The largest non state-owned and second largest coal ... · 3 Blackgold International Holdings...

13

ASX: BGG www.blackgoldglobal.net Mines and Money Hong Kong Presentation March 2013 The largest non state-owned and second largest coal producer in Chongqing, China by coal reserves Blackgold International Holdings Limited For personal use only

Transcript of The largest non state-owned and second largest coal ... · 3 Blackgold International Holdings...

ASX: BGG

www.blackgoldglobal.net

Mines and Money Hong Kong Presentation

March 2013

The largest non state-owned and

second largest coal producer in

Chongqing, China by coal reserves

Blackgold International

Holdings Limited

For

per

sona

l use

onl

y

2

Important notice

This notice applies to this presentation and any information provided in relation to or in connection with the information contained in it.

All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated. References to “Blackgold” or “Company” are references to Blackgold International Holdings Limited or its applicable subsidiaries.

This presentation contains information in summary form and is for information purposes only. It has been prepared without taking into account the investment objectives, financial circumstances, taxation position or particular needs of investors. Some of the information is based on publicly available sources and information provided to the Company, has not been independently verified or may not be complete. It should be read in conjunction with the Company’s other continuous and periodic disclosure announcements lodged with Australian Securities Exchange, which are available at www.asx.com.au.

Forward-looking statements

This presentation contains forward-looking statements which involve a number of risks and uncertainties.

Where the Company expresses or implies an expectation or belief as to future events or results, such expectation or belief is expressed in good faith and believed to have a reasonable basis. However, forward looking statements are subject to risks, uncertainties and other factors, which could cause actual results to differ materially from future results expressed, projected or implied by such forward looking statements. Such risks include, but are not limited to coal price volatility, currency fluctuations, production performance, increased production costs and variances in coal specifications or recovery rates from those assumed in mining plans, project delay or advancement, environmental risks, approvals and cost estimates, as well as political and operational risks, shipping risks and governmental regulation and judicial outcomes.

The Company does not undertake any obligation to release publicly any revisions to any forward looking statement to reflect events or circumstances after the date of this presentation or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

Competent Person’s Statement

The information in this presentation that relates to Coal Reserves is based on information compiled by Tony Cameron, a Competent Person who is a Member of the Australasian Institute of Mining and Metallurgy and a senior associate of Behre Dolbear Asia. Tony Cameron has sufficient experience that is relevant to the style of mineralization and type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2004 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves. Tony Cameron consents to the reporting of this information in the form and context in which it appears.

The information in this presentation that relates to Coal Resources is based on information compiled by Dr. Tony Guo, a Competent Person who is a Registered Professional Geoscientist of the Professional Engineers and Geoscientists of the Province of British Columbia, Canada with the License #31257. He is a senior associate of Behre Dolbear Asia. He has extensive experience that is relevant to the style of mineralization and type of deposit under consideration and to the activity being under taken. He qualifies as a Competent Person as defined in the 2004 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves. Dr. Guo consents to the reporting of this information in the form and context in which it appears.

Unless otherwise stated, all Mineral Resources figures reported represent estimates at January 2013. Rounding, conforming to the JORC Code, may cause some computational discrepancies.

Disclaimer F

or p

erso

nal u

se o

nly

3

Blackgold International Holdings

Company Highlights

Largest non-state owned and second largest coal producer in Chongqing by coal reserves

Vertically integrated operations from coal mining and sourcing, transportation and storage to

sales and marketing

Own and operate four thermal coal mines with total JORC Compliant proved reserves of 65.3Mt

and probable reserves of 37.0Mt for a total of 102.3Mt1

Own logistics platform provided by private loading port, stockpile coal storage facilities, and our

own fleet of hollow-hull barges transporting coal on the Yangtze River

FY2012 total coal production of 1.2Mt, with 2.4Mt expected for FY2013

66.5% CAGR in NPAT from AUD14.5m in FY2010 to AUD40.2m in FY2012

Excellent safety track record – accredited Class 1 / 2 mines with zero fatal injuries or accidents

Well positioned as regional consolidator to capitalize on PRC coal industry consolidation

Listed on the ASX since February 2011, constituent stock of ASX All Ordinaries Index

Planning for dual primary listing in Hong Kong2

Notes:

1. Behre Dolbear Independent Technical Report, as announced on March 18, 2013

2. Subject to regulatory, shareholders approvals as well as market conditions

For

per

sona

l use

onl

y

4

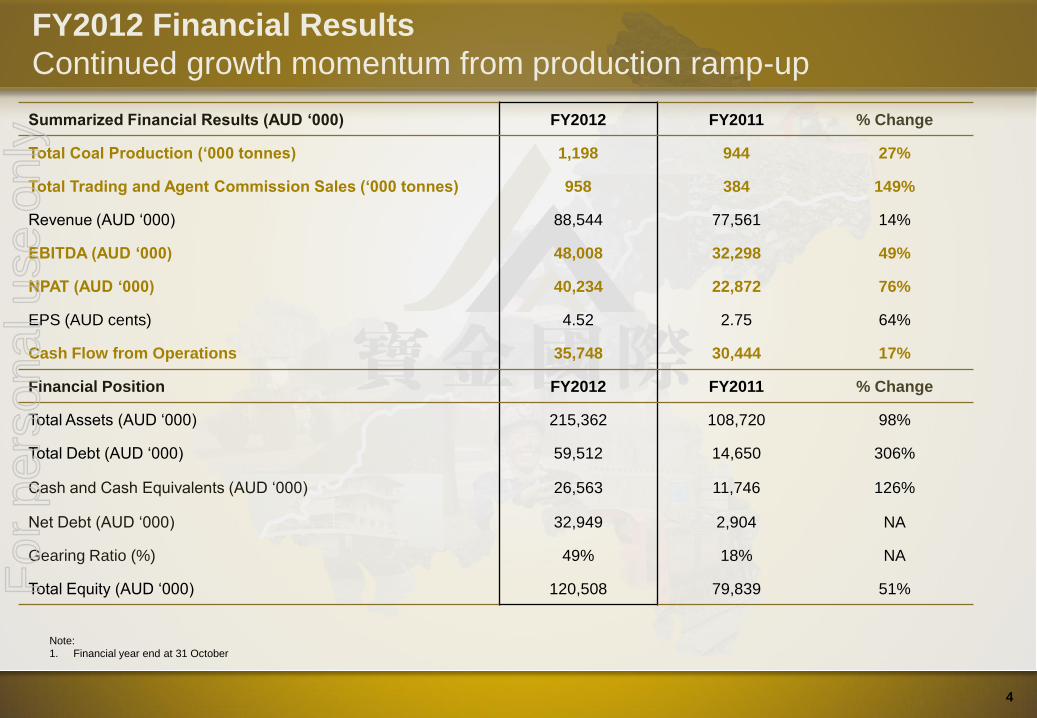

FY2012 Financial Results

Continued growth momentum from production ramp-up

Summarized Financial Results (AUD ‘000) FY2012 FY2011 % Change

Total Coal Production (‘000 tonnes) 1,198 944 27%

Total Trading and Agent Commission Sales (‘000 tonnes) 958 384 149%

Revenue (AUD ‘000) 88,544 77,561 14%

EBITDA (AUD ‘000) 48,008 32,298 49%

NPAT (AUD ‘000) 40,234 22,872 76%

EPS (AUD cents) 4.52 2.75 64%

Cash Flow from Operations 35,748 30,444 17%

Financial Position FY2012 FY2011 % Change

Total Assets (AUD ‘000) 215,362 108,720 98%

Total Debt (AUD ‘000) 59,512 14,650 306%

Cash and Cash Equivalents (AUD ‘000) 26,563 11,746 126%

Net Debt (AUD ‘000) 32,949 2,904 NA

Gearing Ratio (%) 49% 18% NA

Total Equity (AUD ‘000) 120,508 79,839 51%

Note:

1. Financial year end at 31 October

For

per

sona

l use

onl

y

5

Investment Highlights

Experienced management team with proven execution track record

Vertically integrated operations covering entire coal supply value chain

Well positioned as coal sector consolidator in Chongqing region

Solid execution track record with significant production growth pipeline

Strategically located coal mines with logistical advantages and long mine lives 1

2

3

4

5 For

per

sona

l use

onl

y

6

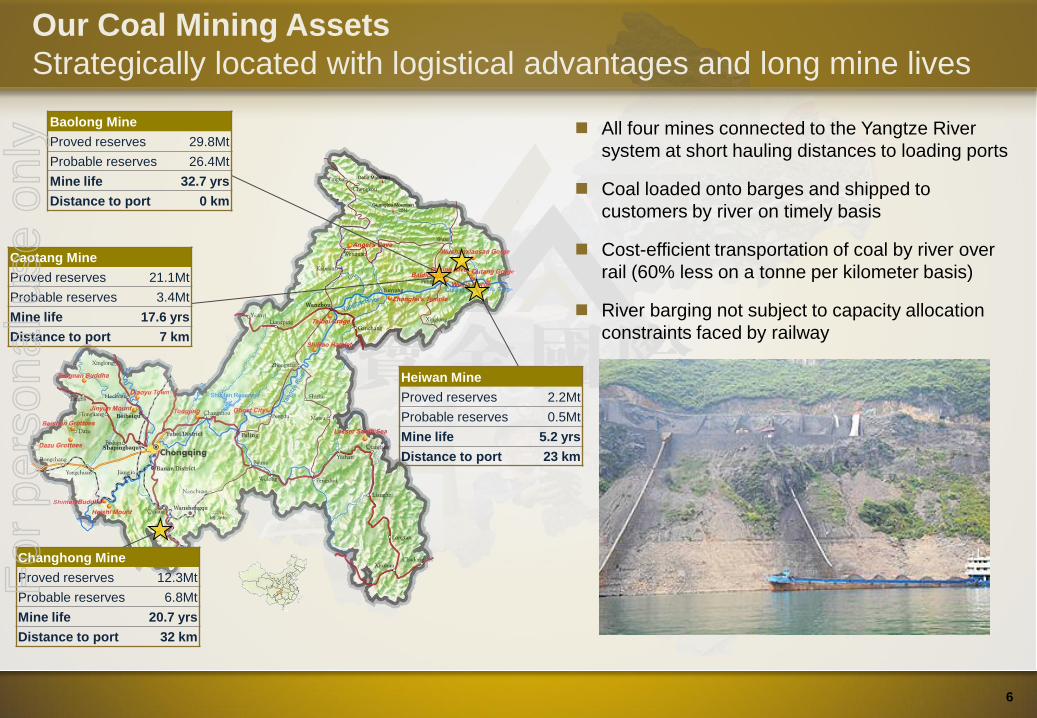

Our Coal Mining Assets

Strategically located with logistical advantages and long mine lives

All four mines connected to the Yangtze River

system at short hauling distances to loading ports

Coal loaded onto barges and shipped to

customers by river on timely basis

Cost-efficient transportation of coal by river over

rail (60% less on a tonne per kilometer basis)

River barging not subject to capacity allocation

constraints faced by railway

Caotang Mine

Proved reserves 21.1Mt

Probable reserves 3.4Mt

Mine life 17.6 yrs

Distance to port 7 km

Baolong Mine

Proved reserves 29.8Mt

Probable reserves 26.4Mt

Mine life 32.7 yrs

Distance to port 0 km

Heiwan Mine

Proved reserves 2.2Mt

Probable reserves 0.5Mt

Mine life 5.2 yrs

Distance to port 23 km

Changhong Mine

Proved reserves 12.3Mt

Probable reserves 6.8Mt

Mine life 20.7 yrs

Distance to port 32 km

For

per

sona

l use

onl

y

7

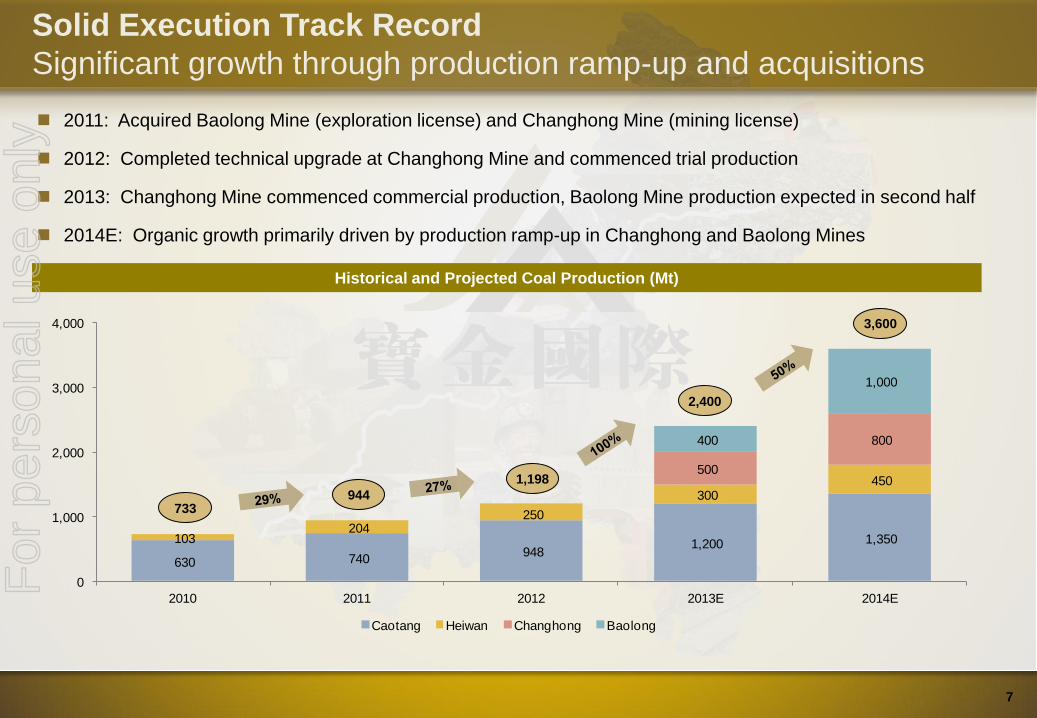

Solid Execution Track Record

Significant growth through production ramp-up and acquisitions

2011: Acquired Baolong Mine (exploration license) and Changhong Mine (mining license)

2012: Completed technical upgrade at Changhong Mine and commenced trial production

2013: Changhong Mine commenced commercial production, Baolong Mine production expected in second half

2014E: Organic growth primarily driven by production ramp-up in Changhong and Baolong Mines

Historical and Projected Coal Production (Mt)

630 740 948

1,200 1,350 103 204

250

300 450

500

800 400

1,000

0

1,000

2,000

3,000

4,000

2010 2011 2012 2013E 2014E

Caotang Heiwan Changhong Baolong

733 944

1,198

2,400

3,600

For

per

sona

l use

onl

y

8

Vertically Integrated Operations

Covering the entire coal supply value chain

Coal sourced from self-production or third

party producers and traders

Own and operate fleet of nine hollow-hull

barges with load capacity of 40,000 tonnes

Private loading port and stockpile coal

storage facilities near our mines

Rights to use seven coal loading ports along

the Yangtze River

Our logistics reach extends from Sichuan

province to Shanghai covering a total of

2,800 km and eight provinces and directly

administered municipalities

Guaranteed and stable transportation

support for our coal products

Sales to end users directly at mine gate or

loading port, or blended coal sales through

our trading arm

Coal Production and

Sourcing

Transportation and

Storage Sales and Marketing

Stockpile Storage at Logistics Hub and Ports

Customers (Coal Traders

and End Users)

Coal Mining

(Self production)

Coal Sourcing (Third Party Coal Producers and Traders)

Transportation by Barges

Storage, Washing,

Blending and Loading onto

Barges

Mining Fees

(Subcontractors)

Ex-Mine Sales

(Sales at Mine Gate or Loading Port)

Coal Trading and

Blended Coal Sales

Caotang Mine

Heiwan Mine

Changhong Mine

Baolong Mine

For

per

sona

l use

onl

y

9

Well Positioned as Coal Sector Consolidator in Chongqing

Capitalize on government driven opportunities

Potential acquisition targets Current Blackgold mines

Baolong Mine

PRC government-driven coal sector consolidation

provides acquisition opportunities

National and local directives require smaller coal

mines to either cease production or be acquired by

larger groups

We are well positioned as regional consolidator

given our status as a listed company, safety track

record, and financial resources

Successfully made two coal mine acquisitions and

integrated into our group’s operations

Continue to focus on making acquisition of mines

situated close to the Yangtze River in the

Chongqing region

For

per

sona

l use

onl

y

10

Experienced Management Team

Proven track record and strong execution capabilities

PENG Yuguo James TONG OU Jun YAO Wenming ZHU Zongxiao LIM Teck Meng

Experienced

management

team

Founder, CEO

and Executive

Director

Chairman and

Non Executive

Director

Executive

Director Chief Geologist

Deputy General

Manager

Financial

Controller

12 years+ in coal

mining and sales

operations

management

12 years+ in

venture capital

investment

20 years+ in coal

mining, trading

and logistics

31 years+ in coal

exploration and

mining

operations

17 years+ in coal

mining and

trading

15 years+ in

accounting and

finance

20 Years of Industry Experience on Average

Proven

execution

track record

Extensive experience in coal production, coal trading, blended coal sales and logistics operations

Successfully completed acquisition and integration of coal mines in Chongqing

Delivered on production ramp-up

Significantly enhanced corporate governance and investor relations since IPO

For

per

sona

l use

onl

y

11

Our Growth Strategies

Acquire additional coal mines in the Chongqing region and further expand and upgrade existing mining operations to increase production capacity

Further investment to increase barging capacity, access to additional loading ports, and stockpile coal storage facilities for storage and blending

Increase investment in mechanization of production process to improve productivity and occupational safety

Plan to build a coal-washing facility at our logistics hub, and expand our logistics hub to handle higher coal throughput

To import coal into China using our import license and expand trading activities

Acquisitions and

capacity

expansion

Coal washing

facility and

expand logistics

hub

Enhance

productivity and

safety

Strengthen

logistics

operations

Strategic

relationship with

international

producers

For

per

sona

l use

onl

y

12

Appendix A

JORC Compliant Coal Reserves and Raw Coal Quality

Notes:

1. Independent Technical Review report by Behre Dolbear Asia, Inc., as announced on the ASX on 18 March 2013.

2. The Company noted there is a discrepancy in the amount of JORC compliant reserves estimated by Behre Dolbear with that indicated in the most recent estimates by Al Maynard & Associates Pty Ltd

(“AM&A”) as announced on 22 February 2013. For details regarding the discrepancy, please refer to the announcement dated 18 March 2013.

JORC Code Compliant Reserves as of 1 January 2013

Mine Proved

(Mt)

Probable

(Mt)

Total

(Mt)

Annual Design

Tonnage (Mt)

Estimated Mine Life

(years)

Caotang 21.1 3.4 24.5 1.5 17.6

Heiwan 2.2 0.5 2.6 0.6 5.2

Baolong 29.8 26.4 56.2 1.8 32.7

Changhong 12.3 6.8 19.0 0.9 20.7

Total 65.3 37.0 102.3 4.8

Average Undiluted Raw Coal Quality of the Reserves as of 1 January 2013

Mine Moisture

(%) ad

Ash

(%) ad

Volatile Matter

(%) ad

FC

(%) ad

Sulphur

(%) ad

CV (kcal/kg)

ar

Caotang 0.63 33.53 7.07 59.32 0.47 4,965

Heiwan 0.76 26.53 6.92 65.56 0.74 5,630

Baolong 0.58 28.39 6.87 62.39 0.57 5,494

Changhong 0.49 18.02 8.89 67.40 2.64 6,788

For

per

sona

l use

onl

y

13

Blackgold International Holdings Limited

12th floor, No.18,Mianhua Street, Yuzhong

District, Chongqing, 400011, PRC

James Chi Ho Tong, Chairman

Tel: +86 (23) 63778222

Fax: +86 (23) 63777154

Mobile: +86 13917552318

E-mail: [email protected]

ASX: BGG

www.blackgoldglobal.net

For

per

sona

l use

onl

y