The Gold Standard 43 July 14

8

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 1 The Gold Standard The journal of The Gold Standard Institute Editor Philip Barton Regular contributors Rudy Fritsch Keith Weiner Sebastian Younan Occasional contributors Thomas Bachheimer Ronald Stoeferle Publius John Butler Charles Vollum The Gold Standard Institute The purpose of the Institute is to promote an unadulterated Gold Standard www.goldstandardinstitute.net President Philip Barton President – Europe Thomas Bachheimer President – USA Keith Weiner President – Australia Sebastian Younan Editor-in-Chief Rudy Fritsch Membership Levels Annual Member US$100 per year Lifetime Member US$3,500 Gold Member US$15,000 Gold Knight US$350,000 Annual Corporate Member US$2,000 Contents Editorial ........................................................................... 1 News ................................................................................. 2 Part II: A Regulatory Model for a Free Gold Standard ........................................................................... 2 A Drawing-Board Currency as Ersatz Constitution . 5 Comments on a Free Gold Standard .......................... 6 Editorial Fans of Central Banking Have an Achilles Heel Most of my writing about the gold standard is about how it works, and how the paper dollar standard doesn’t. A casual conversation I had with someone recently underscored that there is an even stronger argument. Our opponents, those who support central banking and irredeemable paper money, have to make two cases. One is to defend the theory and practice of central banking, that central bankers are wise and honest and that their debt-based paper money works. They have to argue that the dollar does everything you want money to do, such as hold its value, enable proper accounting, encourage savings, support a stable economy, etc. Well, they can go through the motions and fool the ignorant. The other is that they have to defend the use of force against innocent people. Central planners constantly run into the problem that people are not willing cogs. We don’t want to be jammed into the machine where directed. The central planners never have our best interest at heart. Quite the contrary, they seek to sacrifice our property, liberty, goals, and well-being. Supposedly it serves some sort of public good, though it’s never the good of any particular member of the public. Anyways, no one ever goes along voluntarily. Central planners have to pass laws, in order to do whatever good to us that they feel needs doing. Safely backed by the law, they need not worry about our petty little concerns. They can force the unwilling to obey, under threat of loss of property, liberty, and ultimately life. If you don’t agree with this, think about what will happen if you refuse to pay your taxes. It may take a few years, but sooner or later, armed agents of the government will come to arrest you. If you don’t want to be arrested, they will force you into handcuffs. If you are able to fight that off, at some point they will shoot you dead.

-

Upload

ulfheidner9103 -

Category

Documents

-

view

3 -

download

0

Transcript of The Gold Standard 43 July 14

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 1

The Gold Standard

The journal of The Gold Standard Institute Editor Philip Barton Regular contributors Rudy Fritsch Keith Weiner Sebastian Younan Occasional contributors Thomas Bachheimer Ronald Stoeferle Publius John Butler Charles Vollum

The Gold Standard Institute The purpose of the Institute is to promote an unadulterated Gold Standard www.goldstandardinstitute.net President Philip Barton President – Europe Thomas Bachheimer President – USA Keith Weiner President – Australia Sebastian Younan Editor-in-Chief Rudy Fritsch Membership Levels Annual Member US$100 per year

Lifetime Member US$3,500

Gold Member US$15,000

Gold Knight US$350,000

Annual Corporate Member US$2,000

Contents

Editorial ........................................................................... 1 News ................................................................................. 2 Part II: A Regulatory Model for a Free Gold Standard ........................................................................... 2 A Drawing-Board Currency as Ersatz Constitution . 5 Comments on a Free Gold Standard .......................... 6

Editorial

Fans of Central Banking Have an Achilles Heel

Most of my writing about the gold standard is about

how it works, and how the paper dollar standard

doesn’t. A casual conversation I had with someone

recently underscored that there is an even stronger

argument.

Our opponents, those who support central banking

and irredeemable paper money, have to make two

cases. One is to defend the theory and practice of

central banking, that central bankers are wise and

honest and that their debt-based paper money

works. They have to argue that the dollar does

everything you want money to do, such as hold its

value, enable proper accounting, encourage savings,

support a stable economy, etc. Well, they can go

through the motions and fool the ignorant.

The other is that they have to defend the use of

force against innocent people.

Central planners constantly run into the problem

that people are not willing cogs. We don’t want to be

jammed into the machine where directed. The

central planners never have our best interest at heart.

Quite the contrary, they seek to sacrifice our

property, liberty, goals, and well-being. Supposedly it

serves some sort of public good, though it’s never

the good of any particular member of the public.

Anyways, no one ever goes along voluntarily. Central

planners have to pass laws, in order to do whatever

good to us that they feel needs doing. Safely backed

by the law, they need not worry about our petty little

concerns. They can force the unwilling to obey,

under threat of loss of property, liberty, and

ultimately life.

If you don’t agree with this, think about what will

happen if you refuse to pay your taxes. It may take a

few years, but sooner or later, armed agents of the

government will come to arrest you. If you don’t

want to be arrested, they will force you into

handcuffs. If you are able to fight that off, at some

point they will shoot you dead.

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 2

In the case of irredeemable paper money, there are

several ways that the government forces people to

use it. One is the capital gains tax on gold. Another

is the legal tender law. There are others.

The economic arguments for irredeemable paper and

central banking are fallacious and often frivolous.

We can and should confront every falsehood, every

logical error, every misrepresentation of the gold

standard and its defenders. We must also make the

affirmative case for the benefits of the unadulterated

gold standard.

However, we have one more weapon. It demands to

be used, when the context is appropriate. Our

adversaries are confessing to the very failures of their

system. If paper scrip were truly superior to gold,

people wouldn’t need to be forced to use it. When a

bully can’t prevail in an argument using reason, he

becomes violent. Our monetary opponents are

bullies. They resort to force, which is their moral

failing.

This is their Achilles heel, and it’s even more

important than their economic errors.

At best, central bank advocates are Machiavellians,

seeking to use people as a means to their own ends.

At worst, they are little Hitlers and Stalins,

rationalizing their actions with the tired cliché “you

have to break a few eggs to make an omelette.”

We need to strip their veneer of respectability. Many

people will get that, even if they don’t understand

monetary economics.

Keith Weiner

News

Forbes: Your personal debt is not entirely your fault.

≈≈≈

Mining.com: Donald Duck Gold coins sell out in 10

minutes. Scrooge McDuck the heroic accumulator

would have been more appropriate.

≈≈≈

Forbes: America needs the Gold standard more than

ever.

Keith Weiner on Financial Sense.

≈≈≈

RT.com: “The Americans are taking good care of

our gold, we have no reasons for mistrust,” Nobert

Barthle, the German Parliament Budget spokesman,

told RT

≈≈≈

Business Standard: $15b of Chinese loans backed by

Gold that does not exist

≈≈≈

Digital Journal: Gold at the turn of a tap in Montana

≈≈≈

Mineweb: Mali’s first Gold refinery (first since

Mansa Musa)

≈≈≈

Bullion Street: Deutsche Bank opens 1500 tons Gold

vault in London

Part II: A Regulatory Model for a Free

Gold Standard

The primary pitfall that led to the demise of the first

generation of digital gold currency was the lack of a

regulatory model.

Most of the early digital gold companies

incorporated as regular companies without obtaining

special licenses for financial services. After they

grew large enough to warrant government attention,

they found it difficult to obtain financial services

licenses, and most of them were prosecuted and shut

down.

Most governments did not have license categories

for fully reserved digital payment systems in the late

1990’s, so those companies that applied for licenses

were in most cases denied them.

The Regulatory Problem

For the Free Gold Standard vision set forth in Part I,

we need a digital gold transaction system as well as

one or more financial exchanges to efficiently trade

our gold issuance against foreign currency. Those

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 3

roles fit the definition of regulated financial

institutions.

Instead of asking governments to create new

regulations or categories for digital gold systems, let’s

look at the existing landscape of regulated

institutions. Most countries have a pyramid of

financial institutions with a central bank at the apex:

Central Bank

Capital Markets (stocks, commodities, bullion

& forex exchanges)

Commercial Banks, Savings & Loans

E-money Issuers

Non-bank Financial Institution(s)

Money Service Businesses & Agent Networks

(eg. Western Union)

Stock Brokers

Forex Bureaus

Credit Unions

Cooperative Societies (Secondary)

Cooperative Self Help Groups (SHG’s)

These financial institutions often fall under different

regulatory agencies, and in some cases multiple

agencies.

Pathways to Licensed Digital Gold Business

1. Set up a Bank

The safest way to set up a digital gold currency

system from a regulatory perspective is to simply buy

a regular banking license and set up a gold bank.

However, this is also the most expensive and highly

regulated option.

2. E-Money License

The European Union has an “E-money Directive” 1

that allows for e-money licenses for non-bank

financial institutions. An e-money license costs

almost the same as a banking license, and is more

limited in scope. There are limits on total transaction

size and volume per account, which may be

detrimental to our goals.

1 http://ec.europa.eu/internal_market/payments/emoney/index_en.htm

3. Money Service Business

Some countries may allow digital gold companies to

be licensed as Money Service Businesses; however

that is far from certain. Money services regulations

were designed around remittance services, and

bureaucrats may not easily accept the idea of gold

money remittances.

4. Credit Union

A credit union is a special kind of cooperative

society, which hold interesting possibilities. A

cooperative society is a special kind of corporation

where each shareholder only has only one vote, no

matter how many shares they hold. Cooperatives are

for-profit entities that in most cases pay dividends to

the shareholders.

A credit union is a special kind of bank that is

organized as a cooperative society and serves a

limited “field of membership” - often the members

of a cooperative society, or employees of a certain

company, or an association of people holding a

common interest.

In many countries credit unions have lower capital

requirements and regulatory costs than banks.

Credit unions grew out of the Great Depression and

have historically been seen as ways for communities

to organize and help themselves for savings,

checking and getting loans. Consequently, credit

unions often enjoy a kind of sacred political status

and reduced regulatory burden.

In some jurisdictions, such as Hong Kong, credit

unions have explicit authority to trade in bills of

exchange. 2 Credit unions may also issue debit cards,

which means they have access to the global

ATM/debit network. Access to the ATM network

will be important for our goals.

5. General Cooperative Society

A general cooperative society, or “self help group”,

can offer savings and investment services to its

members. Whereas a credit union offers checking

accounts (“front office services”) to members, a

2 Bills of exchange are critical to enable supply chains to perform invoicing and accounting in gold.

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 4

cooperative society is limited to “back end services”,

meaning savings, securities and lending, but not

checking (demand deposits). Obviously, this may

vary from one country to another.

Cooperatives may issue and trade their own shares,

as well as internal investment funds, amongst their

members.

In most countries cooperatives fall under a different

regulatory agency than banks or capital markets.

Given the significant freedom and power that

cooperatives have to offer financial services to

members, this can be a safe regulatory cocoon in

which to nurture the Free Gold Standard until we

have grown large enough to apply for public banking

and capital exchange licenses.

Cooperative societies also have another special

advantage - they can form branches or chapters even

in other countries. A branch is considered to be a

cooperative society itself, as well as being a regulated

institution. This means that the headquarters chapter

may legally rely upon the assurances of other

chapters with regard to the identity of their

members. This could prove to be quite helpful with

regard to Know Your Customer (KYC)

requirements, because it would enable foreign

members of the Society to open a financial account

with our digital gold issuer without having to appear

in person in that country.

A cooperative society coupled with a credit union

hits the “sweet spot” for our needs:

Cooperatives can have a global field of

membership with local chapters.

A cooperative chapter can be relied upon as a

“regulated institution” for KYC.

Cooperatives can issue and trade internal

securities (ie, private equity)

A credit union has all the powers of a bank

for money transfers.

Credit unions may gain access to the global

ATM networks.

Credit unions may support a market in foreign

exchange.

A Long-Term Strategy

As a community of outsiders trying to bootstrap a

Free Gold Standard in a world of fiat money, we

need to use our capital wisely. We need time and

freedom to build and test our systems, make our

mistakes and correct them, before we reach for a

more public market.

Creating a cooperative society, “The Gold Standard

Society”, coupled with a credit union that serves the

members of that Society, I believe that we can

achieve the regulatory model that we need to operate

at low cost without running afoul of government

authorities.

The credit union can act as the first digital gold

issuer, if need be, as well as host the first digital gold

forex exchange - giving us breathing room to grow

our user base as well as our technology and market.

The Society may establish procedures for identity

verification so that the credit union may rely upon

the assurance of a local chapter that Bob is really

Bob - and still satisfy the regulator.

Once the Society has all of its systems working

smoothly, we can apply for banking, securities and

forex exchange licenses in the countries where that

makes the most sense. As we grow, banks, credit

unions and other financial institutions may join the

Society as digital gold issuers.

This seems to me to be the least expensive and

lowest risk regulatory path to creating the Free Gold

Standard and Digital Gold 2.0.

My company, Dinero Limited, has created a pilot

institution in Kenya as a cooperative society that

issues gold accounts to its members and uses our

software to do it. We met with the central bank there

and they affirmed that so long as the cooperative

only offers accounts to members, it is minimally

regulated. We have not yet created a credit union,

but we have demonstrated that this approach can be

effective.3

3 Due to high corruption and weak rule of law, Kenya is not a suitable jurisdiction to act as a base for a worldwide society, which is why we are looking at other jurisdictions for the Gold Standard Society.

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 5

Conclusions

Lack of a viable regulatory model and domiciling in a

hostile jurisdiction were the primary causes of the

demise of the first generation of peer to peer, digital

gold currency systems.

There are multiple regulatory pathways to create an

institution that has the power to issue peer to peer,

digital gold accounts.

Of those pathways, a bank, a credit union, and a

savings cooperative are the three institutions that

offer the most regulatory protection and would still

leave us the freedom to pursue our business model

and goals.

The combination of a cooperative society with a

credit union seems likely to offer the greatest benefit

to us at the lowest cost.

The primary mission of the Gold Standard Society

will be to create a contractual framework to allow

many digital gold issuers to be interoperable. The

special powers of cooperative societies and credit

unions will enable the Society to set up the first

digital gold issuer, as well as a digital bullion market.

Ken Griffith

Ken Griffith can be contacted at [email protected]. Ken was

editor of The Gold Economy Magazine, VP Marketing at e-

Bullion.com, and later started web consulting company Cottage

Networks, LLC to develop quality websites for small companies.

Ken has served on the Dev Team at CMS Made Simple, and was

a founding member of the International Association for

Financial Cryptography in 1998. Ken's current project is Dinero

Limited, a social savings platform for smart phones that works

with social savings groups to improve financial inclusion in

Africa.

A Drawing-Board Currency as Ersatz

Constitution

Twelve years have passed since politicians

introduced the artificial currency euro to half of

Europe without bothering to ask the electorate.

These were turbulent times indeed: the new money

had to be rescued several times, no other currency

before has faced such massive criticism.

The amount of propaganda on behalf of the euro is

unprecedented in history, and the public debate

continues still. Why this should be the case will be

discussed in this article.

The Inception

Right from the beginning, this drawing-board

currency was different from its predecessors. In the

past, all participants in the marketplace introduced

money from the bottom-up. Usually, it emerged

victorious from a variety of competing alternatives

and was subsequently officially endorsed by the

political elites of the day.

In stark contrast, the euro was construed by politics

and introduced in a top-down manner.

On January 1, 2002 – after a rather short planning

and preparation phase (given the complexity of the

project) – humankind’s biggest currency experiment

began. Never before was a currency introduced:

across such diverse countries and regions,

with such varied cultures and ways of life,

with such different economic systems, and

at such different stages in their economic

cycle.

Why the haste, one might ask. After all, it was

commonly known that the different countries had

not converged economically or culturally to an

extent that would have made such a monetary union

feasible.

The mindboggling haste was due to the fact that EU

did not manage to agree on a constitution. Without a

constitution, though, the conglomerate would have

become an „ever closer union“ at a much slower

pace, if at all.

Uniting Peoples and Cultures in Four Steps

The failure to create a constitution is not due to

administrative incompetence but rather to the very

nature of the problem. Historically, societies have

united in a set sequence of steps. The process takes

several centuries and includes the following phases:

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 6

1. Trade

It all starts with an interest in other people’s goods.

Merchant routes and market places are established to

facilitate trade.

2. Foreign trade and military alliances

Military forces safeguard these trading routes.

Military alliances are founded to secure peace.

3. Language, cultural exchange

Travelling merchants bring back home knowledge of

different customs, languages, cuisine and cultures;

these are partially adopted by the people at home.

The exchange of cultures and habits as a major

foundation of unity has begun.

4. Sense of justice/legal system

At the very last moment, societies begin to adopt or

even unify legal habits. The legal system (which in

essence is a codification of prevailing moral

standards) is vital to the identity of individuals –

therefore, they are loath to change it.

With this historical background in mind, it is obvious

that people could not follow politicians’ visions with

their hearts and minds. Despite their pretty names,

the constitution substitutes (Maastricht and Lisbon

treaties) are of only limited use. Without a proper

constitution, the vision of a unified Europe was

doomed to fail. Haste then created the monster

called the euro, which was supposed to be a medium

for European integration and cohesion.

Function Shift

In order to make a political vision come true, legal

procedures were circumvented in a nimble way. An

ersatz medium in the shape of a currency was

created – and we cannot even picture where this will

all end.

The consequences of the shift from money’s original

function as a medium of exchange and store of value

towards constitution substitute can be already felt

everywhere.

While money (just about!) still works as a medium of

exchange, it cannot fulfil its role as a store of value

any more. The massive loss of purchasing power

people suffered since the euro introduction was

unimaginable in times of national currencies.

One might even suspect that this effect was not

altogether unintentional but rather part of the

creeping monetary dispossession of the people of

Europe.

Thomas Bachheimer

President of the Gold Standard Institute Europe

Comments on a Free Gold Standard

Last month Ken Griffith discussed the seven

elements needed for a new Free Gold Standard, a

Digital Gold 2.0. The early digital gold system Ken

discussed was of particular interest to me at the time

because of its possible strategic implications for the

Perth Mint. As a result, I recorded their weekly

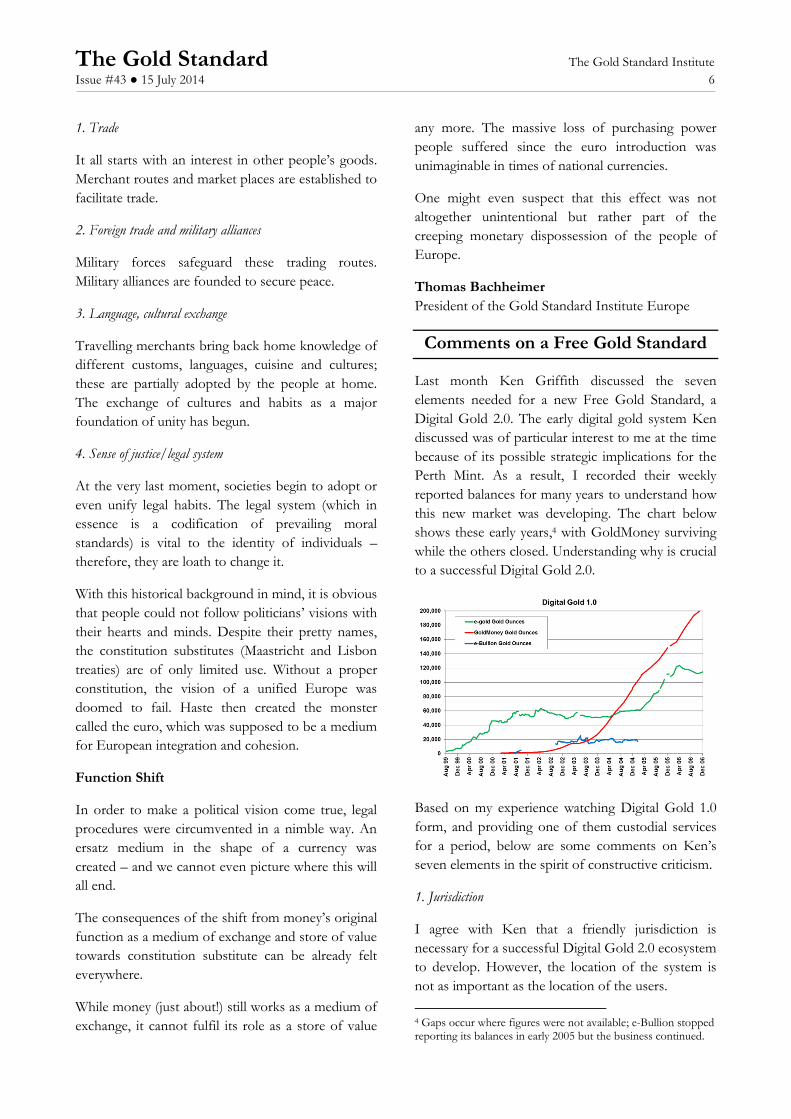

reported balances for many years to understand how

this new market was developing. The chart below

shows these early years,4 with GoldMoney surviving

while the others closed. Understanding why is crucial

to a successful Digital Gold 2.0.

Based on my experience watching Digital Gold 1.0

form, and providing one of them custodial services

for a period, below are some comments on Ken’s

seven elements in the spirit of constructive criticism.

1. Jurisdiction

I agree with Ken that a friendly jurisdiction is

necessary for a successful Digital Gold 2.0 ecosystem

to develop. However, the location of the system is

not as important as the location of the users.

4 Gaps occur where figures were not available; e-Bullion stopped reporting its balances in early 2005 but the business continued.

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 7

A capital gains tax on gold in the jurisdiction of the

user is a huge impediment to people in that country

using gold as money. As the value of fiat currencies

fluctuates around gold it creates gains and losses that

have to be accounted for (software can help with this

burden) and paid, something that does not apply to

the local currency.

While I would not argue that a capital gains tax is so

fatal to a Free Gold Standard that no one should

spend time developing the systems and institutions

for it, I would argue that the prime objective of

organisations such as the Gold Standard Institute

and those involved in digital gold systems should be

the repeal of capital gains taxes on gold in all

jurisdictions.

As a side note, I would argue that any person or

organisation that does not advocate for the

abolishment of such taxes would reveal themselves

as an advocate of a statist Gold Standard rather than

a Free Gold Standard.

2. Primary Specie for Contracts

I disagree with Ken’s recommendation that “we need a

standardized specie for gold contracts that is small enough to

be practical for daily transactions”. In his article on digital

gold 1.0, Ken states that it was a flaw that these

systems used “the spot price of 400 oz gold bars on the

London market, and their contracts were deliverable at that

spot price. To cause physical gold to circulate the digital gold

must be contractually deliverable in the smallest specie, not the

the largest one.”

These days the public is increasingly moving to

digital payments and away from physical cash, as

noted at a recent Mint Director's Conference.

Therefore I do not see that there will be much

demand for “physical gold to circulate”: why should

one need to “cause” it to circulate if the public does

not demand it? If the gold backing digital gold

systems is likely to sit still in a vault and rarely

circulate physically, then the objective should be to

minimize the cost of acquiring such gold.

Mandating the use of 1 gram bars or a similar small

size will add an excessive premium to the “gold

money” unit, a cost which paper currency does not

have. To obtain as wide an adoption as possible, one

needs to reduce friction costs between the digital

gold system and fiat currencies (which people will

have to move between for some time). If people will

lose a significant percentage of their wealth

converting into and out of digital gold because it has

to be backed by small forms of gold it will prevent

adoption.

The lowest cost form of gold is the internationally

accepted 400oz bar. Unlike small bars, the 400oz bar

is numbered, which will facilitate auditing and

transparency. It is a lot less costly to audit one 400oz

bar than 12,441 one gram bars. In addition, the

400oz bar has the greatest trading liquidity, ensuring

that a digital gold system is connected into the wider

gold market in the most efficient manner possible.

A digital gold system will face a fluctuating demand

for its money, as fiat currencies do. When there is a

surge in demand for gold, mandating one gram bars

will place a digital gold system at risk of an inability

to source product due to limited production capacity

in the industry, as we saw in 2008 following the

global financial crisis5. In periods when demand

reduces significantly and the gold behind a system

needs to be liquidated, small size bars or coins will

incur a cost to be melted into 400oz bars, resulting in

the gold money unit trading at a discount. Potential

users will see such systems as unstable in value with

a wide bid/ask spread relative to fiat currencies.

A further argument for the use of 400oz bars is that

each region has different preferences – Asia often

works in gram bars while the US prefers ounce

coins. Whatever form is chosen it is unlikely to have

worldwide appeal.

It would be far more effective for any users wishing

to convert into physical forms to be serviced by the

existing network of bullion dealers, and choose

whatever form or size they wish, rather than a

mandated standard. By leaving convertibility to the

free market a digital gold system is likely to get

enthusiastic engagement from existing bullion

dealers, which will go a long way to attracting

consumer use. Such dealers could also easily use a

5 http://goldchat.blogspot.com.au/2014/01/coin-shortages-and-rationing-are-in-our.html

The Gold Standard The Gold Standard Institute Issue #43 ● 15 July 2014 8

100% backed digital gold system as an alternative to

the London unallocated metal account system for

payment settlement with mints and distributors for

new stocks of small bar or coin.

3. Digital Gold Payments & Accounting

Inter-system clearing is essential for a viable digital

gold ecosystem. It is unlikely that digital gold system

operators in different countries would be willing to

use one global firm as a clearer and would prefer to

trust a local existing precious metal operator like a

refiner or mint, from whom their agent networks

and bullion dealers would source gold locally.

The use of 400oz bars would enable such local or

regional clearers to co-ordinate globally and at least

initially, piggy back off the existing London Precious

Metal Clearing Limited system.

4. Agent Network

To bootstrap a digital gold system existing bullion

dealers and FX operators will need to be accessed.

Even new operators will use existing over-the-

counter trading networks to hedge their transactions.

All of these ultimately settle gold into 400oz bars,

another reason why this should be the standard for a

digital gold system.

5. Electronic Exchanges

In his article, Ken claimed that “we need efficient foreign

exchange between gold and fiat currencies. Therefore we

eventually need an electronic trading market” giving the

example of Bitcoin, which has developed its own

exchanges.

In the case of Bitcoin, this was necessary because

Bitcoin had no prior history of value or exchange

rates with other currencies. This is not the case with

gold, which has a highly liquid market quoted in all

major currencies, and an extensive over-the-counter

network of traders, on which to draw.

In operation, consumers will value a 100% gold

backed digital gold system off existing gold market

pricing, so integration with the current market is

unavoidable. I am not sure of the advantages of

incurring costs in constructing new exchange(s)

when its prices and activity will be arbitraged back to

existing exchanges and the over-the-counter market

by traders in any case. I would suggest that it would

be better to use the existing system and save the cost

and headache of trying to duplicate it.

6. Dispute Resolution System

I agree with Ken that an arbitration or dispute

system voluntarily implemented by the digital gold

operators is essential. It will go a long way to

assuaging Government and regulators that this is a

responsible industry and will minimize the chance of

them taking a negative view of it.

7. Regulatory Model

Ken is correct that complying with existing

regulations is essential but I do not necessarily see

regulators “as wellmeaning parasites”. While it can be

argued that regulations can often be excessive in

areas, many just encode good corporate governance

practices and consumer expectations.

As Ken notes, “e-gold and the other systems were

overwhelmed with a wave of digital crime from 2001 onwards.

Hackers, auction fraud and Ponzi schemes were the primary

pathogens infecting the digital gold systems” - facilitated by

no or little identity verification for accounts.

Whether the US Government waged a “jihad”

against these digital gold systems, or was just validly

trying to shut down the extensive criminal activity

they allowed, it is clear from the earlier chart that the

two major players at the time were losing market

share to GoldMoney (which enforced know your

customer rules) well before any regulatory crack

down by the US Government. This indicates that the

public voted for an operation that complied with

regulatory rules, even if not required to do so.

For me this is the key lesson from the Digital Gold

1.0 experience: being a leader in governance and self-

regulation makes commercial sense as it is what the

mainstream consumer wants and goes a long way to

favourable regulatory treatment.

Bron Suchecki Bron Suchecki writes in a personal capacity and the views

expressed do not represent those of the Perth Mint.

![Gold Exchange Standard - FRASER · C. A* Conant, J* ¥• Jenks, Commissioners] GOLD STANDARD IN INTERNATIONAL TRADE; Report on the Introduction of the Gold-Exchange Standard into](https://static.fdocuments.in/doc/165x107/5ec0eaeb138a746b2f509087/gold-exchange-standard-fraser-c-a-conant-j-a-jenks-commissioners-gold.jpg)