The Impact of Firm Size and Market Size Asymmetries on ...

40

THE IMPACT OF FIRM SIZE AND MARKET SIZE ASYMMETRIES ON NATIONAL MERGERS IN A THREE-COUNTRY MODEL * Luís Santos-Pinto † Faculdade de Economia - Universidade Nova de Lisboa March 2008 Abstract This paper studies incentives for national mergers in a three-country partial equilibrium model where firms and markets may have different sizes. The paper finds that if firm size asymmetries are sufficiently high or firm size asymmetries are small and the third-country market is much larger than home, then there is no conflict of interest between national firms and governments since all of them are in favor of the creation of a national champion. However, if firm size asymmetries are small or moderate and the third- country market is not much larger than home, then firms wish to merge but governments oppose mergers. Keywords: Mergers, International trade, Merger policy, Size asymmetry. JEL Codes: F13, H77, L11, L41. * I am thankful to Eileen Fumagalli, Peter Neary, Helder Vasconcelos, and Pedro Pita Barros for helpful comments and suggestions. I am also thankful to Tiago Pires and João Jalles for excellent research assistance. † Universidade Nova de Lisboa, Faculdade de Economia, Campus de Campolide, PT-1099-032, Lisboa, Portugal. Ph: +351-213801640. Fax: +351-213870933. E-mail address: [email protected].

Transcript of The Impact of Firm Size and Market Size Asymmetries on ...

THE IMPACT OF FIRM SIZE AND MARKET SIZE ASYMMETRIES ON NATIONAL MERGERS IN A THREE-COUNTRY MODEL *

Luís Santos-Pinto†

Faculdade de Economia - Universidade Nova de Lisboa

March 2008

Abstract

This paper studies incentives for national mergers in a three-country partial equilibrium model where firms and markets may have different sizes. The paper finds that if firm size asymmetries are sufficiently high or firm size asymmetries are small and the third-country market is much larger than home, then there is no conflict of interest between national firms and governments since all of them are in favor of the creation of a national champion. However, if firm size asymmetries are small or moderate and the third-country market is not much larger than home, then firms wish to merge but governments oppose mergers.

Keywords: Mergers, International trade, Merger policy, Size asymmetry.

JEL Codes: F13, H77, L11, L41.

* I am thankful to Eileen Fumagalli, Peter Neary, Helder Vasconcelos, and Pedro Pita Barros for helpful comments and suggestions. I am also thankful to Tiago Pires and João Jalles for excellent research assistance. † Universidade Nova de Lisboa, Faculdade de Economia, Campus de Campolide, PT-1099-032, Lisboa, Portugal. Ph: +351-213801640. Fax:+351-213870933. E-mail address: [email protected].

28 Luís Santos-Pinto

1. Introduction

In many European countries there is a heated debate over whether governments and competition authorities

should favor or oppose the creation of national champions.1 An argument often put forth in favor of national

champions is that bigger firms will be in a better position to compete against foreign firms in world markets.2 A

merger of domestic firms can improve national welfare if it increases the market share of domestic firms in

world markets and/or raises prices for consumers in world markets.

This paper contributes to this debate by setting up a simple open economy model with firm size

asymmetries, market size asymmetries, and cost reductions due to mergers. The model is used to make

comparisons between endogenous mergers and mergers that improve national welfare.

The paper considers a partial equilibrium model where competitors in each of two countries, home and

foreign, serve their respective domestic markets, and all firms compete jointly in a third (world) market.3 The

main novelty, by comparison with the existing literature on three-country models of mergers, is that this model

allows for both firm size as well as market size asymmetries. Firm size asymmetries are modeled as different

marginal costs for firms in each country. Market size asymmetries are modeled as different demand curves in

home, foreign and the third-country. Home is assumed to be the small country in that, for any given price,

demand in foreign and in the third-country is larger than demand in home. As is standard in the literature firms

compete à la Cournot and markets are segmented.

The paper starts by providing conditions under which a merger of domestic firms is profitable conditional on

a given market structure in foreign. The paper shows that this happens if either (i) firm size asymmetries are

sufficiently large or (i) firm size asymmetries are small and the domestic market is not much smaller than the

third-country market. The intuition for this result is straightforward. A merger leads to less competition in the

domestic market and in the third-country market, therefore the market power of the firms involved in the merger

increases in these two markets. This allows firms to raise mark-ups since the less efficient firm that takes part in

the merger transfers production to the most efficient firm. This effect creates an incentive for mergers to take

place. However, in the third-country the merger implies that the market share of the merged firm is lower than

the sum of the pre-merger market shares of the firms involved in the merger. This effect reduces the incentive for

1. For example, the French government advocated a merger between the electricity and gas company SUEZ with the firm GAZ DE FRANCE. 2. A recent example in Germany has been the aproval of the merger between the E.ON and RUHRGAS corporations where the German Minister of Economics argued that size was very important at the onset of the energy market liberalization in Europe. 3. A partial equilibrium analysis assumes that the sector in question is very very small and therefore has little if any impact on other sectors of the economy.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 29

mergers to occur. Thus, in this model a merger always increases profits in domestic markets whereas it may or

may not increase profits in the third-country market.

The above conditions are used to characterize the set of Nash equilibria of the merger game played by

domestic and foreign firms. The paper shows that for most firm and market size parameter configurations the

merger game played by firms has a unique pure strategy Nash equilibrium where mergers take place in home and

in foreign. Only if firm size asymmetries are small and the size of the third-country market is relatively large will

the merger game played by firms have a unique pure strategy Nash equilibrium where no mergers take place in

both countries. For a small set of firm and market size configurations the merger game played by firms has

multiple equilibria.

Next the paper provides conditions under which a merger in one of the countries improves that country's

welfare for a given market structure in the other country. These conditions are used to characterize the set of

Nash equilibria of the merger game played by national governments. The paper finds that governments prefer not

to merge national firms when firm size asymmetries are (i) small or (ii) moderate and the size of the third-

country market is not much larger than the home market. However, governments prefer to merge national firms

when firm size asymmetries are (i) high or (ii) moderate-high and the size of the third-country market is much

larger than the home market. There is also a set of firm and market size configurations where the merger game

played by governments has multiple equilibria.

In a final step the paper explains when will firms and governments interests regarding the desirability of

national mergers be aligned or in conflict. The paper finds that if firm size asymmetries are sufficiently high,

then there is no conflict of interest between national firms and governments: all favor the creation of a national

champion. The interests of national firms and governments are also aligned if firm size asymmetries are small

and the third-country market is much larger than home: all oppose the creation of a national champion. However,

if firm size asymmetries are small or moderate and the third-country market is not much larger than home, then a

conflict of interest arises between national firms and governments: firms wish to merge but governments oppose

the merger.

The questions that this paper addresses have many links with the existing literature on merger and

competition policy, specially with papers which extend the analysis to the context of open economies.4 This

literature has taken two different routes. A first set of papers focuses on nationally optimal merger policies and

merger profitability when trade policy instruments are available to national governments--e.g., Richardson

4. The traditional analysis of mergers and acquisitions in industrial organization--Salant et al. (1983) and Deneckere and Davidson (1985)--usually neglects the effects of country borders.

30 Luís Santos-Pinto

(1999), Horn and Levinsohn (2001), and Huck and Conrad (2004). A second line of research is based on the

concept of ``external effects'' of a merger to outsiders. An important early contribution to this topic is Farrel and

Shapiro (1990). This concept was extended to open economies by Barros and Cabral (1994). This literature has

derived rather general conditions under which a merger benefits, or harms, the parties not participating in the

merger. It does not, however, explicitly consider that a merger may lead to cost reductions and so it can not

provide a complete characterization of post-merger equilibrium.

This paper also has links to the recent literature on merger waves. Qiu and Zhou (2007) attempt to model

endogenous mergers more completely, assuming an arbitrary number of heterogeneous firms which differs in

their marginal costs and Cournot competition. They endogenize the order of mergers and consider that firms

choose independently whether, when and whom they merge. Qiu and Zhou (2007) show that mergers are

efficient since firms surviving the mergers are the most efficient firms in the industry. They demonstrate that

some mergers are strategic and occur in waves.

Suedekum (2006) analyzes the profitability of mergers in a model with symmetric firms and trade between

all countries but with iceberg transport costs. Suedekum uses this framework to study the profitability and social

desirability of national versus international mergers. He finds that national mergers can have a negative impact in

world surplus, and so national competition policy can be seen as too permissive. However, the promotion of

national mergers can be in the interest of individual countries if rent extraction possibilities are strong enough.

He also shows that cross-border mergers are more attractive than domestic mergers.

Haufler and Nielsen (2005) is the paper that is most closely related to this one. Like here, they also consider

a three-country model where firms of two countries serve their respective domestic market and a third market.

By contrast to this paper, Haufler and Nielsen assume that firms are symmetric and that a merger creates

synergies which imply a reduction of marginal cost.

The remainder of the paper is organized as follows. Section 2 sets-up the model. Section 3 analyses

conditions under which a merger in one country, conditional on a given market structure in the other country, is

in the interest of the merging firms. Section 4 describes the set of equilibria of the simultaneous move merger

game played by firms. Section 5 analysis conditions under which a merger in one country, conditional on a given

market structure in the other country, increases national welfare. Section 6 describes the set of equilibria of the

simultaneous move game played by governments. Section 7 states conditions under which firms and

governments interests regarding the desirability of national mergers are aligned or in conflict. Section 8

discusses possible extensions of the model. Section 9 illustrates the model by applying it to the cement, mobile

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 31

telecommunications, and fuel industries of Portugal and Spain. Section 10 concludes the paper. The Appendix

contains the proofs of propositions.

2. Set-up

Consider three countries: home, foreign and a third-country (or the rest of the world). Before any merger

takes place there are 2 firms in home and 2 firms in foreign. Firms in each country sell in domestic markets and

there is no bilateral trade between home and foreign. However, home and foreign firms compete in the third-

country market.5

Home and foreign firms are fully owned by residents and produce a homogeneous good. The inverse

demand function in the home country is given by Ph a Qh , with a 1 while the inverse demand

function in foreign is Pf a Qf, with 0,1 . The inverse demand function in the third-country is

P3 a Q3 , with 0, 1 . The previous assumptions imply that, for any given price, demand in the

home market is smaller than or equal to demand in foreign and in the third-country markets.6 Marginal costs are

assumed to be nonnegative and constant. We also assume that there are no fixed costs (this rules out gains from

economies of scale in mergers). Marginal costs of firms are given by cl1 c, cl2 c , where

l h, f and 0, a c /3 . The parameter is an index of cost asymmetry. If 0 all firms

have the same cost. We assume that must be smaller than or equal to a c /3 so that, in the absence of

mergers, even the less efficient firm makes nonnegative profits in all markets. It is useful to define

/ a c and use it as a summary measure of asymmetry.

Following Barros (1998) we assume that when a merger between two firms occurs the less efficient firm

ceases production.7 Because marginal costs are constant, when two firms merge the merged entity will shut

down the high-cost unit and use only the low-cost unit for production. Let i j stand for the merger between

5. Transportation costs between home and the third-country and between foreign and the third country are assumed to be equal to zero.

Transportation cost for third-contry market can be greater than zero (but lower than a ) without changing qualitatively the results in the paper. 6. Normalization of demand for home simplifies the problem and does not change qualitatively the results. 7. Barros (1998) proposes a framework with three asymmetric firms and where mergers are endogenously determined. He tries in this way to explain the intuition behind the relationship between initial market concentration and size asymmetry of firms, showing that a negative relation should be expected.

32 Luís Santos-Pinto

firms i and j . Then, the merged entity's marginal cost is equal to min ci, cj . Therefore, a merger can be

viewed as an acquisition of a high-cost firm by a low-cost firm.8

Firms compete in each market à la Cournot, that is, each firm chooses noncooperatively and simultaneously

the quantity that maximizes its individual profit.9 Each firm sees the markets it serves as segmented, that is, it is

responsible for the choice of how much to produce in each market and it considers not just the output of other

firms but their own choices about where to produce that output as unaffected by its actions. Thus, firms play

separate Cournot games in each market as they take as given the output of each rival in each market and not the

total output of each rival in all markets. This means that each market can be analyzed independently of the other

markets.

The starting point of the analysis is a situation where no merger has yet taken place. So, at the start, the

problem of home firm i is given by

maxq hi;q hi

a Qh chi qih a Q chi qhi,

where the quantities with an asterisk are sold in the third-country. The first-order conditions to this problem

are

a 2qhij i

qhj chi 0.

a 2 qhij i

qhjk

q ,fk chi 0.

Solving the first equation with respect to qhi we obtain the best reply of domestic firm i in the domestic

market

qhia chi

212 j i

qhj.

Solving the second equation with respect to qhi we obtain the best reply of home firm i in the third-

country market

8. Barros (1998) approach also used by Qiu and Zhou (2007). However, Perry and Porter (1985) and Farrell and Shapiro (1990) use different approaches to model the impact of a merger on an industry's cost structure. 9. The assumption of Cournot competition is in line with much of the literature on mergers. Theoretical and empirical arguments in defence of the Cournot model are presented by Haufler and Nielsen (2005). The model proposed by Kreps and Sheinkman (1983) in which firms choose in capacities in the first period and compete in prices in the second period generates Cournot outcomes.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 33

qhia chi

212 j i

qhjk

qfk .

Similarly, at the start, the problem of foreign firm i is given by

maxq fi,q fi

a Qf cfi qfi a Q cfi qfi,

The first-order conditions to this problem are given by

a 2 qfij i

qfj cfi 0

a 2 qfij i

qfjk

qhk cfi 0

Thus, the best reply of foreign firm i in the foreign market is

qfia cfi

212 j i

qfj,

and the best reply of foreign firm i in the third-country market is

qfia cfi

212 j i

qfjk

qhk .

This set-up captures the idea that domestic markets are less competitive than the third-country market (or

rest of the world).

3. Profitability of Conditional Mergers

In this section we characterize the conditions under which a merger in one of the countries is profitable for a

given market structure in the other country. We start by proving conditions under which a domestic merger is

profitable conditional on a given market structure in foreign.

If home firms are not merged they sell qh1 a c /3 and qh2 a c 2 /3 in the home

market. In this case, profits of home firms in the home market are given by h1h a c 2 /9 and

34 Luís Santos-Pinto

h2h a c 2 2/9. If foreign firms are not merged they sell qf1 a c /3 and

qf2 a c 2 /3 in the foreign market. Profits of foreign firms in the foreign market are

f1f a c 2 /9 and f2

f a c 2 2/9 . The market equilibrium in the third-country

market is given by:

qh1a c2

12 qh2 qf1 qf2

qh2a c

212 qh1 qf1 qf2

qf1a c2

12 qh1 qh2 qf2

qf2a c

212 qh1 qh2 qf1

Solving this system we obtain qh1 qf1 a c 2 /5 and qh2 qf2 a c 3 /5 .

The profits of home and foreign firms in the third-county market are given by

h1 f1 a c 2 2/25 and h2 f2 a c 3 2/25 .

If home firms merge the home market becomes a monopoly and the equilibrium quantity is

qh 1 h 2 a c /2. The monopoly profits are h1 h2h a c 2 /4. If home firms merge and foreign

firms are not merged, then the equilibrium in the third-country market is given by

qh1 h2a c2

12 qf1 qf2

qf1a c2

12 qh1 h2 qf2

qf2a c

212 qh1 h2 qf1

Solving this system we obtain qh1 h2 qf1 a c /4 and qf2 a c 3 /4 . The

profits of the merged home firm in the third-country market are h1 h2 a c 2 /16 . A merger of

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 35

home firms is profitable when foreign firms are not merged if the total profits of the merged home firm are

greater than the sum of the profits of the home firms before the merger, that is,

a c 2

4a c 2

16a c 2

9a c 2 2

9a c 2 2

25a c 3 2

25 . (1)

If home firms are not merged but foreign firms are the equilibrium in the third-country market is given by

qh1a c2

12 qh2 qf1 f2

qh2a c

212 qh1 qf1 f2

qf1 f2a c2

12 qh1 qh2

The solution to this system is qf1 f2 qh1 a c /4 and qh2 a c 3 /4 . The

profits of h1 in the third-country market are h1 a c 2 /16 and the profits of h2 are

h2 a c 3 2/16 . If home firms merge and so do foreign firms we have a duopoly in the third-

country market. In this case the equilibrium quantities in the third-country market are

qh1 h2 qf1 f2 a c /3 and profits of the merged home firm by h1 h2 a c 2 /9 . Thus, a

merger of home firms is profitable when foreign firms are merged if

a c 2

4a c 2

9a c 2

9a c 2

16a c 2 2

9a c 3 2

16 . (2)

We use conditions (1) and (2) to state our first result.

36 Luís Santos-Pinto

Proposition 1:

(i) A merger of domestic firms is profitable when foreign firms are not merged if either (a) 0, 761

and hf1,f2 ,1 , with h

f1,f2 63100

7 82 183 2

7 56 140 2 or (b)7

61 , 13 .

(ii) A merger of domestic firms is profitable when foreign firms are merged if either (a) 0, 115 and

hf1 f2 , 1 , with h

f1 f2 50100

1 18 45 2

1 8 20 2 or (b)1

15 , 13 .

Proposition 1 part (i) tells us that when firm size asymmetries are sufficiently high a merger of home firms is

profitable when foreign firms are not merged. However, when firm size asymmetries are small, a merger of

home firms when foreign firms are not merged is only profitable if the third-country market is not too large by

comparison to home. The intuition for this result is as follows. The merger always raises profits in the home

market since it implies moving from a duopoly to a monopoly. However, the impact of the merger on profits in

the third-country market may be favorable or unfavorable to home firms depending on the size of firm size

asymmetries.10 If firm size asymmetries are large enough the merger raises profits in the third-country market.

This happens because large firm size asymmetries imply a large efficiency gain which raises mark-ups (the

difference between price and marginal cost) enough to make up for the loss of market share. By contrast, if firm

size asymmetries are small, a merger of home firms reduces profits in the third-country market. In this case, a

merger of home firms is only profitable if the gains in home are bigger than the losses in the third-country

market. For this to happen the third-country market must be not be excessively large by comparison to home.

Proposition 1 part (ii) says that a merger of home firms is profitable when foreign firms are merged if either

firm size asymmetries are high or firm size asymmetries are low but the third-country market is not much larger

than the home market. Comparing part (i) to (ii) of Proposition 1 we see that a domestic merger is profitable

under less restrictive conditions when foreign firms have merged than when they have not merged.11 This

happens because the gain from a domestic merger in the third-country market is larger when foreign firms are

merged than when foreign firms are not merged. When foreign firms are not merged and domestic firms merge

there is a move from four to three firms in the third-country market. By contrast, when foreign firms are merged

and domestic firms merge there is a move from three to two firms in the third-country market. A move from

10. The merger leads to gains in the home market for any [ ]0,1/ 3δ ∈ . The merger only leads to gains in the third country market if 7 / 61.δ >

11. The set [ ]1 115 3, contains the set [ ]7 1

61 3, and 1 2 1, 2f f f fh hβ β+ ≤ in the relevant range of parameters.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 37

three to two firms has associated a larger increase in mark-ups and a smaller loss of market share for domestic

firms than a move from four to three firms.

We now provide conditions under which a foreign merger is profitable conditional on a given market

structure in home. A merger of foreign is profitable when home firms are not merged if

a c 2

4a c 2

16a c 2

9a c 2 2

25a c 2 2

9a c 3 2

25 . (3)

A merger of foreign firms is profitable when home firms are merged if

a c 2

4a c 2

9a c 2

9a c 2

16a c 2 2

9a c 3 2

16 . (4)

We use conditions (3) and (4) to state the following result.

Proposition 2:

(i) A merger of foreign firms is profitable when domestic firms are not merged if either (a) 0, 761

and fh1,h2 , 1 , with f

h1,h2 63100

7 82 183 2

7 56 140 2 or (b)7

61 , 13 .

(ii) A merger of foreign firms is profitable when domestic firms are merged if either (a) 0, 115 and

fh1 h2 ,1 , with f

h1 h2 50100

1 18 45 2

1 8 20 2 or (b)1

15 , 13 .

Proposition 2 provides conditions under which a foreign merger is profitable when domestic firms are not

merged-part (i)-and when domestic firms are merged-part (ii). The intuition is the same as the one behind

Proposition 1. The only difference here is that if firm size asymmetries are small and the foreign market is larger

than home, then the conditions for a foreign merger to be profitable are less restrictive. Recall that for small firm

size asymmetries a merger of domestic firms implies a gain in the domestic market and a loss in the third-

country market. If the market in foreign is larger than the home market, then, for any given size of the third-

38 Luís Santos-Pinto

country market, the gain in the foreign market of a merger of foreign firms is greater than the gain in the home

market of a merger of home firms. In short, this result shows that when two countries compete in a third-country

market, mergers are more attractive for firms in the country with the largest domestic market.

4. Merger Game Played by Firms

We will now characterize the equilibrium decisions of home and foreign firms assuming that governments

do not interfere in markets. Later on we will analyze the opposite scenario, where governments decide whether

firms merge or not and firms play no role in merger decisions.

At the start we assume that no merger has taken place in either country. Home firms decide jointly whether

they wish to merge or not. Foreign firms also decide jointly if they wish to merge or not. The joint decisions of

home and foreign firms are taken simultaneously. This means we have a simultaneous move game where we can

use the Nash equilibrium concept to make predictions about behavior.

Let the generic merger game played by firms be denoted by Fn, where n is the number of firms in each

country. The relevant payoffs of F2, are summarized in Table I for the two strategies of merge, M, and not

merge N . The upper left part of each cell in Table I displays the profits of the merged home firm (when home

firms choose to merge) or the sum of profits of the two home firms (when home firms choose not to merge) for

each of the two possible market configurations in foreign. The lower right part of each cell displays the profits of

the merged foreign firm (when foreign firms choose to merge) or the sum of profits of the two foreign firms

(when foreign firms choose not to merge) for each of the two possible market configurations in home.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 39

h \ f M N

M

a c 2

4

a c 2

9 ,

a c 2

4

a c 2

9

a c 2

4

a c 2

16 ,

a c 2 a c 2 2

9

a c 2 a c 3 2

16

N

a c 2 a c 2 2

9

a c 2 a c 3 2

16 ,

a c 2

4

a c 2

16

a c 2 a c 2 2

9

a c 2 2 a c 3 2

25 ,

a c 2 a c 2 2

9

a c 2 2 a c 3 2

25

Table I

The next result characterizes the set of Nash equilibria of F2, when home and foreign markets have the

same size, that is, 1 . In this case the game is symmetric with hf1 f2

fh1 h2

M

hf1,f2

fh1,h2

N .

Proposition 3:

(i) If 0, 115 and 0, M , then NE F2,1 N,N .

(ii) If 0, 115 and M, N , then NE F2,1 M, M , N, N , p,p , with

p 63 100 738 800 1647 2000 2

13 162 603 2 .

(iii) If 0, 115 and N, 1 , then NE F2,1 M, M .

40 Luís Santos-Pinto

(iv) If1

15 , 761 and 0, N , then NE F2,1 M, M , N, N , p,p .

(v) If1

15 , 761 and N, 1 , then NE F2,1 M, M .

(vi) If7

61 , 13 , then NE F2,1 M, M .

This result tells us that if firm size asymmetries between firms are small, 0, 115 , then the set of

Nash equilibria of F2,1 depends on the size of the third-country market. If the size of the third-country market

is much larger than the home market, 0, M , then F2,1 has a unique pure strategy Nash equilibrium

(PSNE from now on) where home firms and foreign firms do not merge. For small firm size asymmetries and a

large third-country market, the profit gains in the home market are less than the losses in the third-country

market and so the merger is not profitable. However, if firm size asymmetries are small and the size of the third-

country market is moderately larger than the home market, M, N , then F2,1 has two PSNE and

one mixed strategy Nash equilibrium (MSNE from now on) where firms in each country merge with probability

p . If firm size asymmetries are small but the size of the third-country market is not much larger than the home

market, N, 1 , then F2,1 has a unique PSNE where mergers take place in home and in foreign.

Proposition 3 also tells us that if firm size asymmetries between firms are moderate, 1

15 , 761 , then

we may have two situations. If the size of the third-country market is sufficiently larger than the home market,

0, N , then F2,1 has two PSNE and one MSNE where firms in each country merge with probability

p . However, if the size of the third-country market is not sufficiently larger than the home market, then F2,1

has a unique PSNE where mergers take place in home as well as in foreign. Finally, Proposition 3 tells us that if

firm size asymmetries are large, 7

61 , 13 , then F2,1 has a unique PSNE where mergers take place in

home as well as in foreign. This happens no matter the size of the third-country market. These findings are

summarized in Figure 1.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 41

Figure 1

Figure 1 displays on the horizontal axis the range of values of the summary index of firm size asymmetries,

/ a c , and on the vertical axis the range of values of the size of the third-country market, . We

see that for most parameter configurations the merger game played by firms has a unique PSNE where mergers

take place in both countries--area ( M, M ). Only if firm size asymmetries are small and the size of the third-

country market is relatively large will the merger game played by firms have a unique PSNE where mergers do

not take place in both countries--area ( N,N ). For the remaining configurations of the parameter space--the

area that separates area ( M, M ) from area ( N,N )-the merger game played by firms has two Nash equilibria

in pure strategies and one in mixed strategies.

Next we characterize the set of Nash equilibria of the merger game played by firms when the home market is

smaller than the foreign market. To do that we start by introducing a lemma.

Lemma 1: Let5063

7 126 315 2

7 82 183 2 .

(i) If 0, then fh1 h2

fh1,h2

hf1 f2

hf1,f2 .

(ii) (ii) If , 1 thenfh1 h2

hf1 f2

fh1,h2

hf1,f2 .

42 Luís Santos-Pinto

Proposition 4 characterizes the set of Nash equilibria of F2, when the home market is smaller than the

foreign market, that is, 0,1 .

Proposition 4:

(i) If 0, 115 , 0, and 0, f

h1,h2 , then NE F2, N,N .

(ii) If 0, 115 , 0, and f

h1,h2 , hf1 f2

, then NE F2, N, M .

(iii) If 0, 115 , 0, and h

f1 f2 , 1 , then NE F2, M, M .

(iv) If 0, 115 , , 1 and 0, h

f1 f2 , then NE F2, N,N .

(v) If 0, 115 , , 1 and h

f1 f2 , fh1,h2

, then NE

F2, M, M , N,N , ph ,p , withph

63 100 738 800 1647 2000 2

13 162 603 2 .

(vi) If 0, 115 , , 1 and f

h1,h2 , 1 , then NE F2, M, M .

(vii) If1

15 , 761 and 0, f

h1,h2 , NE F2, M, M , N,N , ph ,p .

(viii) If1

15 , 761 and f

h1,h2 ,1 , then NE F2, M, M .

(ix) If7

61 , 13 , then NE F2, M, M .

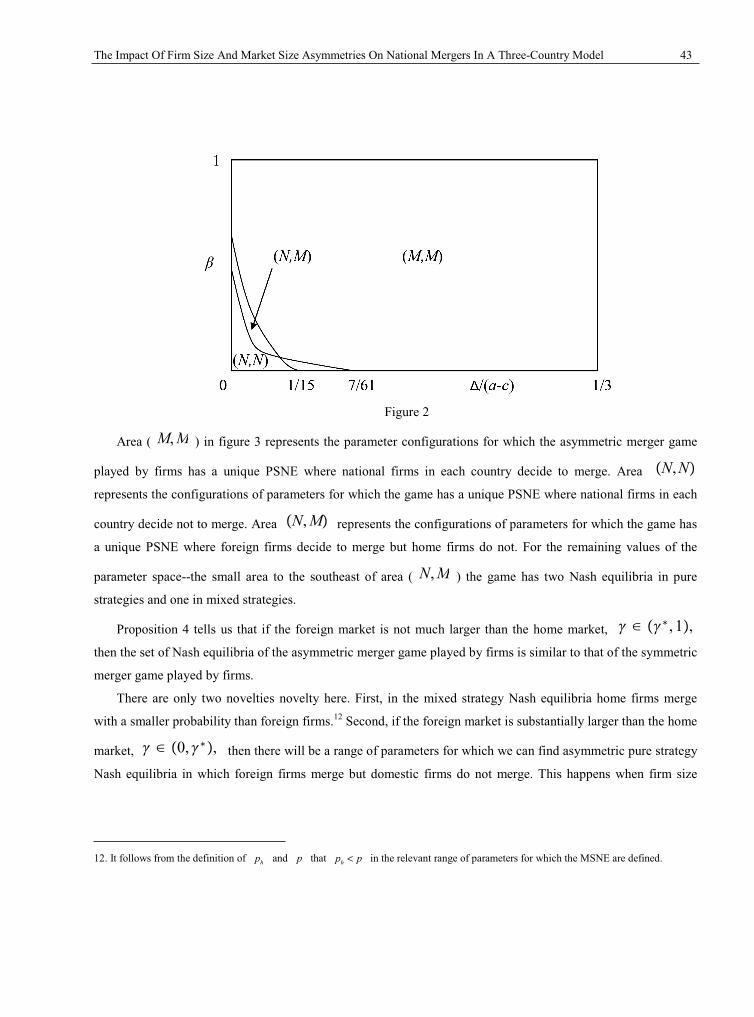

Figure 2 summarizes the findings of Proposition 4.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 43

Figure 2

Area ( M, M ) in figure 3 represents the parameter configurations for which the asymmetric merger game

played by firms has a unique PSNE where national firms in each country decide to merge. Area N,Nrepresents the configurations of parameters for which the game has a unique PSNE where national firms in each

country decide not to merge. Area N, M represents the configurations of parameters for which the game has

a unique PSNE where foreign firms decide to merge but home firms do not. For the remaining values of the

parameter space--the small area to the southeast of area ( N,M ) the game has two Nash equilibria in pure

strategies and one in mixed strategies.

Proposition 4 tells us that if the foreign market is not much larger than the home market, , 1 ,then the set of Nash equilibria of the asymmetric merger game played by firms is similar to that of the symmetric

merger game played by firms.

There are only two novelties novelty here. First, in the mixed strategy Nash equilibria home firms merge

with a smaller probability than foreign firms.12 Second, if the foreign market is substantially larger than the home

market, 0, , then there will be a range of parameters for which we can find asymmetric pure strategy

Nash equilibria in which foreign firms merge but domestic firms do not merge. This happens when firm size

12. It follows from the definition of hp and p that hp p< in the relevant range of parameters for which the MSNE are defined.

44 Luís Santos-Pinto

asymmetries are small, 0, 115 , and the size of the third-country market is moderately larger than the

size of the home market, fh1,h2 , h

f1 f2 .

The intuition for this result comes solely from the fact that if the foreign market is larger than the home

market, then the foreign market profit gains that a merger of foreign firms induces are greater than the home

market profit gains induced by a merger of home firms.

5. Welfare Impact of Conditional Mergers

In this section we provide conditions under which a merger in one of the countries improves that country's

welfare for a given market structure in the other country. As it is usual in the partial equilibrium literature we

measure national welfare as the sum of consumer and producer surplus.

We start by proving conditions under which a domestic merger improves national welfare conditional on a

given market structure in foreign. Consumer surplus at home is given by CSh a ph Qh /2 Qh2 /2,

where Qh is total output produced by home firms. If home firms do not merge, then

Qh 2a 2c /3 and CSh1,h2h 2a 2c 2 /18. If home firms merge, then

Qh a c /2 and CSh1 h2h a c 2 /8 .

Thus, a domestic merger will improve national welfare when foreign firms are not merged if

a c 2

8a c 2

4a c 2

162a 2c 2

18a c 2

9a c 2 2

25a c 2 2

9a c 3 2

25 . (5)

A domestic merger will improve national welfare when foreign firms are merged if

a c 2

8a c 2

4a c 2

92a 2c 2

18a c 2

9a c 2

16a c 2 2

9a c 3 2

16 . (6)

From inequalities (5) and (6) we obtain the following result.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 45

Proposition 5:

(i) A merger of domestic firms improves national welfare when foreign firms are not merged if either (a)

761 , 5

22 and 0,bhf1,f2

, with bhf1,f2 9

507 82 183 2

5 32 44 2 or (b) 5

22 , 13 .

(ii) A merger of domestic firms improves national welfare when foreign firms are merged if either (a)

115 , 5

22 and 0,bhf1 f2

, with bhf1 f2 1 18 45 2

5 32 44 2 or (b)5

22 , 13 .

Part (i) of Proposition 5 says that a merger of domestic firms improves national welfare when foreign firms

are not merged if firm size asymmetries are sufficiently high. It also says that when firm size asymmetries are

moderate a merger of domestic firms only improves national welfare when foreign firms are not merged if the

third-country market is substantially larger than the home market. Finally, it says that for small firm size

asymmetries a domestic merger never raises national welfare when foreign firms are not merged.

Proposition 5 part (ii) states conditions under which a merger of domestic firms improves national welfare

when foreign firms are merged. The conditions are similar to those found in part (i) only less restrictive. This

happens because the gains in the third-country market that are obtained with a merger of domestic firms are

larger when foreign firms are merged than when foreign firms are not merged.

We will now provide conditions under which a foreign merger improves foreign welfare conditional on a

given market structure in home. Consumer surplus in foreign is given by CSf a pf Qf/2 Qf2 /2,

where Qf is total output produced by foreign firms. If foreign firms do not merge, then

Qf 2a 2c /3 and CSf1,f2f 2a 2c 2 /18 . If foreign firms merge, then

Qf a c /2 and CSf1 f2f a c 2 /8 .

So, a foreign merger will be welfare improving for foreign when home firms are not merged if

a c 2

8a c 2

4a c 2

162a 2c 2

18a c 2

9a c 2 2

25a c 2 2

9a c 3 2

25 . (7)

A foreign merger will improve foreign welfare when home firms are merged if

46 Luís Santos-Pinto

a c 2

8a c 2

4a c 2

92a 2c 2

18a c 2

9a c 2

16a c 2 2

9a c 3 2

16 . (8)

From (7) and (8) we derive the following result.

Proposition 6:

(i) A merger of foreign firms improves foreign welfare when domestic firms are not merged if either (a)

761 , 5

22 and 0,bfh1,h2

, with bfh1,h2 9

507 82 183 2

5 32 44 2 or (b) 5

22 , 13 .

(ii) A merger of foreign firms improves foreign welfare when domestic firms are merged if either (a)

115 , 5

22 and 0,bfh1 h2

, with bfh1 h2 1 18 45 2

5 32 44 2 or (b)5

22 , 13 .

Proposition 6 provides conditions under which a foreign merger improves foreign welfare when domestic

firms are not merged--part (i)--and when domestic firms are merged--part (ii). The intuition is similar to that of

Proposition 5. The only difference here is that a merger of foreign firms improves foreign welfare for moderate

firm size asymmetries only if the size of the third-country market is larger than the minimum size of the third-

country market necessary for a merger of home firms to raise welfare at home.

6. Merger Game Played by Governments

We now assume that firms play no active role in merger decisions. Instead national governments are

completely free to determine the market structure in each country.13

Like before we assume that the starting point of this game is a situation where no merger has taken place.

The home government decides whether home firms should merge or not. Similarly, the foreign government

decides whether foreign firms should merge or not. The decisions of home and foreign governments are taken

simultaneously. Given the choice in the other country, each government takes the decision that maximizes its

welfare: the sum of consumer and producer surplus.

13. This is an extreme scenario. The most realistic model would be one where firms in each country propose mergers to a national anti-trust authority and the anti-trust authority allows or blocks mergers. In this case merger decisions are determined by firms' proposals and by the decisions of anti-trust authorities.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 47

Let the generic merger game played by governments be denoted by Gn, where n is the number of firms

in each country. The relevant payoffs for G2, are summarized in Table II for the two strategies of merge, M ,

and not merge, N .

h \ f M N

M

a c 2

8

a c 2

4

a c 2

9 ,

a c 2

8

a c 2

4

a c 2

9

a c 2

8

a c 2

4

a c 2

16 ,

2a 2c 2

9

a c 2 a c 2 2

9

a c 2 a c 3 2

16

N

2a 2c 2

9

a c 2 a c 2 2

9

a c 2 a c 3 2

16 ,

a c 2

8

a c 2

4

a c 2

16

2a 2c 2

9

a c 2 a c 2 2

9

a c 2 2 a c 3 2

25 ,

2a 2c 2

9

a c 2 a c 2 2

9

a c 2 2 a c 3 2

25

Table II

The upper left part of each cell in Table II displays the sum of consumer surplus at home with profits of the

merged home firm (when home firms are merged) or with profits of the two home firms (when home firms are

not merged) for each market configuration in foreign. The lower right part of each cell displays the sum of

48 Luís Santos-Pinto

consumer surplus in foreign with profits of the merged foreign firm (when foreign firms are merged) or with

profits of the two foreign firms (when foreign firms are not merged) for each market configuration in home.

We now characterize the set of Nash equilibria of the merger game played by governments when 1 .

Note that if 1 we have bhf1,gf2 bf

h1,h2 bN bhf1 f2 bf

h1 h2 bM .

Proposition 7:

(i) If 0, 115 , then NE G2,1 N, N .

(ii) If1

15 , 761 and 0,bM , then NE G2,1 M,M , N, N , q,q , with

q 3 21 350 246 800 549 800 2

13 162 603 2 .

(iii) If1

15 , 761 and bM, 1 , then NE G2,1 N,N .

(iv) If7

61 , 522 and 0,bN , then NE G2,1 M,M .

(v) If7

61 , 522 and bN, bM , then NE G2,1 M,M , N, N , q,q .

(vi) If7

61 , 522 and bM, 1 , then NE G2,1 N,N .

(vii) If5

22 , 13 , then NE G2,1 M,M .

Proposition 7 shows that in equilibrium of the merger game played by governments, governments decide not

to merge national firms when firm size asymmetries are small, when firm size asymmetries are moderate-low

and the size of the third-country market is not much larger than the home market, or when firm size asymmetries

are moderate-high and the size of the third-country market is not much larger than the home market. By contrast,

governments decide to merge national firms when firm size asymmetries are high or when firm size asymmetries

are moderate-high and the size of the third-country market is much larger than the home market. In the

remaining cases we have multiple equilibria: both governments decide to merge national firms, both

governments decide not to merge national firms, and each government merges national firms with probability

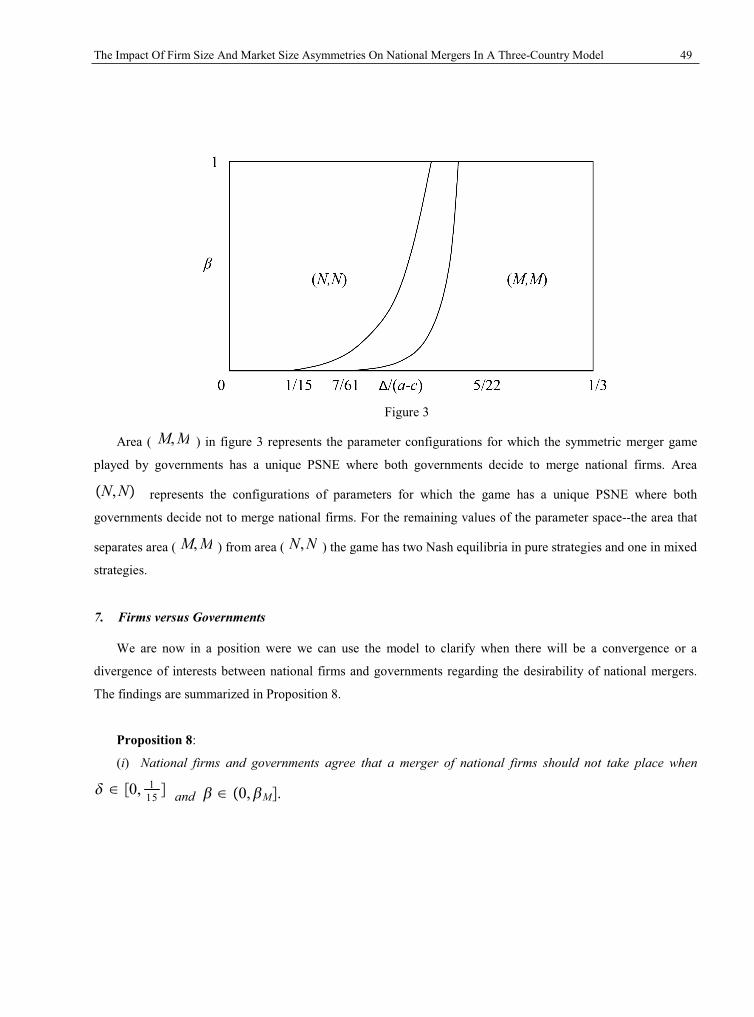

q . The findings are summarized in figure 3.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 49

Figure 3

Area ( M, M ) in figure 3 represents the parameter configurations for which the symmetric merger game

played by governments has a unique PSNE where both governments decide to merge national firms. Area

N,N represents the configurations of parameters for which the game has a unique PSNE where both

governments decide not to merge national firms. For the remaining values of the parameter space--the area that

separates area ( M, M ) from area ( N,N ) the game has two Nash equilibria in pure strategies and one in mixed

strategies.

7. Firms versus Governments

We are now in a position were we can use the model to clarify when there will be a convergence or a

divergence of interests between national firms and governments regarding the desirability of national mergers.

The findings are summarized in Proposition 8.

Proposition 8:

(i) National firms and governments agree that a merger of national firms should not take place when

0, 115 and 0, M .

50 Luís Santos-Pinto

(ii) National firms prefer to merge but governments prefer that national firms do not merge when (a)

0, 115 and N, 1 , (b)

115 , 7

61 and max N , bM , 1 , or (c)

761 , 25 91

89 and bM, 1 .(iii) National firms and governments agree that a merger of national firms should take place when

522 , 1

3 .

This result provides conditions on cost and market size asymmetries under which the interests of national

firms and of national governments will be either alined or in conflict. It says that if firm size asymmetries are

small and the third-country market is much larger than the national market, then the interests of national firms

and governments are alined: all are opposed to the creation of a national champion. It says that the interests of

national firms and governments are also aligned when firm size asymmetries are high: all favor the creation of a

national champion. However, if firm size asymmetries are small or moderate and the third-country market is not

much larger than the national market, then there is a conflict of interest between national firms and governments:

firms prefer to merge but governments are opposed to the merger.14

8. Extensions

There are many possible directions in which one could extend this model. For example, one could relax the

assumption of no trade between home and foreign. In this case competition in domestic markets would resemble

competition in the third-country market and the only difference would be that incentives for mergers would be

weaker.

Another possible extension of the model would be to break the assumption that home and foreign firms have

the same size distribution by assuming, for example, that foreign firms are uniformly more or less efficient than

home firms by a parameter . This extension complicates the analysis since it is no longer possible to find

closed form solutions for the market size thresholds. However, it is possible to parameterize the model

numerically to analyze this situation.

14. Proposition 8 and can be easily understood from visual inspection of Figures 1 and 3.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 51

The most obvious extension would be to look at a situation where we have three firms in home and three

firms in foreign. This extension also makes the analysis harder. If there are three firms in each country we would

need to consider all possible merger combinations. We would need to state not only individually rational

constraints for mergers to be viable but also stability conditions under which the firms outside the mergers would

not make a better offer to one of the participants in the merger.

Another possible modification of the model would be to model explicitly a game between national firms and

competition authorities where firms propose mergers and competition authorities accept or reject mergers

proposed by firms. This extension introduces a sequential aspect to merger analysis in open economies that has

not yet been sufficiently explored.

9. Application: Portugal and Spain

In this section we apply the model to three industries in Portugal and Spain: cement, mobile

telecommunications an fuel retail. There are several characteristic of these three sectors that fit quite well into

the framework of the model. Cement, telephone calls, and fuel are very close to being homogenous products.

The Portuguese and Spanish markets in these three sectors have high market concentration indexes. A large

percentage of profits of Portuguese and Spanish firms in these sectors comes from third-country markets (South

America and Africa).

The question we ask is whether the current industry configuration in each country and in each of these two

industries is stable or unstable. By a stable industry configuration we mean a situation where firms will not

propose mergers or where a merger will be proposed by firms but will be rejected by national governments. In

all other cases we say that the industry configuration is unstable.

It is important to bear in mind that the analysis that follows depends on the assumptions of the model. If

some of the assumptions of the model do not hold (e.g., linear demand, constant marginal costs, homogeneous

products, ect.), then the analysis may no longer be valid.

9.1. Cement

The data collected was obtained directly from different sources (annual report of Secil, annual report of

Cimpor, annual report of Uniland, report of cement industry in Arab countries, European Commission for Latin

America and Caribbean, Sector Report of Cement Industry by Caixa BI) and it refers to the year 2005/2006.

52 Luís Santos-Pinto

The market shares of Portuguese firms in the Portuguese cement market are: Cimpor 52.2% and Secil

47.8%. The market shares of Spanish firms in the Spanish cement market are: Cia Valenciana de Cementos

(CEMEX) 24.8%, Cementos Portland (Uniland - Group Portland Valderrivas) 21.7%, Arland (Lafarge) 9.3%,

Cementos Cosmos (Cimpor) 7.1%, Financera y Minera 6.4% and others 30.7%.

The similar market shares of the Portuguese cement firms in the domestic market suggest that firm size

asymmetry is quite small in Portugal. We can confirm this using the model. The summary index of asymmetry

for Portugal is the solution to

qCimpor/QPT

qSecil/QPT0.5220.478

11 2 ,

or PT 0. 028909 1/15. In Spain the two biggest cement firms also have very similar market

shares. The index of asymmetry for these two Spanish firms is

qCemex/QSP

qPortland/QSP0.2480.217

11 2 ,

or SP 0. 043478 1/15.The two largest firms in Portugal and the two largest firms in Spain compete in third countries. Only 50% of

Cimpor's profits before taxes and depreciation come from sales in the Portuguese market.15 A large percentage of

profits before taxes and depreciation of Cemex and Portland comes from sales in South America and Africa (less

than 50% of total profits). The size of the Spanish cement market is approximately 4 times the size of the

Portuguese cement market and the size of third-country markets is much larger than the size of both domestic

markets put together. This means that should be close to 0.25 and must be smaller than 0.25. Take PT SP 0.028909 0.043478 /2 0.0362. We have that

5063

7 126 315 2

7 82 183 2 0.03620. 529.

So, we have that 0. 25 0.529 . So, assuming

that is less than 0.25, it follows from Proposition 4 that Cimpor and Secil will not wish to merge. However,

it is not clear whether Cemex and Portland wish to merge or to remain separated.

15. Approximately 25% of Cimpor's profits before taxes and depreciation come from sales in Brazil, 11% from sales in Spain and the remaining 14% from sales in Africa.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 53

9.2. Mobile Telecommunications

In Portugal there exist three operators: Vodafone, Optimus and TMN. In Spain the operators are Vodafone,

Movistar and Orange. Both TMN and Movistar have quite significant parts of their profits coming from third

country markets.16

The data collected were obtained directly from Annual Reports of the respective companies and it refers to

the year 2005. The market shares for the Portuguese market are: TMN 44%, Vodafone 35% and Optimus 21%.

For the Spanish case we have: Movistar 46.6%, Vodafone 29.3% and Orange 24.1%.

The summary index of firm size asymmetry for the two largest Portuguese firms is the solution to

qT MN/QPT

qVodafone/QPT0. 440. 35

11 2 ,

or PT 0. 0732. We have that 1/15 PT 0. 0732 7/61. The summary index of firm

size asymmetry for the two largest Spanish firms is the solution to

qMovistar /QSP

qVodafone/QSP0.4660.293

11 2 ,

or PT 0.14122. We have that 7/61 SP 0.14122 5/22. It follows from Proposition 4

that Portuguese firms would like to merge as long as the third-country markets is not too large. It also follows

from Proposition 4 that Spanish firms would like to merge, no matter the size of the third-country market.

Should national governments promote these mergers? According to Proposition 8 Portuguese and Spanish

governments should not allow these mergers since the losses for domestic consumer surplus overtake the

efficiency gains or any profit gains in third-country markets.17

16. In Brasil the three major brands are Vivo, Claro and TIM. It is well known that TMN is owned by Portugal Telecom and Movistar by Telefónica, each company has a participation of 50% in the shareholding that controls 63% of Vivo. 17. If the third-country market is very large we have a region of multiple equilibria. However, for this region to be attained the third-country markets must be really large by comparison with domestic markets. This is clearly not the case in the mobile telecommunications industry in Portugal and Spain.

54 Luís Santos-Pinto

9.3. Fuel Retailing

The market shares of the two largest Portuguese fuel retailers in the Portuguese market are: Galp 37% and

BP 17%. The market shares of the two largest Spanish fuel retailers in the Spanish market are: Repsol 41%

Cepsa 20%. The summary index of firm size asymmetry for the two largest Portuguese firms is the solution to

qGalp /QPT

qBP /QPT0.370.17

11 2 ,

or PT 0.21978. We have that 7/61 PT 0. 21978 5/22. The summary index of firm

size asymmetry for the two largest Spanish firms is the solution to

qRepsol/QSP

qCepsa/QSP0. 410. 20

11 2 ,

or SP 0. 20588. We have that 7/61 SP 0.20588 5/22. We see that firm size

asymmetries of the two largest firms in Portugal and Spain are much larger in fuel retailing industry than in the

cement industry.

It follows from Proposition 4 that no matter the sizes of the Portuguese, Spanish and third-country markets,

Galp and BP would like to merge and so would Repsol and Cepsa. Should national governments promote these

mergers? According to Proposition 7 they should since the large firm size asymmetries are a signal of large

efficiency gains in such mergers. This is enough to compensate the increase in market power associated with

these mergers.

10. Conclusion

This paper studies incentives for national mergers in a partial equilibrium model where firms of two

countries compete in a third-country market. The main novelty of the paper is that it allows for both firm size

asymmetries as well as market size asymmetries. This allows us to characterize the joint impact of cost and

market size asymmetries on incentives for national firms to merge and on incentives for governments to promote

national mergers.

The paper shows that if firm size asymmetries between national firms are sufficiently high, then the interests

of national firms and governments are aligned in favor of creating a national champion. However, firms and

governments agree that no national champion should be created when firm size asymmetries are small and the

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 55

third-country market is much larger than the national market. If firm size asymmetries are small or moderate and

the third-country market is not much larger than the national market, then there is a conflict of interest between

national firms and governments: firms would like to merge but governments oppose mergers.

56 Luís Santos-Pinto

References

Barros, P. and L. Cabral (1994). “Merger Policy in Open Economies”, European Economic Review 38:

1041-1055.

Barros, P. (1998). “Endogenous mergers and size asymmetry of merger participants”, Economic Letters 60,

113-119.

Brander, J. and B. Spencer (1985). “Export subsidies and international market share rivalry”, Journal of

Internacional Economics 18, 83-100.

De Stefano, M. and M. Rysman (2004). “Competition policy as strategic trade with differentiated products”,

mimeo, Boston University.

Dixit, A.(1984), International Trade Policy for Oligopolistic Industries, Economic Journal 94, 1-16.

Farrell, J. and C. Shapiro (1990). “Horizontal Mergers: An Equilibrium Analysis”, The American Economic

Review 80, 107-126.

Fauli-Oller, R. (2000). “Takeover Waves”, Journal of Economics and Management Strategy 9, 189-210.

Forslid, R., Häckner, J. and A. Muren (2005). “When do Countries Introduce Competition Policy?”, CEPR

Discussion Paper No. 5162.

Gowrisankaran, G. (1999). “A dynamic model of endogenous horizontal mergers”, Rand Journal of

Economics 30, 56-83.

Haufler, A. and S.Nielsen (2005). “Merger policy to promote global players?” A Simple Model,'' CESifo

Working Paper No.1523.

Horn, H. and J. Levinsohn (2001). “Merger Policies and Trade Liberalization”, Economic Journal 111, 244-

276.

Horn, H. and L. Persson (2001). “Endogenous Mergers in Concentrated Markets”, International Journal of

Industrial Organization 19, 1213-1244.

Huck, S. and K.Konrad (2004), Merger profitability and trade policy, Scandinavian Journal of Economics

106, 107-122.

Huck, S., K. Konrad and W. Mueller (2005). “Merger without Cost Advantages”, CESifo Working Paper

No 1461.

Kreps, D. and J. Sheinkman (1983). “Capacity Precommitment and Price Competition Yield Cournot

Outcomes”, Bell Journal of Economics 14, 326-337.

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 57

Perry, M. and R. Porter (1985). “Oligopoly and the Incentive for Horizontal Merger”, The American

Economic Review, Vol. 75, No. 1, pp. 219-227.

Qiu, L. and W.Zhou (2006). “Merger waves: A model of Endogenous Mergers”, mimeo.

Richardson, M. (1999). “Trade and Competition Policies: Concordia Discors?”, Oxford Economic Papers

51, 649-664.

Rysman, M.(2001). “Competition Policy as Strategic Trade”, mimeo, Boston University.

Salant, S., S. Switzer, R. Reynolds (1983). “Losses from Horizontal Merger: the Effects of an Exogenous

Change in Industry Structure on Cournot-Nash Equilibrium”, Quarterly Journal of Economics 98, 185-199.

Suedekum, J. (2006). “Cross-Border Mergers and National Champions in an Integrating Economy”, IZA

Discussion Paper N. 2220.

58 Luís Santos-Pinto

Appendix

Proof of Proposition 1: (i) We start the proof by analyzing separately the profitability of the merger in each

market. The change in profits of home firms in the home market is given by the following function

CPha c 2

4a c 2

9a c 2 2

9a c 2 8 a c 20 2

36 . (9)

CPh is concave in and CPh 0 when a c10 and

a c2 . Therefore CPh is

greater than 0 , that is, the merger has a positive effect in profits in the home market for 1/10,1/2 .

Since 0,1/3 by the nonnegative profits condition and by the restriction that 0 then it follows

from this that the merger leads to gains in the home market for any 0,1/3 .

The change in profits of home firms in the third-country market due to the merger is given by

CP3a c 2

16a c 2 2

25a c 3 2

257 a c 2 82 a c 183 2

400 .

CP3 is concave in and CP3 0 when 7 a c /61 and a c /3. Therefore

CPh is greater than 0 for 7/61, 1/3 and so it follows from the above expression that the merger leads

to gains in the third-country market if 7

6113 and losses if

761 . This implies that the merger is

always profitable when 7/61, 1/3 independently of any other parameter. When 0,7/61 , the

merger leads to gains in home but losses in the third-country market. In this case, to evaluate when the merger is

profitable we need to compare the gains in the home market with the losses in the third-country market. The

merger will be profitable for this range of values of when CPh CP3 or

a c 2 8 a c 20 2

367 a c 2 82 a c 183 2

400

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 59

Solving the previous equation with respect to we obtain that the gains in home are greater than the

losses in the third-country market if 63

1007 82 183 2

7 56 140 2 h1 h2f1,f2 . Therefore, if 0, 7/61 and

h1 h2f1,f2 , 1 the merger is profitable because the losses in the third-country are smaller than the gains in

the home market.

(ii) The change in profits of home firms in the home market due to the merger is given by (chm2) and so the

merger leads to gains in the home market for any 0,1/3 . The change in profits of home firms in the

third-country market due to the merger is given by

a c 2

9a c 2

16a c 3 2

16 .

It follows from the above expression that the merger leads to gains in the third-country market if 1

15

and losses if 1

15 . This implies that the merger is always profitable when 1/15, 1/3 . If

0,1/15 , then the merger leads to gains in home but losses in the third-country market. It follows from

(merger3) that the gains in home are greater than the losses in the third-country market if

50100

1 18 45 2

1 8 20 2 h1 h2f1 f2 . Thus, If 0, 1/15 and h1 h2

f1 f2 ,1 the merger is

profitable. Q.E.D.

Proof of Proposition 2: The proof is similar to that of Proposition 1. Q.E.D.

Proof of Proposition 3: (i) If 0,1/15 and 0, M , then it follows from Proposition 1 that

N is a dominant strategy for home firms. Since F2,1 is symmetric N is also a dominant strategy for foreign

firms. Therefore, NE F2,1 N, N when 0,1/15 and 0, M . (ii) If 0,1/15

and M, N , then it follows from Proposition 1 that the best reply of domestic firms to a merger by

foreign firms is for domestic firms to merge. This and the fact that F2,1 is symmetric imply that M,M

60 Luís Santos-Pinto

NE F2,1 when 0,1/15 and M, N . If 0,1/15 and M, N , then it

follows from Proposition 1 that the best reply of domestic firms to N is to play N . This and the fact that

F2,1 is symmetric imply that N,N NE F2,1 when 0,1/15 and M, N . So, for

this range of parameters F2,1 has two symmetric PSNE. It is a well know result that the number of Nash

equilibria of this type of game must be odd. Since there is no other PSNE we must have a MSNE. By definition,

in a MSNE foreign firms randomize between M and N to make domestic firms indifferent between M and

N . Thus, in the MSNE we must have that

p a c 2

4a c 2

9 1 p a c 2

4a c 2

16

p a c 2

9a c 2

16a c 2 2

9a c 3 2

16

1 p a c 2

9a c 2 2

25a c 2 2

9a c 3 2

25

Solving this equation for p we obtain

p 63 100 738 800 1647 2000 2

13 162 603 2 . (10)

Thus, NE F2,1 M, M , N, N , p,p if 0,1/15 and M, N . (iii) If

0,1/15 and N, 1 , then it follows from Proposition 1 that M is a dominant strategy for

home firms. Since F2,1 is symmetric it is also a dominant strategy for foreign firms to play M . Therefore,

NE F2,1 M, M when 0,1/15 and N, 1 . (iv) If 1/15, 7/61 and

0, N , then it follows from Proposition 1 that the best reply of domestic firms to a merger by foreign

firms is for domestic firms to merge. This and the fact that F2,1 is symmetric imply that M,M NE

F2,1 when 1/15, 7/61 and 0, N . If 1/15, 7/61 and 0, N , then it

follows from Proposition 1 that the best reply of domestic firms to N is to play N . This and the fact that

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 61

F2,1 is symmetric imply that N,N NE F2,1 when 1/15, 7/61 and 0, N . In this

case there also exists a MSNE where the probability of playing M is the same as the one obtained in (ii). Thus,

NE F2,1 M, M , N, N , p,p when 1/15, 7/61 and 0, N . (v) If

1/15, 7/61 and N, 1 , then it follows from Propositions 1 that it is a dominant strategy for

domestic firms to play M . Since F2,1 is symmetric it is also a dominant strategy for foreign firms to play

M . Therefore, NE F2,1 M, M when 1/15, 7/61 and N, 1 . (vi) If

7/61, 1/3 , then it follows from Propositions 1 that M is a dominant strategy for domestic firms. Since

F2,1 is symmetric it is also a dominant strategy for foreign firms to play M . Therefore, NE

F2,1 M, M when 7/61, 1/3 . Q.E.D.

Proof of Lemma 1: It follows directly from the definitions of , hf1,f2 , f

h1,h2 ,hf1 f2

and

fh1 h2 . Q.E.D.

Proof of Proposition 4: (i) If 0, 1/15 , and 0, fh1,h2

, it follows from

Propositions 1 and 2 and from Lemma 1(i) that N is a dominant strategy for domestic firms and also for

foreign firms. Therefore NE F2 , N,N when 0, 115 , and 0, f

h1 h2

. (ii) If 0,1/15 , and fh1,h2 , h

f1 f2 , it follows from Propositions 1 and 2 and

Lemma 1(i) that N is a dominant strategy for domestic firms whereas M is a dominant strategy for foreign

firms. Therefore, NE F2 , N,M when 0,1/15 , and fh1,h2 , h

f1 f2 .

(iii) If 0,1/15 , and hf1 f2 , 1 , it follows from Propositions 1 and 2 and from

Lemma 1(i) that M is a dominant strategy for foreign firms and also for foreign firms. Therefore, NE

62 Luís Santos-Pinto

F2 , M,M when 0,1/15 , and hf1 f2 , 1 . (iv) If 0,1/15 ,

and 0, hf1 f2

, it follows from Propositions 1 and 2 and from Lemma 1(ii) that N is a

dominant strategy for home firms and also for foreign firms. Therefore, NE F2 , N,N when

0,1/15 , and 0, hf1 f2 . (v) If 0,1/15 , and

hf1 f2 , f

h1,h2 , it follows from Proposition 1 and from Lemma 1(ii) that the best reply of domestic

firms to a merger by foreign firms is for domestic firms to merge. Additionaly, the best reply of domestic firms

to an absence of merger of foreign firms is for domestic firms not to merge. The same holds for foreign firms.

From here it follows that in this range of parameters the merger game has two PSNE. In one PSNE domestic

firms merge and foreign firms merge in the other PSNE domestic firms do not merge and foreign firms do not

merge. As we have said before given that we have a even number of PSNE we must have one MSNE. In the

MSNE home firms merge with probability ph defined by

pha c 2

4a c 2

9 1 pha c 2

4a c 2

16

pha c 2

9a c 2

16a c 2 2

9a c 3 2

16

1 pha c 2

9a c 2 2

25a c 2 2

9a c 3 2

25

Solving this equation for ph we obtain

ph63 100 738 800 1647 2000 2

13 162 603 2 .

On other hand, in the MSNE foreign firms merge with probability p defined by (p). Thus, NE

F2,1 M, M , N, N , p,p when 0,1/15 , and hf1 f2 , f

h1,h2 . (vi)

If 0, 1/15 , and fh1,h2 , 1 , it follows from Propositions 1 and 2 and from Lemma

1(ii) that M is a dominant strategy for both domestic and foreing firms. Therefore, NE F2, M, M

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 63

when 0, 1/15 , and fh1,h2 ,1 . (vii) If 1/15, 7/61 , and

0, fh1,h2 , it follows from Proposition 1 that the best reply of home firms to M is M and the best

reply of home firms to N is N . The same holds for foreign firms. So, we have one PSNE where domestic

firms merge and foreign firms merge and another PSNE where domestic firms do not merge and foreign firms do

not merge. The MSNE is obtained as in part (v). Thus, NE F2, M, M , N,N , ph ,p when

1/15, 7/61 , and 0, fh1,h2 . (viii) If 1/15, 7/61 and f

h1,h2 ,1 , it follows

from Propositions 1 and 2 that it is a dominant strategy for domestic firms to merge. The same is true regarding

foreign firms. Thus, NE F2, M, M when 1/15, 7/61 and fh1,h2 , 1 . (ix) If

7/61, 1/3 , it follows from Propositions 1 and 2 that it is a dominant strategy for domestic firms to

merge. It is also a dominant strategy for foreign firms to merge. Thus, NE F2, M, M when

7/61, 1/3 . Q.E.D.

Proof of Proposition 5: (i) The change in welfare in the home market given the merger is given by the

following function

CWh3 a c 2

82a 2c 2

18a c 2 a c 2 2

95 a c 2 32 a c 44 2

72 . (11)

CWh is concave in and CWh 0 when 5 a c

22 and a c

2 . Therefore CWh is

greater than 0 for 5/22, 1/2 , that is, the merger has a positive welfare impact in the home market for

5/22, 1/2 . Since 0,1/3 , the merger leads to welfare losses in the home market for

0,5/22 and to gains when 5/22, 1/3 . We know from Propositon 1 that, when foreign firms

have not merged, the merger of domestic firms leads to gains in the third-country market if 7/61, 1/3

and losses if 0,7/61 . Therefore, conditional on foreign firms not having merged, a merger of domestic

64 Luís Santos-Pinto

firms improves national welfare when 5/22, 1/3 and reduces national welfare when 0,7/61 .

When 7/61, 5/22 we have losses at home and gains in the third-country market. In this case the merger

of domestic firms improves national welfare if losses at home are smaller than gains in the third-country market.

This happens if 13

1 18 45 2

7 16 16 2 bhf1,f2 . So, conditional on foreign firms not having merged, a merger

of domestic firms improves national welfare if either (a) 5/22, 1/3 or (b) 7/61, 5/22 and

0,bhf1,f2 .

(ii) We know from (i) that the merger of domestic firms leads to welfare losses in the home market for

0,5/22 and to gains when 5/22, 1/3 . We also know from Proposition 1 that, when foreign

firms have merged, the merger of domestic firms leads to gains in the third-country market if 1/15, 1/3

and losses if 0, 1/15 . Therefore, conditional on foreign firms having merged, a merger of domestic

firms improves national welfare when 5/22, 1/3 and reduces it when 0, 1/15 . When

1/15, 5/22 we have losses at home and gains in the third-country market. In this case the merger of

domestic firms improves national welfare if losses at home are smaller than gains in the third-country market.

That happens if 1 18 45 2

5 32 44 2 bhf1 f2 . So, conditional on foreign firms having merged, a merger of

domestic firms improves national welfare if either (a) 5/22, 1/3 or (b) 1/15, 5/22 and

0,bhf1 f2 . Q.E.D.

Proof of Proposition 6: The proof is similar to that of Proposition 5. Q.E.D.

Proof of Proposition 7: (i) If 0, 1/15 , then it follows from Proposition 5 that N is a dominant

strategy for home. Since G2,1 is symmetric, then N is also a dominant strategy for foreign. Therefore, NE

G2,1 N, N when 0, 1/15 . (ii) If 1/15, 7/61 and 0, bM , then it follows

from Proposition 5 that the best reply of home to N is to play N. Since the game is symmetric the best reply

The Impact Of Firm Size And Market Size Asymmetries On National Mergers In A Three-Country Model 65

of foreign to N is to play N . This shows that N,N NE G2,1 when 1/15, 7/61 and

0, bM . If 1/15, 7/61 and 0, bM , then it follows from Proposition 5 that the best

reply of home to M is to play M. Since the game is symmetric the best reply of foreign to M is to play M

. This shows that M,M NE G2,1 when 1/15, 7/61 and 0, bM . It is a well know

result that the number of Nash equilibria of this type of game must be odd. Since there is no other equilibrium in

pure strategies we must have a MSNE. By definition, in a MSNE foreign randomizes between M and N to

make home indifferent between M and N . Thus, in the MSNE we must have that

q a c 2

8a c 2

4a c 2

9

1 q a c 2

8a c 2

4a c 2

16

q 2a 2c 2

9a c 2

9a c 2

16a c 2 2

9

q a c 3 2

16 1 q 2a 2c 2

9a c 2

9

1 q a c 2 2

25a c 2 2

9a c 3 2

25

Solving this equation for q we obtain

q 3 21 350 246 800 549 800 2

13 162 603 2 .

Thus, NE G2,1 M,M , N,N , q, q when 1/15, 7/61 and 0, bM . (iii) If

1/15, 7/61 and bM, 1 , then it follows from Proposition 5 that N is a dominant strategy for

home. Since G2,1 is symmetric, then N is also a dominant strategy for foreign. Therefore, NE

G2,1 N, N when 1/15, 7/61 and bM, 1 . (iv) If 7/61, 5/22 and

0,bN , then it follows from Proposition 5 that M is a dominant strategy for home. Since G2,1 is

66 Luís Santos-Pinto

symmetric, then M is also a dominant strategy for foreign. Therefore, NE G2,1 M,M when

7/61, 5/22 and 0,bN . (v) If 7/61, 5/22 and bN, bM , then it follows from

Proposition 5 that the best reply of home to N is to play N. Since the game is symmetric the best reply of

foreign to N is to play N . This shows that N,N NE G2,1 when 7/61, 5/22 and

bN, bM . If 7/61, 5/22 and bN, bM , then it follows from Proposition 5 that the best

reply of home to M is to play M. Since the game is symmetric the best reply of foreign to M is to play M

. This shows that M,M NE G2,1 when 7/61, 5/22 and bN, bM . In this case there

also exists a MSNE where the probability of playing M is the same as the one obtained in (ii). Thus, NE

G2,1 M,M , N,N , q, q when 7/61, 5/22 and bN, bM . (vi) If

7/61, 5/22 and bM, 1 , then it follows from Proposition 5 that N is a dominant strategy for

home. Since G2,1 is symmetric, then N is also a dominant strategy for foreign. Therefore, NE

G2,1 N, N when 7/61, 5/22 and bM, 1 . (vii) If 5/22, 1/3 , then it follows

from Proposition 5 that M is a dominant strategy for home. Since G2,1 is symmetric, then M is also a

dominant strategy for foreign. Therefore, NE G2,1 M,M when 5/22, 1/3 . Q.E.D.

Proof of Proposition 8: (i) If 0,1/15 and 0, M , then it follows from Proposition 3(i)

and 7(i) that NE F2,1 NE G2,1 N,N . (ii) If 0,1/15 and N, 1 , then it

follows from Proposition 3(iii) and 7(i) that NE F2,1 M, M N, N NE G2,1 . If

1/15, 7/61 and max N , bM , 1 , then it follows from Proposition 3(v) and 7(iii)

that NE F2,1 M, M N, N NE G2,1 . If 7/61, 25 91 /89 and

bM, 1 , then it follows from Proposition 3(v) and 7(vi) that NE F2,1 M, M N, N NE

G2,1 . (iii) If 5/22, 1/3 , then it follows from Propositions 3(vi) and 7(vii) that NE F2,1 NE

G2,1 M,M . Q.E.D.