THE LEGALITY OF INCREASES IN ROYALTY RATES AND/OR …...before the committee on fiscal policy...

76

BEFORE THE COMMITTEE ON FISCAL POLICY CONCERNING OIL AND NATURAL GAS IN ISRAEL THE LEGALITY OF INCREASES IN ROYALTY RATES AND/OR TAXES APPLICABLE TO EXISTING OIL AND NATURAL GAS RIGHTS IN ISRAEL UNDER THE U.S.-ISRAEL FCN TREATY OPINION AND MEMORANDUM OF LAW ABRAHAM D. SOFAER August 23, 2010 Committee Members: Prof. Eytan Sheshinski (Chairman) Budget Director of the Finance Ministry, Udi Nissan Head of the Israel Tax Authority, Yehuda Nasradishi Head of the National Economic Council, Prof. Eugene Kandel Director-General of the National Infrastructures Ministry, Shmuel Tzemach

Transcript of THE LEGALITY OF INCREASES IN ROYALTY RATES AND/OR …...before the committee on fiscal policy...

BEFORE THE COMMITTEE ON FISCAL POLICY

CONCERNING OIL AND NATURAL GAS IN ISRAEL

THE LEGALITY OF INCREASES IN ROYALTY RATES AND/OR TAXES

APPLICABLE TO EXISTING OIL AND NATURAL GAS RIGHTS IN

ISRAEL UNDER THE U.S.-ISRAEL FCN TREATY

OPINION AND MEMORANDUM OF LAW

ABRAHAM D. SOFAER

August 23, 2010

Committee Members:

Prof. Eytan Sheshinski (Chairman) Budget Director of the Finance Ministry, Udi Nissan Head of the Israel Tax Authority, Yehuda Nasradishi

Head of the National Economic Council, Prof. Eugene Kandel Director-General of the National Infrastructures Ministry, Shmuel Tzemach

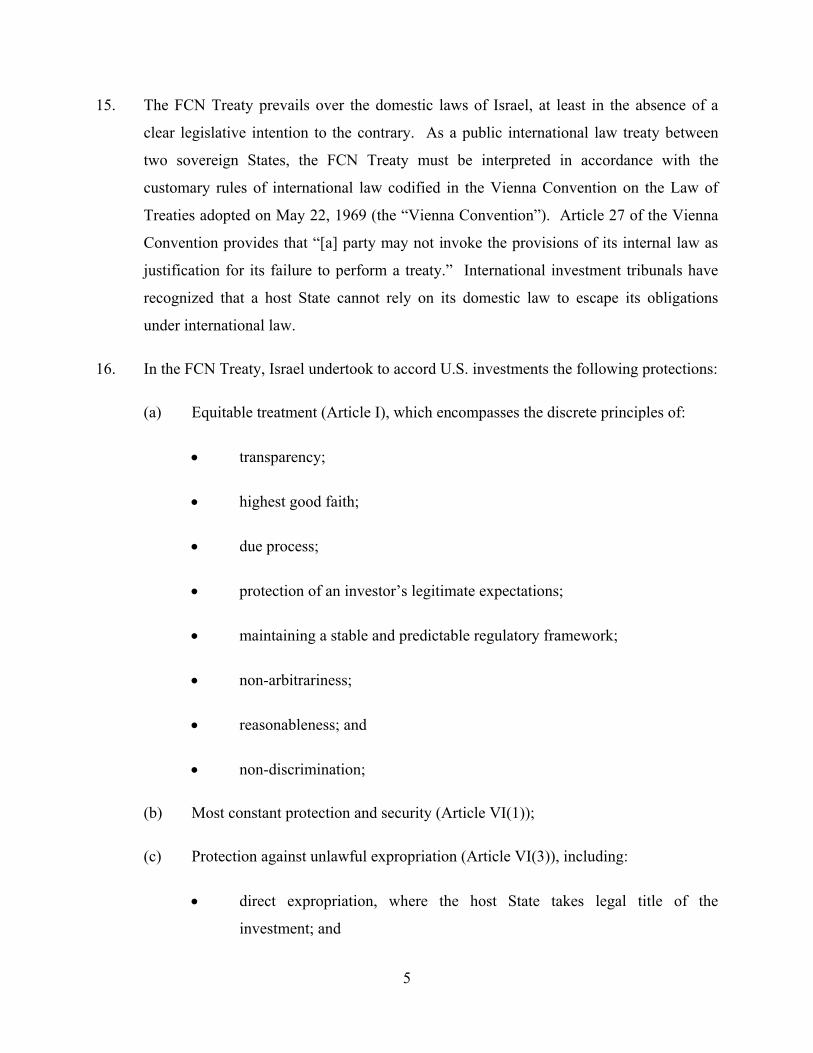

TABLE OF CONTENTS

Page

i

I. INTRODUCTION ............................................................................................................. 1

A. Relevant Qualifications.......................................................................................... 1

B. Scope of Work ....................................................................................................... 3

II. EXECUTIVE SUMMARY ............................................................................................... 4

III. BACKGROUND ............................................................................................................... 9

A. The Fundamentals of Energy Exploration and Development................................ 9

B. Israel’s Efforts to Encourage Energy Investment ................................................ 11

C. The Investment Process and Discoveries of Noble.............................................. 14

D. The Petroleum-Law Review ................................................................................ 17

IV. THE FCN TREATY ........................................................................................................ 19

A. Historical Perspectives......................................................................................... 19

1. The American Perspective ....................................................................... 19

2. The Israeli Perspective............................................................................. 21

B. U.S. and Israel Sign the Treaty ............................................................................ 23

V. APPLICATION OF THE FCN TREATY....................................................................... 24

A. Noble Has Protected Interests under the FCN Treaty.......................................... 24

B. The Substantive Provisions of the FCN Treaty ................................................... 26

1. The “Equitable Treatment” Standard in Article I .................................... 27

i. Israel’s Obligation to Treat Noble’s Investment Transparently and to Provide Noble Due Process ....................... 31

ii. The Treaty Requires Israel to Act Reasonably and in the Highest Good Faith ...................................................................... 32

iii. The Treaty Requires Israel to Protect Noble’s Legitimate Expectations................................................................................. 33

iv. The Treaty Requires Israel to Maintain a Stable and Predictable Environment for Noble’s Investment........................ 37

2. The “Most Constant Protection and Security” Standard in Article VI(1)......................................................................................................... 40

3. The Expropriation Standard in Article VI(3)........................................... 43

4. The Reasonableness and Non-Discrimination Standard in Article VI(4)......................................................................................................... 50

5. The National Treatment and MFN Standards of the FCN Treaty ........... 54

TABLE OF CONTENTS (continued)

Page

ii

a. National Treatment ...................................................................... 56

b. MFN Protection ........................................................................... 57

VI. NOBLE’S REMEDIES IF ISRAEL BREACHES THE TREATY................................. 60

VII. CONCLUSION................................................................................................................ 61

VIII. MY DUTY TO THE COMMITTEE ............................................................................... 62

APPENDIX I - CURRICULUM VITAE OF ABRAHAM D. SOFAER .............................. A-1

TABLE OF AUTHORITIES

Page

iii

International Law Decisions and Awards ADC Affiliate Ltd. v. The Republic of Hungary,

ICSID Case No. ARB/03/16, Award of October 2, 2006...................................... 34, 60-61

Aguas del Tunari S.A. v. Bolivia, ICSID Case No. ARB/02/3, Partial Award of October 21, 2005....................................................................................................................................23

Alex Genin, Eastern Credit Limited, Inc. and A.S. Baltoil v. The Republic of Estonia, ICSID Case No. ARB/99/2, Award of June 25, 2001 ................................................. 28-29

AMCO Asia Corp. and Others v. The Republic of Indonesia, ICSID, Award of November 21, 1984...............................................................................61

American Manufacturing & Trading, Inc. v. Republic of Zaire, ICSID Case No. ARB/93/1, Award of February 21, 1997 .......................................... 40-41

Azurix Corp. v. The Argentine Republic, ICSID Case No. ARB/01/12, Jurisdiction of December 8, 2003....................................................................................................................................27

Azurix Corp. v. The Argentine Republic, ICSID Case No. ARB/01/12, Award of July 14, 2006 ...............................27, 29-30, 41-42

BG Group Plc. v. The Republic of Argentina, UNCITRAL, Final Award of December 24, 2007 ................................................ 32, 50-51

Case Concerning Ahmadou Sadio Diallo (Republic of Guinea v. Democratic Republic of the Congo), ICJ Reports 2007................................................................................................................25

Case Concerning Elettronica Sicula S.p.A. (ELSI) (United States of America v. Italy), ICJ Reports 1989................................................................................................................25

Case Concerning The Barcelona Traction, Light and Power Co., Ltd. (Belgium v. Spain), ICJ Reports 1970..........................................................................................................24, 25

CME Czech Republic B.V. (The Netherlands) v. The Czech Republic, UNCITRAL, Partial Award of September 13, 2001...................... 28, 32, 36-37, 42, 46, 50

TABLE OF AUTHORITIES (continued)

Page

iv

CMS Gas Transmission Co. v. The Argentine Republic, ICSID Case No. ARB/01/8, Objections to Jurisdiction of July 17, 2003................................................................................................................ 38-39

CMS Gas Transmission Co. v. The Argentine Republic, ICSID Case No. ARB/01/8, Award of May 12, 2005 ...........................................31, 37, 61

Compañía de Aguas del Aconquija S.A. and Vivendi Universal S.A. v. Argentine Republic, ICSID Case No. ARB/97/3, Award of August 20, 2007 ................................. 29, 42, 60-61

Compañía del Desarrollo de Santa Elena, S.A. v. The Republic of Costa Rica, ICSID Case No. ARB/96/1, Final Award of February 17, 2000........................................................................................................................45, 47, 49

Continental Casualty Co. v. Argentine Republic, ICSID Case No ARB/03/9, Award of September 5, 2008.................................................27

Duke EnergyElectroquil Partners v. Republic of Ecuador, ICSID Case No. ARB/04/19, Award of August 18, 2008 .................................................31

EnCana Corp. v. Ecuador, LCIA Case No. UN3481, Award of February 3, 2006 ................................................ 44-46

EnCana Corp. v. Ecuador, LCIA Case No. UN3481, Partial Dissenting Opinion of Dr. Horacio A. Grigera Naón of December 30, 2005 ..............................................................45

Enron Corp. Ponderosa Assets, L.P. v. Argentine Republic, ICSID Case No. ARB/01/3, Award of May 22, 2007 .................................................29, 38

Eureko B.V. v. Republic of Poland, UNCITRAL, Partial Award and Dissenting Opinion of August 19, 2005................................................................................................36-37, 46-48

Factory at Chorzow, 1928 P.C.I.J. (Sel. A) No. 17, Decision of September 13, 1928.............................................................................................................................. 60-61

Feldman v. Mexico, ICSID Case No. ARB(AF)/99/1, Award of December 16, 2002........................................................................................................................ 44, 56-57

TABLE OF AUTHORITIES (continued)

Page

v

GAMI Investments, Inc. v. The Government of The United Mexican States, UNCITRAL, Final Award of November 15, 2004 ................................................45, 47, 49

Gas Natural SDG, S.A. v. The Argentine Republic, ICSID Case No. ARB/03/10, Decision on Jurisdiction of June 17, 2005 .....................................................................................................................59

Goetz v. Burundi, ICSID Case ARB/95/03, Award of February 10, 1999 .....................................................43

Lauder v. Czech Republic, UNCITRAL, Final Award of September 3, 2001..............................................................28

LG&E Energy Corp. v. Argentine Republic, ICSID Case No. ARB/02/1, Award on Liability of October 3, 2006.......................................................................................................................... 37-39

Maffezini v. The Kingdom of Spain, ICSID Case No. ARB/97/7, Decision on Jurisdiction of January 25, 2000 .......................................................................................................... 58-60

Maffezini v. The Kingdom of Spain, ICSID Case No. ARB/97/7, Award of November 9, 2000................................................28

Metalclad Corp. v. The United Mexican States, ICSID Case No. ARB(AF)/97/1, Award of August 30, 2000....................................................................................................................................47

Methanex Corp. v. United States of America, UNCITRAL, Final Award on Jurisdiction of August 3, 2005....................................................................................................................................23

Middle East Cement Shipping and Handling Co. S.A. v. Arab Republic of Egypt, ICSID Case No. ARB/99/6, Award of April 12, 2002 ................................................46, 47

Mondev International Ltd. v. United States of America, ICSID Case No. ARB(AF)/99/2, Award of October 11, 2002........................................................................................................................27, 28, 30

MTD Equity Sdn. Bhd. and MTD Chile S.A. v. Republic of Chile, ICSID Case No. ARB/01/7, Award of May 25, 2004 ...........................................29, 38, 57

TABLE OF AUTHORITIES (continued)

Page

vi

National Grid P.L.C. v. Argentine Republic, UNCITRAL Case No. 1:09-cv-00248-RBW (2008), Award of November 3, 2008 ................................................................................................... 41-42

Occidental Exploration and Production Co. v. The Republic of Ecuador, LCIA, Final Award of July 1, 2004 .................................................37-40, 42, 52-53, 56-57

Pope & Talbot Inc. v. The Government of Canada, UNCITRAL, Interim Award of June 26, 2000 ............................................................46, 49

Pope & Talbot Inc. v. The Government of Canada, UNCITRAL, Award on the Merits of Phase 2 of April 10, 2001....................................................................................................................................28

PSEG Global Inc., The North American Coal Corp. Konya Ilgin Elektrik Üretim ve Ticaret Limited Sirketi v. Republic of Turkey, ICSID Case No. ARB/02/5, Award of January 19, 2007 ..................................................37

Revere Copper and Brass Inc. v. Oversees Private Investment Corp., AAA Case No. 16 10 0137 76, Award of August 24, 1978 ..............................................43

RoslnvestCo UK Ltd. v. The Russian Federation, SCC Case No. Arb. V079/2005, Award on Jurisdiction of October 5, 2007 ....................59

Rumeli Telekom A.S. and Telsim Mobil Telekomikasyon Hizmetleri A.S. v. Republic of Kazakhstan, ICSID Case No. ARB/05/16, Award of July 29, 2008 ................................................ 30-31

Saluka Investments BV (The Netherlands) v. The Czech Republic, UNCITRAL, Partial Award of March 17, 2006 .............................................. 28, 32, 50-51

S.D. Myers, Inc. v. Government of Canada, UNCITRAL, Partial Award of November 13, 2000........................................28, 46, 48, 61

Sempra Energy International v. Argentine Republic, ICSID Case No. ARB/02/16, Award of September 28, 2007............................................37

Siemens A.G. v. The Argentine Republic, ICSID Case No. ARB/02/8, Award of February 6, 2007 .......................... 41-42, 51, 53, 61

TABLE OF AUTHORITIES (continued)

Page

vii

Siemens A.G. v. The Argentine Republic, ICSID Case No. ARB/02/8, Decision on Jurisdiction of August 3, 2004.......................................................................................................26, 56, 59

Starrett Housing Corp. v. The Government of the Islamic Republic of Iran, Case No. 24, Final Award of August 14, 1987..................................................................61

Suez and InterAguas v. The Argentine Republic, ICSID Case No. ARB/03/17. Decision on Jurisdiction of May 16, 2006 .....................................................................................................................59

Técnicas Medioambientales Tecmed S.A. v. The United Mexican States, ICSID Case No. ARB (AF)/00/2, Award of May 29, 2003.............................31, 33, 46, 51

Tippetts, Abbett, McCarthy, Stratton v. TAMS-AFFA Consulting Engineers of Iran, UNCITRAL, Award No. 141-7-2 of June 29, 1984, reprinted in 6 Iran-U.S. C.T.R. 219.............................................................................47, 49

Waste Management, Inc. v. Mexico, ICSID Case No. ARB(AF)/00/3, Award of April 30, 2004......................................... 46-48

Wena Hotels Ltd. v. Arab Republic of Egypt, ICSID Case No. ARB/98/4, Award of December 8, 2000 ................................................46

Wickes v. Olympic Airways 745 F.2d 363 (6th Cir. 1984) .............................................................................................20

Zenith Radio Corp. v. Matsushita Electric Industrial Co., Ltd., 494 F. Supp. 1263 (E.D. Pa.1980) .....................................................................................23

International Law Commentary (Treaties, Books, Articles)

American Law Institute, Restatement of the Law Third, Foreign Relations of the United States, American Law Institute Publishers, Vol. 1, 1987, Section 712.......................................................................... 43-44

Commercial Treaties: Hearings on Treaties of Friendship, Commerce and Navigation with Israel, Ethiopia, Italy, Denmark, Greece, Finland, Germany and Japan Before the

TABLE OF AUTHORITIES (continued)

Page

viii

Subcomm. on Commercial Treaties of the Senate Foreign Relations Comm., 83d CONG., 1st SESS. 6 (1953) ...........................................................................................19

DANIEL JOHNSON, INTERNATIONAL PETROLEUM FISCAL SYSTEMS

AND PRODUCTION SHARING CONTRACTS (PENNWELL PUB. CO. 1994) ...........................................................................................................................10

Herman Walker, Jr., Modern Treaties of Friendship, Commerce and Navigation, 42 MINN. L. REV. 805 (1958)....................................................................................... 20-21

Herman Walker, Jr., The Post-War Commercial Treaty Program of the United States, 73 POL. SCI. Q. 57 (1958) ............................................................................................19, 21

Herman Walker, Jr., Treaties for the Encouragement and Protection of Foreign Investment: Present United States Practice, 5 AM. J. COMP. L. 229 (1956)....................................................................... 20-21

Jeswald W. Salacuse & Nicholas P. Sullivan, Do BITs Really Work?: An Evaluation of Bilateral Investment Treaties and Their Grand Bargain, 46 HARV. INT’L L.J. 67 (2005)...........................................................................................27

Joshua Robbins, The Emergence of Positive Obligations in Bilateral Investment Treaties, 13 U. MIAMI INT’L & COMP. L. REV. 403 (2006).............................................................................................................40

KENNETH J. VANDEVELDE, UNITED STATES INVESTMENT TREATIES: POLICY AND PRACTICE (Kluwer 1992)............................................................. 27-28, 40, 50

LUCY REED, ET AL., GUIDE TO ICSID ARBITRATION (Kluwer Law Int’l 2004) ..........................................................................................................................49

President’s Message to the Senate Transmitting The Treaty of Friendship, Commerce and Navigation Between the United States of America and Israel, 82d CONG. REC 1 (Oct. 18, 1951)......................................................................................23

Robert Wilson, Postwar Commercial Treaties of the United States, 43 AM. J. INT’L L. 262 (1949) ............................................................................................20

TABLE OF AUTHORITIES (continued)

Page

ix

Rudolf Dolzer, Fair and Equitable Treatment: A Key Standard in Investment Treaties, 39 INT’L LAWYER 87 (2005) ..............................................................................................30

RUDOLF DOLZER AND CHRISTOPH SCHREUER, PRINCIPLES OF

INTERNATIONAL INVESTMENT LAW (Oxford Univ. Press 2008) ..................................................................................................................................34

Samuel M. Levin, Some Problems of the Economy of Israel, 3 AM. J. ECON. & SOC. 231 (1953) ...............................................................................................21

Vienna Convention on the Law of Treaties adopted on May 22, 1969....................................................................................................................5, 23, 29, 34

Israeli Laws and Regulations

Israel Petroleum Law, 5712-1952.......................................................................................... passim

Israel-U.S. Friendship, Commerce and Navigation Treaty.................................................... passim

x

TABLE OF ABBREVIATED TERMS

AAA American Arbitration Association

BIT Bilateral Investment Treaty

CPR International Institute for Conflict Prevention & Resolution

FCN Friendship, Commerce and Navigation

ICC International Chamber of Commerce

ICJ International Court of Justice

ICSID International Centre for Settlement of Investment Disputes

LCIA London Court of International Arbitration

MFN Most-Favored Nation

NAFTA North American Free Trade Agreement

NEM Noble Energy Mediterranean, Ltd.

UNCITRAL United Nations Commission on International Trade Law

1

I, Abraham D. Sofaer, declare as follows:

I. INTRODUCTION

1. I am the George P. Shultz Senior Fellow at The Hoover Institution, Stanford University,

Stanford, California, USA, 94305-6010. I have been asked by Noble Energy Inc.

(“Noble”) to provide an Opinion and Memorandum of Law concerning the legality of

increases in royalty rates and/or taxes applicable to existing oil and natural gas interests

owned by a U.S. national in Israel under the Friendship, Commerce and Navigation

(“FCN”) Treaty between the State of Israel and the United States of America (the “FCN

Treaty” or “Treaty”) and other related issues. On behalf of Noble, I respectfully submit

this Opinion and Memorandum of Law to the Committee on Fiscal Policy Concerning

Oil and Natural Gas in Israel (the “Committee”).

A. RELEVANT QUALIFICATIONS

2. A resume that summarizes my career is attached to this Opinion and Memorandum of

Law as Appendix I. I am an attorney by training, having received my B.A. degree from

Yeshiva University in History in 1962, and my law degree from the New York University

School of Law in 1965, where I was editor-in-chief of the law review. Soon after

graduating law school, I became a member of the New York bar, having been admitted in

the First Appellate Division.

3. From 1965 to 1967, I served as a law clerk, first to Judge J. Skelly Wright of the U.S.

Court of Appeals for the District of Columbia, and then to Associate Justice William J.

Brennan, Jr. of the U.S. Supreme Court. From 1967 to 1969, I was an Assistant U.S.

Attorney in the Southern District of New York. From 1969 to 1979, I taught at the

Columbia University School of Law, where my principal subjects were Property and

Administrative Law.

4. In 1979, I was appointed a U.S. District Judge for the Southern District of New York,

where I served for six years. My duties as a trial judge included deciding and presiding

over cases involving a variety of subjects, including the interpretation of treaties and

international law. See, e.g., Ariel Sharon v. Time, Inc., 599 F. Supp. 538 (S.D.N.Y. 1984)

(determining the “act-of-state” doctrine does not preclude a court from exercising

2

jurisdiction over a libel suit brought by a high-level Israeli state official regarding alleged

acts performed in the course of his official service); Hener v. United States, 525 F. Supp.

350 (S.D.N.Y. 1981) (interpreting general principles of maritime and international law

over ownership of property lost at sea); Mahmoud v. Alitalia Airlines, 1982 U.S. Dist.

Lexis 16635 (applying provisions of the Warsaw Convention in determining liability for

lost passenger property on an airline); Braka v. Bancomer, S.A., 589 F. Supp. 1465

(S.D.N.Y. 1984) (upholding defendant foreign bank’s argument that the act-of-state

doctrine makes the foreign nation’s alleged breach of the IMF Breton Woods Agreement

nonjusticiable in a U.S. court). I have served as an expert in proceedings in Australia,

Ireland, Israel, and the United Kingdom.

5. I resigned my position as District Judge in 1985 to accept the position of Legal Adviser to

the U.S. Department of State, where for five years I was in charge of the Office of Legal

Adviser. The Department of State is responsible for negotiating commercial treaties on

behalf of the U.S., including bilateral investment treaties. During my tenure as Legal

Adviser, my office negotiated or presented to the Senate several bilateral investment

treaties and was involved in litigating the scope of FCN treaties in the International Court

of Justice (“ICJ”). I was Agent for and argued on behalf of the U.S. in FCN litigation

before the ICJ in a suit against Italy concerning the Raytheon Company, discussed below.

6. From 1990 to 1994, I was Senior Partner at the Washington, D.C. office of the law firm

of Hughes, Hubbard & Reed. My practice there consisted largely of litigation and legal

advice to companies, especially concerning international commercial affairs.

7. From 1994 to the present, I have been the George P. Shultz Senior Fellow at The Hoover

Institution, Stanford University. My work at Stanford consists primarily of scholarship

on subjects related to international law. I also hold the position of Professor of Law (by

courtesy) at the Stanford Law School, where I have taught a course in Transnational Law.

8. During the last 20 years, I have often been appointed to serve as an arbitrator in

commercial matters under the rules of the ICC, the AAA, and the CPR. These cases

often have involved issues requiring application of international law. I have appeared as

an expert witness on international law in two arbitrations under the Bilateral Investment

3

Treaty (“BIT”) between the U.S. and Argentina before the International Centre for

Settlement of Investment Disputes (“ICSID”). I am also a member of the College of

Commercial Arbitrators.

9. In addition to being a member of the bar of New York since 1965, I am a member of the

bars of the District of Columbia and the State of California. I am also qualified to

practice before several federal courts, including the Southern District of New York, the

Court of Appeals for the Second Circuit, and the U.S. Supreme Court. I have been a

member for many years of the American Law Institute. I am also a member of the U.S.

Secretary of State’s Advisory Committee on Public International Law and of the Council

on Foreign Relations.

B. SCOPE OF WORK

10. I have been asked to provide my opinion on the following question: To what extent does

the FCN Treaty limit Israel’s ability to increase royalty rates and/or taxes, or to reduce or

cancel tax benefits, applicable to existing oil and natural gas property rights in which

Noble has an interest in Israel? In providing my answer to that question, I will review the

relevant, substantive provisions of the FCN Treaty, analyze decisions from international

investment tribunals interpreting those provisions, and then provide my views on the

question presented.

11. These are complicated issues, however, and I have advised Noble that my ability to

evaluate the current situation is severely constrained. First, I have been afforded a very

short time within which to prepare my opinion given the complexity of the subject and

the special circumstances surrounding Noble’s activities. Even more significantly, I have

been informed that my opinion must be given before this Committee has indicated what

measures it plans to recommend, and that I may be given no opportunity at all to address

the Committee orally or in writing after it specifies the proposals it intends to make.

12. My opinion would be far more meaningful if the Committee permits me to address, not

only the possible issues, but those actually raised by specified proposals. The obligation

to proceed in a manner consistent with due process and transparency requires, in my

judgment, providing Noble an opportunity to address the Committee after it has

4

announced its intended proposal, if any, for a retroactive change to the royalty rate and/or

taxes applicable to existing oil and natural gas rights. Given that the current royalty rate

has remained unchanged since its enactment 58 years ago, and because no emergency of

any sort exists that would justify a departure from conventional “notice and comment”

procedures generally applicable to administrative agency actions, any change in this

regard should be taken only after full and fair consideration of the legal, economic, and

policy impacts thereof. As discussed below, Israel has accepted legal obligations in the

FCN Treaty regarding transparency, highest good faith, and due process.

II. EXECUTIVE SUMMARY

13. Under the FCN Treaty, Israel undertook to limit its exercise of sovereign powers with

respect to foreign investments made by U.S. nationals. In particular, the FCN Treaty

limits Israel’s ability to retroactively increase royalty rates and/or taxes, or to reduce or

cancel tax benefits, applicable to existing oil and natural gas rights and interests (such as

those granted by existing licenses and leases) held by U.S. nationals.

14. The FCN Treaty applies to Noble’s interests in Israel. Noble is a company incorporated

in the U.S. and is therefore a “company” within the meaning of Article XXII(3) of the

Treaty. It is the 100% owner of Noble Energy Mediterranean, Ltd. (“NEM”), an entity

incorporated in the Cayman Islands and registered for doing business in Israel under the

Israeli Companies Ordinance. NEM is the direct owner of rights in licenses and leases

for the exploration and production of petroleum in Israel. According to ICJ jurisprudence

(discussed below), NEM thus has “rights” in the licenses and leases, and Noble has

corresponding “interests” in those licenses and leases. The relevant provisions in the

FCN Treaty expressly state that they cover both “rights” and “interests” of U.S.

companies in Israel, and the Protocol section of the Treaty expressly states that

expropriation protection applies to both “direct and indirect” investments. Accordingly,

the FCN Treaty limits Israel’s ability to retroactively increase royalty rates and/or taxes,

or to reduce or cancel tax benefits, applicable to Noble’s “interests” in Israel, including

oil and natural gas rights under existing licenses and leases held by NEM.

5

15. The FCN Treaty prevails over the domestic laws of Israel, at least in the absence of a

clear legislative intention to the contrary. As a public international law treaty between

two sovereign States, the FCN Treaty must be interpreted in accordance with the

customary rules of international law codified in the Vienna Convention on the Law of

Treaties adopted on May 22, 1969 (the “Vienna Convention”). Article 27 of the Vienna

Convention provides that “[a] party may not invoke the provisions of its internal law as

justification for its failure to perform a treaty.” International investment tribunals have

recognized that a host State cannot rely on its domestic law to escape its obligations

under international law.

16. In the FCN Treaty, Israel undertook to accord U.S. investments the following protections:

(a) Equitable treatment (Article I), which encompasses the discrete principles of:

! transparency;

! highest good faith;

! due process;

! protection of an investor’s legitimate expectations;

! maintaining a stable and predictable regulatory framework;

! non-arbitrariness;

! reasonableness; and

! non-discrimination;

(b) Most constant protection and security (Article VI(1));

(c) Protection against unlawful expropriation (Article VI(3)), including:

! direct expropriation, where the host State takes legal title of the

investment; and

6

! indirect or “creeping” expropriation, where the host State achieves the

same result by taxation and regulatory measures that makes continued

operation of the investment uneconomical;

(d) Reasonable and non-discriminatory treatment (Article VI(4));

(e) National treatment (Articles V(1), VI(5), VII, and XVI), assuring U.S. investors

no less favorable treatment than treatment extended to Israeli nationals and

companies; and

(f) Most-favored nation (“MFN”) treatment (Articles V(1), VI(5), and XI(3)),

assuring U.S. investors no less favorable treatment than treatment extended to

other foreign investors.

17. Transparency, Highest Good Faith, and Due Process. International tribunals have

interpreted the “equitable treatment” standard in Article I of the Treaty to require the host

State (here, Israel) to act transparently and in the highest good faith with respect to the

protected foreign investment and to afford the investor due process. Consistent with

these standards, Noble should be provided notice and a meaningful opportunity to be

heard after the Committee has announced specific proposals for any changes to royalty

rates and/or taxes applicable to Noble’s interests. The highest good faith standard also

requires that any retroactive changes to existing royalty rates and/or taxes must relate to a

“rational policy,” such as a newly-discovered public need or emergency—and not be

undertaken simply to increase revenues.

18. Protected Expectations and Stable and Predictable Legal Framework. The “equitable

treatment” standard further requires Israel (i) to protect Noble’s legitimate expectations

and (ii) to maintain a stable and predictable legal framework for Noble’s investment.

When Noble invested in Israel, it did so in the face of great uncertainties and risks. No

major oil or natural gas discovery had been made in Israel until Noble discovered

commercially exploitable deposits in 2009 and 2010. Relying on Israel’s royalty rate of

12.5% and the fact that this royalty rate had remained stable for over 50 years, Noble

invested in Israel on the basis of forecasts that reflected its expectation to pay that royalty

7

rate (with no increase in taxes aimed at deriving the same result as an increased royalty

rate). By retroactively1 increasing royalty rates and/or taxes, Israel would undermine

Noble’s reliance and legitimate expectations and would upset the stable and predictable

legal framework that Israel is obligated to provide under the Treaty.

19. Full protection and security. For the same reasons, a retroactive increase in royalty rates

and/or taxes applicable to Noble’s interests would violate the full protection and security

standard in Article VI(1) of the Treaty. International investment tribunals have held that

treatment that is not “equitable” automatically entails an absence of full protection and

security of the investment.

20. Expropriation. Article VI(3) of the Treaty prohibits Israel from expropriating Noble’s

investment without prompt and adequate compensation. International investment

tribunals have ruled that this standard encompasses both direct and indirect expropriation,

the latter where the host State achieves the same result as direct expropriation by taxation

and regulatory measures that make continued operation of the investment uneconomical.

21. Reasonableness. Like the principle of good faith, the reasonableness standard in

Article VI(4) of the Treaty requires that any change in Israeli law affecting Noble’s

interests in Israel be related to a rational public policy. Here, however, it was not until

Noble’s exploration revealed commercially exploitable deposits in the Tamar and Dalit

fields that Israeli officials began to call for increased royalty rates and/or taxes. They did

so only a few months after NEM received two 30-year leases. The reasonableness

standard under the Treaty does not permit Israel to retroactively raise royalty rates and/or

taxes purely for monetary gain, thereby reflecting nothing more than an intent to change

the terms of a protected investment.

22. Non-Discrimination. The non-discrimination standard in Article VI(4) of the Treaty

prohibits Israel from treating Noble’s interests differently than other similarly-situated

companies. International tribunals have held that this standard requires a tax (or the

1 The term “retroactive” in this Opinion and Memorandum of Law refers to the application of royalty rates

and/or taxes to existing oil and natural gas rights in Israel, including licenses and leases and, in some circumstances, permits granted under the Israeli Petroleum Law.

8

reduction or cancellation in tax benefits) be applied “across-the-board”—i.e., not just to

the petroleum sector, but to other natural resource industries as well. Further, I am

informed that an Egyptian company, East Mediterranean Gas Company (“EMG”), is

exempt from paying taxes on the sale and transportation of natural gas pursuant to a

Memorandum of Understanding between Israel and Egypt. While I express no opinion

on that agreement, discriminatory treatment of Noble compared to other foreign investors

would violate Article VI(4) of the FCN Treaty.

23. National Treatment. The FCN Treaty also accords U.S. investors in Israel two contingent

protections: national treatment protection and MFN protection. The former assures non-

discrimination as compared with nationals of the host State; the latter, as compared with

other foreign investors. International tribunals have held that in some circumstances

increased taxes (or the reduction of tax benefits) applicable to only the petroleum

industry, rather than to all natural resource industries, violate the national treatment

standard.

24. MFN Treatment. The MFN protection has been applied to grant both substantive and

procedural rights. Substantively, MFN protection prohibits Israel from treating Noble

less favorably than other foreign investors. For example, discriminatory treatment of

Noble relative to EMG regarding taxes applicable to natural gas sales and transportation

would violate Article XI(3) of the Treaty. Procedurally, MFN clauses have been

interpreted by some tribunals to incorporate procedural rights from other treaties to which

Israel is a party, such as the dispute resolution options available to other foreign

investors.

25. Enforcement of Rights. Article XXIV of the FCN Treaty provides that the U.S. may

bring an action against Israel for a breach of the FCN Treaty before the ICJ, which the

U.S. may do if necessary. Noble may also attempt to use the MFN clause in the Treaty to

avail itself of a dispute resolution clause in another Israeli treaty, such as the Israel-

Ethiopia BIT, which allows a protected investor to bring a direct claim against Israel

before an international tribunal, such as an ICSID tribunal in Washington D.C or an

9

international tribunal established under the Arbitration Rules of the United Nations

Commission on International Trade Law (“UNCITRAL”).

26. Damages. Under international law, Noble would be entitled to damages under the FCN

Treaty that “wipe out all the consequences” of Israel’s breach of the Treaty. Thus, Israel

would be required to put Noble in the same position as it would have been “but for” its

breach. Israel would thus be liable for reimbursement of all royalties and/or taxes that it

collected from NEM in violation of the Treaty, together with any other proximate

damages that result from unlawful royalties and taxes.

III. BACKGROUND

A. THE FUNDAMENTALS OF ENERGY EXPLORATION AND DEVELOPMENT

27. Oil and natural gas exploration and development requires privately-owned companies or

public entities, with the proper equipment and technical ability, to invest enormous funds

to identify commercially exploitable deposits. The prospect of success of any major

project in an area of unproven potential is low. Nine out of ten exploration ventures are

unsuccessful, either finding insufficient resources to market economically or none at all.

Profits are secured only after a long and costly effort. Projects sometimes take five to ten

years from the start of exploration to the point of bringing oil and natural gas to market;

subsequent contracts commonly extend for decades.

28. The total cost of prospecting, developing, and marketing oil and natural gas—especially

from deep, off-shore reserves—is extremely high in both absolute terms and relative to

annual industry net income. A survey of 21 major global oil and natural gas companies,

including Noble, shows that the cost of new investments in the years 1996-2007 reached

117% of cumulative net income for those years.2 Anticipating costs accurately, therefore,

is essential in the oil and natural gas prospecting business.

2 See Investment and Other Uses of Cash Flow by the Oil Industry, 1996-2007, Prepared by Ernst & Young

LLP for the American Petroleum Institute (July 2008), p. ii, available at http://www.api.org/aboutoilgas/upload/EY_Investment_Trend_CY2007_Update_July_2008.pdf.

10

29. Given these risks and uncertainties, the process by which companies determine whether

to invest in petroleum exploration and development depends heavily on financial

projections based on the likelihood of success, the costs of development, the production

levels anticipated, and the profit margins that will result.

30. In forming models for determining whether to invest in undiscovered fields, oil and

natural gas companies consider the following factors, among others:

(a) Capital expenditures on property, plants, and equipment (“PP&E”).3 Without the

requisite technologies, equipment, infrastructure, and personnel, later stages of

exploration and production are unattainable. PP&E costs include company

research and development expenses.

(b) Drilling and exploration expenses. This depends on both the unique

characteristics of the geography of the site and the variable risks associated with

expected and unexpected finds. The cost of operating deepwater drilling

drillships and semisubs, for example, are significant—costing upwards of

$300,000 per day.4

(c) Production costs associated with a particular venture. Production costs include

geography, market commodity prices, regional production history, the existing

regulatory scheme, and contracted royalty requirements. The difference between

the value of production and the cost of extraction is key for determining company

profits.5

(d) Marketing and transportation. A commodity so closely linked to global politics

often finds itself shut out from certain markets due to political tensions. Israel’s

limited trading relationship with its regional neighbors serves as a case in point.

3 Id., see p. 2.

4 See Rigzone Data Center, available at http://www.rigzone.com/data.

5 See DANIEL JOHNSON, INTERNATIONAL PETROLEUM FISCAL SYSTEMS AND PRODUCTION SHARING

CONTRACTS, p. 6, (PennWell Pub. Co. 1994).

11

The absence of pipelines or liquefaction terminals in Israel adds substantially to

transportation costs.6

(e) Total cost of an oil or natural gas well. The total cost of an oil or natural gas well

must factor in the costs associated with the risk of explosion and or environmental

contamination. Protecting against such disasters and the cost of a cleanup effort

may skyrocket, and insurance to cover such risks is costly and limited.

31. On a global scale, the 21 largest oil and natural gas exploration companies spend some

65% of their annual cash flow on PP&E, exploration, research, and development alone.7

When these overhead costs are added to taxation on existing production, the resulting

earnings on an average per U.S. company in the first quarter of 2010 was only 7.3%

(net income/sales).8

B. ISRAEL’S EFFORTS TO ENCOURAGE ENERGY INVESTMENT

32. Since its establishment, Israel has been almost entirely dependent on foreign sources for

oil and natural gas to fuel its growing economy and defense infrastructure. Recognizing

the role played by private investment in the development of energy resources in most

areas of the world, Israel has encouraged foreign investment in the exploration of national

resources by establishing rules to govern such efforts, including commitments regarding

the royalty rate and taxes that would be imposed upon companies issued licenses that

result in leases and production.

33. The Israeli Petroleum Law, 5712-1952 (the “Petroleum Law”) governs exploration and

production of oil and natural gas in Israel, including the royalty rate applicable to such

6 See Putting Earnings Into Perspective: Facts for Addressing Energy Policy, prepared by the American

Petroleum Institute, p. 7 (July 2, 2010), http://www.api.org/statistics/earnings/upload/earnings_perspective.pdf.

7 See Investment and Other Uses of Cash Flow by the Oil Industry, 1996-2007, Prepared by Ernst & Young LLP for the American Petroleum Institute (July 2008), p. 8, available at http://www.api.org/aboutoilgas/upload/EY_Investment_Trend_CY2007_Update_July_2008.pdf.

8 See Putting Earnings Into Perspective: Facts for Addressing Energy Policy, prepared by the American Petroleum Institute, at p. 2 (July 2, 2010), available at http://www.api.org/statistics/earnings/upload/earnings_perspective.pdf.

12

production. Under Article 1 of the Petroleum Law, both licenses and leases are

“petroleum rights.” Article 26 of the Petroleum Law provides that an existing license

must be converted into a lease so long as the licensee has made a discovery in the

licensed area and has made a timely application for the lease. The government has no

discretion to deny the lease in such circumstances. Thus, licenses, along with leases

issued pursuant to them, are sufficient property and economic interests under Israeli law

to qualify for protection under the FCN Treaty. As a result, the Treaty’s constraints on

Israel’s retroactive application of increased royalties and/or taxes to Noble’s interests in

the applicable leases apply with equal force to Noble’s interests in any licenses issued for

exploration purposes.

34. Since its enactment over a half-century ago, the Petroleum Law has provided a consistent

statutory royalty rate on which investors have relied in allocating capital for exploration

and production.9 Article 32 of the Petroleum Law requires the payment of a 12.5%

royalty on the production of petroleum. It provides:

(a) A lessee is liable for a royalty of one-eighth of the quantity of petroleum produced from the leased area and saved, excluding the quantity of petroleum used by the lessee in operating the leased area; and he shall also be liable to a leasehold fee for the leased area at a rate equal to the highest rate of the license fee prescribed by Section 19(a1). A lessee who pays a royalty under sub-section (a) shall be exempt from a leasehold fee for a continuous area of fifty thousand dunams, to be selected by him, around each new well in the leased area and the configuration of which shall be approved by the Commissioner (hereinafter production area) provided that no new production area or part thereof shall anywhere coincide with an earlier production area or part thereof.

(b) The lessee shall pay to the Treasury, at such periods of payment as shall be prescribed by the regulations, the market value at the wellhead of the royalties due from him.

9 The law underwent substantial amendments in 1965, but the royalty provision was unchanged. In 2002,

amendments to increase both taxes and the royalty rate were proposed but ultimately rejected. See, e.g., Zvi Zrahiya & Avi Bar-Eli, State wants higher royalties on gas, oil, Haaretz (April 14, 2010) (“In 2002 the cabinet decided to levy additional taxes of 10% to 50% on profits from sales of natural gas and oil, on top of the 12.5% royalties. . . . But this entire move was halted completely in Novemebr [sic] 2002, when then infrastructures minister Effi Eitam objected and the Knesset Economic Affairs Committee voted down the proposals unanimously. Energy companies also lobbied heavily against, and the U.S. ambassador to Israel at the time also strongly denounced the changes.”) (available at http://www.haaretz.com/print-edition/business/state-wants-higher-royalties-on-gas-oil-1.284235).

13

(c) In the first month of any period of payment, the Commissioner may notify the lessee that in the next following period of payment he wishes to receive the royalty or part thereof in kind in lieu of payment therefor under sub-section (b); in this case, the lessee shall deliver to the Commissioner the quantity of petroleum due to the Treasury in tankage or pipelines designated by the Commissioner and not farther from the well than those of the lessee. Where facilities are available for the conveyance of the petroleum produced by the lessee, the Commissioner may require him to deliver all or part of the petroleum due to the Treasury as royalty in kind at such terminal point as the Commissioner may designate, provided that the cost of conveyance in excess of the cost of delivery as prescribed above shall be borne by the Treasury. The lessee is not bound to store gaseous petroleum due to the Treasury as royalty in kind or to store liquid petroleum due to the Treasury as aforesaid in his own tankage or storage for more than thirty days from the date of production.

(d) Notwithstanding as above provided, the royalty due from the lessee shall not, in any year, be less than the minimum amount prescribed for such year under sub-section (e); and if it appears that it is less than such minimum amount, the lessee shall, after such year within such time as shall be prescribed by the regulations, pay the difference between the royalty and the minimum amount. For the purpose of this provision, the royalty due from the lessee is the amount due from him under subsection (b) plus the market value at the wellhead of the petroleum due from him under sub-section (c).

(e) (1) The minimum amounts payable by the lessee for a particular year, in respect of each one thousand dunams of his production area, shall be the value at the end of that year of a number of barrels of petroleum as specified hereunder:

For the 1st year of the lease - 4 barrels

For the 2nd year of the lease - 6 barrels

For the 3rd year of the lease - 12 barrels

For the 4th year of the lease - 20 barrels

For the 5th and each succeeding year of the lease - 32 barrels

(2) For the purpose of this provision, the number of dunams in respect of a particular year shall be the number of dunams in the production area at the end of that year; and the value of a barrel of petroleum shall be the price of a barrel of Middle East crude oil at the terminal point of a pipeline on the eastern coast of the Mediterranean.

35. The royalty imposed by Article 32 is in addition to the taxes imposed on oil and natural

gas companies. Although the royalty rate is lower than that of States in which oil and

14

natural gas is known to be plentiful, no major oil or natural gas discovery had been made

in Israel until Noble’s efforts resulted in the Tamar and Dalit discoveries and the

prospects already identified in the Leviathan area. A relatively low royalty rate

encouraged potential investors to risk vast sums in territories subject to Israel’s economic

regulatory control.

C. THE INVESTMENT PROCESS AND DISCOVERIES OF NOBLE

36. It is against the backdrop of this specific and well-established regulatory regime that

Noble made a huge long-term investment in Israel by undertaking to explore and develop

oil and natural gas reserves within Israel’s claimed zone of economic control. Noble’s

cost-analysis for development and production included the following elements:

(a) the cost of conducting both 2D and 3D seismic testing;

(b) the drilling of appraisal wells; and

(c) the attendant costs of manning and conducting these intensive off-shore surveys.

37. Incurring these costs, Noble explored for viable sites—many of which proved

commercially unproductive and resulted in substantial losses. Indeed, “there were some

500 previous drills which yielded nothing and caused massive losses in

funds. . . . American partners invested massive amounts of money in the State of Israel

against all odds . . . .”10

38. In July 2006, after these exploration activities, Noble’s wholly owned subsidiary, NEM,

entered into a license to explore an area in the Mediterranean Sea off the coast of Haifa.11

After conducting 3D seismic testing, Noble developed appraisal wells to gauge the

reserves of areas known as the Tamar field (“Tamar”) and the Dalit field (“Dalit”). The

cost of drilling the first exploration well was initially estimated at USD 40 million, but

10 See Roni Sofer, Steinitz: Natural gas profits belong to people, Ynetnews.com (July 6, 2010),

http://www.ynet.co.il/english/articles/0,7340,L-3899626,00.html.

11 “The prospect falls under the Matan licence, which Noble Energy has been operating since July 2006.” Tamar Field, Offshore Technology, http://www.offshore-technology.com/projects/tamar-field/.

15

escalated to more than USD 145 million.12 Noble collected additional 3D seismic data

for over 1,600 square miles of the Tamar region in the second half of 2009, after the

drilling of the second exploration well Dalit-1 and the Tamar-2 appraisal well was

completed in July 2009.13

39. The wells sufficiently defined the petroleum fields at Tamar and Dalit to satisfy Articles

18 and 26 of the Petroleum Law. In December 2009, the Ministry of National

Infrastructure issued two 30-year Leases for Exploration and Production of Oil and

Natural Gas No. I/12 (the “Leases”) to a consortium of companies (the “Lease Holders”),

one for the exploration and production of oil and natural gas in Tamar, and the other for

the exploration and production of oil and natural gas in Dalit. The Leases provide that

the Lease Holders are as follows (with their respective holdings):14

Noble Energy Mediterranean Ltd. 36.0%

Isramco Negev 2, limited partnership 28.75%

Avner Oil Explorations, limited partnership 15.6250%

Delek Drilling, limited partnership 15.6250%

Dor Gas Explorations, limited partnership 4.0%

40. The Leases further provide that NEM is the “operator” of Tamar and Dalit and shall

manage the operations required under the Leases and under the Petroleum Law on behalf

of the Lease Holders.

41. These investments reflect a trade-off in risk allocation. The investors accepted a

calculated risk of petroleum exploration in Israel, including specified contractual, legal,

regulatory, and taxation obligations imposed by contract and/or law (including the

established royalty). At the same time, Israel conferred upon NEM and its partners the

right to produce and sell any commercial quantities or oil or natural gas that they found,

while avoiding the costs and risks of resource development, and retaining the right to

benefit through the established royalty from Noble’s exploration investments and from its

12 Id. 13 See id.

14 Tamar and Dalit Leases, § 4.

16

positive consequences to the Israeli economy. Israel thus reaped guaranteed benefits in

an explicit and public exchange that included a clear understanding of the amount of any

royalty rate set by law at the time of the investment.

42. The Leases, like the Petroleum Law itself, place the entire financial burden of production

on the Lease Holders.15 The Leases make clear, for example, that the “Lease Holder

shall, at its liability only, plan, finance, set up and operate the Production System and the

Lease Holder’s Transmission System . . . .” 16 They also contain an additional,

prospective bank guarantee to the Government on the Lease Holders’ performance:

In order to ensure compliance with the terms of this Lease and as a condition for its granting, the Lease Holder shall produce an unconditional and irrevocable autonomous bank guarantee . . . . The Guarantee shall be valid for the entire Possession Period and for two years after the date on which the Possession Period shall be terminated for any reason whatsoever . . . . The sum of the Guarantee shall be [New Israeli Shekels] thirty-five million . . . .17

43. The Leases further require, in accordance with the Petroleum Law, specific construction

requirements and production timetables, 18 detailed reporting and specific production

methods,19 and extensive security and reporting duties.20 The liability for any legal

action or harm is solely the responsibility of the Lease Holders.21 As British Petroleum

15 See, e.g., Amiram Barkat, Steinitz at odds with Tamar partners on royalties, Globes-online.com (May 30,

2010) (“The partners [in the Tamar discovery] say that the areas where the [extended three dimensional] survey [was carried out] . . . cost some $50 million”).

16 Tamar and Dalit Leases, § 6.2.

17 Id. § 28.1-3.

18 See, e.g., id. §§ 9, 10.

19 See, e.g., id. Ch. E.

20 See, e.g., id. Ch. 6.

21 See, e.g., id. Ch. 9; id. § 29.1-2:

29.1 Instructions given by virtue of authority or by law, including provisions of permits and authorizations, provisions of the Lease, provisions of any law or any other provisions, shall not imply any responsibility or liability whatsoever upon the State or any of its authorities, or any of its employees, towards the Lease Holder, its employees, contractors, consumers or any other third party, and shall not be used as a cause for legal action by any of the above against the said parties, and shall not remove from the Lease Holder the full liability under the law and according to the Lease, to construct and operate facilities in a safe and proper manner.

17

has experienced from recent events in the Gulf of Mexico, this potential liability can be

enormous and represents a risk that must be taken into account in weighing the feasibility

of investments. The Lease Holders also remain responsible through the very end of the

endeavor. The Leases require them to submit a detailed plan determining how the site

will be abandoned when drilling is complete.22

44. Finally, the Leases expressly incorporate the provision of the Petroleum Law regarding

the payment of royalties: “The Lease Holder shall pay royalties in accordance with the

provisions of the law.”23 This provision refers to Article 32 of the Petroleum Law, which

sets the royalty rate at 12.5% of production.

D. THE PETROLEUM-LAW REVIEW

45. In April 2010, as estimates for the petroleum reserves recently discovered by NEM and

its partners continued to rise, Finance Minister Yuval Steinitz created the Committee to

review the Petroleum Law with the potential for a recommended increase in the royalty

rate on production of petroleum and/or in the taxes paid by the producers thereof.24 At

least one bill has already been submitted to the Knesset to modify the Petroleum Law.25

“The committee was instructed to propose an up-to-date policy for future gas and oil

29.2 The authority of the authorization or the supervision under the law or according to the Lease, or the use of any other authority as may be given in accordance with the Lease or any law of the State or any of its authorities or employees, shall not imply to any of the aforementioned any liability whatsoever that falls to the Lease Holder, nor does it remove from or reduce this liability.

22 See, e.g., id. § 27; id. § 27.1 (“Within 30 months of the date of the start of the production period, the Lease Holder shall submit for the authorization of the Commissioner a general plan of abandonment of the production system facilities and sealing of the drilling at the time of the conclusion of the use thereof, whether during the period of possession or subsequent thereto.”).

23 Id. § 33; see id. § 34 (“The Lease Holder shall pay the fees as stated in any law.” (emphasis added)).

24 “Following the discovery of a large natural gas reserve off the Haifa coast, Minister Steinitz decided to check whether companies which received a State concession to search and produce oil and gas were paying the government enough royalties and has a [sic] created a special committee for that purpose. The companies which found natural gas currently pay the government a 12.5% tax.” Amir Ben-David, US diplomat tries to prevent gas royalties raise, Ynetnews.com (May 27, 2010), http://www.ynet.co.il/english/Ext/Comp/ArticleLayout/CdaArticlePrintPreview/1,2506,L-3893557,00.html.

25 See Sharon Wrobel, MKs want more royalties on gas finds, JPost.com (July 13, 2010), http://www.jpost.com/Business/BusinessNews/Article.aspx?id=181341.

18

discoveries, and to study the implications of the present discoveries on the Israeli

economy.”26

46. A major issue of concern for members of the Israeli government, foreign governments,

and private investors is “that finance minister Yuval Steinitz did not state clearly that the

committee would refrain from discussing retroactively increasing royalties on current

leases and natural gas discoveries, including Tamar.”27 Reportedly:

This stance is opposed to the view expressed in the past by Minister of National Infrastructures Dr. Uzi Landau and Prime Minister Benjamin Netanyahu’s bureau. It is also inconsistent with official Ministry of Finance statements and views expressed by senior ministry officials, to the effect that royalties policy should not be changed for areas where seismic tests have been carried out and large amounts of money have been invested.28

47. This concern was echoed by Acting U.S. Ambassador Sievers, who wrote to the Israeli

Finance Minister that a decision to retroactively increase royalty rates and/or taxes may

“undermine confidence in the stability of Israeli fiscal policy and create[] barriers to

international investment.”29 A spokesperson for the Lease Holders likewise observed: “It

is unacceptable that with the news of the latest test results which suggest significant

potential for new discoveries, a committee should discuss the option of retroactively

changing the rules of the game and creating uncertainty and instability among all the

investors, primarily the foreign investors.”30

26 Zvi Zrahiya & Avi Bar-Eli, State wants higher royalties on gas, oil, Haaretz (April 14, 2010),

http://www.haaretz.com/print-edition/business/state-wants-higher-royalties-on-gas-oil-1.284235.

27 Israel Considers Upping Oil & Gas Royalties, Oil in Israel (May 21, 2010), http://www.oilinisrael.net/oil-in-israel-news/oil-in-israel-christian-world-news/israel-royalties.

28 Amiram Barkat, Steinitz at odds with Tamar partners on royalties, Globes-online (May 30, 2010), http://www.globes.co.il/serveen/globes/docview.asp?did=1000563029.

29 Letter from U.S. Ambassador, Marc Sievers to Minister of Finance of the State of Israel, Yuval Steinitz dated April 21, 2010; see also Amir Ben-David, US diplomat tries to prevent gas royalties raise, Ynetnews.com (May 27, 2010), http://www.ynet.co.il/english/Ext/Comp/ArticleLayout/ CdaArticlePrintPreview/1,2506,L-3893557,00.html.

30 Roni Sofer, Steinitz: Natural gas profits belong to people, Ynetnews.com (July 6, 2010), http://www.ynet.co.il/english/articles/0,7340,L-3899626,00.html.

19

IV. THE FCN TREATY

A. HISTORICAL PERSPECTIVES

48. The FCN Treaty is part of an extensive series of bilateral investment treaties signed and

ratified by nations following World War II. The purpose of these treaties is to encourage

and protect foreign investment by creating mutually favorable conditions for investments

by nationals of each State Party in the territory of the other. In addition, the FCN Treaty

was signed in the context of specific historical, political, and economic concerns.

1. The American Perspective

49. The U.S. signed the FCN Treaty with Israel as part of a program developed after World

War II, which carried forward one of its oldest diplomatic activities reaching back to the

Revolutionary War.31 From 1778 onward, with varying degrees of intensity from era to

era, the U.S. has used commercial treaties to “promote trade relations and to protect

shipping and the citizen and his interests abroad, according to legal principles,”32 to

strengthen friendly relations between nations, and to address special diplomatic interests

in the country’s formative years.

50. By the 1930s, however, the U.S. had become firmly established as a leading international

creditor and a major exporter of manufactured goods. That, together with the nation’s

intensified foreign economic interests, sparked a new series of foreign negotiations with

special emphasis on international trade. The reciprocal trade agreements program that

was subsequently developed provided a more precise and efficacious medium for

attaining trade promotion objectives, and in particular for encouraging and protecting

foreign investment. The pre-existing commercial treaties were overhauled in new

31 Herman Walker, Jr., The Post-War Commercial Treaty Program of the United States, 73 POL. SCI. Q. 57,

58 (1958); see Commercial Treaties: Hearings on Treaties of Friendship, Commerce and Navigation with Israel, Ethiopia, Italy, Denmark, Greece, Finland, Germany and Japan Before the Subcomm. on Commercial Treaties of the Senate Foreign Relations Comm., 83d CONG., 1st SESS. 6 (1953).

32 Herman Walker, Jr., The Post-War Commercial Treaty Program of the United States, 73 POL. SCI. Q. 57, 58 (1958).

20

“Friendship, Commerce and Navigation” treaties with a view towards responding to the

needs of foreign investors.33

51. According to Herman Walker, the primary architect of FCN treaties for the U.S., these

bilateral treaties “define the treatment each country owes the nationals of the other; their

rights to engage in business and other activities within the boundaries of the former; and

the respect due them, their property and their enterprises.”34 The FCN treaties “are not

political in character. . . . They are ‘commercial’ in the broadest sense of that term; and

they are above-all treaties of ‘establishment,’ concerned with the protection of persons,

natural and juridical, and of the property and interests of such persons.”35

52. FCN treaties seek to encourage and protect foreign investment by according foreign

investors two categories of rights. First, they grant to foreign investors rights based on

two “contingent standards”: (i) national treatment, which assures nondiscrimination or

no-less-favorable treatment than the citizens or companies of the host State; and (ii) MFN

treatment, which assures treatment no-less-favorable than the treatment of aliens or

companies from other States.

53. Second, FCN treaties accord foreign investors “non-contingent” (or non-relative) rights,

based on what are called “absolute” standards because their meaning is not dependent on

differential treatment.36 Non-contingent (absolute) standards are intended to protect the

rights of foreign nationals regardless of whether the host State provides the same rights to

its own or a third State’s nationals.37 FCN treaties thus include the non-contingent

guarantee that a foreign investor “shall receive not only equal protection, but also a 33 Whereas the pre-World War II treaties discussed foreign investment in one article among approximately 30,

half of the provisions in the post-World War II FCN treaties related to encouraging and protecting foreign investment. Herman Walker, Jr. Treaties for the Encouragement and Protection of Foreign Investment: Present United States Practice, 5 AM. J. COMP. L. 229 (1956).

34 Herman Walker, Jr., Modern Treaties of Friendship, Commerce and Navigation, 42 MINN. L. REV. 805, 806 (1958).

35 Id.

36 Id. p. 811

37 Wickes v. Olympic Airways, 745 F.2d 363, 366-67 (6th Cir. 1984); Herman Walker, Jr., Modern Treaties of Friendship, Commerce and Navigation, 42 MINN. L. REV. 805, 823 (1958); see also Robert Wilson, Postwar Commercial Treaties of the United States, 43 AM. J. INT’L L. 262, 264 (1949).

21

certain minimum degree of protection, as under international law, regardless of a

Government’s possible lapses with respect to its own citizens.”38

54. During the decade 1946-1956, the U.S. negotiated and signed 16 FCN treaties with

countries comprising a cross section of the world in geographical distribution, size, and

national circumstance outside the Soviet bloc. 39 In Asia, those represented include

Nationalist China, Korea, and Japan; in Africa, Ethiopia; in Latin America, Colombia,

Haiti, Nicaragua, and Uruguay; in Europe, Denmark, Germany, Greece, Ireland, Italy,

and the Netherlands; and in the Middle East, Iran and Israel.

2. The Israeli Perspective

55. From the Israeli perspective, the need for capital in the formative years of the nation was

paramount for its future economic and political success.40 From 1948 to 1953, Israel’s

population doubled, with expectations of 300% growth by 1958.41 This placed enormous

strains on the nascent economy.42 Further, the Israeli economy suffered from across-the-

board resource scarcities of petroleum, coal, iron, timber, and machines; of arable land

and adequate rainfall; of raw materials for sundry industries; of dollar exchange; and of

various kinds of consumers’ goods, such as shoes, clothing, meat, soap, paper, and

drugs.43

56. These deficiencies would have been insurmountable in the absence of adequate foreign

capital flows to begin major development:

38 Herman Walker, Jr., Treaties for the Encouragement and Protection of Foreign Investment: Present United

States Practice, 5 AM. J. COMP. L. 229, 232 (1956). Walker describes this as “rule-making in independent terms, without reference to the treatment given to others.” Herman Walker, Jr., Modern Treaties of Friendship, Commerce and Navigation, 42 MINN. L. REV. 805, 811 (1958).

39 Herman Walker, Jr., The Post-War Commercial Treaty Program of the United States, 73 POL. SCI. Q. 57 (1958).

40 Samuel M. Levin, Some Problems of the Economy of Israel, 3 AM. J. ECON. & SOC. 231, 239 (1953).

41 Id. p. 238.

42 Id.

43 Id. p. 239.

22

To Israeli economists, industrialists, and statesmen, the solution of the economic problems confronting the country can only be accomplished through the provision of an adequate supply of such capital; capital drawn from investment sources within the land and without.44

57. The need for capital led the Israeli government in 1950 to pass the Law for the

Encouragement of Capital Investments, which was specifically intended to facilitate the

influx of foreign capital. The law arranged for the movement of duty-free imports, tax

reductions and exemptions, release of foreign exchange for imports of raw materials and

machinery, a limited convertibility of profits into foreign exchange, and preferred status

for new enterprises.

58. Internationally, Israel sought to establish robust and reliable relations with the nation that

quickly became its primary investor and ally, the U.S. Starting with President Harry

Truman’s recognition of the provisional government as the de facto authority of Israel in

May 1948, the U.S. maintained a policy of “friendly and helpful cooperation” with Israel,

of which trade relations soon became an important part. Seeking to strengthen Israel and

its economy, high level officials of the Israeli and U.S. governments convened the

National Planning Conference for Israel and Jewish Rehabilitation in Washington, D.C.

on October 27, 1950. The National Planning Conference formally endorsed the

following goal: “the absorption and creative rehabilitation of large-scale immigration

and for the consolidation and development of Israel’s economy requiring

$1,500,000,000.”45 To that end, it approved a four-point program:

(a) Urging the U.S. to help Israel through grant-in-aid, loans, and other forms of

financial support;

(b) Intensification of efforts to raise gift funds;

(c) Support of a “public loan in the United States as a means of obtaining funds for

the financing of its constructive programs”; and

44 Id.

45 Id. p. 236 (internal quotations omitted).

23

(d) Stimulation of private investment in Israel.46

59. It was in the context of these goals that Israel completed the FCN Treaty with the U.S.,

establishing the MFN status for both countries’ investors and enterprises.47 As President

Truman stated in his message to the U.S. Senate seeking advice and consent, the FCN

Treaty establishes “Israel’s definite intention to encourage foreign investments.”48

B. U.S. AND ISRAEL SIGN THE TREATY

60. The U.S. and Israel signed the FCN Treaty in Washington D.C. on August 23, 1951. The

U.S. ratified the Treaty on December 18, 1953, and Israel ratified it on January 21, 1954.

The nations exchanged ratifications in Washington, D.C. on March 4, 1954, and the

Treaty entered into force one month later, on April 3, 1954. The Treaty is “self-

executing” and thus binding domestic law of its own accord in both States, without the

need for implementing legislation.49

61. As a public international law treaty between two sovereign States, the FCN Treaty must

be interpreted in accordance with Article 31 of the Vienna Convention, the interpretation

rules of which reflect customary international law.50 Article 31 of the Vienna Convention

requires that the terms of the Treaty be interpreted in accordance with their ordinary

meaning in their context and in view of the Treaty’s object and purpose—i.e., the

encouragement and protection of foreign investment.51

46 Id.

47 See id.

48 President’s Message to the Senate Transmitting The Treaty of Friendship, Commerce, and Navigation Between the United States of America and Israel, 82d CONG. REC 1 (Oct. 18, 1951).

49 See Zenith Radio Corp. v. Matsushita Electric Industrial Co., Ltd., 494 F. Supp. 1263, 1266-1267 (E.D. Pa.1980).

50 See, e.g., Aguas del Tunari S.A. v. Bolivia, ICSID Case No. ARB/02/3, Partial Award of October 21, 2005, ¶ 88; Methanex Corporation v. The United States of America, UNCITRAL, Final Award on Jurisdiction of August 3, 2005, Part IV, Chapter B, ¶ 29.

51 Vienna Convention on the Law of Treaties adopted on May 22, 1969 (the “Vienna Convention”), Art. 31.

24

V. APPLICATION OF THE FCN TREATY

A. NOBLE HAS PROTECTED INTERESTS UNDER THE FCN TREATY

62. Noble is a U.S. company, duly registered in the U.S. under the laws of the State of

Delaware. It is therefore a “company” within the meaning of Article XXII(3) of the

Treaty:

As used in the present Treaty, the term “companies” means corporations, partnerships, companies and other associations, whether or not with limited liability and whether or not for pecuniary profit. Companies constituted under the applicable laws and regulations within the territories of either Party shall be deemed companies thereof and shall have their juridical status recognized within the territories of the other Party.

63. Noble is the 100% shareholder of NEM, an entity incorporated in the Cayman Islands

and registered for doing business in Israel under the Israeli Companies Ordinance. NEM

is the direct owner of 36% of the rights in the Tamar and Dalit Leases and has ownership

rights under licenses pursuant to which other discoveries have been made. The question,

therefore, is whether the Treaty covers (and thereby protects) Noble’s interest in NEM’s

rights under the licenses and Leases.

64. Resolution of this issue depends on whether the FCN Treaty accords protection to U.S.

companies’ economic “interests” in Israel rather than merely their property “rights.” This

was the distinction drawn by the ICJ in Barcelona Traction, Light and Power Co., Ltd.

(Belgium v. Spain), where the Belgian government sought to exercise diplomatic

protection against Spain for damage sustained by a Canadian company with Belgian

shareholders. The ICJ rejected the claim on the basis that (i) Belgium may only exercise

protection of “rights” of Belgian citizens affected by Spain’s measures; and (ii) Spain’s

measures could have only affected the rights of the Canadian company, not the rights of

its Belgian shareholders. The ICJ expressly pointed out that the derivative damage

sustained by shareholders affects their interests, but not their rights:

25

Not a mere interest affected, but solely a right infringed involves responsibility, so that an act directed against and infringing only the company’s rights does not involve responsibility towards the shareholders, even if their interests are affected.52

65. It is well-settled, however, that treaties may provide protection for economic “interests”