The impact of Connected Vehicles on the Insurance...

17

PTOLEMUS Consulting Group The impact of Connected Vehicles on the Insurance sector June 2016 - PTOLEMUS intellectual property Insurance Telematics’16

-

Upload

duongthien -

Category

Documents

-

view

216 -

download

0

Transcript of The impact of Connected Vehicles on the Insurance...

PTOLEMUS Consulting Group

The impact of Connected Vehicles on the Insurance sector

June 2016 - PTOLEMUS intellectual property

Insurance Telematics’16

PTOLEMUS

PTOLEMUS in a nutshell

2

Strategy definition

Vision creation, strategic

positioning, business plan development,

board coaching & support

Investment assistance Strategic due

diligence, market

assessment, feasibility study,

M&A, post-acquisition plan

Innovation management

Value proposition definition, product

& services development,

architecture design, assistance to

launch

Business development

Partnership strategies,

detection of opportunities, ecosystem-

building, response to tenders

Our consulting services

Procurement strategy

Specification of requirements &

tender documents, launch of tenders,

supplier negotiation & selection

Implementation

Deployment plans, complex / high risk

project & programme

management, risk analysis &

mitigation strategy

Usage-based charging PAYD / PHYD insurance, road charging / electronic tolling,

fleet leasing & rental, car sharing, Car As A Service, etc.

Telematics & Intelligent Transport Systems ADAS, connected vehicle, crowd-sourcing, fleet

management, eCall, bCall, SVR, tracking, vehicle data analytics (OBD / CAN-bus), VRM, V2X, xFCD

Positioning / Location enablement

M2M & connectivity

Our fields of expertise

Car infotainment & navigation Connected services (Traffic information, fuel prices, speed

cameras, weather, parking, points of interest, social networking), driver monitoring, maps, smartphone

integration, smartphone-, PND- or embedded navigation,

PTOLEMUS is the first strategy consulting firm focused on telematics and geolocation

PTOLEMUS

Our clients are across the mobility ecosystem…

3

Mobile telecom operators

Device / location suppliers

Insurers, aggregators & assistance providersBanks & private equity investors

2012 Directors’ report

(translation from the Italian original which remains the definitive version)

Financial Statements of the Company and the Group at 31 December 2012

27 March 2013

Legal and Administrative Office: 20121 Milan - Foro Buonaparte, 44

Fully paid-up share capital € 314,225,009.80 Tax Code and Milan Company Register no. 00931330583

www.itkgroup.com

Automotive manufacturers & suppliersAnalytics providers

3RQWLDFW���� 3RQWLDFW�%RQHYLOOH����

$OID�5RPHR���� $OID�5RPHR��������

-HHS���� -HHS�&KHURNHH�������� -HHS�*UDQG�&KHURNHH�����9�

OBD2 Bluetooth Dongle basic compatible car models

<HDU 0DQXIDFWXUHU�0RGHO�(QJLQH�/LWHU�

0*�5RYHU���� 0*�5RYHU�PHPV��HFX���� 0*�=5����/���9

0LQL�&RRSHU���� 0LQL�&RRSHU�6����

6DDE���� 6DDE�������

/RWXV�3URWRQ����a 3URWRQ�*(1�����a 3URWRQ�6DYU\���� /RWXV�3URWRQ�6DYY\�������� /RWXV�3URWRQ�6DYY\�����$07

Telematics solution providersApplications providers

ITS operators, regulators & fleets

1PTOLEMUS in a nutshell

PTOLEMUS * Italy, the UK, France, Germany, Russia and the US

Introduction to the 2016 study

3

• 1200+ pages of research using: - 286 interviews in 28 countries

- 5 years of research performed by 6 consultants in 4 countries

- Insights from 25+ consulting projects

- Our experience & vision of the ecosystem incl. OEMs and TSPs

- 422 figures (charts, tables, etc.)

• 42 case studies including Allianz, AllState, Carrot Insurance, Vodafone Auto, Ingenie, OnStar- Progressive, Discovery Insure, Liberty Mutual, Octo Telematics, Renault Amaguiz, State Farm, Unipol, Zurich

• A handbook of 69 suppliers' solutions including our own evaluation and ranking

• 28 insurance markets profiled

• 2020 & 2030 market forecasts - Canada, US, Latin America,

Europe, Russia, South Africa, India, Chinese and Japan

- Personal line / commercial line - Aftermarket / OEM

• Analyses of the disruptive forces at play - ADAS and autonomous vehicles - The eCall & ERA Glonass

mandates - The rise of smartphone apps - Big Data & analytics

• Targeted recommendations for insurers, regulators, TSP, OEMs and operators

The reference report on the subject, quoted by

The Economist, the Financial Times and

the Wall Street Journal

The 2016 study revealed UBI is becoming mainstream

PTOLEMUS

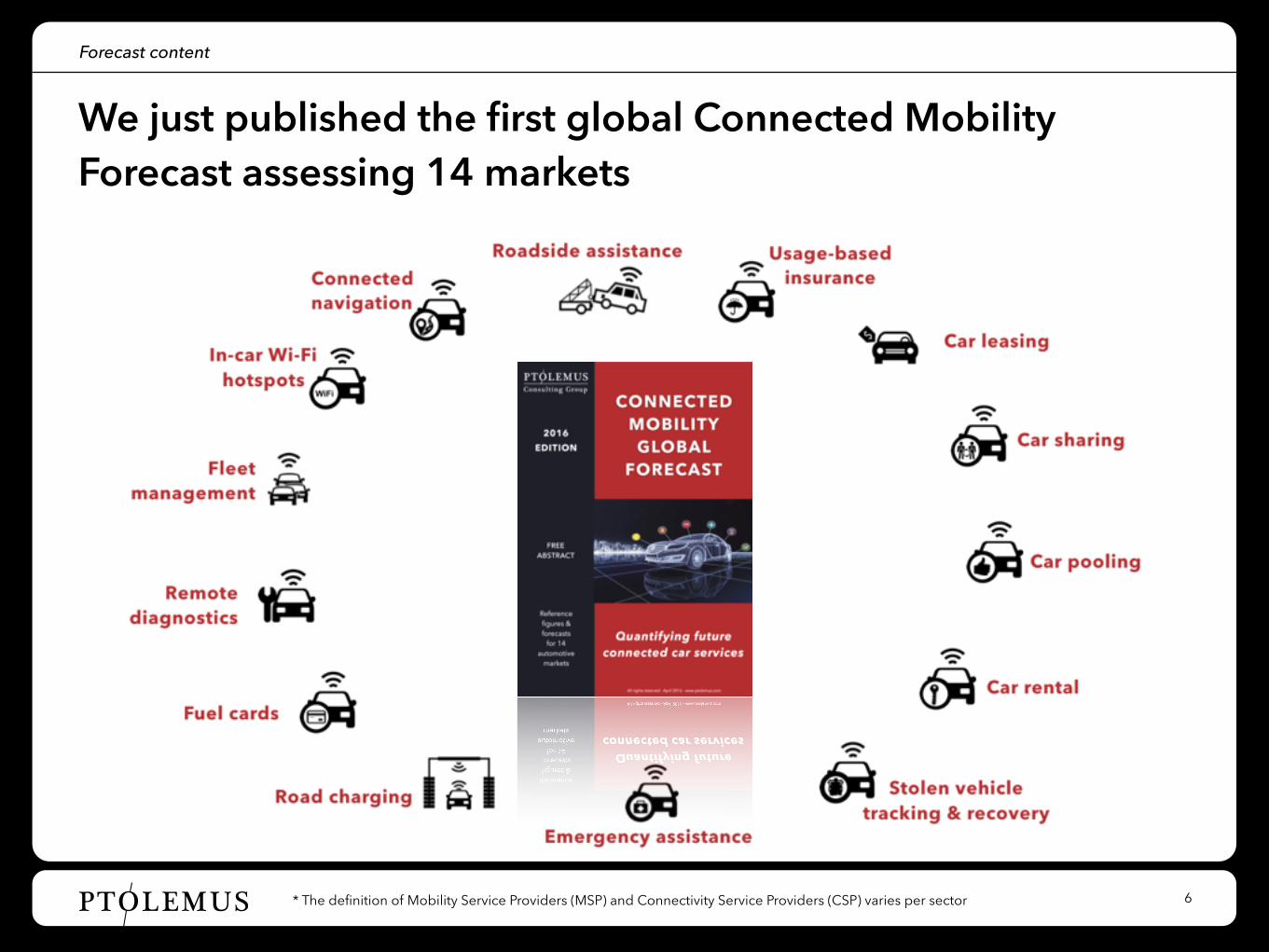

We just published the first global Connected Mobility Forecast assessing 14 markets

5

200-page quantitative analysis of the mobility market

• The future evolution of the whole connected mobility sector analysed

• 18 original graphs encapsulating the essence of the mobility market evolution

• 57 quantitative analysis graph describing each of the 14 markets

Total Addressable Market revealed • Separate analysis of the Total

Addressable Markets (TAM) size in volume and revenue for each of the 14 car-centric mobility applications.

• TAM account given from the perspectives of the MSPs and CSPs*

14 comparative analysis of mobility services based on:

• Delivery, service and business models • Value chains and key players

• Regulatory and competitive environment • Connectivity penetration per region • Key volume and revenue drivers • Current and future market trends • Global forecast to 2020 of the volumes

and revenues per region • 18 countries and areas covered

4800-lines underlying data sheet including:

• The total addressable market in volume and value seen from the Mobility service providers (MSP)* and the Connectivity Service Providers (CSP) perspective

• The total underlying volumes and revenues per country

• The volume and revenue forecasts for the MSP and for the CSP

• The split between OEM and Aftermarket volumes and revenues

… and another thing … 1

* Mobility Service Providers (MSP) and Connectivity Service Providers (CSP) varies per sector

PTOLEMUS 6* The definition of Mobility Service Providers (MSP) and Connectivity Service Providers (CSP) varies per sector

Forecast content

We just published the first global Connected Mobility Forecast assessing 14 markets

PTOLEMUS

Connected Mobility Forecast - some results

UBI is only one out of many mobility services experiencing rapid growth

• The car mobility services market will grow to over $350 billion affecting 650 million cars

• By 2020, 45 out of 80 million new cars will be sold connected worldwide

• The share of aftermarket provision for all service revenues will reach 84% in 2020

• OEMs are embracing mobility

• None of the 14 services will be provided individually in 2020

• At the centre is the ability to access driver and car data

7

Total connected services market revenues forecasts ($ in million)

0

20,000

40,000

60,000

80,000

100,000

2015 2016 2017 2018 2019 2020

Total connected services market revenues for MSP forecasts

($ in million)

Car leasing

Car sharing

Car pooling

UBI

ETC

Fuel services

telematics FMS

Source: PTOLEMUS Consulting Group

PTOLEMUS

Connected Mobility Forecast - some results

UBI is only one out of many mobility services experiencing rapid growth

• The car mobility services market will grow to over $350 billion affecting 650 million cars

• By 2020, 45 out of 80 million new cars will be sold connected worldwide

• The share of aftermarket provision for all service revenues will reach 84% in 2020

• OEMs are embracing mobility

• None of the 14 services will be provided individually in 2020

• At the centre is the ability to access driver and car data

8Source: PTOLEMUS Consulting Group

Penetration of leasing in fleet vehicles and connectivity in leased vehicles worldwide 2020

0%10%20%30%40%50%60%70%80%90%

100%

Fleet vehicles worldwide Connected leased vehicles

39%

61%

83%

17%

LeasedNon-leasedNon-connectedConnected

0%10%20%30%40%50%60%70%80%90%

100%

Fleet vehicles in Europe Connected leased vehicles

49%

51%

68%

32%

LeasedNon-leasedNon-connectedConnected

Penetration of leasing in fleet vehicles and connectivity in leased vehicles Europe 2020

PTOLEMUS Source: PTOLEMUSPTOLEMUS

There are now 50% more UBI programmes than in 2013

9

The growth pattern has changed

The UBI market today

• 292 UBI active programmes in June 2016

• On top of an estimated 45 trials worldwide, many of those in Europe

• New markets are opening: Russia, New Zealand, Thailand, Indonesia, Turkey...

• The fastest growth last year was in the US now the largest market

• 6 insurances have now more than 500K UBI subscribers

• PHYD now leads over PAYD with 78% of North American programmes and 53% of European ones using behaviour based pricing

Source: PTOLEMUS Consulting Group

UBI programmes (Europe)

UK

Italy

France

Germany

Spain

Russia

Belgium

Ireland

Netherlands

Austria

Slovakia

Switzerland

Turkey

Czech republic

Hungary

Belarus

Denmark

Greece

Norway

Portugal

Slovenia

Croatia

8 15 23 30 38 45 53 60

June 2016December 2013

UBI programmes (rest of world)

US

Canada

China

South Africa

Australia

Japan

Brazil

Columbia

Malaysia

Singapore

Thailand

Ecuador

India

Israel

Malta

New Zealand

Taiwan

10 20 30 40 50

June 2016December 2013

PTOLEMUS

UBI is not yet eating to its full potential

• UBI can work outside the Young Driver segment

• Italy has 15% UBI penetration and it still growing fast

• Continued investment from OEMs and Wireless operators

• The number of Smartphone UBI programmes has tripled since 2013

• TBYB is not the only way to introduce smartphone UBI

• Many of its programmes do not use driver data efficiently

10Source: PTOLEMUS Consulting Group

The UBI market today

PTOLEMUS Text

Allianz has finally kicked off the Germany UBI market

• GDV enabled insurers to buy devices together

• 12 volt CLA chosen: price, compatibility, flexibility

• Allianz BonusDrive: ecall, bCall, mobile app

• Allianz Drive: behaviour based pricing with coaching and gamification.

• Privacy attack protection from data protection commissioners

• Taiwan association of insurers is following that model

11

The UBI market today

PTOLEMUS 12

VEHICLE PRODUCTION

DEVICE PRODUCTION

SERVICE PROVISION

DATA MANAGEMENT

TELEMATICS PROCESS

MANAGEMENTDISTRIBUTIONDEVICE

INSTALLATION

Illustration of OEM partnership models

2

GM has been the first OEM to launch its own insurance telematics solution based on OnStar data

Source: PTOLEMUS Note: OEMs may partner with different B2B provider offering different part of the value chain in white label

UBI insurer 1

UBI insurer 2

Tier-1 supplier

Tier-1 supplier

1

2

3

3

4

Tier-1 supplier

UBI market trends - OEMs changing role

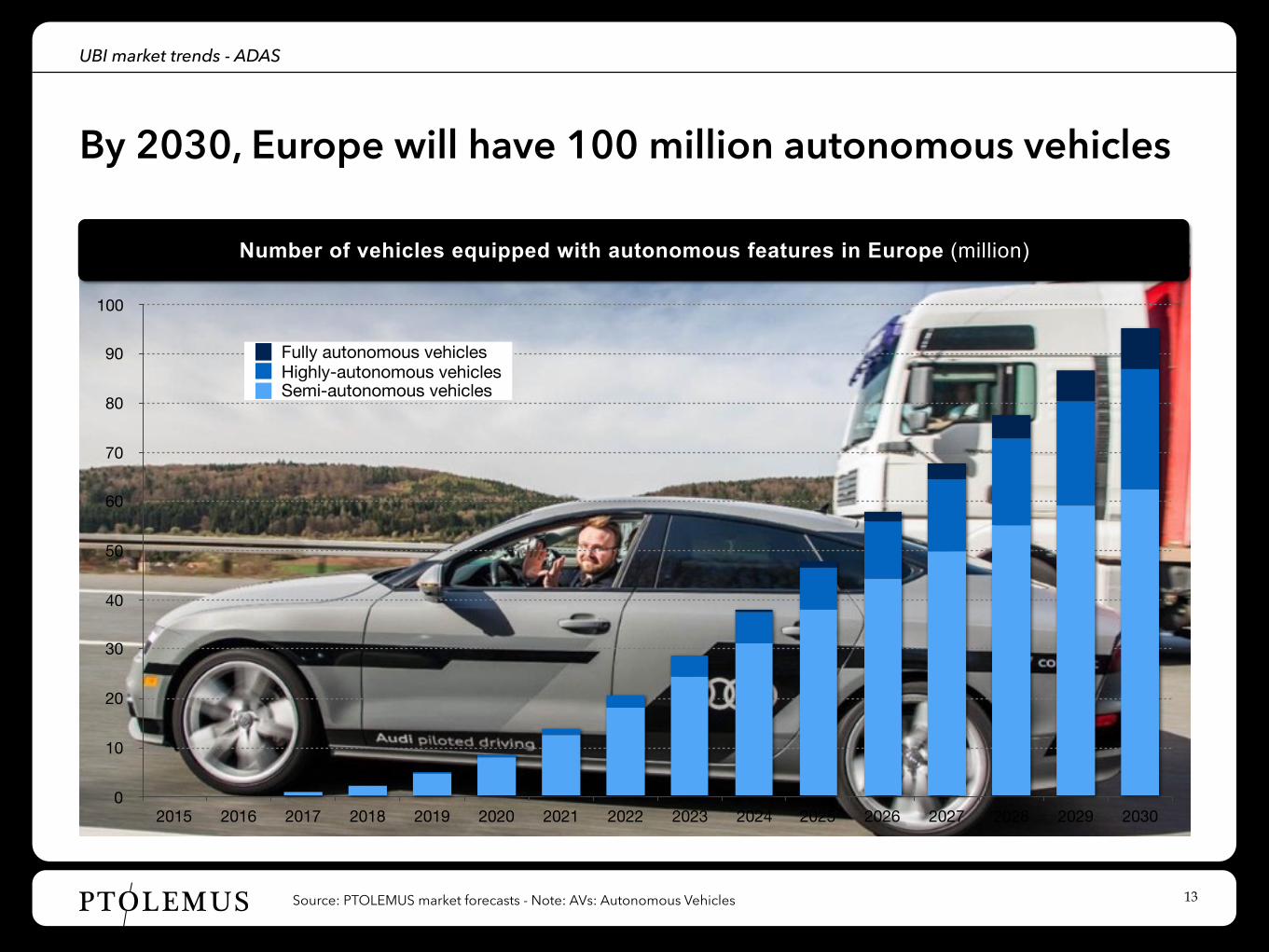

PTOLEMUS Source: PTOLEMUS market forecasts - Note: AVs: Autonomous Vehicles 13

Number of vehicles equipped with autonomous features in Europe (million)

0

10

20

30

40

50

60

70

80

90

100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Semi-autonomous vehiclesHighly-autonomous vehiclesFully autonomous vehicles

By 2030, Europe will have 100 million autonomous vehicles

UBI market trends - ADAS

PTOLEMUS

Autonomy will evolve step by steps

• Developments in autonomy will be split by road types

• OEMs are after the most cost effective way to avoid crashes

• They focus on city and interurban

• Drivers risk profiles are not always improved by autonomy

• Driver monitoring required

• Tesla is going faster and further than any other OEMs

• …while still in BETA

14

They said level 2 meant “feet off”!

UBI market trends - ADAS

PTOLEMUS

Autonomy will evolve step by steps

• Developments in autonomy will be split by road types

• OEMs are after the most cost effective way to avoid crashes

• They focus on city and interurban

• Drivers risk profiles are not always improved by autonomy

• Driver monitoring required

• Tesla is going faster and further than any other OEMs

• …while still in BETA

15

We can all learn a lot from each of the Tesla crashes

UBI market trends - ADAS

PTOLEMUS 23

Conclusion

• Insurance is about to change with less accidents and shift in liability

• Effectively predicting risks using Big Data is the key differentiator

• New devices require successful value proposition

• Car manufacturers partnership will take time and efforts

• Connected mobility services are a source of data but can also transform your business

Thank you!

Insurer will need to look outside the blackbox for find data

PTOLEMUS Consulting Group

S t r a t e g i e s f o r M o b i l e C o m p a n i e s

For more information, contact Thomas Hallauer at [email protected]

Brussels - Chicago - Paris - London - Moscow - Hannover - Milan - Boston

www.ptolemus.com