The Income Investor’s Blueprint · workforce at least part-time to pad or rebuild the funds...

26

The Income Investor’s Blueprint Page 1 The Income Investor’s Blueprint Building Income for Life

Transcript of The Income Investor’s Blueprint · workforce at least part-time to pad or rebuild the funds...

The Income Investor’s Blueprint Page 1

The Income Investor’s Blueprint

Building Income for Life

The Income Investor’s Blueprint Page 2

The Income Investor’s Blueprint Page 3

Table of Contents

Introduction 3The New Reality 4Low Interest Income Environment 4Current Income Alternatives 5Income for Life 8Make Room in Your Budget for Consistent Income 9It's Time to Define Your Income Goals…and Meet Them 9The Dirty Little Secret of Options Trading 10What Happens to All Those Losing Trades Anyway 11Generate Income For Life 11Change Your Mindset! Selling is a Different Game Then Buying 12Selling is Low-Risk Option Strategy 12The Benefits of Selling Options 12Yield 13Capital Risk 13A Long Term Strategy 13The (Hidden Shh…) Benefits of Selling Options For Income 13Capital Risk Redux 13Event Indifference, Market Neutrality 14Another Benefit of Selling Options (Covered Calls) 15The Double Dividend Position 16Let's Get Started Generating Real and Consistent Income 17The Income Investor's Blueprint Plan 17Step 1: Generate "instant cash" in Your Account By Selling Puts 17The Put Selling Strategy in Action 18Rules for Selling Puts 18Step 2: Create Your Own Dividend Machine 19How it Works 19Step 3: Get Paid for Building in Downside Protection With Covered Calls 20How it Works 20Step 4: Press Your Advantage by Rolling Positions 22How it Works 22Why Sell Options Now 23

The Income Investor’s Blueprint Page 4

The Income Investor's Blueprint

Introduction If you're a pre-retiree, or a current retiree (or even planning for retirement) what you're about to read is going to make you nervous. We urge you to read this entire report, however, because you're also going to discover a solution to the two problems plaguing most income investors today:

1. Getting the income you need from your portfolio; 2. Without putting your portfolio at serious risk.

First, let's consider the current "Income Investors" landscape and why it is so hard to create the money you need each month without having to dip into your savings or drawdown your investment account.

• Two generations ago, generating income was all about owning stocks that paid solid dividends;

• Two decades ago, CDs appeared yielding far more than any stock; then, • A decade ago, bonds of all sorts had yields far better than Uncle Sam’s with little

risk; then, • Five years ago annuities made a big comeback when the stock market was cut in

half. Right now the dividend yield on the S&P 500 is at historic lows; the yield on $100,000 worth of Treasury bonds is a measly .002% or four dollars a week; corporate bonds may yield a few dollars more per week but they carry substantially more risk; annuities might look tempting but they freeze your capital – actually, they shrink your capital base and lock in your income regardless of inflation, the economy, even regardless of your needs. Are you nervous about your future and your ability to consistently generate enough income to maintain your lifestyle? Or even, being able to retire? Is there a permanent income strategy that works independent of the economy or stock market? Is there a plan out there that I can depend on out there for decades (not just this month's fad), that I can rely upon to meet my monthly or annual income needs?

The answer is yes. Read on.

The Income Investor’s Blueprint Page 5

The New Reality You’ve planned carefully. You’ve trimmed expenses, cut your debt, funded the kids’ education and contributed to your IRA faithfully. But have you saved enough? More than $6.5 billion has evaporated from retirement accounts since 2007, coinciding with a growing trend of workers postponing their retirements or returning to the workforce at least part-time to pad or rebuild the funds they’ve spent most of their working lives building. If you’re one of the 47% of boomers worried about having sufficient funds and access to health care post-retirement, there may not be as much time left as you think to build a large enough income producing portfolio in today’s stock market.

And even if you have more time, how do you go about this in the middle of a “pro-longed” environment of low interest income investments like we are experiencing today? Low Interest Income Environment Talk about challenging times -- household expenses are gapping higher, and we’ve got a bond market that looks like it’s topping out at 2% on the 30-year Treasury. Meanwhile, the best-performing blue chip stocks are maybe paying out about a 3.5%-4% yield – which may not be all that impressive given the hammering that many of those stocks took last year.

The Income Investor’s Blueprint Page 6

To face retirement in an environment where traditional income investments like CDs, money markets and bonds are producing only 0.05% to 2% is depressing. Nobody wants to cut short their retirement dreams just because we happen to live in a time where yields are so low. And it’s no wonder. A retiree with $100,000 in a money market account might earn about $50 a month on those funds. That’s not exactly what retirement dreams are made of, is it? Even at 10 times that amount, you’re pretty much limited to paying the electric bill and buying groceries without dipping into your nest egg or relying on a job that might not be there for as long as you need it.

Having independent control of your retirement assets with a solid game plan is what we all want. Once that’s taken care of, how do we take our (in many cases, smaller) accounts and make them work harder for us – enough to help us meet and even surpass our financial goals? How then can investors and retirees maintain a stable, low-risk income week after week, without having to take on part-time jobs, or rely on high risk investments?

Current Income Alternatives In order to understand what will work, we need to take a deeper look at what is not working.

The Income Investor’s Blueprint Page 7

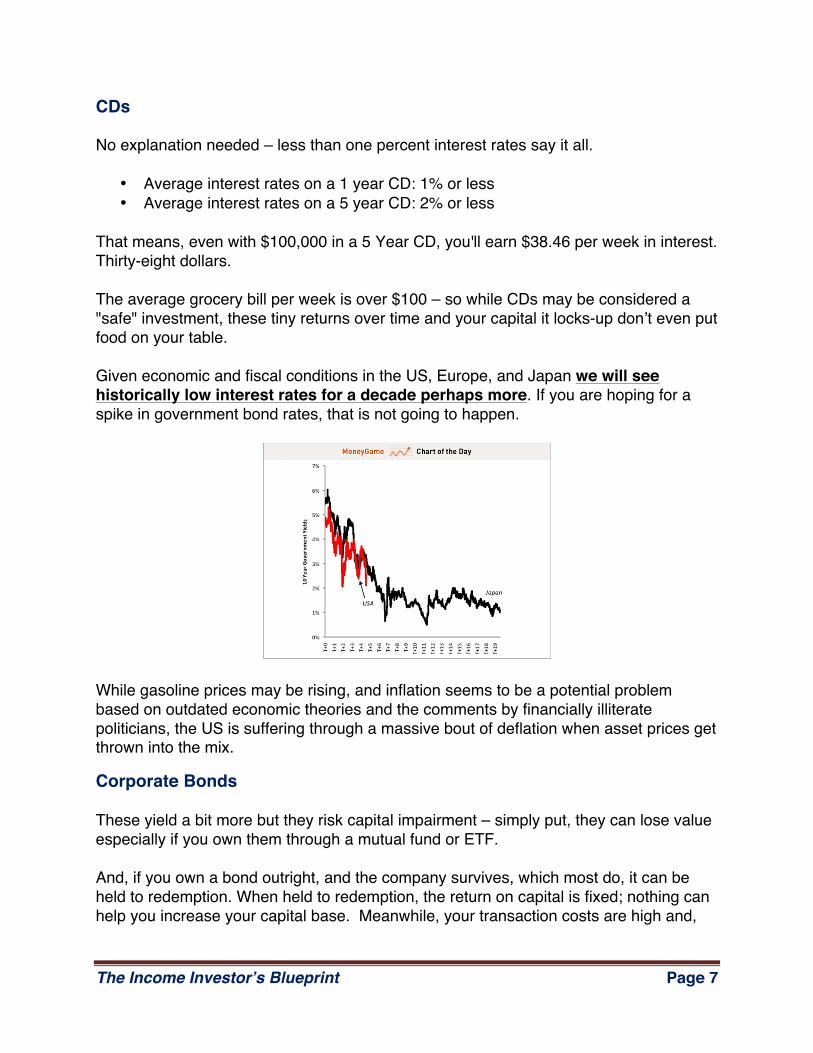

CDs No explanation needed – less than one percent interest rates say it all.

• Average interest rates on a 1 year CD: 1% or less • Average interest rates on a 5 year CD: 2% or less

That means, even with $100,000 in a 5 Year CD, you'll earn $38.46 per week in interest. Thirty-eight dollars. The average grocery bill per week is over $100 – so while CDs may be considered a "safe" investment, these tiny returns over time and your capital it locks-up don’t even put food on your table. Given economic and fiscal conditions in the US, Europe, and Japan we will see historically low interest rates for a decade perhaps more. If you are hoping for a spike in government bond rates, that is not going to happen.

While gasoline prices may be rising, and inflation seems to be a potential problem based on outdated economic theories and the comments by financially illiterate politicians, the US is suffering through a massive bout of deflation when asset prices get thrown into the mix.

Corporate Bonds These yield a bit more but they risk capital impairment – simply put, they can lose value especially if you own them through a mutual fund or ETF. And, if you own a bond outright, and the company survives, which most do, it can be held to redemption. When held to redemption, the return on capital is fixed; nothing can help you increase your capital base. Meanwhile, your transaction costs are high and,

The Income Investor’s Blueprint Page 8

most of all, your yields are still very low, below seven percent and for well rated bonds, below four percent. That means if you are holding a long term bond, the return may not provide you the income you need when cost of living increases and inflation are taken into consideration.

Annuities These income devices are making a comeback as many investors have been pushed out of equity and bond markets by fear of substantial losses to their capital. Yields are low, even if they are guaranteed but as an investor, you are in essence, turning your capital over to a third party in return for the security of their capital and a guaranteed return. You know what the really sad untold story about annuities? You end up locking yourself into an income stream that may not be large enough five or ten years from now to meet your lifestyle preferences. Add to that the danger of hidden inflation (rising food and gas prices), increasing healthcare costs and potential reduction of social security benefits, and your dream retirement may no longer be possible.

High Yield Stocks Put simply – today’s “high-yield” investments are the next "bubble.” There are many good looking high yields investments like closed-end funds, REITs, Master Limited Partnerships and other funds that boast yields of 7% to 12%. Yet, they are very, very high priced as evidenced by the historically low dividend yield of the S&P 500 – to many investors they are over-valued and at risk of suffering an historic collapse should the stock market not hold its current levels. How did this happen? Everyone needs income, or so it seems. But too many investors begin by chasing yield, in other words, they're doing it backwards. Many income investors look at the dividend yield first, the movement of the stock second, the quality of the company third. That is backwards. Investors should always consider the quality of the company and its long term prospects FIRST. Then, the movement of the stock price, then the yield. Doing it this way protects investors from buying high risk companies, which, although you may temporarily collect a high yield, doesn't help when your capital gets cut in half. These stocks and risky income investments can go down and will go down (they did during the crash of 2008 when many REITs and closed end funds were cut in half). Do

The Income Investor’s Blueprint Page 9

individual investors, after one crash, have the stomach to ride out another one as their core capital gets cut so sharply? The impact of capital impairment cannot be overstated. The diagram below pretty much says it all. If your capital base shrinks or is frozen, your total return falls, your capital doesn't appreciate and you are left with less and less income from your investment portfolio.

These are simple explanations of why these income alternatives are inadequate or downright risky. Ok. So after these startling facts and figures, what are you and thousands of other investors looking for income supposed to do? Income for Life There is an easier, simpler way to boost your income than joining the new, growing class of the “working retired” who are postponing their long-anticipated plans for another few years. This income strategy is so effective, that you can earn more in just 10 minutes a week than at the average full-time low-paying job. In fact, 92% of investors following this strategy say they are generating the income they need – just by doing one SIMPLE thing! If you’d like to bring in an extra $500, $1000, $5,000 or more every month (or however much you want) using the money that’s otherwise stagnating in your account—then we have the solution for you. The Income Investor Blueprint is going to teach you how to create a NEW, SUSTAINABLE income stream that you can rely upon to meet your needs without high risk to your capital or long term freezing of your income producing assets.

The Income Investor’s Blueprint Page 10

In this report, you will learn to master the following concepts:

• Create a new, repeatable and sustainable income stream • Protect your capital from Risk • Generate cash weekly, monthly and quarterly • End dependency on low interest or high-risk, capital intensive investments.

Let’s get started. Make Room in Your Budget for Consistent Income You want to generate consistent monthly income, right? For that, you need consistent goals -- the same goal every month. The Income Investor's Blueprint will teach you:

• How to create a minimum target return on your capital of 2% per month. For a $50,000 account, that is $1,000 every month.

• How to tap into an unusual strategy to also create cash every single week, without high risk.

• That capital is not just unused cash in your trading account. If you also own stocks, you'll learn a secret strategy to boosting or even creating a dividend from those stocks.

• Your weekly or monthly target is measured in cash – how much cash at the beginning of a month, how much at the end.

• How to build sustainable income of 1% to 2% a month without tying up your capital for years.

• There are no magic formulas here – the simpler the strategy, the more effective and efficient it becomes. That's because simple means REPEATABLE and sustainable. You will be able to do this again and again.

Be prepared to look at your portfolio in a new way – it’s time to move away from the “how much cash is this going to cost me” mindset and enjoy approaching your nest egg instead with “how much cash is this going to generate?” This isn’t some “here’s the latest hot stock to play” or the “strategy of the moment” that takes a finance degree to learn and execute.

The Income Investor’s Blueprint Page 11

What it is, though, is an easy-to-understand – and just as simple to put into motion, the moment you finish reading this report – approach to defining your income goals and taking the exact steps to meet them! • Each month, every month. • Don’t think about it. Just think of all the stocks in your account just sitting there, earning nothing, or that hot stock you think may be too hot to own at the current price. It’s Time to Define Your Income Goals … and Meet Them Your primary goal is to begin generating an extra $200 to $500 or more in your trading account every month, month after month. That’s a pretty reasonable return, right? Even better, it’s a very realistic goal, and one that you can reach within just a couple of weeks. Then, you'll learn how to add weekly income ON TOP of that monthly income. And the best part is you are going to do it with less risk -- providing better protection for your capital -- and you are going to be able to repeat the income-generation process over and over again to success. Finally, you'll get our secret strategy for tapping into quarterly "cash" on demand you can use to increase your capital base. Together, these three strategies will help you increase your annual income from your portfolio by 24% or higher. First, a quick word: This is a strategy that uses OPTIONS to create income. But not in the way you probably think. That's because most options strategies teach you to BUY options (long). Yet, what they never tell you is that 80% of long options expire… Worthless. That's a 100% loss of premium. Does that seem like a sound strategy? No, of course not. Instead, you'll learn to become the Seller of Options (and you'll have those 80% odds on YOUR side).

The Income Investor’s Blueprint Page 12

The Dirty Little Secret of Option Trading Options are a like a ticking time bomb in your hand. If your preferred method of trading options is to buy calls and puts, that’s like telling the market to just take your money and pay you back “someday, maybe … if you feel like getting around to it.” The truth is, every second you own that option contract is like the second hand of a bomb counting down to zero… blowing up into a useless piece of paper. Why would anyone want to trade options when the deck is stacked against them? Most options traders think of buying options as having “Stocks on Steroids” in their trading accounts. The sad reality is, they continue to cling to that hope, even while they continue to lose money . . . trade after trade (after trade…). What Happens to All Those Losing Trades, Anyway? You know that for every option trade, there are two sides. Buyers can’t buy without sellers. If the options you buy aren’t making you money, you can be certain that the sellers are PROFITING CONSISTENTLY from your losing trades. It’s time to turn the tables … literally. When you move to the other side of the trade, you put those odds squarely back in your favor. That’s how the pros trade . . . taking your money every single time you buy a call or a put. But by becoming an option seller, too, you will understand why the pros prefer their strategy. For starters, you’ll probably quickly get addicted to collecting COLD, HARD cash upfront on every trade. And, the “secret” to selling options is that you enter a trade that has a 99% chance of winning. They're practically GIVING MONEY AWAY on the exchanges. It’s true – the market pays you to make your trades! Not quite sold on selling yet? If building a steady stream of dependable income week-after-week or month-after-month seems impossible, then let’s look at how simple it is to keep the returns flowing in. … Generate Income for Life

The Income Investor’s Blueprint Page 13

You can sell option contracts again and again and again … for as long as you need or want to collect a monthly “bonus” without working harder -- or at all! Consider this . . . . . . You could continue to fight the system and trade options in hopes of the next big MONSTER TRADE (the lottery ticket). . . . Or, you COULD pay yourself FIRST – bringing in $500 each week (or more). Why not turn the tables in your FAVOR . . . and use the sale of options to generate income? Stop trying to hit home runs by “buying options,” and start hitting singles and doubles to score more runs and collect more cash in your account every month. That's why we've developed your personal “blue print” so you can easily create an income machine for yourself: Change Your Mindset! Selling is a different game than buying When you buy an option, you are hoping for a move in the stock based on a chart or event or your brother-in-law’s advice (bad move there). Hopefully, you watch the option move up and then -- when greed, fear or satisfaction set in -- you sell and make a profit. Or you watch it go down and either have an automatic stop loss in to sell it when it hits a certain level or, like most traders, you keep your fingers crossed and hope for the best … until the pain of losing on paper is greater than the fear of losing real money and you sell at a loss. In a recent survey, results showed three out of four options traders still trade this way. Accordingly, the same survey showed that three out of four options expired without being exercised or with any value. And yet, the traders who took the “sell” side of the trade put money in their pocket on Day One of their trades, every single time. Selling is a low-risk option strategy and a low-risk way to generate high monthly income. Here are several things to consider:

• When you sell an option, you are collecting the cash up-front. You are already ahead.

• When you sell an option, you are transferring risk to the buyer. Yes, when you sell options, you assume some risk but not to your capital.

The Income Investor’s Blueprint Page 14

• This cash you collect upfront gives you the ability to manage the position – you have

cash in hand to “close” or buy back the put or call, at a profit or loss, without using any or a good deal more capital. This enables you to conserve capital, the basis for regular monthly income.

• And accepting cash enables you to create targets for your positions, and voila! The sum of these targets, when set properly, gives you a target income for the month … and that is what this is all about.

The Benefits of Selling Options No approach to generating income comes close to the yield, protection of capital and long term viability as selling options to generate income.

Yield The return on capital for an income strategy using the sale of options at its core is many percentage points higher than the strategies highlighted above. In this strategy we target 1.5%-2.0% per month, 18%-24% per year and in given months go well past these targets. These are conservative targets – you're not aiming for pie-in-the-sky returns here: Remember the goal is to create income WITHOUT risk of losing capital.

Capital Risk When you sell a put or a covered call you are selling risk – buyers are taking the risk of a stock moving a certain way, you are selling buyers that risk with little or no risk of losing your capital. If you sell a covered call, your only risk is foregone profit if you sell a call with a strike price higher than the price you paid for the stock. If you sell a put and the stock moves down too much, you can always move the put to a later date, which commits your capital to supporting that position a bit longer, but there is no loss of capital. The proof is in the positions we'll share with you – of the more than 130 positions opened following this strategy, only one has lost money.

A Long Term Strategy The volume of puts and calls positions being opened and traded increases in double digits each month, month over month. Thousands of stocks and ETFs have options you

The Income Investor’s Blueprint Page 15

can sell and more than one hundred and fifty have weekly options you can sell and that number grows every week. The market – the traders, the robots – are trading more and more and buying more and more risk, creating a strategy you can learn, work with and improve not over a period of days or weeks but years.

The (Hidden, Shhh…) Benefits of Selling Options There are two other, somewhat hidden benefits of using an options selling strategy to generate income.

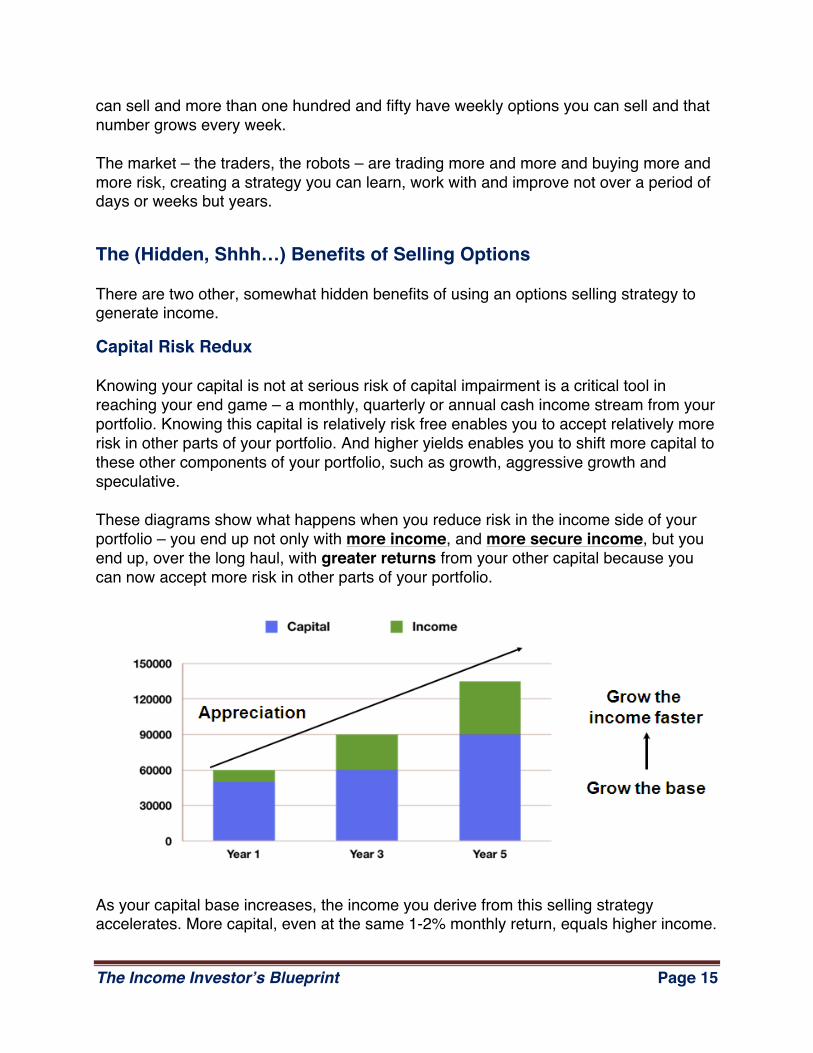

Capital Risk Redux Knowing your capital is not at serious risk of capital impairment is a critical tool in reaching your end game – a monthly, quarterly or annual cash income stream from your portfolio. Knowing this capital is relatively risk free enables you to accept relatively more risk in other parts of your portfolio. And higher yields enables you to shift more capital to these other components of your portfolio, such as growth, aggressive growth and speculative. These diagrams show what happens when you reduce risk in the income side of your portfolio – you end up not only with more income, and more secure income, but you end up, over the long haul, with greater returns from your other capital because you can now accept more risk in other parts of your portfolio.

As your capital base increases, the income you derive from this selling strategy accelerates. More capital, even at the same 1-2% monthly return, equals higher income.

The Income Investor’s Blueprint Page 16

Event Indifference, Market Neutrality The second hidden benefit of selling options is this strategy works in any market condition. You need no longer to worry about unseen political events or flash crashes. You do not have to sit out of the market when things are volatile, and trading goes haywire. For example, we saw some big down days not too long ago. If you had a put position open, you may have rolled the put into a later date but you did not lose capital. Better still, as the market hit the skids for a while, volatility increases and you can actually collect more cash on many of the new put positions you open. You see when you sell options during a period of increasing volatility; it is a good thing for options sellers. Volatility increases premium and time decay, creating shorter-term pay-offs and a boost in monthly returns up to 5%. And you need not worry if we are in bull, a bear or a flat market, short or long term. The options universe is now so large it supports – it encourages – selling options in any market condition. Are you willing to buy a high yielding stock in a falling market? Most people will not. So you sit and wait, and your monthly income pay-out shrinks. And how do you know when it’s safe to invest again in a high-yield stock that has dropped in a falling market? You simple don’t, until it’s already run-up again. With an option selling strategy this is no longer something you have to live-with. You don’t have to wait out the market or take what the market gives you. The best tool – and a favorite among those who adhere to this strategy – is the weekly option. You can sell weekly puts or calls. We sell weekly options every week creating income producing positions that take only 2 to 3 days to collect the cash. This cash almost feels like free money. Yes, the gains may be one half of one percent – but multiply that by fifty times and you have a return of 25% a year, more than two percent a month. That is for two and half days of exposure to the market each week.

Another Benefit of Selling Options (Covered Calls) Many investors artificially separate "core asset” and “trading accounts” and any actions remotely touching options is relegated to the trading account.

The Income Investor’s Blueprint Page 17

This is a big mistake that costs investors money every day. If you own gold, through the ETF the GLD, do you sell calls on it? You should. You can sell weeklies or monthlies and boost your yield to between 8% and 18% depending on how active you are. Do you own Apple at $100 and like to gloat around that special in-law everyone dislikes? If you are not selling calls – weeklies or monthlies – you are missing out on between 15% to 22% a year on Apple shares – the equivalent of a "personal dividend” from your Apple shares, even though Apple doesn't PAY a dividend. There are thousands and thousands of names with calls to be written. You probably own some of them. If you are not writing calls, right now, you are leaving money on the table.

The Double Dividend Position Many of you own high yield stocks – mortgage REITs yielding 13%, MLPs yielding 9% and so on. If you sell calls at the right time, you can come close to doubling that yield. Just take a look at the chart of one of the most owned mortgage REITS, Annaly Capital (NLY). Annaly Capital (NLY) is an income trader’s dream! The stock currently yields 13% -- that is not a misprint. NLY is a Real Estate Investment Trust (REIT) that actually buys insured mortgages with higher interest rates than it pays for its own capital. Simple and effective. You can trade NLY by selling puts or covered calls all day, all week, all month and all year long.

The Income Investor’s Blueprint Page 18

The ups and downs on a high yielding stock are very predictable – the stock goes up as it nears its ex-dividend date then sells off. So you sell a call a week or two before it goes ex-dividend and either buy it back or let it expire worthless after the stock goes ex-dividend. With NLY, you could add 9% or more to your current 13% dividend. Now imagine doing that once or twice a month, every month, and soon you’ll be on your way toward collecting cash in your account from trading options. Let’s Get Started Generating Real and Consistent Income Many investors are partially satisfied – some are completely satisfied –with their income streams. But if they are not selling options they are leaving a great deal of money on the table. Not next year or next month, today. It is not that other income strategies are wrong – they are incomplete or they simply cannot generate the cash and income required by an income investor. There is nothing wrong with Treasuries if you have twenty million dollars in the bank and can live on an income stream of forty thousand dollars.

The Income Investor’s Blueprint Page 19

There is nothing wrong with corporate bonds if you hold them to maturity, are not invested via ETFs or mutual funds, the company does not go bankrupt and you can put two million into bonds to generate just $100,000 in income. There is nothing wrong with annuities if you want to surrender control of your capital and know exactly what is going to happen in your economic life for the next twenty or thirty years. And there is nothing wrong with high yield stocks as long as you are 100% certain they will not go down. Selling options puts or covered calls is the only way you can really reduce risk to your capital and yet generate enough income to meet your expenses and even build towards a retirement dream. The Income Investor's Blueprint Plan—Step by Step Analysis Step 1: Generate “instant cash” in your account by Selling Puts Step 2: Create Your Own Dividend Machine with Covered Calls Step 3: Get paid for Building in Downside Protection Writing Covered Calls Step 4: Press your advantage by closing/rolling/expiring positions Step 1: Generate “instant cash” in your account by Selling Puts Selling puts is actually is a tool you can use to generate income in everything from a bear market to a flat market and bullish market. The advantage to SELLING puts or calls over BUYING calls or puts is evident in the math: The odds of winning are significantly increased to over 80% in your favor. Many professional traders use the short put strategy to buy stocks at prices they want. Nobody wants to pay Google or Apple prices to own shares, but when the stocks pull back – and stocks always pull back – the market helps you to get in at a better price. But what if you don’t want to buy the stock? Don’t sell puts on stocks you wouldn’t want in your portfolio. You will get taken out of the trade if the buyer wants to exercise their rights (to “put” stock to you at the option’s strike price), and those are the kind of stocks you probably want to own! This is always the risk with short puts, but it’s hard to call it a “downside” when you end up owning a good stock at a great price.

The Income Investor’s Blueprint Page 20

Besides, even if you are assigned to take possession of the shares, you can always sell them on the open market. In fact, you can often get out for a better price and, thus, a profit … and repeat the strategy, if you choose. Better yet, if the stock goes up and your put gets assigned, just sell a covered call against the shares and you’ve just established a new position in your portfolio -- and another way to profit! Become a Put Selling Pro That’s how you “save” a short put position that didn’t go the way you expected. But the odds are on your side that the puts will expire without value for the buyer and you will be out of the trade by expiration Friday with no further obligation other than to enjoy the money you made. The reason we want to sell the puts is for the premium collection, not to mention that we don’t have to own the underlying stock for the strategy to work. This is a great alternative to a strategy like covered calls, where you have a significant amount of capital tied up in the position at the outset, and the premium from the short calls pay you to wait for price movement. The Put Selling Strategy in Action Rules for Selling Puts:

1. Locate companies with good products/services, strong earnings, strong technicals and are otherwise fundamentally sound.

2. Look at the stock’s option chain and locate the strike price closest to where the stock is trading.

3. Tell your broker that you want to “sell to open” the at-the-money put options. (Pick an expiration date close to the date you’re initiating the position, such as 1 to 2 weeks or 1 to 2 months out.)

4. Don’t watch your “sold put” positions on your broker screen minute-by-minute or even day-by-day. Focus on the underlying stock price and its movement, not the option contract.

5. As you close in on the all important expiration date, if the underlying stock price is consistently staying above the strike price, you can let it ride to expire worthless (and you keep all of the cash you sold).

6. If you’re worried that it might fall in the last week or few days before expiration, close the position by buying back the contract and keep the cash difference.

7. Keep repeating the strategy for as long as it is working. 8. Remember: If the position is working, the put will expire worthless and you are out of the

trade. If the position turns against you (for example, if the stock drops by more than the premium you collected), you can buy back your puts at any time before assignment.

One thing option sellers should always keep in mind is that, while your trade is still active, you have absolutely no obligation to remain in it.

The Income Investor’s Blueprint Page 21

Step 2: Create your own DIVIDEND MACHINE Suppose you own Starbucks (SBUX) shares. They pay a dividend that would not give you enough cash to buy a latte (Grande, skim, extra foam please). You want income but you are a great believer in the long-term value in the stock. What do you do? Sell covered calls! A stock like Starbucks when used to support the sale of covered calls throughout the year can yield a more than 8% return on the capital you have invested in the stock. And if you manage your positions properly, you will probably not get called out of the stock – the buyer will not exercise the call option. Now is where your knowledge that about 80% of all option contracts expire worthless or unexercised comes in pretty handy. The ability to create your own dividend really resides in your “idea” about Starbucks. Let’s say you do not want to own the stock right now, as you would prefer to stay pretty liquid (pardon the pun). And you still love Starbucks. Instead of owning the shares and selling calls against them, you instead sell puts. Over and over again. No underlying shares needed. You may even yield more than that 8%, because you need 15%-20% less capital, on average, when selling puts. How it Works. You have always loved Starbucks (SBUX) the stock, and the coffee, but don’t feel that you need to own it. However, going into this position, you should be OK with owning the stock, because there is a chance it could be “put” to you by the option buyer. Let’s look at a sample timeline and strategy for selling, and managing, your SBUX put. April 13: The stock is at $35.84. You sell the SBUX May $35 Put; this is the price where you would gladly own the stock for a period of time. The put is trading for $1.06. You sell ten contracts, collecting $1,060 and tying up $35,000 in capital. April 29: The stock is moving on a movement down in coffee prices and an analyst upgrade. It hits $37.50, the yearly high. The put sinks to $0.35. You buy it back, spending $350 in cash. The net gain is $710. Then… April 29: You sell the SBUX July $35 put at $1.77. Five contracts or $17,500 in capital. Net cash in is $885. You put in a “Good until Canceled” order to buy the put back at $0.65, a cash outlay of $325.

The Income Investor’s Blueprint Page 22

June 24: The stock has not been able to punch through the $37.50 level but time decay has hit the option. With four weeks before expiration it has eroded in value to $0.65 and the order goes off. You spend $325 to close it out, and have a net cash gain of $560. Your total net cash gain on both SBUX trades, then, is $1,270. Whatever you do with that income is up to you, but we wouldn’t be surprised if you went out for a celebratory espresso drink first! Step 3: Get paid for Building in Downside Protection Writing Covered Calls With AT&T (T) at $30, the call option with the $30 strike is considered to be at-the-money. At-the-money options have the most “extrinsic value,” or amount of value that decays with time. This is a good thing (to quote Martha Stewart), because as the option seller, you are counting on the option losing value after you’ve made your trade. The takeaway here is that extrinsic value goes to zero on expiration day. That’s the money the option buyer unsuccessfully risked and that you’ve banked! The idea behind the covered call strategy, then, is to sell the option with the most amount of eroding value. That is why you don’t want to be in the position for too long, and it benefits you to use a stock that is stuck in neutral. Another tip: If your stock is at $28.50 and you have your choice between the $28 strike and the $29, it may be to your benefit to sell the out-of-the-money $29-strike calls. You will probably collect less money upfront (as of this writing, the $28s are at 50 cents and the $29s are at 10 cents), but the odds of the option expiring worthless are slightly improved. For my money, I’m more interested in the “reasonably sure thing” than the bigger-potential returns, especially if I’m counting on the returns as regular income. How it Works With AT&T, let’s say you own 500 shares, with a current value of $12,000. That’s a lot of money taking up space in your portfolio with hardly any return. To implement this trade, you’ll tell your broker that you want to “sell to open” 5 contracts of the at-the-money calls. Let’s use the $30s that expire in a few weeks, with a current value of $1.08. In other words: 500 shares @ $30 = 5 call contracts at the $30 strike. This means you collect $108 ($1.08 per share x 100 shares in a contract) per contract. Multiply that by 5 contracts, and you get $540 in your account (before commissions). That cash is yours to keep.

The Income Investor’s Blueprint Page 23

Do that over and over again every month while the stock stagnates, and you don’t have to worry about whether or not your boss is going to give you a raise or cut your holiday bonus this year. Note: A little bit of volatility gives a boost to option premiums. The at-the-money options for AT&T surged to 65 cents when the recent T-Mobile partnership announcement (aka, the “AT&T&T” news) hit the wires, before retreating to 50 cents just a couple days later. While the covered call strategy is one you will usually do independently of market events, it can also help you to take advantage of them. Protection under the ‘Cover’ One last tip: This strategy works best when it’s done repetitively. Don’t short longer-dated call options – you could collect more by selling month to month than shorting a more-expensive call that has more time till expiration. Another benefit to selling month-to-month (or week-to-week) is that you can easily adjust the strike price to mirror the stock if it moves. So, what if the stock does move? Covered calls aren’t for “movers and shakers.” You’re better off using your stocks that are trading in a range but that are slowly moving upward. If you’re not longer-term bullish on a stock, the covered call isn’t the right strategy for the situation. The great news is that the strategy is effective not only when the stock stands still, but also if it moves up a bit or even down a bit. Ultimately, you want the stock to go up. So if AT&T does add a few pennies between now and expiration Friday, you’re still in a good position. But if it takes off and runs, you risk having the call “assigned” and your shares being sold at the $28 strike. If that happens, you can buy the shares back at the market price, but you probably want to stay away from the covered call strategy with this stock, at least in the short term. If the stock falls, you’re “covered” up to the amount you collected from the call. If your stock drops to $27.40 and you collected 60 cents, you’ve broken even. Anything below $27.40, though, and the position is no longer hedged. And that’s how you generate 2% of your money. Step 4: Press Your Advantage by Rolling Closing/Rolling/Expiring Positions How it Works

The Income Investor’s Blueprint Page 24

Let’s say you have $25,000 to commit to generating income from the sale of options.

You decide to sell puts on the ETF for silver—the SLV that is priced around $39.50 right now. Why the SLV? Well, this ETF has been on a nice upward trend and, while it has flattened out lately, you still believe in a long-term bullish trend for silver prices. You’re willing to allocate up to $10,000 capital for this trade, but you will probably not need it. To implement this trade, you would execute an option trade at your online broker and “sell to open” 2 contracts of the in-the-money puts. Let’s use the $39s that expire next month, with a current value of $1.82 per share. Instead of a typical option trade where the broker takes the money out of your account to buy an option (call or put), you are selling 2 contracts and you collecting $364 in your account for making that sale ($1.82 per share x 100 shares in a contract x 2). That $364 of cash is yours to keep . . . for now. Assuming you silver prices don’t collapse overnight or you get put the SLV at the $39 price (which you don’t mind because you are long term bullish on silver prices), you can do one of two things. Wait it out. If the SLV moves higher, the $364 is yours to keep. Or, at some point before expiration, you could buy back those 2 contracts, and because time erodes the price for the buyer of your options, you would probably get a price of $0.75 to $0.80, and pay $150. You’ve still netted $225 in cash in your account. And you’re in and out of the trade in days -- at most, weeks. And it takes about 10 minutes of your time to execute. Now imagine doing that every month, generating $200 per option income trade, and maybe committing to 2 to 3 “put selling” trades each month. All of a sudden, you’re picking up an extra $400 to $600 in your account each month, and you still have your original $25,000 in capital protected. That’s a 28% return on your money, but you didn’t invest (or lose) any of your cash. Why Sell Options Now? All of these possibilities would have been limited or would not have been practical just a couple of years ago. Today, more than thousand “names” are suitable for trading options for income,

The Income Investor’s Blueprint Page 25

ranging from stocks to ETFs to indices. Online brokers have excellent tools not just to investigate positions, but to create them and manage them at very low transaction costs. Plus, trading itself has become much more efficient; you need not worry about whether a position is liquid enough to trade without dealing with overly large bid/ask spreads. And there are really cool options out there – you can play stocks, play banking as a segment, play commodities through ETFs, there are even options that you write weekly and expire weekly. (I sell covered calls on two longer-term positions every Wednesday afternoon). And, market stability has returned. Do not confuse the word “stability” with a market going up, though. Markets do not go up forever – don’t we all know this from personal experience? – And the selling of options is a terrific strategy in bear corrections, bear markets or a bearish move in an individual stock. Whether you are trading for income or some other goal such as capital appreciation, having the tools and the strategies ready for playing the downside is absolutely necessary for success. The Income Investor Blueprint Sounds too simple? You do need to know what to do to analyze a potential position, how to create price targets for closing a position, and what to do when you are called out, are put the stock or when you want to roll or extend a position. This is not hard to learn; it is even easier to execute. And your learning process, if you are really interested in income, will be very different from learning how to buy options. For example, a typical options service or course about buying options always tells you volatility and time decay are the enemies of the options trader. Wrong. They are the enemies of the options buyer. They are the friends – big-time friends – of the options seller. In any case, the market wants to pay you to trade, too. What you do with it is up to you – retire, travel, reduce your workload, buy a great bottle of Scotch (or an entire distillery!) – if you can commit to making 2% a month by selling options, your dreams can get bigger and bigger … right along with your account!

The Income Investor’s Blueprint Page 26

Traders Reserve Copyright All material in this report is, unless otherwise stated, the property of Traders Reserve, LLC. Copyright and other intellectual property laws protect these materials. Reproduction or retransmission of the materials, in whole or in part, in any manner, without the prior written consent of the copyright holder, is a violation of copyright law. A single copy of the materials available through this course may be made, solely for personal, noncommercial use. Individuals must preserve any copyright or other notices contained in or associated with them. Users may not distribute such copies to others, whether or not in electronic form, whether or not for a charge or other consideration, without prior written consent of the copyright holder of the materials. Contact information for requests for permission to reproduce or distribute materials available through this report is listed below:

www.tradersreserve.com [email protected]