The Impact of the Consolidation of the Banking Sector … 2...The Impact of the Consolidation of the...

15

© 2015Research Academy of Social Sciences http://www.rassweb.com 8 International Journal of Financial Economics Vol. 4, No. 1, 2015, 8-22 The Impact of the Consolidation of the Banking Sector on Nigeria Economy Emernini Fabian 1 , Ugwoke Theophilus Ifeanyi 2 Abstract This paper examines the impact of the Consolidation of the Banking Sector on Nigeria Economy specifically the 2005 CBN Consolidation of Banks which increased the minimum capital base from N2 billion to N25 billion. A well developed and vibrant banking Sector is the bedrock of the development of any economy. The rationale for this Consolidation became evident following the failure of many banks to meet up their statutory requirement and obligations as the agent of financial stability and economic development of the country. This study using primary data (questionnaires) and Secondary data investigates the impact of the recent banking Sector Consolidation in Nigeria economy. Five among the banks that were fully involved in the mergers and acquisitions were investigated. When the data obtained from the five banks were analyzed, it was found that the banking Sector Consolidation impacted positively and significantly on the economy of Nigeria. 1. Introduction The banking system plays a fundamental and paramount role in the growth and development of any economy. Financial Systems have long been recognized to play an important role globally in economic development. In fact, the health of the banking system of a nation determines the well-being of the economy (Osaze 2000). This recognition dates back to 1950s, for instance, researchers like Goldsmith (1955), Mickinnon (1973) and Shaw (1973), have demonstrated that financial system could be a catalyst of economic growth and sustainable development if it is well harnessed and developed. Greenwood and Jovanovic (1990) observe that well-functioning financial systems are able to mobilize household savings, allocate resources efficiently, induce liquidity and provide other alternatives of raising funds through individual savings and retained earnings. The Nigeria banking sector has undergone remarkable changes since 1892, when the African Banking Corporation (ABC) was set up to today‟s era of Consolidation. Since inception, the changes in the banking industry have been influenced by the need for a sound banking industry, globalization of operations, technological innovation and adoption of supervisory and prudential requirements that conform to international standards. Soludo (2004) opines that the primary objective of the banking sector reforms is to guarantee an efficient and sound financial system. The reforms are therefore designed to enable the banking system to develop the required flexibility to support the economic development of the nation by efficiently performing its functions as the pivot of financial intermediation. Lemo (2005) observes that the banking Sector reforms were to ensure a diversified, strong and reliable banking industry where there is safety of depositors money and position banks to play active developmental roles in the Nigerian economy for a more meaningful economic development. Availability of capital plays a pivotal role and this capital is made accessible by a well-functioning and developed banking system. 1 Lecturer, Dept. of Economics Imo State University, Owerri Nigeria 2 Lecturer, Dept. of Economics Madonna University, Nigeria

Transcript of The Impact of the Consolidation of the Banking Sector … 2...The Impact of the Consolidation of the...

© 2015Research Academy of Social Sciences

http://www.rassweb.com 8

International Journal of Financial Economics

Vol. 4, No. 1, 2015, 8-22

The Impact of the Consolidation of the Banking Sector on Nigeria

Economy

Emernini Fabian1, Ugwoke Theophilus Ifeanyi

2

Abstract

This paper examines the impact of the Consolidation of the Banking Sector on Nigeria Economy

specifically the 2005 CBN Consolidation of Banks which increased the minimum capital base from N2

billion to N25 billion. A well developed and vibrant banking Sector is the bedrock of the development of

any economy. The rationale for this Consolidation became evident following the failure of many banks to

meet up their statutory requirement and obligations as the agent of financial stability and economic

development of the country. This study using primary data (questionnaires) and Secondary data

investigates the impact of the recent banking Sector Consolidation in Nigeria economy. Five among the

banks that were fully involved in the mergers and acquisitions were investigated. When the data obtained

from the five banks were analyzed, it was found that the banking Sector Consolidation impacted positively

and significantly on the economy of Nigeria.

1. Introduction

The banking system plays a fundamental and paramount role in the growth and development of any

economy. Financial Systems have long been recognized to play an important role globally in economic

development. In fact, the health of the banking system of a nation determines the well-being of the

economy (Osaze 2000). This recognition dates back to 1950s, for instance, researchers like Goldsmith

(1955), Mickinnon (1973) and Shaw (1973), have demonstrated that financial system could be a catalyst of

economic growth and sustainable development if it is well harnessed and developed. Greenwood and

Jovanovic (1990) observe that well-functioning financial systems are able to mobilize household savings,

allocate resources efficiently, induce liquidity and provide other alternatives of raising funds through

individual savings and retained earnings.

The Nigeria banking sector has undergone remarkable changes since 1892, when the African Banking

Corporation (ABC) was set up to today‟s era of Consolidation. Since inception, the changes in the banking

industry have been influenced by the need for a sound banking industry, globalization of operations,

technological innovation and adoption of supervisory and prudential requirements that conform to

international standards.

Soludo (2004) opines that the primary objective of the banking sector reforms is to guarantee an

efficient and sound financial system. The reforms are therefore designed to enable the banking system to

develop the required flexibility to support the economic development of the nation by efficiently

performing its functions as the pivot of financial intermediation. Lemo (2005) observes that the banking

Sector reforms were to ensure a diversified, strong and reliable banking industry where there is safety of

depositors money and position banks to play active developmental roles in the Nigerian economy for a

more meaningful economic development. Availability of capital plays a pivotal role and this capital is

made accessible by a well-functioning and developed banking system.

1Lecturer, Dept. of Economics Imo State University, Owerri Nigeria

2Lecturer, Dept. of Economics Madonna University, Nigeria

International Journal of Financial Economics

9

The major reasons which led to the reform programme in the banking Sector were due to the weak

Capital base of the banks, weak corporate governance, gross insider abuse, sharp practices, overdependence

on Public Sector deposits and insolvency. One may wonder why all these weaknesses on the part of most

banks. It is nothing but majorly due to relaxation by the supervisory authorities of the entry conditions,

Sectoral Credit allocation quotas and interest rate regulation which brought about many undeserving

players into the industry. According to Oyejide (1993) these relaxed measures brought about increase in the

number of banks from 42 in 1986 to 107 in 1990, and by 1992 it had reached 120. Oyejide opined that the

sharp increase in the number of banks without a correspondingly large increase in the capacity of the

regulatory and supervising mechanizing caused both off-site surveillance and on-site examination of banks

to suffer.

Lewis and Stein (1997) observed that rather than mobilizing and allocating resources to needy sectors,

disintermediation was the order of the day as many of the new banks, commonly referred to as new

generation banks, preferred to make money through arbitrage and other rent-seeking activities. Also, many

of the banks owned by local investors were seen to have been set up primarily in other for their owners to

obtain foreign exchange which could be sold at premium, Brownbridge (1996). The banks that were owned

by state governments 25 as of 1989, accumulated bad debts because of the extension of proprietary loans to

the state governments and to politically influential borrowers Brownbridge (1996).Hesse (2007), observed

that following the promulgation of the Banking and other Financial Institutions Decree (BOFID) and some

prudential guidelines, by 2004, 24 existing banks were found insolvent and were liquidated bringing the

number to 89.

Soludo (2006), despite government interventions, the surviving 89 banks were characterized by low

capital base, insolvency and illiquidity, overdependence on public sector deposits and foreign exchange

trading, poor asset quality and weak corporate governance.

The main objective of this paper is to determine the impact of the Consolidation of the banking sector

on the performance of Nigeria economy. This will assess whether the banking sector Consolidation has

made any positive impact towards the improvement of Nigeria economy after the consolidation exercise. In

assessing this, the paper will look at how far has it affected the Capital flow effect, the manufacturing

Sector, the effect on Capital market, total loans and advances of banks. Conversely, has bank Consolidation

impacted negatively to the growth of the economy.

The paper is divided into five sections. First is the abstract and the introduction, Section two is the

review of past research literature on bank Consolidation in Nigeria and other countries‟ experiences. The

third section is on the methodology, the fourth and fifth is the findings, recommendations and conclusion

respectively.

2. Literature Review

In developing countries, particularly in sub-sahara Africa, financial markets are dominated by

commercial banks, which have not been reliable sources of long-term financing. The non-bank sources of

medium and long term financing are generally underdeveloped. The short-term nature of commercial

banks‟ assets and liabilities as well as regulatory reserve requirements in many countries render them

(banks) incapable of supplying long-term capital Edward, (2004). Sanusi (2009) views economic

development as a tool to enhance productive capacity of an economy using available resources to reduce

risks, remove impediments which otherwise could lower costs and hinder investment. The banking Sector

plays the important role of promoting economic growth and development through the process of financial

intermediation. Unfortunately, the sector is yet to actualize this goal due to insufficient capital base.

He indicated that many economists have acknowledged that the financial system, with banks as its

major component, provide linkages for different sectors of the economy and encourage high level of

specialization expertise, economies of scale and a conducive environment for the implementation of

various economic policies of Government intended to achieve noninflationary growth, exchange rate

E. Fabian & U. T. Ifeanyi

10

stability, balance of payments equilibrium and high levels of employment. Reforms generally serve as new

initiative to inject into the existing system an improved and modern ingenuity that would bring in fresh life,

so that the system can conform to the challenges of the present, and enhance the future performance. Berger

Allen (1998) views reform as a technological innovation motivated and designed to enhance intermediation

and general performance for a competitive place in the global standard stability and growth.

Studies by Mckinnon (1973) and Shaw (1973) show that financial repression is correlated with

sluggish growth in developing countries. Such economies, according to Nnanna and Dogo (1998) are

typically characterized by high and volatile inflation and distorted interest and exchange rate structures, low

savings and investments and low level of financial intermediation. Various studies investigated the

relationship between financial system structure and development and the level of economic growth in

Nigeria. These studies include that of Ayadi et al (2007) and that of Ndebbio (2004). The studies relied on

money market indicators and established a positive and significant relationship between financial

development and economic development.

Another view by Banerjee (2009) asserts that there are possibilities of too little risk taking when banks

are not nearly that big. Small banks may be unable to supply risk capital and that the stock market in

principle could directly fund large firms to reach a global scale and by enabling a venture capital model of

funding high risk new ideas. However, he argues that though there are regulatory challenges, increase size,

make the stock market more efficient and daunting. This view goes with the financial sector reforms that

had taken place in banks and the capital market in Nigeria. While Schoar (2009) agrees that a competitive

banking sector is necessary in facilitating firm growth and competition, he argues that equity markets

constitute only a small portion of overall financing in developing countries. She underscores that scale was

important for banks, and tiny banks will not garner sufficient capital to finance small businesses for

expansion. In particular, the banking sector should be established and tailored to improve the real economy

and, as a tool to create jobs and other opportunities.

Asedionlen (2004) opines that recapitalization as a matter of fact may raise liquidity in short term but

will not guaranty a conductivity macroeconomic environment required to ensure high asset quality and

good profitability. India banks recapitalization period was necessitated with the review of Basle accord III

compliance which made the banks to shore-up their capital adequacy ratios and maintain it at 7% of risk

weighted asset which should be met by 2014. This process has mandated the Indian government to equity

stake holding of 59.4% in each bank. This when compared to the process of recapitalization in Nigeria is

totally different, since the pre-requisites of the process is government withdrawal of its funds from the

banks. The need to outline the importance of the market is necessary since the market played a significant

role in sourcing funding and working out the consolidation exercise.

Researchers like Levine and Zervos (1996), Nyong (1997), Barlet (2000),Ewah, Esang, and Bassey

(2009) have shown interest to observe on the stock market performance and economic growth. Capital

market offers a variety of financial instruments that enable economic agents to pool, price and exchange

risk. Through assets with attractive yields, liquidity and risk characteristics, it encourages saving in

financial form. This is very essential for government and other institutions in need of long term funds

(Nwankwo, 1991). The banking sector consolidation took place under the platform of the Nigeria Capital

market via the Stock Market.

The link between the banks and the stock market has a long history of economic relationships. Al-Faki

(2006), views the capital market as a network of specialized financial institutions, that includes series of

mechanism, processes and infrastructure which in various ways facilitate and bring together suppliers and

users of medium to long term capital for investment in economic development projects. Several attempts

have been made by previous writers to link the growth of the capital market with the economy. Both

subsectors had been explored by many researchers on their viability to promote economic growth. Amongst

them who believed that there is a positive relationship that the stock market enhances economic growth

include such views like that of Levine and Zervos (1996) who found a strong relationship between stock

market and economic growth. AlosBarlet (2000) found out that a rising stock price increases the wealth of

International Journal of Financial Economics

11

the economy through the increase in the consumers‟ consumption and increase in investment. This

demonstrated part of the recapitalization exercise in Nigeria as the stock market had more interested

participants.

Levine (1991) argues that developed stock market reduces both liquidity shock and productivity shock

of businessmen to investment funds as well as enhancing the production capacity of the economy, thereby

leading to higher economic growth. This view was supported by king and Levin (1993) that financial

development fosters economic growth.

Cameron (1967) and Mckimon (1973) in their separate studies on Bank consolidation, provide a

linkage between banks‟ financial market and the microeconomics. The argument of these studies is that

there is a symbiotic relationship between financial market and economic growth, noting that a well

developed financial market is a “Sine qua non” for the growth and development of less developed

economies. On the banking sector and holistic economic growth of a nation, Kings and Levine (1993) have

established that the banking sector development is not only a correlation with economic growth, but it is

also a cause of long term growth.

Further works building on the King and Levine thesis were those of Fermandez and Caletoric (1995)

who opined that a strong and stable financial system arising from financial sector consolidation could

impact positively on real economic performance by affecting the composition of savings and influencing

the scope for credit rationing.

Positive Impacts of the Bank Consolidation

Consolidation brought about increased number of shareholders and also increased number of

depositors.

According to 2007 CBN Quarterly Report, the number of shareholders of few selected banks increased

from 4,655,591 in 2004 to 8,258,285 in 2007 representing an increase of 77.3%.

S/N Year No. Of Shareholders Percentage Increase

1 2004 4,655,591 -

2 2007 8,258,285 77.38%

CBN quarterly report, November, 2007.

This increase in the number of shareholders in the banking industry is a clear indication of the growing

investment culture and considerable growth of the sector.

The of number of depositors increased from 17,662 in 2005 to 24,251 in 2007 representing percentage

increase from 29.40% to 37.31%.

S/N Year No. Of Depositors Percentage Increase

1 2005 17,662 29.40%

2 2007 24,251 37.31%

Source: (ChukwumaSoludo, Banks and the National Economy, Progress, Challenges

and the Road Ahead. CBN Quarterly report, 2007. P.22)

The above table which showed a significant increase in the number of depositors is a positive

indication of a restored confidence in the banking industry that was lost in the days of uncertainty and pre-

consolidation era. The increase in number of depositors resulted in the phenomenal growth of the banks

deposit funds from N1,409b in 2003 to N5,358b in 2007 (CBN Quarterly Report, 2007).

Banks Consolidation and Employment Generation

It has been argued that consolidation has led to reduction in employment opportunities. Reduction in

the number of employment is seen as the strongest critics of the impact of consolidation on the economy.

E. Fabian & U. T. Ifeanyi

12

However, with the unfolding of events it has been observed that bank consolidation eventually brought

about increased employment generation. The Nigeria Banking Sector before the December 31st, 2005

consolidation deadline, had a total of 40, 000 skilled workforce of this number, 15,000 were laid off in the

14 banks that could not survive the consolidation mergers and acquisitions with only 25 banks out of a total

of 89 banks coming out successfully; (CBN fourth Annual Monetary Policy Conference, 2004 pg64).

As the 25 successful Mega banks went into aggressive bank network by opening many braches, over

26, 000 new jobs were created exceeding the 15, 000 retrenched. There is also a positive spill-over of

massive job creation in the brokerage firms, insurance companies and other financial institutions operating

within the financial sector. (CBN Quarterly report, 2007).

Innovative Customer Service Delivery

One of the objectives of banking Sector Consolidation is to reduce the risk of Cash carrying system.

Before the Consolidation, large volume of cash had been lost to arm robbery and other risks associated with

cash carrying system. For example, in 2005 alone, Nigeria Commercial banks lost over N1.2b to moving

cash, (The Bullion, vol. 2, 2006, pg 22). This is different from losses to armed robbers by individuals and

cooperate organizations. One trend that has put a check to this ugly trend is the success of the consolidation

of the banking sector which is drawing the economy towards a cashless system.

Many banks have launched a lot of innovative technological and ICT driven packages which reduces

greatly the issue of cash carrying. For example the “Flash Me Cash” package by the First City Monument

Bank plc (FCMB), a system by which a person can make withdrawals by mere phone calls reduces

drastically the risk of carrying cash. According to Iku (2014), to get more people interested in using the e-

payment platform, the Nigerian Inter-Bank Settlement System (NIBSS) is encouraging the use of cards to

pay for goods and services via Point of Sale (PoS) terminal. The agency in collaboration with banks is

working out modalities to ensure that bank customers using cards to pay for goods and services on PoS

terminals and web platforms will be rewarded. All the banks in order to win more customers have

embarked on specialized and unconventional banking services. One of such is the Children Saving Scheme

(CSS) designed to encourage customers to save towards their children education.

All the banks have adopted the Automated Teller Machine (ATM), a cash withdrawal system that

guarantees withdrawals with minimal risk even outside the banking hours of the day and night.

Consolidation Brought about Increased Savings and Investment

With the wiping out of the dubious money bags and highly placed politicians that hijacked the banking

industry for their selfish gains from the system through Consolidation, it brought to existence a system that

has the interest of her customers at heart. This is evidence from various innovative savings and investments

packages that are embarked upon by all banks. For example, recently Diamond bank plc engaged on

aggressive programme of encouraging prospective customers to open saving accounts without any cash

deposit. Many of the banks have engaged in various financial promos through which many customers have

become owners of cars, buildings and other properties including cash prices which have positively

influenced their living standard. The confidence and trust restored to banks as a result of Consolidation

have made many customers to patronize banks.

Reduction in Banks Cost

Mergers and acquisitions which took place during the Consolidation resulted in reduction in banks

cost through a larger market share, higher efficiency and enjoyment of the advantages of economies of

scale (Alvares and Crespi, 2003). Also, Consolidation reduced the over rated number of banks from 89 to a

more manageable size of 25, which are easier to supervise with a stronger and more resilient financial

economy. Various ICT driven innovations embarked upon by many banks have to a very great extent

reduced the cost incurred by customers. One can now transfer huge sum of money from one bank to

another with ease. The mobile money transaction allows mobile phones to be used to send and receive

money, buy recharge cards, pay subscription fees for DStv, pay electricity bills etc.

International Journal of Financial Economics

13

Boost of Manufacturing Sector

With the increased capital base brought about by the Consolidation, many banks are looking for

projects to finance. As rightly captured by Okeke (2006), that before the Consolidation, no bank would

fund your project if you did not have a god father.

He said that since after the Consolidation, banks are virtually on your door step to give you finances.

The government wants Nigerians to participate in downstream Sector of the oil industry, but it was not

possible before the Consolidation for many banks to finance the oil and gas projects due to inadequate

Capital.

Consolidation had strengthen banks and many are now in a position to finance the oil and gas sector

(Ayodele, 2005). Through Consolidation which gave rise to increased capital base of banks, many investors

who had hitherto found it difficult to embark on capital intensive projects can now do that with less stress.

3. Methodology

The research was carried out using primary data sourced from five commercial banks (Access bank,

Diamond bank, Ecobank, First City Monument bank and Mainstreet bank). The choice of these bank was as

a result of the fact that they were deeply involved in the Consolidation exercise including mergers and

acquisition.

A total of one hundred (100) respondents, twenty (20) from each of the banks, were randomly selected

and administered with the questionnaires. At the end, ninety (90) questionnaires were returned out of the

one hundred (100) distributed.

Considering the short period from the date of Consolidation the researcher used the questionnaire

method, analyze the responses and drew inferences there from.

4. Presentation and Data Analysis

This Section deals with data collection, presentation and analysis of the One hundred (100)

questionnaires that were distributed to the five commercial banks investigated viz: Access bank, Diamond

bank, Ecobank, First City Monument Bank and Main Street bank, ninety (90) were required and analyzed

as shown hereunder.

Research Questions

Table I: Do You Think that the Bank Consolidation is Worthwhile?

Variables Respondents Percentage

Yes 83 93

No 7 7

Total 90 100

Source: field survey 2014

On this question, 83 respondent representing 93% are of the opinion that Consolidation is a

worthwhile exercise while only 7 representing 79 said it is not; implying that the exercise is justifiable.

Table 2: Has Consolidation Made any Positive Impact on the Performance of Banks?

Variables Respondents Percentage

Yes 86 96

No 4 4

Total 90 100

Source: Field Survey 2014

E. Fabian & U. T. Ifeanyi

14

96% of the respondents said yes while only 4% said No, showing that it has made positive impact in

banks performance.

Table 3: Do You Think Consolidation Has Increased the Number of Shareholders and Depositors in

the Industry?

Variables Respondents Percentage

Yes 82 91

No 8 9

Total 90 100

Source: Field Survey 2014

91% of the respondents believed that it has increased the number of shareholders and depositors while

only 9% had a negative view implying that Consolidation has actually increased the number of

shareholders and depositors.

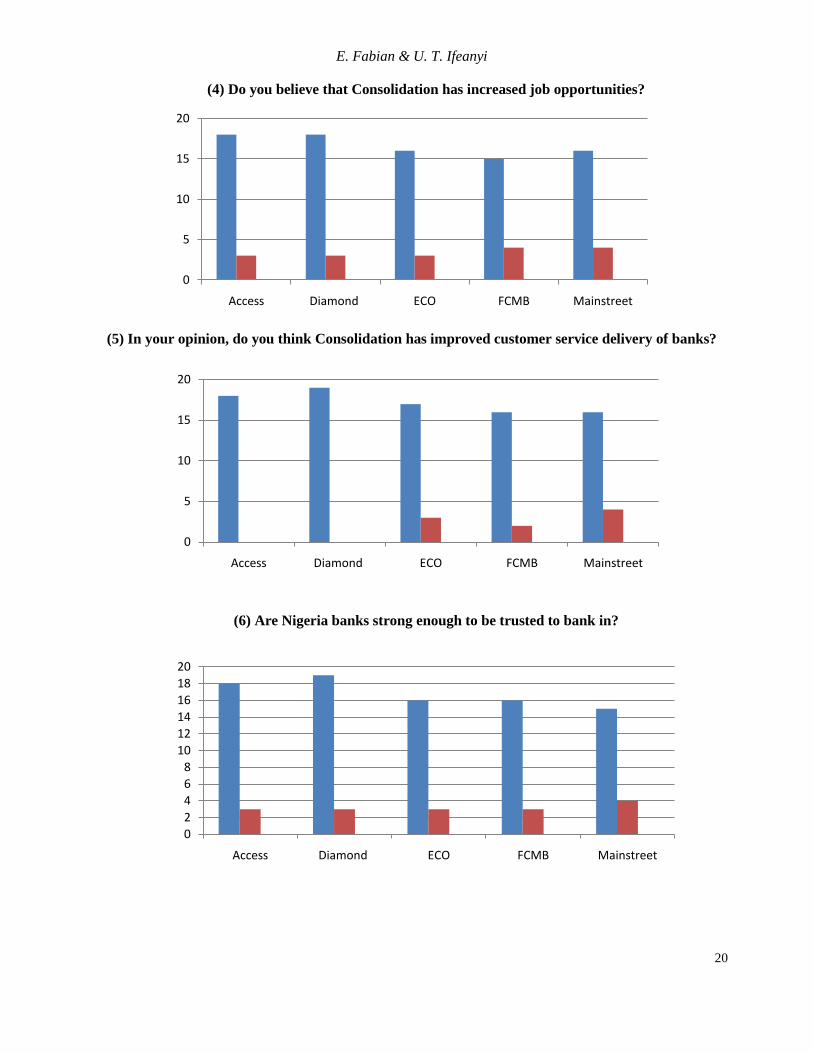

Table 4: Do you believe that Consolidation has Increased Job Opportunities?

Variables Respondents Percentage

Yes 82 91

No 8 9

Total 90 100

Source: Field Survey 2014

82 respondents representing 91% believed that it has increased job opportunities while only 8

representing 9% had a negative opinion, signifying that it has actually increased employment opportunities

in the country.

Table 5: In your Opinion, do you think Consolidation has Improved Customer Service Delivery of

Banks?

Variables Respondents Percentage

Yes 85 94

No 5 6

Total 90 100 Source: Field Survey 2014

94% believed that it has improved customer service delivery while only 6% had a negative view

indicating that it has improved customer delivery.

Table 6: Are Nigeria Banks Strong Enough to be Trusted to bank in?

Variables Respondents Percentage

Yes 82 91

No 8 9

Total 90 100

Source: Field Survey 2014

91% emphatically hold the view it is strong enough to be Trusted while only 9% disagreed, implying

that the Nigerian Banks are strong enough to be trusted to bank in.

International Journal of Financial Economics

15

Table 7: In your own view, do you think Consolidation has contributed positively in reduction of

banks costs.

Variables Respondents Percentage

Yes 86 96

No 4 4

Total 90 100

Source: Field Survey 2014

96% believed that it has positively reduced banks costs while 4% has a negative opinion, indicating

that Consolidation has contributed in reduction of banks costs.

Table 8: Has Consolidation Brought a Boost to Manufacturers or not?

Variables Respondents Percentage

Yes 81 90

No 9 10

Total 90 100

Source: Field Survey 2014

90% of the respondents said yes while only 10% said No, it indicates that Consolidation has brought a

boost to manufacturers.

Table 9: Do you think Consolidation has Contributed to the Increase in GDP and the Overall

Economic Growth?

Variables Respondents Percentage

Yes 87 97

No 3 3

Total 90 100

Source: Field Survey 2014

From the responses, 97% said yes while only negligible number of 3 people had a negative view

indicating that Consolidation very highly contributed to the increase in GDP and the overall economic

growth.

Table 10: Has increased in banks Capital base any positive impact on banks’ performance.

Variables Respondents Percentage

Yes 84 93

No 6 7

Total 90 100

Source: Field Survey 2014

93% said Yes while only 7% said „NO‟, this indicates that Consolidation has impacted positively to

banks‟ performance.

Table 11: In your opinion, has Consolidation restored the confidence of Nigerians to patronize the

Banks?

Variables Respondents Percentage

Yes 82 91

No 8 9

Total 90 100

Source: Field Survey 2014

E. Fabian & U. T. Ifeanyi

16

91% of the respondents believed in the statement while only 9% disagreed. This indicates that there is

a restored confidence of Nigerians on our banks.

Table 12: Do you think Consolidation has improved banks efficiency and overall productivity?

Variables Respondents Percentage

Yes 88 98

No 2 2

Total 90 100

Source: Field Survey 2014

Out of the total respondents received, 88 representing 98% said that it has improved banks efficiency

and overall productivity while only a negligible number of 2 had a negative view indicating that

Consolidation has highly improved banks efficiency and productivity.

Summary of Findings

It is necessary to give a concise summary of the findings from the five commercial banks investigated

in this study. From the results obtained it was found as follows;

1. That Consolidation increased the number of shareholders and depositors.

2. That Consolidation brought about increased job opportunities.

3. That Consolidation brought within the system improved innovative customer service delivery.

4. That Consolidation led to increased savings and investment.

5. It brought about reduction in banks cost.

6. Consolidation boosts the manufacturing sector.

5. Recommendation

1. Although Consolidation has impacted positively on creation of more job opportunities, we have not

yet reached the eldarado-much expected promise land as regards employment of the teaming youths.

Banks should give more loans and incentives to market-oriented agricultural projects, agribusiness and

agro-services. By so doing, this will reduce drastically the Africa‟s food import bill which is estimated at

$35billion annually and also minimize the rural-urban migration.

2. In most economies particularly in developing countries like Nigeria, Small and Medium Enterprise

(SMEs) accounts for over 75% of the entire business. The supervisory authorities (CBN) should

intensify more actions on all the commercial banks to encourage the SMEs. Loans to the SMEs

should be at a minimal interest rate. Also, banks should envolve a policy of not stopping at giving

loans to prospective SMEs investors but also supply managerial skills like guiding the SMEs

operators in book-keeping, general accounting, organizing regular enlightment programmes on ratios,

seminars etc.

In furtherance to achievements of this goal, there should be proper enlightment of the public as regards

the benefits of bank Consolidation by the Securities and Exchange Commission (SEC).

3. CBN should regulate interest rates charged by commercial banks on loans by pursuing a policy of a

simple digit interest rate. This will go a long way in encouraging investors to invest in developmental

projects.

International Journal of Financial Economics

17

6. Conclusion

Having enumerated many benefits of the impact of banking sector consolidation on Nigeria economy,

one can strongly attest that the banks have come to be a strong agent of the stability of the Nigeria business

environment and an investable tool for grass root orientation and development. The consolidation of the

baking sector has transformed Nigeria‟s financial system and created opportunities higher growth. These

benefits, however will not be actualized if the authorities fail to work diligently to ensure that past

weakness do not continue in post consolidation era. Efforts must therefore be stepped up to strengthen

supervision and regulatory intension for the continual realization of the objectives of the banking reforms.

References

Al-faki, M. 2006."The Nigerian Capital Market and Socioeconomic Development". A Paper

presented at the 4th distinguished Faculty of Social Science, Public Lectures,

University of Benin Pg. 9-16

Alvares, R. and Crespi.G. (2003) Determinant of Technical Efficiency in Small Firms. Small

Business Economics 20, 233-244.

Ayodele, Aminu 2005.Foreign Capital inflows.The gains, the pains.This Day

Newspaper, November 16,216.

Banerjee, A. 2009. Difficult Trade-Offs free Exchange, Economist blogs. Available:

www.economist.comblogs/freeexchangellin roundtable

Barlett, B. 2000 "Opinion editorial on the effect of Stock Market on the economy" National

Centre for policy analysis.

Berger, Allen N. 1998. The Efficiency Effect of Bank Mergers and Acquisition: A Preliminary

look at the 1990's in Bank Merger and Acquisition, Y Amilud and G. Miller (eds)

Boston: Kluwer Academy

Brownbridge, M. 1996. The impact of Public Policy on the Banking System in Nigeria. Zaria,

Nigeria: Institute of Development Studies.

Cameron, R. 1967. Banking in the Early Stage of industrialization. New York. Oxford University

Press.

CBN Fourth Annual Monetary Policy Conference 2004.Pg. 64.

ChukwumaSoludo, Banks and the National Economy, Progress, Challenges and the Road Ahead.

CBN Quarterly Report, 2007 pp. 22.

Edward, S. 2004. Capital Mobility and Economic performance, Are Emerging Economies

Different? NBER P. 8076

Ewah, S.O.E, Esang, A.E and Bassey, J.U. 2009."Appraisal of Capital Market Efficiency on

Economic Growth in Nigeria". International Journal of Business and Management,

December, 219-225

Fernandez, D. and Caletovic, A. 1995."SchurnpeterMigut BC Right - but why? Explaining the

Relationship between Finance Development and Growth" John Hopkins:

University of SAIS working paper in International Economics

Greenwood, J. and Jeranovic, B. 1990."Financial Development, Growth and the

Distribution ofIncome" Journal of Political Economy, 98, 1076-1107.

Goldsmith R. 1995. Financial Structure and development" New Haven. Yale University

Publication and Press

E. Fabian & U. T. Ifeanyi

18

IkaChuks (2014) Chairman, Committee ofE-Banking industry Heads (CEBIH), The Nation

Newspaper, Wed. April 23, 2014 p. 27

King, R.G. &Levine R. (1993a) "Finance Entrepreneurship and Growth: Theory and Evidence"

Journal of Monetary Economics 32 (December), 513-42.

Lemo T. 2005. "Regulatory Oversight and Stakeholder" A Paper presented at the BGL Mergers

and Acquisitions Interactive Seminar held at Eko Hotels and Suites, Victoria

Island Lagos.

Levine, R. 1991. "Stock Market Growth and Tax Policy"! A journal of finance Vol. 46 (4) pp

1445-1465

Levine, R. and Zeavos, S. 1991. "Stock Market Development and Long-Run Growth". The

World Bank Economic Review, 10 (3) 323-339

Lewis, P. and Stein, H. 1997. Shifting Fortunes: The Political economy of financial

liberalization in Nigeria.World Development, 25, 5-22

Mckinnon, R.I. 1973. Money and Capital in Economic Development, Washington D. C. Brooking

Institution

Mckinnon, R.I. and Shaw 1973. "Money and Capital in Economic Development", Washington,

D.C., The Brookings Institution, Nigerian Stock Exchange fact books 2001-2011

Okeke, E 2006.Effect of the Recapitalization on the Nigerian Economy. Sun News January 21.

Osaze B.E. 2000. The Nigerian Capital Market in the African and \Global Financial

System. Benin City: Bofic Consulting Group Ltd.

Oyejide, T.A. 1993. Effect of Trade and Macroeconomic Policies on African Agriculture.In

R.M. Bantisa and A. Valdes (Eds). The bias against agriculture: Trade and

macroeconomic policies in developing Countries (Chapter 12) San Francisco, C.A.

Sain, T.A. 2009."The impact of Bank Reform on Commercial Bank Performance in Nigeria"

Journal of Economies Thought 1(6): 31-33

Soludo, C. 2006, June 7-9. Beyond Banking Sector Consolidation in Nigeria. Paper presented at

the 1ih Annual Nigerian Economic Summit. Transcorp Hilton, Abuja The bullion, Vol. 2.2006 p.

22.

International Journal of Financial Economics

19

Appendix

(1) Do you think that the bank Consolidation is worthwhile?

(2) Has Consolidation made any positive impact on the performance of banks?

(3) Do you think Consolidation has increased the number of shareholders and depositors in the

industry?

0

2

4

6

8

10

12

14

16

18

Access Diamond Eco FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

20

Access Diamond ECO FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

Access Diamond ECO FCMB Mainstreet

E. Fabian & U. T. Ifeanyi

20

(4) Do you believe that Consolidation has increased job opportunities?

(5) In your opinion, do you think Consolidation has improved customer service delivery of banks?

(6) Are Nigeria banks strong enough to be trusted to bank in?

0

5

10

15

20

Access Diamond ECO FCMB Mainstreet

0

5

10

15

20

Access Diamond ECO FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

20

Access Diamond ECO FCMB Mainstreet

International Journal of Financial Economics

21

(7) In your own view, do you think Consolidation has contributed positively in reduction of banks

costs.

(8) Has Consolidation brought a boost to manufacturers or not?

(9) Do you think Consolidation has contributed to the increase in GDP and the overall economic

growth?

0

5

10

15

20

Access Diamond ECO FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

20

Access Diamond ECO FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

20

Access Diamond ECO FCMB Mainstreet

E. Fabian & U. T. Ifeanyi

22

(10) Has increase in banks Capital based any positive impact on banks’ performance.

(11) In your opinion, has Consolidation restored the confidence of Nigerians to patronize the Banks?

(12)Do you think Consolidation has improved banks efficiency and overall productivity?

0

2

4

6

8

10

12

14

16

18

20

Access Diamond ECO FCMB Mainstreet

0

2

4

6

8

10

12

14

16

18

Access Diamond ECO FCMB Mainstreet

0

5

10

15

20

25

Access Diamond ECO FCMB Mainstreet