THE GOODMAN REPORT

4

1 This firm is not a CPA firm. THE GOODMAN REPORT Fall 2016 Millennials: Late to the Party, Right on Time for the Economy By: Quinten Womack Analyst/Trading Assistant Millennials have suffered, or perhaps provoked, the ire of their elders for how slowly they have matured. The largest generation in Ameri- can history—84.7 million versus 79 million when the Baby Boomers’ were in their 20s and 30s—has rewritten the playbook for adulthood. As of yet, Millennials have delayed embracing marriage, parenthood, and homeownership due in part to their financial hardships. Entering adulthood in the midst of the least robust economic recovery in American history and saddled with college debt, Millennials are the product of the environment in which they were raised. But, that environment is changing. As the economy recovers, wages grow, and college debt is paid off or forgiven, Millennials are increasingly likely to turn the corner towards adulthood. Recent studies bear out this thesis: Marriage: A 2015 Allstate/National Journal poll revealed that two-thirds of Millennials believe marriage is relevant. 73% of Millennials believe one should wait to get married until they are financially stable, explaining the delay in mar- riage. Parenthood: A report by the National Center for Health Statistics revealed that while births per capita are at an all-time low, the absolute number of births is on par with the post-WWII baby boom. The report also noted that the birth rate for teenage mothers is at an all-time low and that the birth rate for unwed mothers is 15% below its 2007 peak, meaning fewer children potentially born into poverty. Homeownership: The rate of homeownership in the U.S. has been in steady decline since the Great Recession. The financial burden of homeownership and the psychological shock of a housing-based recession have weighed on homeownership rates, but that may be about to change. National homebuilders are turning their focus from luxury homes to more-affordable homes as a shortage of entry-level homes persists, and a 2015 study by the National Association of Realtors and Portland State University showed 42% of millennials want to live in a conventional suburban home. Hence, we could have titled this article “Get Off My Lawn, You Kids! And Buy Your Own!” Savings: A 2016 study by Bankrate.com indicated that a higher percentage of Millennials (86% ) were saving some of their in- come, higher than for any other age group. Savings translate into the financial stability Millennials are seeking before they make the above major life commitments. Millennials are reaching an inflection point; they’re employed, accumulating wealth, and putting the Great Recession behind them. In do- ing so, they will grow the economy, becoming more voracious consumers like the generations before them as they grow into true adulthood. Be it buying a new home or a crib, Millennials are taking up the mantle of maturity the only way Millennials know how: in their own unique way and without regard for tradition. URGENT WARNING: INVESTORS ARE PLAYING ON THE TRACKS, THE TRAIN IS COMING, AND THERE IS NO CONDUCTOR (okay, you know such headlines are not characteristic of The Goodman Report , and this was intended to get your attention) By: Steven R. Goodman, CPA, CFP ® President & Chief Investment Officer Headlines can be dangerous. In today’s world the 24/7 digital news cycle is where most people get their news. Just as in the olden days when the paperboy would stand on the corner hawking the daily paper with the incantation “Disaster strikes, read all about it” as an inducement to pur- chase the paper, today’s digital news headlines have taken over that job. In the digital world advertisers pay per click, meaning that the more peo- ple who click on an article, the more that the media company gets paid and the more eyeballs hit the page showing whatever is being hawked. (continued on page 3)

Transcript of THE GOODMAN REPORT

1

This firm is not a CPA firm.

THE GOODMAN REPORT Fall 2016

Millennials: Late to the Party, Right on Time for the Economy

By: Quinten Womack

Analyst/Trading Assistant

Millennials have suffered, or perhaps provoked, the ire of their elders for how slowly they have matured. The largest generation in Ameri-

can history—84.7 million versus 79 million when the Baby Boomers’ were in their 20s and 30s—has rewritten the playbook for adulthood.

As of yet, Millennials have delayed embracing marriage, parenthood, and homeownership due in part to their financial hardships. Entering

adulthood in the midst of the least robust economic recovery in American history and

saddled with college debt, Millennials are the product of the environment in which

they were raised. But, that environment is changing. As the economy recovers, wages

grow, and college debt is paid off or forgiven, Millennials are increasingly likely to

turn the corner towards adulthood. Recent studies bear out this thesis:

Marriage: A 2015 Allstate/National Journal poll revealed that two-thirds of

Millennials believe marriage is relevant. 73% of Millennials believe one should

wait to get married until they are financially stable, explaining the delay in mar-

riage.

Parenthood: A repor t by the National Center for Health Statistics revealed

that while births per capita are at an all-time low, the absolute number of births is

on par with the post-WWII baby boom. The report also noted that the birth rate for teenage mothers is at an all-time low and that the

birth rate for unwed mothers is 15% below its 2007 peak, meaning fewer children potentially born into poverty.

Homeownership: The rate of homeownership in the U.S. has been in steady decline since the Great Recession. The financial

burden of homeownership and the psychological shock of a housing-based recession have weighed on homeownership rates, but that

may be about to change. National homebuilders are turning their focus from luxury homes to more-affordable homes as a shortage of

entry-level homes persists, and a 2015 study by the National Association of Realtors and Portland State University showed 42% of

millennials want to live in a conventional suburban home. Hence, we could have titled this article “Get Off My Lawn, You Kids! And

Buy Your Own!”

Savings: A 2016 study by Bankrate.com indicated that a higher percentage of Millennials (86% ) were saving some of their in-

come, higher than for any other age group. Savings translate into the financial stability Millennials are seeking before they make the

above major life commitments.

Millennials are reaching an inflection point; they’re employed, accumulating wealth, and putting the Great Recession behind them. In do-

ing so, they will grow the economy, becoming more voracious consumers like the generations before them as they grow into true adulthood.

Be it buying a new home or a crib, Millennials are taking up the mantle of maturity the only way Millennials know how: in their own

unique way and without regard for tradition.

URGENT WARNING: INVESTORS ARE PLAYING ON THE TRACKS, THE TRAIN IS

COMING, AND THERE IS NO CONDUCTOR (okay, you know such headlines are not characteristic of The Goodman Report, and this was intended to get your attention)

By: Steven R. Goodman, CPA, CFP®

President & Chief Investment Officer

Headlines can be dangerous. In today’s wor ld the 24/7 digital news

cycle is where most people get their news. Just as in the olden days when

the paperboy would stand on the corner hawking the daily paper with the

incantation “Disaster strikes, read all about it” as an inducement to pur-

chase the paper, today’s digital news headlines have taken over that job.

In the digital world advertisers pay per click, meaning that the more peo-

ple who click on an article, the more that the media company gets paid

and the more eyeballs hit the page showing whatever is being hawked. (continued on page 3)

2

This firm is not a CPA firm.

THE GOODMAN REPORT PAGE 2

Investing in Equities During Turbulent Environments

By: Ed Roth CFA, CPA, CFP®, CEBS

Vice President, Investment Advisory Services

Successful, long-term equity investing is based on fundamental analysis utilizing quality information. This prudent approach is

not altered by short-term volatility or by short-term tumultuous events. Why? First, it is important to recognize that there has

been a long and abundant history of turbulent environments for the equity markets to navigate. For example, The Great Depres-

sion, World War II (and several other wars), Black Friday, the Tech Bubble, The Great Recession, Brexit, periods of high and low

inflation, numerous blends of fiscal and monetary policies, etc. Second, history also contains many positive environments that

have more than offset the adverse financial impacts equity markets may have encountered. Logically this must be the case, other-

wise the equity markets would have a negative return since inception and this simply has not occurred. Now, I’m not suggesting

the only way for equity prices to go is up. Yet, despite countless, negative events, significant market declines, and investor angst

during these times, the S&P 500 is at, or near, its highest level ever!

We further this point via the graphs below. Each illustrates positive growth of a $10,000 investment in both the S&P 500 and the

Barclay’s Intermediate Gov’t/Corp Bond Index since 2008, and the last 25 and 50 years, respectively. The graphic immediately

below is labeled with notable events since the beginning of 2008. Although the bar graphs are not “event” labeled, we know his-

tory contains numerous examples of both positive and negative happenings. The conclusion is apparent. The equity market (S&P

500) has persevered and produced not only positive returns, but long-term returns well in excess of those associated with fixed

income investments.

Other key observations:

1) Turbulent events are neither isolated nor rare. These events are what cause volatility in equity markets. And perhaps

the more salient point is that investors can and do overreact or misinterpret the “news.”

2) Despite these events, and recognizing that past performance is no guarantee of future results, the long-term dominant perfor-

mance trend for equities as represented by the S&P 500 is positive.

3) Given a meaningful measurement period, fixed income securities typically provide lower returns versus equities as evidenced

by a comparison of the S&P 500 vs. the Barclay’s Intermediate Gov’t/Corp Bond Index.

4) Even though long-term returns for fixed income investments lag those of equities, fixed income securities are a necessary com-

ponent of a diversified risk-managed portfolio.

In sum, by adhering to a prudent, long-term investment strategy, equity investors will find opportunities even during turbulent

environments and, often, at lower prices.

3

This firm is not a CPA firm.

THE GOODMAN REPORT PAGE 3

(continued from page 1)

In some cases, those landing pages simply have ads, in other cases the articles themselves are the ads. Of particular danger are

those that have the little subscript reading “sponsored content.” Beware that these are not real articles but advertisements in dis-

guise. In the financial press, that content may have the goal of directing you to buy a subscription to an investment newsletter,

selling you gold, or in some cases are a doorway to outright fraud. In many cases, clients have forwarded links to articles that

are in fact sponsored content. Despite those ads running on respected mainstream websites, we have found that some of that

content is placed by parties that have previously been found by the SEC to have misled or even defrauded investors. The old

adage, buyer beware, should extend to a warning of caution when clicking on propaganda disguised as news.

Now for the real urgent warning. In the ongoing debate over active versus passive investing, the major ity of the ar ticles

would have you think that costs are the only issue. There are far more considerations than cost, such as risk management, tax

efficiency, and financial advisory services. Recently, I presented Active versus Passive Investing: Beyond the Biases at two

conferences: one hosted by the Houston CPA Society, and the other by the TSCPA. I delivered an unbiased two-hour presenta-

tion of the pros and cons of each approach. While our firm engages primarily in active management, we also use passive invest-

ing strategies, as appropriate. There was, though, one concept and related set of graphics that caused a few jaws to drop, and I

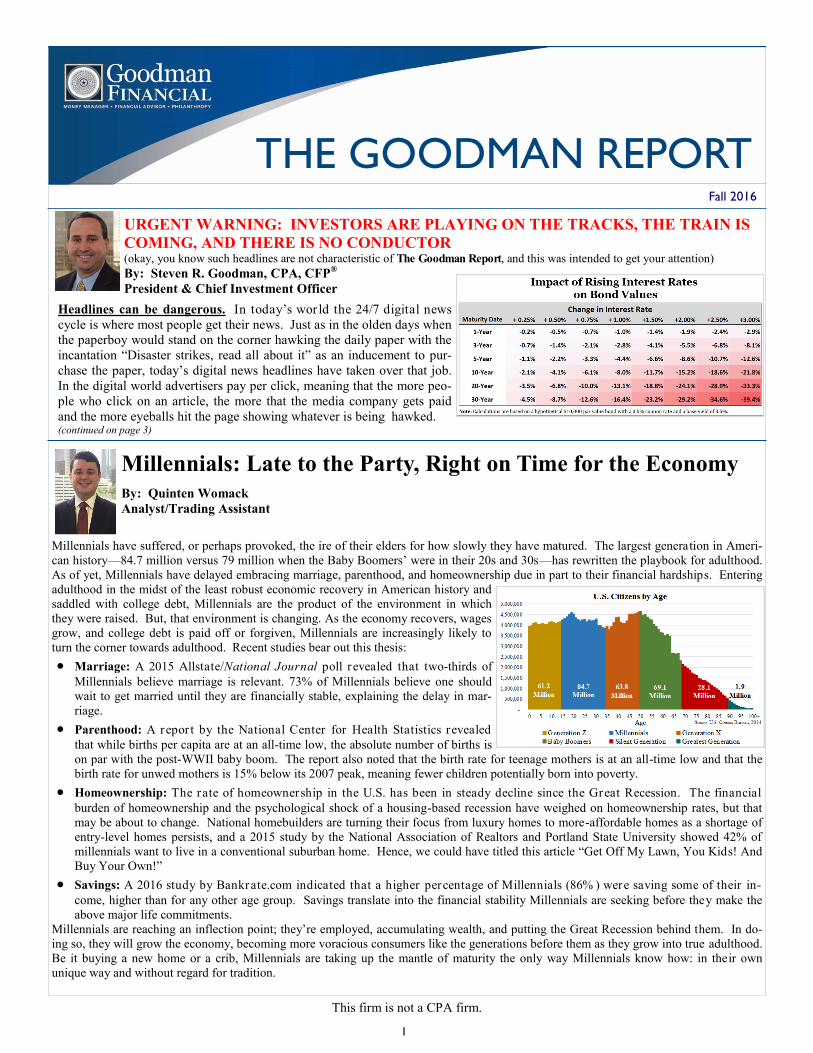

have included them here. We all know that bond prices fall when interest rates rise, with the magnitude greatest for longer term

bonds. Per the chart on page 1, a 20-year bond and 30-year bond are set to drop 33% and 39%, respectively if interest rates were

to increase by 3% (not much more than the Fed has predicted over the next several years). It is for that reason that in the current

environment our client accounts are comprised almost exclusively of individual bonds maturing in the next several years (our

typical bond ladder is 1-6 years). We also know that bond mutual funds (including index funds and exchange traded funds

(ETFs) hold a diversified portfolio of individual bonds. What most people don’t think about is that even with intermediate term

bond mutual funds there may be a substantial portion of the fund that are comprised of long term bonds. With that said the typi-

cal reaction to the chart on page 1 is who would be so crazy to take the risk of purchasing these 20 and 30 year bonds. The an-

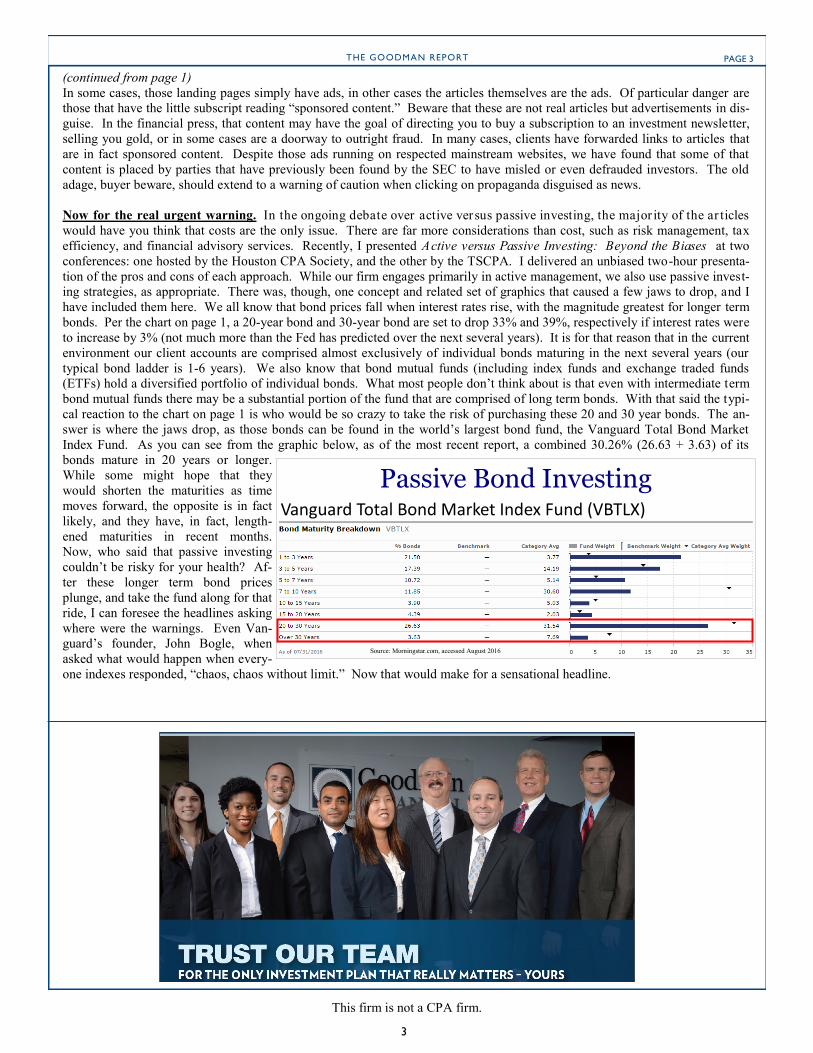

swer is where the jaws drop, as those bonds can be found in the world’s largest bond fund, the Vanguard Total Bond Market

Index Fund. As you can see from the graphic below, as of the most recent report, a combined 30.26% (26.63 + 3.63) of its

bonds mature in 20 years or longer.

While some might hope that they

would shorten the maturities as time

moves forward, the opposite is in fact

likely, and they have, in fact, length-

ened maturities in recent months.

Now, who said that passive investing

couldn’t be risky for your health? Af-

ter these longer term bond prices

plunge, and take the fund along for that

ride, I can foresee the headlines asking

where were the warnings. Even Van-

guard’s founder, John Bogle, when

asked what would happen when every-

one indexes responded, “chaos, chaos without limit.” Now that would make for a sensational headline.

Vanguard Total Bond Market Index Fund (VBTLX)

Passive Bond Investing

Source: Morningstar.com, accessed August 2016

4

This firm is not a CPA firm.

The Goodman Report

Inside This Issue:

Urgent Warning: Investors Are Playing on the

Tracks, the Train Is Coming, and There Is No

Conductor

Millennials: Late to the Party, Right on Time

for the Economy

Investing in Equities During Turbulent

Environments

Focus on Philanthropy

5177 Richmond Avenue, Suite 700

Houston, Texas 77056

Phone: 713-599-1777

Fax: 713-599-1811

Toll Free: 877-599-1778

Email: [email protected]

Website: www.goodmanfinancial.com

Philanthropy is part of our culture; our core purpose is helping people, doing what is right, and providing peace of mind.

Occasionally we see tangible proof of the rewards of our philanthropic efforts. Regular readers of The Goodman Report

may recall that at the end of 2014 as part of our 25th anniversary celebration we invited clients to nominate a charity for a

$25,000 bequest. With 24 nominees, there were plenty to choose from and the winner was The Lingap Children’s Founda-

tion (www.lingapcenter.org). But way at the end of the list, alphabetically, was client-nominated Water to Thrive. It gar-

nered our attention and a check. The proposition was that each $5,000 donation funded a water well in Africa, and in 2016,

our well was dug and the water began flowing. As water is the most precious resource, it can be a life saver, especially in

Africa. We hope these photos touch you as they did us. For more information on Water to Thrive, an Austin, Texas chari-

ty, visit www.watertothrive.org.

Focus on Philanthropy