The influence of non-financial values and goals on the ...FILE/dis4518.pdf · The influence of...

213

The influence of non-financial values and goals on the internationalisation process of Austrian, German and Swiss family businesses to emerging Asia DISSERTATION of the University of St. Gallen, School of Management, Economics, Law, Social Sciences and International Affairs to obtain the title of Doctor of Philosophy in Management submitted by Stephan Erdödy from Hungary and Germany Approved on the application of Prof. Dr. Li Choy Chong and Prof. Dr. Martin Hilb Dissertation no. 4518 Gutenberg AG, Schaan 2016

-

Upload

vuongthuan -

Category

Documents

-

view

214 -

download

1

Transcript of The influence of non-financial values and goals on the ...FILE/dis4518.pdf · The influence of...

The influence of non-financial values and goals on the

internationalisation process of Austrian, German and Swiss

family businesses to emerging Asia

DISSERTATION

of the University of St. Gallen,

School of Management,

Economics, Law, Social Sciences

and International Affairs

to obtain the title of

Doctor of Philosophy in Management

submitted by

Stephan Erdödy

from

Hungary and Germany

Approved on the application of

Prof. Dr. Li Choy Chong

and

Prof. Dr. Martin Hilb

Dissertation no. 4518

Gutenberg AG, Schaan 2016

ii

The University of St. Gallen, School of Management, Economics, Law, Social

Sciences and International Affairs herby consents to the printing of the present

dissertation, without herby expressing any opinion on the views herein expressed.

St. Gallen, May 30, 2016

The President:

Prof. Dr. Thomas Bieger

iii

Dedicated to my parents

iv

Acknowledgements

I would like to thank Prof. Dr. Li Choy Chong for his guidance and outstanding

support throughout the process of this thesis. Prof. Chong has always encouraged me

to strive for the best possible result. I would also like to express my gratitude to my

second supervisor, Prof. Dr. Martin Hilb, for his support and advice.

Moreover, I would like to thank those people who have participated in the interviews

for this thesis and made this project possible.

Especially, I would like to thank my dear friend Philipp Bierl, with whom I had many

inspiring conversations and whose continuous support has advanced my thinking on

many business and personal matters. Thank you for this, Philipp!

Finally, I would like to thank my family, for their patience and loving support during

all phases of my life and especially during my time as a PhD student.

Munich, 17 December 2015,

Stephan Erdödy

v

Abstract

Family Businesses (FBs) represent the backbone of the economies of Austria,

Germany and Switzerland (AGS). These companies are different from their non-

family peers in terms of both resources and capabilities. Especially FBs seem to have

specific non-financial values and goals influencing their decision- and strategy-

making. The field of non-financial values and goals in FBs is, however, largely

uncovered. At the same time, these FBs increasingly need to internationalise in order

to grow. The prospering regions of Asia, specifically China and the ASEAN states,

have become the target of internationalisation activities of these companies. Still, how

these FBs internationalise is not known.

Furthermore, it can be assumed that the non-financial values and goals of FBs

influence the internationalisation process to emerging Asian countries. Nonetheless,

existing theories are insufficient to explain this phenomenon.

Driven by this gap in management research, this study used Straussian Grounded

Theory to set forth a new theory on how non-financial values and goals influence the

internationalisation process of AGS FBs to emerging Asia. The study found that non-

financial values and goals are main referencing points for international decision- and

strategy-making. While non-financial values exercise influence beyond the scope of

context and time, non-financial goals remain unchanged in nature, but have a dynamic

influence on the internationalisation process at different points in time.

With these results, the present study contributes to research of non-financial values

and goals by identifying the difference between values and goals and by describing

their nature. It also contributes to FBs internationalisation studies by shedding light on

the nature of the internationalisation process of AGS FBs to emerging Asia. Further, it

yields implications for FB management to understand how their non-financial values

and goals influence the internationalisation process and how they can be managed.

vi

Zusammenfassung

Familienunternehmen (FU) stellen das Rückgrat der österreichischen, deutschen und

schweizer Volkswirtschaften (DACH) dar. Diese Unternehmen weisen deutliche

Unterschiede, sowohl in ihren Ressourcen und Fähigkeiten, zu ihren nicht-FU

Wettbewerbern auf. Insbesondere scheinen FU spezielle nichtökonomische Werte und

Ziele zu haben, die ihre Entscheidungs- und Strategiefindungsprozesse beeinflussen.

Gleichzeitig internationalisieren FU verstärkt, um zu wachsen. Die aufstrebenden

Regionen Asiens, vor allem China und die ASEAN Staaten, sind zu Hauptzielen von

Internationalisierungsaktivitäten dieser Unternehmen geworden. Allerdings ist

unbekannt, wie FU dorthin internationalisieren.

Des Weiteren kann davon ausgegangen werden, dass nichtökonomische Werte und

Ziele von FU den Internationalisierungsprozess nach Asien beeinflussen. Existierende

Theorien sind allerdings nicht darauf ausgerichtet, dieses Phänomen hinreichend zu

erklären.

Aufgrund dessen, verwendet diese Studie die Straussian Grounded Theory um eine

neue Theorie über den Einfluss nichtökonomischer Werte und Ziele auf den

Internationalisierungsprozess von DACH FU nach Asien zu etablieren. Die Ergebnisse

dieser Studie zeigen, dass nichtökonomische Ziele wichtige Entscheidungsgrundlagen

für Internationalisierungsstrategien sind. Während nichtökonomische Werte ihren

Einfluss über Kontexte und Zeiträume hinweg ausüben, bleiben nichtökonomische

Ziele zwar an sich unverändert, aber haben einen dynamischen Einfluss auf den

Internationalisierungsprozess zu verschiedenen Zeitpunkten.

Mit ihren Ergebnissen trägt diese Studie zur Forschung über nichtökonomische Werte

und Ziele in FU bei, indem sie Werte und Ziele klar trennt und ihre einzelnen Attribute

definiert. Zusätzlich erweitert sie das Wissen über FU Internationalisierungsprozesse.

Abschließend gibt die Studie praktische Hinweise für die Unternehmensführung von

FUs, wie nichtökonomische Werte und Ziele den Internationalisierungsprozess nach

Asien beeinflussen und wie sich diese steuern lassen.

vii

Table of Contents

Acknowledgements ...................................................................................................... iv

Abstract .......................................................................................................................... v

Zusammenfassung ........................................................................................................ vi

Abbreviations ............................................................................................................... xi

Tables ........................................................................................................................... xii

Figures ......................................................................................................................... xiii

1. Introduction ............................................................................................................... 1

1.1 Research context ................................................................................................... 1

1.2 Previous research .................................................................................................. 2

1.3 Research objectives ............................................................................................... 3

1.4 Key definitions ...................................................................................................... 4

1.4.1 Defining the FB ..................................................................................................... 4

1.4.2 Defining values and goals ..................................................................................... 7

1.4.3 Defining internationalisation ................................................................................. 9

1.4.4 Defining process .................................................................................................. 10

1.4.5 Defining emerging Asia ...................................................................................... 10

1.5 Dissertation structure .......................................................................................... 11

2. Research context ..................................................................................................... 13

2.1 FBs in AGS ......................................................................................................... 13

2.1.1 The economic role of FBs in AGS ...................................................................... 13

2.1.2 The role of internationalisation for AGS FBs ..................................................... 14

2.2 The economic development of emerging Asia ................................................... 16

2.2.1 Economic development from 1950 to 1995 ........................................................ 16

2.2.1.1 China ........................................................................................................... 16

2.2.1.2 The ASEAN states ........................................................................................ 17

2.2.2 Economic development since 1995 ..................................................................... 19

2.3 The culture of AGS and emerging Asia .............................................................. 21

viii

2.4 Summary ............................................................................................................. 24

3. Literature review and research question .............................................................. 25

3.1 Non-financial values and goals ........................................................................... 26

3.1.1 Economic model of man ...................................................................................... 26

3.1.1.1 Agency theory .............................................................................................. 27

3.1.2 Humanistic model of man ................................................................................... 28

3.1.2.1 Behavioural theory of the firm .................................................................... 29

3.1.2.2 Stewardship theory ...................................................................................... 30

3.1.3 Mixed models ...................................................................................................... 32

3.1.3.1 Behavioural agency theory .......................................................................... 32

3.1.3.2 Socioemotional wealth view ........................................................................ 33

3.2 Internationalisation processes of the company ................................................... 36

3.2.1 Economic school of internationalisation ............................................................. 36

3.2.1.1 Transaction cost theory ............................................................................... 37

3.2.1.2 Internalisation theory .................................................................................. 38

3.2.1.3 Eclectic framework ...................................................................................... 39

3.2.1.4 Resource-based theory ................................................................................ 41

3.2.2 Internationalisation as an experimental learning process .................................... 42

3.2.2.1 Psychic distance .......................................................................................... 43

3.2.2.2 The Uppsala model of internationalisation ................................................. 45

3.2.2.3 Innovation-related models – the Born Global theory .................................. 48

3.3 Research gap and research question .................................................................... 51

4. Methodology ............................................................................................................ 55

4.1 Research philosophy ........................................................................................... 55

4.2 Research approach – the choice of qualitative research ..................................... 57

4.3 An inductive approach ........................................................................................ 59

4.4 Arguments for the use of grounded theory ......................................................... 59

4.5 Data collection and analysis ................................................................................ 61

4.6 Data collection strategy ....................................................................................... 62

4.6.1 Data sampling ...................................................................................................... 62

4.6.2 Data sources ......................................................................................................... 63

ix

4.6.3 Data analysis procedures ..................................................................................... 66

4.6.3.1 Open coding ................................................................................................. 66

4.6.3.2 Axial coding ................................................................................................. 68

4.6.3.3 Selective coding ........................................................................................... 69

4.6.4 Pilot case .............................................................................................................. 69

4.6.5 Expert interviews ................................................................................................. 71

4.6.6 Ensuring validity and reliability .......................................................................... 75

4.7 Limitations of this research ................................................................................. 76

5. Findings from the cases .......................................................................................... 77

5.1 Non-financial values and goals of AGS FBs ...................................................... 77

5.1.1 Non-financial values of AGS FBs ....................................................................... 77

5.1.2 Non-financial goals of AGS FBs ......................................................................... 79

5.1.3 Summary of findings on non-financial values and goals of AGS FBs ................ 82

5.2 Internationalisation process of AGS FBs to emerging Asia ............................... 83

5.2.1 Internationalisation strategies of AGS FBs to emerging Asia ............................. 83

5.2.1.1 Internationalisation paths of AGS FBs ........................................................ 83

5.2.1.2 Market entry modes and target markets of AGS FBs to emerging Asia ...... 86

5.2.2 Internationalisation strategy development of AGS FBs to emerging Asia ......... 89

5.2.2.1 The strategy- and decision-making process ................................................ 89

5.2.2.2 Decision drivers ........................................................................................... 90

5.2.2.3 Internationalisation timing .......................................................................... 91

5.2.3 Summary of findings on the internationalisation process of AGS FBs to

emerging Asia ..................................................................................................... 93

5.3 Cross-case analysis .............................................................................................. 94

6. Influence of non-financial values and goals on the internationalisation process

of AGS FBs to emerging Asia .............................................................................. 101

6.1 Non-financial values and goals of AGS FBs .................................................... 102

6.2 Internationalisation pattern to emerging Asia ................................................... 103

6.2.1 Timing ............................................................................................................... 103

6.2.2 Market pattern ................................................................................................... 105

6.2.3 Internationalisation path .................................................................................... 106

x

6.3 International management ................................................................................. 110

6.3.1 Planning and strategy-making ........................................................................... 110

6.3.2 International knowledge management ............................................................... 112

6.3.3 International cultural management .................................................................... 115

6.3.4 International financial management .................................................................. 118

6.3.5 International human resources management ..................................................... 120

6.3.6 International network management ................................................................... 123

6.3.7 International control management ..................................................................... 126

6.3.8 International marketing management ................................................................ 128

6.4 Incremental process of AGS FB internationalisation to emerging Asia and the

dynamic influence of non-financial values and goals ....................................... 132

6.5 Proposition table ................................................................................................ 134

7. Conclusion ............................................................................................................. 140

7.1 Theoretical implications .................................................................................... 140

7.1.1 Non-financial values and goals in AGS FBs ..................................................... 141

7.1.2 AGS FB internationalisation processes to emerging Asia ................................ 142

7.1.3 Influence of non-financial values and goals on the internationalisation process of

AGS FBs to emerging Asia ............................................................................... 143

7.1.4 Straussian grounded theory in FB internationalisation studies ......................... 144

7.2 Managerial implications .................................................................................... 145

7.3 Future research .................................................................................................. 146

8. List of References .................................................................................................. 148

9. Appendix ................................................................................................................ 175

xi

Abbreviations

Abbreviation Meaning

AGS Austria, Germany and Switzerland

ASEAN Association of Southeast Asian Nations

BG Born Global

DACH Deutschland, Österreich und Schweiz

EU European Union

FB Family Business

FDI Foreign Direct Investment

GDP Gross Domestic Product

HR Human Resources

IMF International Monetary Fund

IP Intellectual Property

KfW Kreditanstalt für Wiederaufbau

KPI Key Performance Indicator

MNE Multinational Enterprise

US/USA United States/United States of America

WTO World Trade Organisation

xii

Tables

Table 1: Research problem and questions .................................................................. 4

Table 2: Average share of AGS FB export sales as percentage of total sales........ 14

Table 3: Summary of the agency theory ................................................................... 27

Table 4: Summary of the stewardship theory .......................................................... 31

Table 5: Research problem and research question.................................................. 54

Table 6: Qualitative and quantitative research approaches ................................... 58

Table 7: Sources of evidence used for this study...................................................... 64

Table 8: Example of the open coding process .......................................................... 67

Table 9: Changes in the interview guide ................................................................... 70

Table 10: Key information on the expert interviewees ........................................... 73

Table 11. Actions to ensure validity and reliability ................................................. 75

Table 12: Internationalisation paths of AGS FBs to emerging Asia ...................... 84

Table 13: Overview of international activities of AGS FBs in emerging Asia ...... 87

Table 14: Cross-case analysis ..................................................................................... 95

Table 15: Internationalisation timing of AGS FBs to emerging Asia .................. 104

Table 16: Internationalisation market pattern of AGS FB to emerging Asia..... 106

Table 17: Internationalisation pattern of AGS FB to emerging Asia .................. 109

Table 18: Internationalisation planning and strategy-making of AGS FBs to

emerging Asia ............................................................................................................ 112

Table 19: International knowledge management of AGS FBs ............................. 115

Table 20: International cultural management of AGS FBs .................................. 118

Table 21: International financial management of AGS FBs ................................ 120

Table 22: International HR of AGS FBs ................................................................ 123

Table 23: International network management of AGS FBs ................................. 126

Table 24: International control management of AGS FBs ................................... 128

Table 25: International marketing management of AGS FBs .............................. 132

Table 26: Proposition table ...................................................................................... 135

Table 27: Theoretical contributions on non-financial values and goals in FBs .. 142

Table 28: AGS FB internationalisation process to emerging Asia ....................... 143

Table 29: Influence of non-financial values and goals on the internationalisation

process of AGS FB to emerging Asia ...................................................................... 144

xiii

Figures

Figure 1: Triangle of family business definition ........................................................ 5

Figure 2: Interest groups in FBs .................................................................................. 6

Figure 3: Influence of values on goals and actions .................................................... 8

Figure 4: Estimated future development of international sales of AGS FBs ........ 14

Figure 5: Future international growth markets of AGS FBs ................................. 15

Figure 6: Annual GDP growth in Greater China and the ASEAN states (in %) . 19

Figure 7: GDP per capita growth in Greater China and ASEAN states (in %) ... 20

Figure 8: Annual foreign direct investment net inflow ($billions) ......................... 21

Figure 9: The revised Uppsala model of 2009 .......................................................... 47

Figure 10: Philosophical assumption in social sciences ........................................... 56

Figure 11: Grounded theory’s recursive analysis approach ................................... 61

Figure 12: Principals of the honourable merchant .................................................. 79

Figure 13: Non-financial values and goals of AGS FBs .......................................... 83

Figure 14: First international activities of AGS FBs ............................................... 91

Figure 15: First market entry of AGS FBs in Asia .................................................. 92

Figure 16: Non-financial values and goals of AGS FBs ........................................ 103

Figure 17: The establishment chain of international production to emerging Asia

and influencing non-financial values and goals ..................................................... 107

Figure 18: Development of family influence on internationalisation planning and

strategy-making over time ....................................................................................... 111

Figure 19: The influence of quality and reputation goals on the branding strategy

..................................................................................................................................... 131

Figure 20: The influence of non-financial values and goals on an AGS FB’s

internationalisation strategy formulation to emerging Asia ................................. 133

1

1. Introduction

1.1 Research context

Family Business (FB) research argues that FBs differ substantially from their non-FBs

counterparts (Chua et al., 2003; Zellweger et al. 2013). Certain non-financial values,

goals and characteristics and overall the close relationship between the family, the

individual and the business (Gersick et al., 1997, Gómez-Mejía et al., 2007, 2011) are

found to provide valuable assets to the company and are seen to be key pivotal

reference points for decision-making (Gómez-Mejía, 2007, 2011). Also, FBs try to

preserve and enhance these non-financial values and goals (Berrone et al., 2012).

At the same time FBs increasingly find themselves in an international business

environment (Claver et al., 2007). Previous studies have shown that FBs act differently

in the international environment, compared to non-FBs. Factors such as limited access

to capital (Fernandéz & Nieto, 2005), the influence of their ownership structure

(Fernandéz & Nieto, 2006; Holt, 2012) or lack of managerial capabilities (Graves &

Thomas, 2008) make FBs act cautiously and may restrain internationalisation. On the

other side, FBs wish to pass the company on to the next generation (Berrone et al.,

2012) and may want to provide job opportunities for family members (Gómez-Mejía

et al., 2007) and therefore need to observe growth opportunities, e.g. through

internationalisation (Claver et al., 2009).

Austria, Germany and Switzerland (AGS) are traditionally rich of FBs (Niefert et al.,

2009). In Austria 90% (Dörflinger et al., 2013), in Germany 93% (Niefert et al., 2009)

and in Switzerland 88% (Fueglistaller & Zellweger, 2007) of all privately held firms

are FBs. In addition, FBs provide a high percentage of jobs being subject to social

insurance (Stiftung Familienunternehmen, 2015). Also, they employ up to three

quarters of their employees on domestic shores while stock exchange listed non-FBs

from AGS only employ about a third of their staff in AGS.

Internationalisation is at the very heart of AGS FBs success, as about 80% are

involved in international activities (PWC, 2012). On average, 35% of total corporate

sales are generated from internationalisation activities. German-speaking FBs have led

the internationalisation wave to the prospering regions of Asia (China and the

2

Association of Southeast Asian States (ASEAN) for many years (KfW Economic

Research, 2012). According to PWC (2013), Asia accounts for 31% of international

sales of AGS FBs. China for instance, is the second most important international

market for AGS FBs, accounting for 27,4% of international sales. Internationalising to

Asia is therefore considered a necessity in the industry. Many FBs from AGS are

already present in Asia or are looking more seriously into deepening their commitment

(^ Economic Research, 2012; PWC, 2012).

Given the important role of FBs in AGS, it is beneficial to understand how their non-

financial values and goals affect their strategy-making. This is especially important

looking on the internationalisation process of such firms to emerging Asian countries.

As a consequence, deepening knowledge in this specific area is indeed a necessity.

1.2 Previous research

FB research just recently started to realize that there are non-financial values and goals

in FBs and that they may be captured in defining factors or endowments (Gómez-

Mejía et al., 2007, 2011; Berrone et al., 2012; Pukall & Calabró, 2013). The field

acknowledges that non-financial values and goals act as pivotal reference points of

decision and strategy-making and hence influence the business deeply (Naldi et al.,

2013). However, previous research falls short on explaining what exactly non-

financial values and goals in FBs are and how to distinguish them. In addition,

previous studies have not acknowledged how, why, when, where and by whom non-

financial values and goals play out in decision and strategy-making processes, but only

that they affect decision and strategy-making. Also, this field has mainly been

developed conceptually and lacks empirical proof across different data population and

cultural contexts (Pukall & Calabró, 2013). As a consequence not much about non-

financial values and goals in FBs and their specific influence is known.

Internationalisation studies have widely relied on theories that gained their empirical

grounding from samples of large, mainly manufacturing, multinational companies

(McDougall & Oviatt 1996, Johanson & Vahlne, 2009). Studies on SME and FB

internationalisation share the view that established theories are not satisfactory in

explaining internationalisation (Thai, 2008) and that they lack a processual perspective

(Kontinen & Ojala, 2010a). Furthermore, previous studies looked on FB

3

internationalisation from developed markets e.g. from Western Europe1 (Gallo & Pont,

1996; Fernandéz & Nieto, 2005, 2006; Claver et al. 2007; Pinho, 2007; Claver et al.,

2009), the Scandinavian countries (George et al., 2005; Kontinen & Ojala, 2010 a,

2010 b; 2011 a, 2012) or from the Anglo-Saxon world (Okoroafo, 1999; Davis &

Harveston, 2000; Zarah, 2003; Graves & Thomas, 2008). Oddly enough, these studies

rarely focused on particular target markets (Kontinen & Ojala, 2010a), which can be

described as a main issue in internationalisation. In addition, they have left AGS FBs

uncovered, despite their economic importance and the cultural influences on non-

financial values and goals that might apply in this context.

How non-financial values and goals shape the internationalisation process of AGS FBs

to emerging Asia is therefore an unresearched field (Pukall & Calabró, 2013; Liang et

al., 2014). Given the economic relevance of FBs in AGS countries and the status quo

in the research streams of non-financial values and goals of FBs, as well as FB

internationalisation there is a strong need for explanatory studies in this neglected area.

1.3 Research objectives

This research endeavour was triggered by the lack of research on non-financial goals

and values in FBs and the missing explanatory power of current internationalisation

theories. This work‟s main aim has therefore been to connect both research areas and

try to understand how non-financial values and goals in FBs shape the

internationalisation process. Due to the adopted focus the context of AGS FBs

internationalising to emerging Asia was chosen, mainly stemming from the virtually

non-existent body of research in this area despite the economic importance of FBs in

AGS and the high level of internationalisation activities of these firms in the emerging

countries of Asia.

With this, the author follows the call of Kontinen & Ojala (2010) to fill the gap of

research on FB internationalisation directed toward a specific target market and the

call of Pukall & Calabró (2013) on the effect of family related factors on FB

internationalisation and the suggestion of Liang et al. (2014) for a deeper investigation

of how family dynamics affect internationalisation processes. The research problem,

goals, questions and objectives are visualized in Table 1.

1 Not including AGS

4

Table 1: Research problem and questions

Research problem Research goals

No existing theory provides satisfactory answers

about the influence of non-financial values and

goals on the internationalisation process of AGS

FBs to emerging Asia

1) Shed light on an unexpected problem

2) Advance theory

Research question Research objective

Overall RQ0: How do non-financial values and

goals influence the internationalisation process of

AGS FBs to emerging Asia?

Sub RQ1: What are non-financial values and

goals in AGS FBs and what is the difference

between the two?

Sub RQ2: What is the nature of the

internationalisation process of AGS FBs to

emerging Asia?

To understand how non-financial values

and goals influence this process

To understand what the non-financial

values and goals of AGS FBs are and

where the difference between the two lies

To learn about their internationalisation

strategy development in the chosen

context

Source: Author`s own creation

The contributions of this study are severalfold. Firstly, it contributes to a) the literature

of non-financial values and goals, b) research on FB internationalisation and c) it helps

to investigate the intercept of the two above fields by looking at how non-financial

goals and values shape the internationalisation process of AGS FBs to emerging Asia.

Secondly, this study delivers insights for FB owners and managers to help them

understand the dynamics that shape the internationalisation process of their businesses.

1.4 Key definitions

This section provides definitions of important key concepts employed in this

dissertation. These concepts were used differently in previous studies. It is therefore

necessary to define each concept for its use in this particular study. The following

paragraphs describe how these concepts are to be understood and why they were

chosen for this research endeavour.

1.4.1 Defining the FB

FB studies have not yet agreed on a common definition of FBs – in fact Gómez-Mejía

et al., (2011) doubt that there will ever be a consensus over this question.

What makes FBs different from other companies is the family involvement (Gómez-

Mejía et al., 2007). Gallo & Sveen (1991) define FBs by two determinants; family

ownership and family control - “a firm where the family owns the stock and exercises

5

full managerial control” (Gallo & Sveen, 1991, p.182). Litz (1996) points out that

intra-organizational aspirations (also often referred to as trans-generational

aspirations) are equally important. These three dimensions can be described as the FB

triangle (as depicted in Figure 1.).

Figure 1: Triangle of family business definition

Source: Own creation based on definition by Litz (1996)

Despite this definition there is considerable heterogeneity among FBs (Melin &

Nordqvist, 2007). Sirmon et al. (2008) differentiates between family-influenced and

family-controlled firms. This study looks on FBs defined as “(a) firm controlled by a

family through involvement in management and ownership, coupled with a

transgenerational vision for the firm” (Zellweger et al. 2013, p. 231).

Additionally, and in order to fully understand the FB it is useful to consider the

various stakeholder groups within a FB. These groups are well summarized by Hilb‟s

(2013) four circle model of stakeholders in FBs as depicted in Figure 2.

6

Figure 2: Interest groups in FBs

Source: Adapted from Hilb et al. (2009, p.10)

The first circle relates to the business owner (Hilb, 2013). The ownership status can

differ from one FB to another. In some cases only one person owns the company

whereas in other cases ownership may be scattered among many family members.

Still, also family members without shares may be actively involved in the company.

The second circle represents the family, regardless of whether family members

actually own company stocks. They may still have significant real or psychological

influence on the FB. The management circle would usually hint at non-family

management. However, this study looks specifically on family-managed FBs (as

defined by Zellweger et al, 2013). Consequently, there is minimum of family

involvement in day-to day management (at least one family member holds a

managerial position). Therefore, this circle may address family as well as non-family

management (as not all management positions are usually held by family members).

The interests of the management may be different from the interests of the family that

7

is not involved in the company management. The last circle relates to the board of

directors (Hilb, 2013). This institution might not exist in every FB. The areas where

the circles overlap describe both possible areas of synergy and of tensions.

This model depicts well, that also FBs are embedded in a complex field of multi-

stakeholders aspirations which can significantly influence the FBs non-financial value

and goal set as well as its strategy-making (Hilb et al., 2009; Hilb, 2013; Zellweger et

al., 2013).

Bearing Hilb‟s (2013) suggestions about the multi-stakeholder perspective in mind this

study uses Zellweger et al. (2013) definition to define and understand the FB. The

reason for this choice is first, that this definition gives a holistic understanding of FBs

and second, that family controlled-firms are the ones where non-financial values and

goals can be expected to show the clearest impact on decision-making (Chrisman et al.,

2012; Zellweger et al. 2013). Thirdly, the intra-organizational aspiration dimension is

included in this definition and captures the behavioural dimension as well as the

possible source of non-financial values and goals, and is therefore well-suited to a

study of the latter (Gómez-Mejía, 2007).

1.4.2 Defining values and goals

Hofstede et al. (1990) referred to values as the driving force behind goals and hence as

the foundation for business behaviour to achieve these goals. Gómez-Mejía et al.

(2007; 2011) introduced the view that values and goals are key pivotal reference points

in FBs for the decision-making process. However, details about the influence of values

on goals and how they may depend on each other is a field that has barely been

covered (Felden & Hack, 2014). Researchers assume that values have long-term

impact on goals and herewith directly influence actions as depicted in Figure 3: Felden

& Hack point out that values and goals may change over time due to external and

internal influences.

8

Figure 3: Influence of values on goals and actions

Source: Adapted from Felden & Hack (2014, p. 36)

Values

Looking specifically on values there have been various attempts to define the term.

The definition of Rockeach (1973) has gained widest acceptance in the field. He

described values as “enduring beliefs that a specific mode of conduct is personally or

socially preferable to an opposite or converse mode of conduct or end-state of

existence” (Rockeach, 1973, p. 5). Guth & Tagiuri (1965) points out that every person

has his/her own set of values. Although the number of personal values tends to be low

and they are commonly influenced by the socio-cultural environment, they are also

existent on a collective level. Specifically, in FBs the family can be seen as the source

of such values. To provide a definition for values in FBs, Felden & Hack (2014) have

collected a set of five criteria, as follows:

Socially inspired and shared within the family (Roth et al. 2009, as cited in

Felden & Hack, 2014)

Serve as orientation framework for family members, because values influence

the social identity of the family (Verplanken & Holland, 2002)

Influence perception and code of conduct of family members (Meglino &

Ravlin, 1998, as cited in Felden & Hack, 2014)

Valid across contexts (Hitlin & Piliavin, 2004)

Stable over time (Klein, 1991)

This study understands values analogous to Rockeach‟s (1973, p. 5) definition and the

five criteria collected by Felden & Hack (2014) and outlined above. This is because

9

Rockeach‟s (1973) definition clearly describes that values exist for guiding inter-

human conduct and provide a framework for ethical behaviour, while Felden & Hack‟s

(2014) list presents a set of defining criteria specifically for values in FBs and stress

that the values of the family become the values of the whole organization.

Goals

Felden & Hack (2014) claim that goals can be derived from values. In organizations,

goals constitute results which are to be achieved by the entity. Depending on the

nature of goals, there may be a hierarchy among them. However, Felden & Hack

(2014) fail to provide a specific definition of goals. In general, the field‟s lack of

definitional clarity on values is dwarfed by the lack of consensus on the definition of

goals. Looking at basic etymology, a goal is “the object of a person’s ambition or

effort; an aim or desired result” (Oxford Dictionary, 2015). Such goals do not need to

be directed toward a tangible output but can be intangible as well. Single goals may

not always be independent from each other but may, in fact, cause each other (Felden

& Hack, 2014). In addition, there may be goals that act against each other.

This study therefore understands non-financial goals of FBs as defined by their

etymology (Oxford Dictionary, 2015). Further, it understands goals as inspired by the

family value system. It focuses on non-financial goals that may yield economic and

non-economic results. The use of this definition is appropriate, because the field has so

far done little to provide a comprehensive definition of goals (Perrow, 1970; Tagiuri &

Davis, 1992; Felden & Hack, 2014). Further, it is open to the nature and possible

interrelationships of goals and to their connection with values. Finally, it allows for

non-financial values, which is the purpose of this study and a barely covered field

(Pukall & Calabró, 2015).

1.4.3 Defining internationalisation

One of the original definitions of internationalisation comes from Turnbull (1987). He

describes internationalisation as outward movement of a firm‟s international

operations. Common agreement on a universal internationalisation definition however,

has not been achieved so far (Andersen, 1997). In an attempt to come up with a

holistic definition Lehtinen & Penttinen (1999, p. 13) suggested the following:

“Internationalisation of a firm concerns the relationships between the firm and

its international environment, derives its origin from the development and

10

utilization process of the personnel’s cognitive and attitudinal readiness and is

concretely manifested in the development and utilization process of different

international activities, primarily inward, outward, and cooperative operations.”

Lehthinen & Penttinen‟s (1999) definition combines three perspectives; the network

dimension, the behavioural influence of the decision-makers and lastly, the process

perspective. All three perspectives match well with the purpose of this study to answer

how non-financial values and goals shape the internationalisation process of AGS FB

to emerging Asia and are hence applied in the remainder of this thesis.

1.4.4 Defining process

Hjorth et al. (2015) state that process studies view the world as something underway,

constantly becoming and perishing. Hirsch (1990) describes processes as sequences of

events and actions that describe how things change over a given time period. Hirsch

adds that theory building, using this definition, will provide answers for the “how?”

and “why?” a process takes a particular course. In 1997, Pettigrew altered this

definition by including a contextual element: “a sequence of individual or collective

events actions and activities unfolding over time in context” (Pettigrew, 1997, p. 338).

Pettigrew‟s (1997) definition is the most appropriate for the use in this study due to the

following reasons. Strategy-making, such as internationalisation, itself is a process

shaped by individuals or collectives, within one or between several companies. Also,

this definition introduces the contextual element in processes, which is given looking

on FB internationalisation to emerging Asia and in the observation of the impact of

non-financial values and goals on this process, which are contextual by nature.

1.4.5 Defining emerging Asia

This study focuses specifically on greater China and the ASEAN member countries

(ASEAN, 2015). To distinguish these regions from the rest of the Asian continent and

to find a term that makes this text easier to read, the following countries are hence

referred to as emerging Asia: China, Hong Kong, Taiwan, Vietnam, Laos, Myanmar,

Thailand, Cambodia, Philippines, Malaysia, Singapore, Indonesia and Brunei

Darussalam.

This includes a large number of different countries with distinct cultures, languages

and economic development stages. But these countries also share strong similarities, in

11

culture and religion, history and taste. In addition, all these states are characterised by

fast and dynamic economic development. This study therefore treats this region as one

broad cultural and geographical area and will highlight differences in the empirical

results, if applicable.

1.5 Dissertation structure

Chapter 1 presented an overview of the research context, as well as the theoretical and

practical reasons for this study. It emphasises the importance of understanding how

non-financial values and goals shape the internationalisation process of AGS FBs.

Also, the research gap is identified and the research objectives and questions posed. In

addition, key definitions for this study are provided.

Chapter 2 provides an introduction into the research context by showing the economic

importance of FBs in AGS and the role that internationalisation plays for these

companies. It also gives a brief overview of the economic development of emerging

Asia from the 1960s until 1995 and provides up-to-date economic data on emerging

Asia from 1995 until today to demonstrate the attractiveness of this prosperous region.

Also it offers insights into the role of culture of the studied regions of AGS and

emerging Asia.

Chapter 3 comprises the literature review. It reviews existing theories in the fields of

non-financial values and goals of FBs and corporate decision-making. The same is

done for internationalisation theories, with an emphasis on internationalisation theories

relevant for FBs. This chapter also delineates the research problem and questions, and

concludes that existing theories do not have the explanatory power to address the set

research question and that hence a new theory is needed to fulfil the objectives of this

study.

Chapter 4 presents the chosen methodology. It comments on the epistemological tenets

and chosen research design by advocating the use of a qualitative research

methodology, namely the Straussian grounded theory. It also describes how samples

were chosen, data collected and analysed, and which validity measures were taken to

improve the robustness of the new theory. Lastly, it comments on the limitations of

this study.

12

Chapter 5 presents the empirical findings of this research project, organised analogous

to the two sub-RQs presented in Table 1. In the first part, it reports in detail on non-

financial values and goals in AGS FBs. In the second part, findings on the

international strategy-making of AGS FBs to emerging Asia are presented.

Chapter 6 puts forward the new theory on the influence of non-financial values and

goals of AGS FBs on their internationalisation process to emerging Asia by answering

the overall RQ (as stated in Table 1). The new theory was developed under Straussian

grounded theory making techniques.

Chapter 7 delineates theoretical and practical implications and contributions of this

study. It concludes the dissertation with proposing future research areas, building on

the insights of this research project.

13

2. Research context

The following chapter provides an introduction into the wider business and economic

context of the research project. It demonstrates the economic importance of FBs in

AGS (in section 2.1) and shows the contribution of internationalisation to the growth

of FBs, specifically internationalisation to Asia. Further, it touches upon emerging

Asia‟s economic development (in section 2.2) and provides current economic data to

highlight the economic potential of emerging Asia.

2.1 FBs in AGS

2.1.1 The economic role of FBs in AGS

FBs play a special role in the economies of AGS: in Austria 90% of privately held

companies are FBs (Dörflinger et al., 2013), in Germany 93% (Niefert et al., 2009),

and in Switzerland 88% (Fueglistaller & Zellweger, 2007). However, these numbers

are often estimations, based on changing FB definitions (Wenzel, 2014). FBs are not

only numerous, but also known for their high-quality products. Up to 1,000 German

FBs belong to the list of world market leaders in their respective market (BDI, 2014).

FBs are commonly associated with the German word “Mittelstand” (The Economist,

2015a). “Mittelstand” has even been adapted in the English language to describe

Germany‟s system of highly specialized and mostly family-owned, medium-sized

companies which have created industrial clusters and structures in their home regions

and are found to contribute significantly to their country‟s economic vibrancy and

stability (The Economist, 2015a). Similar praise is given to FBs in Austria and

Switzerland. Also, FBs were faster to catch up than non-FBs after the financial crisis

(PWC, 2012).

48% of sales2 across all existing companies in Germany, are generated by FBs

(Stiftung Familienunternehmen, 2015), while in Austria this figure is 61% (Dörflinger,

et al, 2013). The benefit for society becomes visible when the contribution of FBs to

the labour market is taken into consideration. In Austria 71% of all employees work in

FBs (Dörflinger et al., 2013) and in Switzerland around 64% (Fueglistaller &

Zellweger, 2007). In Germany 56% of employee contracts subject to social insurance

are prepared by FBs (Stiftung Familienunternehmen, 2015). In the period from 2006 to

2012 the Top 500 German FBs increased their workforce by 11%, while DAX

2 Excluding state owned companies

14

companies decreased their workforce by 7.3% in the same period (BDI, 2014). It is

also found that around 71% of employees of German Top 500 FBs actually work in

Germany, while this figure is only 38% in DAX companies.

2.1.2 The role of internationalisation for AGS FBs

Looking specifically at internationalisation, data shows that it has become a main

source of growth to FBs (PWC, 2012). Nowadays, international sales already represent

up to 48% of total sales of Austrian, 31% of German, and 32% of Swiss FBs. These

percentages are expected to grow by 2017, as shown in Table 2.

Table 2: Average share of AGS FB export sales as percentage of total sales

Country In 2012 Estimate for 2017

Austria 48% 52%

Germany 31% 37%

Switzerland 32% 33%

Source: Adapted from PWC (2012)

Export sales as a proportion of overall sales are expected to grow by 5% across AGS

FBs between 2012 and 2017. In addition, the majority of AGS FBs clearly sees future

exports on the rise (44% of FBs in AGS) as shown in Figure 4.

Figure 4: Estimated future development of international sales of AGS FBs

Source: Adapted from PWC (2012)

15

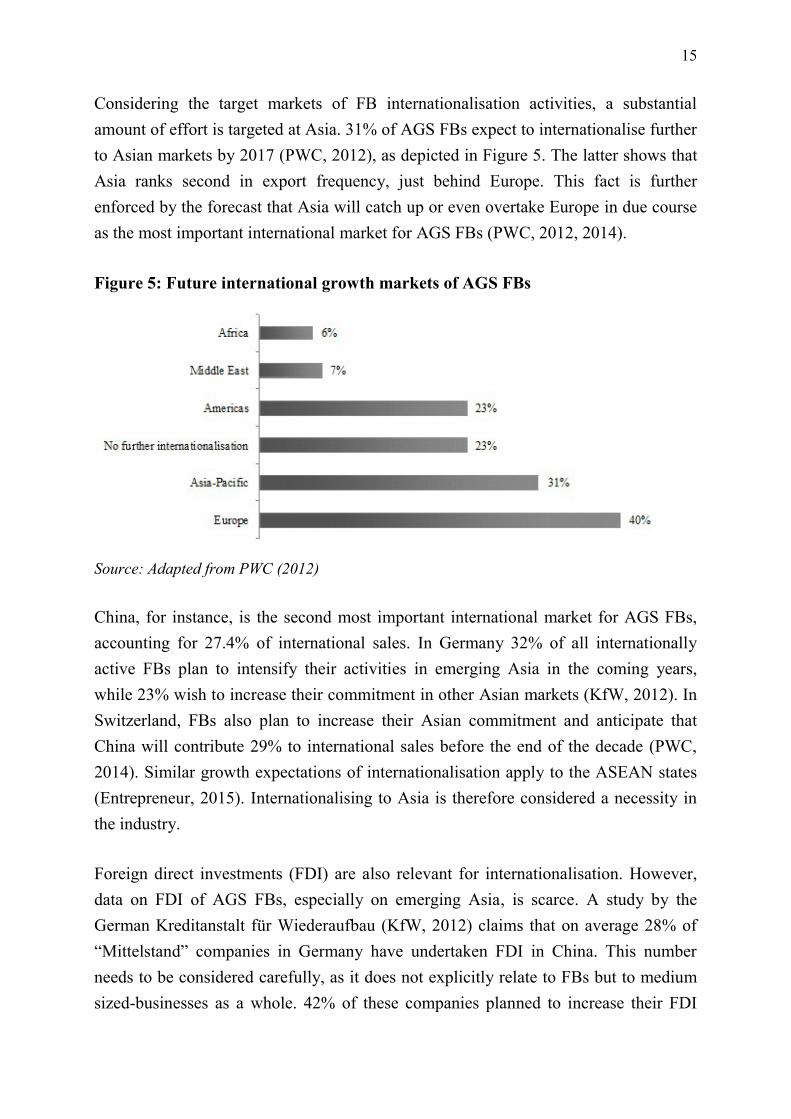

Considering the target markets of FB internationalisation activities, a substantial

amount of effort is targeted at Asia. 31% of AGS FBs expect to internationalise further

to Asian markets by 2017 (PWC, 2012), as depicted in Figure 5. The latter shows that

Asia ranks second in export frequency, just behind Europe. This fact is further

enforced by the forecast that Asia will catch up or even overtake Europe in due course

as the most important international market for AGS FBs (PWC, 2012, 2014).

Figure 5: Future international growth markets of AGS FBs

Source: Adapted from PWC (2012)

China, for instance, is the second most important international market for AGS FBs,

accounting for 27.4% of international sales. In Germany 32% of all internationally

active FBs plan to intensify their activities in emerging Asia in the coming years,

while 23% wish to increase their commitment in other Asian markets (KfW, 2012). In

Switzerland, FBs also plan to increase their Asian commitment and anticipate that

China will contribute 29% to international sales before the end of the decade (PWC,

2014). Similar growth expectations of internationalisation apply to the ASEAN states

(Entrepreneur, 2015). Internationalising to Asia is therefore considered a necessity in

the industry.

Foreign direct investments (FDI) are also relevant for internationalisation. However,

data on FDI of AGS FBs, especially on emerging Asia, is scarce. A study by the

German Kreditanstalt für Wiederaufbau (KfW, 2012) claims that on average 28% of

“Mittelstand” companies in Germany have undertaken FDI in China. This number

needs to be considered carefully, as it does not explicitly relate to FBs but to medium

sized-businesses as a whole. 42% of these companies planned to increase their FDI

16

commitment in the future. Among the group of supporters of further FDI commitment,

38% wish to increase their investments in China and 23% in other Asian countries.

2.2 The economic development of emerging Asia

The economic development of emerging Asia has not been a heterogeneous process

due to the diversity of countries in this region. Mainly socio-economic ideologies such

as communism have kept many countries away from the international market place.

Since the 1970s/1980s there has nevertheless been a process of change which opened

up many of the former closed economies. A short overview of this development is

provided in the context of the period from 1950/1960 until 1995; then several

economic indicators since 1995 are selected to highlight the economic attractiveness of

emerging Asia.

2.2.1 Economic development from 1950 to 1995

2.2.1.1 China

The political developments of the 1940s and 1950s after years of civil war and the

ultimate victory of the communists under Mao Zedong over national forces led China

into almost three decades of political and economic isolation from the rest of the

world. It was not until the year 1978 that China began to open itself and its market to

the world (Chen et al., 1995). Two issues triggered this shift in policy. Firstly,

increasing pressure from the Soviet Union, especially after Vietnam became part of the

Soviet‟s sphere of influence, made China look for mighty partners outside Asia, e.g.

the USA. Secondly, there was a realisation among the communist elite that little

progress was being made with the country‟s current economic policy. China‟s annual

GDP per capita growth was well below her prospering neighbours Japan and South

Korea. Total factor productivity painted an even grimmer picture, as it had had

remained stagnant or even declined since 1957 (Chen et al., 1995).

This situation was the basis on which Deng Xiao-Ping proposed his reform agenda at

the meeting of the communist party‟s central committee in 1978 (Chen et al., 1995).

The party leadership agreed on a policy of the “Open Door” and introduced the “Law

of the People‟s Republic of China on Joint Ventures Using Chinese and Foreign

Investment” in July 1979, which laid the legal foundation for investments in China. In

the subsequent years, the government established a growing number of special

17

industrial zones (e.g. Shenzhen and Zhuhai). Such zones were extended to even more

regions within the country in 1985. These years also saw several amendments and

changes to the joint venture law (e.g. 1988 and 1990) which significantly improved the

business climate for foreign investors. These measures triggered the inflow FDI, which

gained momentum in the late 1980s. In 1991, China received $34.4 billion in FDI,

Hong Kong being the biggest foreign investor, followed by the USA, Japan, the UK

and Germany. Since the early 1990s, China has continued to open its economy and

attract an ever-increasing inflow of FDI (Chen et al., 1995).

2.2.1.2 The ASEAN states

The Association of Southeast Asian States (ASEAN) was established in 1976 by

Indonesia, Malaysia, Philippines, Singapore and Thailand with the aim of creating a

union of economic, social and cultural progress (ASEAN, 2015). In the years from

1984 to 1999 the small oil Sultanate of Brunei Darussalam3 joined the association

together with Laos, Myanmar and Cambodia.

The economic development of ASEAN member states was not homogeneous due to

the deep structural and economic differences among the member states4. Three groups

with different development patterns can be identified (Hill, 1994): the core group

Singapore, Malaysia, Thailand (and to a certain extent Indonesia), the Indochinese

countries (Vietnam, Laos, Myanmar and Cambodia) and the Philippines.

The driving forces of ASEAN‟s economic development were Singapore, Malaysia,

Thailand (and to a certain extend Indonesia) (Hill, 1994). These countries emerged

from colonialism (except Thailand, which has never been a colony) while generally

keeping liberal economic tenets. They also generally adopted pragmatic, effective and

outward-looking policies. This specifically applied (and still does) to Singapore, which

managed to become part of the first world in less than a generation under the wise

leadership of Lee Kuan Yew, while Indonesia was the country which remained most

closed within in this group (The Economist, 2015b). In 1994 Singapore represented

less than 1% of ASEAN‟s population, but contributed around 40% to the association‟s

exports (Hill, 1994). This was somehow paralleled by the rapid growth of these

economies and structural changes over the years, which had less pro-foreign trade

3 Due to its small size and limited economic unimportance, Brunei‟s development is not

discussed in detail 4 Member states as of 2015

18

policies than its ASEAN fellows. These developments created a positive environment

for foreign investors of all kinds. Between 1965 and 1990 economic growth in

Indonesia, Thailand and Malaysia was roughly double that of World Bank‟s “middle

income” parameter, compared to similar countries in the developing world (Hill,

1994).

The countries of Indochina underwent a different development (Hill, 1994). They can

be counted among the late reformers. These countries were characterised by extreme

poverty, radical political ideologies (some still prevailing) and limited accessibility for

foreign investment. This has changed in the last decade and these markets have been

opened to the global economy. Within this group, Vietnam managed to open its

economy by introducing a reform process in 1986. At that time the average per capita

income was $100, but this has increased to roughly $2,000 in 2014 (World Bank,

2015). Myanmar, Laos, and Cambodia did not manage to effectively open their

markets until 1995, and in fact Myanmar only took this step in 2011. It can be said,

however, that these countries have started to adopt the same policies of pragmatism,

effectiveness and outward orientation as their peers in the south over the past 15 years,

and are in the process of opening their economies (World Bank, 2015).

A special case is the Philippines (Hill, 1994). The country inherited much from its

former colonial occupants, such as libertarian economic attitudes and a small state.

From independence until 1970 the Philippines was among the progressive economies

within ASEAN. However, from 1970 until the mid-1980s its GDP per capita stagnated

and put it far behind Thailand, which it had still surpassed in 1970 in terms of GDP

per capita. This can be attributed to many factors, but specifically to protectionist

government behaviour and loose fiscal policies. 1986 marked a turning point, when

deep structural reform policies were introduced (World Bank Operations Evaluation

Department, 1998). The following years saw continuous reform efforts, which began

to bear fruit around 1994-1995 (International Monetary Fund, 1998).

In sum, ASEAN member states experienced different rates of development due to their

diverse political, economic and historic factors. Since mid-1990 (and in the case of

Cambodia, Laos and Myanmar even later) all of these markets have become part of the

world economy and present a highly dynamic and emerging region.

19

2.2.2 Economic development since 1995

After 1995 most countries in emerging Asia had fully opened their markets to world

trade and foreign investors. To highlight the region‟s economic vibrancy and

attractiveness, also for AGS FBs, three main economic indicators are presented and

explained in the following.

Figure 6 shows the annual GDP growth in emerging Asia. Especially Greater China5

showed an average annual GDP growth rate of 6.52% between 1995 and 2014 (World

Bank Database, 2015). ASEAN6 reported an average annual GDP growth of 4.91% in

the same time period. The overall annual GDP has shown a considerable growth since

the 1990s, only interrupted by the 1998 Asian Financial Crisis and the Global

Financial Crisis of 2008/2009.

Figure 6: Annual GDP growth in Greater China7 and the ASEAN states (in %)

Source: Based on data from the World Bank (2015)8

Annual GDP per capita growth paints a similar picture as depicted in Figure 7. While

the Chinese annual GDP per capita grew on average 5.69% per year between 1995 and

2014, ASEAN9 states were slightly behind with 3.27% in the same time period (World

Bank Database, 2015). The overall positive economic development has created wealth

for the peoples of the region. China has managed to create a growing middle class,

accounting for some 250-300 million people (KPMG, 2012). Estimates predict that by

2027 around 800 million Chinese will belong to the middle class. Nevertheless, there

5 China and Hong Kong

6 Does not include Laos (data was not reported to the World Bank)

7 China and Hong Kong

8 Does not include Laos (data not reported to the World Bank)

9 Does not include Laos (data not reported to the World Bank)

20

are substantial differences in real GDP per capita within emerging Asia, ranging from

$56,287 in Singapore to $1,090 in Cambodia (World Bank Database, 2015).

Figure 7: GDP per capita growth in Greater China10

and ASEAN states (in %)

Source: Based on Data from the World Bank (2015)

In addition, emerging Asian countries have become main targets of AGS companies‟

export activities. In 2014, German companies alone sold goods and services worth

87.11 EUR billion to Greater China11

and about 22.27 EUR billion to ASEAN12

states

(Statistisches Bundesamt, 2015). In 2014, Swiss companies exported goods and

services accounting for some 36.05 billion EUR (39.02 CHF) to greater China13

(Statistik Schweiz, 2015). Much smaller volumes apply to Austrian companies, which

had an export volume of 3.13 EUR billion to China and 1.65 billion to ASEAN in

2014 (Statistik Austria, 2015).

A more informative indicator for the international attractiveness of a market for

foreign companies than export volumes (as mentioned above) is FDI inflow (KPMG,

2012). Figure 8 shows that Greater China14

attracted by far the largest portion of

incoming investments between 1995 and 2013 (World Bank Database, 2015).

Specifically, since 2004 Greater China has seen an increasing influx of foreign

investment. This may in part be due to the considerable softening of joint venture

laws, being a matter of critique by many foreign companies, and China‟s entry into the

World Trade Organisation in 2001 which forced it to adapt more foreign investor-

friendly policies and standards (KPMG, 2012). It should be noted that for several years

10

China & Hong Kong 11

China, Hong Kong & Taiwan 12

Not including Cambodia 13

China and Hong Kong 14

China and Hong Kong

21

there has been a shift in the type of FDI. The 1990s and early 2000s saw FDI

capitalising on the competitive production cost basis. Today FDI is becoming more

and more an issue of customer access and proximity (KPMG, 2012).

Figure 8: Annual foreign direct investment net inflow ($billions)

Source: Based on Data from the World Bank (2015)

A similar picture appears in the case of the ASEAN15

states, though the total number

of FDI inflow is more modest (World Bank Database, 2015). Also in this case, a

steady rise can be observed since 2004, only interrupted by the world financial crisis

of 2008/2009. In 2013/2014, FDI in ASEAN accounted for roughly 8% of global FDI

(ASEAN Investment Report 2013/2014). Between 2012 and 2014 ASEAN states

received some $58.0 billion in FDI from countries from the European Union16

(ASEAN, 2015). As a consequence, the European Union is the biggest source of FDI

to ASEAN.

2.3 The culture of AGS and emerging Asia

When international business is concerned the role of culture needs to be addressed.

Tylor (1974, p. 1) defined culture as “that complex whole which includes knowledge,

belief, art, morals, law, custom, and any other capabilities and habits acquired by man

as part of a society”. Often this definition is supplemented by adding that culture is a

process over successive generations (Parson, 1954). Despite those who claim that

globalization is marginalizing local cultures by diluting their authenticity it is

unchallenged that hug cultural differences prevail, ranging from language, religion and

15

Does not include Laos (data not reported to the World Bank) 16

Including Switzerland

22

tastes to business ethics (Kvint, 2010). Kvint (2010) calls culture a strategic risk factor

that needs to be carefully considered for a successful internationalization strategy.

In order to provide guidance on assessing culture numerous scholars have undertaken

studies to yield frameworks that could henceforth be used by sociologist, and

companies, to study this issue. Two contributors to this debate are Laurent (1997) and

Hofstede et al. (2010).

Laurent (Laurent, 1997, as cited in Hilb, 2013) provided a set of 10 dimensions

ranging from attributes such as time horizon, decision driver, over way of decision-

making to goals of interaction. The assessment of these attributes results in a nation

either being a hard (e.g. the USA) or a soft culture (e.g. Vietnam).

Similar to Laurent, and based on a sample of 116.000 IBM employees across the

globe, Hofstede et al. (2010) developed six cultural dimensions. 1. power distance, 2.

individualism vs. collectivism, 3. masculinity vs. feminity, 4. uncertainty avoidance

index, 5. long-term orientation and 6. indulgence versus restraint. Each dimension

describes a key cultural evaluation parameter. For example, power distance relates to

the way, power and hierarchy are understood in a culture. The USA is a country that

shows very low power distance, as the people have equal rights and in an organization

setting favour flat hierarchies between peers and subordinates (Hofstede, et al. 2010).

The situation is different in China where strict hierarchies in both society and

organizations are highly valued. Though Hofstede‟s work has become the target of

extensive critique in the field of cultural sciences it is widely applied in management

science (Fischer et al., 2010; Mazanec et al., 2015).

Looking on the geographical setting of this thesis, two cultural areas are studied; AGS

on the one side and emerging Asia (as defined in section 1.4.5) on the other. Logic

implies that larger sets of countries as used in this study show cultural heterogeneity.

Turning to AGS it becomes clear that the single countries show many differences in

the dimensions laid out by Laurent (1997, as cited in Hilb, 2013) and Hofstede (2010).

While Germany is in Laurent‟s evaluation certainly a hard culture when it comes to

negotiations and power transferral within an organization, Austria and Switzerland are

soft in that respect. Looking on Hofstede‟s et al. (2010) dimension of long-term

orientation, however, all three countries share a similar orientation for rather long

23

relationships in life and business. Despite these academic categories there are obvious

cultural similarities like geographical proximity, religion, language and history. All

three countries were once members of the Holy Roman Empire and Austria and

Germany only became formally separated after Emperor Franz Joseph I. had called an

end to the union in 1806 (Putzger, 1999). Despite the differences between the AGS

countries it is still justifiable to treat them as a broad cultural area, which may differ in

single specific factors but share the important fundaments of culture, language, history

and religion.

Looking on emerging Asia (as defined in section 1.4.5) a similar situation becomes

observable. The countries of emerging Asia stretch from China‟s cold northern borders

with Russia to the tropical islands of Indonesia. Naturally, these countries show many

cultural differences. Looking on Laurent‟s (2010) approach to distinguish between

hard and soft cultures, Hong Kong and Singapore show common characteristics of

hard cultures (The Economist, 2015b), comparable to the Anglo-Saxon world or to a

certain degree even Germany, (e.g. both Asian nations value achievements of results

rather than relationships) (Hofstede et al. 2010). By contrast, Thailand and or other

countries in south east Asia are soft cultures and stress the importance of long-term

relationships with people over the achievements of fast results (Hofstede et al. 2010).

But also strong cultural similarities exist. One example is religion, as Buddhism and

Confucianism (in their different denominations) are the most widespread faiths in this

region (although Islam is predominant in Malaysia and Indonesia after having replaced

Buddhism several centuries ago) (Encyclopaedia Britannica, 2016). In addition, some

of these Asian nations host powerful diasporas of other ethnicities within their country.

This specifically applies to the Chinese minorities in south east Asia, e.g. in Singapore

or Thailand where ethnic Chinese make up 11% of the total population (Academy for

Cultural Diplomacy, 2016). These minorities often hold substantial power in both

business and public service. Furthermore, historical similarities exist. China‟s

emperors had strong influence on their southern neighbours for centuries, so that many

historical similarities and linkages exist (Wright, 2001). Especially history since the

rise of colonialism and de-colonialization has confronted the region with similar

events and problems. In contrast to AGS emerging Asia cannot rely on one lingua

franca. In fact, especially south east Asia is a mosaic of different languages

(Encyclopaedia Britannica, 2016). Nevertheless, and despite the considerable

differences, the region of emerging Asia has strong cultural similarities on many levels

24

(as explained above) and can therefore be treated as one broad cultural region for the

purposes of this thesis.

2.4 Summary

This chapter has demonstrated that FBs play an important part in the national

economies of AGS. Internationalisation has become a main source of growth for these

FBs. Asia, specifically emerging Asia, has become a main playfield of international

activities and growth endeavours. The countries of emerging Asia have taken different

paths of economic development, while finally become part of the global economy.

Nowadays, emerging Asia is characterised by high rates of economic growth and is an

important region for FDI. Despite the considerable cultural differences within AGS

and emerging Asia it is still justifiable to threat them as one broad cultural area as the

single countries share basic cultural, historic and religious fundamentals.

25

3. Literature review and research question

The literature review of this thesis is divided into two major fields, i.e. non-financial

values and goals and internationalisation of FBs.

FB studies usually attempt to identify the essence of FBs by looking at specific

economic resources or varying attitudes towards risk, while others use capabilities

(Habbershon, et al., 2003; Fernández & Nieto, 2005, 2006), e.g. managerial

capabilities or softer factors such as FB culture (Ward, 1988; Corbetta & Salvato,

2004). To view the source of the FB‟s uniqueness as a product of its non-financial

values and goals is a dormant field that awaits discovery.

As a result of this, FB studies have drawn on common theories that deal with general

questions of company and agent behaviour, but do not specifically cover what is

understood by non-financial values and goals. As a consequence, this literature review

attempts to identify and review existing theories that have already been applied (in the

field of FB studies), which seek to explain why decisions are made, implying that

these are influenced by individual non-financial and goal settings. In this group, two

major tenets can be distinguished. On the one side are theories with economic tenets,

for example the Agency Theory (Jensen & Meckling, 1976; Eisenhardt, 1986) and the

Behavioural Agency Theory (Wiseman & Goméz-Mejia, 1998), which claim that the

profitability of decision-making depends on the alignment of the owner‟s and

manager‟s interests (goals respectively) and inclination toward risks (Kahneman &

Tversky, 1972).

This school, however, sees goals in rational-economic terms and does not address non-

financial values. On the other side are humanistic models, such as the Stewardship

Theory, which account for the intrinsic motivation of good company management and

accept non-financial goals as source. Still, they do not comment on the nature and

deeper impact of the latter. A few years ago a hybrid version, rooted in both traditions,