The Microfinance Rating Market Outlook_2007_updated

32

The Microfinan ce Rating Market Outlook The Rating Fun d Market Survey 2006 Gail Buyske

-

Upload

ashraful-islam-rafi -

Category

Documents

-

view

220 -

download

0

Transcript of The Microfinance Rating Market Outlook_2007_updated

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 1/32

The Microfinance Rating Market Outlook The Rating Fund Market Survey 2006

Gail Buyske

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 2/32

The Rating Fund would like to thank ADA (Appui au Développement Autonome), theMIX (Microfinance Information eXchange), and the Rating Agencies who contributedto this report.

2

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 3/32

Table of Contents

List of AcronymsList of Tables and Figures

Executive Summary Introduction 5Microfinance Rating Industry Overview 6Credit Risk Ratings and Global Risk Assessments 8Demand 10Supply 16Regional Results 22Conclusion 26

Appendices

Appendix 1: Survey Methodology

Appendix 2: Mandatory MFI Ratings Appendix 3: Regional Microfinance Rating Markets

3

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 4/32

List of Acronyms

ACP Africa, Caribbean, and Pacific StatesBRAC Bangladesh Rural Advancement Committee

CDO collateralized debt obligationDWM developing world marketsEECA Eastern Europe and Central AsiaEU European UnionIDB Inter-American Development Bank IFC International Finance CorporationIFI international financial institutionLAC Latin America and the CaribbeanMBB MicroBanking BulletinMENA Middle East and North AfricaMFI microfinance institutionMISFA Microfinance Investment Support Facility for Afghanistan

MIX Microfinance Information eXchange, Inc.MIV microfinance investment vehiclePENSA Program for East Indonesia SME AssistancePKSF Palli Karma-Sahayak FoundationSEC Securities and Exchange CommissionSIDBI Small Industries Development Bank of IndiaSPV special purpose vehicleSRI socially responsible investor/investmentSSA South and Sub-Saharan Africa

4

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 5/32

List of Tables and Figures

Table 1: Microfinance rating industry overview Table 2: Global risk assessments and credit risk ratings by region, 2006 Table 3: Average MFI rating report prices

Table 4: Regional average rating report prices Table 5: Market penetration ratios Table 6: Three largest MFI rating countries by region

Figure 1: Regional ratings market trendFigure 2: Global risk assessments and credit risk ratingsFigure 3: Market share by regionFigure 4: Market share evolution, LAC and Asia

5

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 6/32

Executive Summary

This report provides an overview of the state of the microfinance institutions (MFIs) rating field as of the end of 2006. This evaluation of the demand and supply side dynamics of thefield is based on the 2006 Market Survey conducted by the Rating Fund and interviews with

market participants.

Demand side issues will have the most significant future impact on the field, with MFI rating agencies having demonstrated their ability to respond effectively to demand from investorsand MFIs. The most significant impact on demand will come from increased activity of investors. The most likely outcome of more investment is more demand for mainstreamcredit agency ratings, so that investors can meet their own regulatory requirements and work in an information environment that is familiar to them. This change in demand would affectonly the upper end of the market and would not threaten specialized MFI rating agencies,particularly if there are mechanisms for new generations of MFIs to be introduced to therating field. There are also other growth opportunities for specialized rating agencies (such associal ratings agencies): continued expansion of global risk assessment products and

development of credit risk rating products recognized by global capital markets.

Two other major demand side issues are (1) the potential growth and impact of requiredratings of regulated MFIs (these are now required in four countries) and (2) Basel II, which will encourage borrowers, such as MFIs, to obtain mainstream credit risk ratings to reducetheir borrowing costs.

The demand and supply side issues discussed here should be seen in the context of theimpressive growth of MFIs and the MFI rating field. For example, international investmentin MFIs increased from an estimated US$1.7 billion in 2004 to at least US$4.2 billion in2006; the number of ratings and assessments increased by 23 percent, from 327 to 403. The

MFI rating field will inevitably face challenges as the market continues to evolve, but it hasthe advantage of facing these challenges in a growing market.

6

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 7/32

Introduction

The MFI rating field is in an exciting period of growth and change as rating agencies adaptto the evolving needs of MFIs and investors and as they position themselves for the future. Two facts about the microfinance field reflect the potential growth opportunities for rating

agencies: (1) international investment in MFIs increased from US$1.7 billion in 2004 to atleast US$4.2 billion in 2006, and (2) MFIs reporting to the Microfinance InformationeXchange, Inc., (the MIX) increased their loan portfolios from US$4.3 billion in 2003 toUS$7.1 billion in 2005.1

MFI rating agencies are demonstrating notable flexibility on the supply side of the market, asevidenced by factors such as geographic expansion, ongoing product development, and theformal alliance of two specialized rating firms. Therefore, the issues that will affect thenature and rate of future growth primarily concern demand. Key questions include thefollowing:

• Will demand become more institutionalized as a result of regulatory requirements?

• Will there be a shift in the current emphasis on global risk assessments compared tocredit risk ratings (global risk assessments account for two-thirds of MFIevaluations)?

• Will the greater involvement of investors lead to more demand for mainstream creditrisk ratings?

• What will be the impact of the conclusion of the Rating Fund, which has, so far, co-financed a quarter of the ratings?

Demand for credit risk ratings is likely to increase, but this is unlikely to diminish demandfor global risk assessments, which fulfill an important diagnostic function.

This report is based on the 2006 Market Survey conducted by the Rating Fund andinterviews with market participants. 2 It consists of an overview of the MFI rating industry;an explanation of the field’s two major products—credit risk ratings and global risk assessments—and a summary of developments in both product areas; a discussion of thedemand side dynamics for MFI ratings and assessments; a discussion of supply sidedynamics; a summary of regional developments; and a conclusion.

MFI Rating Industry Overview

The MFI rating field has been growing at a double digit pace since at least 1997. Expansioncontinued in 2006, with the total number of ratings and assessments increasing by 23 percent,

1 These investment data are based on investments by international financial institutions (IFIs) andmicrofinance investment vehicles (MIVs), which represent the two largest classes of MFI investors. Othertypes of investments are not included. Elizabeth L. Littlefield, “Building Financial Systems for the Poor,MIVs and DFI Investment Examined,” Proceedings of the second annual Cracking the Capital MarketsConference, New York, Presentation March 19, 2007. The MFI data are from Blaine Stephens,“Commercialization continues apace,” MicroBanking Bulletin, Issue 14, Spring 2007. (www.mbb.org) TheMIX is an association created to increase transparency and benchmarking; over 1000 MFIs provideinformation to the MIX regularly. (www.mixmarket.org)2 The survey methodology and the summary characteristics of the rated MFIs are discussed in Appendix 1.

7

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 8/32

from 327 to 403, following growth of 14 percent in 2005 and 27 percent in 2004. 3 (Table 1)Particularly relevant is that 165 MFIs obtained ratings or assessments for the first time,compared with 109 in 2005. This indicates the field’s ongoing growth potential. Repeatratings and assessments also increased, from 218 to 238. Increased demand was largely market driven, with mandatory ratings accounting for only 48 of the ratings in 2006,

compared with 44 in 2005. The Rating Fund accounted for slightly less than one-quarter of the total ratings and assessments in both 2005 and 2006. 4

Table 1: Microfinance rating industry overview

1997–2006 2005 2006 Total number of ratings and assessments completed 1,809 327 403First-time ratings or assessments 721 109 165Repeat ratings or assessments 1,088 218 238Global risk assessments 1,188 217 275Credit risk ratings 621 110 128Mandatory credit risk ratings 314 44 48Proportion of Rating Fund co-financed ratings NA5 22% 24%

Growth in the number of MFI rating agencies reflects a sense of dynamism similar to thatshown by the growth in the number of ratings. The field has grown in 10 years toencompass more than 15 rating agencies, several of which have significant global coverage.One example of the ongoing changes in the field is the formal affiliation of MicroRate andM-CRIL—now called MicroRating International (MRI). This period also was marked by thegeographic expansion of several MFI rating agencies; increased activity by mainstream creditrisk rating agencies; and the emergence of PRIME, a specialized rating agency in Indonesia.

Regional rating markets can be readily divided into two groups based on size (i.e., the

number of ratings concluded in 2006).6 The first group includes Latin America and theCaribbean (LAC) (208 ratings) and Asia (111). The second group includes South and Sub-Saharan Africa (SSA) (30 ratings), Eastern Europe and Central Asia (EECA) (37 ratings), andthe Middle East and North Africa (MENA) (17 ratings). The least penetrated rating marketappears to be SSA. The number of MFIs from the region that report to the MIX andMicrobanking Bulletin (MBB) is in the same range as for LAC and Asia, but the number of ratings is considerably lower.

3 These figures include multiple ratings of the same MFI in one year.4 The increase in the Rating Fund’s share of total ratings was largely driven by an increase of Rating Fundratings in Latin America and the Caribbean (its largest market) from 36 in 2005 to 60 in 2006. Thisincrease reflected the cumulative result of marketing the Rating Fund program by the Fund and the ratingagencies, as well as efforts by MFIs to use the Fund before its closing in 2007.5 The Rating Fund began operations in 2001.6 These data include multiple ratings of the same MFI in one year.

8

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 9/32

Regional Rating Markets Trend

0

50

100

150

200

250

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

C r e d i t R i s k R a t i n g s a n d G l o b a l R i s k A s s e s s m e n t s

LAC

Asia

EECA

SSA

MENA

Note:No data was re ported f or Asia in 1997. No data was reported for EECA and SSA in 1997 and 1998. No data

was reported for MENA in 1997, 1998, and 1999.

Figure 1: Regional rating markets trend

Credit Risk Ratings and Global Risk Assessments

The MFI ratings field produces two basic types of rating products: credit risk ratings andglobal risk assessments.

Credit risk ratings focus on the likelihood that an issuer of debt—whether an MFI or someother entity—will be able to meet its debt servicing obligations. Credit risk ratings used onthe global capital markets represent a statistical probability of default, based on substantialhistorical data. Most credit risk ratings of MFIs reflect a higher degree of judgment—not astatistical probability—because there is not yet sufficient historical data about most MFIs.Mainstream credit risk rating agencies and several locally or regionally based credit agencies,such as CRISIL in India and Class & Asociados and Equilibrium in Peru, produce credit risk ratings for MFIs.

Global risk assessments provide a broader assessment of an MFI’s operations and its prospectsthan the exclusively creditworthiness focus of credit risk ratings. The global risk assessmentis the first product created by the MFI rating field. It can provide a broad range of diagnosticinformation about the MFI’s management, social mission, products, risk management,

growth capacity, etc., in addition to its creditworthiness. Global risk assessments areproduced by the four specialized rating agencies with a global outreach (Microfinanza Rating,MicroRate, M-CRIL, and Planet Rating), CRISIL in India, and PRIME in Indonesia. CRISILand MicroRate are the only organizations to produce both credit and global risk assessments,although several of the specialized rating agencies are developing credit risk products.

A comparison of credit risk ratings and global risk assessments shows that credit risk ratingsare almost exclusively a LAC product. Asia is the only other region in which credit risk

9

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 10/32

ratings (3) were produced in 2006. (See Table 2.) LAC also stands out because not only doesit have a high number of credit risk ratings (125), but global risk assessments are widely usedas well (83). Although the contributing factors are complex, these characteristics may bepartly the result of LAC’s more advanced stage of development in the MFI ratings field.LAC is the first region to adopt MFI ratings, and it is the largest market based on total

number of ratings produced. (In 1997, there were 27 ratings and assessments in LAC,followed by 33 in 1998, before the Asian market began to emerge with 22 ratings in 1999. There were 208 ratings in LAC in 2006—including multiple ratings of the same MFI in oneyear—followed by 111 in Asia.) An additional factor is that several LAC countries havemandatory credit risk ratings for MFIs that meet certain criteria.

Table 2: Global risk assessments and credit risk ratings by region, 2006

Global risk assessments Credit risk ratings7

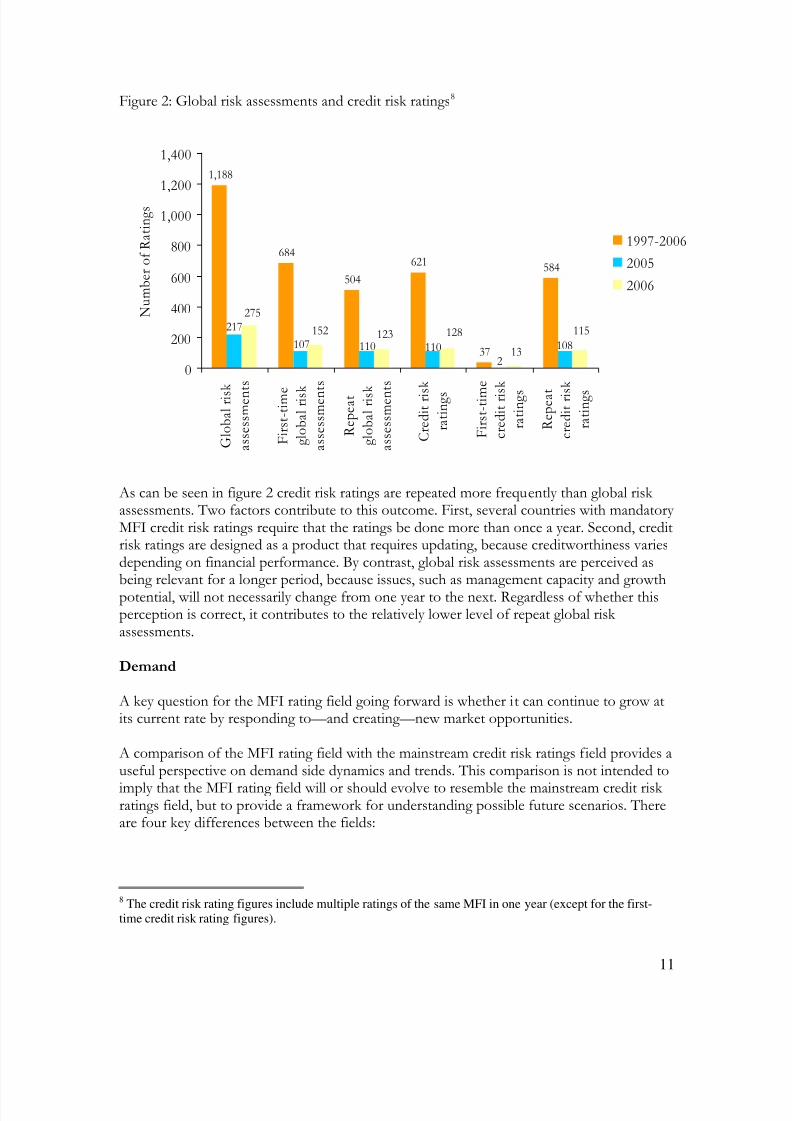

LAC 83 125 (47 mandatory) Asia 108 3 (2 mandatory)SSA 30 0EECA 37 0MENA 17 0 Total 275 128 (47 mandatory) Figure 2 reflects worldwide use of global risk assessments. Global risk assessmentsaccounted for two-thirds of the evaluations completed in 2006; credit risk ratings accountedfor one-third. The difference between the two products is particularly marked whenconsidering first-time assessments and ratings. There were 152 first-time global risk assessments in 2006 and just 12 first-time credit risk ratings.

Global risk assessments are often the first external evaluation product used by MFIs,

because they are useful as a diagnostic tool. As MFIs grow and their need to accessinstitutional funding increases, they may shift to seeking credit risk ratings or obtaining acredit risk rating as a supplement to a global risk assessment. Some MFIs seek out global risk assessments because they are interested in global visibility and access to internationalfinancial institutions (IFIs) and microfinance investment vehicles (MIVs). On the other hand,some MFIs seek credit risk ratings to comply with local regulation and/or financing fromlocal banks.

7 Mandatory risk ratings include multiple ratings of the same MFI in one year.

10

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 11/32

Figure 2: Global risk assessments and credit risk ratings 8

1,188

684

504

621

37

584

108

2

110110107

217 115

13

123152

275

128

0

200

400

600

800

1,000

1,200

1,400

G l o b a l r i s k

a s s e s s m e n t s

F i r s t - t i m e

g l o b a l r i s k

a s s e s s m e n t s

R e p e a t

g l o b a l r i s k

a s s e s s m e n t s

C r e d i t r i s

k

r a t i n g s

F i r s t - t i m

e

c r e d i t r i s

k

r a t i n g s

R e p e a t

c r e d i t r i s

k

r a t i n g s

N u m b e r o f R a t i n g s

1997-2006

2005

2006

As can be seen in figure 2 credit risk ratings are repeated more frequently than global risk assessments. Two factors contribute to this outcome. First, several countries with mandatory MFI credit risk ratings require that the ratings be done more than once a year. Second, creditrisk ratings are designed as a product that requires updating, because creditworthiness variesdepending on financial performance. By contrast, global risk assessments are perceived asbeing relevant for a longer period, because issues, such as management capacity and growthpotential, will not necessarily change from one year to the next. Regardless of whether thisperception is correct, it contributes to the relatively lower level of repeat global risk assessments.

Demand

A key question for the MFI rating field going forward is whether it can continue to grow atits current rate by responding to—and creating—new market opportunities.

A comparison of the MFI rating field with the mainstream credit risk ratings field provides auseful perspective on demand side dynamics and trends. This comparison is not intended to

imply that the MFI rating field will or should evolve to resemble the mainstream credit risk ratings field, but to provide a framework for understanding possible future scenarios. Thereare four key differences between the fields:

8 The credit risk rating figures include multiple ratings of the same MFI in one year (except for the first-time credit risk rating figures).

11

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 12/32

• Unlike in the mainstream credit ratings field, there is only limited institutionalizeddemand for MFI ratings and assessments

• Unlike in the mainstream credit ratings field, there is no demonstrated relationship,as yet, between MFI ratings and assessments and the cost of funding

• Unlike in the mainstream credit ratings field, it is not standard practice for the debt

issuer to pay for the ratings• The mainstream credit rating industry does not provide a global risk assessment

product

The mainstream credit risk ratings field is demand driven; regularly recurring demand forcredit risk ratings is built into the structure of the world’s capital markets. In the UnitedStates, for example, the Securities and Exchange Commission uses ratings created by nationally recognized statistical rating organizations to identify “investment grade” securitiesthat can be purchased by organizations, such as insurance companies and pension funds. The 2004 Basel II Agreement will create an even larger role for mainstream credit rating agencies, because the capital adequacy of banks will be based on the credit ratings these

agencies assign to the banks’ borrowers.

A second characteristic of the mainstream credit risk rating market is the close relationshipbetween a borrower’s rating and cost of funding. Because credit risk ratings express astatistical probability of default, the process of market arbitrage means all borrowers with thesame rating will have similar funding costs.

These two factors create significant incentives for investors to demand ratings and forborrowers to provide them. For investors, ratings are a decision-making tool that expandsthe pool of eligible investments. For borrowers, ratings increase access to funding andprovide a road map for how to reduce borrowing costs by improving their ratings.

These factors also help to explain the third characteristic of mainstream ratings: the issuerpays the rating agency’s fee. Although there is ongoing debate about how to manage theresulting conflict of interest, the simple fact that the practice exists illustrates the value of ratings to issuers.

Although none of these characteristics currently applies to MFI ratings, there are importantdevelopments in all three areas. The three largest MFI rating markets in the world, based onthe number of ratings completed in 2006, are Peru9 (86), India (70), and Bolivia (60).10 Eachof these markets has some form of required MFI rating. Bolivia has mandatory ratingsestablished by government regulation as part of its overall financial sector regulatory framework. The Indian apex bank, the Small Industries Development Bank of India (SIDBI),

requires ratings from all of its MFI partners and accounts for 70 percent of rating demand. Itis instructive to contrast the experience of India with that of Bangladesh. Although,Bangladesh has a large MFI market, the apex organization Palli Karma-Sahayak Foundation

9 For details on Peru’s regulation see appendix 2.10 In the case of Bolivia, 17 MFIs received ratings in 2006; a total of 57 ratings were multiple ratings for thesame MFIs. Most of the multiple ratings reflected regulatory requirements that certain MFIs be rated fourtimes a year. In some cases, these MFIs contracted voluntary global risk assessments in addition to themandatory credit risk ratings.

12

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 13/32

(PKSF) does its due diligence internally and does not require ratings. Although there weresix assessments in Bangladesh in 2005, none was conducted in 2006. An interesting test caseis posed by Afghanistan, where the apex organization Microfinance Investment SupportFacility for Afghanistan (MISFA) is in the process of launching an external assessment of the15 MFIs it funds. If Afghanistan follows the examples of Bolivia and India, the

demonstration effect created by these ratings will lead to more demand for ratings by otherinvestors and MFIs.

Required ratings are not the only factor explaining the growth of these rating markets. Notonly are India and Bolivia large MFI markets with substantial funding from investors, butnot all markets with required ratings for regulated MFIs have grown rapidly. Pakistan is anexample of a large MFI market with required ratings for MFI banks (all banks in Pakistanmust be rated), yet there were only four MFI ratings in 2006.11 Unlike in Bolivia, requiredratings in Pakistan—where MFIs are largely funded by donors and donor-funded apexorganizations—have not led to demand for voluntary ratings. Nevertheless, these three largerating markets underscore the potential role of institutionalized demand in developing theMFI rating field. Particularly relevant for further market development is the impact these

required ratings may be having on the rest of the market, bearing in mind the complexity of the cause-and-effect relationship. Nonmandatory ratings increased in Bolivia in 2006, whileseveral commercial banks in India, including ICICI, have begun to follow SIDBI’s exampleand require microfinance ratings.

Separate from the issue of mandatory ratings, there was more demand in 2006 for ratingsfrom other investors, with several specialized MFI investors requiring ratings as part of theirdue diligence process and/or monitoring processes.12 Although the use of MFI ratings andassessments is far from being institutionalized, this is a significant development for a fieldthat is barely 10 years old.

Although MFI rating agencies interviewed for this survey agreed unanimously that ratingsfacilitated MFI access to funding, these impressions are not conclusive evidence. Onespecific example of this relationship is in India, where SIDBI established a minimum ratingsthreshold for its MFI partners. In addition to anecdotal evidence that ratings affect the costof funding, Peru provides a specific case: the MFI’s rating level determines what fee it paysto the deposit guarantee agency.

The answer to the question of who pays for an MFI rating varies by country and timing. Inseveral cases, donors, government organizations, and/or microfinance networks initiatedrating programs and paid for part or all of the ratings. Examples of organizations other thanMFIs that pay or have paid for ratings include the European Union (EU), FSDU, and

several other funders in Uganda; SIDBI in India; and the Islamic Development Bank inPalestine. The Rating Fund has played an important role in encouraging MFIs to initiateratings and to cover part of the costs themselves. Presumably, as more investors require

11 Microfinance banks in Pakistan that do not collect deposits are not required to provide ratings until theyhave been operating for three years. There are six microfinance banks in Pakistan, most of which haverecently been established.12 An incomplete list of examples includes responsAbility, Blue Orchard, Oikocredit, Deutsche Bank Foundation, and Grameen Foundation.

13

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 14/32

ratings and MFIs can see a clear relationship between having a rating and access tofunding—as well as potentially the price of funding—MFIs will have an increased incentiveto initiate and pay for ratings themselves.

Although the lack of global institutionalized demand and a clear rating–price relationship

limits demand for ratings of MFIs compared with credit risk ratings for private capitalmarkets borrowers, a third factor works in the opposite direction by adding a source of demand. As noted, global risk assessments play an important role as a diagnostic tool that isnot replicated by credit risk ratings. They are also the preferred evaluation product for MFIsundergoing their first external analysis.

Within this overall context for the demand dynamics of the MFI ratings field, there are fourimportant—or potentially important—developments. These concern the consumers of MFIratings and assessments, transaction structures, regulation, and the Rating Fund.

Consumers of ratings and assessments As microfinance has become better known to the international financial community and as

MFI rating agencies have increased their capacity, the spectrum of consumers of MFI ratingsand assessments has expanded as well.

The original consumers of MFI rating products were donors who helped develop themicrofinance field and managers and investors seeking guidance for benchmarking andinstitution building. These consumers have been increasing their use of MFI evaluations,including for the early stages of program design. Examples include the Islamic DevelopmentBank in Palestine, the World Bank in Mali, and the EU in Uganda. National MFIassociations, such as those in Haiti and Pakistan, play a key role in encouraging theirmembers to obtain ratings or assessments; the role of apex organizations has already beennoted.

Private investors have emerged as an increasingly important type of MFI rating consumer. These investors range from purely commercial, profit-seeking investors, to socially responsible investors (SRIs). Not only has investment in MIVs increased by almost US$1.4billion over two years to reach US$2 billion in 2006, but 30 new MIVs were created over thissame period—there were 74 MIVs as of year end 2006.13 Although these figures give animpression of the growth of private investment in MFIs, they reflect only the investmentbeing made through MIVs. Total investment in MFIs, including by IFIs and privateinvestors, is even higher.14

What impact will this new type of investor have on the MFI rating field? Some private

investors are beginning to require ratings or assessments as a precondition to investment. The longer term question is whether these investors will require mainstream credit risk ratings for at least their larger investments. These ratings would provide three potentialadvantages to such investors: they would enable them to comply with any domestic

13 Littlefield, “Building Financial Systems for the Poor.”14 IFI investment in MFIs totaled US$1.1 billion in 2004 and increased to US$2.2 billion during 2006.Littlefield.

14

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 15/32

requirements regarding eligible investments; they would increase the liquidity of investments;and they use rating methodologies that are familiar to private investors.

In assessing the impact of such a development, keep in mind that the MFI field has limitedcapacity to absorb significant flows of new capital. As of year end 2006, 40 MFIs reporting

to the MIX reported gross loan portfolios of over US$100 million; 11 others had gross loanportfolios of over US$85 million.15 Nevertheless, even small amounts of private investmentcould have a significant impact on the characteristics of the ratings field.

Two alternative outcomes, which also apply to transaction structures discussed below, are (1)mainstream and specialized rating agencies could work together to create microfinance creditrisk ratings and/or (2) specialized agencies could develop credit risk rating methodologiesthat would be recognized by private investors. Increased investment by SRIs could raisedemand for social rating products.

Transaction structures A second and related demand side development concerns the structure of MFI transactions.

Borrowers with limited track records and/or those located in countries with low credit risk ratings sometimes enhance their credit risk ratings by borrowing through offshore specialpurpose vehicles (SPVs) that are created to limit lenders’ exposure to the risk of theborrower and its country of operations. 16 This structure enables the borrower to raise fundsat a higher credit risk rating and lower cost. SPVs can be created for different types of transactions. One type of transaction that has grown increasingly popular is collateralizeddebt obligations (CDOs), in which a debt issue is divided into different tranches of risk,based on factors such as guarantees and priority of access to cash flow from the underlying pool of borrowers.

Minimizing the cost of these types of structured transactions entails maximizing their

liquidity. This consideration could increase pressure on borrowers to obtain ratings frommainstream ratings agencies with internationally recognized rating scales.

15 www.mixmarket.org16 An MFI, for example, can take a pool of its loans, transfer it to an offshore incorporated SPV, and raisefunding against the security of that specific pool of loans.

15

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 16/32

Three Precedent-Setting MFI Ratings

In 2006, the Bangladesh Rural Advancement Committee (BRAC) successfully completed the

first AAA-rated local currency microcredit securitization ever undertaken by an MFI. Thistransaction will give BRAC access to US$180 million in local currency funding over six years,thus providing funding at a lower cost and for a longer tenor than has previously beenavailable. The transaction entails the assignment of BRAC’s loan receivables to a specialpurpose trust. This trust issues certificates that represent collateral in the underlying receivablesto the certificate holders. The certificates are collateralized by loans at a ratio of 150 percent.Partly because of the high level of collateralization and the high credit quality of BRAC’sborrowers, the transaction was rated AAA (the highest rating) by the Credit Rating Agency of Bangladesh.

The first rated microfinance CDO was a US$60 million loan securitization created by

Developing World Markets (DWM) that closed in June 2006. It will provide funding for up tofive years to approximately 30 MFIs in 15 countries. The CDO has three debt tranches, of which the most senior tranche was rated A1 by MicroRate, using the Moody’s credit risk rating scale. (This is the highest Moody’s rating.)

The first publicly rated microfinance CDO is to be issued by BlueOrchard Finance and wasrated by Standard & Poor’s (S&P) in May 2007. Investors will receive notes collateralized by the microfinance loan portfolios (the underlying loans are not secured) of 21 MFIs located in13 developing countries. The MFIs will receive five-year funding in a variety of currencies,depending on their needs. The US$108 million transaction has different tranches with differentratings, depending on the structure of the tranche. The preliminary rating for a tranche of US$42 million is AA (the second highest S&P rating).

Regulation A third potential demand side trend concerns regulation. Currently, Bolivia, Ecuador, Peru,and Pakistan require credit risk ratings of MFIs that meet certain criteria, such as those thattake deposits. In Nigeria, a global risk assessment is required for microfinance NGOsapplying for banking licenses. The criteria applied for determining whether an MFI rating isrequired, as well as for authorizing MFI rating agencies, are summarized in Appendix 2.Because these requirements reflect each country’s overall financial sector regulation—creditrisk ratings are required for banks in these countries as well—the question of whether other

countries will follow this example in the future is more of a financial sector question than aspecifically microfinance question.

Another regulatory issue is the likelihood that the introduction of Basel II will put pressureon MFIs with significant bank funding to obtain ratings. Because banks will be obliged toallocate more capital to borrowers that do not have credit risk ratings, nonrated MFIs willface higher borrowing costs.17

17 The rating agencies must be authorized by the national financial authorities in each country.

16

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 17/32

Rating Fund A fourth factor influencing the demand side of the MFI ratings field is the Rating Fund. Thisprogram was initially created by IDB and CGAP in 2001 and was later expanded to includethe EU/ACP Microfinance Programme. A total of 356 ratings was co-financed during the

life of the Fund—24 percent of the total voluntary ratings covered in the Rating Fundsurvey.18 The Rating Fund played a critical role in encouraging broader issuance of ratings by subsidizing the cost of ratings, up to three times, with decreasing subsidies. Anecdotalfeedback from rating agency interviews indicates that many MFIs are now prepared to pay for ratings with their own resources, but that the growth of first-time ratings for smallerMFIs could decrease now that there is a higher financial hurdle.

There are two possible countervailing developments. One is the creation of nationalorganizations, such as those in Indonesia, Uganda, and Azerbaijan, that help to subsidizeratings costs. The other is the momentum the field is creating, as demonstrated by growing private investor demand for ratings and assessments. The Rating Fund, itself, will beevaluated in a separate report.

Supply

This discussion of the supply side of the MFI rating field addresses suppliers and their rating products.

There are three broad categories of MFI ratings suppliers:1. Specialized MFI rating agencies, with regional or global coverage

(Microfinanza Rating, MicroRate, Planet Rating, and M-CRIL all haveregional or global coverage, while PRIME covers only Indonesian MFIs)

2. Regionally or single-country based rating agencies that rate a range of

financial organizations, such as Class & Asociados in Peru and CRISIL inIndia

3. Mainstream credit risk rating agencies (Fitch Ratings, Moody’s, and S&P)

The only rating agencies that currently produce both credit risk ratings and global risk assessments are CRISIL and MicroRate, although a Pakistani credit risk rating agency createdby Japan Credit Rating and a local market intelligence group, Vital Information Services,(JCR-VIS) and Microfinanza Rating have partnered on at least one rating. The specializedMFI rating agencies have historically produced only global risk assessments, while the othertypes of firms have produced credit risk ratings. The three mainstream credit risk rating agencies produced 48 of the 403 ratings and assessments included in the 2006 survey (12

percent); 46 of these were in Bolivia.

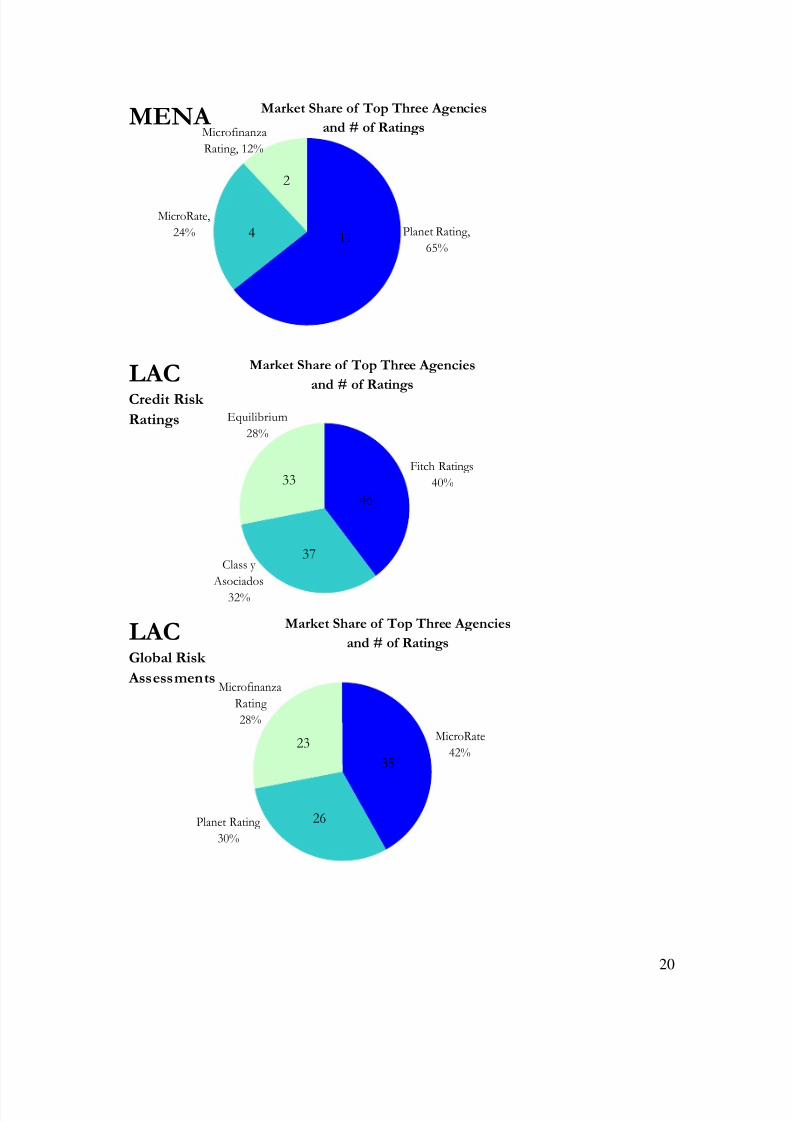

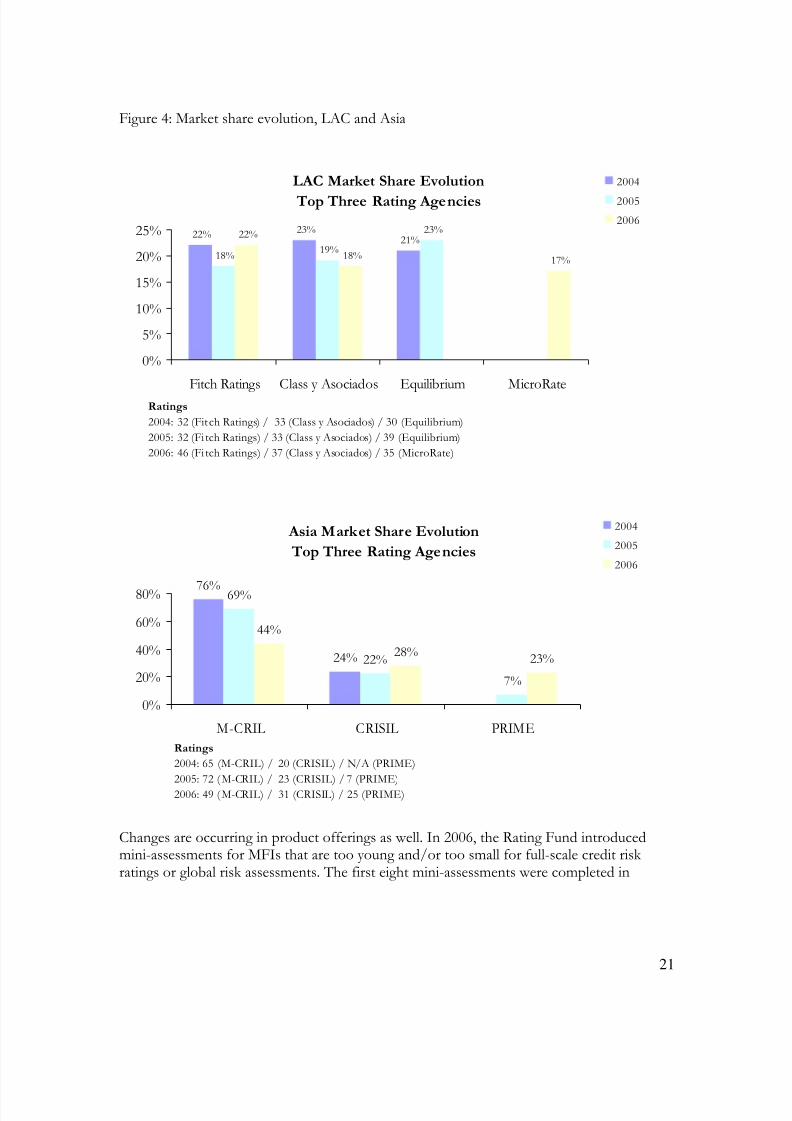

Figure 3 provides a market share overview by region. It shows considerable market sharediversity, with Planet Rating being the only rating agency to hold the number one marketposition in two regions. Figure 4, which illustrates market share shifts in the two largestmarkets, LAC and Asia, underscores the competitiveness in the MFI rating field and the

18 The Rating Fund co-financed voluntary ratings.

17

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 18/32

flexibility of MFI rating agencies in responding to new market opportunities. 19 In LAC,market share rankings have shifted significantly each year, with Fitch Ratings jumping fromthird position to first in 2006, as it has expanded from mandatory to voluntary ratings. LACdata, which combine credit risk ratings and global risk assessments, also show thatMicroRate, which provides global risk assessments, has attained the third largest market

share over a three-year period. In Asia, M-CRIL has held on to its first ranking position buthas been losing absolute market share, while a new rating agency, PRIME, has grown quickly.

PRIME’s rapid emergence, as the result of a project undertaken by the International FinanceCorporation (IFC), Program for East Indonesia SME Assistance (PENSA), and Mercy Corps, demonstrates the underpenetrated nature of the Indonesian market. The majority of PRIME’s clients received assessments for the first time. An important test for PRIME’sfuture will take place in 2007, as it shifts from providing ratings subsidized by its founders tobecoming a fully for-profit ratings agency. Another example of developments in the Asianrating market is provided by JCR-VIS. JCR-VIS works with Microfinanza Rating to provideclients a choice of credit risk ratings or global risk assessments. It also has a joint venture with CRISIL in Bangladesh.

19 The most significant players in SSA have been Planet Rating and MicroRate, where their 50/50 marketshare in 2004, based on 7 ratings each, had evolved in favor of Planet Rating by 2006, with 20 ratings and67 percent market share. The CEE/NIS market has been dominated by Microfinanza Rating, which hashad at least 60 percent market share for the past three years, following by Planet Rating. Planet Rating hasconsistently had the largest market share in MENA.

18

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 19/32

Figure 3: Market Share by Region

M-CRIL,

44%

CRISIL, 28%

PRIME, 23%

49

31

25

Asia Market Share of Top Three Agencies

and # of Ratings

MicrofinanzaRating, 3%

MicroRate,

30%PlanetRating,

67%

SSA

Market Share of Top Three Agencies

and # of Ratings

20

1

9

Microfinanza

Rating, 62%

Planet Rating,

32%

M-CRIL, 5%EECA Market Share of Top Three Agencies

and # of Ratings

12

2

23

19

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 20/32

MicroRate,

24% Planet Rating,

65%

Microfinanza

Rating, 12%

MENA Market Share of Top Three Agencies

and # of Ratings

11

2

4

Fitch Ratings

40%

Equilibrium

28%

Class y

Asociados

32%

Market Share of Top Three Agencies

and # of RatingsLACCredit Risk

Ratings

46

37

33

MicroRate

42%

Microfinanza

Rating

28%

Planet Rating

30%

Market Share of Top Three Agencies

and # of RatingsLACGlobal Risk

Assessments

35

26

23

20

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 21/32

Figure 4: Market share evolution, LAC and Asia

LAC Market Share Evolution

Top Three Rating Agencies

22% 23%21%

18%19%

23%22%

18% 17%

0%

5%

10%

15%

20%

25%

Fitch Ratings Class y Asociados Equilibrium MicroRate

2004

2005

2006

Ratings

2004: 32 (Fit ch Ratings) / 33 (Class y Asociados) / 30 (Equilibrium)

2005: 32 (Fi tch Ratings) / 33 (Class y Asociados) / 39 (Equilibrium)

2006: 46 (Fi tch Ratings) / 37 (Class y Asociados) / 35 (MicroRate)

Asia Market Share Evolution

Top Three Rating Agencies

76%

24%

69%

22%

7%

44%

28%23%

0%

20%

40%

60%

80%

M-CRIL CRISIL PRIME

2004

2005

2006

Ratings

2004: 65 (M-CRIL) / 20 (CRISIL) / N/A (PRIME)

2005: 72 (M-CRIL) / 23 (CRISIL) / 7 (PRIME)

2006: 49 (M-CRIL) / 31 (CRISIL) / 25 (PRIME)

Changes are occurring in product offerings as well. In 2006, the Rating Fund introducedmini-assessments for MFIs that are too young and/or too small for full-scale credit risk ratings or global risk assessments. The first eight mini-assessments were completed in

21

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 22/32

Uganda in 2006. 20 Mini-assessments are intended to serve as a stepping stone that will leadto full-scale assessments. Although none of the MFI rating agencies interviewed for thissurvey anticipates that mini-assessments will become a major part of its business, mini-assessments may help replace the Rating Fund’s role in encouraging new generations of MFIs to issue ratings.

Two new potential product directions underscore the point made earlier that the MFI ratingsfield will not necessarily evolve into a subset of the mainstream credit risk ratings field. Oneproduct being considered is a rating specifically designed to address an organization’s socialmission. Although clearly relevant to MFIs, it could also have a broader application. Anotherpossible product is a rating of self-help groups (SHGs) active in India. 21

Work is also underway to fine tune existing rating products. An important question on thisagenda is how to address sovereign risk. Again comparing mainstream and MFI rating agencies, mainstream credit agencies have global rating scales that explicitly incorporatesovereign risk.22 These ratings are comparable globally. A company in India with a BB rating from S&P represents the same risk of default as a company with a BB rating from S&P in

the United States.

Specialized MFI rating agencies historically have not incorporated sovereign risk into theirevaluations. This has arguably not been necessary for global risk assessments, because they are not exclusively focused on creditworthiness issues that could be affected by sovereignrisk issues. Therefore, some specialized MFI rating agencies have global scales that do notincorporate sovereign risk, while others have scales that are not comparable betweencountries. Historically, sovereign risk has not been an issue for most users of MFI ratings,for whom the primary value was the in-depth analysis of the MFI itself. This situation isshifting, both as private investors become more interested in microfinance and need a moreglobally consistent rating scale that incorporates sovereign risk and as rating agencies

themselves expand their geographic presence and need to ensure ratings consistency.23

AnS&P Working Group created to develop an MFI rating methodology may provide animpetus for further developments. S&P has declared its intention to develop its own rating criteria for MFIs.24

20 MFIs with assets of US$200,000 to US$1 million were eligible for mini-assessments subsidized by theRating Fund.21The Reserve Bank of India defines an SHG as “a registered or unregistered group of micro entrepreneurshaving homogeneous social and economic background voluntarily coming together to save small amountsregularly, to mutually agree to contribute to a common fund and to meet their emergency needs on mutualhelp basis.” As of March 2002, the National Bank for Agriculture and Rural Development, India’s apex

bank for rural development, provided banking services to 461,478 SHGs, covering 7.8 million families.This is only a portion of the total number of SHGs in India.http://www.rbi.org.in/scripts/FAQView.aspx?Id=7.22 There are also specific national scales for some countries.23 The inherent complexity of creating such a scale is exacerbated by the fact that many countries withextensive MFI activity have relatively low country risk ratings. Applying the basic principle that the creditrisk rating of a financial institution will always be somewhat constrained by the creditworthiness of thecountry in which it operates, the result is that the ratings of the MFIs operating in a low-rated country willbe compressed.24

Standard & Poor’s, Microfinance: Taking Root in the Global Capital Markets, June 2007.

22

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 23/32

A related consideration is that each MFI rating agency has its own scale, and there is no clearmapping between scales. Therefore an investor trying to evaluate the Indian MFI market, foran example, cannot readily compare the ratings reports of the agencies operating in thatmarket. (By contrast, there is a generally accepted view in the capital markets abouthow the ratings of mainstream credit rating agencies correlate, despite some differences in

the underlying methodologies.) Although there has been some discussion among specializedrating agencies about the need to formally map their ratings scales, to date, there has notbeen sufficient incentive to do so. This lack of incentive may reflect a strategy by someagencies to gain sufficient market share so that their scale dominates.

A final issue on the supply side concerns the cost of MFI ratings. Although the averagerating cost globally did not change significantly between 2005 and 2006, the costdifferentiation between the regions is noteworthy, with LAC and Asia demonstrating thelowest average ratings costs. This partially reflects the higher competition in those regions, which has led rating agencies both to lower costs and to devise ways to maintain theirmargins by expanding their on-the-ground presence. Another factor influencing the Asianresults is the high volume and low cost structure in India. (See tables 3 and 4.)

Table 3: Average MFI rating report prices25

2005 2006

Global risk assessment US$10,777 US$10,810Credit risk rating US$9,876 US$9,734 Average US$10,716 US$10,729 Table 4: Regional average rating report prices, 2006

Region Average cost

LAC US$9,777 Asia US$8,846SSA US$12,470EECA US$13,158MENA US$12,942

Regional Results

Although 10 years of rapid growth might be expected to have exhausted the MFI rating market’s potential, there still appears to be scope for expansion. Table 5 compares thenumber of MFIs that have had at least one rating or assessment completed between 1997

and 2006 with two estimates of the total number of MFIs per region. The more conservativeestimate, in the first column, is the number of MFIs that reports to MIX Market and MBB. The high-end estimate in the second column includes all types of MFIs, including creditcooperatives. The actual potential MFI rating market is somewhere between these two setsof figures, although presumably closer to the MIX and MBB figures, which capture a largeproportion of MFIs with the desire and ability to maximize their transparency.

25 Based on survey data.

23

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 24/32

Both data sets show that LAC and Asia are the largest markets in terms of the estimatednumber of MFIs. They are also the largest in terms of total MFI assets. Both markets areclose to saturation in terms of MFI ratings, according to MIX/MBB data; however, there isconsiderable room for growth according to the less conservative data set. Even if the

conservative data are used, however, the figure for the number of rated MFIs is based on thenumber of MFIs that have had at least one rating since 1997. Even if the number of MFIseligible for ratings does not increase, which seems highly unlikely, the market can still grow as MFIs are rated regularly.

An interesting outcome of these comparisons concerns SSA, in which the number of MIX/MBB MFIs (243) is comparable to those for LAC (244) and Asia (299). In contrast toLAC and Asia, however, the SSA market has demonstrated the lowest interest in MFI ratings. This is reflected in the low 36.6 percent market penetration (according to the moreconservative data). Some of the factors contributing to this outcome include the relatively small overall size of the SSA market (US$3.16 billion in total MFI assets); slowerdevelopment of commercial interest in this market compared to LAC and Asia; a relatively

high number of investors that do their own due diligence; and a number of larger MFIs in west Africa are cooperatives that have not actively sought external funding. Ratings in SSAalso have been relatively expensive compared those in LAC and Asia (Table 8). However,this should change as more specialized agencies open offices in SSA. 26 The combination of gradually increasing investor interest in SSA MFIs and greater on-the-ground marketing andrating capacity is expected to result in increased market penetration. There have been severallocal donor projects stimulating ratings and assessments by co-funding or subsidizing them(e.g., in Uganda and Mali). 27 It will be instructive to see whether these subsidized ratingscreate momentum and are followed by ratings requested by the same and other MFIs without or with less donor funding.

Although the EECA region has similar penetration as that of the SSA region according tothe conservative calculation (32.6 percent), the EECA market has shown more rapid growthsince 2002 and is seen as having considerable potential. The fact that average MFI size isrelatively large (total MFI assets are US$6.39 billion) creates a larger likelihood that moreMFIs will be interested in ratings. MFIs in the EECA region also have demonstrated acommitment to transparency; nine of the 20 winners of 2006 CGAP Transparency Awards were from the EECA region.

Finally, because of the low estimated number of MFIs in MENA—35 according to the moreconservative data—and the low total MFI assets figure (US$661.7 million), the potential forsignificant growth in MENA appears to be relatively low.

26 Planet Rating opened an office in Senegal in 2005 and in Uganda in 2006. Microfinanza Rating will beopening an office in Kenya in 2007. MicroRate has had an office in Johannesburg for several years.27 Uganda provides an example of how this situation could change in the future. Ugandan MFIs havebeen the biggest issuer of ratings since 1999, with seven of the 26 ratings having been issued in 2006. Theincrease in 2006 was largely because of an initiative by the local rating fund to finance mini-assessments.Mali also showed significant growth in 2006, registering nine ratings in 2006, compared with three ratingsin the previous seven years. These ratings were financed by USAID and the World Bank.

24

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 25/32

Table 5: Market penetration ratios

Estimatednumber of MFIs,

based onMFIsreporting to MIX Market andMBB a

Estimatednumber of MFIs,

including creditcooperativesb

Total MFIassets, basedon MIX

Market andMBB data,c inUS$ billions

MFIsratedat

leastonce,1997– 2006

Marketpenetrationratio, based

on MIX/MBB data(%)

Marketpenetration,including

creditcooperatives(%)

LAC 244 2000 12.49 230 94.3 10.4 Asia 299 1800 8.37 315 105.3 6.2SSA 243 1050 3.16 89 36.6 2.9EECA 187 180 6.39 61 32.6 20.6MENA 35 73 661.7 26 74.3 23.3 Total 1,008 5,103 31.1 721 71.5 14.1a MIX, June 2007. Based on all MFIs reporting to MIX Market and MBB.b CGAP, “Financial Institutions with a Double Bottom Line: Implications for the Future of Microfinance,”Occasional Paper No. 8, July 2004.c The MFI assets figure is based on 948 MFIs. It is based on the number of MFIs that report total assetinformation; the total number of MFIs (1008) is based on the number of MFIs that report borrowerinformation. Adrian Gonzalez, MIX research analyst, compiled this information.

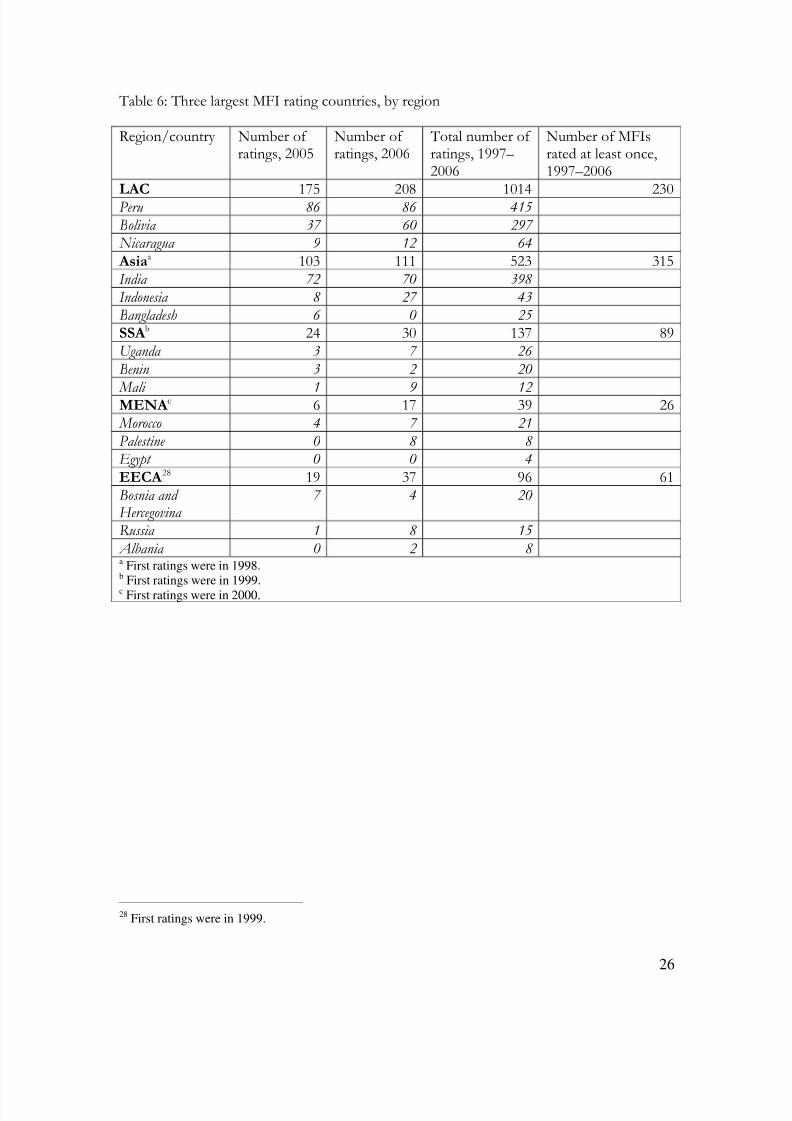

A more detailed discussion of the key characteristics and developments in each region isprovided in Appendix 3. Table 6 provides an overview of the three largest countries by ratings in each region.

25

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 26/32

Table 6: Three largest MFI rating countries, by region

Region/country Number of ratings, 2005

Number of ratings, 2006

Total number of ratings, 1997– 2006

Number of MFIsrated at least once,1997–2006

LAC 175 208 1014 230Peru 86 86 415

Bolivia 37 60 297

Nicaragua 9 12 64

Asiaa 103 111 523 315India 72 70 398

Indonesia 8 27 43

Bangladesh 6 0 25

SSA b 24 30 137 89Uganda 3 7 26

Benin 3 2 20

Mali 1 9 12 MENA c 6 17 39 26 Morocco 4 7 21

Palestine 0 8 8

Egypt 0 0 4

EECA 28 19 37 96 61Bosnia and Hercegovina

7 4 20

Russia 1 8 15

Albania 0 2 8 a First ratings were in 1998.b First ratings were in 1999.c First ratings were in 2000.

28 First ratings were in 1999.

26

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 27/32

Conclusion

The future development of the MFI rating field will depend significantly on the demand sideof the business. It appears that the most significant impact on demand for MFI ratings willcome from the increased activity of private investors representing the entire spectrum of

purely for-profit investors and SRIs. Because MFIs have limited absorption capacity,relatively little private investment can have a significant impact on MFIs and potentially therating market. The most likely outcome of more private investment is more demand formainstream credit agency ratings. This would allow private investors to meet their ownregulatory requirements and work in a familiar information environment. Such a change indemand would affect only the very upper end of the MFI market and would not threatenspecialized MFI rating agencies, particularly if there are mechanisms for new generations of MFIs to be introduced to the rating field. An alternative outcome would be closercooperation between specialized and mainstream rating agencies to develop MFI credit risk ratings or, for some specialized agencies, to develop credit risk ratings recognized by privateinvestors.

The fact that specialized rating agencies produce an important noncredit risk rating product—global risk assessments—provides further growth potential unrelated to theactivities of mainstream credit risk rating agencies. The Outlook Survey and interviewsconfirm the value of these assessments. Not only are they the first external evaluationproduct typically used by MFIs, but some MFIs that need credit risk ratings also use globalrisk assessments. The global risk assessment methodology lends itself to the development of assessments with an exclusive focus on social performance, which is a potential futuregrowth area for MFI rating agencies.

A final demand side issue concerns the potential growth and impact of required ratings, whether mandatory, as in Ecuador, or the result of a policy action by a key national player,

such as SIDBI in India. Basel II is likely to result in more demand for MFI ratings fromcommercial banks that fund MFIs. This will reduce the capital charge for banks and lowerthe cost of funding for MFIs.

This report highlighted the flexibility and dynamism MFI rating agencies have demonstratedon the supply side of the field, as illustrated by their geographic expansion, the involvementof new rating agencies, continued product development, and a formal affiliation betweentwo specialized firms. The future may bring other types of affiliation or consolidation as well,as the result of intensifying consolidation and the conclusion of the Rating Fund. Althoughadapting to a changing market is a significant challenge, growth and increasing competitionare characteristics of a successful market.

27

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 28/32

Appendix 1: Survey Methodology

The data analyzed in this survey encompass an estimated 90–95 percent of the rating agencies that evaluate MFIs and are based on information provided by the four globally active specialized rating agencies (M-CRIL, Microfinanza Rating, MicroRate, and Planet

Rating); seven regional rating agencies (Apoyo y Asociados, Class y Asociados, CRISIL,Equilibrium, JCR-VIS, PRIME, and PCR Holding); and two mainstream rating agencies(Fitch Ratings and S&P).29

The data include all the ratings partially financed by the Rating Fund (356 in total, of which98 in 2006) as well as 1,453 ratings financed independently of the Fund (305 of which werecompleted in 2006). Generally, the more recent independently financed ratings were of largerMFIs; the maximum asset size for Rating Fund eligibility as of January 2006 was US$30million. (Previously there was no size limit.) The maximum average loan size was US$2000, with exceptions considered.

Every MFI rating is counted as one rating, including in countries such as Ecuador and

Bolivia, where MFIs meeting certain criteria must be rated more than once a year.

29 BRC, Ecuability, Feller Rate, and Moody’s participated in the 2005 survey but not the 2006 survey. The2006 data for Ecuability and Moody’s were added to the 2006 survey from other sources.

28

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 29/32

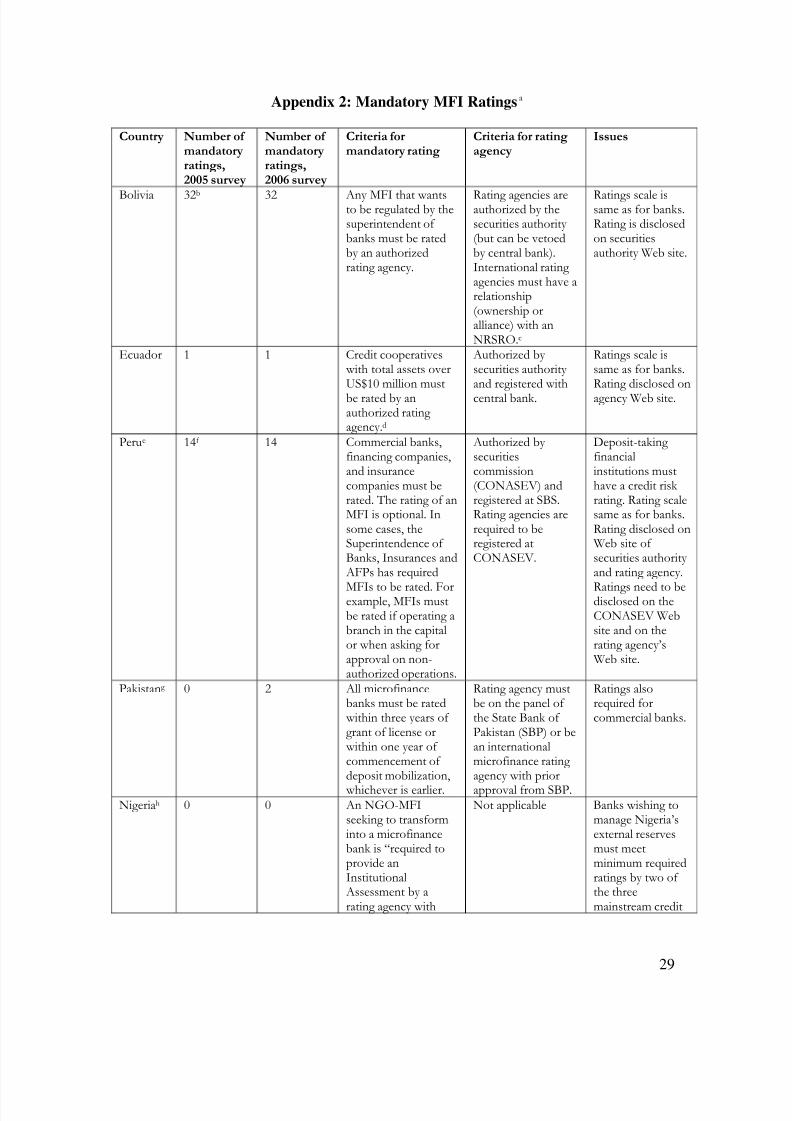

Appendix 2: Mandatory MFI Ratingsa

Country Number of

mandatoryratings,2005 survey

Number of mandatoryratings,2006 survey

Criteria formandatory rating

Criteria for ratingagency

Issues

Bolivia 32b 32 Any MFI that wantsto be regulated by thesuperintendent of banks must be ratedby an authorizedrating agency.

Rating agencies areauthorized by thesecurities authority (but can be vetoedby central bank).International rating agencies must have arelationship(ownership oralliance) with anNRSRO.c

Ratings scale issame as for banks.Rating is disclosedon securitiesauthority Web site.

Ecuador 1 1 Credit cooperatives with total assets overUS$10 million mustbe rated by anauthorized rating agency.d

Authorized by securities authority and registered withcentral bank.

Ratings scale issame as for banks.Rating disclosed onagency Web site.

Perue 14f 14 Commercial banks,financing companies,and insurancecompanies must berated. The rating of anMFI is optional. Insome cases, theSuperintendence of Banks, Insurances and AFPs has required

MFIs to be rated. Forexample, MFIs mustbe rated if operating abranch in the capitalor when asking forapproval on non-authorized operations.

Authorized by securitiescommission(CONASEV) andregistered at SBS.Rating agencies arerequired to beregistered atCONASEV.

Deposit-taking financialinstitutions musthave a credit risk rating. Rating scalesame as for banks.Rating disclosed on Web site of securities authority and rating agency.

Ratings need to bedisclosed on theCONASEV Website and on therating agency’s Web site.

Pakistang 0 2 All microfinancebanks must be rated within three years of grant of license or within one year of commencement of deposit mobilization, whichever is earlier.

Rating agency mustbe on the panel of the State Bank of Pakistan (SBP) or bean internationalmicrofinance rating agency with priorapproval from SBP.

Ratings alsorequired forcommercial banks.

Nigeriah 0 0 An NGO-MFIseeking to transforminto a microfinancebank is “required toprovide anInstitutional Assessment by arating agency with

Not applicable Banks wishing tomanage Nigeria’sexternal reservesmust meetminimum requiredratings by two of the threemainstream credit

29

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 30/32

specialization in microfinancing.”

risk rating.agenciesi

a Unless otherwise noted, information for Bolivia, Ecuador, and Peru is from Enrique Diaz Ortega, “MFIrating: Some Latin American experiences in a regulated environment,” III Rating Forum, Quito, Ecuador,September 12-13, 2006.b Each mandatory rating is produced four times per year.c Author correspondence with Enrique Diaz Ortega, microfinance consultant.d Author correspondence with Massimo Vita, Microfinanza Rating.e Informative profile, MFI regulation and supervision in Peru,http://www.microfinancegateway.org/resource_centers/reg_sup/micro_reg/country/36/ f Each mandatory rating is produced two times per year.g Credit risk rating of Microfinance Banks, Prudential Regulation 29 for Microfinance Banks, State Bank of Pakistan, BSD Circular No. 10 of 2003, http://www.sbp.org/pk/bsd/2003/C10.htmh “Regulatory and Supervisory Framework for Microfinance Banks (MFBs) in Nigeria,”http://www.cenbank.org/OUT/PUBLICATIONS/GUIDELINES/DFD/2006/REGULATORY%20GUIDELINES.PDFi “Recent Developments in Nigeria’s financial system, IFLR1000 Country Reports,”http://www.iflr1000.com/default.asp?page=38&CH=3&sIndex=2&CountryID=95

30

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 31/32

Appendix 3: Regional Microfinance Rating Markets

Latin America and the Caribbean (LAC) The LAC market remained the largest MFI rating market in 2006, having increased by 33ratings to a total of 208 ratings. Bolivia accounted for most of the growth. Bolivia is the

region’s second largest market, where the number of ratings jumped from 37 in 2005 to 60in 2006. Because of the multiple ratings required for regulated MFIs, these figures representratings for 14 MFIs. The primary impetus for the growth in Bolivia was the expansion of Fitch Ratings into providing ratings for unregulated MFIs; previously its work consisted of mandatory MFI ratings for regulated MFIs. The fact that unregulated MFIs had a voluntary interest in being rated may indicate the positive impact of mandatory ratings on marketdevelopment.

The Peruvian market continued to be the largest market in the LAC region, accounting for86 of a total of 208 ratings in 2006. The Peruvian market may be one of the few markets tohave reached a maturity level; the number of ratings did not change between 2005 and 2006.Fourteen of the 2006 ratings were mandatory.

There were two particularly noteworthy shifts in LAC during 2006. First, the number of ratings in Ecuador increased from four to 17; over half of the 2006 ratings were completedby Microfinanza Rating, which opened an office in Ecuador in 2006 and became thecountry’s first authorized MFI rating agency. The fact that establishing an in-country presence led to such a significant increase in rating clients underscores the growth potentialof at least some markets. Second, the number of ratings in Haiti decreased from 12 to one. The Haitian National Network of Microfinance Institutions had encouraged all of itsmembers (18) to undergo institutional diagnostics(funded by USAID) in 2005. Theinstitutional strengthening programs that resulted are currently being implemented, withfollow-up ratings or assessments planned for the end of the process.

Asia Asia showed considerably less growth than LAC in 2006—a net increase of eightassessments—largely as a result of no growth in its largest market, India (70 of 111 ratings). This situation is expected to change in 2007, because some mandates awarded in 2006 werenot completed until 2007. Nevertheless, because the Indian market is already highly penetrated, large increases in the number of Indian MFI assessments are not anticipated.

A new development in the 2005–06 period has been the emergence of PRIME, an MFIrating agency in Indonesia.

Sub-Saharan Africa (SSA) There was an absolute increase of six assessments in SSA in 2006, resulting in 30 ratings intotal for the year. This relatively underdeveloped market may grow in the future as moreprivate investors become active in the region and as specialized rating agencies increase theiron-the-ground presence.

Uganda provides a possible road map for the future. Ugandan MFIs have been the biggestissuer of ratings since 1999, with seven of the 26 ratings having been issued in 2006. Theincrease in 2006 was largely because of an initiative by the local rating fund to finance mini-

31

7/31/2019 The Microfinance Rating Market Outlook_2007_updated

http://slidepdf.com/reader/full/the-microfinance-rating-market-outlook2007updated 32/32

assessments. Mali also showed significant growth in 2006, registering nine ratings in 2006,compared to a total of three ratings in the previous seven years. These ratings were financedby USAID and the World Bank. The question for the future is whether these donor-fundedratings ultimately translate into increased market-generated demand for ratings.

Eastern Europe and Central Asia (EECA) The EECA region showed noteworthy growth in 2006, with the number of assessmentsincreasing from 19 to 37.

The two most significant users of assessments in the region were Bosnia and Herzegovinaand Russia. Bosnia and Herzegovina has had a total of 20 assessments since 1999, of whichfive were completed in 2006. The fact that three of these assessments were repeat exercisesreflects their perceived usefulness. Russia has had a total of 15 assessments, of which eight were completed in 2006. This growth reflects increased MFI activity in Russia, with one MFIhaving recently converted to a bank and another receiving the first license to be supervisedby the Central Bank as a non-bank MFI.

Several rating agencies mentioned in interviews that this region interests them; therefore thegood growth results of 2006 are likely to be repeated.

Middle East and North America (MENA) MENA represents the smallest market in terms of the estimated number of MFIs. This isreflected in the number of assessments, which grew from six in 2005 to 17 in 2006. It seemsunlikely that the dynamics in this region will change significantly unless there is a largeincrease in the number of MFIs.

Morocco is by far the biggest issuer of assessments; it accounts for half of the microfinance

borrowers in the region. Twenty-one of the region’s 39 assessments over the past sevenyears have been for Moroccan MFIs. Seven of these ratings were completed in 2006. Withfour ratings completed in Morocco in 2005, this is an encouraging trend.

The most noteworthy development in 2006 was the inception of an Islamic DevelopmentBank project in Palestine that led to the issuance of eight MFI assessments. These were thefirst MFI assessments to take place in Palestine.