“The Life Insurance Industry in Malaysia”olis.or.jp/e/pdf/20171025_Moheeb.pdf · 2018-01-08 ·...

21

“The Life Insurance Industry in Malaysia” Syed Moheeb CEO, The Malaysian Insurance Institute OLIS 50 th Anniversary Symposium

Transcript of “The Life Insurance Industry in Malaysia”olis.or.jp/e/pdf/20171025_Moheeb.pdf · 2018-01-08 ·...

“The Life Insurance Industry in Malaysia”

Syed Moheeb

CEO, The Malaysian Insurance Institute

OLIS 50th Anniversary Symposium

2

Life Insurance Companies in Malaysia About LIAM

The Life Insurance Association of Malaysia (LIAM) is a trade association registered under the Societies Act 1966.

LIAM has 16 Member Companies: 10 pure life companies 4 composite companies 2 life reinsurance companies

Penetration Rate: 54.6% Life Insurance & Family Takaful

48.0 49.7 51.6 51.6 52.2 53.5 54.5 54.9 54.9 54.6

40.3 41.8 42.4 40.5 39.6 40.5 40.7 40.6 40.3 39.9

7.8 7.9 9.2 11.1 12.6 12.9 13.8 14.3 14.7 14.6

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

%

Year

Total Penetration Rate Conventional Family Takaful

3

Penetration Rate – Past & Present

4

77,736

18,652

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Individually Tied Agents Bank Staff

No. of Intermediaries (as at 30 June 2017)

Source : LIAM Statistics

Current State of Insurance Industry

Individual Agents Bancassurance

POS Assurance Direct Distribution :

Online / Mobile Insurance Direct Distribution : Walk-in to Branch

Financial Advisors

5

Distribution Channels

National Agenda :

75% Malaysians with Life Insurance /Takaful By 2020

Penetration Target

• Support long-term growth & development of the life insurance & family takaful industry

• Provide conducive environment for greater penetration while protecting consumers’ interest and needs

• Initiatives under the Framework are categorised into 3 areas:

i. Greater operational flexibility for insurers & takaful operators to promote competitive environment and product innovation

ii. Diversification of product distribution channels to widen outreach to increase insurance & takaful

penetration

iii. Strengthening market practice to enhance consumers’ protection through instilling

greater professionalism in the industry

6

Objectives of LIFE Framework

Access – Developing a Viable Multi-Distribution Channel Leveraging on the strength of agency channel

•Raising the quality of advice and service provided by agents • An industry-wide service guide • Implementation of the BSC through an

allocation of a portion of total remuneration to reward the right behaviours: • Increased commitment and activity

• Enhanced advisors’ competency

• Better point of sale advice to customers • Better after sales service

to achieve a more professional and productive full-time agency force leading to a higher insurance and takaful penetration rate.

Preservation of policy value

LIFE Framework : Future Landscape

7

i. Enhancement of Financial Advisers (FA) Framework • Minimum paid-up capital unimpaired

by losses reduced from RM100,000 to RM50,000 wef 1 January 2015

• Qualifying requirements – recognition of equivalent qualifications from MFPC and FPAM

• Access to full range of life insurance/family takaful products offered by life insurers/takaful operators

8

LIFE Framework : Initiatives

ii. Introduction of Service Guide from 1 July 2016 to enhance consumer awareness of financial advisory services for insurance/takaful products • Increase transparency of services

provided by intermediaries and allow consumers to be aware of, and anticipate the level of service when purchasing insurance/takaful products

Under the LIFE Framework issued by Bank Negara Malaysia (23 November 2015), various initiatives have been introduced for implementation, such as :

1 2 3

Customer Portal Please visit our Customer portal at XXXX for on-line access to your policy information

If you are not satisfied with the services of our agent, or require additional support from our Company, you may contact us at 03-xxxxxxxx

What Services can you expect from our Agent?

During the Term of the Policy

Continuous Policy Servicing

Assist in renewal of policy

Provide continuous service e.g. policy modifications, change of address and frequency of premium payments. If the agent has left the Company, we shall appoint a new agent to service you

Assist you in making a Claim

Guide you through the standard procedures on how to file an insurance claim

When you Decide to Buy a Policy

Assist you with the Policy Application

Explain the importance of answering the questions in the proposal form fully and accurately

Submit your application for underwriting after you have signed the proposal form

Arrange for medical examination with one of our panel clinics, if required

Provide information on making a nomination to ensure policy moneys are received by your beneficiaries in the event of death

Explain the Policy Terms and Conditions

Your policy document will be delivered to you (by hand or via post) within xx days

Go through the policy terms and conditions with you to ensure that this is the right plan that you have purchased

Before you Buy a Policy

Assist you in Choosing the Right Insurance Plan

Go through with you the Customer Fact Find form to understand your insurance needs and financial goals

Recommend suitable insurance plan after assessing your needs

Explain Product Features

Explain the product features, benefits payable, exclusions, premiums and charges

Provide Product Disclosure Sheet to assist you in making informed decision and to facilitate product comparison

Deal only with registered agents

You can check the status of the agent via the Life Insurance Association of Malaysia’s (LIAM) website or via Short Message Service (SMS). Visit http://www.liam.org.my/index.php/customer-zone/know-your-agent for more details.

iii. Availability of Online Account Facilities • Online access to insurance/takaful accounts

for policyowners/takaful participants wef 1 July 2016

• Access to information on • status of policies/certificates • real-time updates to policy/certificate details • download forms for transactions

iv. Direct Distribution Channels for Pure Protection Products

• All insurers/family takaful operators required to offer commission-free standalone pure protection products i.e. term, critical illness and medical and health insurance/takaful through at least one direct channel i.e. online website or walk-in to Head Office/branch

• 1 July 2017 – pure protection term products • 1 July 2018 - pure protection critical illness

and pure protection medical and health products

10

LIFE Framework : Initiatives

v. Direct Distribution Channels for Pure Protection Products

All insurers/family takaful operators required to offer commission-free standalone pure protection products i.e. term, critical illness and medical and health insurance/takaful through at least one direct channel i.e. online website or walk-in to Head Office/branch • 1 July 2017 – pure protection term products • 1 July 2018 - pure protection critical illness and

pure protection medical and health products

27.0 25.5 15.6 10.0 10.0

88.1

0.020.040.060.080.0

100.0

Balanced Score Card Name : ABC Year : 2015

BSC SCORE :

vi. Introduction of product comparator

• To help consumers compare suitable life insurance/family takaful products offered by different life insurers/family takaful operators

• Financial education website with self-assessment tool / financial calculator will be introduced in Phase 1 and product comparator in Phase 2

11

LIFE Framework : Initiatives

Information online: Product Comparator to Shop and Compare

vii. Limits under Agency Financing Scheme (AFS)

• Limits on AFS removed wef 1 December 2015

• Any credit facility granted by life insurer/family takaful operator to its agent shall continue to be provided only from the life insurer’s/family takaful operator’s shareholders’ fund

• The relevant capital requirements on credit facilities in the RBC framework, will continue to apply.

12

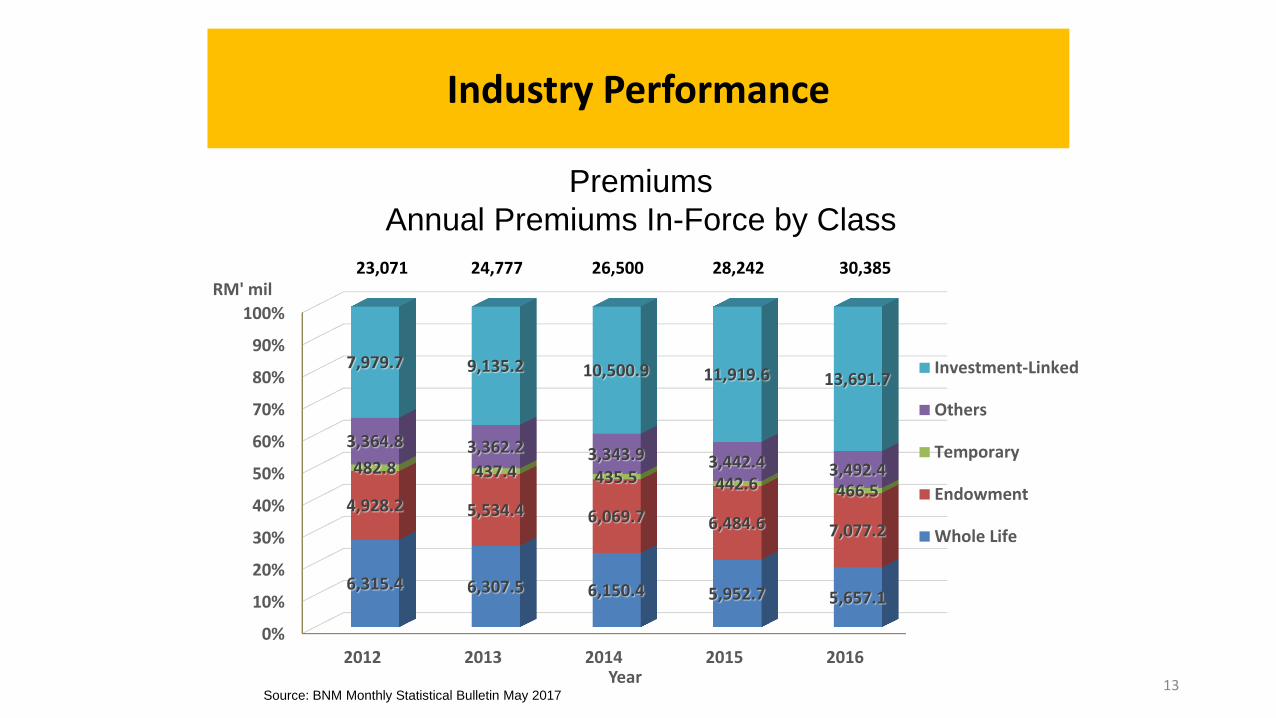

Premiums

New Business by Class

Source: BNM Monthly Statistical Bulletin May 2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

609.7 562.6 363.4 282.2 276.9

1,311.7 1,351.7 1,593.2 1,536.0 1,981.3

1,631.8 1,819.7 1,931.6 1,874.7 1,787.2

1,316.9 1,042.5 1,075.1 1,606.4 1,756.7

3,325.5 3,347.8 3,950.4 3,612.0 3,764.1

5.5 42.9 35.6 196.2 181.4

RM' mil

Year

Annuity

Investment-Linked

Others

Temporary

Endowment

Whole Life

8,201 8,167 8,949 9,107 9,748

Performance of Life Insurance Industry

13

Premiums

Annual Premiums In-Force by Class

Source: BNM Monthly Statistical Bulletin May 2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

6,315.4 6,307.5 6,150.4 5,952.7 5,657.1

4,928.2 5,534.4 6,069.7 6,484.6 7,077.2

482.8 437.4 435.5 442.6 466.5

3,364.8 3,362.2 3,343.9 3,442.4 3,492.4

7,979.7 9,135.2 10,500.9 11,919.6 13,691.7

RM' mil

Year

Investment-Linked

Others

Temporary

Endowment

Whole Life

23,071 24,777 26,500 28,242 30,385

Industry Performance

14

Sums Insured In-Force by Class

Source: BNM Monthly Statistical Bulletin May 2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

193,895.3 194,644.4 192,575.5 189,731.1 187,258.9

70,326.2 70,924.5 69,743.9 69,043.7 75,357.2

446,901.6 480,723.7 499,327.5 527,969.7 524,130.4

62,278.5 58,735.7 72,549.5 75,528.6 72,740.6

248,305.3 284,679.2 330,825.3 376,173.9 440,278.4

200.1 267.6 318.0 348.6 392.9

RM

(m

illio

ni)

Year

Annuity

Investment-Linked

Others

Temporary

Endowment

Whole Life

1,021,907 1,089,975 1,165,340 1,238,796 1,300,158

Performance of Life Insurance Industry (3)

Key Findings:

1. Many Malaysian households are substantially underinsured. The average protection gap for families whose primary wage earner have both life and medical insurance was RM553,000 per family (to last for at least 5 years).

2. Families whose primary wage earner was covered by life policy only and not medical policy, had a slightly higher gap, at RM642,000 per family

3. The average protection gap for the group headed by a breadwinner who was not covered by either life or medical insurance was largest, at about RM723,000 per family.

4. The average mortality gap for each member of a family was between RM100,000 to RM150,000

• Hence, there exists a vast potential for growth in the Life insurance market. The results of this study are expected to spur the insurance industry to move forward in achieving the targeted penetration rate of 75% by 2020 under the Economic Transformation Plan

15

Protection Gap Study 2012/2013

LIAM conducted a study in 2013 to examine the potential mortality gap among Malaysian families in 2012 whose main wage earners were either insured under life and medical insurance, or not insured under either policy.

16

• To promote good business practice, professional standards and fair competition among insurance companies.

• A self-monitoring mechanism has been put in place and the CEOs are required to submit a statement of compliance to the Association and Bank Negara Malaysia.

• Breach of Association rules will subject an insurance company to a fine not exceeding RM200,000.00.

Self-Regulatory Measures

17

Self-Regulatory Measures

Guideline Objective

Professionalism of Agents - Minimum Qualitative Criteria for Life Agency Force

To set industry standards on recruitment and promotion of agents, maintenance of contract, education requirements and continuing professional development.

Replacement of Policies

To discourage twisting of policies and mis-selling.

Rule on Pinching of Agents

To prevent mass migration or buying of agency leaders.

Guideline Objective

Code of Ethics & Conduct

To promote and maintain the highest degree of standards and integrity among employees and intermediaries in the life insurance sector.

Treat Customers Fairly (TCF)

To ensure that the policyholders are treated fairly from the prospecting stage to the end of the contractual relationship.

Client Charter To further enhance consumer protection and raise the standard of the industry’s customer service.

Joint Insurance-Takaful Council (JITC)

To promote consistency in the rules, regulations and guidelines in the life insurance, takaful and general insurance business sectors , and to provide a mechanism for the resolution of any inter-sector disputes and complaints and the conduct of enquiries on any inter-sector disputes and complaints

18

• The basic criteria for recruitment of agents are:

• Minimum 18 years old and Minimum SPM/MCE qualification (O-Level)

• Must pass the Pre-Contract Examination for Insurance Agents (PCEIA) and Certificate Examination in Investment-Linked Life Insurance (CEILLI) conducted by the Malaysian Insurance Institute (MII)

• Must be registered with LIAM through his/her insurance company

• Must not be an undischarged bankrupt

• Training and Education

• New agents must complete 30 hours of training within first 12 months of appointment and 20 hours of training in the 2nd year of appointment.

• The 1st year syllabus covers :-

• Legal aspects of insurance (Nomination, Assignment, Estate distribution, Basic Principles of Insurance – insurable interest, incontestable clause, cooling off period etc.

• Technical product knowledge

• Treat Customer Fairly and Life Insurance Sales Cycle

• Effective Self-Management

• Regulatory Requirements such as Replacement of Policies, Anti-money laundering, Professional ethics and conduct, Guidelines on Product Transparency and Disclosure etc.

Minimum Qualitative Criteria

• The 2nd year syllabus covers :- • Basic Time Value of Money Knowledge, • Simple Fact Finding Process, • Intermediate Insurance Selling Skills, • Effective Prospecting

• Agents who have been in the industry for more than one year are required to undergo 30 Continuing Professional Development (CPD) hours as well as to attend Module 1 and 2 of the Registered Financial Planner (RFP) programme.

• The RFP is the first local financial planning programme developed in Malaysia which provides practitioners with skills and knowledge that are readily applicable to other sectors such as client relations, risk management and personal finance.

• The Basic Agency Management Course (BAMC) is a 30-hour training programme designed to equip potential agency leaders with sound management skills.

• All agents are required to complete the BAMC and pass the examination prior to promotion to agency supervisors.

• Effective 2011, newly promoted agency leaders are required to complete 40 hours of training in their first year of promotion.

19

In consultation with BNM, LIAM introduced the Code of Ethics and Conduct for the life insurance industry in April 1990. It was revised and the 2nd edition was published in May 1999, following the implementation of the Insurance Act 1996.

The code is applicable to all directors (executive and non-executive), employees and intermediaries.

It is aimed at promoting and maintaining the highest degree of standards and integrity among employees and intermediaries in the life insurance industry.

Code of Ethics & Conduct

The contents and objectives comprise three parts:- Guidelines on the Code of Conduct Code of Ethics and Conduct for Life Insurance

Selling Statement of Life Insurance Practice.

Companies are required to submit a quarterly report to BNM on breaches observed very quarter of the year and the corrective or punitive actions taken.

Cases of fraud are to be reported to BNM and the police.

20

• To prevent churning or twisting of life insurance policies arising from the movement of agents.

• Conservation units must also be set up to provide advice to policyholders against the disadvantages of surrendering their policies.

• New insurer must refund premiums and old insurer must reinstate the policy if the policyholder decides to continue with old policy.

• Punitive actions taken against agents who replace policies includes:

1) forfeiture of commissions;

2) warning letter; and 3) Termination.

Replacement of Policies Rule on Pinching of

Agents

• Disallow buying over of supervisors and managers by offering higher financial incentives;

• Disallow pinching or poaching of agents from competitors.

Client Charter

• All insurers are required to post their client charter on their respective websites with effect from January 2011

• To provide value added service, greater transparency, integrity and timeliness of service to consumers

• Cultivate trustworthiness between consumers and companies.

• Commitment to combat fraud and maintain confidentiality of data.

Treating Customers Fairly

• TCF pertinent principles are three-fold

• To avoid mis-selling

• To ensure fair terms and conditions; and

• Not to restrict customers’ freedom of choice

• Specific information that must be provided to the customers during the sales process, after-sales and during the policy exit process includes minimum standard of disclosures in the form of relevant, timely, reliable, consistent and comparable information.

Joint Insurance-Takaful Council (JITC)

• To study the respective practices and existing rules, regulations and guidelines in event of any inconsistency in market practices brought to the attention of the JITC, and make recommendations to the Three(3) Sectors with a view to harmonizing the market practices;

• To make recommendations to the insurance and takaful authorities on improvements and amendments to any rules, regulations and guidelines as and when necessary;