The Impact of Liquidity on Profitability on Selected Banks of Bangladesh

78

“The Impact of Liquidity on Profitability of Selected Banks in Bangladesh”

-

Upload

samia-ibrahim -

Category

Documents

-

view

59 -

download

5

Transcript of The Impact of Liquidity on Profitability on Selected Banks of Bangladesh

“The Impact of Liquidity on Profitability of Selected Banks in Bangladesh”

Prepared by:

Samia Ibrahim

An Internship Report Presented in Partial Fulfillment of the Requirement for the

Degree Bachelor of Business Administration

Independent University, Bangladesh.

May, 2014

“The Impact of Liquidity on Profitability of

Selected Banks in Bangladesh”

Prepared by:

Md. Samia Ibrahim

Has been approved by

Md. Nayeem Abdullah

Assistant Professor

School of Business

Independent University, Bangladesh.

May 2014

Letter of Transmittal

May 22nd 2014

Mr. Nayeem AbdullahAssistant ProfessorIndependent University, Bangladesh

Subject: Submission of internship report on “The Impact of Liquidity on Profitability of Selected Banks in Bangladesh”

Dear Sir,

This is a great pleasure for me to submit my internship report on The Impact of Liquidity on Profitability of Selected Banks in Bangladesh” as a requirement for my graduation. I have prepared this report during my three months long Internship program at Mercantile Bank Limited, Khatungonj Branch, Chittagong. I was privileged to be associated with such an experienced, efficient and helpful team in such a reputed Bank. This has been a great source of learning for me and helped me a lot to achieve practical knowledge.

I have put my best effort in making this report and tried to make this report informative, practical, and relevant. I hope and believe that this report will satisfy your requirements and expectations.

However, I would like to express my sincere gratitude to you for your kind guidance, cooperation and suggestions in preparing this report which will definitely help me in future endeavors. It would be my immense pleasure if you find this report informative.

I shall be happy to provide any further query and clarification regarding this report.

Yours Sincerely,

Samia IbrahimID: 1020627 Dept: BBAIndependent University, Bangladesh

Acknowledgement

First of all I am grateful to Almighty ALLAH.

I would like to thank all my honorable faculty members, who over the years, played a big role in

grooming me into whatever I am today, especially my honorable supervisor, Mr. Nayeem

Abdullah for being so kind, cooperative, and supportive the entire time. I am grateful to him for

his valuable suggestions and time that he has spent on me in guiding me. The past few months

have been a wonderful experience for me, full of challenges and satisfaction. This has obviously

been a great source of learning for me and a transition period from a student life to professional

life.

I would like to acknowledge my great appreciation towards everyone at Mercantile Bank

Limited for being so warm in their approach and for bestowing such responsibility on me all the

while, making me feel completely at ease. A special thanks to my External Internship

Supervisor, Mr. Jashim Uddin, V.P., Head of Khatungonj Branch Mercantile Bank Limited for

giving me time and for providing me with all kinds of support by suggesting me about

completing the report.

Finally, I would like to thank all the employees of MBL who helped me in conducting my

research by taking out time for me from their extremely busy schedule to discuss on various

issues with me and making me more knowledgeable about the Banking industry. Without them I

would not have been able to complete my report.

Table of ContentsChapter Particular Page no:

Executive Summary iChapter 1: Introduction 1

1.1 introduction 21.2 Statement of the problem 21.3 Purpose of the Study 31.4 Scope of the study 31.5 Methodology 3

1.5.1 Research Design 31.5.2 Research Instrument 41.5.3 Research Sample 51.5.4 Data Sources 51.5.5 Limitations 5

Chapter 2: Banking Sector of Bangladesh 7Chapter 3: Company profile : Mercantile Bank Limited 8

3.1 Overview of Mercantile Bank Limited 14 3.1.1 Mission 15 3.1.2 Vision 15 3.1.3. Objectives 15 3.1.4 Functional Departments 16 3.1.5 Corporate Information 16

Chapter 4: Literature Review 174.0 Literature Review 184.1 Conceptual Framework 214.2 Definition of Liquidity & profitability 224.3 Independent Variables : Liquidity Ratios 22 4.3.1 Loan Deposit Ratio (LDR) 22 4.3.2 Cash Deposit Ratio (CDR) 23 4.3.3 Deposit Asset Ratio (DAR) 234.4 Dependent Variables : Profitability Ratios 23 4.4.1 Return on Asset (ROA) 24 4.4.2 Return on Equity (ROE) 24

Chapter 5: Research Objectives, Questions, Hypothesis & Hypotheses 255.1 Objectives of the Study 265.2 Research Questions & Hypothesis 265.3 Hypotheses 26

Chapter 6: Findings & Analysis 276.1 Evaluation of Profitability 286.2 Evaluation of Liquidity 296.3 Analysis of Impact on Liquidity on Profitability 33 6.3.1 Descriptive Analysis 33 6.3.2 Correlation Analysis 34 6.3.3 Regression results 35

Chapter 7: Conclusion 39

Bibliography 41Appendix 43

Executive Summary

Profitability and liquidity are the most prominent issues in the banking sector all over the world.

The ultimate goal for any organization is to maximize profitability. However, in case of banks,

too much attention on profitability may lead the bank into a pitfall by diluting the liquidity

position. It is very much important to maintain an optimum level of liquidity while generating

good amount of profit. This study is initiated to find out the relationship between liquidity and

profitability. The study five scheduled private commercial banks in Bangladesh over a period of

past 5 years from 2008 to 2012. To examine the impact of liquidity on profitability, descriptive

statistics, and correlation analysis has been executed. Profitability ratios, ROA and ROE are

assumed to be the dependent variable and the independent variables are liquidity measures, i.e.

Loan Deposit Ratio, Deposit Asset Ratio and Cash Deposit ratio. However, the descriptive

analysis has revealed that the values of standard deviation and variance of profitability ratios are

higher than those of the liquidity measures. Therefore, profitability is more volatile than liquidity

measures. The Pearson’s correlation analysis and findings suggest that there is no significant

relationship between liquidity and profitability among the selected banks in this study over the

period of observation. The regression analysis also shows that there is no significant impact of

liquidity measures on profitability. The r square of liquidity measures is found to be 0.50 and

0.46 with ROA and ROE respectively. Therefore, only 46% and 50% of the variation in ROA

and ROE can be explained by the liquidity measures.

Chapter One

Introduction

1.1. Introduction

Generally, the banking business involves mobilization of funds from the surplus units to the

deficit units in the economy of a country. While performing these functions, banks undertake

many risks and prominent among those risks is liquidity risk. Liquidity risk is the risk of loss

incurred by the bank due to its inability to meet the cash needs. It may include the cash needs for

lending and investment commitments and deposit withdrawals and liability maturates, in the

normal course of business (Amengor, 2010). The bank’s profitability depends on its ability to

generate revenue in excess of costs, withstanding negative shocks. Bank profitability is usually

expressed as a function of internal and external factors. The variables which mostly determine

bank profitability are expense management, loan composition and bank credit, composition of

bank deposits, market interest rates, bank earning and operating efficiency, changes in capital

and liquidity management.

The study will attempt to find out the impact of liquidity on profitability of some selected banks

in Bangladesh. I will consider five randomly selected banks to represent the overall banking

industry scenario of Bangladesh. The study will help to find relationship between liquidity and

profitability and suggest solutions for better profitability.

1.2 Statement of the Problem

Liquidity risk is one of the prominent risks faced by banks. Determining the optimum level of

liquidity is quite critical and important too because it can affect the banks’ performance and

profitability. This research seeks to establish a relationship between liquidity and profitability

which may assess in liquidity management in the banks in Bangladesh.

1.3 Purpose of the Study

There has been a wide range of study on the concepts of liquidity and profitability. Some studies

were made to find the interaction between the two while some were made on the proper

management of these two variables. My research differs from the previous works as such

research was not done in the context of Bangladeshi banking sector using recent data.

1.4 Scope of the Study

Liquidity is of great importance to banks because it determines the banks’ ability to meet its

current cash needs, such as payment obligation and other financial commitments. A bank is

considered to be liquid when it has sufficient cash and other short term financial instruments like

treasury bills and certificates. It has always been a matter of discussion for the banks’

management to determine how much liquid asset should be maintained. Adequate liquidity helps

banks to grab lucrative loans situations during periods of expanding economic activities. But by

maintaining surplus liquidity, the bank can lose attractive long-term investment opportunities

which might be profitable. In this research this relationship between liquidity and profitability

will be investigated.

1.5 Methodology of the Research

1.5.1 Research design

This study aimed to establish a relationship between liquidity and profitability of banks in

Bangladesh through an empirical research. The data used in this study are compiled from income

statements and cash flow statements from the annual report of each year of the selected banks.

The sample has been tested through descriptive statistics, correlation analysis and regression

analysis.

1.5.2 Research instrument

In this study, descriptive statistics has been used to compare the means of the profitability ratios

and the liquidity ratios. The trade-off between liquidity and profitability was analyzed through

Pearson Correlation Coefficient analysis and represented through correlation matrix. The

hypotheses have been tested by applying linear regression using SPSS. The profitability ratios

are the dependent variables whereas liquidity measures are the independent variable. The

variables to analyze the liquidity impact on profitability using regression analysis are as follows:

Dependent Variables:

Return on Assets = Net Income after Taxes / Total Assets

Return on Equity = Net Income after Taxes / Total Equity Capital Account

Independent Variables:

Loan Deposit Ratio = Loans and Advances / Total Deposit

Deposit Asset Ratio = Total Deposit / Total Assets

Cash Deposit Ratio = Cash & Equivalent / Total Assets

MODELS

The research model is as follows:

ROA= α1 + β11 LTD + β12 DTA + β13 CTD + Ui -----------------------model (1)

ROE = α2 + β 21 LTD + β22 DTA + β23 CTD + Ui -----------------------model (2)

α : the constant , β: the regression coefficient, Ui : error

1.5.3 Research Sample

A sample of five private commercial banks have been randomly selected and examined to find

the impact of liquidity on profitability over the period of five years during 2008 to 2012. The

selected banks are-

Bank Asia Limited

Mercantile Bank Limited

Prime Bank Limited

Eastern Bank Limited

South East Bank Limited

1.5.4 Data Sources

All the relevant data regarding the study were collected from the following sources:

Secondary source:

Annual report of the selected banks

Financial statements of the selected banks

Policy guideline of the banks

Related journal & articles.

1.5.5 Limitations

The allocated time was not sufficient to gather knowledge and to make the study a

complete and fruitful one. It was one of the main constraints that affected covering all

aspects of the study.

The data is collected from secondary sources; hence the reliability of data is questionable.

Only a small sample of five banks has been considered in this study due to lack of time.

For the lack of practical knowledge, some shortcoming may be available in the paper.

Personal barriers such as inability to understand some terms were also a limitation.

Chapter Two

Banking Sector of Bangladesh

2.1 Banking Sector of Bangladesh

The Financial sector of Bangladesh, like most in developing countries, is dominated by banking

industry. After the independence of Bangladesh in 1971, all the domestic banks were merged and

grouped into few state owned commercial banks. However, their performance was not

satisfactory in terms of profitability, customer service and overall performance. To set up a

proper regulatory system that would diagnose such problems and correct them was also tough

while the government intervention were in existence everywhere. Therefore, banking concept

like profitability, liquidity and capital adequacy were alien to bank managers. Some private

banks were allowed to operate in the market in 1980s, they begun to perform satisfactorily. Later

more private commercial banks were allowed to play in the market. At present private

commercial banks are dominant in respect of market share and profitability in the banking sector

of Bangladesh.

2.1.1 Banking System in Bangladesh

Before the independence, the branch banking system of Bangladesh is inherited from the

British colonial regime. There were 44 banks and financial institutions in operation in erstwhile

Pakistan before the partition of Indo-Pak sub-continent in 1947. After the emergence of Pakistan

in 1947, State Bank of Pakistan became the Central Bank of Pakistan in July 1948. In the whole

Pakistan there were 36 scheduled commercial banks in operation until 1971. Local business

groups of East Pakistan owned only two banks, Eastern Mercantile Bank Ltd. (presently Pubali

Bank Ltd.) and Eastern Banking Corporation Ltd. (presently Uttara Bank Ltd.) established in

1959 with headquarters in Dhaka.

After the independence, banking industry in Bangladesh started its journey with 6 nationalized

commercialized banks, 2 State owned specialized banks and 3 Foreign Banks. In the 1980's

banking industry achieved significant expansion with the entrance of private banks. Now, banks

in Bangladesh are primarily of two types:

Scheduled Banks: The banks which get license to operate under Bank Company Act,

1991 (Amended in 2003) are termed as Scheduled Banks.

Non-Scheduled Banks: The banks which are established for special and definite

objective and operate under the acts that are enacted for meeting up those objectives, are

termed as Non-Scheduled Banks. These banks cannot perform all functions of scheduled

banks.

2.1.2 Private Commercial Bank

Local private commercial bank started operation in the decades of 1980's. We can

categorize local private bank in the following manner:

First generation bank: Those established in the decades of 1980s.

Second generation bank: These banks started operation in 1990 to 1995.

Third generation bank: After 1998, these banks are established.

At present, there are thirty local private commercial banks operating in Bangladesh. PCBs

dominate the banking sector of Bangladesh. More than fifty percent of total deposits and assets

are covered by the PCBs. The performance of PCBs is much better than SCBs and DFIs in all

respects. Bangladesh‘s PCBs have quickly occupy market share at the expense of the state-

owned commercial banks (SCB) and presently grasp more than 59 percent of total deposits

whereas it is only 28 percent for the SCBs and PCBs assets coverage is 58% whereas it is only

29% in SCBs.

Table 1 and figure 1 shows the number of banks from the year 1975 to 2010. Then number of

Nationalized and Specialized Banks remained almost the same with only a little change. The

number of Foreign Banks grew up a little but decreased to 9 after the year 2000. However, the

number of private banks had a rising trend up to the year 2005. The number of private banks

increased substantially in the period from 1995 to 2000. 14 new private banks were allowed to

come into operation in this period. After the year 2000, only 3 more private banks came into the

market. The number of private banks remain unchanged after the year 2005 i.e. 30.

Number of Banks in Bangladesh from 1975 to 2010

1975 1980 1985 1990 1995 2000 2005 2010

Total Number of banks 12 14 21 24 31 49 48 47

Nationalized Banks 6 6 4 4 4 4 4 4

Specialized Banks 2 2 2 3 5 5 5 4

Private Banks 8 10 13 27 30 30

Foreign Banks 4 6 7 7 9 13 9 9

No. of bank branches 1611 3820 4943 5539 5813 6065 6412 7246

Table 1- Number of Banks in Bangladesh from 1975 to 2010

1975 1980 1985 1990 1995 2000 2005 20100

10203040

6 6 4 4 4 4 4 42 2 2 3 5 5 5 48 10 13

27 30 30

4 6 7 7 9 13 9 9

Number of Banks in Bangladesh from 1975 to 2010

Nationalized Banks Specialized Banks Private Banks Foreign Banks

Figure 1- Number of banks in Bangladesh from 1975-2010

2.1.3 The Current Structure of Financial System in Bangladesh

At present the financial system in Bangladesh is mainly comprised of two types of institutions

like banks and non-bank financial institution (NBFIs). The formal financial sector in Bangladesh

includes: (a) Bangladesh Bank as the central bank, (b) 47 commercial banks, including (c) 30

non-bank financial institutions (NBFIs) – licensed by the Bangladesh Bank; (d) A total of 62

insurance companies have been operating in Bangladesh, (e) 2 stock exchanges and, (f) Some co-

operative banks. Besides, a good number of semi-formal micro finance institutions (MFIs) also

are operating in Bangladesh.

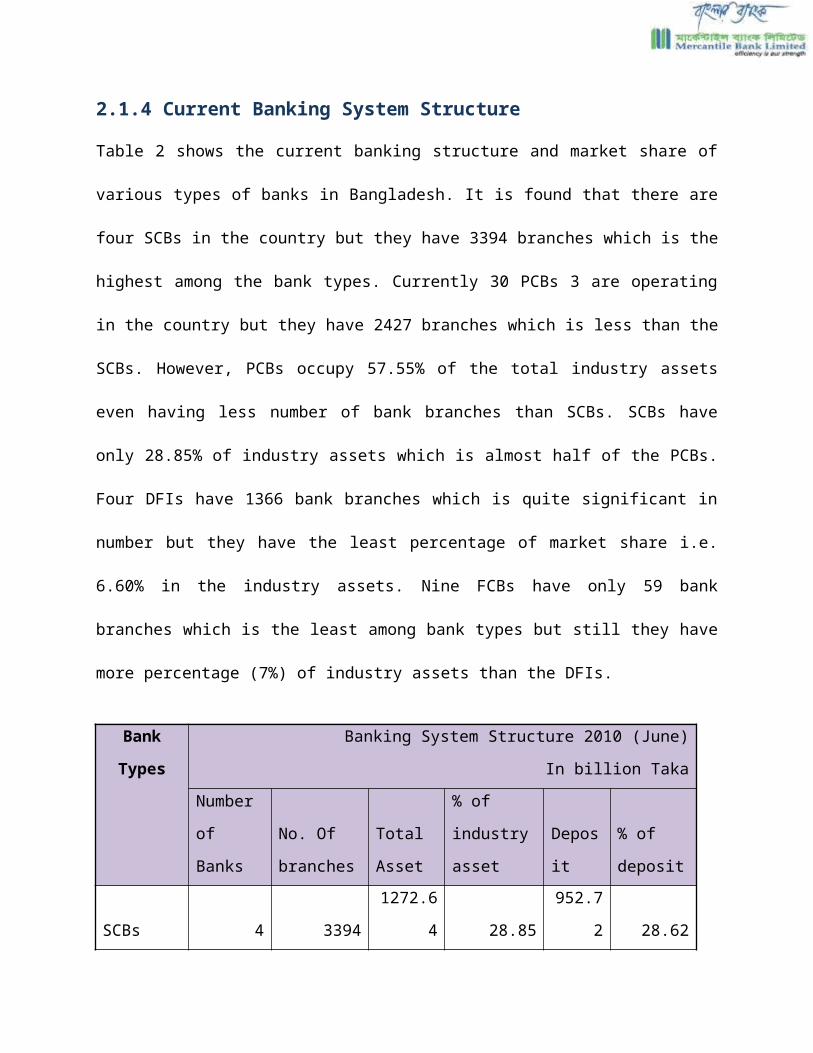

2.1.4 Current Banking System Structure

Table 2 shows the current banking structure and market share of various types of banks in

Bangladesh. It is found that there are four SCBs in the country but they have 3394 branches

which is the highest among the bank types. Currently 30 PCBs 3 are operating in the country but

they have 2427 branches which is less than the SCBs. However, PCBs occupy 57.55% of the

total industry assets even having less number of bank branches than SCBs. SCBs have only

28.85% of industry assets which is almost half of the PCBs. Four DFIs have 1366 bank branches

which is quite significant in number but they have the least percentage of market share i.e. 6.60%

in the industry assets. Nine FCBs have only 59 bank branches which is the least among bank

types but still they have more percentage (7%) of industry assets than the DFIs.

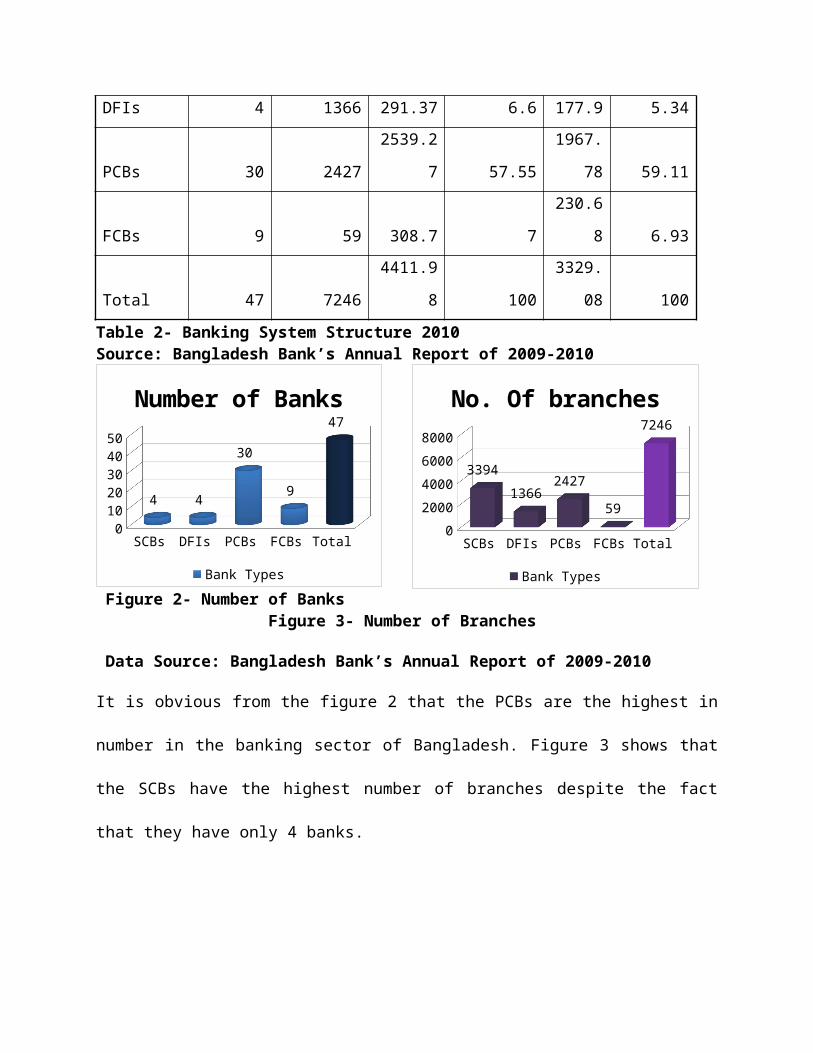

Bank

Types

Banking System Structure 2010 (June) In billion

Taka

Number

of Banks

No. Of

branches

Total

Asset

% of

industry

asset Deposit

% of

deposit

SCBs 4 3394 1272.64 28.85 952.72 28.62

DFIs 4 1366 291.37 6.6 177.9 5.34

PCBs 30 2427 2539.27 57.55 1967.78 59.11

FCBs 9 59 308.7 7 230.68 6.93

Total 47 7246 4411.98 100 3329.08 100

Table 2- Banking System Structure 2010Source: Bangladesh Bank’s Annual Report of 2009-2010

SCBs DFIs PCBs FCBs Total0

10

20

30

40

50

4 4

30

9

47

Number of Banks

Bank Types

Figure 2- Number of Banks Figure 3- Number of Branches

Data Source: Bangladesh Bank’s Annual Report of 2009-2010

It is obvious from the figure 2 that the PCBs are the highest in number in the banking sector of

Bangladesh. Figure 3 shows that the SCBs have the highest number of branches despite the fact

that they have only 4 banks.

SCBs DFIs PCBs FCBs Total0

10002000300040005000600070008000

3394

13662427

59

7246

No. Of branches

Bank Types

Chapter Three

Company Profile: Mercantile Bank Limited

3.1. Overview of Mercantile Bank Limited

Mercantile Bank Limited (MBL) emerged as a new commercial bank to provide efficient

banking services and to contribute socio-economic development of the country. The Bank

commenced its operation on June 2, 1999. The Bank provides a broad range of financial services

to its customers and corporate clients. The Board of Directors consists of eminent personalities

from the realm of commerce and industries of the country. Strategic objectives are achieving

positive Economic Value Added (EVA) each year, to be one of the top three Financial

Institutions in Bangladesh in terms of cost efficiency, to achieve 20% return on shareholders'

equity or more, on average.

Mercantile Bank Limited (MBL) provides various commercial banking services in Bangladesh.

The company provides a range of services, including accepting deposits, making loans,

discounting bills, and conducting money transfer and foreign exchange transactions, as well as

performing other related services, such as safe keeping, collections, issuing guarantees,

acceptances, and letters of credit. Its deposit products include double benefit deposit, family

maintenance deposit, monthly savings, quarterly benefit deposit, special savings, advance benefit

deposit, and pension and family support schemes. The company also offers consumers credit,

doctor’s credit, car loan, and rural development schemes, as well as provides lease financing,

personal loans, and small loans. In addition, it offers online services and debit and credit card

facilities. As of December 31, 2011 the company operated 75 branches and 3 small and medium

enterprise service centers in Bangladesh. Mercantile Bank Limited founded in 1999 and it is

headquartered in Dhaka, Bangladesh. Mercantile Bank Limited emerged as a new commercial

bank to provide efficient banking services and to contribute socio-economic development of the

country. The Bank provides a broad range of financial services to its customers and corporate

clients. The Board of Directors consists of eminent personalities from the realm of commerce

and industries of the country. Mercantile Bank Limited, a scheduled commercial bank in the

private sector incorporated in Bangladesh under the Banking Companies Act 1991. 30, sponsors

established the bank and it started its operations on 2 June 1999 with an authorized capital of TK

800 million divided into 8 million ordinary shares of TK 100 each. On 31 December 2001, its

paid up capital was TK 596.5 million. The Vision of the bank is “Would make finest corporate

citizen.”Its mission is to become most caring, focused for equitable growth based on diversified

deployment of resources and nevertheless would remain healthy and gainfully profitable Bank.

3.1.1 Mission

“Will become most caring, focused for equitable growth based on diversified deployment of

resources, and nevertheless would remain healthy and gainfully profitable Bank”

3.1.2 Vision“Would make finest corporate citizen”

3.1.3 Objectives

Strategic objectives• To achieve positive Economic Value Added (EVA) each year.

• To be market leader in product innovation.

• To be one of the top three financial institutions in Bangladesh in terms of cost efficiency.

• To be one of the top five financial institutions in Bangladesh in terms of market share in

all significant market segment they serve.

Financial objective• To achieve 20% return on shareholders’ equity or more, on average

3.1.4 Mercantile Bank’s Functional Departments

The Mercantile Bank Limited has the following departments, which includes the whole

operations of the bank. The departments are listed below with their major section in the

following table.

Departments in Mercantile Bank Limited

Major Sections Department Name

BranchesGeneral Banking DepartmentCredit DepartmentForeign Exchange Department

Human Resources Department

Corporate OfficeInternational DivisionTreasuryIT (Information Technology)Card Division

Table 3- Departments in MBL

3.1.5 Corporate Information

HEAD OFFICE

61, Dilkusha Commercial Area Dhaka-

1000

Phone: +88-02-9559333, 9553892, 9561140 Fax:

+88-2-9561213

Swift: MBLBBDDH

E-mail: [email protected] m

Website: www.mblbd.co m

Chapter four

Literature Review

4.0 Literature Review

Banks today are under great pressure to perform- to meet the objectives of their stockholders,

employees, depositors and borrowing customers, while somehow keeping government regulators

satisfied that the bank’s policies, loans and investments are sound (Rose, 2004-2005).

Commercial banks are profit seeking organizations. Banks have to earn profits because if they

don’t, they would not work as all the shareholders would sell off the shares if proper dividends

are not earned. Hence they have to earn profits for their shareholders and at the same time satisfy

the withdrawal needs of its customers.

Bourke (1989) finds some evidence of a positive relationship between liquid assets and bank

profitability for 90 banks in Europe, North America and Australia from 1972-1981. On the other

hand, other researchers argue that, holding liquid assets imposes an opportunity cost on the bank

given their low return relative to other assets, thereby having a negative effect on profitability.

For example, Molyneux and Thornton (1992) and Goddard, et al (2004) find evidence of a

negative relationship between the two variables for European banks in the late 1980s and mid‐1990s, respectively. According to Eichengreen and Gibson (2001), the fewer the funds tied up

in liquid investments, the higher we might expect profitability to be. In effect, various authors

have found varying relationships between the liquidity and profitability of banks in various

countries.

Eljelly (2004) examined the relation between profitability and liquidity measured by current

ratio and cash gap (cash conversion cycle) on a sample of joint stock companies in Saudi Arabia

using correlation and regression analysis. They found a negative relationship between

profitability and liquidity indicators. In order to test Hirigoyen hypothesis, Pimentel et al (2005)

performed an empirical study with a sample of retailing companies in the Brazilian market for

the period of 2000 to 2003. The authors found out for the analyzed sample that the larger the

current ratios, the smaller the ROE, thus there would be a negative correlation among liquidity

and profitability on the short run.

Banks are obliged to pay cash before asset driven cash collections occur, increasing their

illiquidity (Adrian & Shin, 2009). Bank liquidity management involves a tradeoff between the

cost of attaining higher liquidity and the cost of inefficient allocation of such liquidity. Providing

financial services across borders helps to transfer liquidity to those locations where it is scarce,

but at the cost of probable inefficient fund allocation. These inefficiencies may arise from not

having enough cash to finance the maximum possible number of positive net present value,

thereby, resulting in lessened opportunities for shareholder value creation (Dietrich & Vollmer,

2010). The relationship between the liquidity and the profitability of banks listed on Ghana Stock

Exchange is presented by Lartey V, Antwi1 S, Boadi E. (2013) study. Seven out of the nine

listed banks were involved in the study. The study was descriptive in nature. It used the

longitudinal time dimension, specifically, the panel method. Document analysis was the main

research procedure used to collect secondary data for the study. The financial reports of the

seven listed banks were studied and relevant liquidity and profitability ratios were computed.

The trend in liquidity and profitability were determined by the use of time series analysis. The

main liquidity ratio was regressed on the profita

bility ratio. It was revealed that for the period 2005-2010, both the liquidity and the profitability

were droping. It was also revealed that there was a very weak positive relationship between the

liquidity and the profitability of the listed banks in Ghana.

The effect of bank capital structure and liquidity on profitability using Nigerian data during the

period from1980 to 2006 studied is presented by Uremadu S. (2012), The data were analyzed

using descriptive statistics and the auto-regressive distributed lag (ADL) model. The study

practiced data on an OLS methodology that incorporated unit root tests for stationary and co-

integration. The study found a positive impact of cash reserve ratio, liquidity ratio and corporate

income tax; and a negative effect of bank credits to the domestic economy, savings deposit rate,

gross national savings (proxy for deposits with the central bank), balances with the central bank,

inflation rate and foreign private investments, on banking system profits. They equally noticed

that liquidity ratio drive banks’ profits in Nigeria, closely followed by balances with the central

bank and then, gross national savings and foreign private investments, followed case in that

order.

Using bank level data for 80 countries in the 1988-1995 periods, a study suggested that interest

margins differences and banks‟ profitability reflect a variety of determinants such as; bank

characteristics, macroeconomic conditions, explicit and implicit bank taxation, deposit insurance

regulation, overall financial structure, and several underlying legal and institutional indicators

(Demirgüç-Kunt and Huizinga,1998). Shahchera, Mahshid (2012) analyzed the impact of

liquid asset holdings on bank profitability for a sample of Iranian banks. Applying the

Generalized Method of Moment (GMM), this study analyzed the profitability of listed banks

using unbalanced panel data over the period of 2002-2009. An important finding of this study is

that the business cycle significantly affects bank profits. The coefficient of regulation is negative

and significant. Therefore if regulators reduce the constraints imposed on banks, banks obtain

profit. Liquidity is of vital importance to the daily operations of a bank. Maintenance of a sound

liquidity position of the bank is necessary to protect the bank against uncertainties of its business.

Maintenance of liquidity bears both risk and return. A tradeoff between these two elements can

minimize the conflict between liquidity versus profitability of a bank (Islam, M. Muzahidul

(2008). As stated by Islam (2008) Koch (1992) believed that there is a short-run tradeoff

between liquidity and profitability. The more liquid a bank is, the lower are its return on equity

(ROE) and return on assets (ROA), all other things being equal. Therefore, statistical

significance of liquidity on profitability can be a great factor for potential investors. In a nutshell

the influence of banks‟ liquidity cannot be negligible when considering profit motive.

4.1 Conceptual framework

Based on the literature review discussed above, an analysis has been conducted to draw a

relationship between the liquidity and profitability of the banks in Bangladesh. The dependent

variables in this study are Return on Assets (ROA) and Return on Equity (ROE) and the

independent variables are the liquidity ratios derived for this study, i.e. Loan Deposit Ratios

(LTD), Deposit Asset Ratios (DAR), Cash Deposit Ratios (CDR).

Figure 4- Conceptualization Model

Before evaluating the impact it is a precondition to be conceptually sound about the items to be

used for measuring the performance. This part mainly deals the theoretical guideline and

definition required for understanding about different terms.

4.2 Definition of liquidity and profitability

Liquidity is the ability of the bank to convert assets into cash. It is also called marketability or

short-term solvency. The liquidity of a business bank is usually of particular interest to its short-

term creditors since the liquidity of the bank measures its ability to pay those creditors.

Profitability can be defined as the final measure of economic success achieved by a company in

relation to the capital invested in it. This economic success is determined by the magnitude of the

net profit accounting (Pimentel, 2005). The assessment of profitability is usually done through

the ROA (Return on Assets =Net Income / Total Assets) and ROE (Return on Equity = Net

Income / Equity), which is the ultimate measure of economic success.

4.3 Independent Variables: Liquidity Ratios

Liquidity Ratios are ratios that come off the Balance Sheet and hence measure the liquidity of the

bank as on a particular day i.e. the day that the Balance Sheet was prepared. Liquidity Ratios are

used to examine the liquidity risk faced by the bank. A decrease in liquidity ratio increases the

liquidity risk of the bank. The ratios that are used in this study are discusses below

4.3.1 Loan Deposit Ratio (LDR)

This ratio insures the optimality of loan and deposit. LDR calculated as:

Loan Deposit Ratio = Loans and Advances / Total Deposit

A higher loan deposit ratio indicates that a bank takes more financial stress by making excessive

loan. Therefore lower loan deposit ratio is always favorable to higher loan.

4.3.2 Cash Deposit Ratio (CDR)

Cash deposit ratio is calculated from the balance sheet data. It determines the bank’s

effectiveness in liquidity management.CDR is calculated as follows:

Cash Deposit Ratio = Cash & Equivalent / Total Deposit

Cash in a bank vault is the most liquid asset of a bank. Therefore a higher CDR indicates that’s a

bank is relatively more liquid than a bank which has lower CDR. Depositors trust to bank is

enhanced when a bank maintain a higher cash to deposit ratio.

4.3.3 Deposit Asset Ratio (DAR)

Deposit asset ratio is another traditional liquidity measure on the liability side. The ratio of

deposits to assets is calculated as:

Deposit Assets Ratio = Total Deposits / Total Assets

It indicates the broad "reliable" base of funding for the bank. This ratio establishes how much of

the bank’s assets are funded by deposits, rather than borrowed funds or equity.

4.4 Dependent Variables: Profitability Ratios

Every bank is most concerned with its profitability. Profitability ratios show a bank's overall

efficiency and performance. One of the most frequently used tools of financial ratio analysis is

profitability ratios which are used to determine the bank's bottom line. Profitability measures are

important to managers and owners alike.

Profitability ratios show a bank's overall efficiency and performance. We can divide profitability

ratios into two types: margins and returns. Ratios that show margins represent the firm's ability

to translate sales dollars into profits at various stages of measurement. Ratios that show returns

represent the firm's ability to measure the overall efficiency of the firm in generating returns for

its shareholders. In case of bank return ratios are considered to judge its profitability.

4.4.1 Return on asset (ROA)

The Return on Assets ratio is an important profitability ratio because it measures the efficiency

with which the bank is managing its investment in assets and using them to generate profit. It

measures the amount of profit earned relative to the bank's level of investment in total assets.

The return on assets ratio is related to the asset management category of financial ratios.

The calculation for the return on assets ratio is,

Return on Assets = Net Income after Taxes / Total Assets

4.4.2 Return on Equity (ROE)

This ratio indicates how profitable a company is by comparing its net income to its average

shareholders' equity. The return on equity ratio (ROE) measures how much the shareholders

earned for their investment in the company. The higher the ratio percentage, the more efficient

management is in utilizing its equity base and the better return is to investors. The calculation for

the return on assets ratio is,

Return on Equity = Net Income after Taxes / Total Equity Capital Account

Chapter fiveResearch Objectives, Questions,

Hypothesis & Hypotheses

5.1 Objectives of the Study

Evaluating the profitability of selected banks.

Evaluating the liquidity of selected banks.

Evaluating the impact of liquidity measures on profitability of the selected banks

5.2 Research Questions and Hypothesis

The research questions for this study are given below:

1. Is there any significant impact of liquidity on ROA of the selected banks?

2. Is there any significant relationship of liquidity on the ROE of the selected banks?

The following hypotheses have been formulated for the study-

H01: There is no significant impact of independent variables on dependent variable return on

asset (ROA).

HA1: There is a significant impact of independent variables on dependent variable return on asset

(ROA).

H02: There is no significant impact of independent variables on dependent variable return on

equity (ROE).

HA2: There is a significant impact of independent variables on dependent variable return on

equity (ROE).

5.3 Hypotheses

There is no significant impact of independent variables on dependent variable return on

asset (ROA).

There is no significant impact of independent variables on dependent variable return on

equity (ROE).

Chapter Six Findings & Analysis

6.0 Findings & Analysis

6.1 Evaluation of Profitability

The profitability of any business concern can be understood by analyzing the Profit And Loss

Account of that concern. Profit And Loss Account shows the revenue generated, corresponding

expenditure and the resulting profit or loss.

6.1.1 Return on asset

2008 2009 2010 2011 2012

0.700000000000001

1.72 2.22 2.18 1.871.22 1.32

1.86 1.7 1.021.3

2.372.22 2.05

1.241.68000000000

001

2.34

3.192.52

1.321.09

1.66

2.26

1.32

0.950000000000001

ROABAL MBL PBL EBL SEBL

Figure 5- Return on assets of the banks

Analysis: As we know that the Return on Assets ratio is an important profitability ratio because

it measures the efficiency with which the bank is managing its investment in assets and using

them to generate profit. Furthermore, the higher the percentage, the better, because that means

the bank is doing a good job using its assets. In this sense, over the years Bank Asia Limited

grabbed a better position than the previous considering the rise in ROA over the years with

reaching to about 1.87% in 2012 compared to 0.7% in 2008.On the other hand the ROA of

Mercantile Bank Limited, Prime Bank Limited, Eastern Bank Limited and South East Bank

Limited has increased over the year 2008 to 2010 but fell down in 2012 following 2011.

6.1.2 Return on Equity

2008 2009 2010 2011 20127.11 19.61

32.12 32.03 2317.55

18.819.84 17.95

13.4220.58

30.1921.65 20.19

13.5318.64

22.123.61

19.03

14.44

12.08

16.5119.41

10.47

8.42

ROEBAL MBL PBL EBL SEBL

Figure 6– Return on equity of the banks

Analysis: The return on equity ratio (ROE) measures how much the shareholders earned for their

investment in the company. The higher the ratio percentage, the more efficient management is in

utilizing its equity base and the better return is to investors. There was an increase in Return on

Equity for all the five banks over the year 2008 to 2010.The ROE of all the five banks shown a

downfall over the year 2011 to 2012.

6.2 Evaluation of Liquidity

These ratios signify liquidity of a bank since these ratios are important in measuring the ability of

a bank to meet both its short term and long term obligations. Hence a decrease in these ratios

increases liquidity risk of the bank. There are several measures for evaluating liquidity of a bank

appeared as follows:

6.2.1 Loan deposit ratio

2008 2009 2010 2011 2012

94% 92% 92% 87% 84%

88% 83% 88%78% 80%

85% 83% 93%87% 88%

95% 97% 104% 108% 105%

88%80%

88%84% 83%

LDR

SEBLEBLPBLMBLBAL

Axis Title

Figure 7- LDR of the banks

Analysis: From 2008 to 2010, the loan deposit Ratio of Bank Asia Limited and Mercantile Bank

Limited were very high, but it showed a slight downfall in loan deposit ratio in the years 2011

and 2012. So, it is found that Bank Asia Limited & Mercantile Bank Limited is in better

position in terms of LDR now than the previous years because a higher LDR indicates that a

bank takes more financial stress by making excessive loan. From 2008 to 2012 the LDR of Prime

Bank Limited, Eastern Bank Limited and South East Bank Limited was very high. So it is found

that these banks are not in a good position because they have higher loan deposit ratio.

6.2.2 Deposit Asset ratio

2008 2009 2010 2011 2012

79% 79% 82% 81% 78%

88% 88% 87% 88% 86%

79% 86% 81% 80% 77%

76% 70% 69% 64% 62%

85% 86% 81% 80% 90%

DAR

BAL MBL PBL EBL SEBL

Figure 8- DAR ratio of the banks

Analysis: Deposit to asset ratio is calculated from the balance sheet data. From our study, we

observe, Eastern Bank Limited and Prime Bank Limited has shown a declining trend in

deposit asset ratio from 2009 to 2012. The DAR of South East Bank Limited declined from

2009-2011 with a slight increase in 2012. This Bank has low liquidity Risk. Mercantile Bank

Limited and Bank Asia Limited maintained almost constant deposit asset ratio over the five years

while the DAR of Prime Bank Limited has been fluctuating with the least deposit asset ratio in

2012.

6.2.3 Cash Deposit Ratio

2008 2009 2010 2011 2012

10%9% 8% 9%

10%

21%26%

8% 7%10%

10%

10%

9% 9% 10%

18%

21%

15% 16%22%

11%11%

8% 10%

13%

CDRBAL MBL PBL EBL SEBL

Figure 9- CDR ratio of the banks

Analysis: Cash deposit ratio is calculated from the balance sheet data. It determines the bank’s

effectiveness in liquidity management. From our study, we observe, Bank Asia Limited has

shown a downfall in cash deposit ratio from 2009 to 2010 with a slight increase in 2011 and

2012.This Bank has low liquidity Risk. With slight increase in 2009 Mercantile Bank Limited

has shown downfall in CDR from 2010 to 2012 which is very alarming and signifies that the

bank is facing high liquidity risk. Prime Bank Limited has shown a downfall from 2010 to 2011

with a slight increase in 2012.This bank has low liquidity risk. Eastern Bank Limited has shown

downfall from 2010 to 2011 but the CDR increased in 2012.It signifies that the bank has low

liquidity risk. South East Bank has shown downfall from 2010 to 2011 with a slight increase in

2012.It has low liquidity risk.

6.3 Impact of liquidity on profitability

The dependent variable, ROA and ROE of the banks over the past five years are shown in table

10 and 11. The tables 12-14 show all the independent variables, Loan-Deposit ratio, Deposit-

Asset ratio, Cash-Deposit ratio respectively, of the banks over 2008-2012. The averages of all

the dependent and independent variables are shown in table 15 in the Appendix. These ratios are

used to examine correlation and to conduct regression analysis to show the impact of Liquidity

on Profitability of the five selected banks.

6.3.1 Descriptive Analysis

Variables N Minimum Maximum Range Mean Std. Dev. Variance

ROA 5 1.2 2.35 1.15 1.75 0.47 0.22

ROE 5 14.56 23.33 8.77 18.92 3.83 14.69

LTD 5 0.86 0.93 0.07 0.89 0.03 0.0009

DTA 5 0.79 0.86 0.07 0.82 0.03 0.0009

CTD 5 0.10 0.15 0.05 0.12 0.03 0.0009

Table 4: Descriptive Statistics of the variables.

Table 4 shows descriptive statistics for the dependent and independent variables. It illustrates the

maximum and minimum, mean, standard deviation and variance values of the dependent and

independent variables over the years under observation. The descriptive statistics reveal that the

average of the profitability ratios, ROA and ROE, are 1.75 and 18.92 respectively. The means of

the liquidity measures Loan Deposit ratio, Deposit Asset ratio and Cash Deposit ratio are 0.89,

0.82 and 0.12 respectively, which is much lower than the averages of the profitability. Similarly,

the standard deviation and variance values of profitability ratios are also found to be higher than

those of the liquidity measures. Therefore, it can be concluded that profitability is more volatile

than liquidity measures.

6.3.2 Correlation Analysis

Table 5 indicates the correlation between the dependent variables with the various independent

used in the study. As it is shown in the table, the correlation values are found to be both positive

and negative between the independent and dependent variables.

Variables ROA ROE LDR DAR CDR

ROA 1

ROE 0.96**0.01

1

LDR 0.540.35

0.530.36

1

DAR -0.670.27

-0.670.21

-0.690.20

1

CDR -0.320.60

-0.030.96

-0.210.74

-0.020.97

1

** Correlation is significant at the 0.01 level (2-tailed).Pearson Correlation Sig. (Two- tailed)

Table 5: Correlation Matrix

The R values are found to be positive between loan to deposit ratio and both the profitability

ratios, ROA and ROE (0.54 and 0.53 with ROA and ROE respectively). However, the R value of

deposit asset ratio is negative with ROA and ROE and it is -0.67 in both the cases. The R values

between cash asset ratio and ROA and ROE are -0.32 and -0.03 respectively, hence it is also

found to be negative. Therefore, there is a moderate positive correlation between loan deposit

ratio with ROA and ROE while there is a moderate negative correlation between deposit asset

ratio and profitability ratios, ROA and ROE respectively. There is a weak negative correlation

between cash deposit ratio and the profitability ratios. It can also be concluded that all the

correlations between the liquidity ratios and profitability ratios are statistically insignificant at

0.01 level.

Therefore, both the null hypotheses are accepted and the alternate hypotheses are rejected. That

is, there is no significant correlation between the liquidity ratios with ROA and ROE.

6.3.3 Regression Results

Regression analysis of ROA

To examine the research hypotheses SPSS program is used to conduct simple regression

analysis. Following tables reports the result of simple regression analysis of the independent

variables with ROA.

Regression on Return on Assets

Variable B SE B β Sig. R SquareLTD 0.65 17.90 0.04 0.98 0.50DTA -6.46 17.25 -0.37 0.77CTD -8.35 18.14 -0.41 0.73

Table 6: Regression analysis (Return on Assets)

ANOVA (Return on Assets)

Source Sum of Squares Degree of freedom

Mean of Square

F-statistics

Significance

Regression

Residual

Total

0.43

0.45

0.88

3

1

4

0.14

0.45

0.85 0.83

Table 7- Analysis of Variance

Here in table 6 ROA is dependent variable and Loan to deposit ratio, Deposit to Asset ratio and

Cash to Deposit ratio are independent variables. The table shows that deposit to asset ratio and

cash to deposit ratio are negatively associated with ROA whereas Loan to Deposit Ratio is

positively associated with ROA. At 10% level of significance the association between ROA and

independent variables – Loan Deposit ratio, Deposit Asset ratio and Cash Deposit ratio is

statistically insignificant that indicates the independent variables have no significant impact on

ROA.

The coefficient of determination reported in Table 6 by R-square indicates that 50% of the

changes in ROA can be explained by the independent variables.

Table 7 reports the results of ANOVA. The data indicates that at 10% level of significance, the

regression model as whole is found to be insignificant. The reason for the regression model to be

statistically insignificant could be use of limited data on only five banks and for five years. We

can also find that the value of F (0.85) is not significant, at α=5% and this does not support the

alternate hypothesis. Therefore, the liquidity of the selected banks in Bangladesh has no

significant influence on the profitability of the banks. There is no significant impact of

independent variables, Loan Deposit ratio, Deposit Asset ratio, and Cash Deposit ratio on the

dependent variable return on asset (ROA). Therefore, the first null hypothesis is accepted.

Regression analysis of ROE

Following tables reports the result of simple regression analysis of the independent variables

with ROE.

Regression on Return on Equity

Variable B SE B Β Sig. R Square

LTD 12.84 152.81 0.09 0.95 0.46

DTA -82.31 147.25 -0.58 0.68

CTD -10.69 154.85 -0.06 0.96

Table 8- Regression analysis (Return on Equity)

ANOVA (Return on Equity)Source Sum of Squares Degree of

FreedomMean Square F-Statistics Significance

Regression

Residual

Total

27.06

31.71

58.77

3

1

4

9.02

31.71

0.38 0.84

Table 9- Analysis of Variance

Here in table 8 ROE is dependent variable and Loan deposit ratio, Deposit Asset ratio and Cash

Deposit ratio are independent variables. The tables show that deposit asset ratio and cash deposit

ratio are negatively associated with ROE whereas Loan to Deposit Ratio is positively associated

with ROE. At 10% level of significance the association between ROE and independent variables

– Loan Deposit ratio, Deposit Asset ratio and Cash Deposit ratio is statistically insignificant that

indicates the independent variables have no significant impact on ROE.

The coefficient of determination reported in Table 8 by R-square indicates that 46% of the

changes in ROE can be explained by the independent variables.

Table 9 reports the results of ANOVA. The data indicates that at 10% level of significance, the

regression model as whole is found to be insignificant. The reason for the regression model to be

statistically insignificant could be use of limited data on only five years over a period of five

years. The result also shows that the value of F (0.38) is insignificant, at α=5%. Hence, the

independent variables do not have impact of the return on equity as well. Therefore, the second

null hypothesis is also accepted.

.

Chapter Seven

Conclusion

7.0 Conclusion

This study had attempted to investigate the impact of liquidity and profitability of the private

commercial banks in Bangladesh by focusing on certain ratios over a period of five years. Five

private commercial banks have been selected to undertake the research. Liquidity and

profitability in private commercial banks are two sensitive issues in the operations of the banks

and the information on these two are seriously hoarded. Consequently, a study on these two

issues is quite difficult. However, the major concern of this study was to figure out if the amount

of liquidity maintained by the banks effect their profitability as these two issues are much

important to the main stakeholders of the banks. The shareholders desire maximum profitability

as a return on their investment, while the depositors opt for a maximum liquidity as a guarantee

for safety and ability to pay their money on demand. The research carried out several analyses to

test the impacts of the variables and found that there is no significant relationship. The

correlation values have been found to be negative between return on assets and return on equity

with cash to deposit ratio and deposit to asset ratio respectively. But the correlation between

ROA and ROE with loan to deposit ratio has been found positive according to the correlation

matrix. The simple regression test was conducted to test the hypotheses. The test also showed

that the liquid ratios are negatively correlated with all the profitability measures. Hence, null

hypothesis is accepted and alternate hypothesis is rejected. That is, there is no significant

relationship between liquidity and profitability among the selected banks. That means that

profitability in the banks is not significantly influenced by liquidity maintained and vice versa.

Bibliography

I. Adrian, T. & Shin, H. S. (2009) “Money, Liquidity, and Monetary Policy,” American

Economic Review, vol. 99(2), p. 600-605

II. Amengor, E. C. (2010). Importance of Liquidity and Capital Adequacy to Commercial

Banks”. A Paper Presented at Induction Ceremony of ACCE, UCC Campus, 14 (2), 49-58.

III. Annual Report (2008-2012) of Mercantile Bank Limited

IV. Annual Report (2008-2012) of Bank Asia Limited

V. Annual Report (2008-2012) of Prime Bank Limited

VI. Annual Report (2008-2012) of Eastern Limited

VII. Annual Repot (2008-2012) of South East Bank Limited

VIII. Annual Report 2008-2012, Bangladesh Bank, Dhaka.

IX. Bourke, P., (1989), "Concentration and other Determinants of Bank Profitability in

Europe". Journal of Banking and Finance, pp65-80.

X. Dietrich, D., & Vollmer, U. (2010) “International Banking and Liquidity Allocation:

Cross-border Financial Services vs. Multinational Banking,” Journal of Financial Services

Research, vol. 37, p.45-69.

XI. Eichengreen, B. and H.D. Gibson (2001). “Greek banking at the dawn of the new

millennium.” CERP Discussion Paper 2791.

XII. Eljelly, A. (2004). Liquidity – profitability tradeoff: an empirical investigation in an

emerging market. IJCM, 14 (2), 48-61.

XIII. Goddard, J., Molyneux, P. & J.O.S. Wilson (2004). "Dynamics of Growth and Profitability

in Banking," Journal of Money, Credit and Banking 36, 1069-1090.

XIV. Islam, M. Muzahidul (2008). Liquidity Management. Text Book on Islamic Banking, 2nd

Edition,November, pp.101-111. Dhaka (Bangladesh): Islamic Economics Research

Bureau.

XV. Lartey V., Antwi1 S., Boadi E. (2013), “The Relationship between Liquidity and

Profitability of Listed Banks in Ghana.”International Journal of Business and Social

Science, Vol. 4 No. 3; PP. 71-86.

XVI. Molyneux, P. & J. Thornton (1992), “Determinants of European Bank Profitability: A

Note,” Journal of Banking and Finance, Vol. 16, No. 6, pp. 209-19.

XVII. Pimentel, R. C., Braga, R., & Casa Nova, S. P. C. (2005). Interação entre rentabilidade e

liquidez: um estudo exploratório. Revista de Contabilidade do Mestrado em Ciências

Contábeis da UERJ, Rio de Janeiro – 10 (2), PP. 83-98.

XVIII. Rose, Peter S. (2004-2005). Commercial Bank Management, pp.149-198. U.S.A:

Irwin/McGraw-Hill Companies.

XIX. Shahchera, Mahshid (2012). The Impact of Liquidity Asset on Iranian Bank Profitability.

International Conference on Management, Behavioral Sciences and Economics Issues

(ICMBSE'2012), pp. 131-135. Penang, Malaysia.

XX. Uremadu S. (2012), “Bank Capital Structure, Liquidity and Profitability Evidence from the

Nigerian Banking System.” International Journal of Academic Research in Accounting,

Finance and Management Sciences, Volume 2, Issue 1 (2012) ISSN: 2225-8329.

Appendix

Table 10– ROA of the banksBanks 2008 2009 2010 2011 2012Bank Asia 0.70 1.72 2.22 2.18 1.87Mercantile Bank

1.22 1.32 1.86 1.70 1.02

Prime Bank 1.30 2.37 2.22 2.05 1.24EBL 1.68 2.34 3.19 2.52 1.72Southeast Bank 1.09 1.66 2.26 1.32 0.95

Table 11- ROE of the banksBanks 2008 2009 2010 2011 2012Bank Asia 7.11 19.61 32.12 32.03 23.00

Mercantile Bank

17.75 18.80 19.84 17.95 13.42

Prime Bank 20.58 30.19 21.65 20.19 13.53EBL 18.64 22.10 23.61 19.03 14.44Southeast Bank 12.08 16.51 19.41 10.47 8.42

Table 12- Loan to Deposit Ratio of the banksBanks 2008 2009 2010 2011 2012Bank Asia 0.94 0.916 0.92 0.87 0.84Mercantile Bank 0.88 0.83 0.88 0.78 0.71Prime Bank 0.85 0.83 0.93 0.87 0.88EBL 0.95 0.97 1.04 1.08 1.05Southeast Bank 0.88 0.80 0.88 0.84 0.83

Table 13: Deposit to Asset Ratio of the banksBanks 2008 2009 2010 2011 2012Bank Asia 0.79 0.79 0.82 0.81 0.78Mercantile Bank

0.88 0.88 0.87 0.88 0.86

Prime Bank 0.79 0.86 0.81 0.80 0.77EBL 0.76 0.70 0.69 0.64 0.62Southeast Bank 0.85 0.86 0.81 0.80 0.90

Table 14- Cash and Equivalent to Deposit Ratio of the banksBanks 2008 2009 2010 2011 2012Bank Asia 0.10 0.09 0.08 0.09 0.10Mercantile Bank

0.21 0.26 0.08 0.07 0.10

Prime Bank 0.10 0.10 0.09 0.09 0.10EBL 0.18 0.21 0.15 0.16 0.22Southeast Bank 0.11 0.11 0.08 0.10 0.13

Table 15- Average value of all the variablesRatios 2008 2009 2010 2011 2012Average ROA 1.198 1.882 2.35 1.954 1.36Average ROE 15.323 21.442 23.326 19.934 14.562Average LDR 0.9 0.869 0.93 0.888 0.862Average DAR 0.814 0.818 0.80 0.786 0.862Average CDR 0.14 0.15 0.10 0.10 0.13