The global economy effects on commodity dependent countries like zambia

19

The Global Economy Effects on Commodity Dependent Countries like Zambia 17 th November 2016 Kampamba Shula US Job Market China PMI Global Commodity Trends The Dollar Effect The Trump Effect Global Copper Outlook Zambia Copper Outlook

-

Upload

kampamba-shula -

Category

Economy & Finance

-

view

274 -

download

0

Transcript of The global economy effects on commodity dependent countries like zambia

The Global Economy

Effects on Commodity Dependent Countries like Zambia

17th November 2016

Kampamba Shula

US Job Market

China PMI

Global Commodity Trends

The Dollar Effect

The Trump Effect

Global Copper Outlook

Zambia Copper Outlook

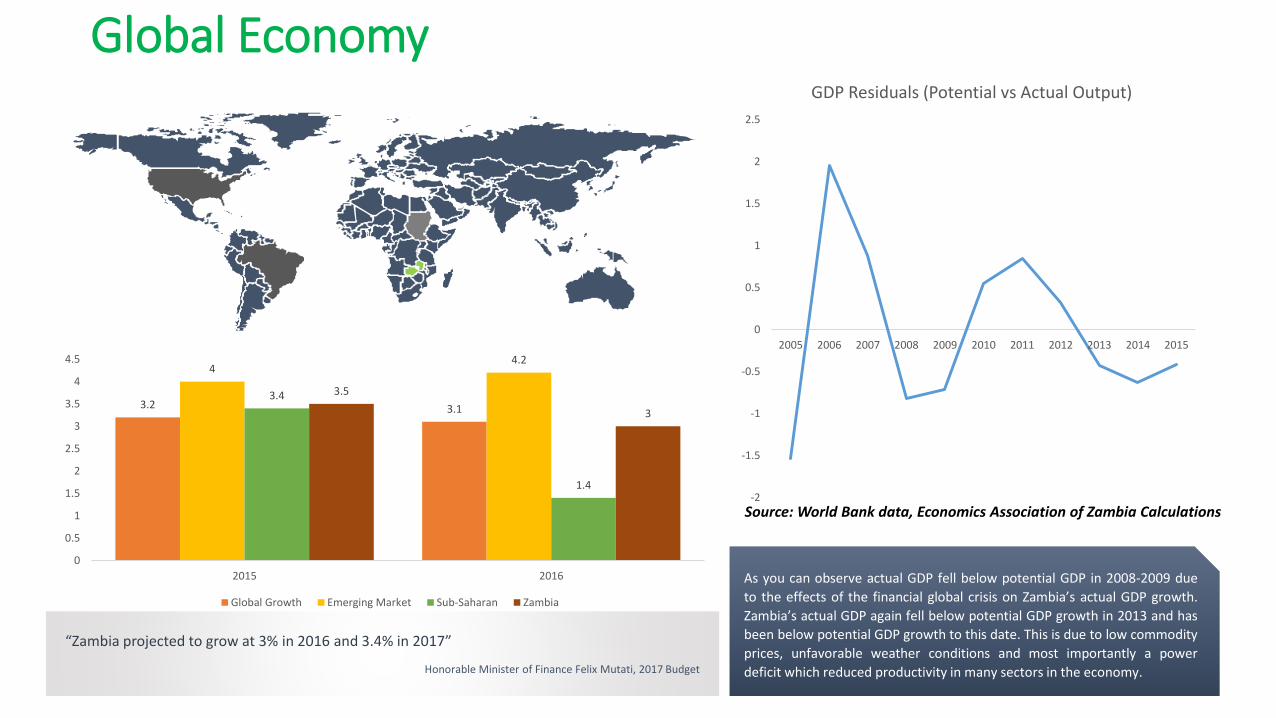

3.2 3.1

44.2

3.4

1.4

3.5

3

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2015 2016

Global Growth Emerging Market Sub-Saharan Zambia

“Zambia projected to grow at 3% in 2016 and 3.4% in 2017”

Honorable Minister of Finance Felix Mutati, 2017 Budget

As you can observe actual GDP fell below potential GDP in 2008-2009 due

to the effects of the financial global crisis on Zambia’s actual GDP growth.

Zambia’s actual GDP again fell below potential GDP growth in 2013 and has

been below potential GDP growth to this date. This is due to low commodity

prices, unfavorable weather conditions and most importantly a power

deficit which reduced productivity in many sectors in the economy.

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GDP Residuals (Potential vs Actual Output)

Global Economy

Source: World Bank data, Economics Association of Zambia Calculations

US Job Market

0

50

100

150

200

250

300

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16

Tho

usa

nd

sNon Farm Payrolls

Non Farm payrolls is a monthly report which measures the change in the number of

people employed, excluding the farming industry. Job creation is the best indicator of

the state of the US economy. It is a key variable used by the US federal Reserve in

determining whether or not to raise interest rates from their near zero zone since

2008.

0

50

100

150

200

250

300

May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16

Tho

usa

nd

s

Forecast Non Farm Payrolls

Non Farm payrolls are projected on a monthly basis using estimates from a survey of

Economists. The performance of the US economy is to a large extent measured by how

much actual Non Farm payrolls exceed or fall short of the analysts estimates.

Source: US Bureau of Labour Statistics Source: US Bureau of Labour Statistics

US Job Market

-2

-1

0

1

2

3

4

2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1 2016 Q2 2016 Q3

Manufacturing Sector Labour Prodcutivity

Manufacturing sector labor productivity increased 1.0 percent in the third quarter of 2016, as output and hours worked increased 1.1 percent and 0.1 percent, respectively. Over the

last four quarters, manufacturing sector productivity increased 0.2 percent, as output was unchanged and hours worked declined 0.1 percent.

However we must take into consideration the seasonality of manufacturing productivity which falls in the fourth quarter. The outlook for 2017 is positive given the influence of a

Trump Presidency in the first quarter of 2017.

Source: US Bureau of Labour Statistics

46

47

48

49

50

51

52

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16

Actual China PMI Projected China PMI

China Purchasing Managers Index (PMI)

The Chinese HSBC Manufacturing PMI is a composite indicator designed to provide an overall view of activity in the manufacturing sector and acts as an leading indicator for the whole

economy. When the PMI is below 50.0 this indicates that the manufacturing economy is declining and a value above 50.0 indicates an expansion of the manufacturing economy

The official manufacturing

Purchasing Managers' Index

(PMI), which measures

large state-owned

factories, came in at 51.2

for October, official data

showed.

Figures above the 50 level

suggests expansionary

activity while sub-50 levels

indicate contraction.

Source: Caixin PMI

China Purchasing Managers Index (PMI)

40%

53%

7%

Manufacturing Services Other

Manufacturing's contribution to overall growth has been slipping over the years as Beijing transitions its

economy from industry to consumption, accounting for around 40 percent of gross domestic product.

Services, on the other hand, now makes up more than half of the economy and the sector, which includes

real estate, restaurants, and e-commerce, has been on a steady upwards climb.

Economists say the pattern over the past few months suggested

sustained economic growth, but a growing dependence on

government spending and an overheated property market may pose

increased risks later this year with debt levels continuing to rise.

Source: World Bank

Global Commodity Trends

0

1000

2000

3000

4000

5000

6000

7000

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

Copper US$ per tonne

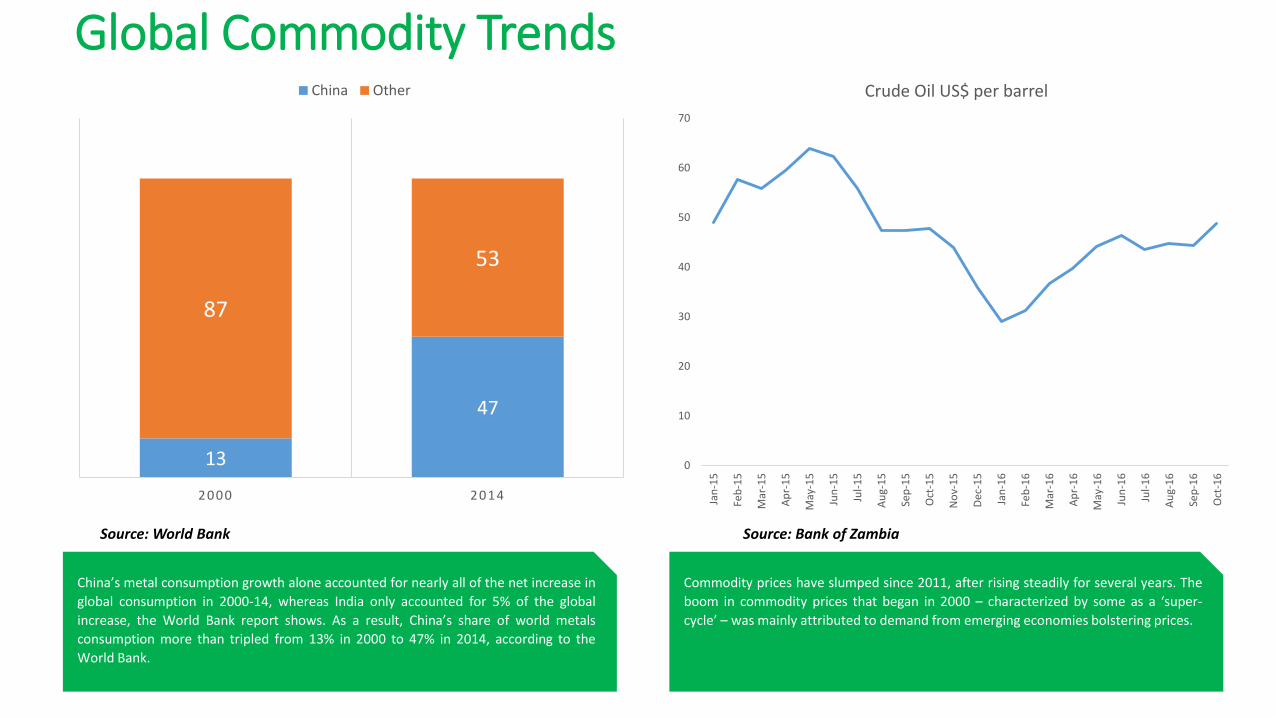

But perhaps the most important single factor affecting commodity prices right now is

China. For much of the last two decades, growth in demand from China sustained

commodity producers as a slew of infrastructure and manufacturing projects drove

demand. This trend began to weaken.

The downswing in commodity prices was sharp in 2015, particularly following the

financial volatility that started mid-August, after China’s shock devaluation of the

renminbi – with investors fretting about the country’s slowing economy.

China PMI (Year)

Source: Caixin PMI Source: Bank of Zambia

Global Commodity Trends

13

47

87

53

2000 2014

China Other

0

10

20

30

40

50

60

70

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

Crude Oil US$ per barrel

China’s metal consumption growth alone accounted for nearly all of the net increase in

global consumption in 2000-14, whereas India only accounted for 5% of the global

increase, the World Bank report shows. As a result, China’s share of world metals

consumption more than tripled from 13% in 2000 to 47% in 2014, according to the

World Bank.

Commodity prices have slumped since 2011, after rising steadily for several years. The

boom in commodity prices that began in 2000 – characterized by some as a ‘super-

cycle’ – was mainly attributed to demand from emerging economies bolstering prices.

Source: World Bank Source: Bank of Zambia

Global Commodity Trends

6.3

4.6

2011 2014

Commodity Exporting Country Growth

2.7

0.1

1.4

2.1

2013 2014

Brazil Mexico

IMF data shows real GDP growth in this group of countries decreased to 4.6% in 2014

from 6.3% in 2011, but the picture was mixed, as the commodity prices shifts have

created winners and losers in this volatile asset class.

Brazil, a commodity-exporting country, saw its GDP growth fall to 0.1% in 2014 from

2.7% in 2013. Meanwhile, Mexico, a manufacturing exporter boosted by low oil prices

saw its economic growth strengthen. Mexico’s real GDP rose to 2.1% in 2014 from

1.4% in 2013, and is projected to increase to 2.8% in 2016 from a projected 2.3% in

2015

Source: IMFSource: IMF

Most commodities are denominated in

dollars. But, the dollar's value has risen

over the past two years, making it

more expensive to sell and buy

commodities with respect to local

currencies. As a result, emerging

markets, which typically maintain

competitive exchange rates with

respect to the greenback, have been

hit by the dollar appreciation. The

result is a decline in overall commodity

sales.

The Dollar Effect

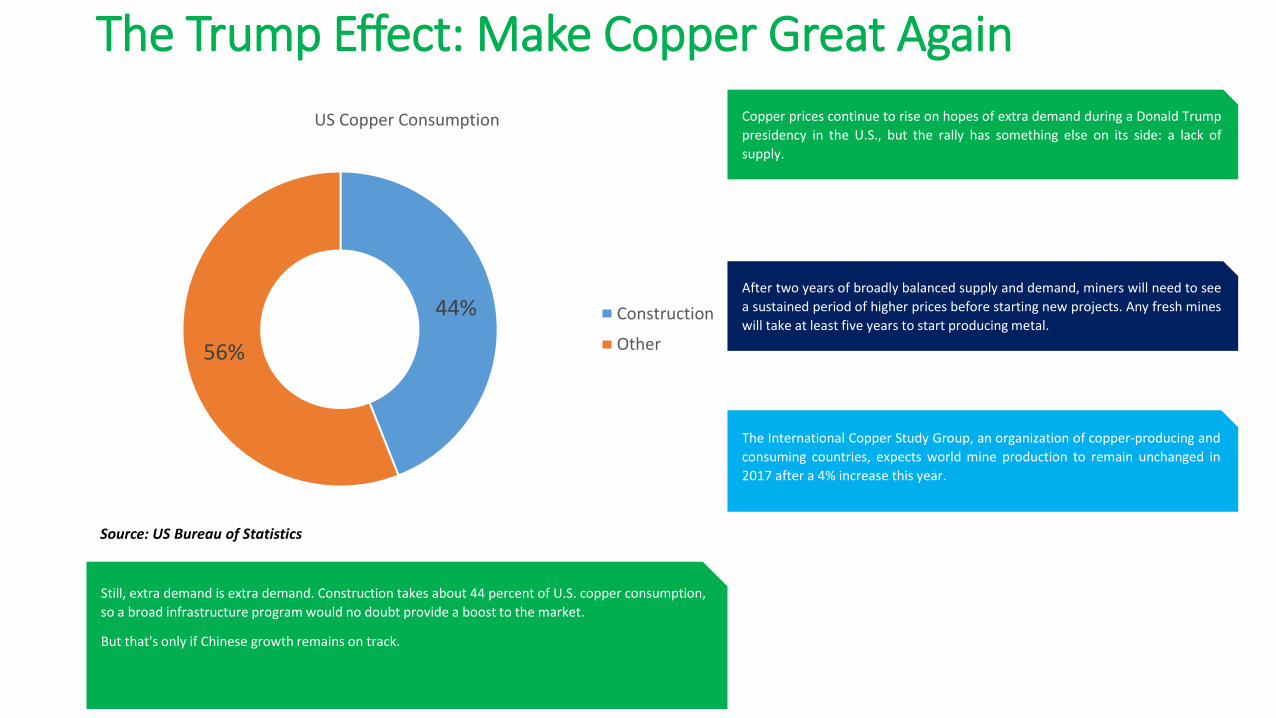

The Trump Effect: Make Copper Great Again

A big part of President-elect Donald Trump's appeal was his promise to restore, among other things, U.S. manufacturing and mining jobs that have disappeared over several decades. A big

infrastructure investment plan, however, does appear to be in the works, worth perhaps $1 trillion. Copper prices have surged on the back of it, up 13 percent since Tuesday and extending

a rally that began 3 weeks ago

The Trump Effect: Make Copper Great Again

China now accounts for more than half of global refined copper demand versus 7.5 percent for the U.S. That chart pretty much sums up the economic resentments that played some part in

Trump's victory. The salient point for copper investors, though, is that a 10 percent increase in U.S. copper demand is equivalent to less than a 1.5 percent increase in Chinese copper

consumption. And we haven't seen U.S. demand grow at anything close to that pace in almost 20 years.

Source: Wall Street Journal

The Trump Effect: Make Copper Great Again

Still, extra demand is extra demand. Construction takes about 44 percent of U.S. copper consumption,

so a broad infrastructure program would no doubt provide a boost to the market.

But that's only if Chinese growth remains on track.

44%

56%

US Copper Consumption

Construction

Other

Copper prices continue to rise on hopes of extra demand during a Donald Trump

presidency in the U.S., but the rally has something else on its side: a lack of

supply.

After two years of broadly balanced supply and demand, miners will need to see

a sustained period of higher prices before starting new projects. Any fresh mines

will take at least five years to start producing metal.

The International Copper Study Group, an organization of copper-producing and

consuming countries, expects world mine production to remain unchanged in

2017 after a 4% increase this year.

Source: US Bureau of Statistics

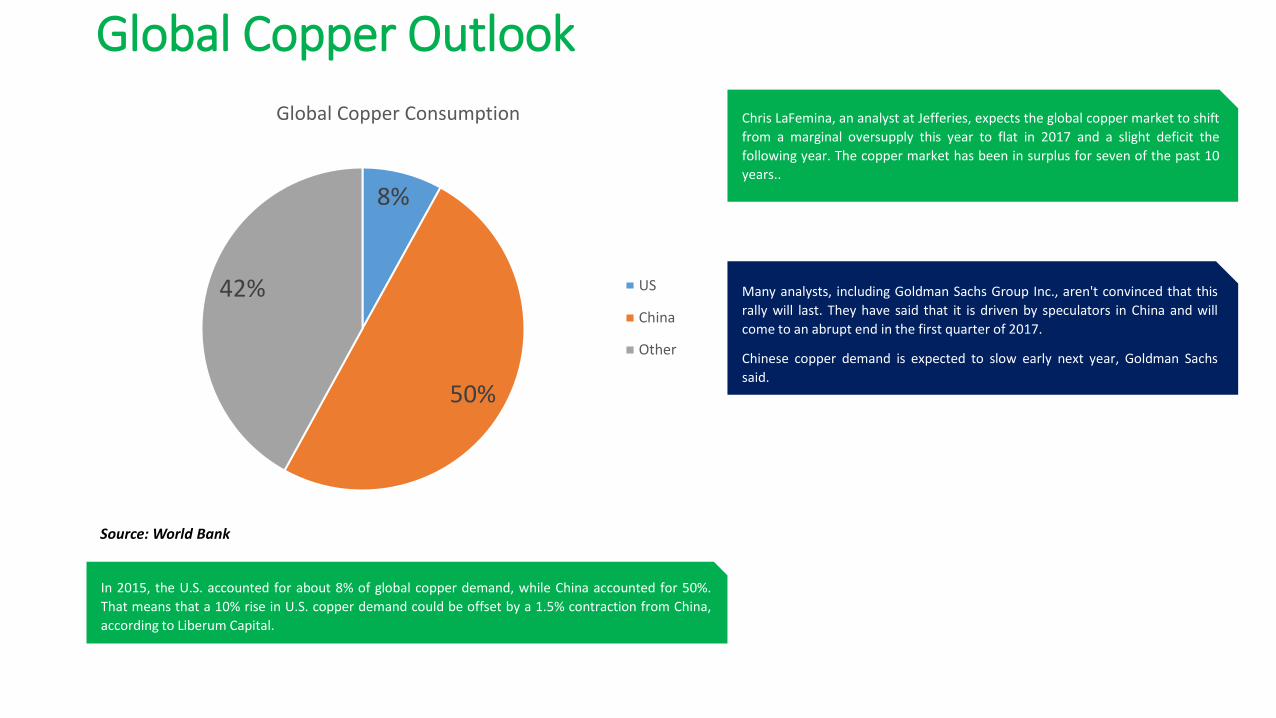

Global Copper Outlook

In 2015, the U.S. accounted for about 8% of global copper demand, while China accounted for 50%.

That means that a 10% rise in U.S. copper demand could be offset by a 1.5% contraction from China,

according to Liberum Capital.

Chris LaFemina, an analyst at Jefferies, expects the global copper market to shift

from a marginal oversupply this year to flat in 2017 and a slight deficit the

following year. The copper market has been in surplus for seven of the past 10

years..

Many analysts, including Goldman Sachs Group Inc., aren't convinced that this

rally will last. They have said that it is driven by speculators in China and will

come to an abrupt end in the first quarter of 2017.

Chinese copper demand is expected to slow early next year, Goldman Sachs

said.

8%

50%

42%

Global Copper Consumption

US

China

Other

Source: World Bank

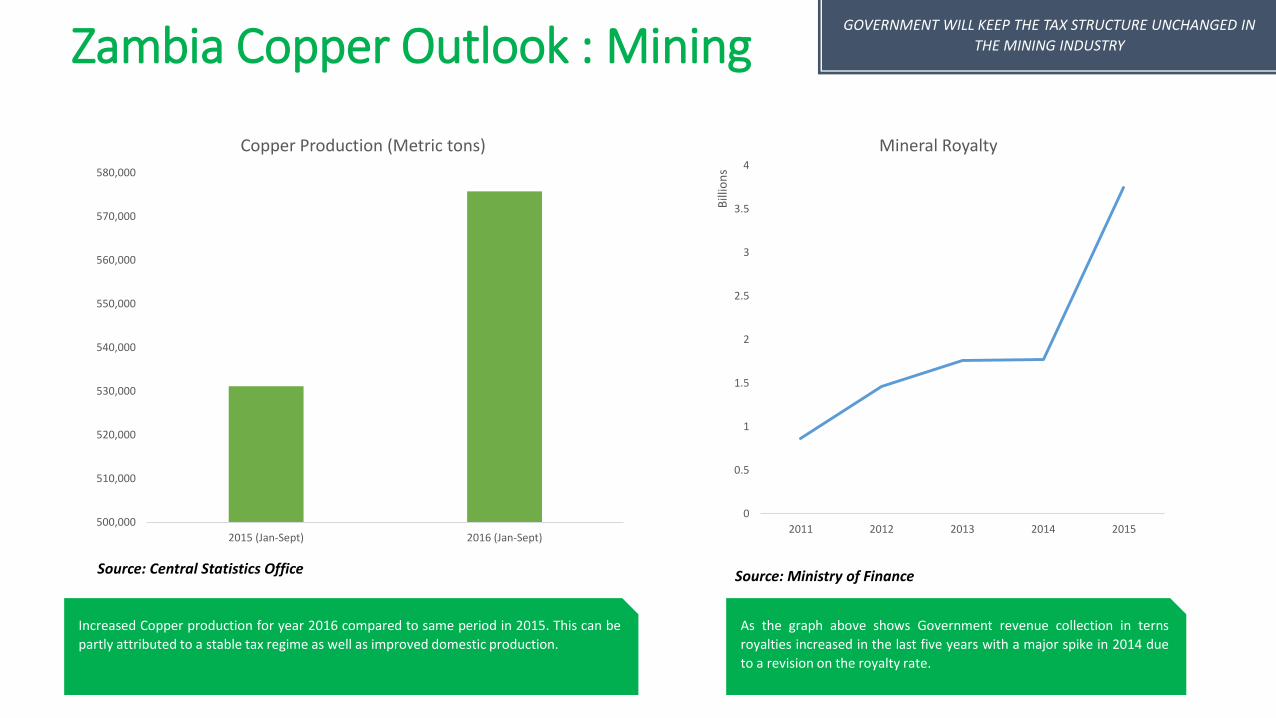

Zambia Copper Outlook : Mining

500,000

510,000

520,000

530,000

540,000

550,000

560,000

570,000

580,000

2015 (Jan-Sept) 2016 (Jan-Sept)

Copper Production (Metric tons)

0

0.5

1

1.5

2

2.5

3

3.5

4

2011 2012 2013 2014 2015

Bill

ion

s

Mineral Royalty

As the graph above shows Government revenue collection in terns

royalties increased in the last five years with a major spike in 2014 due

to a revision on the royalty rate.

Increased Copper production for year 2016 compared to same period in 2015. This can be

partly attributed to a stable tax regime as well as improved domestic production.

GOVERNMENT WILL KEEP THE TAX STRUCTURE UNCHANGED IN

THE MINING INDUSTRY

Source: Central Statistics Office Source: Ministry of Finance

Zambia Copper Outlook: Energy

65,881

183,659

48,020

375,549

71,454

5,526

77,925

23,052

395,944

2,729,904

4,414,352

OTHERS

AGRICULTURE

QUARRIES

MANUFACTURING

ENERGY AND WATER

CONSTUCTION

TRADE

TRANSPORT

FINANCE AND PROPERTY

SERVICES

MINING

- 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000 3,500,000 4,000,000 4,500,000 5,000,000

SECTOR CONSUMPTION (MWh), JAN-SPET 2016

SECTOR CONSUMPTION

The bulk of electricity consumption still goes to the Mining sector followed by services, Finances and property and then manufacturing. Government has indicated in the 2017 budget that

it will begin negotiations to have power purchase agreements with the mines moved to cost reflective tariffs.

GOVERNMENT WILL MOVE TO COST REFLECTIVE TARIFFS BY END OF 2017 TO

ATTRACT PRIVATE SECTOR INVESTMENT WHILE MAINTAINING THE LIFE LINE TARIFF

TO PROTECT POORER HOUSEHOLDS.

Source: Zesco

Zambia Copper Outlook: Trade Balance

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2015 (Jan-Sep) 2016 (Jan-Sep)

Export Earnings (US$ Billions)

Copper ExportEarnings

Non-TraditionalExport Earnings

-$2,000

-$1,500

-$1,000

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

Mill

ion

s

Trade balance

0

2

4

6

8

10

12

Bill

ion

s

Exports (US$) Imports (US$)

As the trade balance graph shows over the past 2 years Zambia has recorded trade deficits and more importantly Zambia’s gap between imports and exports began to narrow as far

back as 2011.This shows our terms of trade have deteriorated greatly owing to less copper exports. The outlook will remain bleak till sometime in 2018.

Source: Central Statistics Office Source: Central Statistics Office Source: Central Statistics Office

Zambia Copper Outlook: Exchange rate

Zambia’s exchange rate will also play a major part of the copper outlook in 2017 as Copper is priced in dollars. A stronger dollar relative to the Kwacha will dampen copper exports on the

international market.

0.0000

2.0000

4.0000

6.0000

8.0000

10.0000

12.0000

14.0000

16.0000

18.0000

20.0000

K/US$ K/Euro K/BPS K/ZAR

Source: Bank of Zambia

Contacts

For the Full Report on “The Global Economy-Effects on Commodity

Dependent Countries like Zambia” Contact:

Kampamba Shula – Programs Officer

26 Parairenyatwa Road,

Rhodes Park, Lusaka

Telephone: +260 211 842 088;

P.O. Box 38006

Twitter: @EAZambia

Facebook: Economics Association of Zambia