© The McGraw-Hill Companies, Inc., 2008 McGraw-Hill/Irwin Merchandising Activities Chapter 6.

Upload

imogene-dayCategory

view

217download

0

©The McGraw-Hill Companies, Inc. 2006McGraw-Hill/Irwin

Chapter Six

Accounting for Merchandising Businesses—Advanced Topics

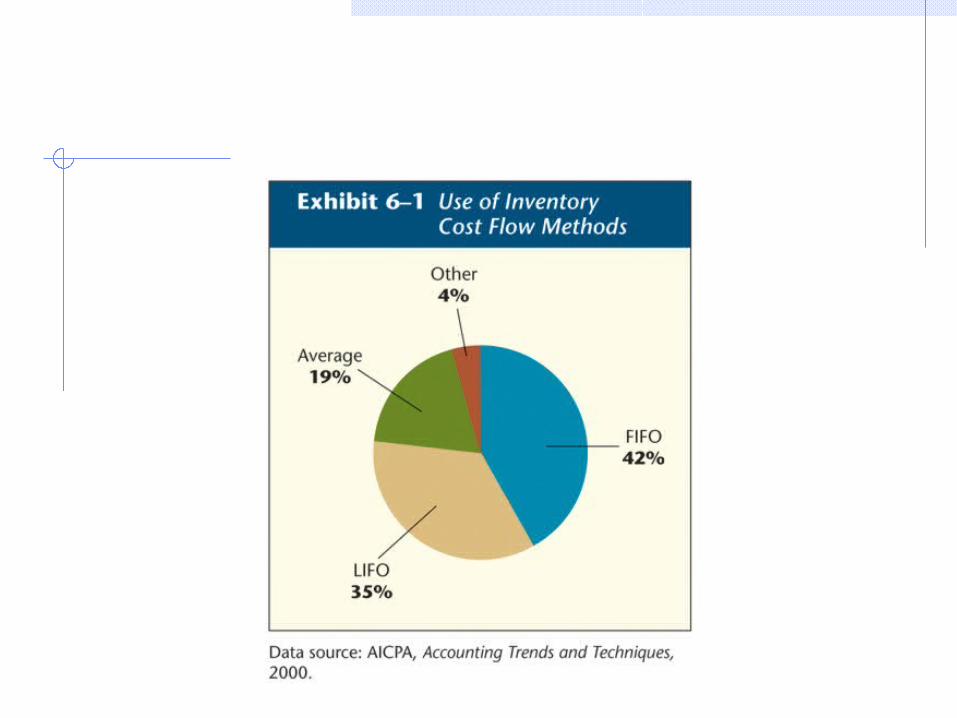

Inventory Cost Flow Methods

Four Common Inventory Cost Flow Methods

Specific Identificatio

n

First-in, First-Out

(FIFO)

Last-in, First-Out

(LIFO)

Weighted Average

Specific Identification

When a company’s inventory consists

of many high-priced, low-

turnover goods the record keeping

necessary to use specific

identification is more practical.

Specific Identification

Assume Baker Company purchased two identical inventory items: the first for $100 and the second

for $110.

Using specific identification, when the first item is sold, cost of

goods sold would be $100. When the second item is sold, cost of goods sold

would be $110.

First-in, First-out

The first-in, first-out cost flow

method requires that the cost of the

items purchased first be assigned to Cost of Goods Sold.

First-in, First-out

Assume Baker Company purchased two identical inventory items: the first for $100 and the second

for $110.

Using first-in, first-out, the cost assigned to the first item sold would be $100

(the first cost in). The cost of goods sold assigned to

the second item sold would be $110.

Last-in, First-out

The last-in, first-out cost flow

method requires that the cost of the

items purchased last be assigned to Cost of Goods Sold.

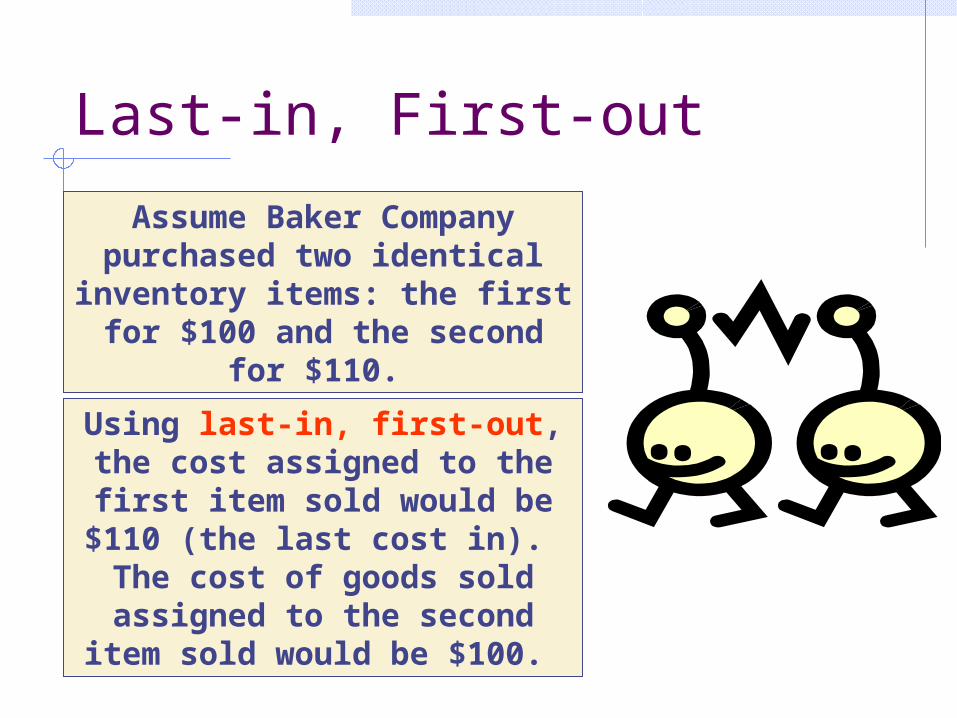

Last-in, First-out

Assume Baker Company purchased two identical inventory items: the first for $100 and the second

for $110.

Using last-in, first-out, the cost assigned to the first item sold would be $110

(the last cost in). The cost of goods sold assigned to

the second item sold would be $100.

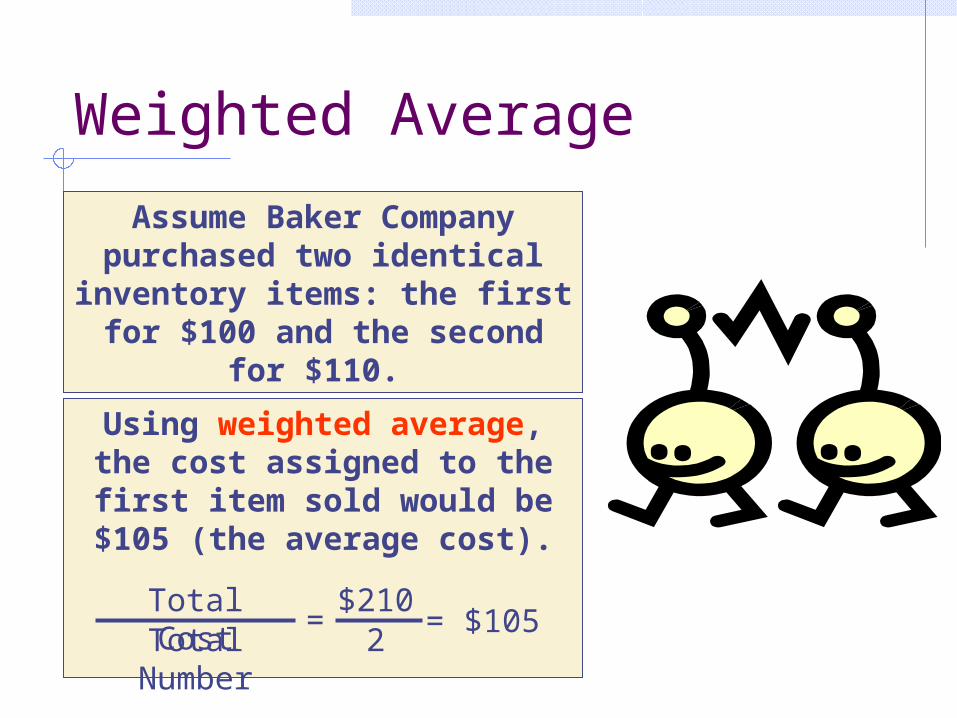

Weighted Average

The weighted average cost flow

method assigns the average cost of the items available to

Cost of Goods Sold.

Weighted Average

Assume Baker Company purchased two identical inventory items: the first for $100 and the second

for $110.

Using weighted average, the cost assigned to the first item sold would be $105 (the average cost).

Total CostTotal

Number

=$210

2= $105

Physical Flow

Our discussions about inventory cost flow

methods pertain to the flow of costs through

the accounting records, not the actual physical flow of goods.

Cost flows can be done on a different basis than physical flow.

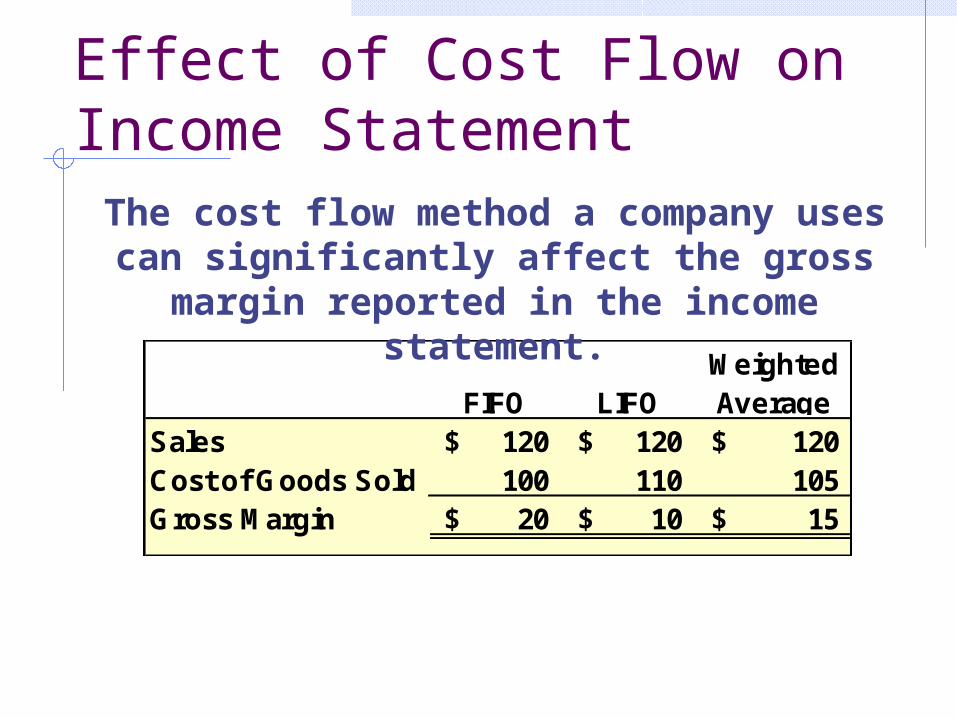

Effect of Cost Flow on Income Statement

FIFO LIFOWeighted Average

Sales 120$ 120$ 120$ Cost of Goods Sold 100 110 105 Gross Margin 20$ 10$ 15$

The cost flow method a company uses can significantly affect the gross margin reported in the income

statement.

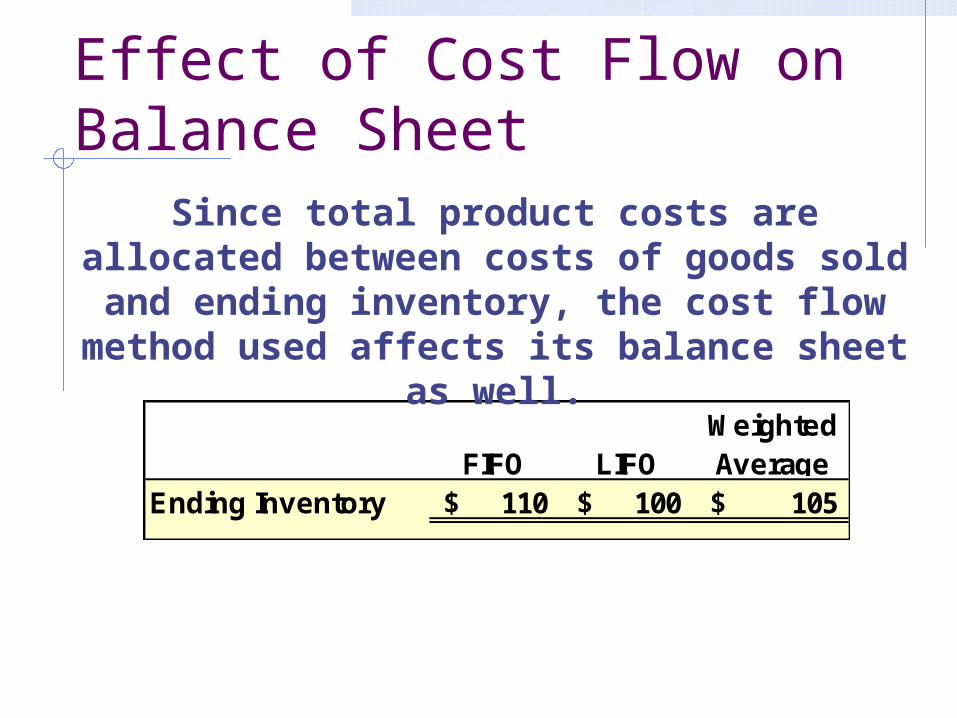

Effect of Cost Flow on Balance Sheet

FIFO LIFOWeighted Average

Ending Inventory 110$ 100$ 105$

Since total product costs are allocated between costs of goods sold and

ending inventory, the cost flow method used affects its balance sheet as well.

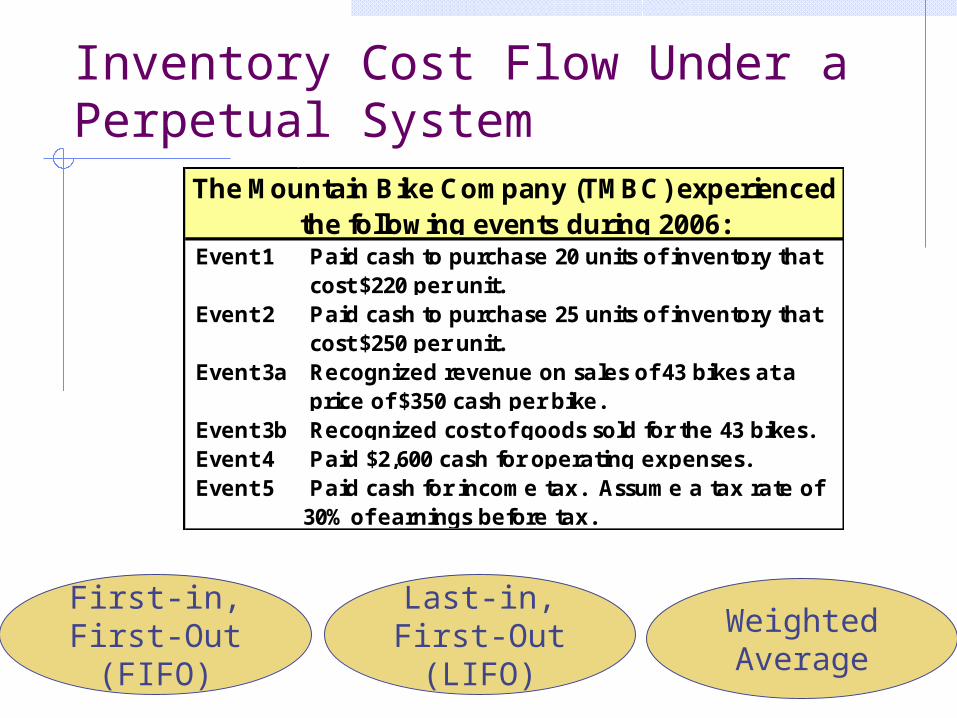

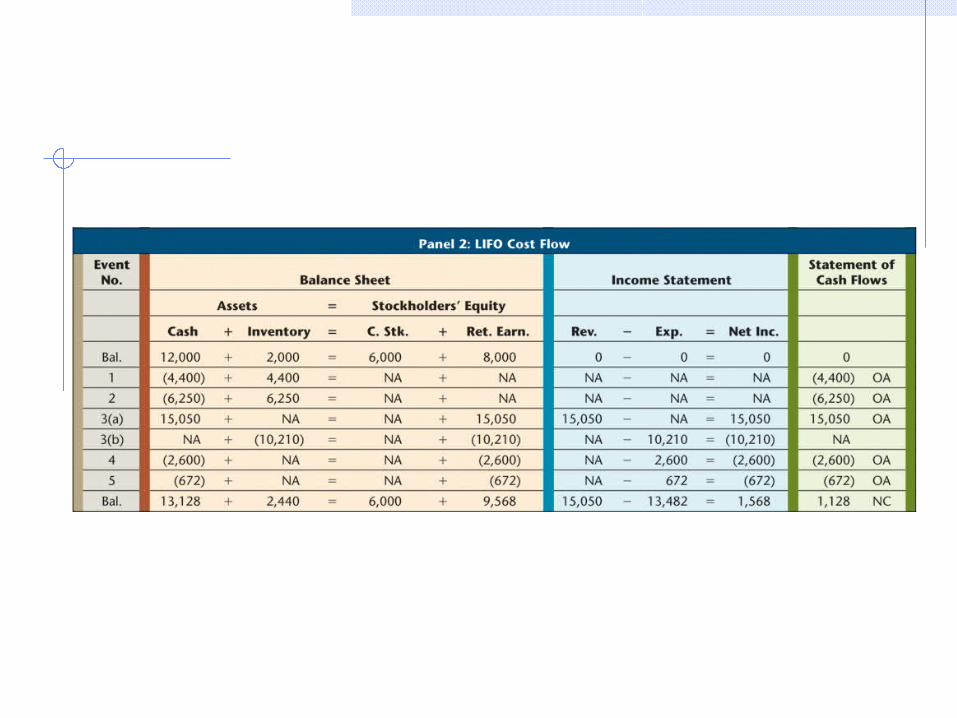

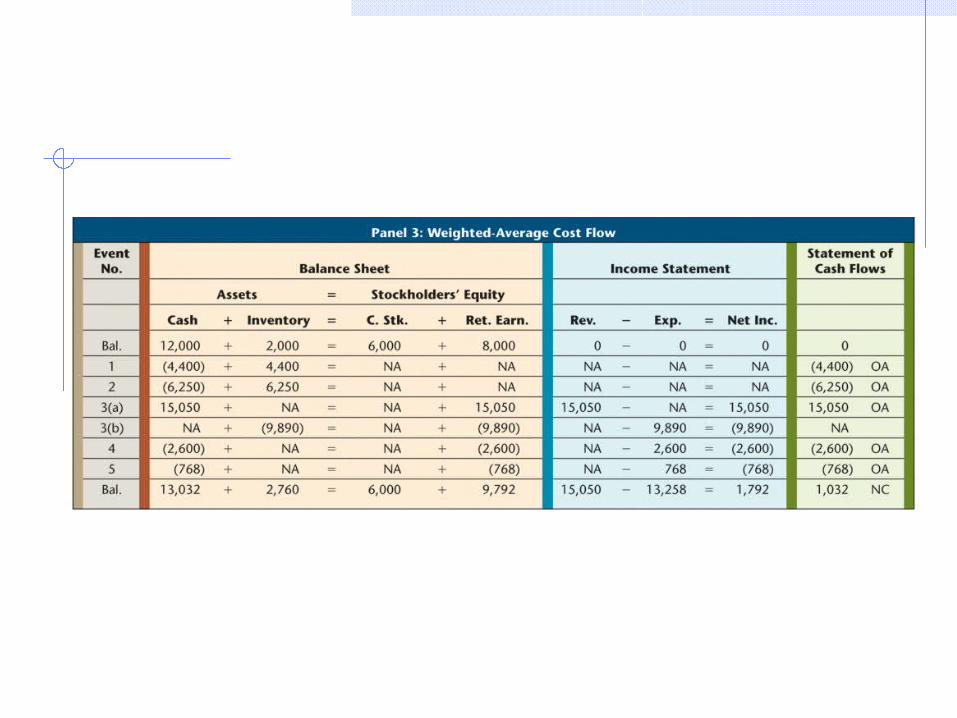

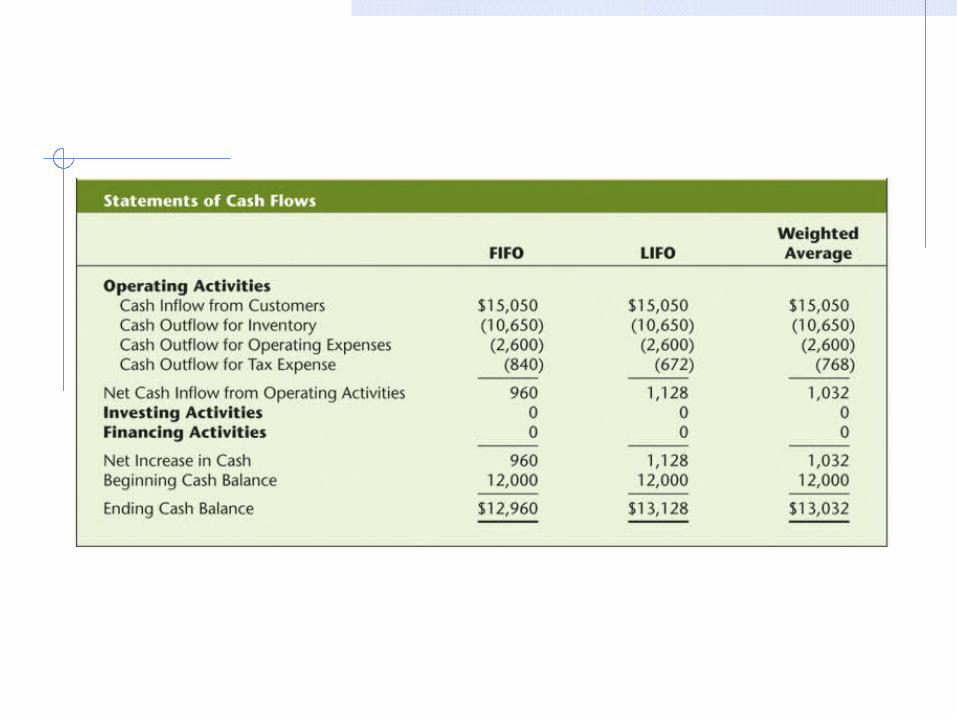

Inventory Cost Flow Under a Perpetual System

Event 1 Paid cash to purchase 20 units of inventory that cost $220 per unit.

Event 2 Paid cash to purchase 25 units of inventory that cost $250 per unit.

Event 3a Recognized revenue on sales of 43 bikes at a price of $350 cash per bike.

Event 3b Recognized cost of goods sold for the 43 bikes. Event 4 Paid $2,600 cash for operating expenses. Event 5 Paid cash for income tax. Assume a tax rate of

30% of earnings before tax.

The Mountain Bike Company (TMBC) experienced the following events during 2006:

First-in, First-Out

(FIFO)

Last-in, First-Out

(LIFO)

Weighted Average

First-in, First-out Inventory Cost Flow

Jan. 1 Beginning inventory 10 units @ 200$ = 2,000$ Mar. 18 First purchase 20 units @ 220$ = 4,400 Aug. 21 Second purchase 13 units @ 250$ = 3,250 Total cost of the 43 bikes sold 9,650$

FIFO Cost of Goods Sold

Cost of goods sold is an expense and, thus, decreases

net income.

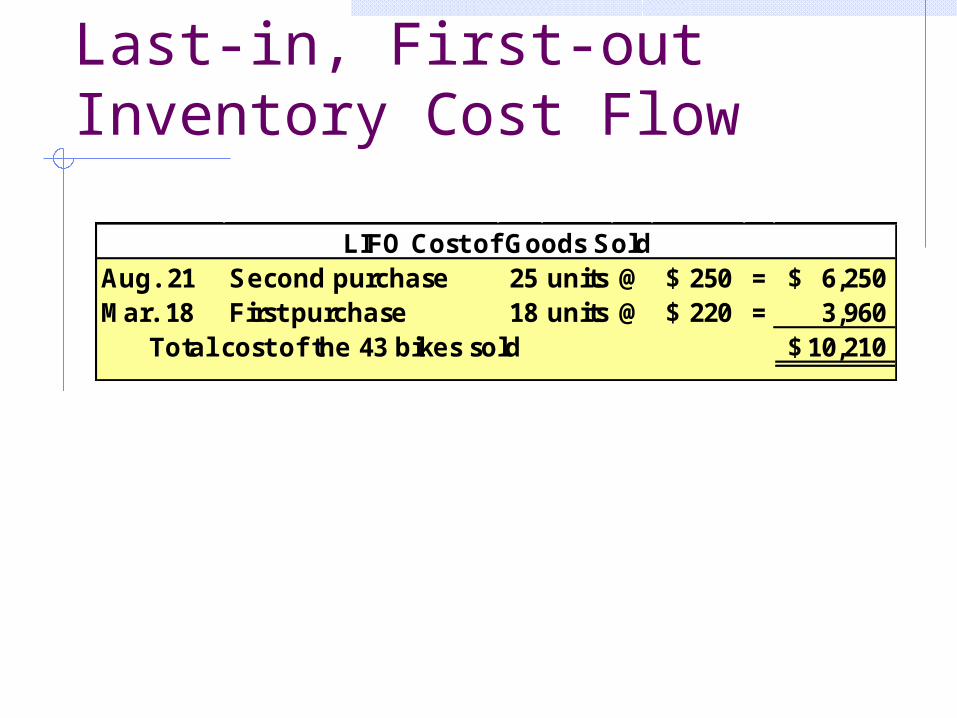

Last-in, First-out Inventory Cost Flow

Aug. 21 Second purchase 25 units @ 250$ = 6,250$ Mar. 18 First purchase 18 units @ 220$ = 3,960 Total cost of the 43 bikes sold 10,210$

LIFO Cost of Goods Sold

Weighted Average Inventory Cost Flow

Total cost of the 43 bikes sold 43 units @ 230$ = 9,890$ Weighted Average Cost of Goods Sold

Total CostTotal

Number

=$12,650

55= $230

Inventory Cost Flow When Sales and Purchases Occur Intermittently

In our previous examples, all

purchases were made before any goods were

sold. This section addresses more

realistic conditions when sales

transactions occur intermittently with

purchases.

Sharon Sales Company (SSC)

Date TransactionJan. 1 Beginning inventory 100 units @ 20.00$ = 2,000$ Feb. 14 Purchased 200 units @ 21.50$ = 4,300 Apr. 5 Sold 220 units @ 30.00$ = 6,600 June 21 Purchased 160 units @ 22.50$ = 3,600 Aug. 18 Sold 100 units @ 30.00$ = 3,000 Sept. 2 Purchased 280 units @ 23.50$ = 6,580 Nov. 10 Sold 330 units @ 30.00$ = 9,900

Sharon Sales CompanyDescription

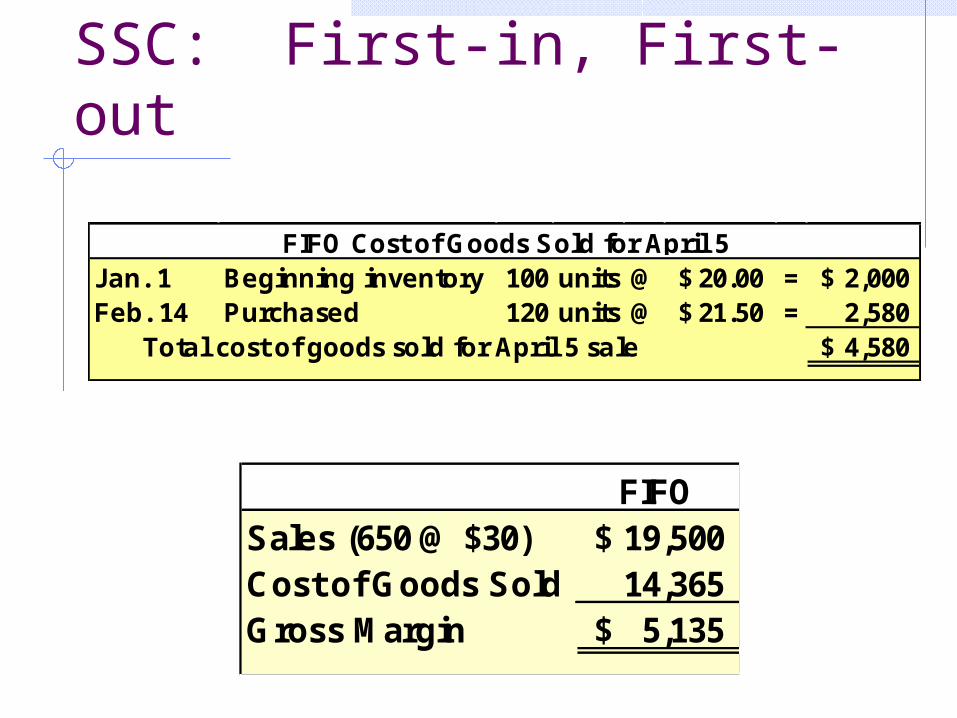

Let’s use FIFO to determine the cost of goods sold and inventory for SSC at the end of 2008.

This table describes the beginning inventory, purchases, and sales transactions for SSC during

2008.

SSC: First-in, First-out

FIFOSales (650 @ $30) 19,500$ Cost of Goods Sold 14,365 Gross Margin 5,135$

Jan. 1 Beginning inventory 100 units @ 20.00$ = 2,000$ Feb. 14 Purchased 120 units @ 21.50$ = 2,580 Total cost of goods sold for April 5 sale 4,580$

FIFO Cost of Goods Sold for April 5

Weighted Average and LIFO Cost FlowsWhen

maintaining perpetual inventory

records, using the weighted

average or LIFO cost flow

methods leads to timing

difficulties.

Further discussion of these methods

is beyond the scope of this text.

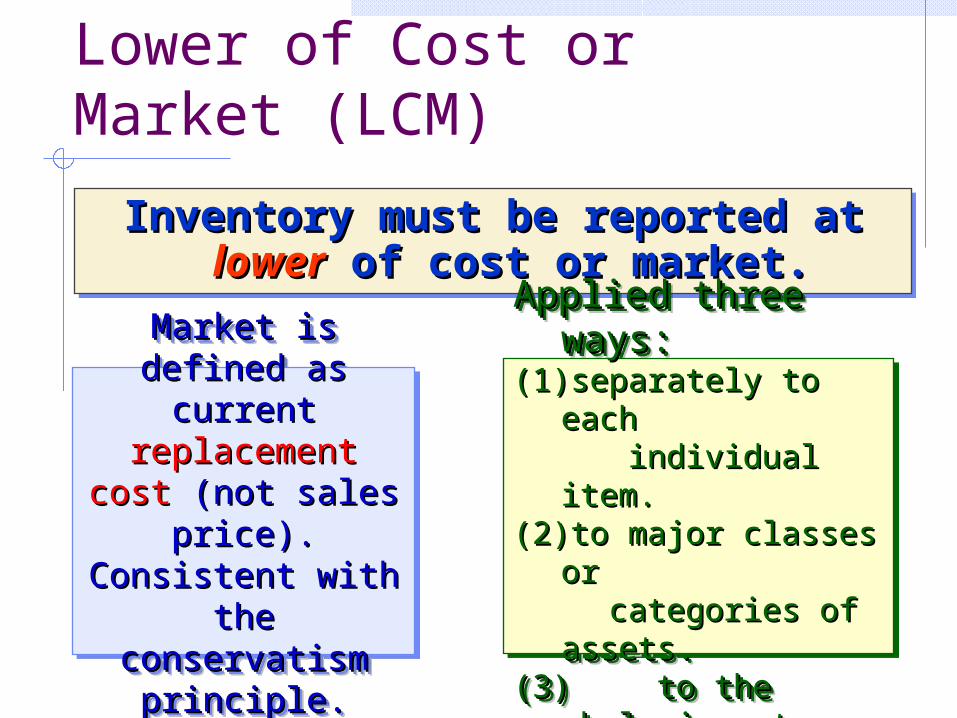

Lower of Cost or Market (LCM)

Inventory must be reported at Inventory must be reported at lowerlower of cost or market.of cost or market.

Inventory must be reported at Inventory must be reported at lowerlower of cost or market.of cost or market.

Applied three ways:Applied three ways:(1)(1) separately to each separately to each individual item.individual item.(2)(2) to major classes or to major classes or categories of assets.categories of assets.(3)(3) to the whole inventory.to the whole inventory.

Applied three ways:Applied three ways:(1)(1) separately to each separately to each individual item.individual item.(2)(2) to major classes or to major classes or categories of assets.categories of assets.(3)(3) to the whole inventory.to the whole inventory.

Market is defined as Market is defined as current current replacement replacement

costcost (not sales (not sales price).price).

Consistent withConsistent withthe conservatismthe conservatism

principle.principle.

Market is defined as Market is defined as current current replacement replacement

costcost (not sales (not sales price).price).

Consistent withConsistent withthe conservatismthe conservatism

principle.principle.

Lower of Cost or Market (LCM)

To illustrate lower of cost or market, To illustrate lower of cost or market, assume Wilson Office Supply Company assume Wilson Office Supply Company has in ending inventory 100 calculators has in ending inventory 100 calculators

purchased at a cost of $14 each. purchased at a cost of $14 each.

To illustrate lower of cost or market, To illustrate lower of cost or market, assume Wilson Office Supply Company assume Wilson Office Supply Company has in ending inventory 100 calculators has in ending inventory 100 calculators

purchased at a cost of $14 each. purchased at a cost of $14 each.

Cost Market LCMSituation 1 14$ 18$ 14$ Situation 2 14$ 11$ 11$

Fraud Avoidance in Merchandising Businesses

Because inventory and cost of goods sold accounts are so significant, they are

attractive targets for concealing fraud.

Because of this, auditors and financial analysts carefully examine them for signs of

fraud.

Fraud Avoidance in Merchandising Businesses

Ending Inventory is

Accurate

Ending Inventory is Overstated

Beginning Inventory 4,000$ 4,000$ Purchases 6,000 6,000 Cost of Goods Aval. for Sale 10,000 10,000 Ending Inventory (3,000) (4,000) Cost of Goods Sold 7,000$ 6,000$

Sales 11,000$ 11,000$ Cost of Goods Sold (7,000) (6,000) Gross Margin 4,000$ 5,000$

Ending Inventory is

Accurate

Ending Inventory is Overstated

Assets Cash 1,000$ 1,000$ Inventory 3,000 4,000 Other Assets 5,000 5,000 Total Assets 9,000$ 10,000$

Stockholders' EquityCommon Stock 5,000$ 5,000$ Retained Earnings 4,000 5,000 Total Stockholders' Equity 9,000$ 10,000$

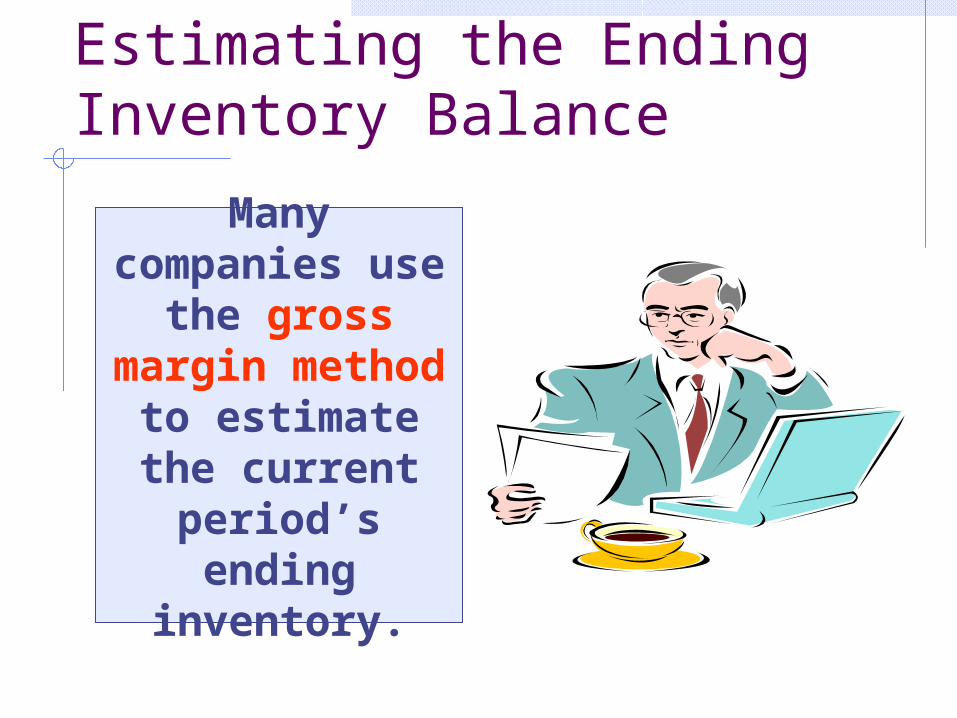

For interim financial statements, we may need to estimate ending inventory and cost of goods sold.

Estimating the Ending Inventory Balance

Many companies

use the gross margin

method to estimate the

current period’s ending

inventory.

Calculate the expected gross margin ratio using prior period’s financials.

Multiply the expected gross margin ratio by the current period’s sales to estimate the amount of gross margin.

Subtract the estimated gross margin from sales to estimate cost of goods sold.

Subtract the estimated cost of goods sold from the amount of goods available for sale to estimate the ending inventory.

Calculate the expected gross margin ratio using prior period’s financials.

Multiply the expected gross margin ratio by the current period’s sales to estimate the amount of gross margin.

Subtract the estimated gross margin from sales to estimate cost of goods sold.

Subtract the estimated cost of goods sold from the amount of goods available for sale to estimate the ending inventory.

The Gross Profit Method

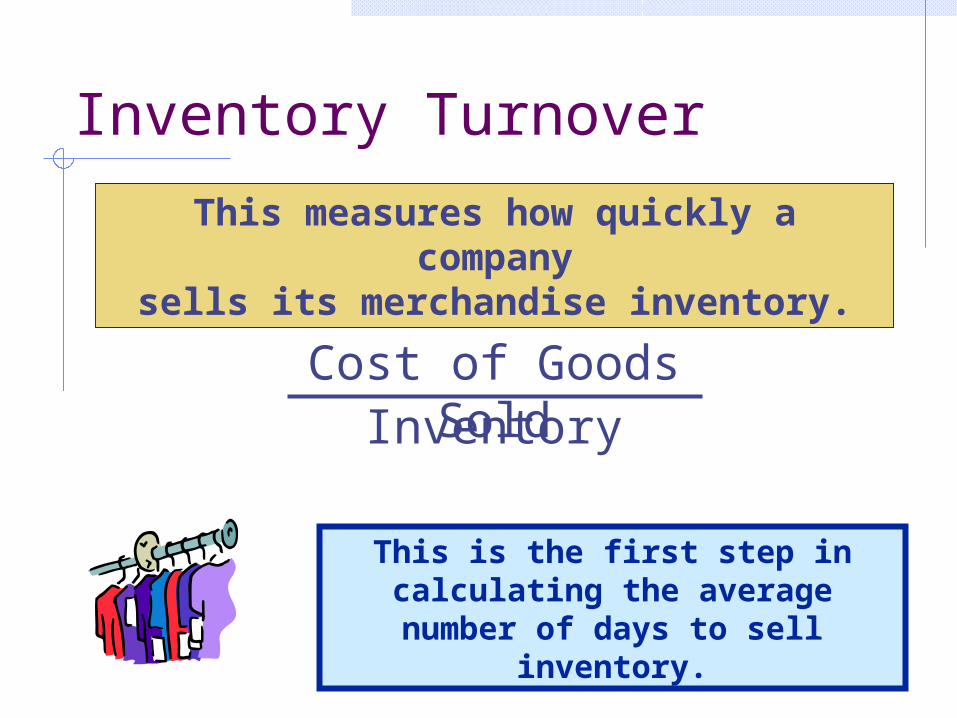

Inventory Turnover

Cost of Goods SoldInventory

This measures how quickly a company

sells its merchandise inventory.

This is the first step in calculating the average number of days to sell

inventory.

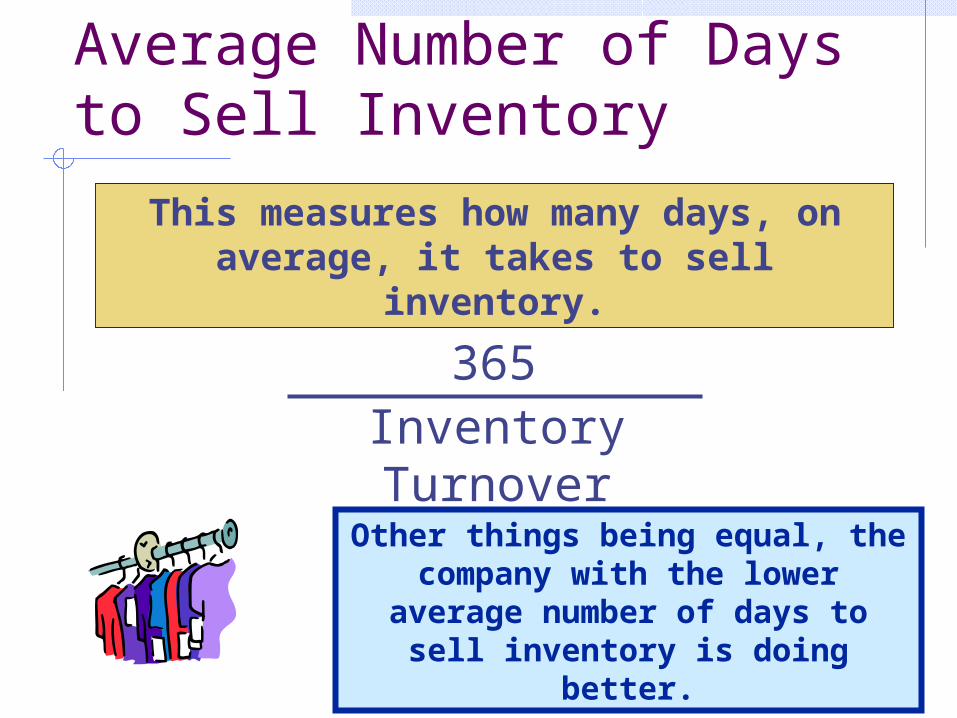

Average Number of Days to Sell Inventory

365Inventory Turnover

This measures how many days, on average, it takes to sell inventory.

Other things being equal, the company with the lower average

number of days to sell inventory is doing better.

End of Chapter Six