The global financial crisis - Impact on Irish banks and regulations

22

1 Electronic Assignment Cover sheet Students Number : Maria Petronela Toma 1642529 Magdalena Maria Grzes 1645065 Course Title: MSc International Banking and Finance Lecturer Name: Enda Murphy Module/Subject Title: International Financial Institutions and Markets Assignment Title: The Global Financial Crisis – Impact on Banks and Regulation No of Words: 3172

-

Upload

maria-pusha -

Category

Documents

-

view

222 -

download

0

Transcript of The global financial crisis - Impact on Irish banks and regulations

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 1/22

1

Electronic Assignment Cover sheet

Students Number :

Maria Petronela Toma 1642529

Magdalena Maria Grzes 1645065

Course Title: MSc International Banking and Finance

Lecturer Name: Enda Murphy

Module/Subject Title: International Financial Institutions and Markets

Assignment Title: The Global Financial Crisis – Impact on Banks and Regulation

No of Words: 3172

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 2/22

2

Contents

Abbreviations ...................................................................................................................................... 3

The Global Financial Crisis – Impact on Irish Banks and Regulation ....................................................... 4

1. Introduction .................................................................................................................................... 4

2. The impact on Irish banks ̀ liquidity, profitability and solvency .................................................... 5

3. The managerial shortcomings in banks and the deficiencies in bank regulation ......................... 9

4. Irish Government Interventions in Financial Markets .................................................................. 12

5. Conclusions ................................................................................................................................... 14

References ........................................................................................................................................ 15

Appendices ........................................................................................................................................ 18

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 3/22

3

The Global Financial Crisis – Impact on Irish Banks and Regulation

Abbreviations

AIB Allied Irish Bank

Anglo Anglo Irish Bank

ATM Automated Teller Machine

BIS Bank for International Settlements

bn billion

BoI Bank of Ireland

CB Central Bank of Ireland

EBS Educational Building Society

ECB European Central Bank

EU European Union

FR Financial Regulator

GDP Gross Domestic Product

GNP Gross National Product

IL & P Irish Life and Permanent

IMF International Monetary Fund

INBS Irish Nationwide Building Society

NAMA National Asset Management Agency

OECD Organization for Economic Co-operation and Development

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 4/22

4

The Global Financial Crisis – Impact on Irish Banks and Regulation

1. Introduction

The economy of Ireland has changed in recent years from an agricultural focus to a

modern knowledge economy and transformed itself from one of Europe‟s poorest countries

into one of its wealthiest, earning itself the nickname “Celtic Tiger” (The Guardian, 2009).

The boom started in the late 1980s and brought rising investment and growth in employment

and household formation, this economic miracle being widely admired and emulated (Central

Bank, 2010, p. 20-21)

Once with the 2008 global financial crisis, the Irish economy has been one of the

worst-hit euro-zone economies due to the high exposure of the banking sector to the property

market and the boom associated with that over the recent history (Mayer Brown, 2009, p. 1).

In early January 2009, a Irish Times editorial stated that: “We have gone from the Celtic

Tiger to an era of financial fear with the suddenness of a Titanic-style shipwreck, thrown

from comfort, even luxury, into a cold sea of uncertainty” (The Irish Times, 2009a).

The collapse of the building boom left Irish banks facing large losses to builders and

developers. Despite denials by the banks that they faced any difficulties, their share prices

started to slide steadily after March 2007. The crisis came to a peak on 29 September with a

run in wholesale markets on the most aggressively expansionary of the Irish banks, Anglo-

Irish. (Kelly, 2009)

Nearly 15,000 financial service providers are authorized by the Irish Financial

Regulator with over 80 authorized credit institutions (Financial Regulator, 2009). The main

retail banks in Ireland are Allied Irish Bank (AIB), Bank of Ireland, Ulster Bank, National

Irish Bank, Permanent TSB and Bank of Scotland (Ireland).

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 5/22

5

The purpose of this paper is to investigate the global financial crisis in Ireland and the

impact it had on its banks and regulation. The paper is divided in five sections: the first part

briefly presents the economic context, the following section shows the extent to which the

global financial crisis has impacted bank liquidity, profitability and solvency in Ireland. The

third section analyzes the extent to which managerial shortcomings in the Irish banks, and

deficiencies in bank regulation, have contributed to the financial crisis. The fourth section

presents the Irish Government interventions in financial markets to stabilise banks and

prevent disorderly failures and the last part summarizes the findings and provides a

conclusion.

2. The impact on Irish banks ` liquidity, profitability and solvency

The Basel Committee of Banking supervision defines funding liquidity as the ability

of banks to meet their liabilities, unwind or settle their positions as they come due (BIS,

2008). In other words, liquidity refers to banks‟ funds, funds that mostly consist of customer

deposits and various bonds and which are used for their daily operations, such as filling

ATMs or issuing loans. Solvency is the ability of a business to have enough assets to cover its

liabilities. Banks can become insolvent if they suffer big losses on their assets (mortgages,

loans or government bonds) and are obliged by law to hold certain reserves of capital in order

to avoid insolvency.

A bank manages the risk that too many of its lenders will look for their money all in

the same time by holding cash reserves, and by using the money markets for short-term

borrowing. According to the Governor of the Irish Central Bank (Central Bank, 2010,

P.121), Irish banks, for fifty years, had no difficulty in accessing any short term funding

needed, thus never had to deal with liquidity problems, but starting with August 2007, and

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 6/22

6

especially with the events of September 2008, the access of banks worldwide to short-term

borrowing became very constrained, as risk aversion and uncertainty rose. Governor

Honohan also argues that putting a solvent but illiquid bank into bankruptcy is an

unnecessary cost for the society, and this is when emergency liquidity assistance from the

central bank becomes necessary. However, the main difficulty is determining whether the

bank is solvent or not.

Before the 2008 crisis hit, there were no major concerns about the health of the

banking sector. In 2006, IMF stated: “Financial institution profitability and capitalisation are

currently very strong, with Irish banking sector profits amongst the highest in Western

Europe. Reflecting their good performance, the major Irish banks receive upper medium to

high-grade ratings from the international ratings agencies.” (IMF, 2006, p.5)

Starting with 2007, some liquidity concerns emerged, but they were not considered

major threats to the banking system. According to Honohan, although a Liquidity Group was

established by the Central Bank in early 2008 to obtain information on liquidity

developments from the main credit institutions and to identify any potential problems at an

early stage, a comprehensive picture of the actual liquidity flows had not been put in place

before early 2009. During 2008, the liquidity situation deteriorated, as reflected in the

unprecedented recourse to financing from the European Central Bank which rose from a

monthly average of around €6 billion in September 2007 to €20 billion in September 2008.

(Central Bank, 2010, 116-117)

In early September 2008, the diminishing access of banks to liquidity became the

urgent focus of attention for Central Bank. Anglo Irish Bank was the most vulnerable but the

Central Bank considered the problem essentially one of liquidity rather than of solvency.

In the following paragraphs, the situation of the profitability, liquidity and solvency in

the three most problematic Irish banks is discussed.

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 7/22

7

Anglo Irish Bank

Anglo is a property-focused commercial lending bank that accumulated more than

€100 billion in assets by September 2008, helped by a substantial reliance on wholesale

funding. (Standard & Poor, 2011a)

In August 2008 Anglo Irish Bank released an Interim Management Statement that was

in line with expectations that the company`s earnings would rise 15% for the full year to

September 30th. Anglo stated that the economic environment would remain significantly

challenged, but according to Fitch Ratings Anglo„s long-term rating at A+ remained stable.

(Central Bank, 2010, p.162)

In just a month, the situation of the bank changed entirely with the fall of the property

market and the wholesale funding market dislocation, leading to the bank`s nationalisation in

January 2009. Since 2009, Anglo has been making important losses. The bank reported at the

end of March 2010 a €17.7 billion loss, the largest in Irish corporate history (Reuters, 2010)

bringing its cumulative loss to €30.4 billion since October 2008. The 2010 result reflected a

loan impairment charge of €19.3 billion, which, according to Standard & Poor (2011a)

clearly exceeded Anglo's €1.8 billion operating profit that came largely from a one-time €1.6

billion gain on the repurchase of its own hybrid securities (see Table 1 in Appendices).

As a result of the losses, Anglo has been heavily reliant on capital support from the

Irish government, and in order to avoid insolvency and collapse, the bank was nationalized in

December 2008, when the Irish government announced plans to inject €1.5bn of capital for a

75% stake in the bank. (The Telegraph, 2008)

Anglo and Irish Nationwide Building Society experience liquidity issues and therefore

are entirely dependent on the Irish central bank for future funding via its Emergency

Liquidity Assistance program (see Table 2 in Appendices). At the beginning of July 2011 the

legal merger of the INBS business into Anglo took place.

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 8/22

8

Bank of Ireland

Over the past years Bank of Ireland's performance has also been severely affected by

the consequences of the sharp falls in property prices, the general dislocation of the wholesale

funding markets, and specifically weak investor appetite for exposures to Irish banks.

Through the crisis time, BoI has benefited from significant government support: capital

injections, the purchase of BoI's weakest property-related loans by the National Asset

Management Agency, and access to liquidity from the monetary authorities. Standard &

Poor`s (2011b) states that the liquidity support was most evident through the third and fourth

quarters of 2010 when BoI, like many domestically owned Irish banks, saw a marked outflow

of wholesale deposits.

Standard & Poor`s (2011b) calculated the bank`s pre tax loss at €3,442 million for

2010, compared with an underlying pre tax loss of €2,839 million for the nine months to end-

2009. Even with the weakest loans having been transferred to NAMA and anticipating a

continued tight focus on operating expenses, S&P expects BoI's earnings through 2011 and

2012 to continue to decrease (see Table 3 and Table 4 in Appendices).

AIB

In August 2008, AIB released the results for the first half of the year, which were

generally in line with expectations of pre-tax profits of just over €1.3 billion for the first half

of 2008, up 8.6% on the same period of 2007, but the bank announced it expects earnings per

share to decline by 8-10 percent instead of the previous growth. (Central Bank, 2010, 161-

162)

By the end of 2008, the situation of AIB`s profitability reversed. According to

Moody`s (2009) the 2008 operating profit after provisions for impairment was reduced by

62% to 862 million euro, compared to 2007. Moody`s saw a weakening trend in AIB`s

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 9/22

9

profitability and a neutral trend in its liquidity. AIB`s liquidity was impacted by its growing

reliance on market funding, which decreased in 2008, reducing the bank`s loan to deposit

ratio at the end of 2008 to 142% from 158% in 2007. (Moody`s 2009)

3. The managerial shortcomings in banks and the deficiencies in bank

regulation

As capital adequacy and risk management go to the core of the operations of a bank,

the ability of directors to understand the internal governance of banks is critical in order to

exercise sound judgment about the affairs of the bank. (Kostyuk, Takeda, Hosono, 2010,

p.79) These requirements are reflected in the Basel Committee on Banking Supervision„s

principles of corporate governance for banking organizations (BIS, 2006). The Basel

Committee emphasised that poor corporate governance risk may lead to the bank losing

market confidence, which may further lead to a liquidity crisis or trigger a bank run.

According to Kostyuk, Takeda, Hosono (2010) this resonates in the Irish context as poor

governance was a contributory factor to the situation which emerged in the case of Anglo

Irish Bank in 2008 and early 2009 prior to and subsequent to nationalisation.

In Ireland, the management of all banks lost awareness of the riskiness of their

portfolios, assuming that prices could only go on rising or, at worst, stabilise. The best

example of mismanagement of Irish financial institutions was Anglo Irish Bank, which

through aggressive property lending had gone from an insignificant merchant bank in the

1990s to the joint-second largest bank by 2007. The two large retail banks, AIB and Bank of

Ireland came under pressure from analysts to match the profits and growth of Anglo Irish.

(Kelly, 2009, p.23)

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 10/22

10

The chairman Sean FitzPatrick, CEO David Drumm, and board member Lars

Bradshaw of Anglo Irish Bank, all resigned in December 2008, following the revelation of a

loan scandal (RTE, 2008). FitzPatrick and Bradshaw took out loans in order to purchase

Anglo Irish shares. From 2000 – 2008, FitzPatrick transferred the loans to another bank prior

to year-end audits, therefore causing "Loans to Directors" to be understated. In 2008, the loan

to FitzPatrick and Bradshaw reached €87 million but the transfer resulted in the accounts

showing only about €40 million outstanding to directors, instead of €150 million. The head of

the Financial Regulator, Patrick Neary was pressured into resignation in January 2009, as

financial authorities failed to prevent this behaviour.

On 12 February 2009, details of a further controversial transaction misrepresenting

the accounts of Anglo-Irish Bank became public. Anglo-Irish Bank lent €4bn to Irish Life &

Permanent (IL&P) for 1 day as an inter-bank loan, and a subsidiary of Irish Life placed a

deposit of a similar amount with Anglo, which was recorded as a customer deposit.

Following a discussion with the Minister for Finance, a board meeting of IL&P accepted the

resignation of two senior IL&P executives. (The Irish Times, 2009b)

Moreover, a related concern is the practice of Irish directors to hold a number of

simultaneous directorships in major companies. Grant Thornton Corporate Governance

Review (2009) gives a few examples, of which the Chairman of Anglo Irish Bank who was a

director of four other Irish listed companies. Similarly, directors of AIB and IL&P were also

the directors of four other Irish listed companies, this practice being inappropriate at times of

crisis.

Although the Irish financial regulatory system was perceived as robust and modern,

the Irish banking crisis has brought to the surface its shortcomings (Kostyuk, Takeda,

Hosono, 2010, p.81). Nyberg (2011) considers that the Central Bank and the Financial

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 11/22

11

Regulator was aware of the risks but appear to have judged them insufficiently alarming to

take major restraining policy measures.

An OECD report suggests that the supervisory issues that contributed to the Irish

banking crisis were two-fold (OECD, 2009, p.36). Firstly, the corporate governance issues at

Anglo Irish Bank and the facilitation of the transfer of the loans to other credit institutions

suggest that the threat of enforcement by the Financial Regulator was too weak. Secondly, the

OECD (2009) suggested that excessive lending growth was tolerated by the Irish Financial

Regulator despite very high asset growth being a well-established predictor of banking

difficulties. In addition, the OECD suggested that the Irish Financial Regulator failed to

recognise the full impact and the riskiness of the decisions taken by each financial institution.

Nyberg (2011) considers there was a general state of denial in the Central Bank,

where the belief in a soft landing was consistent and probably continued up until and

including the crisis management phase. “The problems in Anglo and INBS in particular, were

not hidden but were in plain sight of the FR and the CB. The funding strategy of Anglo was

obvious from its balance sheet and the concentration to the more speculative part of the

market was generally known. Similarly, INBS‟s expansion into development lending was

also clearly documented and the governance problems in the bank were widely known by the

authorities.” (Nyberg, 2011, p.vii)

According to Nyberg (2011), neither the Central Bank nor the Department of Finance

seem to have considered the implications of a possible interruption in the flow of foreign

funding. The Department of Finance and the Minister for Finance were regularly provided

with a Financial Stability Report, written by the Central Bank and the Financial Regulator,

report that did not warn about the serious risks the banks could face because of this bubble.

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 12/22

12

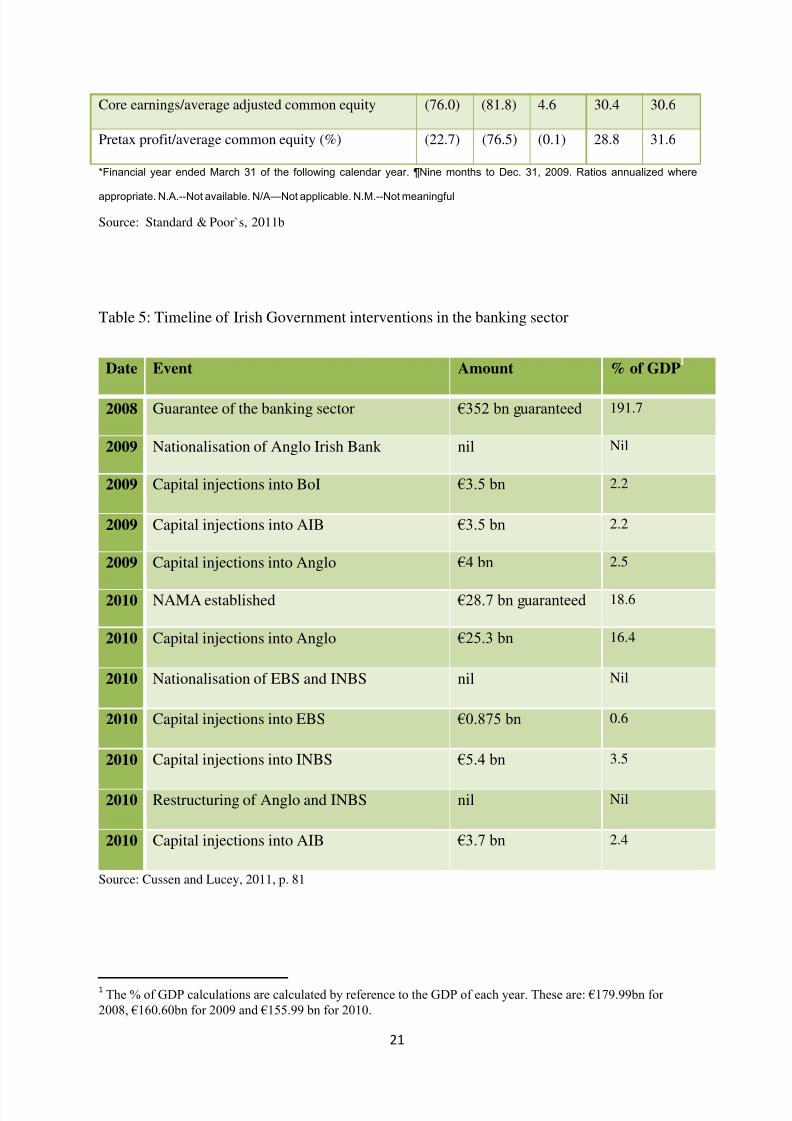

4. Irish Government Interventions in Financial Markets

Since September 2008 the Irish Government has had to intervene significantly in the

banking sector in a myriad of ways. These have included guaranteeing the Irish banking

sector, nationalizing and restructuring distressed banks, creating an entity to manage impaired

assets, and providing capital injections (see Table 5. in Appendices) (Cussen and Lucey,

2011, p. 84).

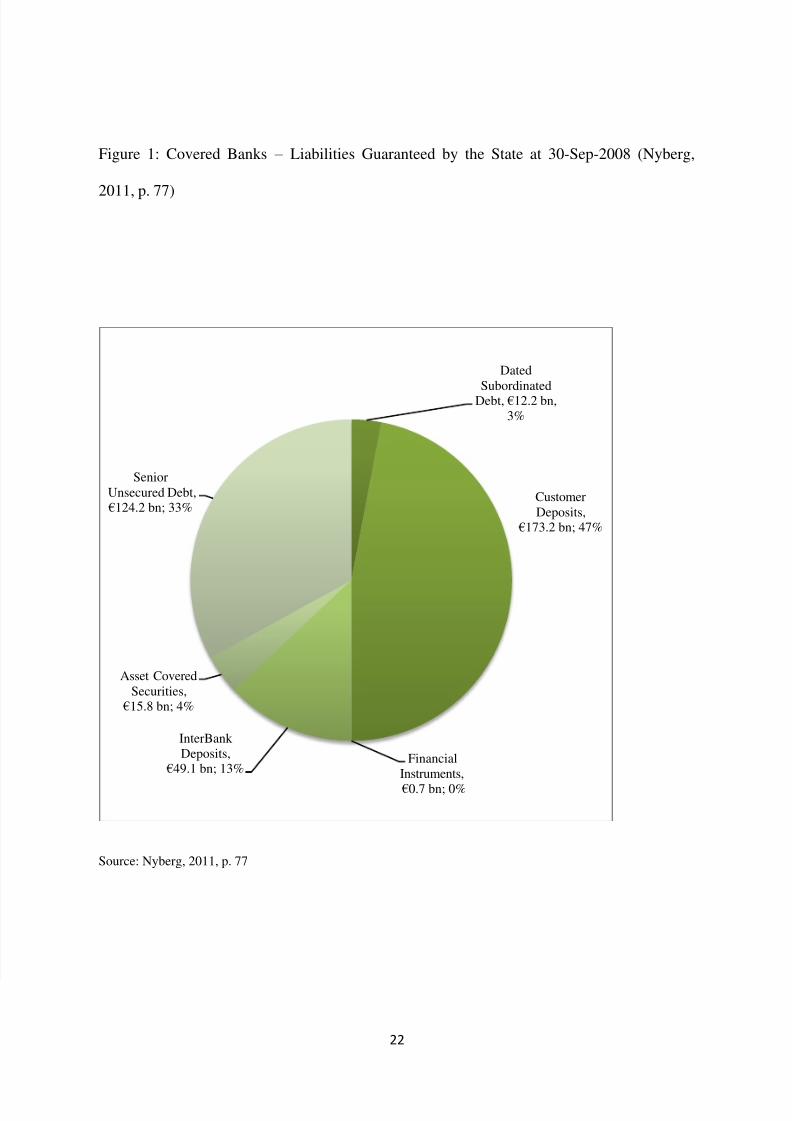

State guarantees:

In September 2008, the Irish Government advertised a state guarantee that intended to

save the Irish banking system. The Irish State guaranteed for the deposits, senior debt and

dated subordinated debt of participating Irish credit institutions for the period until 29

September 2010. The State covered liabilities include retail and corporate deposits, interbank

deposits, senior unsecured debt, covered bonds and, subject to certain restrictions,

subordinated debt (see Figure 1. in Appendices) (Nyberg, 2011, p. 77). Liabilities covered

initially amounted to €352 billion, which was equivalent to almost three times the value of

Irish GDP (Cussen and Lucey, 2011, p. 83). The Irish state covered under the deposit

protection scheme for banks and buildings societies form up to a maximum of €100,000 per

qualifying deposits per institution.

Capital injections:

In late December 2008, the Irish Government decided to support a recapitalization

program for credit institutions through the National Pension Reserve Fund. Since 2009, up to

October 2011, the Irish authorities have provided the banking sector with capital injections

amounting to €64 billion. (Cussen and Lucey, 2011)

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 13/22

13

In 2009 the Irish State provided two Irish banks, Allied Irish Bank and Bank of

Ireland, with capital injections of €3.5 billion each. The largest capital injections were

provided to Anglo and INBS. During 2010, capital injections to Anglo and INBS totaled

€25.3 billion and €5.4 billion (Cussen and Lucey, 2011, p. 82).

European Commission (2011) summed the capital injections into Irish banks during the

crisis, as of 28 January 2011, to €46.3bn (29% of GDP) as follows:

Anglo Irish Bank -Total: €29.3bn (18.3 % of GDP)

Allied Irish Bank (AIB) - Total: €7.2bn (4.5% of GDP)

Bank of Ireland - Total: €3.5bn (2.25% of GDP)

Irish Nationwide Building Society - Total: €5.4bn (3.5% of GDP),

EBS Building Society - Total: €0.9bn (0.5% of GDP)

National Asset Management Agency (NAMA):

In early 2009, the Irish Government announced a further government initiative

concerning establishing an asset management company, the National Asset Management

Agency. The Agency has acquired portfolios of property loans from banks operating in

Ireland in return for issue of Irish government bonds to the banks. These government bonds

are intended to enable Irish banks to access liquidity and provide credit to the Irish economy

over an extended period of up to ten years (NAMA, 2010, p. 2). The purchases would be

funded by NAMA issuing debt securities, 95 per cent of which were guaranteed by the Irish

Government (Cussen and Lucey, 2011, p. 85).

Public ownership of banks:

By the end of July 2011, the Irish State had provided €64 billion of capital to the six

Irish banks. These large capital injections mean that most of these banks are now owned by

the State. In January 2009, Anglo was the first bank to pass into public ownership, followed

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 14/22

14

in the middle of 2010 by EBS and INBS, and at the end of 2010 by AIB (Cussen and Lucey,

2011, p. 87). At the beginning of 2011 Anglo and INBS merged into a single company

renamed the Irish Bank Resolution Corporation (IBRC).

5. Conclusions

During the boom years the Irish banks experienced continuous growth and

profitability, followed after September 2008 by a free fall. They lost liquidity, went from

huge profits to huge losses and some were even threatened with insolvency. Although the

crisis had been building for 18 months, the government and financial regulators appear to

have been taken entirely by surprise. The authorities were obliged then to take unpopular

measures in order to safeguard the Irish banking system, injecting billions in some banks

from the taxpayer`s “pocket”.

The purpose of any business is to make profit by taking risks, but the group thinking

and herding, which were common amongst banks, made them not see the risks they took as

threatening, at any point. The financial institutions were blinded by success, and we think that

none of them wanted to even take in consideration the risks, because of the fear that they will

lose the race towards higher profitability. The fear of losing the entire business was

somehow forgotten and replaced with the “fear” of not taking enough advantage of the

infinite opportunities to make huge profits that were on the market.

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 15/22

15

References

1. BIS. 2006. Basel Committee on Banking Supervision Enhancing corporate governance for

banking organizations [Online] Available:

http://www.bis.org/publ/bcbs122.pdf [9 November 2011]

2. BIS. 2008. Basel Committee on Banking Supervision. Liquidity Risk: Management and

Supervisory Challenges [Online] Available:

http://www.bis.org/publ/bcbs136.pdf [9 November 2011]

3. Central Bank. 2010. The Irish Banking Crisis Regulatory and Financial Stability Policy

2003-2008. A Report to the Minister for Finance by the Governor of the Central Bank .

Dublin, Central Bank.

4. Cussen, M. and Lucey, M. 2011. Treatment of Special Bank Interventions in Irish

Government Statistics. Cork: Central Statistic Office. Available:

http://www.centralbank.ie/publications/Documents/Treatment%20of%20Special%20Bank%20Interventions%20in%20Irish%20Government%20Statistics.pdf [28 October 2011]

5. European Commission. 2011. The Economic Adjustment Programme for Ireland.

Available:

http://ec.europa.eu/economy_finance/publications/occasional_paper/2011/pdf/ocp76_en.pdf

[9 November 2011]

6. Financial Regulator. 2009. Annual Report of the Financial Regulator 2008 , Dublin: The

Financial Regulator.

7. Grant Thornton. 2009. ISEQ Corporate Governance Review 2009, Grant Thornton, Dublin.

[Online] Available:

http://www.grantthornton.ie/db/Attachments/Publications/Public_interest/Grant%20Thornton%20Cor

porate%20Governance%20Review%202009.pdf [9 November 2011]

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 16/22

16

8. Kostyuk, A.N., Takeda, F., Hosono K. 2010. Anti-crisis paradigms of corporate

governance in banks: a new institutional outlook . [Online] Available:

http://www.ucema.edu.ar/u/ra/Books_and_Contributory_Chapters_in_Edited_Books_-

_/Contributory_Chapters_in_Edited_Books/Apreda_-_State-

Owned_Banks_in_Latin_America_-_Edited_by_Kostyuk.pdf [9 November 2011]

9. Kelly, Morgan. 2009. The Irish Credit Bubble. WP09/32, UCD Centre for Economic

Research. [Online] Available: http://www.ucd.ie/t4cms/wp09.32.pdf [9 November 2011]

10. IMF. 2006, Financial Sector Assessment Report , International Monetary Fund.

11. Irish Deposits. Guarantee Schemes. [Online] Available:

http://www.irishdeposits.ie/Guarantee_schemes[8 November 2011]

12. Mayer Brown. 2009. Summary of Government Interventions in Financial Markets

Ireland. [Online]. Available:

http://www.mayerbrown.com/london/article.asp?id=7851&nid=369 [8 November 2011]

13. Moody`s. 2009. Credit Opinion: Allied Irish Banks, plc. Dublin [Online] Available:

http://www.aib.ie/servlet/BlobServer/document.pdf?blobkey=id&blobwhere=125267695903

0&blobcol=urlfile&blobtable=AIB_Download&blobheader=application/pdf&blobheadernam

e1=Content-Disposition&blobheadervalue1=document.pdf [9 November 2011]

14. RTE. 2008. Chairman of Anglo Irish Bank Sean Fitzpatrick has resigned in a controversy

over directors' loans. [Online] Available:

http://www.rte.ie/news/2008/1218/fitzpatricks.html [8 November 2011]

15. Nyberg, P. 2011. Misjudging risk: Causes of the Systemic Banking Crisis in Ireland.

Report of the Commission of Investigation into Banking Crisis in Ireland. Available:

www.bankinginquiry.gov.ie [29 October 2011]

16. National Asset Management Agency (NAMA). 2010. The National Asset Management

Agency: A Brief Guide. Available:

http://www.irishtimes.com/focus/2010/namaguide/index.pdf [1 November 2011]

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 17/22

17

17. OECD. 2009. OECD Economics Surveys: Ireland 2009 [Online] Available:

http://www.irishtimes.com/focus/2009/oecd/index.pdf [9 November 2011]

18. Reuters. 2010. Anglo Irish Bank posts Ireland's biggest ever loss. [Online]

http://www.reuters.com/article/2010/03/31/us-angloirishbank-idUSTRE62U38C20100331

[9 November 2011]

19. Standard & Poor`s. 2011a. Ratings Direct: Anglo Irish Bank Corp. Ltd. Available:

http://www.ibrc.ie/Investors/Credit_Ratings/S_P_updates_its_research_on_Anglo_Irish_Ban

k.pdf [9 November 2011]

20. Standard & Poor`s. 2011b. Ratings Direct: Bank of Ireland [Online] Available:

http://www.bankofireland.com/fs/doc/wysiwyg/Report%20on%20Bank%20of%20Ireland.pd

f [9 November 2011]

21. The Irish Times. 2009a. No time for whingers. 1 January 2009 [Online]. Available:

http://www.irishtimes.com/newspaper/opinion/2009/0103/1230842387565.html

[6 November 2011]

22. The Irish Times. 2009b. Statement by Irish Life & Permanent [Online]. Available:

http://www.irishtimes.com/newspaper/breaking/2009/0213/breaking12.html?via=rel

[7 November 2011]

23. The Guardian. 2009. Why the party’s over in Ireland. 18 January 2009 [Online].

Available: http://www.guardian.co.uk/business/2009/jan/18/ireland-economy-crash

[6 November 2011]

24. The Telegraph. 2008. Ireland pours €5.5bn into banking sector and takes control of

Anglo Irish [Online]

http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/3899326/Ireland-pours-

5.5bn-into-banking-sector-and-takes-control-of-Anglo-Irish.html [9 November 2011]

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 18/22

18

Appendices

Table 1: Anglo Irish Bank Corp. Ltd. Asset Quality, Funding and Liquidity Ratios

-Year-ended Dec. 31-

(%) 2010 2009 2008 2007 2006

Gross nonperforming assets/customer loans plus

other real estate owned

45.8 29.6 1.3 0.5 0.5

Net nonperforming assets/customer loans plus other

real estate owned

24.7 10.9 0.1 0.1 (0.0)

Loan loss reserves/gross nonperforming assets 61.2 70.9 95.5 88.1 102.7

Loan loss reserves/customer loans 28.1 21.0 1.3 0.4 0.5

New loan loss provisions/average customer loans 14.5 20.9 1.3 0.3 0.2

Net charge-offs/average customer loans 0.7 0.1 0.1 0.1 0.0

Customer deposits/funding base 17.1 35.3 56.4 61.3 60.1

Total loans/customer deposits 326.4 265.7 144.4 128.9 134.8

Total loans/customer deposits plus long-term funds 164.3 150.2 100.0 84.7 93.7

Customer loans (net)/assets (adjusted) 36.0 66.1 71.2 68.3 67.1

Source: Standard & Poor`s, 2011a

Table 2: Anglo Irish Bank Corp. Ltd. Profitability Ratios

-Year-ended Dec. 31-

(%) 2010 2009 2008 2007 2006

Net interest income/average earning assets 0.9 1.7 2.0 2.0 1.9

Net interest income/revenues 161.7 179.6 97.3 88.8 85.9

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 19/22

19

Fee income/revenues (14.2) (21.0) 6.8 9.1 10.7

Market-sensitive income/revenues (14.8) (56.7) (5.3) 1.1 2.2

Personnel expense/revenues 28.3 22.6 10.6 13.3 16.9

Noninterest expenses/revenues 57.5 40.5 16.9 22.3 26.4

New loan loss provisions/revenues 1,692.2 1,779.2 45.3 8.5 5.3

Pretax profit/revenues (3,838.6) (1,511.8) 40.4 70.5 68.3

Tax/pretax profit (0.2) 0.9 15.3 18.9 22.6

Noninterest expenses/average adjusted assets 0.3 0.4 0.3 0.5 0.5

Pretax profit/average common equity (457.5) (309.5) 19.2 36.9 39.0

Source: Standard & Poor`s, 2011a

Table 3: Bank of Ireland Asset Quality, Funding and Liquidity Ratios

-Year-ended Dec. 31-

(%) 2010 2009¶ 2008* 2007* 2006*

Gross nonperforming assets/customer loans plus

other real estate owned

10.7 10.9 4.7 1.1 1.1

Net nonperforming assets/customer loans plus other

real estate owned

6.8 6.9 3.5 0.7 0.8

Loan loss reserves/gross nonperforming assets 39.3 39.2 27.8 39.4 30.9

Loan loss reserves/customer loans 4.2 4.3 1.3 0.4 0.3

New loan loss provisions/average customer loans 3.5 4.0 1.1 0.2 0.1

Net charge-offs/average customer loans 0.6 0.1 0.2 0.0 0.0

Customer deposits/funding base 47.6 56.3 51.4 52.0 46.2

Total loans/customer deposits 183.8 158.8 163.0 158.1 173.6

Total loans/customer deposits plus long-term funds 124.4 109.5 113.8 108.1 134.7

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 20/22

20

Customer loans (net)/assets (adjusted) 73.3 75.2 71.8 72.9 71.3

*Financial year ended March 31 of the following calendar year. ¶Nine months to Dec. 31, 2009. Ratios annualized where

appropriate. N.A.--Not available. N/A—Not applicable. N.M.--Not meaningful.

Source: Standard & Poor`s, 2011b

Table 4: Bank of Ireland Profitability Ratios

-Year-ended Dec. 31-

(%) 2010 2009¶ 2008* 2007* 2006*

Net interest income/average earning assets 1.4 1.7 2.0 1.8 1.6

Net interest income/revenues 71.9 78.3 89.3 70.9 65.2

Fee income/revenues 13.1 8.4 12.6 15.7 19.0

Market-sensitive income/revenues (4.4) (0.8) (9.5) (5.7) (1.5)

Personnel expense/revenues 35.0 30.3 30.7 29.1 32.0

Noninterest expenses/revenues 62.2 53.2 54.7 50.7 55.5

New loan loss provisions/revenues 157.8 155.7 39.3 5.5 2.6

Net operating income before loan loss

provisions/loan loss provisions

23.9 30.0 115.4 902.6 1,680.6

Net operating income after loan loss

provisions/revenues

(120.0) (109.0) 6.1 43.8 41.9

Pretax profit/revenues (33.1) (69.5) (0.2) 45.5 50.3

Tax/pretax profit 35.9 19.0 585.7 11.8 15.6

Core earnings/revenues (103.1) (92.8) 6.2 38.6 35.5

Core earnings/average adjusted assets (1.8) (1.8) 0.1 0.9 0.8

Noninterest expenses/average adjusted assets 1.1 1.0 1.1 1.2 1.3

Core earnings/average risk-weighted assets N.M N.M 0.4 1.4 1.3

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 21/22

21

Core earnings/average adjusted common equity (76.0) (81.8) 4.6 30.4 30.6

Pretax profit/average common equity (%) (22.7) (76.5) (0.1) 28.8 31.6

*Financial year ended March 31 of the following calendar year. ¶Nine months to Dec. 31, 2009. Ratios annualized where

appropriate. N.A.--Not available. N/A—

Not applicable. N.M.--Not meaningful

Source: Standard & Poor`s, 2011b

Table 5: Timeline of Irish Government interventions in the banking sector

Date Event Amount % of GDP

2008 Guarantee of the banking sector €352 bn guaranteed 191.7

2009 Nationalisation of Anglo Irish Bank nil Nil

2009 Capital injections into BoI €3.5 bn 2.2

2009 Capital injections into AIB €3.5 bn 2.2

2009 Capital injections into Anglo €4 bn 2.5

2010 NAMA established €28.7 bn guaranteed 18.6

2010 Capital injections into Anglo €25.3 bn 16.4

2010 Nationalisation of EBS and INBS nil Nil

2010 Capital injections into EBS €0.875 bn 0.6

2010 Capital injections into INBS €5.4 bn 3.5

2010 Restructuring of Anglo and INBS nil Nil

2010 Capital injections into AIB €3.7 bn 2.4

Source: Cussen and Lucey, 2011, p. 81

1 The % of GDP calculations are calculated by reference to the GDP of each year. These are: €179.99bn for

2008, €160.60bn for 2009 and €155.99 bn for 2010.

7/30/2019 The global financial crisis - Impact on Irish banks and regulations

http://slidepdf.com/reader/full/the-global-financial-crisis-impact-on-irish-banks-and-regulations 22/22

22

Figure 1: Covered Banks – Liabilities Guaranteed by the State at 30-Sep-2008 (Nyberg,

2011, p. 77)

Source: Nyberg, 2011, p. 77

Dated

SubordinatedDebt, €12.2 bn,

3%

Customer

Deposits,

€173.2 bn; 47%

Financial

Instruments,

€0.7 bn; 0%

InterBank

Deposits,

€49.1 bn; 13%

Asset Covered

Securities, €15.8 bn; 4%

Senior

Unsecured Debt,

€124.2 bn; 33%