THE JUBILEE INITIATIVE FOR FINANCIAL INCLUSION Spring 2012 Evaluation Meeting.

51

THE JUBILEE INITIATIVE FOR FINANCIAL INCLUSION Spring 2012 Evaluation Meeting

-

Upload

ann-barham -

Category

Documents

-

view

215 -

download

2

Transcript of THE JUBILEE INITIATIVE FOR FINANCIAL INCLUSION Spring 2012 Evaluation Meeting.

THE JUBILEE INITIATIVE FOR

FINANCIAL INCLUSION

Spring 2012 Evaluation Meeting

Agenda

Presentation Poverty & Payday Loans Microfinance & Alternatives The JiFFi Solution? Further Questions & Challenges Immediate Plans

Critique & Discussion

Methodology

Existing Literature Center for Responsible Lending Filene Research Institute Reports and Papers

Conversations Professors Community leaders Community members

•Consideration of Poverty & PDLs•What is a PDL? Who uses PDLs?•How are PDLs beneficial?•Why might PDLs be problematic?

Poverty & Payday Loans (PDLs)

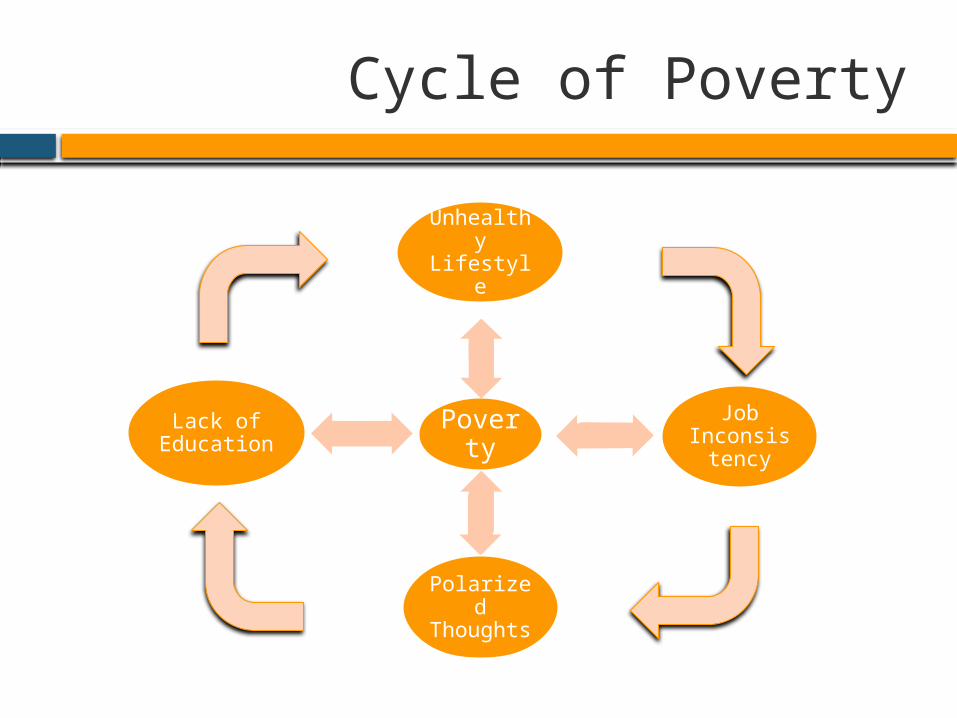

Cycle of Poverty

Poverty

Unhealthy Lifestyle

Job Inconsistency

Polarized Thoughts

Lack of Education

Is It Our Problem?

What does poverty mean for the community? Stints in human potential Wastes resources Hurts the economy

A sustainable community must work to break the cycle of poverty

Poverty Payday Loans

Poverty is not just an economic class, but a job in itself People have learned to manage poverty

The cycle of poverty cannot be broken if it is being managed! Using payday lenders to

Buy extra appliances Loan money to friends and family Pay off a bill

Payday Loans (PDL)

Cash advance against paycheck• $100-500 + fees due next payday• Features rollovers to extend loan

termMarketed for emergency use• Speedy application and

underwriting process• Short term focus• A safety net?

User Demographics

Average Age: 38 Median Income: $25,000 - $30,000 42% homeowners 84% high school graduates Minorities and the lower working-class

African-American neighborhoods have three times as many payday lending stores per capita…

5.5 per 10,000 households working-class neighborhoods vs. 3.4 per 10,000 in poor neighborhoods

Center for American Progress, Who Borrows from Payday Lenders?

Brick and Mortar Payday Stores

Bank Payday Loans

Stores in South Bend

A.Check Into Cash

B.CashlandC.Advance

AmericaD.Cash PlusE.ChecksmartF. Personal

Finance Co.G.Check ‘n Go

Benefits

Responsive to emergency situations Accessible location and time Speedy underwriting process

Tolerates tarnished credit No credit check Does not show up on credit reports

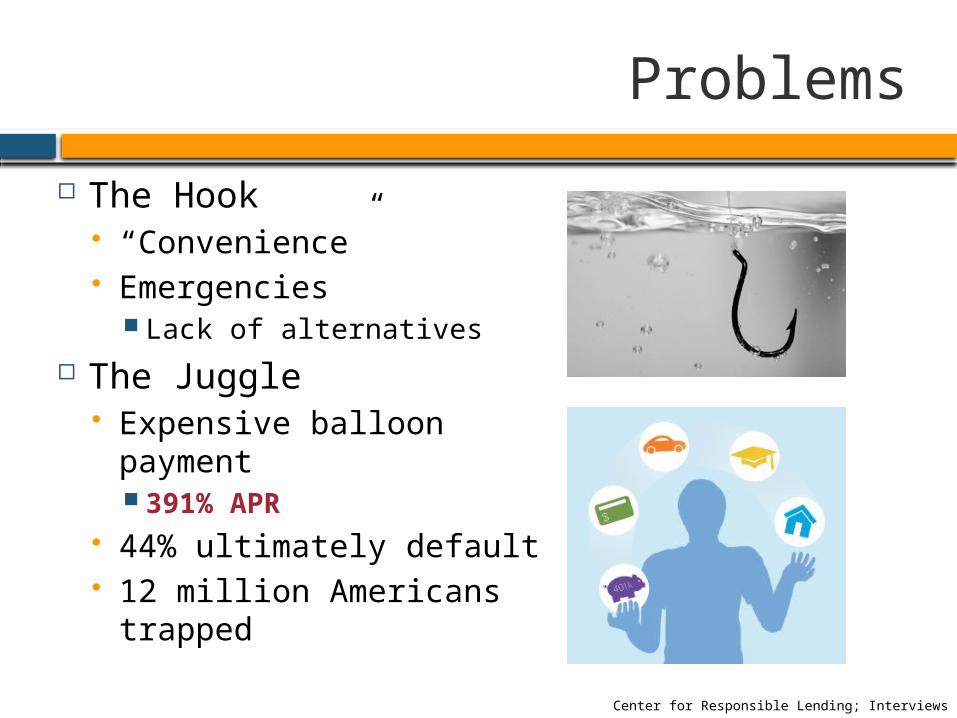

Problems

The Hook “Convenience” Emergencies

Lack of alternatives The Juggle

Expensive balloon payment 391% APR

44% ultimately default 12 million Americans

trappedCenter for Responsible Lending; Interviews

Problems

Inability to repay bank payday loan and meet basic obligations$25,000 Salary $35,000 Salary

Before tax income for two-week pay period $ 962 $ 1,346 minus taxes (66) (105)After tax income 896 1,241

Payday loan balance and fee due (550) (550)

Money left over 346 691 Basic expenses per two-week period (housing, transportation, food healthcare)

(798) (895)

Surplus/(Deficit) $ (452) $ (204) Loan leads to dependence on more loans Average borrower has 9 repeat loans/yr

Center for Responsible Lending

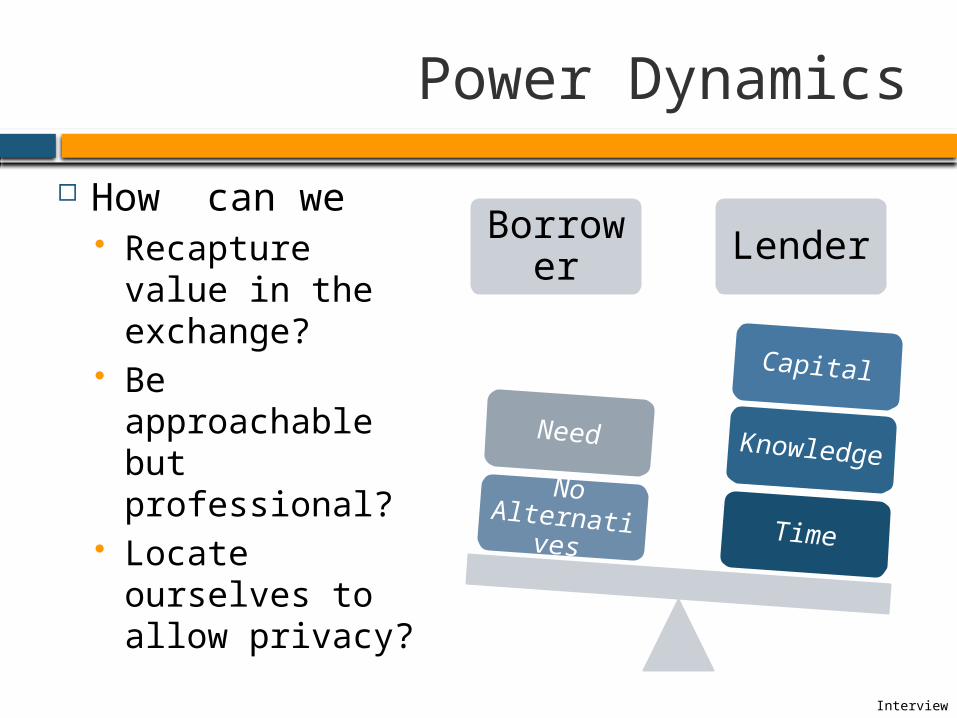

Power Dynamics

How can we Recapture value

in the exchange? Be approachable

but professional? Locate ourselves

to allow privacy?

Borrower Lender

Time

Knowledge

Capital

No Alternative

s

Need

Interview

Impact Summary

Set-up

•Difficult macroeconomic environment

•Paycheck to paycheck lifestyle of poverty

•Emergency and/or unexpected spending

Burden

•Fees - $4.2 bill. in annual profits in a $50 bill. industry

•2.5% of possible family expenditures

•Strenuous loan terms - prominent debt trap

Result

•Wealth stripping – from low or fixed income families

•Effectively weakens purchasing power of working poor

•Breaks the economic backbone in the long run

Center for Responsible Lending, Bureau of Labor Statistics, US Census Bureau

•What is microfinance?•How and why does it work internationally?•Does it work domestically?•Is JiFFi a microfinance organization?

Microfinance

Microfinance

Umbrella term that incorporates many services

The provision of financial services to: Underprivileged Micro-entrepreneurs Small businesses

Lack access to traditional financial services Due to high transaction costs associated with

serving these client categories

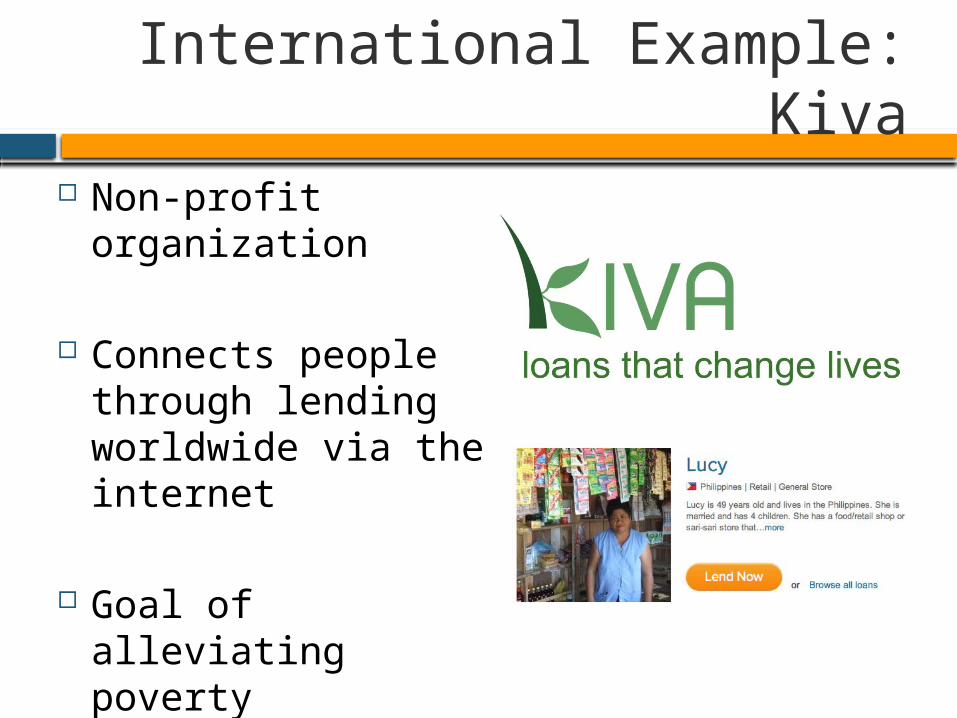

International Example: Kiva

Non-profit organization

Connects people

through lending worldwide via the internet

Goal of alleviating poverty

International Example: Grameen Bank

Helps the world's poorest improve their lives and escape poverty Especially women

Provides the poor access to small loans essential information viable business

opportunities

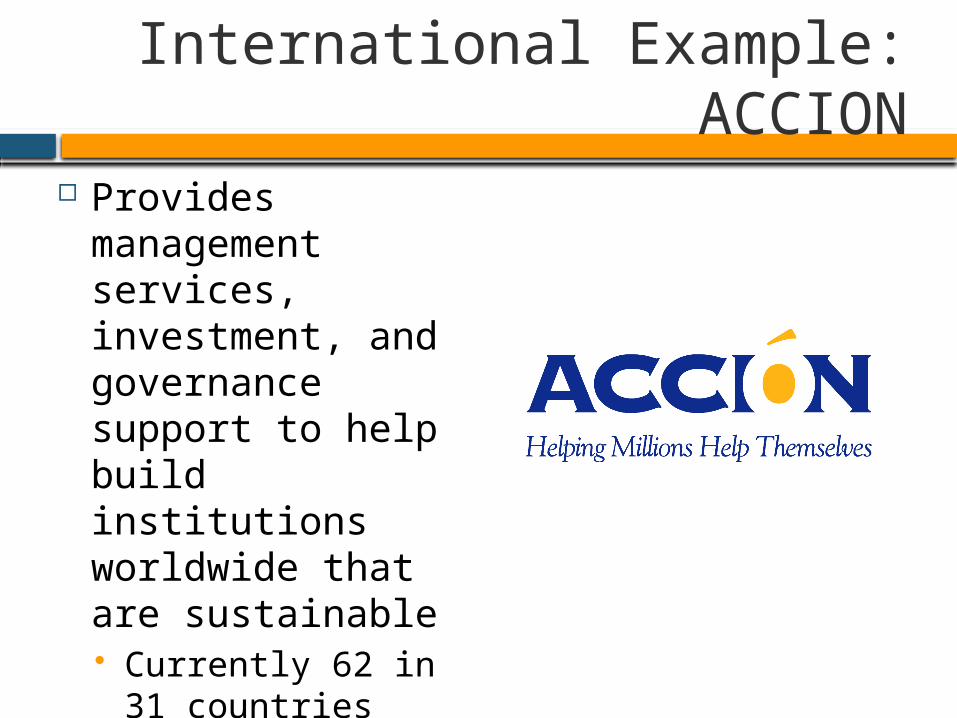

International Example: ACCION

Provides management services, investment, and governance support to help build institutions worldwide that are sustainable Currently 62 in 31

countries Franchise model

Domestic Success & Failure

Success

• Working Capital• Based in Boston• Now part of the

ACCION International network

• Stand-alone peer lending organization

• Operated within existing social groups

• Worked with entrepreneurs

• Also offered a credit building product

Failure

• Good Faith Fund• Based in Pine Bluff,

Arkansas• Imported the Grameen

Bank model • Formed new social

groups• Rather than

working with existing groups

• Did not use groups as an accountability measure• No assumption of

lending responsibility by group

Demographics

Rural Arkansas is vastly different than Boston South Bend is somewhere in the middle

South Bend is home to diverse population 24.8% Black; 11.0% Hispanic, 2.3% Mixed

Can we harness the community to build a successful model like that of international organizations? SJC Bridges out of Poverty participants’

cohesion a great exampleCity-data.com

Is JiFFi a Microfinance Organization?

“Having the opportunity to

earn a little more cash by starting

some kind of business is

perceived by many of the poor as not worth the risk or effort.”

- Richard Taub

Not quite, but focus on: Trust-based

relationships rather than transactional ones

Financial education Building credit Investments for the

future Not just consumption

Future plans for micro-venturing arm

•South Side Community Federal Credit Union•GoodMoney•ZestCash•Others

Existing Alternatives to PDL

South Side Community Federal Credit Union

Payday Alternative Loans (+) $200 - $1000; 15% Terms from 1 to 6 months Free credit building &

financial education classes

Challenges Requires membership Low volume

Interview

GoodMoney

Collaboration between Prospera Credit Union & Goodwill stores

Short-term loans half the rates

payday lenders Other banking

services Referrals to the

Financial Information and Service Center (FISC)*

ZestCash

Founded by former CIO of Google

Features user tailored loans For-profit, very expensive

High fees Compound interest

Other

Banks & Credit Unions Option usually exhausted

Personal Finance Companies Similar steep fees

Family & Friends Potential negative social implications Only 5% consider this alternative

Caskey, Economics of Payday Lending

•What are the lessons?•What are the goals to achieve?•What should a JiFFi loan look like?

The JiFFi Solution?

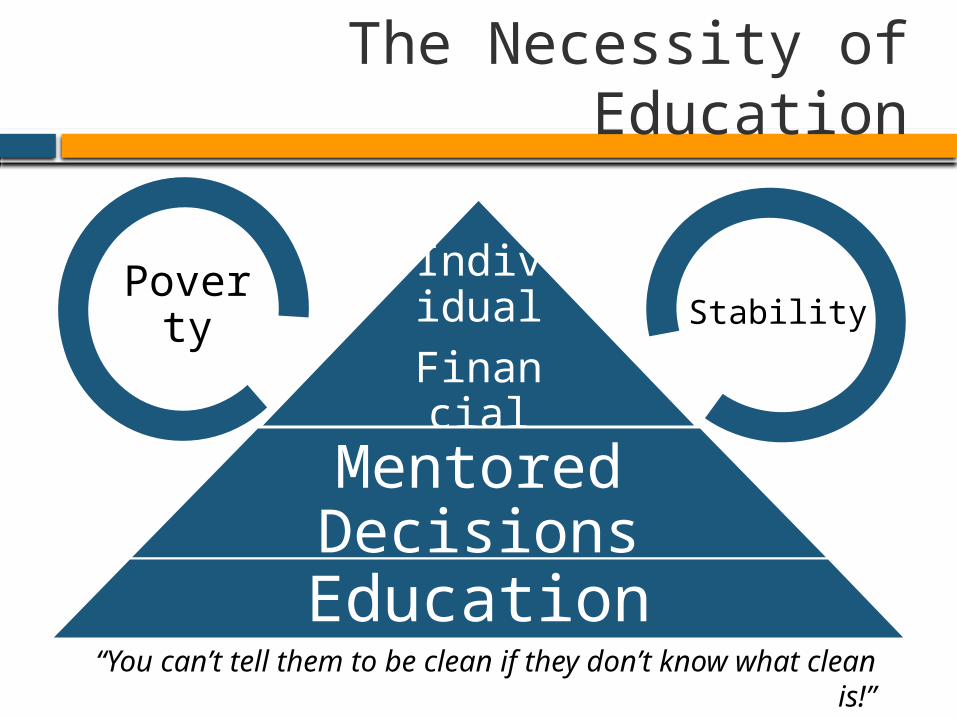

The Necessity of Education

Individual Financial Success

Mentored DecisionsEducation

Poverty Stability

“You can’t tell them to be clean if they don’t know what clean is!”

Class Perspectives

Necessary to understand

Each social class has its own habits

Habits determine what drives actions: what is the motivation? The final goal?

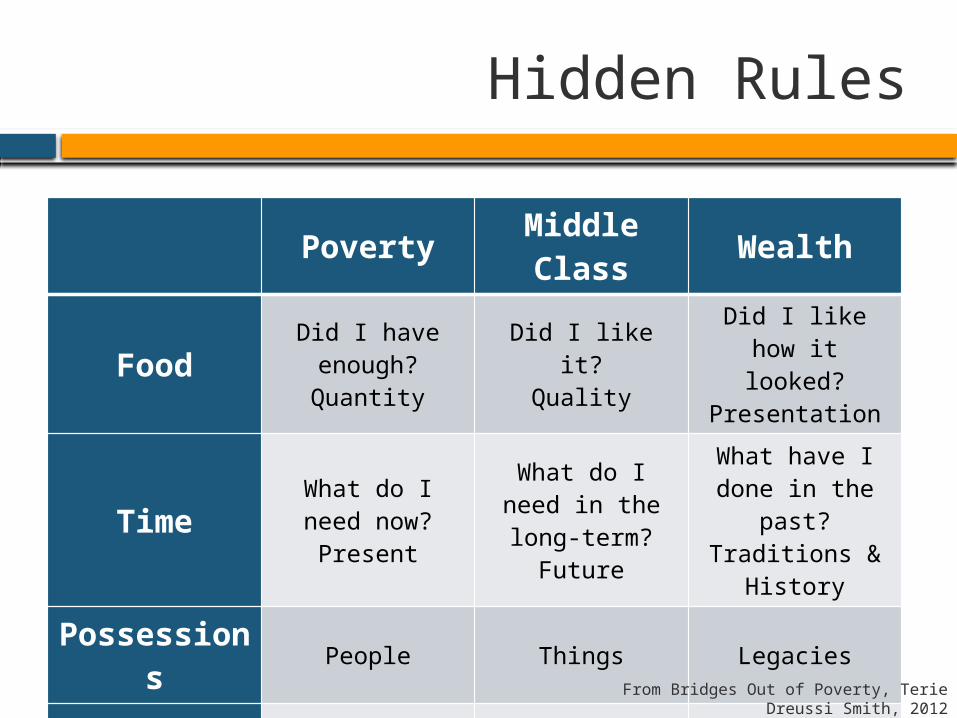

Hidden Rules

PovertyMiddle Class

Wealth

FoodDid I have enough?Quantity

Did I like it?Quality

Did I like how it looked?

Presentation

TimeWhat do I need

now?Present

What do I need in the long-

term?Future

What have I done in the

past?Traditions &

History

Possessions

People Things Legacies

Money To be used! To be managed! To be invested!From Bridges Out of Poverty, Terie Dreussi

Smith, 2012

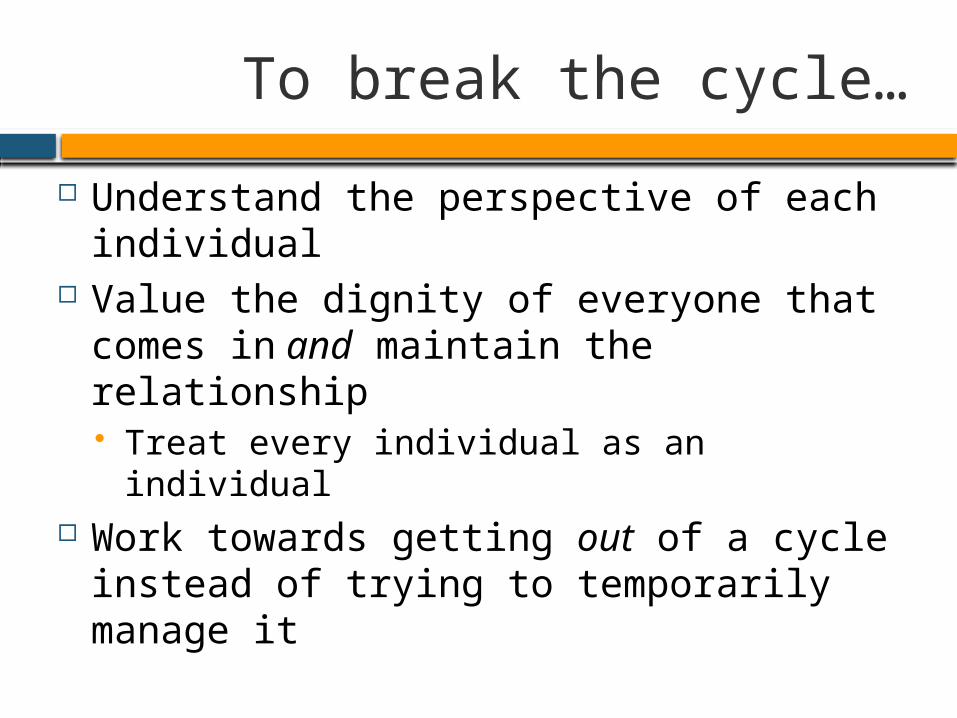

To break the cycle…

Understand the perspective of each individual

Value the dignity of everyone that comes in and maintain the relationship Treat every individual as an individual

Work towards getting out of a cycle instead of trying to temporarily manage it

Ingredients for Success

JiFFi

Appropriate Financial Tools

Long Term Relations

Education & Guidance

Emergencies happen Nudge factor

Vision of possibilities Trading “rules”

Clients’ long term success Client sets financial

goals Provide accountability

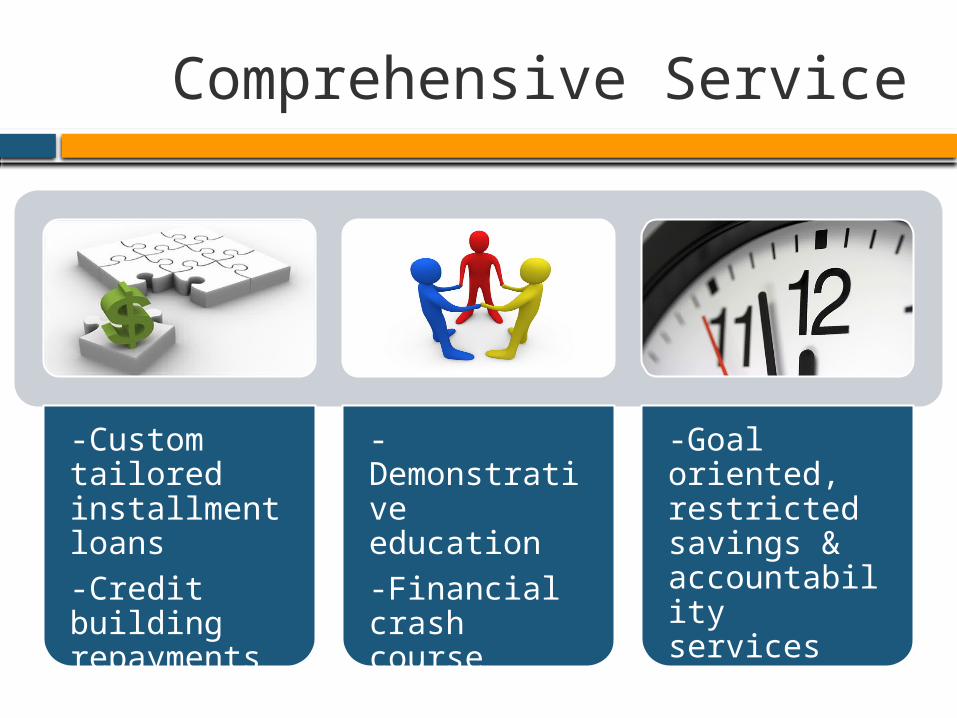

Comprehensive Service

-Custom tailored installment loans-Credit building repayments

-Demonstrative education-Financial crash course series

-Goal oriented, restricted savings & accountability services

Product Snapshot

• Statement of purpose required; amount co-determined with JiFFi

• 12% simple interest, custom tailored repayment plan

• Redeemable “In Your Own Interest” amount (33% of interest)

JiFFi Personal Loan

• Goal-oriented savings and matching program• Inaccessible unless pre-determined conditions are

met

Restricted Savings Program

• Platform for ND students and community entrepreneurs to meet

Consultation (Future)

Achieve Multiple Goals

Solve

Emergency

EstablishRelationship

Guide FinancialDecisions

Encourag

e Communication

JiFFi

Value Dignity

Busi

ness

Soci

al

•What are some social challenges?•What are some business problems?•We need your help!

Further Questions & Challenges

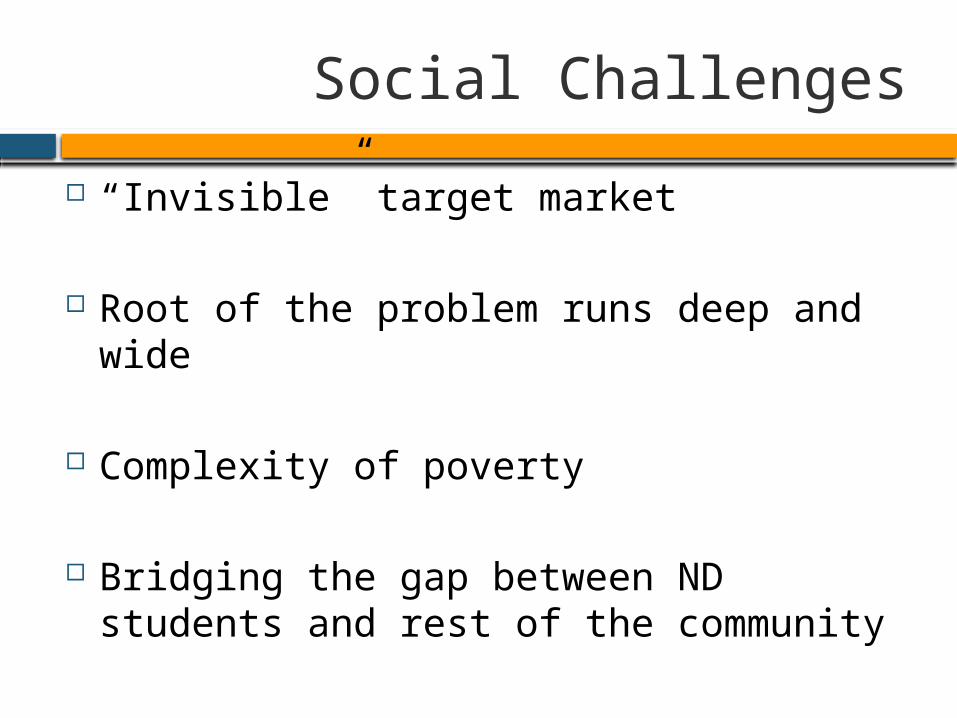

Social Challenges

“Invisible” target market

Root of the problem runs deep and wide

Complexity of poverty

Bridging the gap between ND students and rest of the community

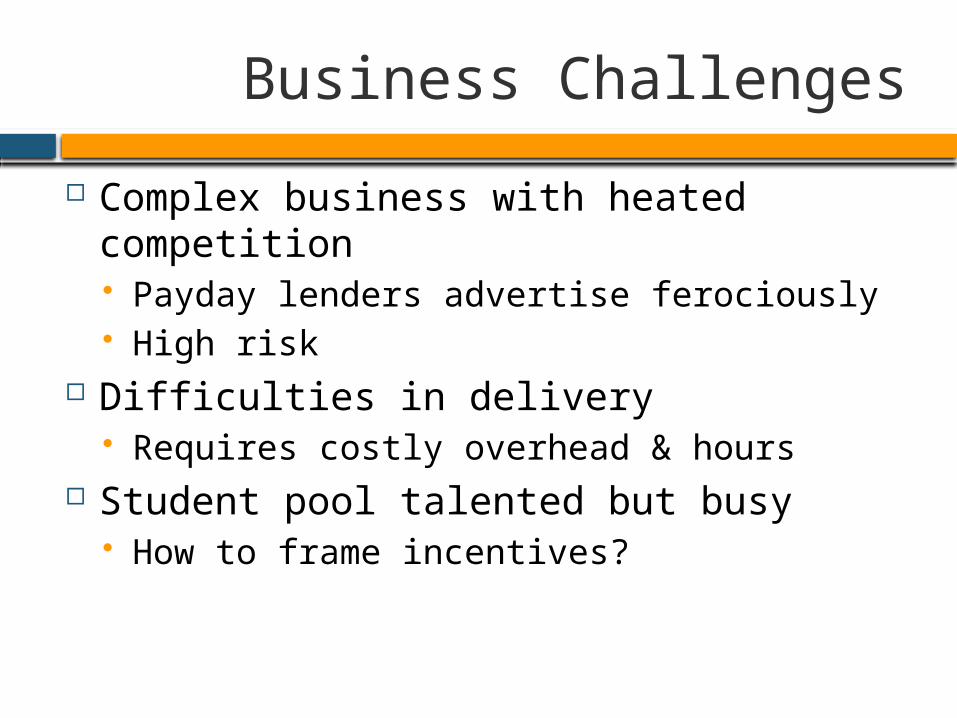

Business Challenges

Complex business with heated competition Payday lenders advertise ferociously High risk

Difficulties in delivery Requires costly overhead & hours

Student pool talented but busy How to frame incentives?

South Bend Household Budget Est.

Indiana Business Review

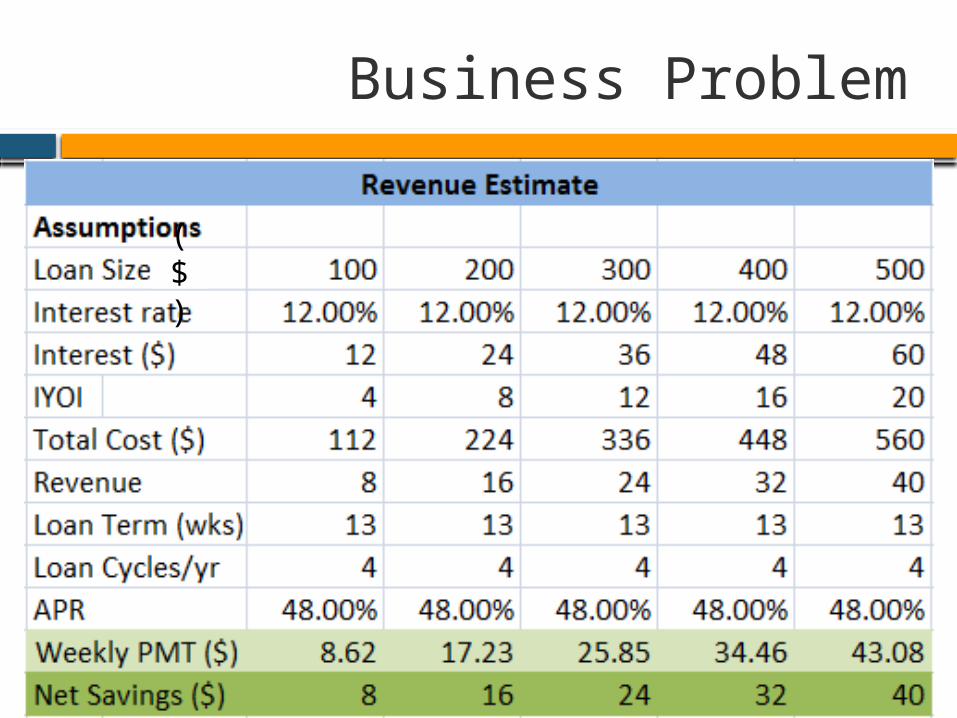

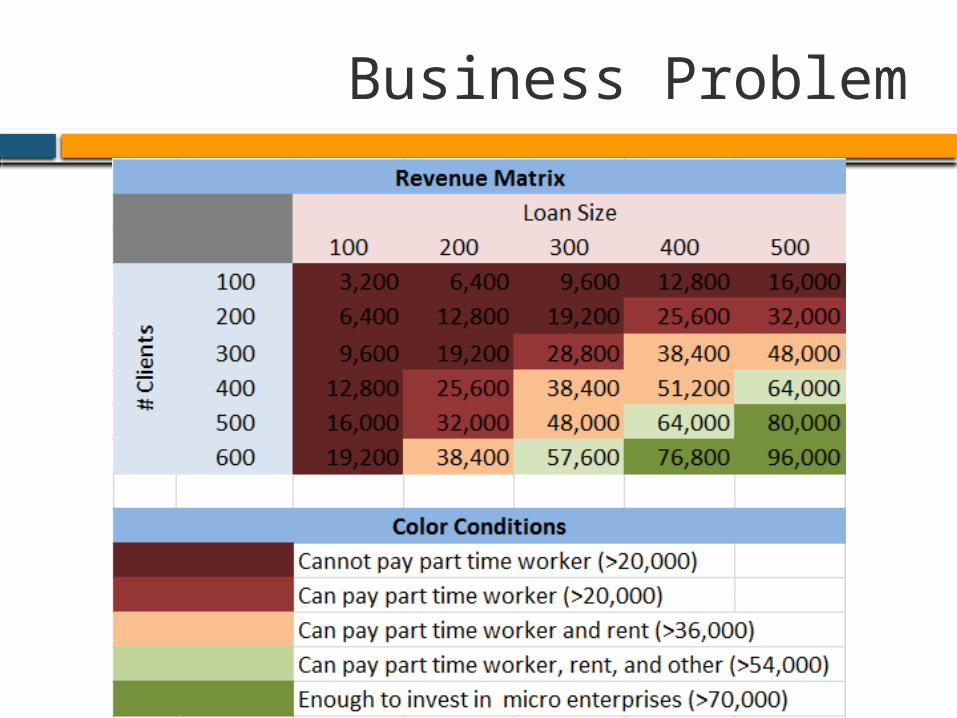

Business Problem

($)

Business Problem

Business Problem

Simplistic & optimistic estimate Overall loss of $(8,332) in the first year 2014 full capacity overall income of

$2,800

We Need Your Help!

Academic assistance Data collection & impact evaluation Legal support Business plan generation

Student & faculty involvement Human capital intensive – student groups Board of advisors – faculty and other leaders

Local cooperation Complex problems; help from local

organizations Input and support from local government

What are we going to do in the Summer and Fall?

Immediate Plans

Plans

Summer Personal research and development

Summer programs & internships Acquaint with community

Fall Re-evaluate purpose, model, team McCloskey Business Plan Competition Test products

Video

Summary

Presentation Payday Loans Microfinance & Alternatives The JiFFi Solution? Further Questions & Challenges Immediate Plans Video

Critique & Discussion