THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS · PDF fileobjectives clearly...

5

Page 1 of 5 © Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plc ICIS accepts no liability for commercial decisions based on the content of this report THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS MAY 2016 The scale-up of new polymer plants in the Middle East, including the 1.43m tonne/year polyethylene (PE) capacity of Borouge 3 at Ruwais, Abu Dhabi, and the 1.32m tonne/year plant recently launched by Sadara at Jubail, Saudi Arabia, will have a huge impact on global PE markets. Polypropylene (PP) production will also increase, with the ramp-up of Borouge 3. Another factor set to significantly impact global polymer markets is the lifting of sanctions in Iran. This will speed up polymer investments in Iran, where new PE capacity was already scheduled to go on stream this year. Total polyolefin demand in the region, however, accounted for a mere 4% of total world demand in 2015. While there are attempts to develop downstream converting industries in the region, this still leaves plenty of material available for export. The Middle East is now an established player in the global polymers market. Since the early 2000s, the Middle East has emerged as the low-cost region for export-oriented polyolefins production. The abundance of cheap gas reserves in the region has provided a massive competitive advantage, especially with the rise in crude oil prices seen at the beginning of this millennium and more recently in 2007 and in 2009-2010 after the global financial crisis. The Middle East – as we all know – has traditionally enjoyed a significant advantage in terms of feedstocks that promoted a progressive expansion of capacity in the region, primarily driven by Saudi Arabia, and more recently by Iran, the UAE, and Qatar (but so far limited to PE in Qatar). WHITEPAPER Image credit: Borouge

Transcript of THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS · PDF fileobjectives clearly...

Page 1 of 5© Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plcICIS accepts no liability for commercial decisions based on the content of this report

THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS

MAY 2016

The scale-up of new polymer plants in the Middle East, including the 1.43m tonne/year polyethylene (PE) capacity of Borouge 3 at Ruwais, Abu Dhabi, and the 1.32m tonne/year plant recently launched by Sadara at Jubail, Saudi Arabia, will have a huge impact on global PE markets. Polypropylene (PP) production will also increase, with the ramp-up of Borouge 3.

Another factor set to significantly impact global polymer markets is the lifting of sanctions in Iran. This will speed up polymer investments in Iran, where new PE capacity was already scheduled to go on stream this year.

Total polyolefin demand in the region, however, accounted for a mere 4% of total world demand in 2015. While there are attempts to develop downstream converting industries in the region, this still leaves plenty of material available for export.

The Middle East is now an established player in the global polymers market. Since the early 2000s, the Middle East has emerged as the low-cost region for export-oriented polyolefins production. The abundance of cheap gas reserves in the region has provided a massive competitive advantage, especially with the rise in crude oil prices seen at the beginning of this millennium and more recently in 2007 and in 2009-2010 after the global financial crisis.

The Middle East – as we all know – has traditionally enjoyed a significant advantage in terms of feedstocks that promoted a progressive expansion of capacity in the region, primarily driven by Saudi Arabia, and more recently by Iran, the UAE, and Qatar (but so far limited to PE in Qatar).

WHITEPAPER

Image credit: Borouge

© Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plcICIS accepts no liability for commercial decisions based on the content of this report

THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS

Page 2 of 5

The capacity expansion in the region has been such to determine a change in the global petrochemical industry landscape. In 2005, the Middle East accounted for 9.6% of global PE capacity and 4.6% of PP. But by 2015, ten years later, both shares had at least doubled, up by 18.6% for PE and 12.4% for PP.

Regional consumption has grown at a fairly average rate of 6.5%/year (PE) and 6.9%/year (PP) during 2000-2015. These compare with average global growth rates of 3.9%/year (PE) and 4.8%/year (PP).

However, as already stated, total polyolefin demand in the region only accounted for a mere 4% of total world market in 2015.

The largest consuming country is – and will be – Iran, followed by Saudi Arabia. These are also the most populous countries in the region (together account for around a hundred million people). Other sizeable markets include UAE, Israel, Jordan, Kuwait, Lebanon, Oman and Qatar.

Source: ICIS Supply and Demand Database, ICIS Consulting

Source: ICIS Supply and Demand Database, ICIS Consulting

© Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plcICIS accepts no liability for commercial decisions based on the content of this report

THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS

Page 3 of 5

The Middle East will certainly see a major drive to boost local consumption growth. In recent years, governments in the Gulf region have taken several initiatives to try to further progress from an export-oriented petrochemical market.

In recent years, the focus was on the development of the downstream converting industry. The objectives clearly are the diversification of the economy and the expansion of the petrochemical value chain.

The largest investments have been in Saudi Arabia and in the UAE, with many initiatives put in place for new Small-Medium Enterprises in the plastics processing industry. This is growing in the form of industrial clusters especially in Saudi Arabia, but also in the UAE where the Abu Dhabi Polymers Park is attracting lots of foreign investment.

The vast majority of the processing capability in the region is organised around these clusters, and is also now happening in Oman and Qatar. The noticeable exception is probably in pipe production, which is more geographically dispersed by its nature.

Future market potential is seen in applications like: films (packaging film in particular), pipe, automotive components, households, fibres, wire and cable. But still, at the end of the decade, domestic consumption will only account for 23% of regional PE production and 32% of PP production.

Source: ICIS Supply and Demand Database, ICIS Consulting

Source: ICIS Supply and Demand Database, ICIS Consulting

© Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plcICIS accepts no liability for commercial decisions based on the content of this report

THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS

Page 4 of 5

In terms of applications in the Middle East, PE is largely used in packaging, particularly bags and heavy-duty sacks. The dominating process for PE is blown and cast films (especially stretch films), and there have been recent investments in developing multi-layer extrusion capacity. Apart from packaging and other films, HDPE is also quite commonly used for producing containers, crates and bottles – but the latter historically faced competition from polyethylene terephthalate (PET) as in many markets elsewhere in the world. Other applications are in white goods’ components, and injection moulding. High density PE (HDPE) pipes are growing in importance (for example in water transportation) as well as fittings.

New applications will also emerge as product differentiation grows from the local polymer plants, for instance special low density (LDPE) grades from Borouge for wire and cable applications.

PP is mostly used in fibres and film – especially biaxially oriented polypropylene (BOPP). Fibres are dominated by carpet manufacturing, woven PP for heavy-duty sacks, and non-wovens (mainly for exports). With the expansion of product grades capability, block and random copolymer uses are growing fast in applications like appliances, and consumer goods. Injection moulding use is relatively lower than extrusion, due to the historical low development of industries like electronics, automotive and white goods.

Alongside weaker Chinese demand, another factor likely to determine a change in the Middle East petrochemical industry landscape is the lifting of sanctions in Iran, which will undoubtedly speed up polymer investments in the country. However, it is widely debated whether the end of UN-imposed sanctions on Iran will have immediate implications for its PE-PP export capability.

International sanctions concerned Iran oil, gas and petrochemicals investments. Prior to sanctions, the country had considered and announced multiple petrochemical capacity additions based on its vast gas reserves, but its international isolation resulted in continuous delays. The delays resulted from a lack of technical resources, rather than any lack of final market recipients globally. Sanctions had brought a general slowdown in new projects execution.

According to ICIS Consulting, in 2014 Iran exported approximately 1.2m tonnes of HDPE, 800,000 tonnes of LDPE and only a few dozen tonnes of linear low density (LLDPE) material. In 2015, export volumes increased for all PE types – up to 1.3m of HDPE, 850,000 tonnes of LDPE and 150,000-160,000 tonnes of LLDPE, and a similar amount of PP. These volumes will grow further this year, thanks to the opening of new trade opportunities and the possible increase of PE capacity in the country.

European buyers may be the most hesitant to invite back Iranian imports. They may be worried about possible banking issues and the insecurity of Iranian sellers’ shipping schedules. According to sources, some volumes from Iran were offered to Europe a couple of months ago, certainly for PE,

Source: ICIS Supply and Demand Database, ICIS Consulting

© Copyright 2016 Reed Business Information Ltd. ICIS is a member of RBI, part of RELX Group plcICIS accepts no liability for commercial decisions based on the content of this report

THE MIDDLE EAST – NEW PLANTS, NEW PLAYERS, NEW PRODUCTS

Page 5 of 5

and certainly further volumes will be made available later this year. But, overall, Iranian producers and traders will need time before they reintegrate effective business connections with Europe.

Nonetheless, many are already renewing the REACH (Registration, Evaluation, Authorisation and restriction of Chemicals) certificates necessary to trade material in Europe, and banks will move quickly to re-join the Society for Worldwide Interbank Financial Telecommunication (SWIFT) banking system, which will be the key to ease payments from non-Iranian customers.

In terms of new capacity for 2016, according to official information, it is thought that Mahabad Petrochemical’s 300,000 tonne/year HDPE/LLDPE swing capacity will start operations this year – the plant was close to completion by the end of 2015. ICIS Consulting also estimates that the 300,000 tonne/year LDPE project by Kordestan Petrochemical at Sanandaj will enter production during the second half of 2016.

Exports from the country will increase, further investments are very likely even before the end of the decade, PE and PP will also be moved back to Europe. Some further investments are not confirmed yet, and are most likely possible in the next decade.

Globally, capacity increases will more than meet additional demand this year, especially for PE, so global average operating rates will move downwards. And this is likely to affect global prices at some point during 2016.

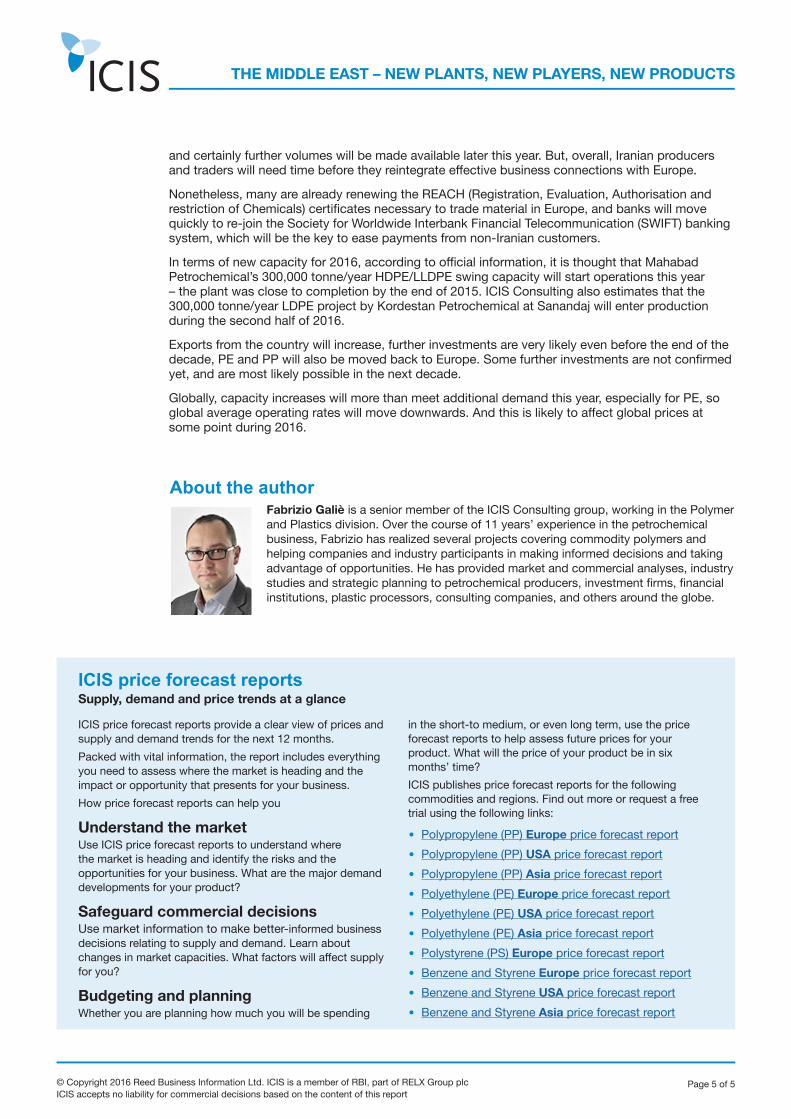

About the authorFabrizio Galiè is a senior member of the ICIS Consulting group, working in the Polymer and Plastics division. Over the course of 11 years’ experience in the petrochemical business, Fabrizio has realized several projects covering commodity polymers and helping companies and industry participants in making informed decisions and taking advantage of opportunities. He has provided market and commercial analyses, industry studies and strategic planning to petrochemical producers, investment firms, financial institutions, plastic processors, consulting companies, and others around the globe.

ICIS price forecast reports provide a clear view of prices and supply and demand trends for the next 12 months.Packed with vital information, the report includes everything you need to assess where the market is heading and the impact or opportunity that presents for your business.How price forecast reports can help you

Understand the marketUse ICIS price forecast reports to understand where the market is heading and identify the risks and the opportunities for your business. What are the major demand developments for your product?

Safeguard commercial decisionsUse market information to make better-informed business decisions relating to supply and demand. Learn about changes in market capacities. What factors will affect supply for you?

Budgeting and planningWhether you are planning how much you will be spending

in the short-to medium, or even long term, use the price forecast reports to help assess future prices for your product. What will the price of your product be in six months’ time?ICIS publishes price forecast reports for the following commodities and regions. Find out more or request a free trial using the following links:

• Polypropylene (PP) Europe price forecast report

• Polypropylene (PP) USA price forecast report

• Polypropylene (PP) Asia price forecast report

• Polyethylene (PE) Europe price forecast report

• Polyethylene (PE) USA price forecast report

• Polyethylene (PE) Asia price forecast report

• Polystyrene (PS) Europe price forecast report

• Benzene and Styrene Europe price forecast report

• Benzene and Styrene USA price forecast report

• Benzene and Styrene Asia price forecast report

ICIS price forecast reportsSupply, demand and price trends at a glance