The Investor's Guide to the New Zealand Seafood Industry 2017 · Coriolis report “New Zealand...

82

THE INVESTOR’S GUIDE TO THE NEW ZEALAND SEAFOOD INDUSTRY 2017 Part of the New Zealand Food & Beverage Information Project FINAL REPORT; v1.05; June 2017

Transcript of The Investor's Guide to the New Zealand Seafood Industry 2017 · Coriolis report “New Zealand...

THE INVESTOR’S GUIDE TO THE NEW ZEALAND SEAFOOD INDUSTRY 2017 Part of the New Zealand Food & Beverage Information Project

FINAL REPORT; v1.05; June 2017

STEERING & GUIDANCE

This project would not have been possible without the strong guidance of ourSteering Committee. In particular, we would like to thank Andrew McCallumof MBIE for his tireless energy in keeping this project on track, while at thesame time pushing us forward.

Draft versions of parts of this document were distributed to key firms forcomment, addition or correction. This was done in the form of emails andphone calls. We thank those who helped us in this process for their time andeffort. We also thank those who provided their photos.

We are grateful for all of the input we have received, but the report is oursand any errors are our own.

Finally, we acknowledge the support of the Ministry of Business, Innovationand Employment (MBIE), New Zealand Trade and Enterprise (NZTE) and theMinistry of Primary Industries (MPI). It is their funding that has made thisreport possible.

CONSTRAINTS & INHERENT LIMITATIONS

This work was commissioned by the Ministry of Business, Innovation andEmployment (MBIE) and prepared by Coriolis. This work is based onsecondary market research, analysis of information available or provided toCoriolis by our client, and a range of interviews with industry participants andindustry experts. Coriolis have not independently verified this informationand make no representation or warranty, express or implied, that suchinformation is accurate or complete.

The report is dated June 2017 and Coriolis accepts no liability for, and has notundertaken work in respect of, any event subsequent to that date, which mayaffect the report.

Key global trade data analysed in all sections of the F&B Information projectare calculated and displayed in US$. This is done for a range of reasons:

- It is the currency most used in international trade- It allows for cross country comparisons (e.g. vs. Denmark)- It removes the impact of NZD exchange rate variability- It is more comprehensible to non-NZ audiences (e.g. foreign investors)- It is the currency in which the United Nations collects and tabulates

global trade data

Anyone should feel free to call the authors if any of the material cannot beunderstood or accessed. We always welcome opportunities to discuss ourresearch with our readers and users.

Projected market information, analyses and conclusions contained herein arebased (unless sourced otherwise) on the information described above and onCoriolis’ judgment, and should not be construed as definitive forecasts orguarantees of future performance or results. Neither Coriolis nor its officers,directors, shareholders, employees or agents accept any responsibility orliability with respect to this document.

Coriolis wishes to draw your attention to the following limitations of theCoriolis report “New Zealand Seafood Industry 2017“ (the Coriolis Report)including any accompanying presentation, appendices and commentary (theCoriolis Commentary):

a. Coriolis has not been asked to independently verify or audit theinformation or material provided to it by, or on behalf of the Client, or any ofthe parties involved in the project;

b. the information contained in the Coriolis Report and any CoriolisCommentary has been compiled from information and material supplied bythird party sources and publicly available information which may (in part) beinaccurate or incomplete;

c. Coriolis makes no representation, warranty or guarantee, whether expressor implied, as to the quality, accuracy, reliability, currency or completeness ofthe information provided in the Coriolis Report and any Coriolis Commentary,or that reasonable care has been taken in compiling or preparing them;

d. the analysis contained in the Coriolis Report and any Coriolis Commentaryare subject to the key assumptions, further qualifications and limitationsincluded in the Coriolis Report and Coriolis Commentary, and are subject tosignificant uncertainties and contingencies, some of which, if not all, areoutside the control of Coriolis; and

e. any Coriolis Commentary accompanying the Coriolis Report is an integralpart of interpreting the Coriolis Report. Consideration of the Coriolis Reportwill be incomplete if it is reviewed in the absence of the Coriolis Commentaryand Coriolis conclusions may be misinterpreted if the Coriolis Report isreviewed in absence of the Coriolis Commentary.

Coriolis is not responsible or liable in any way for any loss or damageincurred by any person or entity relying on the information in, and theRecipient unconditionally and irrevocably releases Coriolis from liability forloss or damage of any kind whatsoever arising from, the Coriolis Report orCoriolis Commentary including without limitation judgments, opinions,hypothesis, views, forecasts or any other outputs therein and anyinterpretation, opinion or conclusion that the Recipient may form as a resultof examining the Coriolis Report or Coriolis Commentary.

The Coriolis Report and any Coriolis Commentary may not be relied upon bythe Recipient, and any use of, or reliance on that material is entirely at theirown risk. Coriolis shall have no liability for any loss or damage arising out ofany such use.

Unless otherwise noted, all photos used in this discussion document wereprovided by the New Zealand Story resource (www.nzstory.govt.nz),purchased by Coriolis from a range of stock photography providers asdocumented, or are low resolution, complete product/brand for illustrativepurposes used under fair dealing/fair use for both “research and study” and“review and criticism”. Our usage of them complies with New Zealand law ortheir various license agreements.

Cover image: New Zealand Story

Where appropriate, this document is Copyright © 2017 Coriolis and MBIE.However, please feel welcome to use, refer to and cite this research.

+ Purpose

+ Situation summary

+ Drivers of success

+ Investment opportunities

+ SWOT

+ Supply chain

+ Global situation

+ Consumption

+ Production

+ Import demand

+ Key markets

+ Market growth

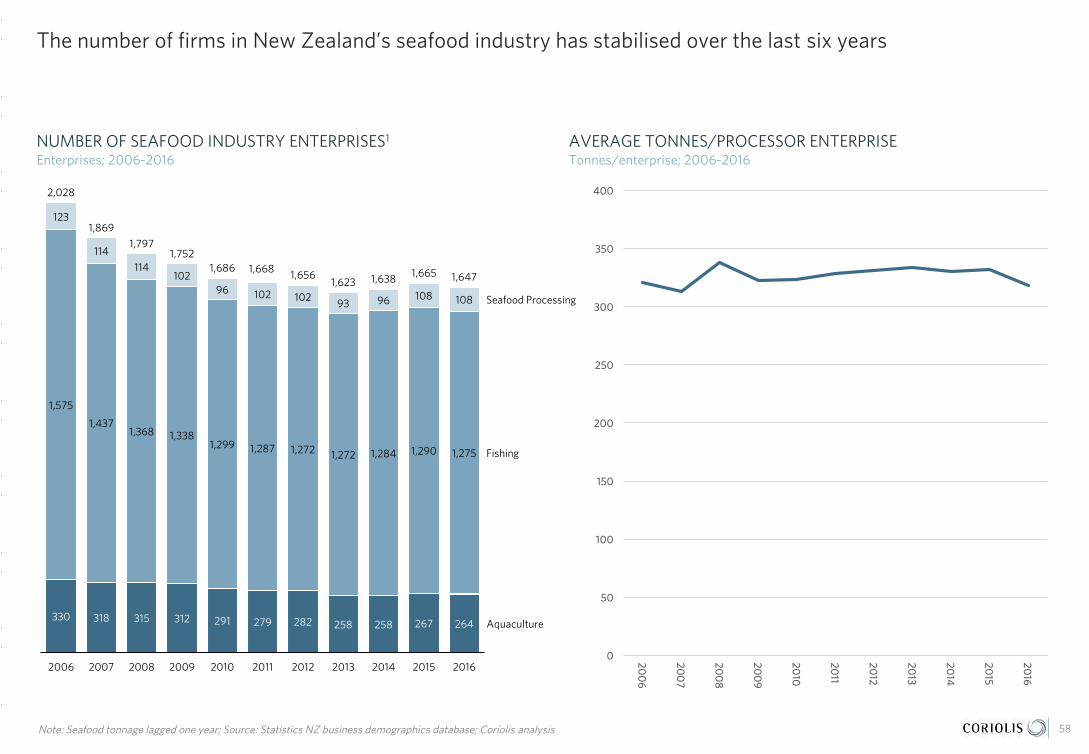

+ Number of firms

+ Employment

+ Yield/productivity

+ Production

+ Regional activity

+ Growth upside

+ Segmentation

+ Key products

+ Exports by product

+ Horizons for growth

+ Emerging export stars

+ New viable options

+ Mega-trends driving change

+ Innovation & new products

Market Overview

Context & Conclusions

Production Categories Growth & Innovation

01 02 03 04INTRO

TABLE OF CONTENTS

+ Enterprises

+ Employment

+ Turnover

+ Ownership

+ Foreign investors

+ Acquisitions

+ Investments

+ Firm Profiles

Firms Performance

05

Pages 3-10 Pages 11-26 Pages 27-31 Pages 32-40 Pages 41-54 Pages 55+

PURPOSE Why did the New Zealand government undertake this project?

4

The project presents a comprehensive, business-focused overview of the total New Zealand food & beverage industry.

The project pulls together the available information on the food and beverage industry into one place, in a form which is familiar and useful to business. The reports contain analysis and interpretation of trends and opportunities to materially assist with business strategy and government policy.

The information will be of vital use to businesses, investors, government, and research institutions as the industry expands and diversifies. This industry view will be very useful to government, enabling better dialogue and the opportunity to address issues collectively.

– As support for raising capital

– As a base of market intelligence to enable business to be much more targeted in their own market research

– Reviewing and informing offshore market development (including export and investment) strategies

– Assisting in identifying areas of innovation and R&D for the future

– Identifying strategic partners and collaborators

– Enabling a company to benchmark performance with that of its competitors

– Monitoring industry activity

– Gaining a better understanding of their own industry sector

– Identifying internal capability needs or external inputs

While the government collects large amounts of industry data, little of this has an investor or industry-driven perspective.

This information will provide much greater insight into the industry, which is useful for a range of policy developments, from regulatory frameworks to investment in science and skills and facilitating access to international markets.

In particular, a single source of factual information will enable government agencies to better coordinate their efforts across the system and be more responsive to addressing industry issues.

All project resources are available online at:

www.foodandbeverage.govt.nz

What is the purpose of the project? What benefit will this bring to businesses? How will government use the reports?

SITUATION SUMMARY: WILD CAPTURE While New Zealand has a large and sustainably managed wild catch fishery, there is little likelihood of significant volume or throughput increases going forward

5

ALL SEAFOOD: CONSUMERS/MARKETS

Per capita consumption of wild capture seafood hasbeen flat-to-declining globally, due to overfishing andpopulation growing faster than capture quantity. This“deficiency” is being made up for by a massiveexpansion in aquaculture.

Increased consumer demand for seafood across mostdeveloped countries is being driven by (1) scientificresearch showing health benefits and (2) changingdiets. At the same time, key seafood consumingcountries (e.g. South East Asia (SEA), China) areexperiencing growing incomes leading to increasedability to pay for (or demand) more seafood. Thissituation has supported prices.

The majority of fish consumption globally occurs inrestaurants and other foodservice outlets.Supermarkets underperform in seafood (relative toother proteins); significant sales occur in moretraditional channels (e.g. fishmongers and wetmarkets)

Demand for sustainable product varies by market.There is increasing demand in Western markets(Europe/North America), for sustainable productsoften driven by retailers (and vocal activists).However, there is currently low/no demand in Asianand developing markets for sustainability.

NZ exports seafood to over a hundred countries.Broadly speaking Western markets account for about

half of value and the growing Asian market the otherhalf.

Fresh seafood is a highly perishable product and thehighest value products are often those sold fresh(unlike some other foods). Bulk fish for furtherprocessing is also a key channel for NZ.

WILD CAPTURE: NEW ZEALAND

New Zealand has access to a strong set of naturalresources for wild capture fishing. The country is anisolated island nation in the middle of the SouthPacific, 2,100 kilometres from Australia. It has theninth largest exclusive fishing zone (EEZ1) and thetenth longest coastline of any country in the world.

Multiple sources suggest New Zealand’s fisheries areamong the most sustainable fisheries in the world (ona par with Alaska and Iceland). New Zealand useseffectively the same catch management system asIceland. However sustainable management has led toa decline in total wild capture over the past 15 yearsand there is low potential for substantial futuregrowth. Precision Harvesting research over recentyears is driving towards increasing the quality andtherefore value of the catch.

New Zealand has an efficient, modern seafoodindustry with large modern boats, in particular thedeep sea freezer trawlers. More than 130 species arecommercially fished in New Zealand’s EEZ, a similarspecies mix to Australia, Chile, Argentina, etc. The

main catch by volume is hoki, followed by mackereland squid. Rock Lobster are a major export that haveshown strong growth on rapidly growing demandfrom China.

Wild capture fishing is reasonably consolidated, witha handful of major firms and a range of secondaryfirms. Consolidation is more pronounced in deepwater fishing, less so in closer waters.

The industry has mixed ownership, with New ZealandMaori tribal interests predominating, but with onelisted firm (Sanford) and strong private ownershipand foreign investment (primarily Japanese).

WILD CAPTURE: COMPETITORS

NZ achieves a 7% share of the temperate SouthernHemisphere (S.H.) wild catch.2 New Zealandcompetes in the first instance with other colder waterSouthern Hemisphere countries, primarily Australia,Chile, Argentina, and South Africa. Secondarily, thisgroup compete with Northern Hemisphere colderwater fisheries, including Norway, Canada, Iceland,USA/Alaska, UK/Scotland.

Globally the wild capture seafood industry isfragmented with a huge number of medium to smallsized firms competing. Around the world in-shorefishing is highly fragmented and primarily localaround the world. Deepwater fishing is moreconsolidated due to capital requirements for largeboats, but still fragmented globally.

1. EEZ = Exclusive Economic Zone; 2. defined as Chile, Argentina, Brazil, South Africa, NZ & AU; Source: Coriolis

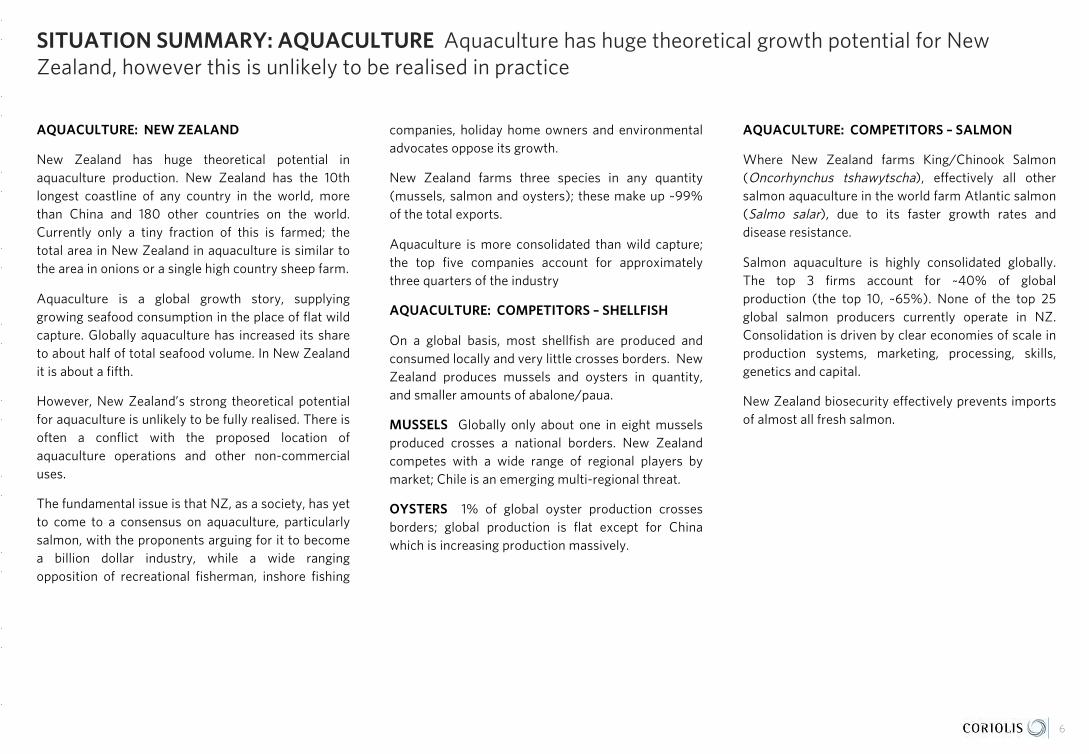

SITUATION SUMMARY: AQUACULTURE Aquaculture has huge theoretical growth potential for New Zealand, however this is unlikely to be realised in practice

6

AQUACULTURE: NEW ZEALAND

New Zealand has huge theoretical potential inaquaculture production. New Zealand has the 10thlongest coastline of any country in the world, morethan China and 180 other countries on the world.Currently only a tiny fraction of this is farmed; thetotal area in New Zealand in aquaculture is similar tothe area in onions or a single high country sheep farm.

Aquaculture is a global growth story, supplyinggrowing seafood consumption in the place of flat wildcapture. Globally aquaculture has increased its shareto about half of total seafood volume. In New Zealandit is about a fifth.

However, New Zealand’s strong theoretical potentialfor aquaculture is unlikely to be fully realised. There isoften a conflict with the proposed location ofaquaculture operations and other non-commercialuses.

The fundamental issue is that NZ, as a society, has yetto come to a consensus on aquaculture, particularlysalmon, with the proponents arguing for it to becomea billion dollar industry, while a wide rangingopposition of recreational fisherman, inshore fishing

companies, holiday home owners and environmentaladvocates oppose its growth.

New Zealand farms three species in any quantity(mussels, salmon and oysters); these make up ~99%of the total exports.

Aquaculture is more consolidated than wild capture;the top five companies account for approximatelythree quarters of the industry

AQUACULTURE: COMPETITORS – SHELLFISH

On a global basis, most shellfish are produced andconsumed locally and very little crosses borders. NewZealand produces mussels and oysters in quantity,and smaller amounts of abalone/paua.

MUSSELS Globally only about one in eight musselsproduced crosses a national borders. New Zealandcompetes with a wide range of regional players bymarket; Chile is an emerging multi-regional threat.

OYSTERS 1% of global oyster production crossesborders; global production is flat except for Chinawhich is increasing production massively.

AQUACULTURE: COMPETITORS – SALMON

Where New Zealand farms King/Chinook Salmon(Oncorhynchus tshawytscha), effectively all othersalmon aquaculture in the world farm Atlantic salmon(Salmo salar), due to its faster growth rates anddisease resistance.

Salmon aquaculture is highly consolidated globally.The top 3 firms account for ~40% of globalproduction (the top 10, ~65%). None of the top 25global salmon producers currently operate in NZ.Consolidation is driven by clear economies of scale inproduction systems, marketing, processing, skills,genetics and capital.

New Zealand biosecurity effectively prevents importsof almost all fresh salmon.

DRIVERS OF SUCCESS New Zealand’s success in seafood has three key drivers

Source: photo credit (purchased or creative commons (freenzphotos.com)) 7

- Strong natural resources for wild capture fishing

- Resources available for aquaculture

- Substantial exclusive fishing zone (EEZ) available for fishing

- Isolated location protected by natural barriers

Available resource

IDEAL WATER & CLIMATE EFFICIENT PEOPLE & SYSTEMS LOCATION & MARKETS

Trusted byconsumers

High share in key products

- Long history of seafood production

- Industry focused on export for over 100 years

- Large pool of skilled people

- Strong Quota Management System and support networks

- Well-organised, cohesive industry

- Excellent proximity to East & South-East Asian markets

- CER agreement with Australia

- Excellent market access across Asia

- NZ was the first developed country to sign a free trade deal with China (2008)

INVESTMENT OPPORTUNITIES There are limited opportunities for new external investment in wild capture; regulatory change and fundamental drivers create more opportunities in aquaculture

8

OOVVEERRAALLLL There are limited entry vehicles for newinvestors into seafood, as industry ownership of largerfirms is locked up by:

- Maori interests (unlikely to sell),

- Family businesses (Talleys, United, Independent, Solander, Vela) unlikely to sell without generational change.

- Cornerstone shareholdings of large global seafood companies (e.g. Nissui in Sealord)

- Long-term cornerstone shareholders in both publicly-listed firms: Sanford (Amalgamated) and New Zealand King Salmon (Oregon Group)

Investors seeking smaller opportunities will find awide range of opportunities among the second tier ofinteresting and innovative firms, many of which areseeking capital.

WILD CAPTURE The industry has a strong andeffective sustainability management system. Thissystem implies that New Zealand will have relativelymore fish in the future compared with overfishedcountries and regions.

Main source of value creation in wild capture is incost reductions via consolidation. This consolidation

is on-going, but progress is slow due to the ownershipissues discussed above. There are also opportunitiesin value creation through delivering a greater percentof the catch to the market in a more fresh/lessdamaged form (see the Precision Seafood HarvestingPrimary Growth Partnership programme, which is apartnership between industry and the Crown.’).

There are opportunities for growth and certainlyopportunities to find new markets for by-products andfish species that are not currently processed orretained.

AAQQUUAACCUULLTTUURREE The attractiveness of New Zealandaquaculture varies by species:

OYSTERS Pacific oysters have low growth potential,due to risks with potential new viral breakouts andglobal market structure/situation.

MUSSELS The industry is mature and consolidatingrapidly. Mussels are relatively low value use of space.Returns over the past twenty years have been mixedand cyclical, particularly for smaller operators (drivingindustry consolidation).

The SpatNZ Primary Growth Partnership programmeis a partnership between industry and the Crownwhich is supporting selective breeding. Theprogramme is on target to deliver hatchery grownmussel spat and will likely deliver constant

incremental gains in the future. However these aremore likely to maintain New Zealand’s relativecompetitiveness (e.g. vs. Chile) rather than translateinto dramatically increased profitability.

SALMON Theoretically New Zealand has hugepotential in salmon aquaculture; in practiceregulations and competing interests will likelyconstrain success. Industry is showing on-goingconsolidation. The largest salmon producer – NewZealand King Salmon – listed on the NZX/ASXsharemarket in late 2016.

NEW SPECIES New Zealand scientists are working ona wide range of new species, however these are allhighly speculative and unproven commercially todate. Only investors with transferable capabilities orstrong appetite for risk should participate. Recentpreliminary success in scampi aquaculture stands out.

FURTHER PROCESSING There are opportunities forinvestment in further processing of New Zealand bulkingredients (e.g. “white fish”) into consumer readyproducts, however this is primarily a greenfieldsopportunity for firms with transferrable skills.

There are clear opportunities for investment inseafood derived products (e.g. nutraceuticals,supplements, petfood)

SWOT ANALYSIS New Zealand has a stable and sustainable position in the global seafood industry

STRENGTHS WEAKNESSES

- Clean water and generally healthy aquatic environment- Unsubsidised industry- Early introduction of quota management system prevented collapse of stocks

through overfishing- Stocks generally at sustainable levels or rebuilding- Regularly ranked in top three sustainable regions- Efficient, modern industry with large modern boats, in particular the deep sea

freezer trawlers- Stable, long-term ownership in place across most major firms - Only country farming green lipped mussels (Perna canaliculus); others farm a

different green shelled species (perna viridis, etc.) or blue mussels (mytilus sp.)- Limited presence of disease in aquaculture species- Unique access to some bio-secure markets (particularly Australia & Japan)- Parts of domestic industry protected from imports by biosecurity measures- Government support of industry R&D

- Most industry wild capture growth metrics negative (Quota system)- Wild catch volume has fallen since 1998 leading to reduced throughput- Relatively small producer on a global scale- Supply fluctuates year-to-year with availability of wild capture fish- Mussels and oysters have low value per hectare; salmon development limited by

regulatory challenges - Most EEZ space low productivity deep water- Industry is bulk supply driven, rather than specialised/consumer focused- Firms primarily small/sub-scale with limited access to capital- Competing users of coastal space for aquaculture (e.g. holiday houses)- Highly regulated- No competitive advantage around aquaculture feed production due to low scale- Lack of market integration, not capturing in-market value- Limited in-market knowledge

OPPORTUNITIES ISSUES/THREATS/RISKS

- Consumer perceptions of health benefits of seafood- Large amounts of fish body currently going to meal and waste- Use of by-products for nutraceuticals /cosmetics sector- Growing interest by some more wealthy consumers in Western markets for eco-

labelling and environmental certification (driven by retailers)- Growing middle class in China and SE Asia- Gradual removal of global fishing subsidies- Ongoing removal of trade barriers and negotiation of new free trade agreements- Streamline regulations- New/improved supply chain technology

- New Zealand’s wild capture continues to decline- Other countries “catching up” on sustainability (e.g. Argentina)- Low cost competitors in low wage/low regulation/higher productivity warm

waters- NIMBY (not in my back yard) attitudes limiting industry activity- Single issue special interest groups driving domestic regulatory agenda- Rising costs of airfreight reducing feasibility of fresh exports

9

SUPPLY CHAIN New Zealand has a robust seafood supply chain that produces seafood products from wild capture and aquaculture

1. There may be one or more layers of wholesaling, depending on product or market; some wholesale functions maybe captive inside retailers or foodservice operators; 2. Includes product for housebrands, canners, fish meal manufacturers; Source: Coriolis analysis

SIMPLIFIED MODEL OF NEW ZEALAND SEAFOOD SUPPLY CHAINModel; 2017

10

Aquaculture

New Zealand waters

Seafood processing (wild+aquaculture)

Seafood wholesale

SeafreightAirfreight

Supermarkets

Fishmongers

Foodservice

Seafood wholesale1

(in-market)

Supermarkets/Fishmongers

Industrial2

Foodservice

Internationalmarkets

Domesticmarket

Non-NZ waters

Wild capture

Distributorwholesaler

SecondaryProcessing(in-market)

Global Market Overview

+ Global situation

+ Consumption

+ Production

+ Import demand

+ Key markets

+ Market growth

01

Fundamental demographic and production shifts have led to the global seafood market experiencing ongoing changes in both supply and demand

CONSUMPTION

- Global seafood consumption is concentrated in E/SE Asia (particularly China), Europe and the Americas

- Global per capita seafood consumption (all forms) is showing moderate growth (1.4% per year)

PRODUCTION

- Global production is 200m tons of seafood- Wild capture stalled around 1990, while aquaculture continues to

grow - As a result of the stall in wild capture, particularly of marine fish, the

global production mix is shifting dramatically to aquaculture production of freshwater fish, aquatic plants and molluscs

- Global seafood production (capture and aquaculture) is concentrated in E/SE Asia; New Zealand is a smaller, second tier producer overall

GLOBAL TRADE

- Global cross-border seafood trade volumes are growing (10y CAGR4%) with moderate price gains across the cycle leading to solid export value growth (10y CAGR 6%)

DEMAND: PRODUCT CATEGORIES

- Total global cross-border seafood trade is spread across a wide range of products

- White fish (US$38b), processed seafood ($23.9b), salmon ($15.1b) and prawns ($14.7b) stand out for size

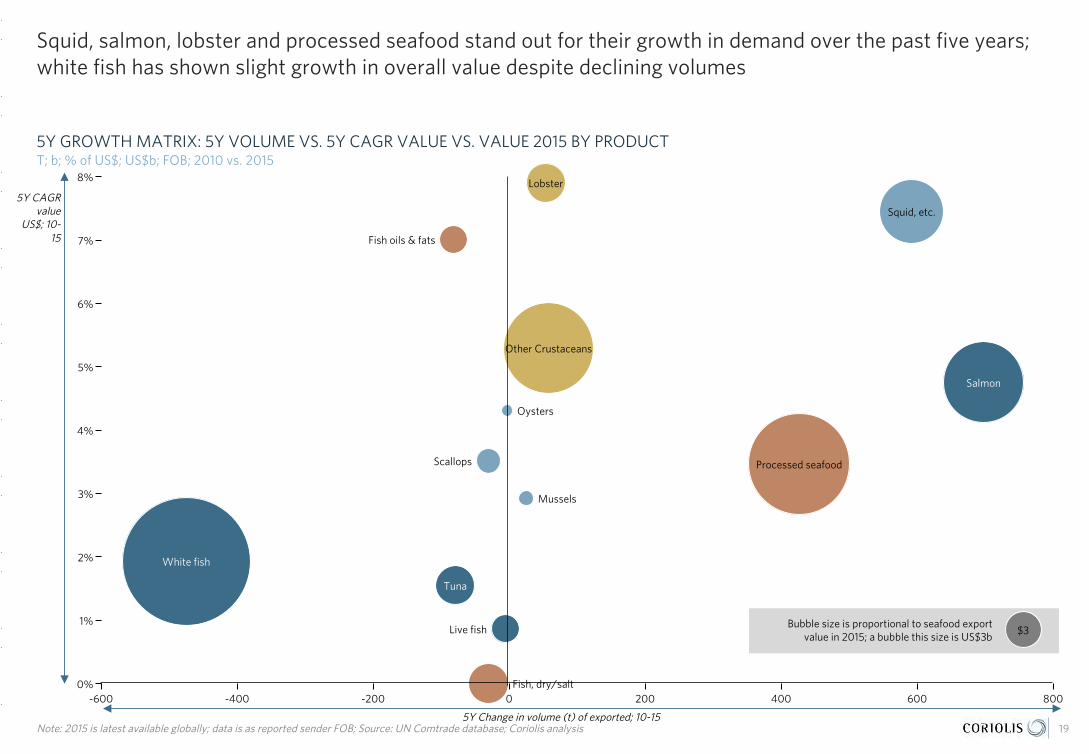

- Squid, salmon, lobster and processed seafood stand out for their growth in demand over the past five years; white fish has shown slight growth in overall value despite declining volumes

DEMAND: IMPORT MARKETS

- Total global cross-border demand for seafood was US$122b in 2015; the key markets are Europe ($48.2b), the US ($17.8b), Japan ($11.7b) and China/HK (~$10b)

- Vietnam, Thailand, South Korea, China and a wide range of other smaller markets stand out for import market growth; Japan and Russia shrank over the period

- Markets vary in average seafood import price, with Hong Kong, the USA, Canada and Japan, followed by the “Big 4” Europeans, standing out as high value markets

SUPPLY: EXPORTERS

- China is the largest seafood exporter overall; New Zealand is a second tier exporter, similar in size to Australia and Argentina

- New Zealand is achieving moderate export price gains but no increase in volume

- Exporters vary in their average seafood export price, driven largely by product mix; New Zealand achieves a similar return to the US and Norway

12

Global seafood consumption is concentrated in E/SE Asia (particularly China), Europe and the Americas; global per capita seafood consumption (all forms) is showing moderate growth (1.4%)

0

5

10

15

20

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

200

1

200

3

200

5

200

7

200

9

2011

2013

13* Final supply after processing & trade; * CAGR = Compound Annual Growth Rate; Note: 2013 is latest UN consumption data available as of April 2017; Source: UN FAOStat database; Coriolis analysis

AVAILABLE SEAFOOD SUPPLY BY REGION*Kilograms; millions; food supply quantity; 2013

50Y GLOBAL SEAFOOD CONSUMPTION PER CAPITAKilograms/person; food supply quantity; 1963-2013

Total = 132,829

Europe

Am

ericas

Australasia

NA

/ME/C

A

E/SE AsiaS Asia

SS Africa

Philippines3,108

Spain1,989

16,739816

China47,754

13,729

UK1,316

5,113

Indonesia7,039

France2,152

Other E/SE Asia5,798

Other A

mericas

1,924

78,3707,787

Other S A

sia956

10,274

Italy1,529 India

6,310

NA

/ME/C

A5,113

Vietnam2,995

New

Zealand

112A

ustralia60

9

Brazil2,178

Bangladesh3,008

Turkey455

Canada792

Mexico1,280

Japan6,179

Russia3,275

Other Europe6,023

Peru672

SS Africa

7,787

Myanmar2,897

USA6,883

S. Korea2,600

Pac. Is.95

50yCAGR1.4%

10

Global production is 200m tons of seafood; wild capture stalled around 1990, while aquaculture continues to grow

14* Diadromous fishes (migrate between fresh and salt water (e.g. salmon, eels) Note: 2015 is latest data available for all countries globally in UN FISHStat as of April 2017; Source: UN database; Coriolis

GLOBAL SEAFOOD PRODUCTION BY TYPE & METHODTonnes; m; landed; greenweight; 2015

40 YEAR GLOBAL SEAFOOD PRODUCTION BY METHODTonnes; million; 1975-2015

40yCAGR

3%

Total = 200

Aquatic plants

AquacultureCapture

Other misc.

Freshwater fishes

Crustaceans

Molluscs

Marine fishes

Diadromous fishes*

94

1

44

3

66

10

106

7

7

2

5

1

7

1

29

16

19921991

40y CAGR

1981

1975

19951996

1980

19931994

1990

1985

1982

1986

19841983

19791978

1989

40y ABS

1976

1988

Capture

1987

1977

1997

2012

200

2

200

6

200

9

200

1

2010

200

420

05

200

3

2011

2013

Aquaculture

200

7

2015

1998

200

8

200

01999

2014

78

159

80

163

76

72

189193

200

68

71

74

167176

181

74

81

108

136

112

103

136

103

125

129129

132

121

123

9198

152

156

88

153

140

106

140

100

149

105

31

101 8%

1%

As a result of the stall in wild capture (particularly of marine fish), the global production mix is shifting dramatically to aquaculture production of freshwater fish, aquatic plants and molluscs

15Source: UN FAOStat database; Coriolis analysis

40 YEAR GLOBAL SEAFOOD PRODUCTION BY TYPE & METHODTonnes; million; 1975-2015

GLOBAL SEAFOOD PRODUCTION SHARE BY TYPE & METHOD% of tonnes; 1975-2015

Other aquaculture

2015

Crustaceans

Molluscs

Freshwater fishes

Molluscs

40y ABS

1985

Aquatic plants

Other capture

Marine fishes

1995 20051975

Freshwater fishes

3%

3%

2%

3%

3%

5%

2%

100%

-2%

-0%

-42%

100%100%100%

-1%

+20%

100%

2%

+6%

-1%

+7%

+12%

70%

58%

2%

75%

8%

8%

6%

46%

33%

1%

5%

9%

15%

1%

6%

8%

3%

4%

5%

4%

4%

5%

22%

16%

10%

4%

4%

4%

5%

3%

7%

5%

5%

5%

6%

4%

2%

2005

Freshwater fishes

Other aquaculture

Crustaceans

40y ABS

Molluscs

1975

Molluscs

Other capture

40y CAGR

1995

Aquatic plants

2015

Marine fishes

Freshwater fishes

1985

+42

4

3

3

200

4

9%

2%

91

6%

8%

1%

1%

68

2%

3%

9%

152

+6

+16

+15

+28125

+15

+1

+4

+4

14

29

7

2

3

916

3

0

1

24

44

13

2

4

12

16

8

1

2

51

7

2

7

5

7

7

2

6

4

5

66

4

7064

72

10

3

8

5

6

Aquaculture

Capture

Global seafood production (capture and aquaculture) is concentrated in E/SE Asia; New Zealand is a smaller, second tier producer overall

16Note: 2015 is latest data available for all countries globally in UN FISHStat as of April 2017; Source: UN database; Coriolis analysis

GLOBAL SEAFOOD PRODUCTION BY KEY COUNTRIES & REGIONTonnes; million; 2015

GLOBAL SEAFOOD PRODUCTION BY KEY REGIONTonnes; million; 1975-2015

Total = 200

Europe

Am

ericas

Australasia

NA

/ME/C

A

E/SE Asia

S Asia

SS Africa

21.3

Chile3.2

France0.7

18.0

Other E/SE Asia6.5

Other Europe4.6

Bangladesh3.7

1.6

China79.4

Japan4.7

15.0

Pac. Is.0

.8

129.7

USA5.5

6.3

Peru4.9

7.7

India10.1

Other S A

sia1.3

Denmark0.9

Australia

0.2

Mexico1.7

Turkey0.7

New

Zealand

0.5

Philippines4.5

Russia3.8

Brazil1.3

SS Africa

7.7

UK0.9

Iceland1.3

Other A

mericas

3.7

Viet Nam6.2

Myanmar3.0

Norway3.8

S Korea3.3

Canada1.1

NA

/ME/C

A6.3

Indonesia22.2

Spain1.3

1995

Other E/SE Asia

40y ABS

S. Asia

North America

201520051975

SS Africa

1985

Australasia

Europe

China

Indonesia

NA/ME/CA

C/S America

40y CAGR

5

52

9

33

200

79

2%

68

-1%

91

3%1%

7%

1%

7%

2%

3%

4%

+8

-5

+4

+1

152

+3

+10

+21

+74

125

+5

+12

15

2321

14

22

254

3

18

2017

2 210 14

77

77 7

5

2225

24

15

18

28

7

22

4

1

2

2

4

2

68

5

7 10

46

3

Global cross-border seafood trade volumes are growing (10y CAGR 3%) with moderate price gains across the cycle leading to solid export value growth (10y CAGR 6%)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

17Note: data is as reported sender FOB; Source: UN FAO database; Coriolis classification and analysis

GLOBAL EXPORT VOLUMEKG; b; 2005-2015

GLOBAL AVERAGE EXPORT PRICEUS$/kg; actual; 2005-2015

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

GLOBAL EXPORT VALUEUS$; b; 2005-2015

10yCAGR

3%

10yCAGR

3%

$0

$20

$40

$60

$80

$100

$120

$140

$160

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

10yCAGR

6%

X =

Global cross-border seafood trade is spread across a wide range of products, though white fish (US$38b), processed seafood ($23.9b), salmon ($15.1b) and prawns ($14.7b) stand out for size

Note: “Squid, etc.” uses trade codes under HS03047-03079; Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

GLOBAL SEAFOOD EXPORT VALUE BY PRODUCT CLASS/TYPEUS$; b; FOB; 2015

18

Total = $121.8

MolluscsLive fish Fish ProcessedCrustaceans

$29.4$1.8 $11.7$56.6 $22.4

White fish$38.0

Live fish$1.8

Salmon$15.1

Tuna$3.5

Oysters$0.3

Mussels$0.5

Squid, etc.$9.4

Fish oils & fats$1.7

Fish, dry/salt$3.7

Prawns$14.7

Processed seafood$23.9

Scallops$1.4

Other Crustaceans$4.1

Lobster$3.6

Bubble size is proportional to seafood export value in 2015; a bubble this size is US$3b

Squid, salmon, lobster and processed seafood stand out for their growth in demand over the past five years; white fish has shown slight growth in overall value despite declining volumes

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY PRODUCT T; b; % of US$; US$b; FOB; 2010 vs. 2015

19

0%8000 200 400-200 600-600 -400

2%

5%

3%

4%

1%

8%

7%

6%

$3

Squid, etc.

Oysters

Scallops

Salmon

White fish

Live fish

Tuna

Fish oils & fats

Fish, dry/salt

Processed seafood

Mussels

Other Crustaceans

Lobster

5Y Change in volume (t) of exported; 10-15

5Y CAGRvalue

US$; 10-15

Total global cross-border demand for seafood was US$122b in 2015; the key markets are Europe ($48.2b), the US ($17.8b), Japan ($11.7b) and China/HK (~$10b)

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

GLOBAL SEAFOOD IMPORT VALUE BY RECEIVING COUNTRY/REGIONUS$; b; FOB; 2015

20

Total = $121.8

SS Africa

NA

/ME/C

A

Europe S Asia E/SE AsiaAmericasAustraliasia

France$6.1

Spain$5.8

$24.3$1.8

Italy$5.5

Other Americas$1.3 Turkey

$0.2

Other E Asia$2.8

$48.2 $40.5

SS Africa

$2.7

Venezuela$0.0

Saudi$0.5

Chile$0.3

$0.7$3.6

Colombia$0.3

Other Europe$19.7

United Kingdom$4.1

$2.7

Germany$5.2

Singapore$1.1

Brazil$1.1

Other S A

sia$0

.4

Other SE Asia$1.2

Canada$2.6

Malaysia$1.0

Egypt$0.6

Vietnam$4.4

Thailand$2.6

Mexico$0.8

UAE$0.6

Hong Kong SAR$4.3

USA$17.8

Russia$1.4

China$6.6

Other Pacific

$0.3

Sri Lanka$0

.3

Australia$1.4

Other N

A/M

E/CA

$1.9

South Korea$4.8

Japan$11.7

New

Zealand

$0.2

Bubble size is proportional to seafood import value in 2015; a bubble this size is US$3b

Vietnam, Thailand, South Korea, China and a wide range of other smaller markets stand out for import market growth; Japan and Russia shrank over the period

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY RECEIVING COUNTRY/REGIONT; b; % of US$; US$b; FOB; 2010 vs. 2015

21

400 500-200 2001000-100 300

5%

0%

-5%

20%

15%

10%

600

S Korea

Other SE Asia

China

Other E Asia

Spain

Japan

$3

Hong Kong SAR

France

Colombia

Other Americas

Italy

UK

Other EuropeGermany

USA

Australia

New Zealand

Canada

Mexico

Chile

Brazil

Other S Asia

Other NA/ME/CA

Sri LankaVietnam

Malaysia

Singapore

Thailand

Turkey

SS Africa

EgyptSaudi

UAE

Russia

5Y Change in volume (t) of imported; 10-15

5Y CAGR value US$;

10-15

Markets vary in average seafood import price, with Hong Kong, the USA, Canada and Japan, followed by the “Big 4” Europeans, standing out as high value markets

Note: therefore area under chart is proportional to import value (volume x $/kg); Source: UN Comtrade data; Coriolis analysis and classifications

TOTAL GLOBAL SEAFOOD IMPORT VOLUME VS. AVERAGE IMPORT PRICE BY KEY MARKETKG; millions; US$/kg; actual; 2015

22

Sri Lanka

UA

E

Hong K

ong SAR

Japan

Canada

Australia

Venezuela

Vietnam

Spain

UK

South Korea

EgyptT

urkey

Italy

Germ

any

Russia

Other Europe

Other E A

sia

Other Pacific

SS Africa

Thailand

Other A

mericas

Chile

Saudi

Other S A

sia

Malaysia

Mexico

Brazil

Other N

A/M

E/CA

France

China

Other SE A

siaC

olombia

Singapore

USA

$2.99 $2.50

$4.86

$3.64

$5.45

$2.69

$5.33

$2.58

$1.79$2.0

8

$2.36

$1.63

$6.00

$5.38

$2.49$2.52

$3.03

$1.65

$3.26

$4.31

$5.33

$3.97

$7.28

$5.54

$6.25

$5.67

$9.99

$3.21

$3.75

$2.08

$3.37

$4.10

$4.15

$2.62

$3.78

Proportional to import volume in 2015

Average import

value per kilogramUS$/kg

2015

Weighted average $4.13

China is the largest seafood exporter overall; New Zealand is a second tier exporter, similar in size to Australia and Argentina

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

GLOBAL SEAFOOD EXPORT VALUE BY SENDING COUNTRY/REGIONUS$; b; FOB; 2015

23

Total = $121,840

AmericasAustralasia S Asia

E/SE Asia

NA

/ME/C

A

Europe

SS Africa

Other E/SE Asia$4,891

$42,364$23,893

$2,346

Netherlands$3,377

$2,660

Hong Kong SAR$760

$5,336 $42,917$2,323

Mexico$986

Russia$2,824

Belarus$258

Other Europe$15,590

Other Americas$1,465

Denmark$3,221

Other Pacific

$152

China$19,758

Argentina$1,445

USA$5,751

Australia

$1,066

New

Zealand

$1,105

NA

/ME/C

A$2,660

Turkey$704

Vietnam$6,573

Ecuador$3,533

Norway$9,078

Spain$3,645

Chile$4,456

Japan$1,902

SS Africa

$2,346

Canada$5,063

Other S Asia$519

India$4,818

Sweden$3,668

Indonesia$3,609

Peru$1,193

Thailand$5,424

New Zealand’s seafood trade share is drifting lower, similar to other Southern Hemisphere cool water peers other than Chile (which has a strong aquaculture sector)

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

GLOBAL EXPORT MARKET SHARE: KEY SOUTHERN HEMISPHERE COOL WATER SEAFOOD EXPORTERS% of value; US$; 2005-2015

24

2013

Australia

20152014

New Zealand

2005 2006 2007

10Y Change

South Africa

Argentina

2008 2011 20122010

Chile

2009

0.5%0.6%

0.5%

-0.5%

-0.4%

0.3%-0.3%

0.0%

0.0%

0.3%

0.4%0.5%0.5%

0.3%0.3%0.3%

3.8%

3.5%

3.8%

3.7%

4.0%

2.8%

3.9%

3.7%

3.5%

3.3%

3.2%

1.0% 1.0%1.1%

1.3%

1.1%1.0%

0.9% 0.9%0.9%1.0%

1.0%1.0%1.0%

1.1%

1.4%

1.2%

0.9%

0.8% 0.9%0.8%

0.9%0.8%

1.4%

1.3%1.3%

1.2%

1.6%

1.3%

1.1%1.2%1.2%

1.2%

1.1%

Bubble size is proportional to seafood import value in 2015; a bubble this size is US$3b

New Zealand is achieving moderate export price gains but no increase in volume

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY EXPORTING COUNTRY/REGIONT; b; % of US$; US$b; FOB; 2010 vs. 2015

25

600-200

15%

4002000

0%

18%

750-10%

-450

-5%

5%

-400

10%

Denmark Netherlands

Russia

Turkey

Other Europe

Belarus

Ecuador

Chile

New Zealand

$3

USA

Other Americas

Norway

Peru

Mexico

NA/ME/CA

Canada

SpainArgentina

Other S Asia

China

Thailand

Other E/SE Asia

Hong Kong SAR

Japan

India

Vietnam

SwedenIndonesia

SS Africa

5Y Change in volume (t) of exported; 10-15

5Y CAGRvalue US$;

10-15

Exporters vary in their average seafood export price, driven largely by product mix; New Zealand achieves a similar return to the US and Norway

Note: therefore area under chart is proportional to import value (volume x $/kg); Source: UN Comtrade data; Coriolis analysis and classifications

SEAFOOD EXPORT VOLUME VS. AVERAGE EXPORT PRICE ACHIEVED BY EXPORTING COUNTRY/REGIONKG; millions; US$/kg; actual; 2015

26

China

Mexico

Australia

Spain

Hong K

ong SAR

Sweden

Other A

mericas

Canada

Belarus

Chile

Indonesia

Turkey

Norway

Japan

Vietnam

Other S A

sia

Thailand

Other Europe

NA

/ME/C

A

Denm

ark

India Russia

Peru

Other E/SE A

sia

Other Pacific

Argentina

SS Africa

Ecuador

New

Zealand

Netherlands

USA

$2.83

$3.48

$4.30

$4.0

5

$5.01

$5.09

$5.51

$5.21

$3.26$2.94

$3.27

$4.13

$3.66 $3.59

$4.61

$4.4

5

$4.60

$6.99

$7.55$16.15

$3.89

$4.39

$7.54

$2.40

$2.04

$3.42

$3.87

$4.98

$4.13

$2.78

$3.54

Proportional to export volume in 2015

Average export

value per kilogramUS$/kg

2015

Weighted average $4.13

Rock Lobster

New Zealand Seafood Production

+ Number of firms

+ Employment

+ Yield/productivity

+ Production

+ Regional activity

+ Growth upside

02

New Zealand produces sustainable quantities of seafood through wild capture and aquaculture

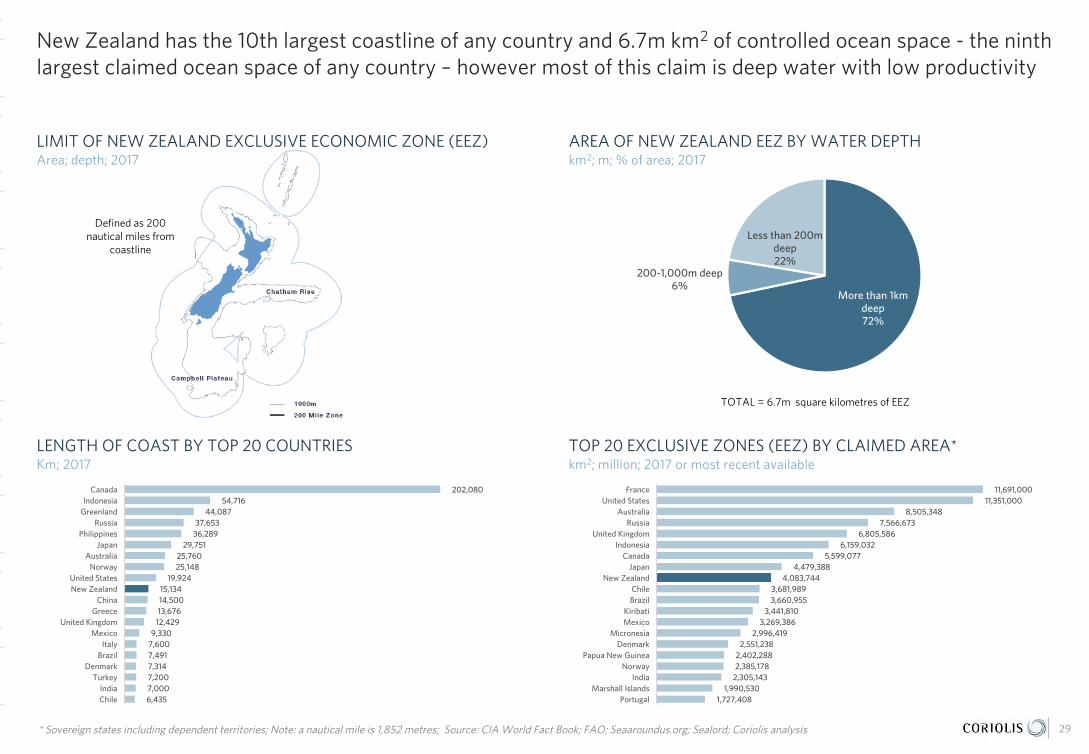

- New Zealand has the 10th largest coastline of any country and 6.7m km2 of controlled ocean space - the ninth largest claimed ocean space of any country – however most of this claim is deep water with low productivity

- New Zealand produces significant amounts of seafood under both wild capture and aquaculture

- Wild capture volumes have benefited from the increase in the allowed Hoki (Blue Grenadier) catch, while aquaculture production has achieved long-term growth

28

Defined as 200 nautical miles from

coastline

New Zealand has the 10th largest coastline of any country and 6.7m km2 of controlled ocean space - the ninth largest claimed ocean space of any country – however most of this claim is deep water with low productivity

29

LIMIT OF NEW ZEALAND EXCLUSIVE ECONOMIC ZONE (EEZ)Area; depth; 2017

AREA OF NEW ZEALAND EEZ BY WATER DEPTHkm2; m; % of area; 2017

202,080 54,716

44,087 37,653

36,289 29,751

25,760 25,148

19,924 15,134 14,500 13,676

12,429 9,330

7,600 7,491 7,314 7,200 7,000 6,435

CanadaIndonesia

GreenlandRussia

PhilippinesJapan

AustraliaNorway

United StatesNew Zealand

ChinaGreece

United KingdomMexico

ItalyBrazil

DenmarkTurkey

IndiaChile

LENGTH OF COAST BY TOP 20 COUNTRIESKm; 2017

TOP 20 EXCLUSIVE ZONES (EEZ) BY CLAIMED AREA*km2; million; 2017 or most recent available

* Sovereign states including dependent territories; Note: a nautical mile is 1,852 metres; Source: CIA World Fact Book; FAO; Seaaroundus.org; Sealord; Coriolis analysis

TOTAL = 6.7m square kilometres of EEZ

11,691,000 11,351,000

8,505,348 7,566,673

6,805,586 6,159,032

5,599,077 4,479,388

4,083,744 3,681,989 3,660,955

3,441,810 3,269,386

2,996,419 2,551,238

2,402,288 2,385,178

2,305,143 1,990,530

1,727,408

FranceUnited States

AustraliaRussia

United KingdomIndonesia

CanadaJapan

New ZealandChileBrazil

KiribatiMexico

MicronesiaDenmark

Papua New GuineaNorway

IndiaMarshall Islands

Portugal

More than 1km deep72%

200-1,000m deep6%

Less than 200m deep22%

New Zealand produces significant amounts of seafood under both wild capture and aquaculture

0

100

200

300

400

500

600

700

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

200

0

200

2

200

4

200

6

200

8

2010

2012

2014

30

TOTAL NZ WILD CAPTURE SEAFOOD PRODUCTIONTonnes; 000; 1950-2015

AQUACULTURE PRODUCTION PER KILOMETRE OF COAST Tonnes; actual; 1950-2015

NZ WILD CAPTURE PER PERSONKG/capita; actual; 1950-2015

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

195019521954195619581960196219641966196819701972197419761978198019821984198619881990199219941996199820

00

200

220

04

200

620

08

2010

2012

2014

SHARE OF TOTAL SEAFOOD PRODUCTION BY TYPE% of tonnes; 1950-2015

Note: 2015 data latest available as of April 2017; Source: UN FAO FishStat database; MFish/MAF/MPI; Coriolis analysis

50-76CAGR

3%

97-08CAGR-3.2%

76-97CAGR

11%

UNCLOS 1982EEZ 200nm

08-15CAGR-0.6%

-

20

40

60

80

100

120

140

160

180

200

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

200

0

200

2

200

4

200

6

200

8

2010

2012

2014

Aquaculture

Wild capture

-

1

2

3

4

5

6

7

8

9

10

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

200

0

200

2

200

4

200

6

200

8

2010

2012

2014

Wild capture volumes have benefited from the increase in the allowed Hoki (Blue Grenadier) catch, while aquaculture production has achieved long-term growth

31

TOTAL WILD CAPTURE BY SPECIES GROUPTonnes; 000; 1975-2015

TOTAL AQUACULTURE PRODUCTION BY KEY SPECIES Tonnes; 000; 1975-2015

Note: 2015 data latest available as of April 2017; Source: UN FAO FishStat database; MFish/MAF/MPI; Coriolis analysis

1989

1987

19901991

1988

Pacific salmon

1992

197719781979

1976

AbaloneOyster

1975

198419851986

1983

198019811982

2013

1999

200

520

06

1998

2010

200

0

200

2

2011

200

3

200

1

2012

200

4

1997

1994

2015

1995

1993

Mussel

200

8

2014

1996

200

9

200

7

105

112 111

11091

97

11710

0

19

94

7577

92

11

1712

49

51

5253

2728

29

70

86

105

1

92

2

112

2

108

3

7

87

10

76

33 3

85

200

5

1995

Arrow squid

200

7

2011

200

6

1996

Oreo dories nei

200

0

200

220

01

200

9

Other

1999

200

320

04

1997

2010

200

8

1998

1994

Orange roughy

1987

2015

1976

19811982

1988

1986

Silver warehou

1983

Ling

1984

Hoki

1975

1985

1977

Snoek

1992

19781979

2012

1993

1980

2013

1989

Mackerels nei

Southern blue whiting

2014

Blue mackerel

19911990

6369

7898

19620

820

3

169

117154

167

545

477

495

546

570589

551

453 4

44

44

3 433

44

2

44

04

374

30

352386

470

316

208

241

277

433

648

600

553

649

453

5574

25

New ZealandCategory Performance

+ Segmentation

+ Key products

+ Exports by product

03

New Zealand has a solid position in select seafood products where it has real strengths

33

- New Zealand has a stable wild seafood catch, is a leader in rock lobster and is innovating in mussel and salmon products

- Exports are spread across six categories

- however wild capture (54%), rock lobster (20%), and mussels (14%) are the largest

- Export value is growing across the cycle

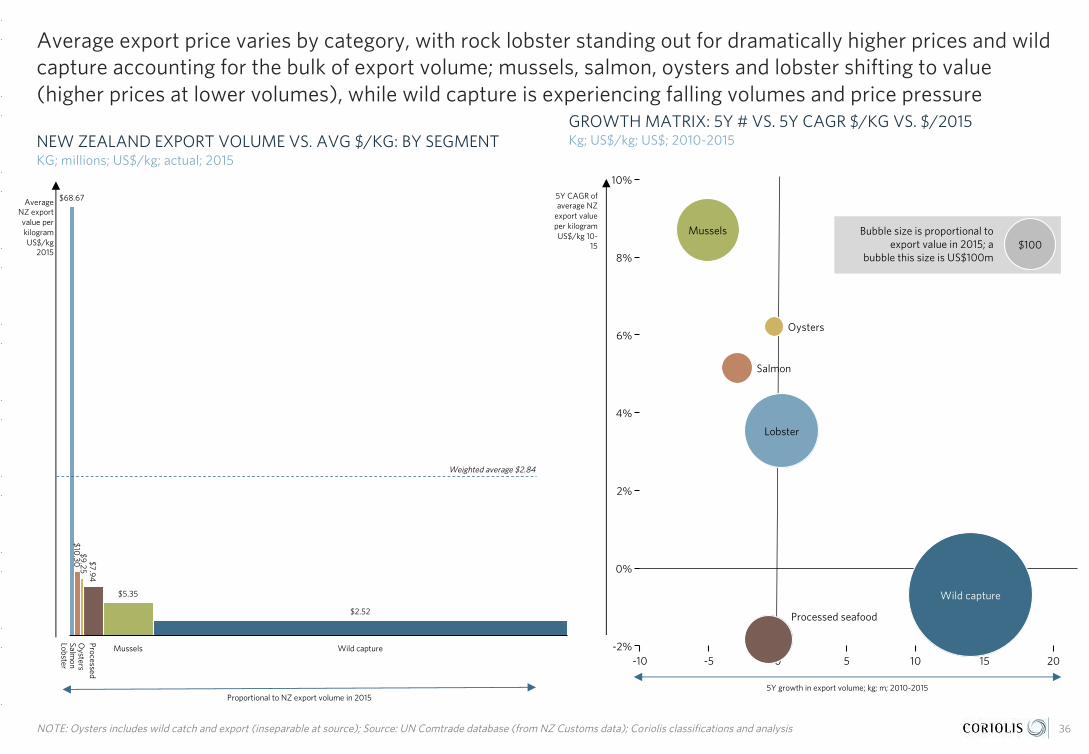

- Average export price varies by category, with rock lobster standing out for dramatically higher prices and wild capture accounting for the bulk of export volume

- Mussels, salmon, oysters and lobster are shifting to value (higher prices at lower volumes), while wild capture is experiencing falling volumes and price pressure

- WILD CAPTURE Thanks to pioneering quota management systems, New Zealand has a long-term, sustainable supply of ~450k tonnes of wild capture seafood available

- ROCK LOBSTER* New Zealand has a long-term, sustainable supply of rock lobster available; export value growing strongly, with almost all volume now going to China/Hong Kong

- MUSSELS New Zealand has a strong position in green shelled mussel aquaculture, producing a third of global green supply; export value growing strongly

- SALMON New Zealand is the global market leader in King/Chinook Salmon aquaculture, a small but premium species; there is potential for further strong growth

OVERVIEW BY CATEGORY

* Rock Lobster: While rock lobster is a “wild capture” seafood in New Zealand, this project considers it separately, due to its significance and growth

New Zealand has a stable wild seafood catch, is a leader in rock lobster and is innovating in mussel and salmon products

Source: photo credit (purchased, courtesy of firms or fair use; low resolution; complete product/brand for illustrative purposes); Coriolis classifications and analysis 34

WILD CAPTURE

- Stable, predictable, secure long term supply of fish

- NZ pioneering of wild catch quota management has prevented collapse of fish stocks (unlike competitors)

StableSupply

MUSSELS

- Modern and consolidated industry

- Proven supply chain, track record in in-store merchandising systems

- Recently implemented breeding program driving productivity gains

Pioneering Farmer & ExporterUnique Species

ROCK LOBSTER

- Well managed fishery

- Stable supplies

- One of two major global suppliers of spiny red rock lobster (rest of world primarily clawed lobster)

- Growing strongly into China and wider Asia

Major GlobalExporter

SALMON

- Highly consolidated and at scale

- Effectively only global supplier of farmed Chinook; others hampered by disease

- Lack of key salmon diseases (e.g. ISA)

- Huge potential for growth (5x/10x)

#1 Global FarmedChinook/King Salmon

KEY HIGH-LEVEL CATEGORIES

Exports are spread across six categories, however wild capture (54%), rock lobster (20%), and mussels (14%) are the largest; exports are growing across the cycle

35NOTE: “processed seafood is seafood relevant global trade codes under HS 1603-1605 (see page 80 for details); oysters includes wild catch and export (inseparable at source); Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NEW ZEALAND SEAFOOD EXPORT VALUE BY SEGMENTUS$; m; 2015

NEW ZEALAND SEAFOOD EXPORT VALUE BY SEGMENTUS$; m; 2005-2015

Processed seafood

Mussels

2009 2010 2011

Oysters

2007 2008 2014 2015

Wild capture

2012

Lobster

201320062005

Salmon

$131

$1,218

$104

$96

$1,242

$115

$206

$1,105

$153

$129

$1,236

$77 $83$95

$949

$853$83

$907

$1,033 $90

$1,187

$873 $875

$79

$163

$174

$181

$89 $128

$116

$205$12$12

$12

$223

$214

$11

$554$505

$583$574 $539 $559

$673$598

$80$82

$733$678 $668

$10

$36

$113$114

$37$44

$30

$126

$167

$150$144

$142

$124

$119

$15

$13

$14

$12

$15$12

$19 $36

$52

$42

$27$26

$30

Wild capture$598 54%

Lobster$214 20%

Mussels$153 14%

Salmon$36 3%

Oysters$14 1%

Processed seafood, $90 ,

8%

Average export price varies by category, with rock lobster standing out for dramatically higher prices and wild capture accounting for the bulk of export volume; mussels, salmon, oysters and lobster shifting to value (higher prices at lower volumes), while wild capture is experiencing falling volumes and price pressure

36NOTE: Oysters includes wild catch and export (inseparable at source); Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NEW ZEALAND EXPORT VOLUME VS. AVG $/KG: BY SEGMENTKG; millions; US$/kg; actual; 2015

GROWTH MATRIX: 5Y # VS. 5Y CAGR $/KG VS. $/2015Kg; US$/kg; US$; 2010-2015

Bubble size is proportional to export value in 2015; a

bubble this size is US$100m

Processed

Lobster

Mussels

Oysters

Wild capture

Salmon

$9.25

$2.52

$7.94

$68.67

$10.30

$5.35

Proportional to NZ export volume in 2015

Average NZ export value per kilogramUS$/kg

2015

Weighted average $2.84

105

6%

4%

10%

8%

2%

2015

0%

-2%-10 -5 0

$100

Lobster

Wild capture

Mussels

Processed seafood

Oysters

Salmon

5Y CAGR of average NZ

export value per kilogramUS$/kg 10-

15

5Y growth in export volume; kg; m; 2010-2015

WILD CAPTURE Thanks to pioneering quota management systems, New Zealand has a long-term, sustainable supply of ~450k tonnes of wild capture seafood available

37Source: US FishStat database; UN Comtrade database; photo credit (CC BY-SA 1.0); Coriolis classifications and analysis

NZ WILD CAPTURE SEAFOOD EXPORTSUS$m; 2005-2015

-

100

200

300

400

500

600

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

200

1

200

4

200

7

2010

2013

Hoki

Other marine

SquidOther

WILD CAPTURE OF SEAFOOD IN NZ WATERST; 000; 1950-2015

Other Crustaceans

2005 2015

10Y CAGR 10Y ABS

White fish

Squid, etc.

Tuna

Scallops

Live fish

-$87

-$1

+$14

+$1

+$93

+$5$598

$2$1

$505

$574

$412

$15

$32

$20

$126

$2 $39

$1

-11%

-11%

3%

6%

$18

6%

2%

ROCK LOBSTER New Zealand has a long-term, sustainable supply of rock lobster available; export value growing strongly, with almost all volume now going to China/Hong Kong

0

2

4

6

8

10

12

195019521954195619581960196219641966196819701972197419761978198019821984198619881990199219941996199820

00

200

220

04

200

620

08

2010

2012

2014

38Source: US FishStat database; UN Comtrade database; Coriolis classifications and analysis

NEW ZEALAND SPINY RED ROCK LOBSTER CATCH VOLUMET; 000; 1950-2015

GLOBAL CHILLED ROCK LOBSTER EXPORT VALUE BY REGIONUS$m; 2005 vs. 2015

NZ CHILLED/FROZEN LOBSTER EXPORT VALUE BY DESTINATIONUS$m; 2005-2015

EXAMPLE PRODUCTS: KIWI LOBSTER2017

$61

$155

$213

$19

$8

$1

2005 2010 2015

$214

Other

CAGR10%

$163

China/HK$80

OtherEurope

15%

Australia

2005

10Y ABS10Y CAGR

South Africa

New Zealand

2015

Other

+$136

+$338

+$16

$862

$351

+$21$26

$183

$42$76

$521

$212 11%

5%

3%$66 $87

11%

CAGR9%

MUSSELS New Zealand has a strong position in green shelled mussel aquaculture, producing a third of global green supply; export value growing strongly

0

20

40

60

80

100

195019521954195619581960196219641966196819701972197419761978198019821984198619881990199219941996199820

00

200

220

04

200

620

08

2010

2012

2014

39

NEW ZEALAND MUSSEL EXPORT VALUEUS$m; 2005-2015

NZ MUSSEL AQUACULTURE PRODUCTIONTonnes; 1950-2015

NZ SHARE OF GLOBAL MUSSEL EXPORT VALUE BY TYPE% of US$; share of tonnage; 2015

EXAMPLE PRODUCTS: SEALORD2017

Source: US FishStat database; UN Comtrade database; photo credit (courtesy Sealord); Coriolis classifications and analysis

France6%

OtherEurope

15%

2015

10Y CAGR 10Y ABS

2005

Mussels, prepared

Mussels (not-live)

Mussels, live +$1

-$14

$156

$182

$151

$43

$112

$1

$1

-4%

+$40

5%

$29

3%

CAGR2%

Mussels, liveMussels, preparedMussels (not-live)

48.1%

0.7%0.9%

NZ Share of world trade

% of US$; 2015

Proportional to cross-border volume in tonnes in 2015

SALMON New Zealand is the global market leader in King/Chinook Salmon aquaculture, a premium species produced by aquaculture in New Zealand

40Source: UN FishStat database; UN Comtrade database; photo credit (courtesy the great people at Mt Cook Salmon); Coriolis classifications and analysis

NEW ZEALAND SALMON EXPORT VALUEUS$m; 2005 vs. 2015

AGGREGATE GLOBAL SALMON EXPORT GROWTHUS$b; 2005 vs. 2015

AVERAGE EXPORT PRICE: WHOLE CHILLED SALMON: NZ & PEERSUS$/kg; FOB; 2016

EXAMPLE PRODUCTS: MT COOK ALPINE SALMON2017

$3.2

$0.6 $0.7

$1.8

$9.5

$1.6 $1.1

$2.9

Salmon, chilled whole Salmon, smoked Salmon, frozen whole Other salmon

CAGR12%

2005

CAGR11%

2015

CAGR5%

CAGR5%

Salmon, chilled whole

2005

10Y ABS10Y CAGR

Salmon, smoked

Salmon, frozen whole

2015

Other

+$8

+$15

+$2

$44

$19

+$0$3

$11

$4$5

$26

$13 10%

5%11%$0 $1

9%

CAGR9%

$11.10

$8.26

$7.61

$7.35

$7.17

$6.66

$5.84

New Zealand

United Kingdom

Australia

Canada

Norway

Chile

USA

New ZealandGrowth & Innovation

+ Horizons for growth

+ Emerging export stars

+ New viable options

+ Mega-trends driving change

+ Innovation & new products

04

New Zealand firms continue to develop a range of innovative new seafood products

42

THREE HORIZONS OF GROWTH

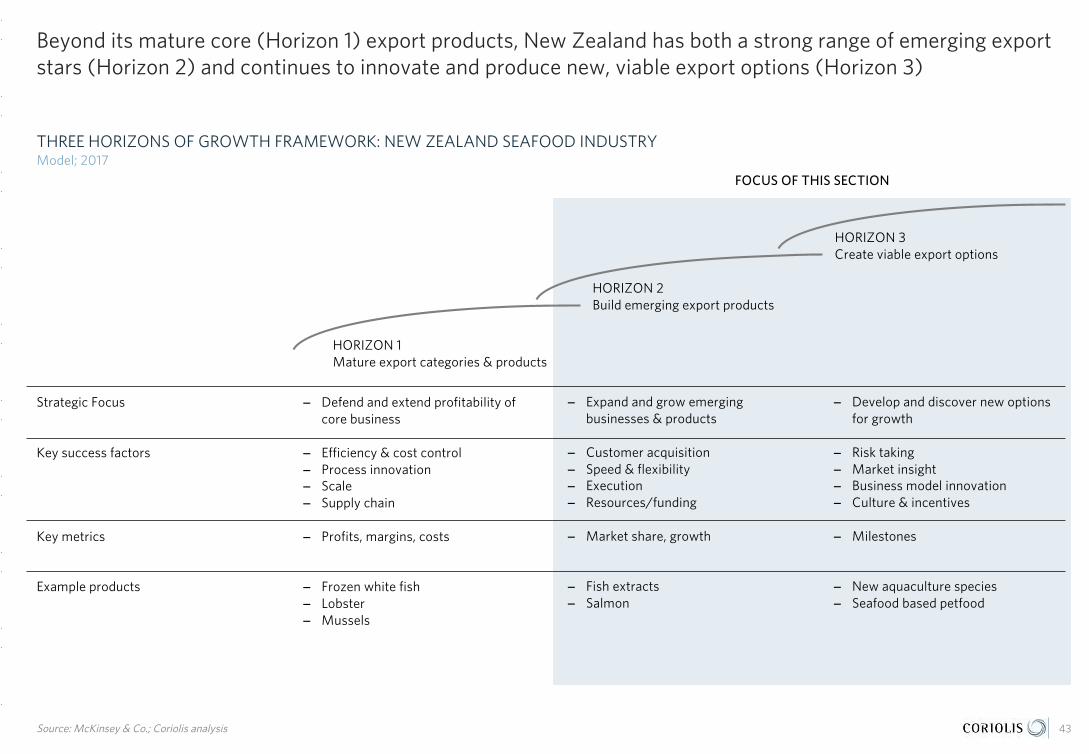

- Beyond its mature core export products (Horizon 1), New Zealand has both a strong range of emerging export stars (Horizon 2) and continues to innovate and produce new, viable export options (Horizon 3)

HORIZON 2: EMERGING EXPORT STARS

- In Horizon 2, New Zealand is building a range of emerging export products

- Two seafood products emerge as “growth stars” – fish extracts and whole salmon – from an evaluation of ten years of product-level trade growth

- Fish extract exports are growing and the product plays to New Zealand strengths in nutraceuticals

- New Zealand whole chilled salmon exports are growing, with the US market as the key success, having grown from US$2m to US$15m in a decade

HORIZON 3: NEW, VIABLE OPTIONS

- In Horizon 3, New Zealand is creating and nurturing a wide range of viable options for future export success

- Four broad global consumer mega-trends are driving growth and new product development in the food & beverage industry

- New Zealand seafood products succeeding on-shelf in export markets are aligned with these trends

- These trends drive new product development, through (1) packaging, (2) product, (3) category and (4) channel innovation; success, however, often comes down to implementation and execution

- New Zealand seafood firms are delivering on…

- Packaging-driven innovation

- Product-driven innovation

- Category and channel innovation

Beyond its mature core (Horizon 1) export products, New Zealand has both a strong range of emerging export stars (Horizon 2) and continues to innovate and produce new, viable export options (Horizon 3)

Source: McKinsey & Co.; Coriolis analysis

THREE HORIZONS OF GROWTH FRAMEWORK: NEW ZEALAND SEAFOOD INDUSTRYModel; 2017

43

HORIZON 1Mature export categories & products

HORIZON 2Build emerging export products

HORIZON 3Create viable export options

Strategic Focus

Key success factors

Key metrics

Example products

FOCUS OF THIS SECTION

− Defend and extend profitability of core business

− Efficiency & cost control− Process innovation− Scale− Supply chain

− Profits, margins, costs

− Frozen white fish− Lobster− Mussels

− Expand and grow emerging businesses & products

− Customer acquisition− Speed & flexibility− Execution− Resources/funding

− Market share, growth

− Fish extracts− Salmon

− Develop and discover new options for growth

− Risk taking− Market insight− Business model innovation− Culture & incentives

− Milestones

− New aquaculture species − Seafood based petfood

In Horizon 2, New Zealand is building a range of emerging export products

Source: McKinsey & Co.; Coriolis analysis

THREE HORIZONS OF GROWTH FRAMEWORK: NEW ZEALAND SEAFOOD INDUSTRYModel; 2017

44

Strategic Focus

Key success factors

Key metrics

Example products

HORIZON 1Mature export categories & products

HORIZON 2Build emerging export products

HORIZON 3Create viable export options

− Defend and extend profitability of core business

− Efficiency & cost control− Process innovation− Scale− Supply chain

− Profits, margins, costs

− Frozen white fish− Lobster− Mussels

− Expand and grow emerging businesses & products

− Customer acquisition− Speed & flexibility− Execution− Resources/funding

− Market share, growth

− Fish extracts− Salmon

− Develop and discover new options for growth

− Risk taking− Market insight− Business model innovation− Culture & incentives

− Milestones

− New aquaculture species − Seafood based petfood

Bubble size is proportional to export

value in 2015; a bubble this size is

US$100m

Two seafood products emerge as “growth stars” – fish extracts and whole salmon – from an evaluation of ten years of product-level trade growth

Note: Data on this page is product level trade codes, not segment level aggregates as presented earlier; Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NZ SEAFOOD EXPORT GROWTH STAR MATRIX: 10Y VALUE GROWTH VS. 10Y CAGR $ VS. VALUE IN 2015US$; CAGR on US$; 2005-2015

45

140

15%

-15%

-25 0 50 100

20%

10%

-10%

5%

-5%

0%

Frozen fish meat

Salmon, chilled whole

Prawns, frozen

Skipjack tuna, frozen whole

Oysters

Chilled fish, nes.

Squid (non-chilled)

Mussels (not-live)

Other prep fish

Mussels, prepared

Frozen fish livers and roes

Frozen fish fillets

Mackerel, frozen

$100

Longfin tuna, frozen whole

Frozen fish, nes

Salmon, frozen whole

Rock Lobster, freshChilled fish fillets

Fish extracts

Hake, frozen

10y ABS growth in export value; US$; b; 2005-2015

10y CAGRgrowth in

export value;

US$; 2005-

2015

Fish extract exports are growing and the product plays to New Zealand strengths in nutraceuticals

46Source: UN Comtrade database (from NZ Customs data); photo credit (courtesy Seadragon); Coriolis classifications and analysis

FISH EXTRACT EXPORT VALUE BY MARKETUS$; m; 2005-2015

EXAMPLE: RECENT INVESTMENT IN NEW ZEALAND2016

201520142008 200920072005 2006 2012 20132011

South Korea

2010

Europe

Other

North America

Other E/SE Asia

$7

$1 $6$7

$19

$5$1

$2

$5

$3

$5$1 $6

$2 $7

$33

$0

$43

$0

$0

$0

$32

$0

$4

$26

$11

$21

$7

$5

$34

$20

$14

$1

$0

$1

$1

$2

$1

$2

$1

$2$1

$1$1 $2

$1

$1

$1

$2

$9

$3

$2

$1

$3

$4

$6

$3$1

$1

$1

$2

$1$3

$4

$1

$5

CAGR16%

- Invested $10.8m in new fish oil processing facility, Nelson, New Zealand

- Fully commissioned August 2016- Capacity to refine up to 5,000t of Omega-3 fish oil- Oil sourced from sustainable and traceable Marine Stewardship

Council certified species

New Zealand whole chilled salmon exports are growing, with the US market as the key success, having grown from US$2m to US$15m in a decade

47Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

CHILLED WHOLE SALMON EXPORT VALUE BY MARKETUS$; m; 2005-2015

EXAMPLE: RECENT NZ FIRM ACTIVITIES IN THE US MARKETSelect activities; 2016

201520142008 200920072005 2006 2012 20132011

Japan

2010

North America

Australia

Other

Other E/SE Asia

$11.0$2.1

$14.7

$17.2

$0.5

$16.9

$4.3

$7.4

$5.3

$6.6

$5.1

$4.5

$3.3

$6.0

$3.6$21.3

$0.4

$26.1

$0.4$0.4

$0.5

$26.9

$0.4

$0.6

$0.5

$27.7

$0.4

$17.5

$0.4

$19.7

$0.4

$23.6$2.9

$12.0$2.6

$7.2

$2.2

$5.1

$1.8

$4.3

$6.1

$4.8

$0.5

$0.5

$0.7

$8.0

$0.7

$5.8

$0.5

$10.1

$4.7

$9.0

$5.2

$6.7$6.4

$6.3

$5.9

$5.8

$3.1

$4.1

$2.5

$5.7

$5.2

$15.2

$3.2$4

.8

CAGR9%

- “Seafood Watch” the globally respected consumer seafood guide on sustainable seafood gives New Zealand Chinook salmon a “Best Choice” 2016

- Ora launched in USA in 2012

- Ora raised specifically for the restaurant trade, targeting high value and highly discerning customers

In Horizon 3, New Zealand is creating and nurturing a wide range of viable options for future export success

Source: McKinsey & Co.; Coriolis analysis

THREE HORIZONS OF GROWTH FRAMEWORK: NEW ZEALAND SEAFOOD INDUSTRYModel; 2017

48

Strategic Focus

Key success factors

Key metrics

Example products

HORIZON 1Mature export categories & products

HORIZON 2Build emerging export products

HORIZON 3Create viable export options

− Defend and extend profitability of core business

− Efficiency & cost control− Process innovation− Scale− Supply chain

− Profits, margins, costs

− Frozen white fish− Lobster− Mussels

− Expand and grow emerging businesses & products

− Customer acquisition− Speed & flexibility− Execution− Resources/funding

− Market share, growth

− Fish extracts− Salmon

− Develop and discover new options for growth

− Risk taking− Market insight− Business model innovation− Culture & incentives

− Milestones

− New aquaculture species − Seafood based petfood

Four broad global consumer mega-trends are driving growth and new product development in the food & beverage industry

Source: Boston Consulting Group; Datamonitor; Coriolis research and analysis; Photo credit: Image(s) used under license from Shutterstock.com 49

HEALTH & WELLNESS AUTHENTIC & RESPONSIBLE EASY & CONVENIENT SENSORY & INDULGENT

− Mid-high income countries experiencing an aging population

− Spread of Western lifestyle and Western diseases of affluence (e.g. obesity)

− Ongoing waves of media hype around fad diets and new "superfoods"

− Food presented and viewed as both the problem and the solution

− Dramatic global shift to city living; 1800=3%, 1900=14%, 2015=50%; developed nations 75%+; 400 cities 1m+

− Loss of attachment to the land and food production

− Ongoing "rights revolution" now spreading to animals

− Ongoing waves of food scares around contamination, additives

− Dramatic increase in female participation on the workforce globally

− Consumers working longer hours to maintain relative income

− Work hours no longer just "9 to 5"; food needs at all times (e.g. night shift)

− Growing income polarisation into “haves and have-nots”

− Strongly emerging trend to premium (and discount) at the expense of the mid-market

− Emerging middle class across developing world driving consumption growth

− Incredible power of food and beverages in many social settings

− May be addressing specific conditions (e.g. weight management; cholesterol)

− May target a specific family member (e.g. omega 3 for joint pain in grandparents)

− May reflect wider "healthy living" worldview

− May target specific foods perceived as high risk, unethical or visible (e.g. unsustainable fish species)

− May target a specific family member (e.g. mercury levels for children)

− May represent a need for an immediate solution (e.g. thirst, hunger)

− May represent an easy solution to a future challenge (e.g. prepared seafood canapes for easy entertaining)

− May range from "everyday luxury" to an occasional "treat"

− May be used to demonstrate social status, taste or style (e.g. fresh lobster for Chinese banquets)

I am concerned about my health and am trying to live a healthy lifestyle

I am mindful of where my food comes from and how it is produced

I am trying to achieve work-life balance and need quick-and-easy meal solutions

I like to indulge in rich and sumptuous living beyond the bare necessities

FOUR CONSUMER FOOD & BEVERAGE MEGA-TRENDS

Natural mussels

New Zealand seafood products succeeding on-shelf in export markets are aligned with these trends

Source: various online websites; Coriolis research and analysis 50

Trusted brand

NZ mussels

Cooked, shelled, ready-to-eat

Secret marinade

Ready-to-eat

Omega 3

Manuka smoked

Salmon slices

Ready-to-eat

Premium New Zealand

NZ king salmon

NZ King Salmon

Kosher Kiwi

Ready-to-eat

Manuka smoked

Australia Singapore Singapore

H&W

A&R

A&R

E&C

E&C

S&I

H&W

A&R