The Impact of Venture Capital Investments on Industry Performance Tim Loughran Sophie Shive...

34

The Impact of Venture Capital Investments on Industry Performance Tim Loughran Sophie Shive University of Notre Dame

-

date post

20-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of The Impact of Venture Capital Investments on Industry Performance Tim Loughran Sophie Shive...

The Impact of Venture Capital Investments on Industry

Performance

Tim Loughran

Sophie Shive

University of Notre Dame

Venture Capital – Background

• From 1980-2005, VC funding totaled $394.2 billion.

• 500 VC funds concentrated in CA, MA and a few other states.

• Raise funds from wealthy individuals, pension funds and endowments and invest it in new companies.

• Began just after WW II, but took off in 1979 when “prudent man” rule allowed pensions to invest.

Venture Capital - Background

• VCs provide both cash and expertise to young firms, and then plan their exit

• 20-35% of VC-funded firms are taken public – bulk of VC’s returns are here (Gompers and Lerner, 2002).

• Brau, Francis, and Kohers (2003) find that IPOs get a 22% premium over the average price paid for privately-held firms.

• Apple Computer, Sun Microsystems, Yahoo, eBay, and Google were all VC funded firms.

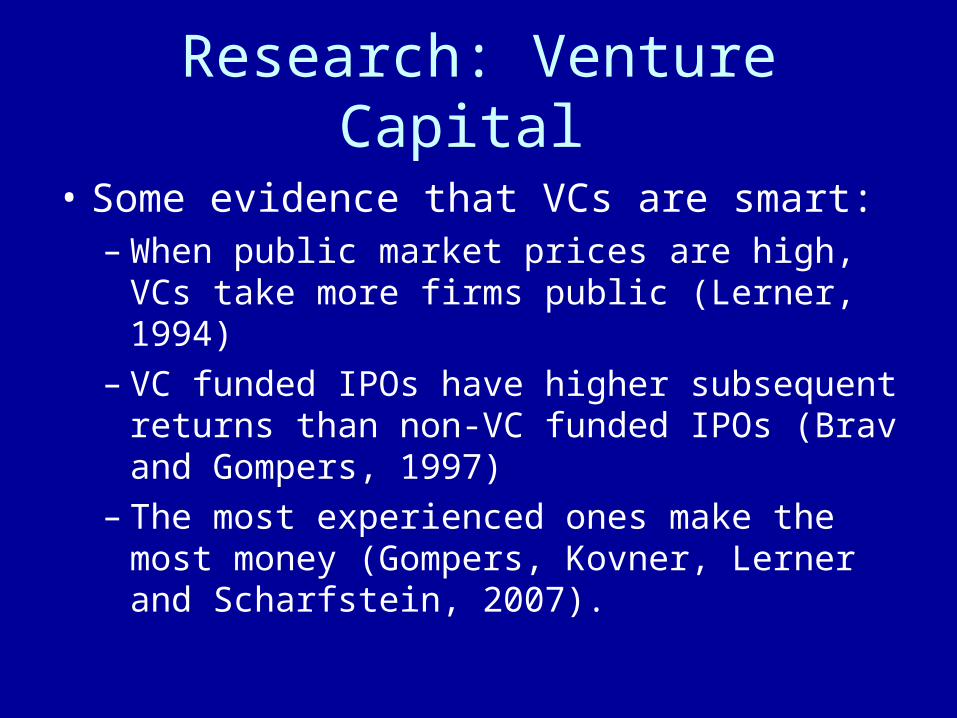

Research: Venture Capital

• Some evidence that VCs are smart: – When public market prices are high, VCs take

more firms public (Lerner, 1994)– VC funded IPOs have higher subsequent

returns than non-VC funded IPOs (Brav and Gompers, 1997)

– The most experienced ones make the most money (Gompers, Kovner, Lerner and Scharfstein, 2007).

Research: Industry Returns

• Less competitive industries earn lower returns (Hou and Robinson, 2006)

• The market reacts slowly to information contained in some industries (Hong, Torous and Valkanov, 2007)

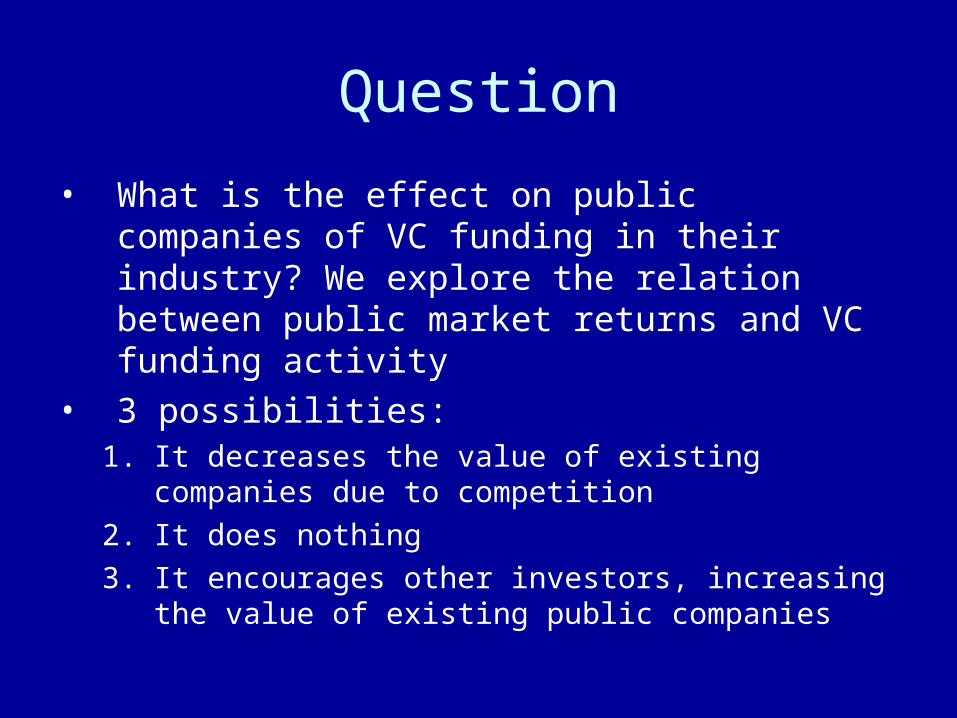

Question

• What is the effect on public companies of VC funding in their industry? We explore the relation between public market returns and VC funding activity

• 3 possibilities: 1. It decreases the value of existing companies due to

competition

2. It does nothing

3. It encourages other investors, increasing the value of existing public companies

Summary of Findings

• In an panel of 3,502 quarterly industry observations, more VC funding is related to lower subsequent industry returns

• VC funding is negatively related to industry ROA in the subsequent year.

• Our results are generally significant for both the EW and VW returns.

• Also true for both the bubble and non-bubble periods.

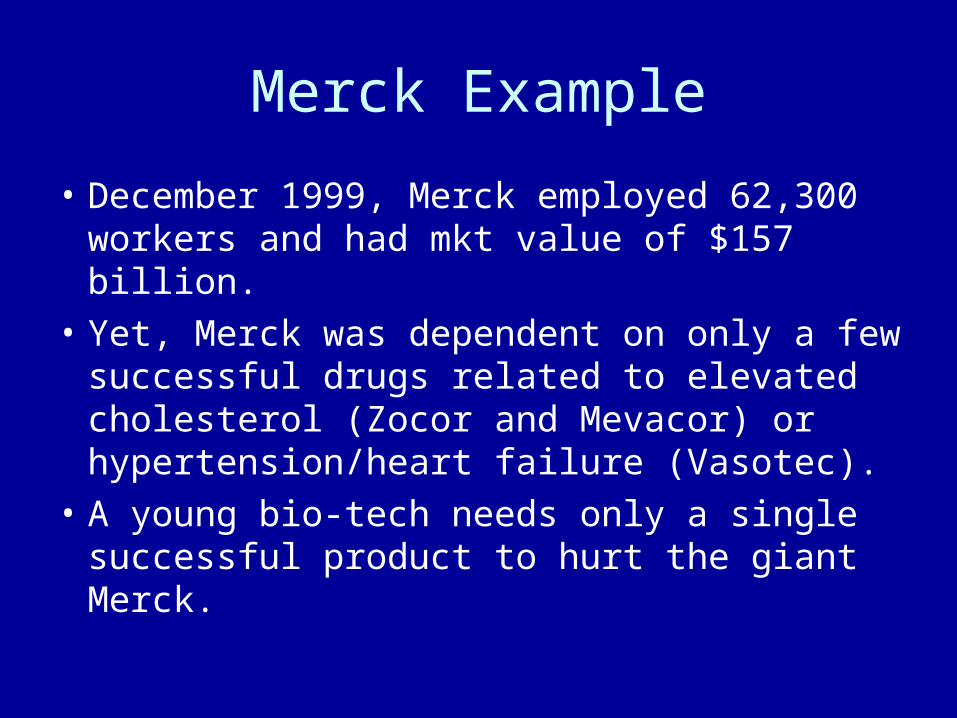

Merck Example

• December 1999, Merck employed 62,300 workers and had mkt value of $157 billion.

• Yet, Merck was dependent on only a few successful drugs related to elevated cholesterol (Zocor and Mevacor) or hypertension/heart failure (Vasotec).

• A young bio-tech needs only a single successful product to hurt the giant Merck.

Yahoo/Google Example

• In our dataset, Google received two rounds of VC money: June 4, 1999 “other early stage” infusion of $25 million and September 1, 2000 “expansion” infusion of $15.175 million.

• Yahoo was more established than Google, and it also had older technology.

Market Values

• Yahoo had mkt value of $67 billion when Google received “expansion” money.

• In August of 2004 (Google’s IPO date), Yahoo had $42 billion value.

• By September 2007, Yahoo had $30 billion market value (Google is now $164 billion).

Outline of talk

• Data

• Methodology

• Main results

• Robustness

• Industry Return on Assets

• Conclusion

Data

• Venture capital (VC) data is from Thomson’s VentureXpert database: – Data is self-reported by the VCs or the

companies they invest in– all VC disbursements between 1980 and

2005. – Re-code industries into Fama-French 48: 34

industries have at least one round of funding.

• Other sources: Ken French’s website, CRSP, Compustat

Fig 1: Quarterly level of Nasdaq and VC disbursements

01

02

03

0L

eve

l of V

C F

un

din

g in

Bill

ion

s$

02

00

04

00

06

00

0N

asd

aq

Le

vel

1980 1985 1990 1995 2000 2005

Nasdaq VC Funding

Fig 2: Quarterly level of Nasdaq and VC disbursements scaled by assets

0.5

11

.5V

C F

un

din

g/T

ota

l A

sse

ts, %

02

00

04

00

06

00

0N

asd

aq

Le

ve

l

1980 1985 1990 1995 2000 2005

Nasdaq VC Funding/Total Assets

Types of VC Funding

• Early Stage– Seed (1.9% of total funding)– Startup (17.2%)– Other Early Stage (6.9%)

• Expansion (57.3%)

• Later Stage (16.8%)

• We exclude Other Stage (Acquisitions, Special Situation, VC Partnership)

Data

• Over 83% of total VC funding goes to five industries: – Business Services: 37.3%– Telecommunications: 24.4%– Pharmaceutical Products: 9.2%– Computers: 6.6%– Chips and Electronic Equipment: 5.7%

Fig. 3. VC Disbursements for the Five Most-Funded Industries, 1980-20050

.2.4

.6P

ropo

rtio

n o

f T

ota

l Fu

nd

ing

1980 1985 1990 1995 2000 2005Year

BusSv TelcmDrugs CompsChips

Data• Other variables:

– Value and equal weighted industry returns and book/market from Ken French’s website

– Log (Number of IPOs + 1) from SDC– Herfindahl Index of sales from Compustat:

Sum of squares of firm sales

(Total industry sales)2

A high value means low competition

Hou and Robinson (2006) show H is related to returns

H =

Table 2: Summary Statistics by Industry and Quarter

Variable N Mean Min Max Median

VC Dollars (M)

3,502 110.1 0

15,174 7.3

VC Dollars/Assets

3,502 0.21% 0.00% 45.38% 0.01%

VW - Industry Return

3,502 3.8% -42.2% 68.6% 4.1%

EW - Industry Return

3,502 4.1% -41.8% 78.8% 3.5%

VW - Book/Market

3,502 0.58 0.09 1.81 0.51

EW - Book/Market

3,502 0.54 0.08 1.74 0.47

Log(NIPOs+1)

3,502 0.28 0 3.43 0

Herfindahl Index

3,502 0.14 0.01 0.73 0.10

Methodology

• Regression with quarterly and industry fixed effects and errors clustered by quarter and industry (Petersen, 2007, Thompson, 2006).

Table 3: Industry Fixed Effects Regressions

VC/A B/M Ret-1 Ret-2 IPO Herf Mkt-Rf SMB HML MOM I Q

VWRaw

-33.10 Y Y

(-4.92)

-30.90 3.86 0.07 0.05 -0.08 3.24 Y Y

(-5.64) (2.46) (1.72) (1.43) (-0.15) (1.29)

VWExcess

-22.22 4.54 0.04 0.01 -0.50 2.43 0.95 0.14 0.13 2.67 Y N

(-6.25) (6.57) (1.97) (0.26) (-1.02) (0.84) (25.55) (2.07) (1.77) (0.51)

EWRaw

-36.00 Y Y

(-4.01)

-34.09 -1.03 0.17 0.00 -0.34 1.64 Y Y

(-4.55) (-0.54) (3.19) (0.11) (-0.82) (0.57)

EWExcess

-27.64 1.03 0.09 -0.01 -0.65 1.08 0.88 1.03 0.28 6.42 Y N

(-4.39) (0.77) (3.30) (-0.68) (-1.45) (0.33) (16.12) (7.67) (2.54) (0.95)

N ranges from 3,468 to 3,502, R-Square ranges from 0.52 to 0.65

VC/A is the VC funding for each industry-quarter divided by total industry assets

Mkt-Rf, SMB, HML, MOM are contemporaneous; remaining variables are lagged.

Ind and Time are industry and quarter dummy variables.

T-statistics in parentheses; Standard errors clustered by quarter and industry.

Comments

• VC/Assets consistently significant

• IPOs and Herfindahl are generally not significant

• Are our results due to a certain time period, like the internet bubble period of 1998-2001?

Table 4: Time-period Break-down

VC/A is the VC funding for each industry-quarter divided by total industry assets

Industry and quarterly dummies are included

T-statistics in parentheses; Standard errors clustered by quarter and industry.

VC/A B/M Ret-1 Ret-2 IPO Herf N R2

VW Returns

All -30.90 3.86 0.07 0.05 -0.08 3.24 3,468 0.56

(-5.64) (2.46) (1.72) (1.43) (-0.15) (1.29)

NB -97.10 2.66 0.05 0.04 0.03 2.89 2,924 0.61

(-4.85) (1.99) (1.81) (1.12) (0.08) (1.01)

B -68.21 11.68 0.08 0.02 -0.59 5.26 544 0.48

(-10.23) (1.55) (0.74) (0.19) (-0.25) (0.50)

EW Returns

All -34.09 -1.03 0.17 0.00 -0.34 1.64 3,468 0.65

(-4.55) (-0.54) (3.19) (0.11) (-0.82) (0.57)

NB -97.55 -2.62 0.11 0.00 -0.19 2.14 2,924 0.70

(-2.00) (-1.90) (3.47) (0.00) (-0.43) (0.65)

B -73.59 9.40 0.27 -0.01 -2.10 -8.99 544 0.56

(-9.09) (0.71) (2.02) (-0.10) (-0.99) (-0.68)

Table 5: Funding Stage Break-down

VC/A B/M Ret-1 Ret-2 IPO Herf I&Q N R2

VW Returns

Seed -496.00 3.87 0.08 0.05 -0.08 3.27 Yes 3,468 0.56

(-1.47) (2.48) (1.74) (1.42) (-0.16) (1.31)

Startup -137.00 3.86 0.07 0.05 -0.08 3.26 Yes 3,468 0.56

(-5.12) (2.46) (1.73) (1.46) (-0.16) (1.30)

OtherEarly -402.00 3.84 0.07 0.05 -0.08 3.23 Yes 3,468 0.56

(-4.72) (2.47) (1.73) (1.43) (-0.15) (1.29)

Expansion -53.94 3.86 0.07 0.05 -0.08 3.24 Yes 3,468 0.56

(-5.87) (2.47) (1.72) (1.43) (-0.15) (1.29)

Later -212.00 3.89 0.07 0.05 -0.07 3.22 Yes 3,468 0.56

(-5.80) (2.46) (1.73) (1.42) (-0.14) (0.74)

EW Returns

Seed -1230.00 -1.04 0.17 0.00 -0.35 1.61 Yes 3,468 0.65

(-2.79) (-0.55) (3.20) (0.07) (-0.83) (0.55)

Startup -158.00 -1.03 0.17 0.01 -0.35 1.66 Yes 3,468 0.65

(-5.22) (-0.55) (3.18) (0.12) (-0.83) (0.57)

OtherEarly -411.00 -1.04 0.17 0.00 -0.34 1.64 Yes 3,468 0.65

(-4.17) (-0.55) (3.19) (0.10) (-0.82) (0.57)

Expansion -57.91 -1.03 0.17 0.00 -0.34 1.65 Yes 3,468 0.65

(-4.06) (-0.54) (3.18) (0.11) (-0.82) (0.57)

Later -221.00 -0.99 0.17 0.00 -0.33 1.63 Yes 3,468 0.65

(-5.23) (-0.52) (3.20) (0.09) (-0.80) (0.57)

Table 6: Industry Break-down

VC/A B/M Ret-1 Ret-2 IPO Herf N R2

VW Returns

Business -51.2 -5.81 -0.04 -0.06 -3.30 -30.32 102 0.08

Services (-2.55) (-0.36) (-0.38) (-0.59) (-0.88) (-0.66)

Telecom -1391.1 -0.91 -0.08 0.10 -5.33 -442.52 102 0.22

(-2.74) (-0.39) (-0.85) (0.84) (-2.03) (-1.88)

Drugs -1538.0 -4.10 -0.01 0.05 -2.66 -3.71 102 0.09

(-1.11) (-0.46) (-0.07) (0.54) (-1.62) (-0.06)

Computers -1412.7 13.02 0.04 0.11 -0.96 -591.67 102 0.05

(-1.70) (1.17) (0.27) (0.78) (-0.46) (-1.55)

Chips -9462.5 11.13 0.01 0.03 -1.06 -147.77 102 0.21

(-5.40) (0.78) (0.09) (0.27) (-0.48) (-2.32)

EW Returns

Business -44.3 -6.50 0.00 -0.06 -3.72 -13.13 102 0.04

Services (-1.59) (-0.33) (0.01) (-0.57) (-0.87) (-0.25)

Telecom -2246.0 -5.32 0.03 -0.00 -7.56 -202.84 102 0.10

(-2.00) (-1.27) (0.32) (-0.04) (-1.85) (-0.38)

Drugs -5786.3 -32.89 0.08 0.10 -6.40 196.86 102 0.11

(-3.03) (-1.70) (0.81) (0.95) (-2.15) (1.71)

Computers -1881.0 1.45 0.03 -0.05 -2.79 -448.87 102 0.05

(-1.76) (0.10) (0.29) (-0.43) (-0.97) (-0.95)

Chips -8310.3 3.62 0.01 0.07 -2.36 -137.73 102 0.10

(-3.35) (0.20) (0.09) (0.64) (-0.74) (-1.77)

Some Robustness Checks

• Including industries with zero funding

• Including “other stages”

• Other control variables: industry size, dividend yield, IPO initial returns, additional lags of the number of IPOs, equity share in new issues (Baker & Wurgler, 2000)

More Robustness: Redefining Industries

• Same analysis for “Tech” industry as defined by Loughran and Ritter (2004).

• Consistent significance at 1% level for EW and VW returns

Industry Operating Performance

• Does VC funding affect the subsequent year’s ROA for firms that are already public?

• Poor stock returns and poor operating performance for the same industry should be expected to go together.

• We compute ROA as Industry net income before extraordinary items from Compustat divided by total assets.

• We include Capex to assets and R&D to assets ratios.

• Also include industry and yearly dummies, and errors are clustered by both industry and year.

Table 7: Return on Assets

VC/ACAPEX/

A R&D/A Const I Y N R2

-38.43 0.04 No No 850 0.00

(-3.52) (8.78)

-28.47 0.03 Yes Yes 850 0.47

(-7.94) (8.06)

-25.41 0.11 0.20 0.01 Yes Yes 850 0.47

(-5.59) (1.64) (0.91) (2.10)

Dependent variable is industry-level return on assets: Net Income Before Extraordinary Items/Assets. Independent variables lagged one year.I and Y are industry and annual dummiesT-statistics are in parentheses; standard errors are clustered by industry and year

Conclusion

• Findings– Higher VC funding is associated with lower industry

returns in the subsequent quarter during 1980-2005.– True for equal and value weighted returns– Remains true in or out of the bubble. – True for most funding types and most of the 5 main

industries. – VC funding is negatively related to industry ROA in

the subsequent year.

Conclusion

• Our empirical results are consistent with the capital market myopia work of Sahlman and Stevenson (1985).

• Overoptimism on the part of venture capitalists leads directly to overfunding of a few key industries which precedes a decline in both industry stock returns and operating performance.

• Questions?