster, Columbia, and

Ross • MO has long history and established significant market size• Increasing rivalry expected as more firms enter the attractive

market (both domestic and foreign import)

Power Mowers: Medium to Low • Main competitors include Western International, Roper, MTD,

and Aircap • 152 firms produced lawn and garden equipment in the U.S. in

1982• Estimated that MO has significant market power as one of the

largest manufacturers in power mowers• Rivalry is expected to increase significantly as imports continue

to grow rapidly

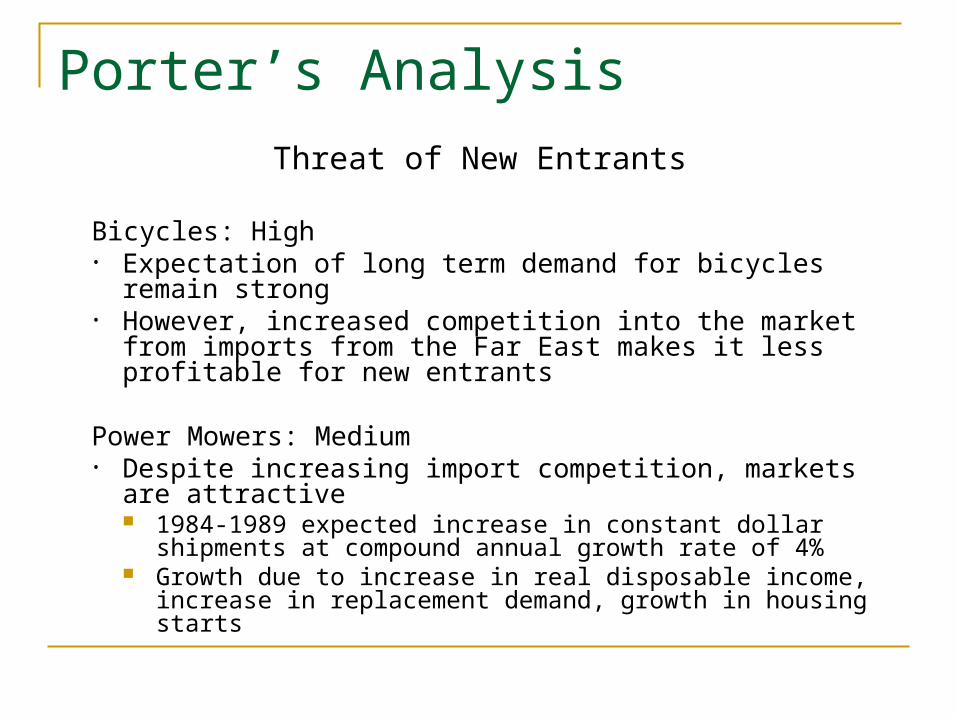

Porter’s Analysis

Threat of New Entrants

Bicycles: High• Expectation of long term demand for bicycles remain strong• However, increased competition into the market from

imports from the Far East makes it less profitable for new entrants

Power Mowers: Medium• Despite increasing import competition, markets are

attractive 1984-1989 expected increase in constant dollar shipments at

compound annual growth rate of 4% Growth due to increase in real disposable income, increase in

replacement demand, growth in housing starts

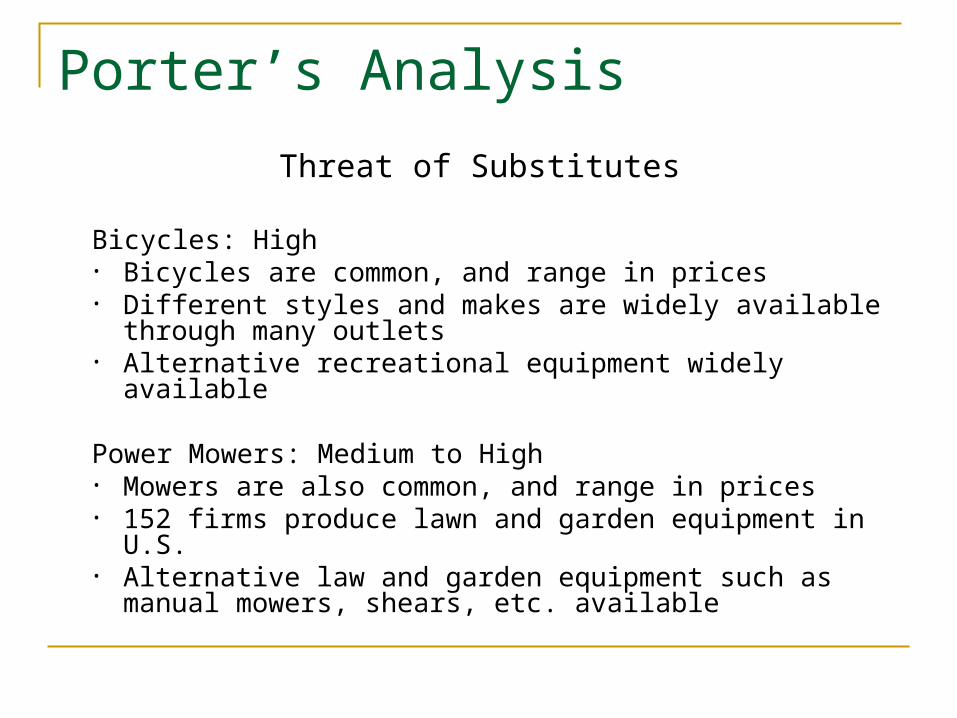

Porter’s Analysis

Threat of Substitutes

Bicycles: High• Bicycles are common, and range in prices• Different styles and makes are widely available through

many outlets• Alternative recreational equipment widely available

Power Mowers: Medium to High• Mowers are also common, and range in prices• 152 firms produce lawn and garden equipment in U.S.• Alternative law and garden equipment such as manual

mowers, shears, etc. available

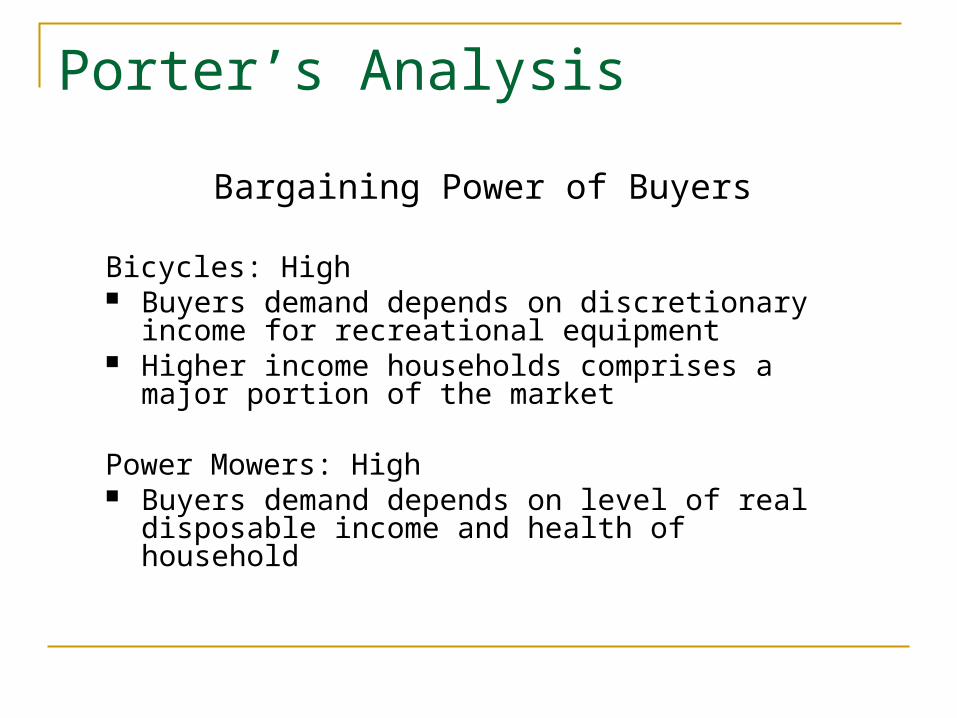

Porter’s Analysis

Bargaining Power of Buyers

Bicycles: High Buyers demand depends on discretionary income for

recreational equipment Higher income households comprises a major portion

of the market

Power Mowers: High Buyers demand depends on level of real disposable

income and health of household

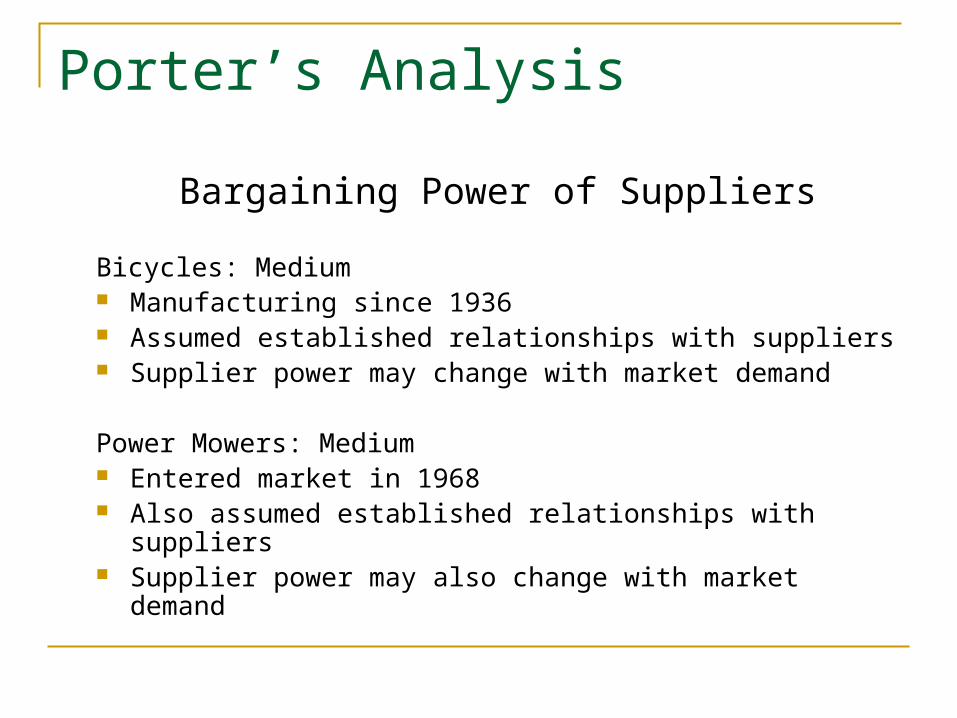

Porter’s Analysis

Bargaining Power of Suppliers

Bicycles: Medium Manufacturing since 1936 Assumed established relationships with suppliers Supplier power may change with market demand

Power Mowers: Medium Entered market in 1968 Also assumed established relationships with suppliers Supplier power may also change with market demand

Porter’s Analysis

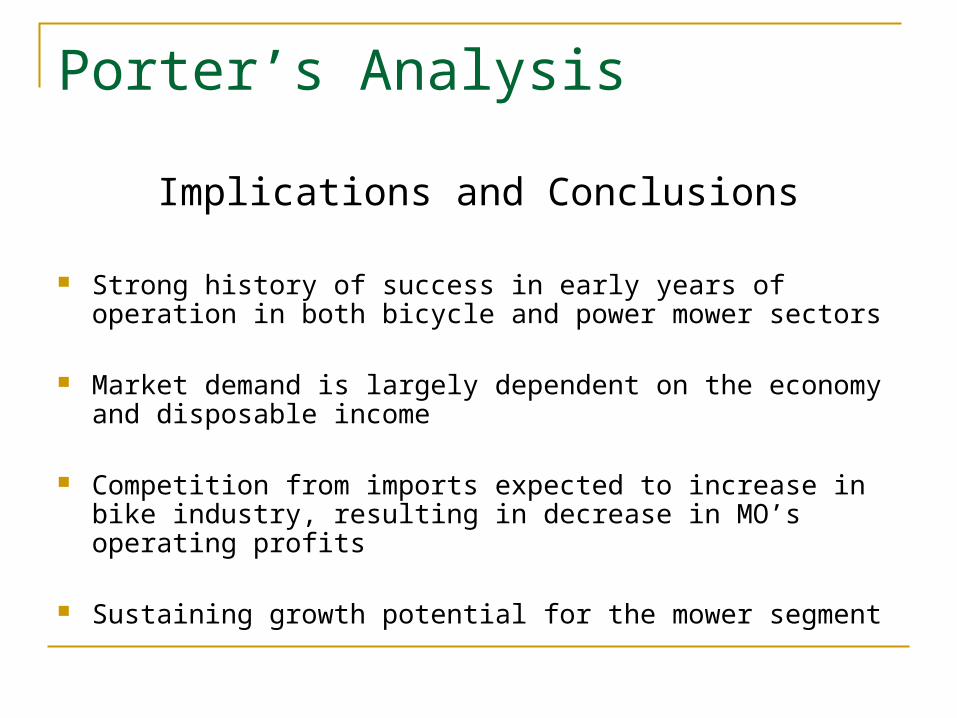

Implications and Conclusions

Strong history of success in early years of operation in both bicycle and power mower sectors

Market demand is largely dependent on the economy and disposable income

Competition from imports expected to increase in bike industry, resulting in decrease in MO’s operating profits

Sustaining growth potential for the mower segment

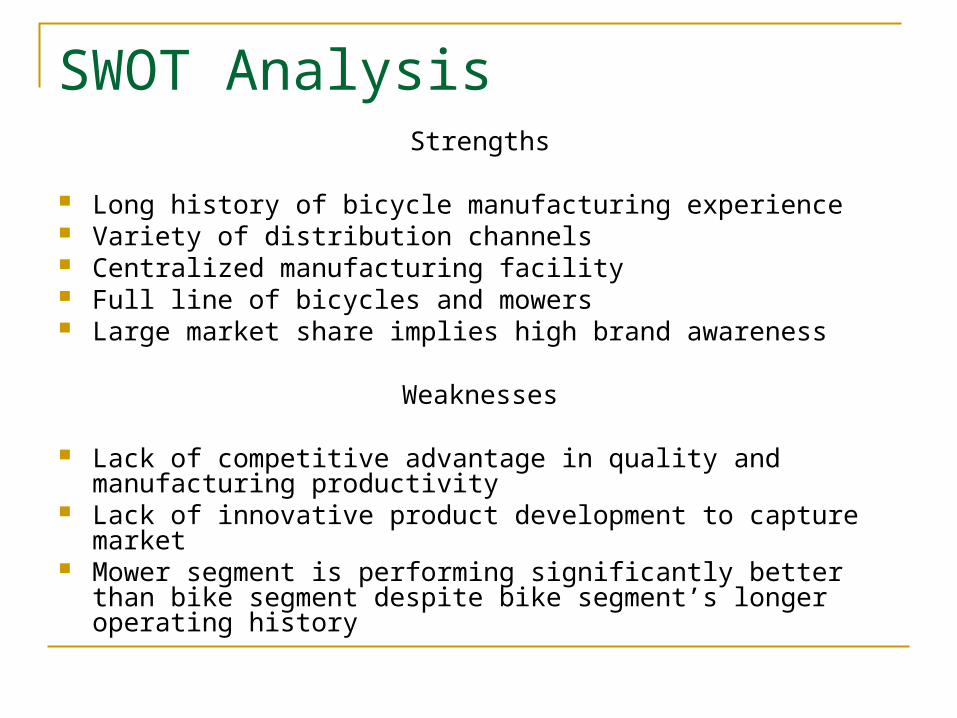

SWOT AnalysisStrengths

Long history of bicycle manufacturing experience Variety of distribution channels Centralized manufacturing facility Full line of bicycles and mowers Large market share implies high brand awareness

Weaknesses

Lack of competitive advantage in quality and manufacturing productivity

Lack of innovative product development to capture market Mower segment is performing significantly better than bike

segment despite bike segment’s longer operating history

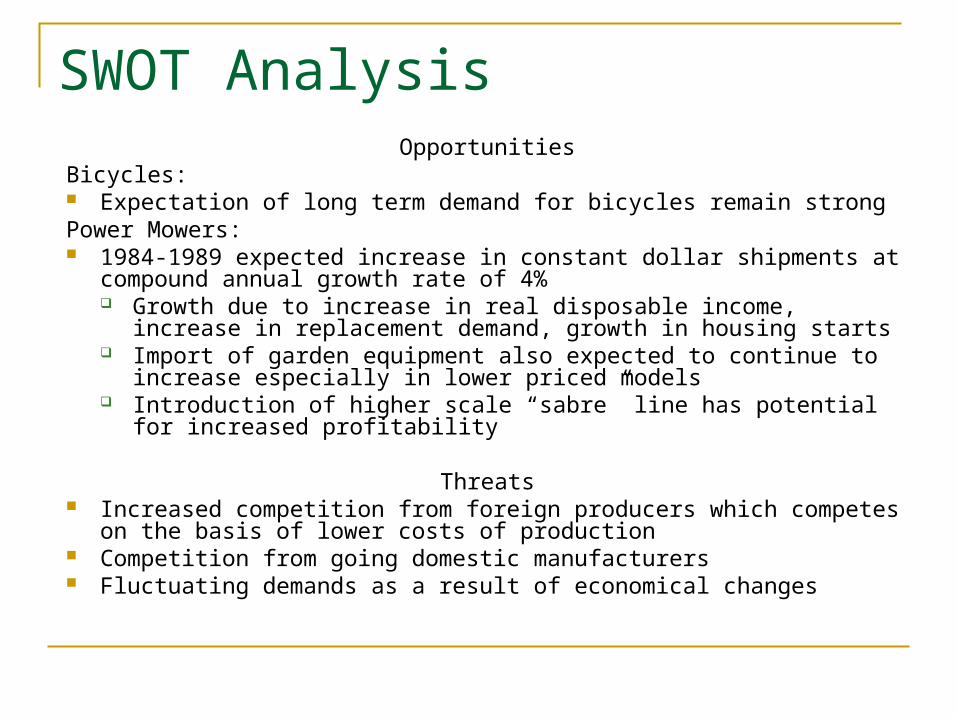

SWOT AnalysisOpportunities

Bicycles: Expectation of long term demand for bicycles remain strongPower Mowers: 1984-1989 expected increase in constant dollar shipments at compound

annual growth rate of 4% Growth due to increase in real disposable income, increase in

replacement demand, growth in housing starts Import of garden equipment also expected to continue to increase

especially in lower priced models Introduction of higher scale “sabre” line has potential for increased

profitability

Threats Increased competition from foreign producers which competes on the basis

of lower costs of production Competition from going domestic manufacturers Fluctuating demands as a result of economical changes

SWOT Analysis

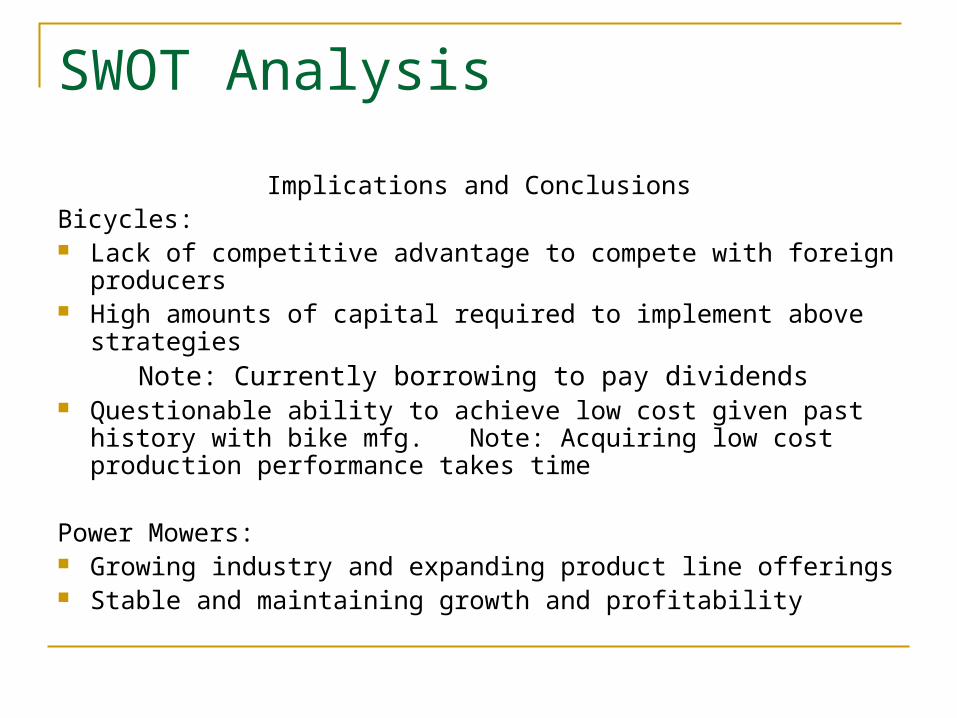

Implications and ConclusionsBicycles: Lack of competitive advantage to compete with foreign producers High amounts of capital required to implement above strategies

Note: Currently borrowing to pay dividends Questionable ability to achieve low cost given past history with

bike mfg. Note: Acquiring low cost production performance takes time

Power Mowers: Growing industry and expanding product line offerings Stable and maintaining growth and profitability

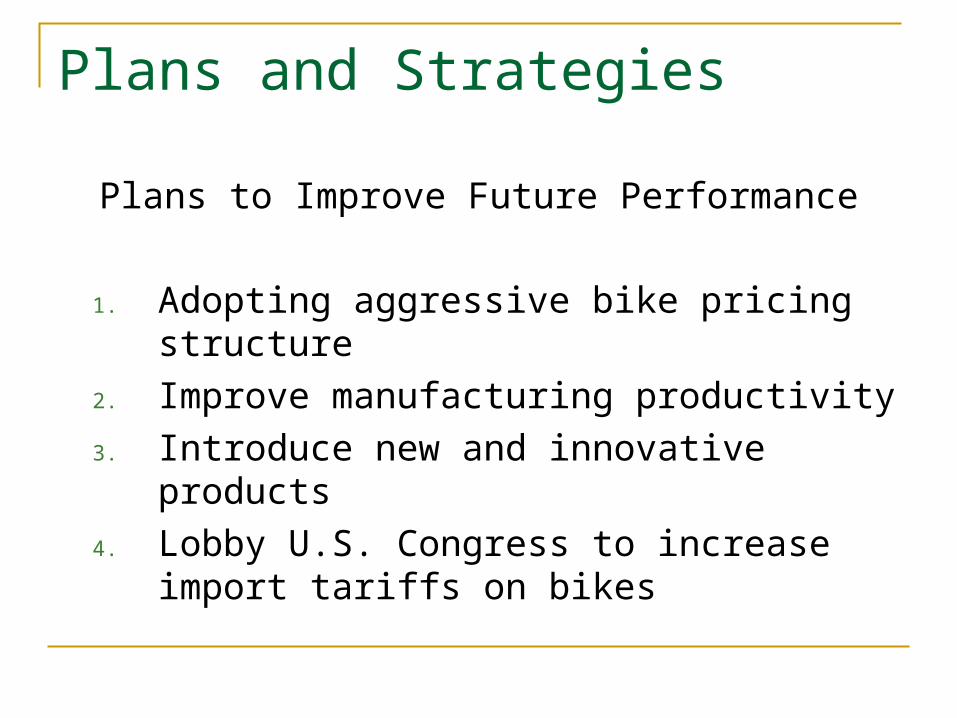

Plans and Strategies

Plans to Improve Future Performance

1. Adopting aggressive bike pricing structure

2. Improve manufacturing productivity

3. Introduce new and innovative products

4. Lobby U.S. Congress to increase import tariffs on bikes

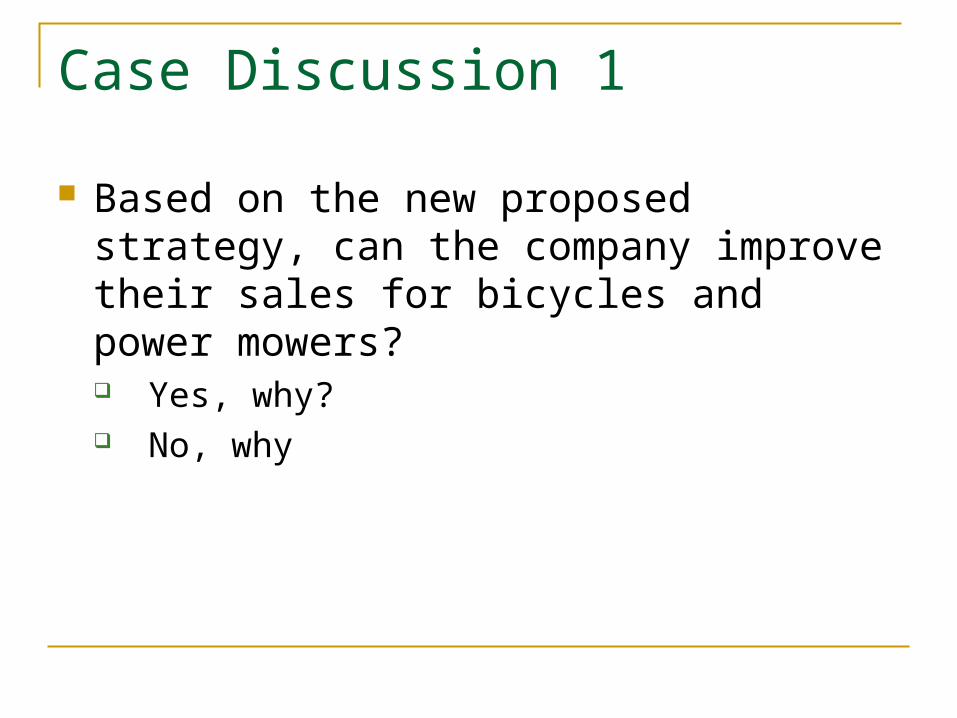

Case Discussion 1

Based on the new proposed strategy, can the company improve their sales for bicycles and power mowers? Yes, why? No, why

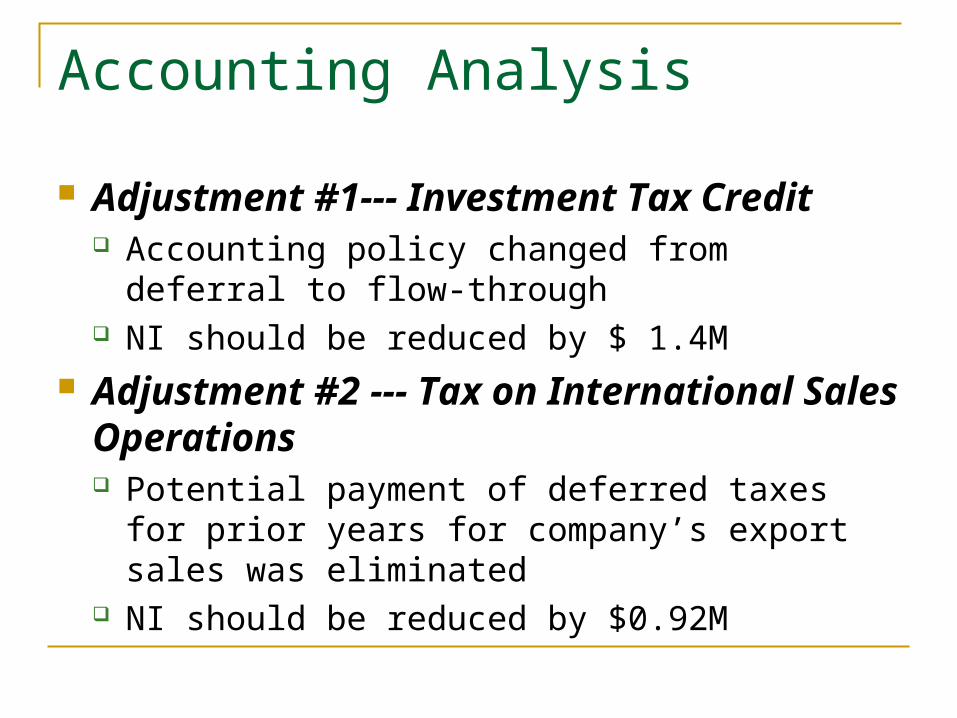

Accounting Analysis

Adjustment #1--- Investment Tax Credit Accounting policy changed from deferral to flow-

through NI should be reduced by $ 1.4M

Adjustment #2 --- Tax on International Sales Operations Potential payment of deferred taxes for prior years

for company’s export sales was eliminated NI should be reduced by $0.92M

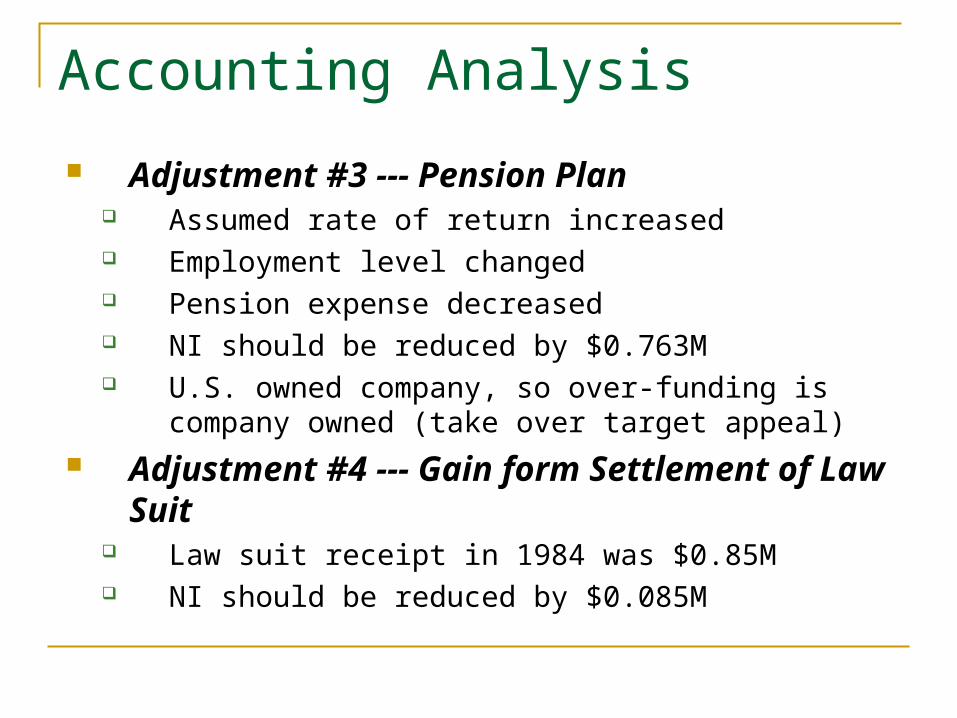

Accounting Analysis

Adjustment #3 --- Pension Plan Assumed rate of return increased Employment level changed Pension expense decreased NI should be reduced by $0.763M U.S. owned company, so over-funding is company

owned (take over target appeal) Adjustment #4 --- Gain form Settlement of Law

Suit Law suit receipt in 1984 was $0.85M NI should be reduced by $0.085M

Accounting Analysis

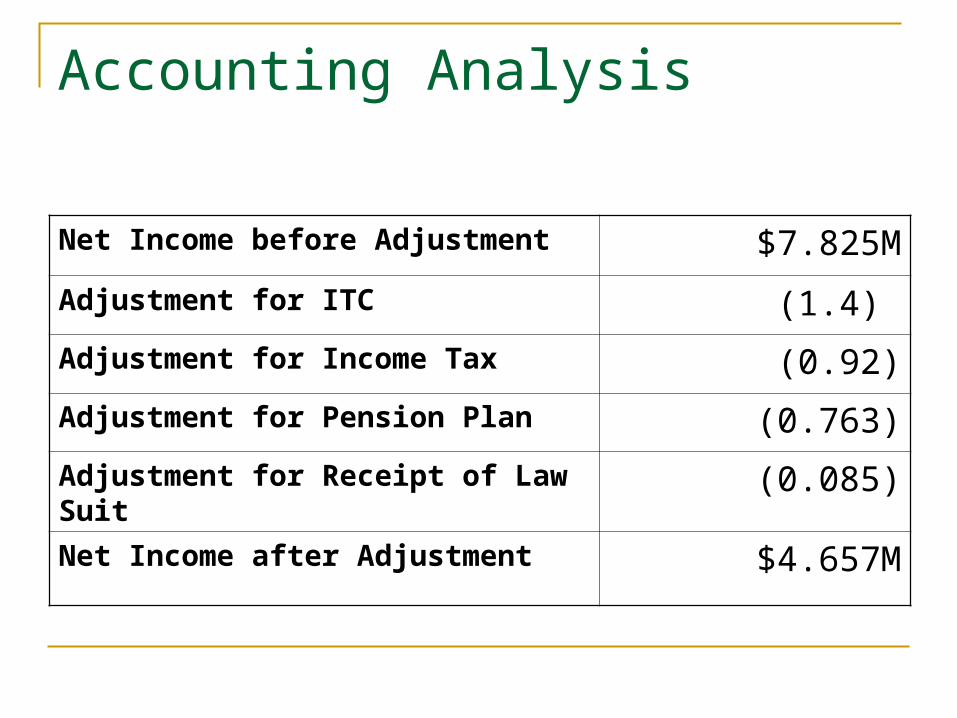

Net Income before Adjustment $7.825M

Adjustment for ITC (1.4)

Adjustment for Income Tax (0.92)

Adjustment for Pension Plan (0.763)

Adjustment for Receipt of Law Suit (0.085)

Net Income after Adjustment $4.657M

Financial Analysis - DUPONT

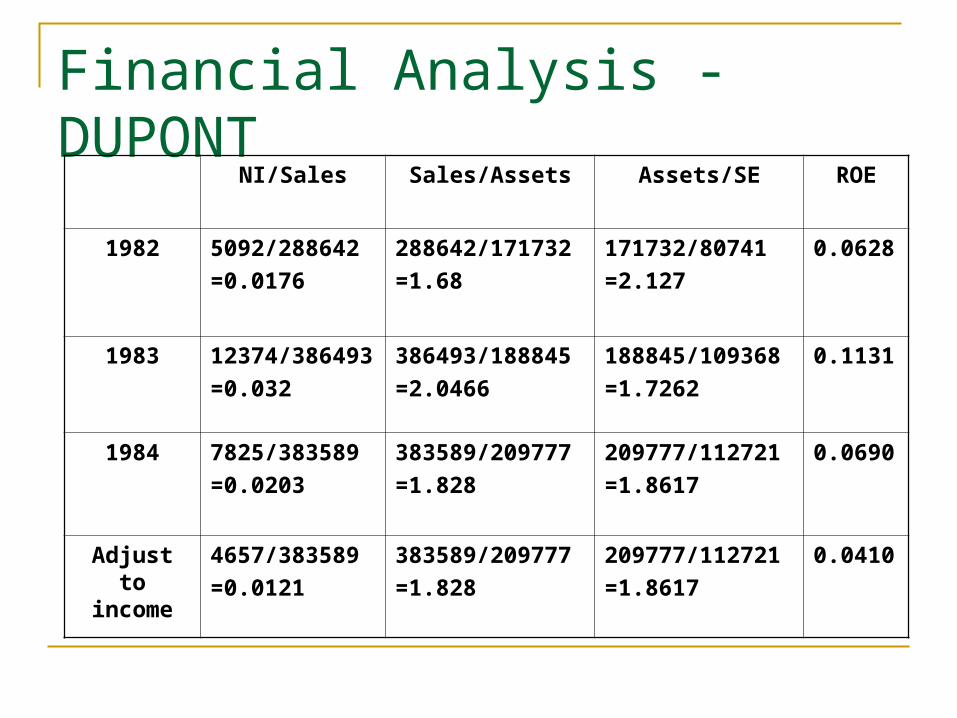

NI/Sales Sales/Assets Assets/SE ROE

1982 5092/288642

=0.0176

288642/171732

=1.68

171732/80741

=2.127

0.0628

1983 12374/386493

=0.032

386493/188845

=2.0466

188845/109368

=1.7262

0.1131

1984 7825/383589

=0.0203

383589/209777

=1.828

209777/112721

=1.8617

0.0690

Adjust to income

4657/383589

=0.0121

383589/209777

=1.828

209777/112721

=1.8617

0.0410

Financial Analysis - DUPONT

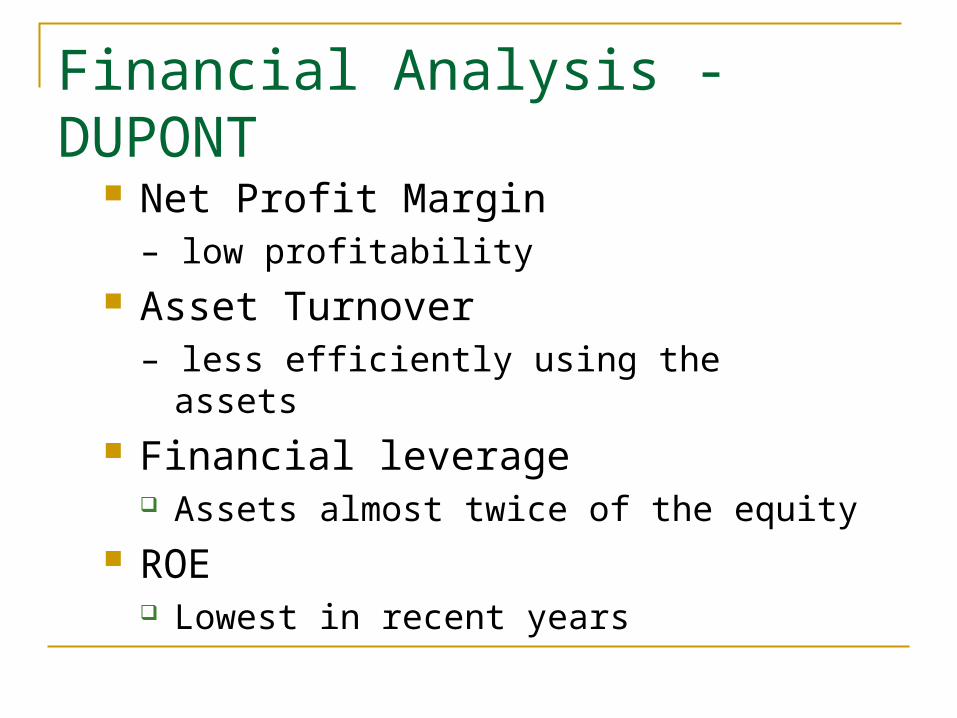

Net Profit Margin – low profitability

Asset Turnover – less efficiently using the assets

Financial leverage Assets almost twice of the equity

ROE Lowest in recent years

Financial Analysis

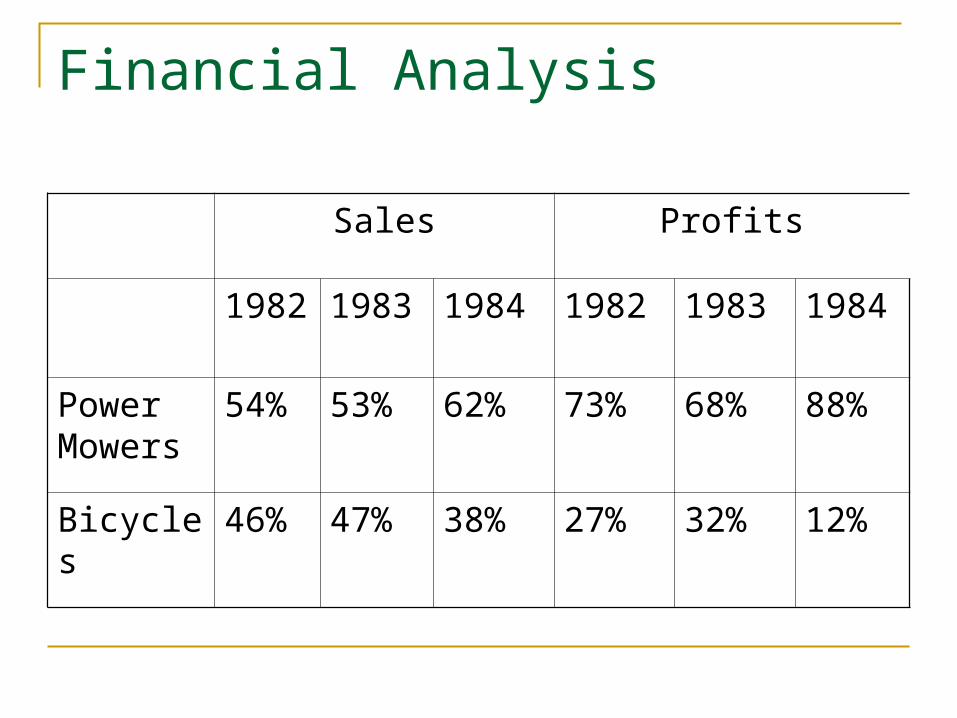

Sales Profits

1982 1983 1984 1982 1983 1984

Power Mowers

54% 53% 62% 73% 68% 88%

Bicycles 46% 47% 38% 27% 32% 12%

Financial Analysis

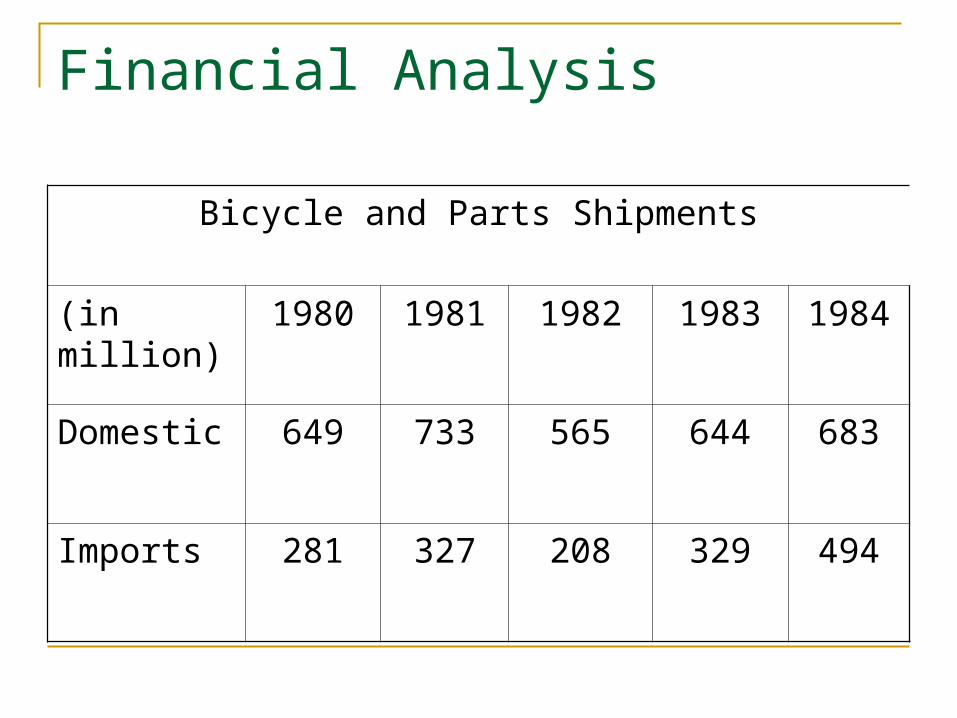

Bicycle and Parts Shipments

(in million) 1980 1981 1982 1983 1984

Domestic 649 733 565 644 683

Imports 281 327 208 329 494

Financial Analysis

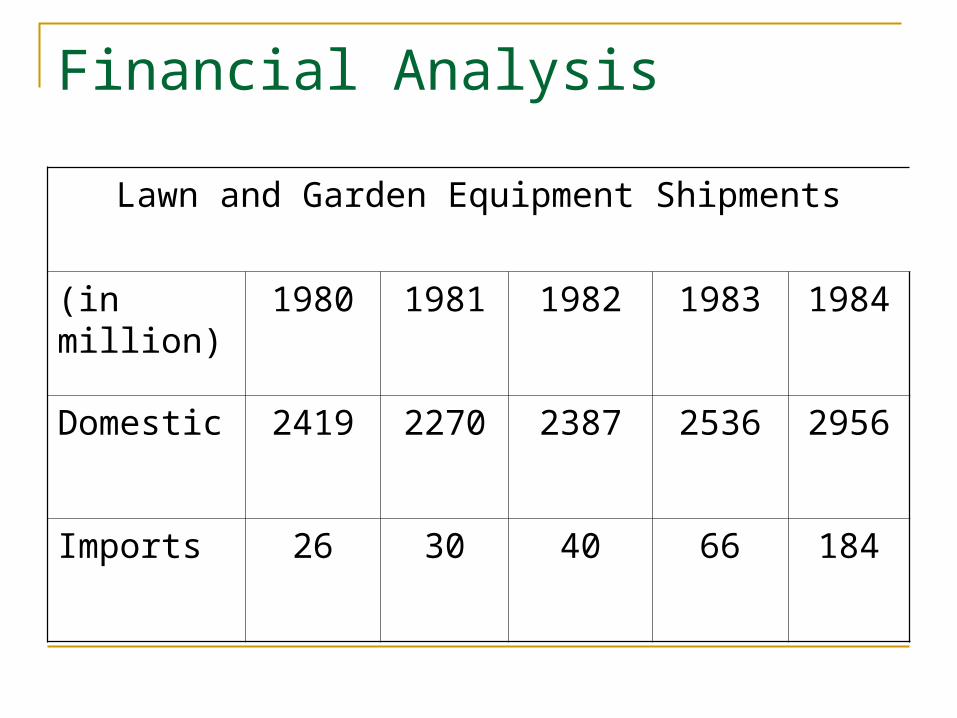

Lawn and Garden Equipment Shipments

(in million) 1980 1981 1982 1983 1984

Domestic 2419 2270 2387 2536 2956

Imports 26 30 40 66 184

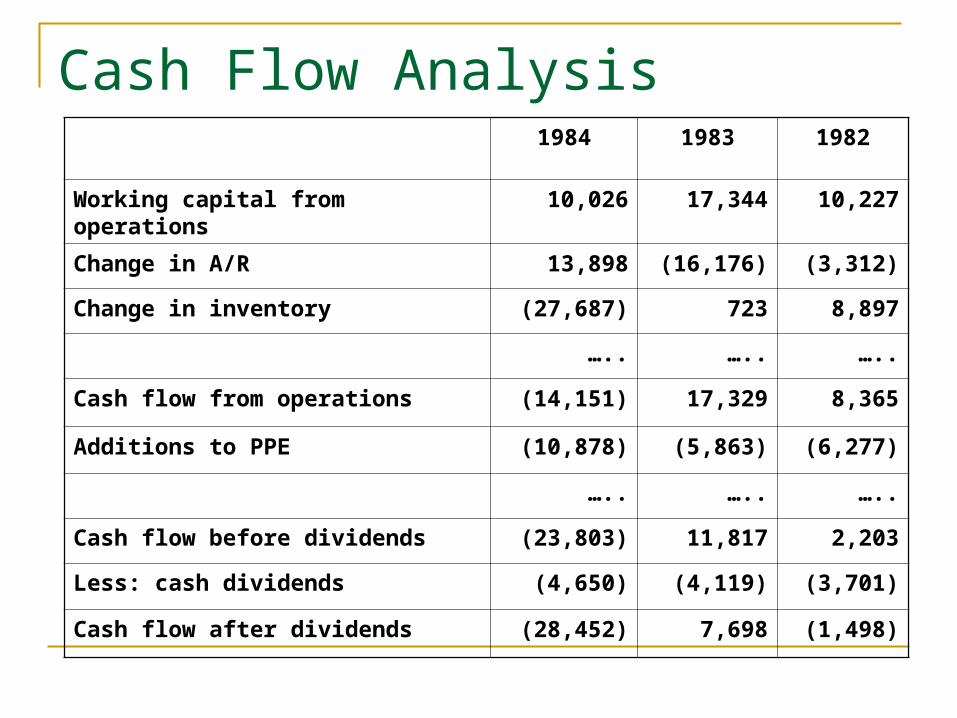

Cash Flow Analysis1984 1983 1982

Working capital from operations 10,026 17,344 10,227

Change in A/R 13,898 (16,176) (3,312)

Change in inventory (27,687) 723 8,897

….. ….. …..

Cash flow from operations (14,151) 17,329 8,365

Additions to PPE (10,878) (5,863) (6,277)

….. ….. …..

Cash flow before dividends (23,803) 11,817 2,203

Less: cash dividends (4,650) (4,119) (3,701)

Cash flow after dividends (28,452) 7,698 (1,498)

Class Discussion 2

As security analysts: Would you keep the company’s stock under the

equity income fund? Would you keep a different equity portfolio? Would you consider to sell it?

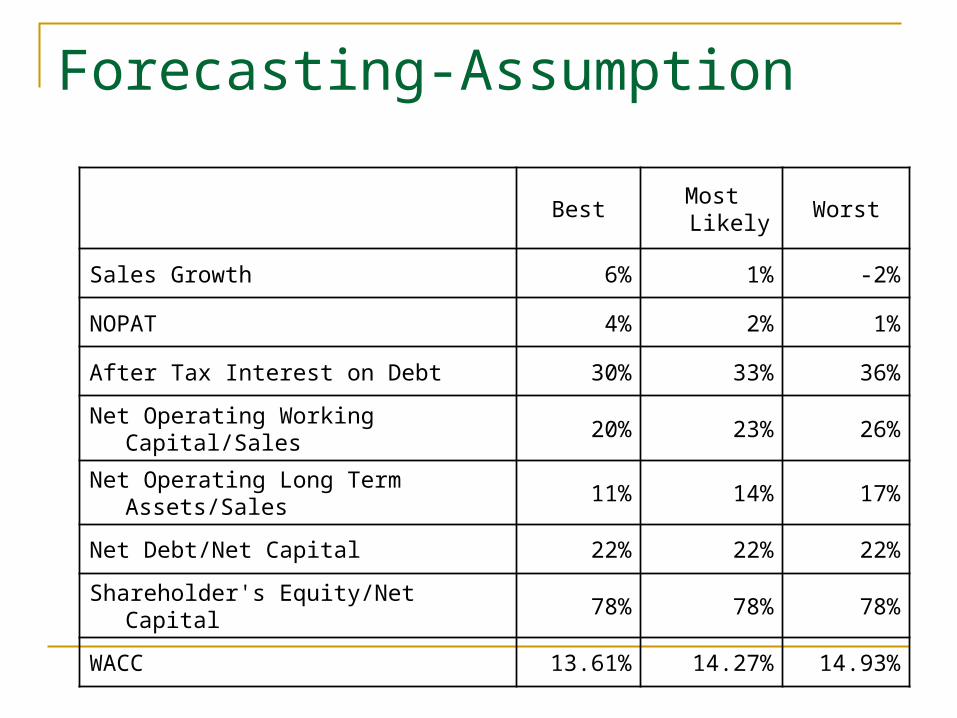

Forecasting-Assumption

BestMost Likely

Worst

Sales Growth 6% 1% -2%

NOPAT 4% 2% 1%

After Tax Interest on Debt 30% 33% 36%

Net Operating Working Capital/Sales

20% 23% 26%

Net Operating Long Term Assets/Sales

11% 14% 17%

Net Debt/Net Capital 22% 22% 22%

Shareholder's Equity/Net Capital 78% 78% 78%

WACC 13.61% 14.27% 14.93%

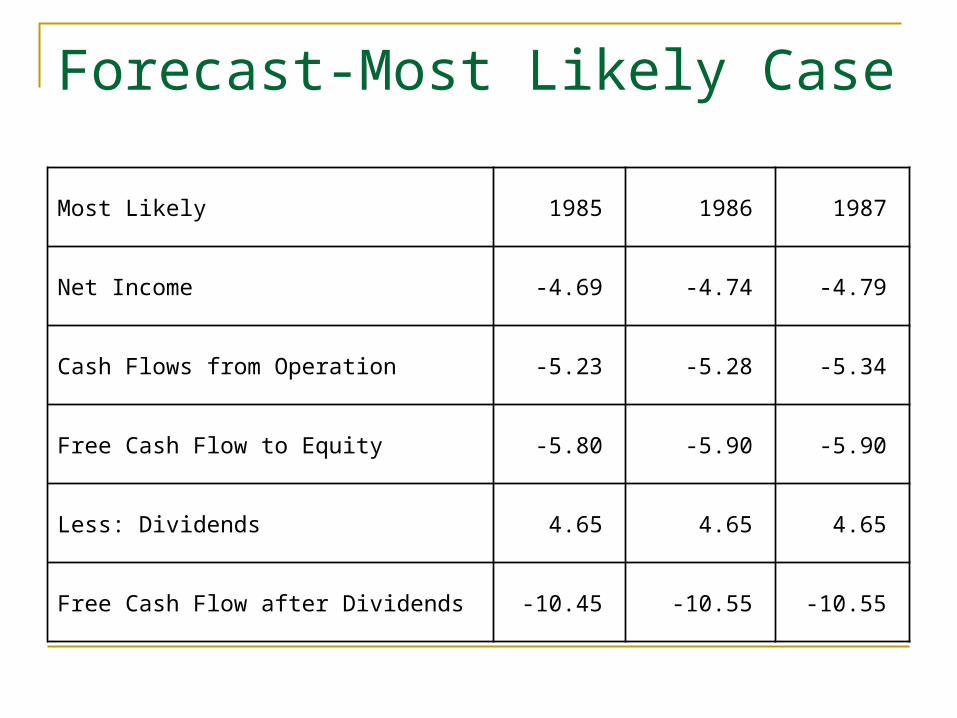

Forecast-Most Likely Case

Most Likely 1985 1986 1987

Net Income -4.69 -4.74 -4.79

Cash Flows from Operation -5.23 -5.28 -5.34

Free Cash Flow to Equity -5.80 -5.90 -5.90

Less: Dividends 4.65 4.65 4.65

Free Cash Flow after Dividends -10.45 -10.55 -10.55

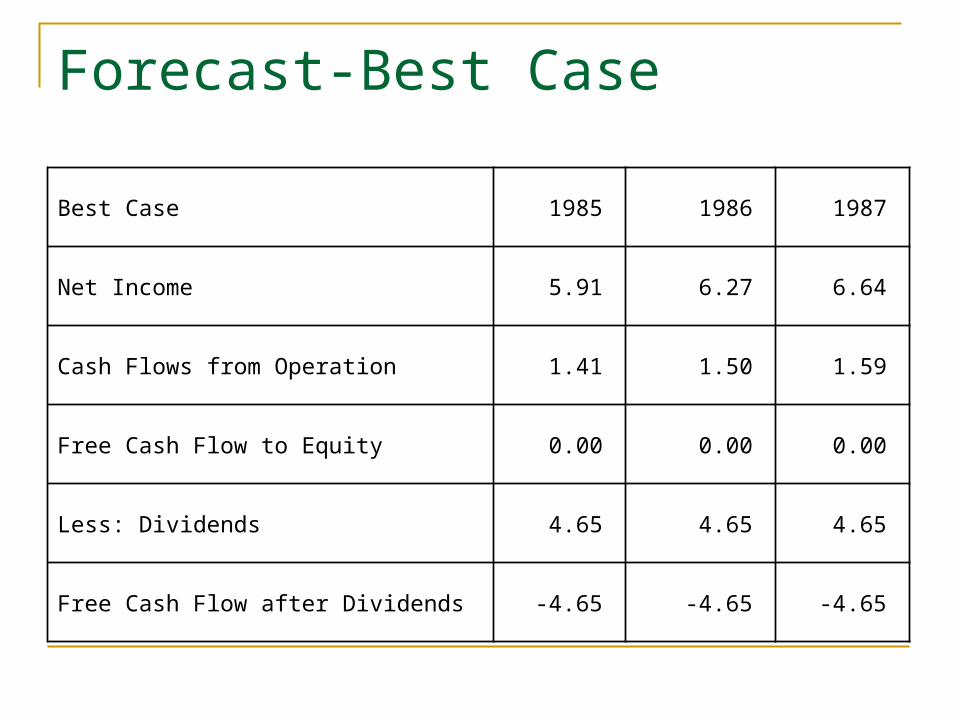

Forecast-Best Case

Best Case 1985 1986 1987

Net Income 5.91 6.27 6.64

Cash Flows from Operation 1.41 1.50 1.59

Free Cash Flow to Equity 0.00 0.00 0.00

Less: Dividends 4.65 4.65 4.65

Free Cash Flow after Dividends -4.65 -4.65 -4.65

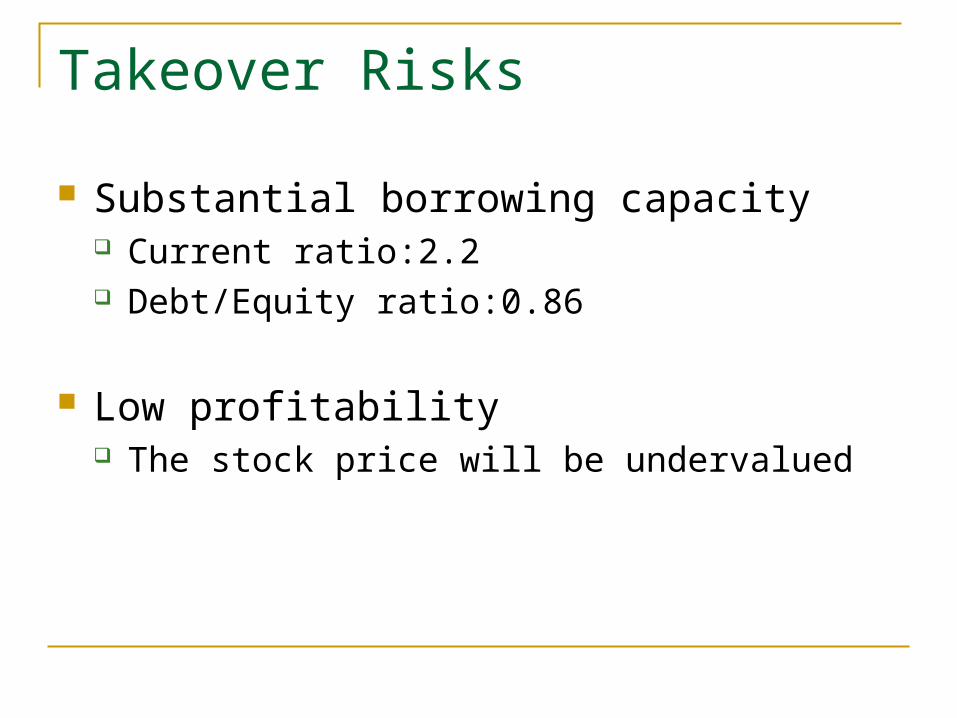

Takeover Risks

Substantial borrowing capacity Current ratio:2.2 Debt/Equity ratio:0.86

Low profitability The stock price will be undervalued

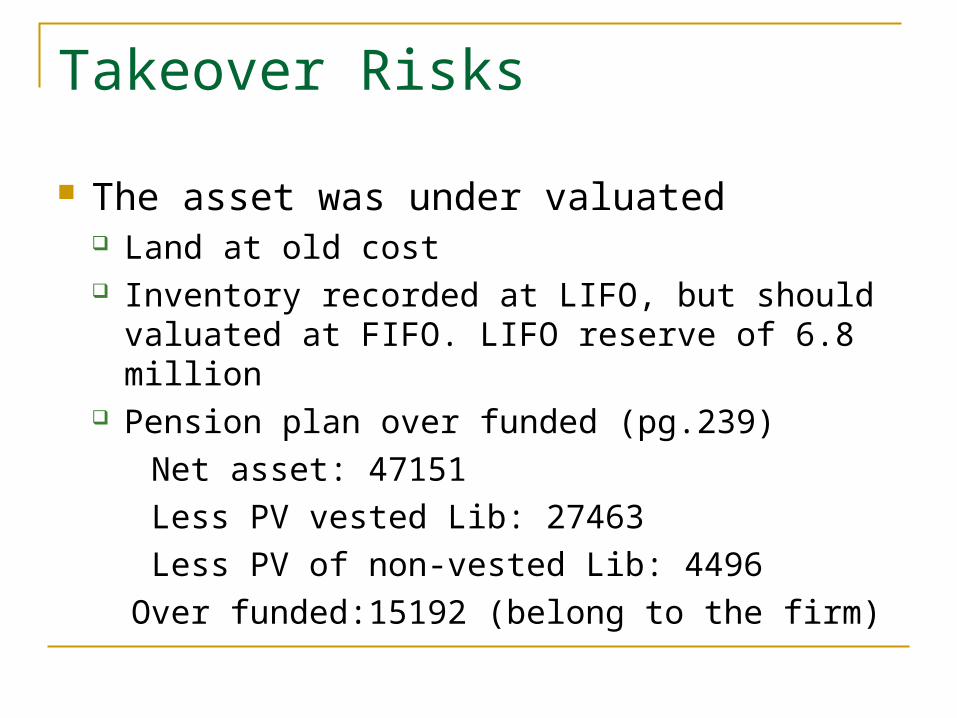

Takeover Risks

The asset was under valuated Land at old cost Inventory recorded at LIFO, but should valuated at

FIFO. LIFO reserve of 6.8 million Pension plan over funded (pg.239)

Net asset: 47151

Less PV vested Lib: 27463

Less PV of non-vested Lib: 4496

Over funded:15192 (belong to the firm)

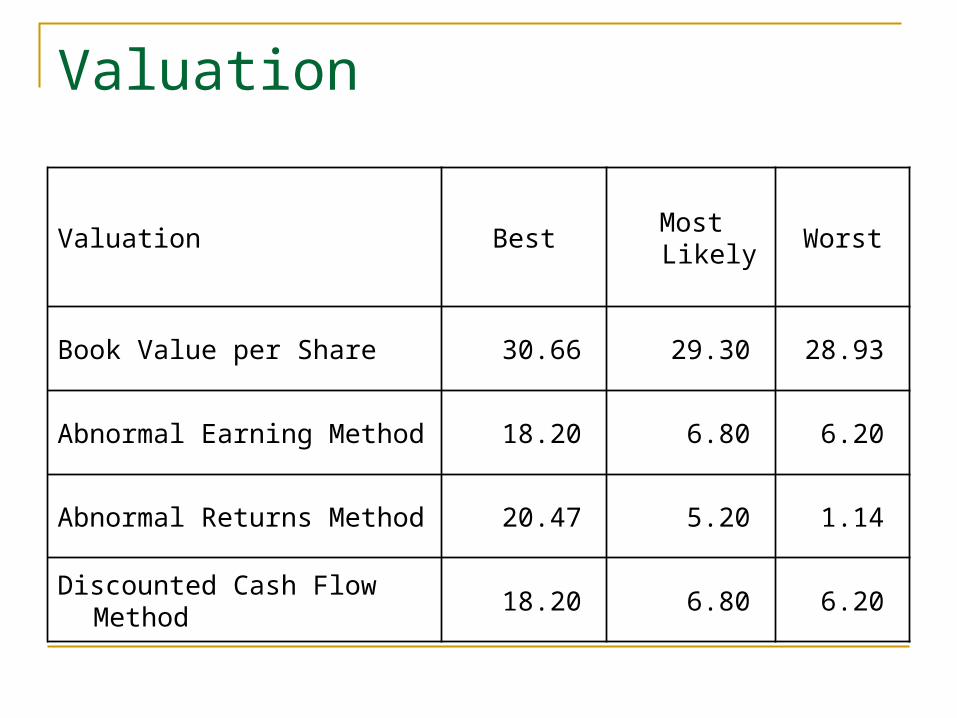

Valuation

Valuation BestMost Likely

Worst

Book Value per Share 30.66 29.30 28.93

Abnormal Earning Method 18.20 6.80 6.20

Abnormal Returns Method 20.47 5.20 1.14

Discounted Cash Flow Method

18.20 6.80 6.20

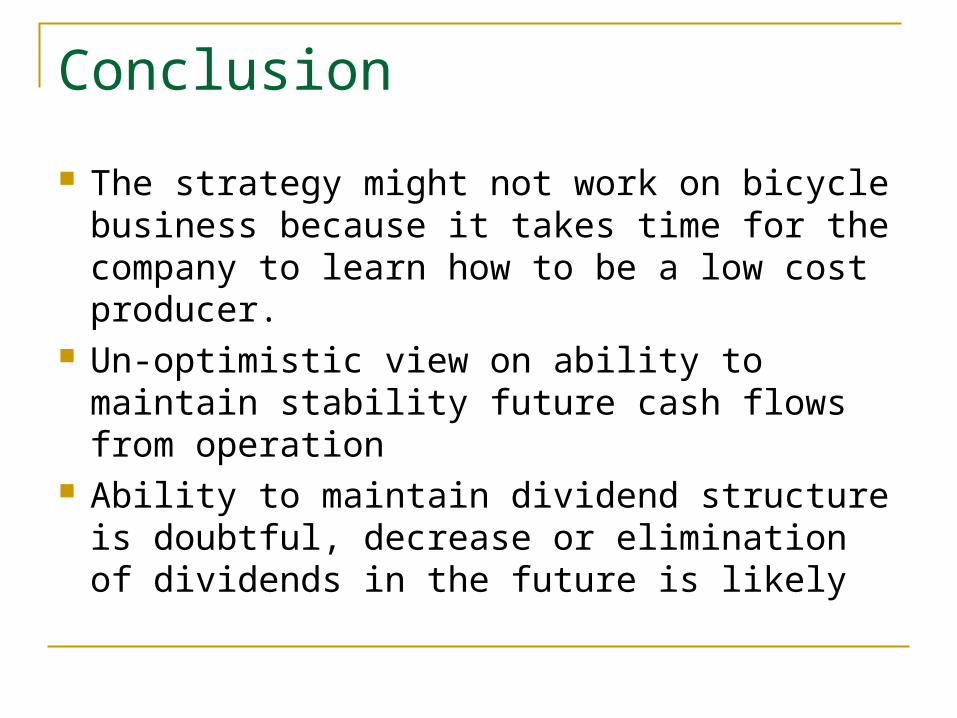

Conclusion

The strategy might not work on bicycle business because it takes time for the company to learn how to be a low cost producer.

Un-optimistic view on ability to maintain stability future cash flows from operation

Ability to maintain dividend structure is doubtful, decrease or elimination of dividends in the future is likely

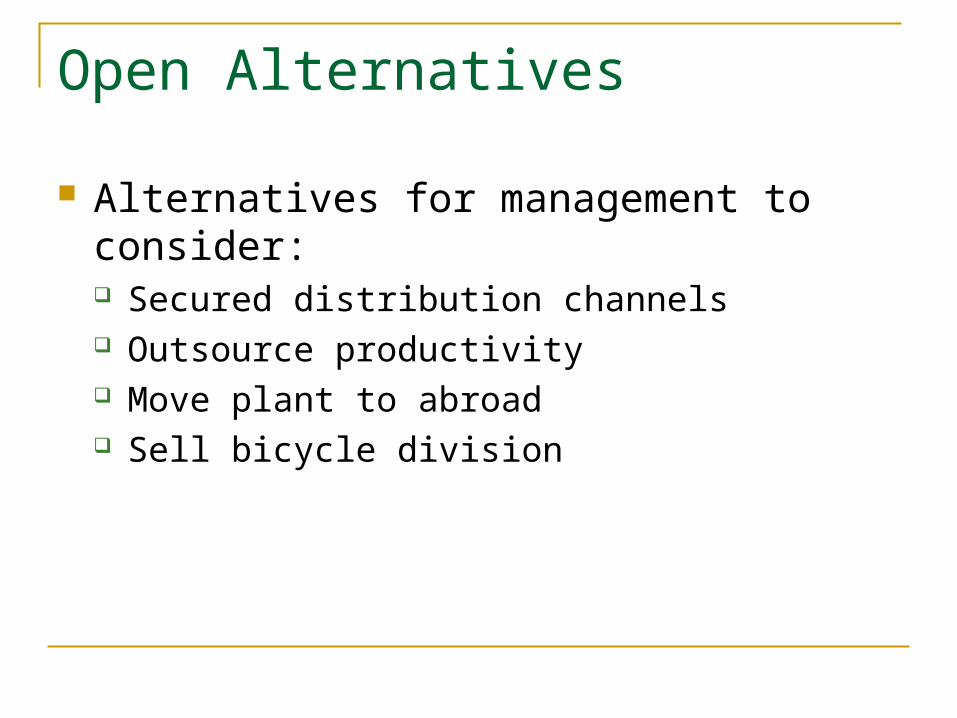

Open Alternatives

Alternatives for management to consider: Secured distribution channels Outsource productivity Move plant to abroad Sell bicycle division

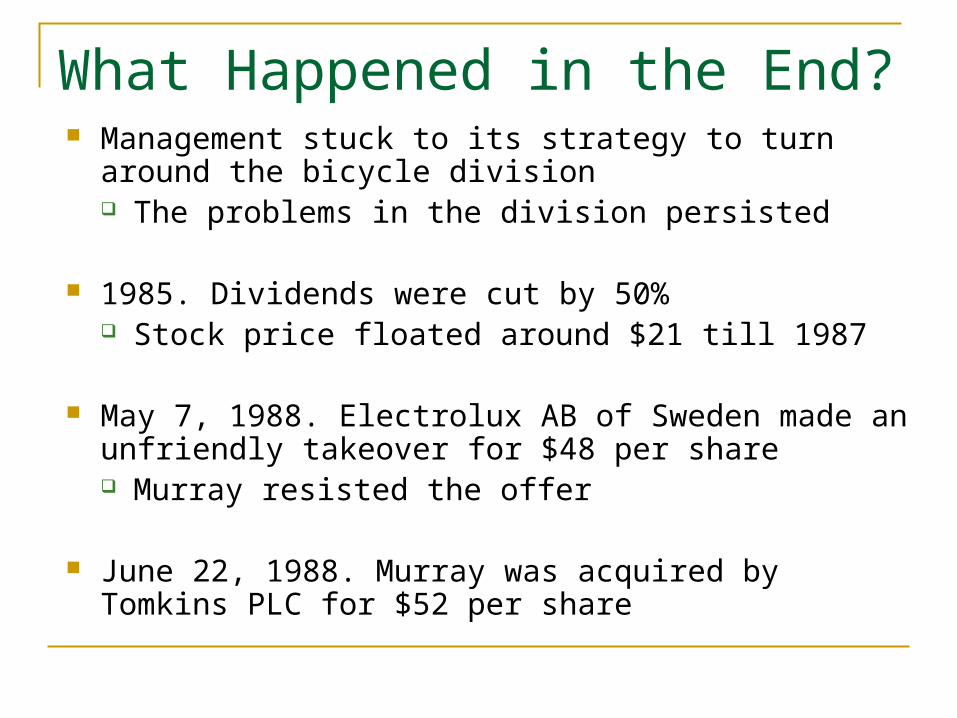

What Happened in the End? Management stuck to its strategy to turn around the

bicycle division The problems in the division persisted

1985. Dividends were cut by 50% Stock price floated around $21 till 1987

May 7, 1988. Electrolux AB of Sweden made an unfriendly takeover for $48 per share Murray resisted the offer

June 22, 1988. Murray was acquired by Tomkins PLC for $52 per share

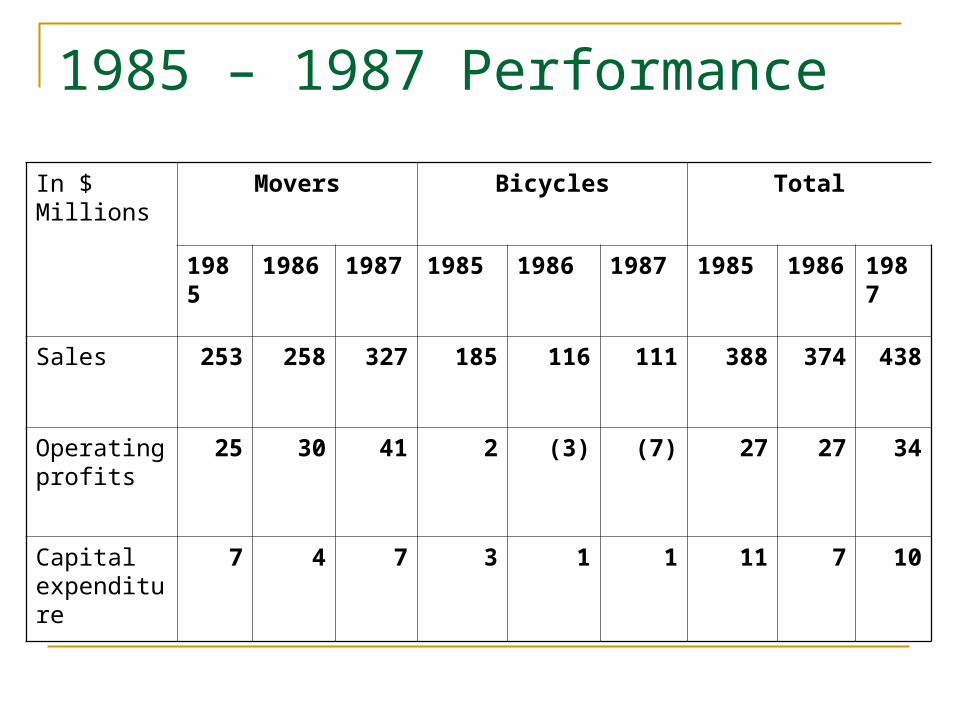

1985 – 1987 Performance

In $ Millions Movers Bicycles Total

1985 1986 1987 1985 1986 1987 1985 1986 1987

Sales 253 258 327 185 116 111 388 374 438

Operating profits

25 30 41 2 (3) (7) 27 27 34

Capital expenditure

7 4 7 3 1 1 11 7 10

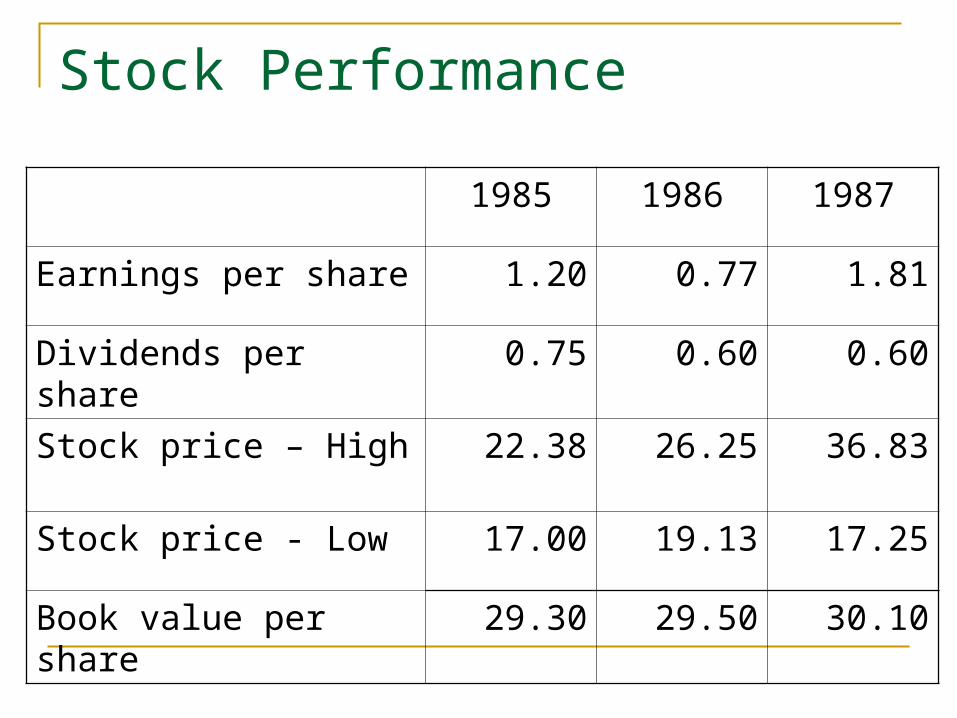

Stock Performance

1985 1986 1987

Earnings per share 1.20 0.77 1.81

Dividends per share 0.75 0.60 0.60

Stock price – High 22.38 26.25 36.83

Stock price - Low 17.00 19.13 17.25

Book value per share 29.30 29.50 30.10

QUESTION?