The Future of Wage and Hour under Trump - …. (Wage and Hour Division) Senior Policy Adviser: Keith...

24

The Future of Wage and Hour under Trump ABA Labor and Employment Law Conference November 11, 2017 Washington, D.C. Jeremy Glenn Cozen O’Connor Chicago, IL Hope Pordy Spivak Lipton LLP New York, NY M. Patricia Smith National Employment Law Project New York, NY

Transcript of The Future of Wage and Hour under Trump - …. (Wage and Hour Division) Senior Policy Adviser: Keith...

The Future of Wage and Hour under Trump

ABA Labor and Employment Law Conference

November 11, 2017

Washington, D.C.

Jeremy Glenn

Cozen O’Connor

Chicago, IL

Hope Pordy

Spivak Lipton LLP

New York, NY

M. Patricia Smith

National Employment

Law Project

New York, NY

i

TABLE OF CONTENTS1

Page

I. WHO’S WHO IN THE DEPARTMENT OF LABOR?......................................................1

A. Secretary of Labor: Alexander Acosta .....................................................................1

B. Deputy Secretary of Labor: Patrick Pizzella ............................................................1

C. Solicitor of Labor: Kate O’Scannlain ......................................................................1

D. Deputy Solicitor of Labor: Nicholas Geale .............................................................2

E. (Wage and Hour Division) Administrator: Cheryl Stanton .....................................2

F. (Wage and Hour Division) Deputy Administrator: Bryan Jarrett ............................3

G. (Wage and Hour Division) Senior Policy Adviser: Keith Sonderling .....................3

II. JOINT EMPLOYMENT ......................................................................................................3

A. What is Joint Employment? .....................................................................................3

B. 2015 & 2016 Administrator’s Interpretations Memos .............................................5

C. Department of Labor Abandons 2015 & 2016 Administrator’s Interpretations

Memos......................................................................................................................5

D. House of Representatives Introduce The “Save Local Business Act”

(H.R. 3441) ..............................................................................................................5

E. What Does This Mean For You? .............................................................................7

III. THE FAIR LABOR STANDARDS ACT WHITE COLLAR EXEMPTIONS:

WHERE ARE WE NOW? ...................................................................................................7

IV. THE TIP CREDIT UNDER THE FLSA ...........................................................................12

A. The Basics. .............................................................................................................12

B. Direct Cash Wage of $2.13 ....................................................................................13

C. Notice of Provisions of Section 203(m).................................................................14

D. Mandatory Tip Pooling ..........................................................................................15

E. “Voluntary” Tip Sharing ........................................................................................15

V. DOL REGULATIONS & GUIDANCE UNDER SCRUTINY DURING THE

TRUMP YEARS ................................................................................................................16

A. The Impact of Dual Jobs & Non-Tip Producing Duties on Employers’

Use of the Tip Credit..............................................................................................16

B. Who Owns The Tips When No Tip Credit Is Taken? ...........................................19

1 These materials have been prepared for continuing legal education purposes and do not constitute legal advice. They

should not be used in place of independent legal research.

1

I. WHO’S WHO IN THE DEPARTMENT OF LABOR?

A. Secretary of Labor: Alexander Acosta

Alexander Acosta, nominated by President Trump, was confirmed as the Secretary of

Labor on April 28, 2017. Acosta is a native of Miami, Florida. He earned his undergraduate and

law degrees from Harvard University. After law school, Acosta worked as a law clerk for Justice

Alito at the U.S. Court of Appeals for the Third Circuit. Acosta then worked at Kirkland & Ellis

before going on to teach at George Mason University’s School of law. Prior to his appointment as

Secretary of Labor, Acosta had served in three presidentially appointed, Senate-confirmed

positions: 2002, he was appointed as a member of the NLRB; 2003, he was appointed Assistant

Attorney General for the Civil Rights Division of the Department of Justice; 2005-2009 he served

as U.S. Attorney for the Sothern District of Florida.

B. Deputy Secretary of Labor: Patrick Pizzella

Patrick Pizzella has been nominated for Deputy Secretary of Labor. Pizzella had his

confirmation hearing in front of the HELP Committee on July 13, 2017. The Committee has not

voted on whether to advance Pizzella to the Senate floor yet. Pizzella, a New York native, currently

serves as the Acting Chairman of the Federal Labor Relations Authority. From 2001-2009, Pizzella

served as Assistant Secretary of Labor for Administration and Management in the Department of

Labor during the George W. Bush presidency. He received a B.S. in Business Administration from

the University of South Carolina.

C. Solicitor of Labor: Kate O’Scannlain

Kate O’Scannlain was nominated by President Trump to be the next Solicitor of Labor, on

September 28, 2017. O’Scannlain grew up in Portland, Oregon, and attended the University of

Notre Dame where she received her B.A. and J.D. O’Scannlain is currently a partner in the

2

Washington D.C. office of Kirkland & Ellis LLP. At Kirkland & Ellis, her practice primarily

focuses on labor and employment law, including commercial litigation, providing regulatory

advice, and counseling on mergers, acquisitions, restructuring, and private equity.

D. Deputy Solicitor of Labor: Nicholas Geale

Nicholas Geale is the Deputy Solicitor of Labor, and was confirmed February 17, 2017.

Prior to the recent nomination of O’Scannlain, Geale was serving as the Acting Solicitor of Labor.

Geale also serves as Chief of Staff for Secretary Acosta, as of August 20, 2017. Geale earned his

undergraduate degree at Claremont McKenna College, and earned his law degree from

Georgetown Law. From 2006-2009, he served at the U.S. Department of Labor as an attorney in

the Office of the Solicitor and as Counselor to the Deputy Secretary of Labor. Prior to his federal

service, Geale had six years of experience in labor and employment matters, general commercial

litigation, and alternative dispute resolution in private and public practice, including serving as

Assistant General Counsel for the Washington Metropolitan Area Transit Authority.

E. (Wage and Hour Division) Administrator: Cheryl Stanton

Cheryl Stanton was recently nominated to be the Administrator of the Department of

Labor’s Wage and Hour Division. Stanton currently serves as the Executive Director for the South

Carolina Department of Employment and Workforce, a position she has served since 2013. Prior

to that job, Stanton worked as a labor and employment attorney in both the public and private

sectors. In the public sector (2005-2008), she served as Associate White House Counsel for

President George W. Bush, and was the administrations liaison to the Department of Labor, the

EEOC, and the NLRB. In the private sector, she represented employers in wage-and-hour matters

at the firm Ogletree Deakins Nash Smoak & Stewart. Stanton received her undergraduate degree

from Williams College, and received her J.D. from the law school at the University of Chicago.

3

F. (Wage and Hour Division) Deputy Administrator: Bryan Jarrett

Bryan Jarrett has been installed as the acting administrator of the Wage and Hour Division

until Stanton is officially confirmed. After Stanton assumes control as Administrator, Jarrett will

remain in the Wage and Hour Division as the Deputy Administrator. Hiring Jarrett follows a

pattern of Trump administration appointees having a background representing employers in

workplace lawsuits. Jarrett most recently practiced labor and employment law at the firm Morgan

Lewis. He earned a law degree from Stanford University in 2011, and clerked on the U.S. Court

of Appeals for the Eighth Circuit.

G. (Wage and Hour Division) Senior Policy Adviser: Keith Sonderling

Keith Sonderling joined the Wage and Hour Division as a senior policy adviser. Sonderling

is the agency’s first political appointee. Prior to his appointment, Sonderling practiced law at the

Gunster Law Firm in Boca Raton, Florida. His practice focused on defending employers in labor

and employment cases. His work at Gunster includes cases in which he represented companies

accused of violating the FLSA, FMLA, and discrimination claims. In 2012, he was appointed by

Florida Gov. Rick Scott (R) to the state’s Fourth District Court of Appeals Judicial Nomination

Commission, and later became chair. Sonderling is also listed as a board member of the Greater

Boca Raton Chamber of Commerce.

II. JOINT EMPLOYMENT

A. What is Joint Employment?

Joint employment is the theory that separate entities have enough control over the same

employee(s) so that a court or administrative agency would find the employers jointly liable.2

2 See NLRB v. Browning-Ferris Indus. of Pa. Inc., 691 F.2d 1117 (3d Cir. 1982) (“A finding that companies are joint

employers assumes in the first instance that companies are what they appear to be—independent legal entities that

have merely historically chosen to handle jointly…important aspects of their employer-employee relationship.”).

4

Joint employers under the Fair Labor Standards Act (“FLSA”) can be held liable for wage-and-

hour violations, while joint employers under the National Labor Relations Act (“NLRA”) can

face unfair labor practice charges or be required to bargain with unions.

The determination of whether a joint employment relationship exists will vary by

jurisdiction, and will depend on which test is used. “There are three commonly used tests for

evaluating joint employment relationships: (1) the common law control test, (2) the economic

realities test, and (3) hybrid analyses that rely upon the two previous tests and may also include

additional factors.”3 For the common law control test, “the primary focus is usually on whether

the putative joint employer exerts sufficient control over the manner and means of the workers’

employment, considering such factors as: [a]authority to hire and fire employees, promulgate work

rules and assignments, and set conditions of employment…day-to-day supervision of

employees…and [c]ontrol of employee records, including payroll.”4 The economic realities test

considered an analysis of factors such as “[t]he permanency of the relationship; the degree of

control exercised by the alleged employer; the degree of skill and independent initiative required

in performing the job; the extent of the relative investments of the worker and the alleged

employer; and the degree to which the worker’s opportunity for profit and loss is determined by

the alleged employer.”5 As stated previously, the hybrid test involved an analysis of both the

control test and the economic realities test.6

3 Law360, Joint Employment Relationships: Best Practices And Risks,

https://www.law360.com/articles/906291/joint-employment-relationships-best-practices-and-risks (March 28,

2017). 4 Id. 5 Id. See Thibault v. Bellsouth Telecommunications Inc., 612 F.3d 843 (5th Cir. 2010). 6 See Butler v. Drive Auto. Indus. of Am. Inc., 793 F.3d 404 (4th Cir. 2015).

5

B. 2015 & 2016 Administrator’s Interpretations Memos

David Weil was appointed Administrator of the Wage and Hour Division of the

Department of Labor by President Obama in April of 2014, and served as such until January 2017.

In 2015 and 2016, the Department of Labor issued two memos (called “Administrator’s

Interpretations”) by David Weil’s Wage and Hour Division regarding joint employment. The first

memo dealt with the definition of employment under the FLSA, and clarified existing law

regarding the distinction between employees and independent contractors. The second memo

addressed how to determine joint employment relationships under the FLSA and the Migrant and

Seasonal Worker Protection Act. The Administrator’s Interpretations expanded instances of when

two companies are legally responsible for the same employee—something that was seen as a threat

to franchised brands and those employing contractors on a large scale. This was viewed as a

positive step for the labor side in joint employment issues. However, with the election of President

Trump—known for being pro-management—the Obama Administration’s guidance would

become short-lived.

C. Department of Labor Abandons 2015 & 2016 Administrator’s

Interpretations Memos

On June 7, 2017, the Department of Labor announced it was abandoning the 2015 and 2016

Obama Administration’s guidance. While abandoning the Administrator’s Interpretations does not

change the legal responsibilities of employers under the FLSA, it signaled to employers a shift in

enforcement priorities.

D. House of Representatives Introduce The “Save Local Business Act” (H.R.

3441)

On July 27, 2017, Republican lawmakers in the U.S. House of Representatives introduced

new legislation, the “Save Local Business Act,” to narrow the definition of joint employment under

the FLSA and the NLRA. The bill aims to amend the FLSA and the NLRA so that companies

6

would qualify as joint employers of workers hired by another business only if they directly and

immediately exercise significant control over essential working conditions of particular workers.

Those essential terms include hiring or firing decisions, determination of individuals’ pay rates

and benefits, worker discipline, day-to-day supervision of employees, and assignment of positions,

tasks, and individual work schedules. The bill would give businesses more clarity for structuring

deals with contractors, while employee advocates fear that the bill could shield companies that

outsource labor from facing liability for workplace violations.

Lawmakers primarily framed the bill as a response to the NLRB’s 2015 ruling in

Browning-Ferris Industries, which expanded the test for joint employment under the NLRA

beyond direct and immediate control to consider indirect or unexercised control.7 The NLRB ruled

that organizations with indirect control over contractors, franchisees, or staffing agency workers

can be considered their joint employer.8 Prior to this decision, direct and immediate control was

the required standard for joint employment. On August 4, 2017, the D.C. Circuit overruled the

NLRB’s decision on appeal, and remanded the case to be re-evaluated. If the bill passes, it will

restore the joint employment test to what it had been prior to the 2015 NLRB decision—a

requirement of direct and immediate control, instead of the much broader standard supported by

the NLRB’s decision.

On October 4, 2017, the House Education and the Workforce Committee approved the

Save Local Business Act (H.R. 3441) in a 23-17 party-line vote. The committee’s approval

prepares the bill for potential consideration by the full House of Representatives. The bill has 95

co-sponsors, including three moderate Democrats. The legislator who introduced the bill, Rep.

Bradley Byrne (R-Ala.) stated in public remarks that, “H.R. 3441 … clarifies that two or more

7 Browning-Ferris Indus. of Cal. Inc., 362 N.L.R.B. No. 186 (Aug. 27, 2015). 8 Id.

7

employers must have ‘actual, direct, and immediate’ control over essential terms and conditions

of employment to be considered joint employers.” A companion bill has yet to be introduced in

the Senate.

E. What Does This Mean For You?

Joint employment continues to present employers across the country with a unique and

difficult challenge. While the proposal of the “Save Local Business Act” would provide clarity,

the current state of the joint employment relationship remains in flux. Between the NLRB’s

Browning-Ferris decision, the D.C. Circuit remanding the case, and the stark contrast between the

Obama Administration’s interpretations of joint employment compared with the Trump

Administration’s stance on the issue, employers are still left with uncertainty.

With that being said, there are important considerations for employers to make to help

ensure compliance with the FLSA and NLRA. Employers should review all contracts with staffing

agencies and other contractors to ensure that they do not wave a joint employment red flag. The

main consideration being that employers should ensure (as best as possible) that control over the

employee(s) rests with the contractors. Employers need to analyze the factual realities of the

employment relationship such as the length of the job commitment, the extent of the putative

employer’s control and supervision over the putative employee, and whether the putative employee

was assigned solely to the putative employer. Finally, employers should be sure to analyze the

economic realities of the employment relationship such as the method and form of payment and

benefits, who furnishes the work space and equipment, and who sets work hours.

III. THE FAIR LABOR STANDARDS ACT WHITE COLLAR EXEMPTIONS:

WHERE ARE WE NOW?

The Fair Labor Standards Act (the “FLSA” or the “Act”) guarantees a minimum wage for

all hours worked and limits to 40 hours per week the number of hours an employee can work

8

without additional compensation. Section 13(a)(1) of the FLSA, which was included in the original

Act in 1938, exempts from these minimum wage and overtime pay protections ‘‘any employee

employed in a bona fide executive, administrative, or professional capacity’’ (the “White Collar”

or “EAP Exemption”).9 The statute delegates to the Secretary of Labor the authority to define and

delimit the terms of the EAP exemption.10

Since 1940, the regulations implementing the EAP exemption have generally required each

of three tests to be met for the exemption to apply: (1) The employee must be paid a predetermined

and fixed salary that is not subject to reduction because of variations in the quality or quantity of

work performed (the ‘‘Salary-Basis Test’’); (2) the amount of salary paid must meet a minimum

specified amount (the ‘‘Salary-Level Test’’); and (3) the employee’s job duties must primarily

involve executive, administrative, or professional duties as defined by the regulations (the ‘‘Duties

Test’’).11

Prior to the 2016 rule, the Department of Labor (the “Department”) had updated the salary

level requirements seven times since 1938, most recently in 2004 when the salary test for EAP

Exemption was set at $455 per week.12

The Department also modified the duties tests in 2004, eliminating the ‘‘long’’ and

‘‘short’’ tests that had been part of the regulations since 1949 and replacing them with the

‘‘standard’’ test. The long test had paired a lower salary requirement with a stringent duties test

(including a 20 percent cap on the amount of time most exempt employees could spend on

9 29 U.S.C. § 213(a)(1).

10 Id.

11 See 29 C.F.R. part 541.

12 See 2004 Overtime Rule, 69 Fed. Reg. 22122 (Apr. 23, 2004).

9

nonexempt duties), while the short test paired a higher salary requirement with a less stringent

duties test.13

On March 13, 2014, President Obama signed a Presidential Memorandum directing the

Department to update the EAP regulations.14 The memorandum instructed the Department to look

for ways to modernize and simplify the regulations while ensuring that the FLSA’s intended

overtime protections are fully implemented.15

Following issuance of that Memorandum, the Department conducted an extensive outreach

program, ultimately meeting with over two hundred organizations and stakeholders to identify

concerns with the current regulations and suggestions for changes. That input informed the

Department’s notice of proposed rulemaking (the “NPRM”), published on July 6, 2015, to revise

the existing regulations for the EAP Exemption.16

In the NPRM, the Department proposed setting the standard salary level at the 40th

percentile of weekly earnings of full-time salaried workers nationally. The Department further

proposed to automatically update these levels annually to ensure that they would continue to

provide an effective test for exemption. In the NPRM, the Department also asked for the public’s

comments on whether nondiscretionary bonuses or incentive payments should count toward some

portion of the required salary level. Finally, the Department also discussed concerns with the

standard duties tests and sought comments on a series of questions regarding possible changes to

the tests.17

13 See id.

14 79 Fed. Reg. 18737 (Apr. 3, 2014). 15 See id.

16 NPRM for 2016 Overtime Rule, 80 Fed. Reg. 38516 (July 6, 2015).

17 See generally id.

10

The Department promulgated a final rule on May 23, 2016.18 In the final rule, the

Department set the standard salary level equal to the 40th percentile of earnings of full-time

salaried workers in the lowest-wage Census Region (currently the South). This resulted in a salary

level of $913 per week, or $47,476 annually, for a full-year worker. The Department included in

the regulations a mechanism to automatically update the salary and compensation thresholds every

three years by maintaining the fixed percentiles of weekly earnings set in this Final Rule.19

The Department also revised the regulations to permit employers for the first time to count

nondiscretionary bonuses, incentives, and commissions toward up to 10 percent of the required

salary level for the standard exemption, so long as employers pay those amounts on a quarterly or

more frequent basis. Finally, the Department did not make any changes to the duties tests. The

Rule was to become effective December 1, 2016.20

The State of Nevada and twenty other states filed suit against the Department challenging

the final rule in Nevada v. United States Department of Labor.21 The same day, business plaintiffs

filed a similar action challenging the final rule in Plano Chamber of Commerce v. Perez,22 which

was assigned to the same judge. On November 22, 2016, United States District Court Judge, Amos

Mazzant, granted an emergency motion for preliminary injunction and enjoined the Department

from implementing and enforcing the final rule.23

18 2016 Overtime Rule, 81 Fed. Reg. 32391 (May 23, 2016).

19 See id.

20 See id.

21 No. 16-CV-731(E.D. Tex. Sept. 20, 2016).

22 No. 16-CV-732 (E.D. Tex. Sept. 20, 2016).

23 Nevada v. U.S. Dep’t of Labor, 218 F.Supp.3d 520 (E.D. Tex. 2016).

11

On December 1, 2016, the Department of Justice on behalf of the Department filed a notice

to appeal the preliminary injunction to the United States Court of Appeals for the Fifth Circuit.24

On June 30, 2017, the Department of Justice filed its reply brief with that court.25

On July 26, 2017, the Department published a Request for Information (the “RFI”) about

the 2016 final rule.26 The Department sometimes uses RFIs when it wants public input on whether

a new rule or changes to an existing rule are needed. This RFI solicited feedback on questions

related to the salary level test, the duties test, the inclusion of non-discretionary bonuses and

incentive payments to satisfy a portion of the salary level, the salary test for highly compensated

employees, and automatic updating of the salary level tests. The 60-day comment period for all

issues raised in the RFI ended on September 25, 2017.27

On August 31, 2017, Judge Mazzant granted summary judgment against the Department

in the two cases, which he had consolidated. The Court held that the final rule’s salary level

exceeded the Department’s authority to define the Exemption, and concluded that the final rule is

invalid. The Court did not vacate the rule, despite a request for that relief, nor did the Court enjoin

the Department. After the decision, the Department stated that it was still accepting comments on

its RFI.28 The department received 165,000 comments in response to the RFI.29

24 Notice of Appeal, Nevada v. U.S. Dep’t of Labor, No. 16-CV-732 (E.D. Tex. Dec. 1, 2016).

25 Reply Br. for Appellants, Nevada v. U.S. Dep’t of Labor, No. 16-41606 (5th Cir. June 30, 2017).

26 RFI, 82 Fed. Reg. 34616 (July 26, 2017).

27 Id.

28 https://www.dol.gov/whd/overtime/final2016/litigation.htm

29 Vin Gurrieri, OT Rule Comments Show Sharp Divide On Salary Threshold, Law360.com, Sept. 27, 2017,

https://www.law360.com/employment/articles/967879/ot-rule-comments-show-sharp-divide-on-salary-

threshold?nl_pk=f804f568-2788-442c-90af-

fbb2f20fd702&utm_source=newsletter&utm_medium=email&utm_campaign=employment.

12

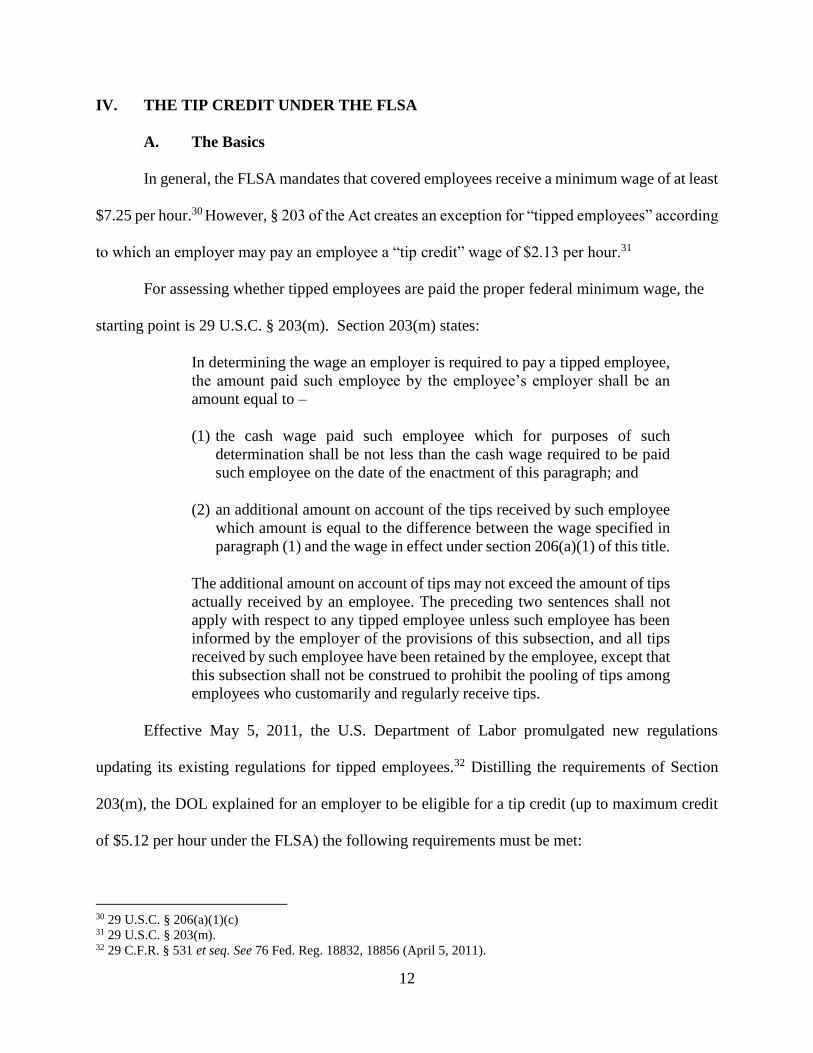

IV. THE TIP CREDIT UNDER THE FLSA

A. The Basics

In general, the FLSA mandates that covered employees receive a minimum wage of at least

$7.25 per hour.30 However, § 203 of the Act creates an exception for “tipped employees” according

to which an employer may pay an employee a “tip credit” wage of $2.13 per hour.31

For assessing whether tipped employees are paid the proper federal minimum wage, the

starting point is 29 U.S.C. § 203(m). Section 203(m) states:

In determining the wage an employer is required to pay a tipped employee,

the amount paid such employee by the employee’s employer shall be an

amount equal to –

(1) the cash wage paid such employee which for purposes of such

determination shall be not less than the cash wage required to be paid

such employee on the date of the enactment of this paragraph; and

(2) an additional amount on account of the tips received by such employee

which amount is equal to the difference between the wage specified in

paragraph (1) and the wage in effect under section 206(a)(1) of this title.

The additional amount on account of tips may not exceed the amount of tips

actually received by an employee. The preceding two sentences shall not

apply with respect to any tipped employee unless such employee has been

informed by the employer of the provisions of this subsection, and all tips

received by such employee have been retained by the employee, except that

this subsection shall not be construed to prohibit the pooling of tips among

employees who customarily and regularly receive tips.

Effective May 5, 2011, the U.S. Department of Labor promulgated new regulations

updating its existing regulations for tipped employees.32 Distilling the requirements of Section

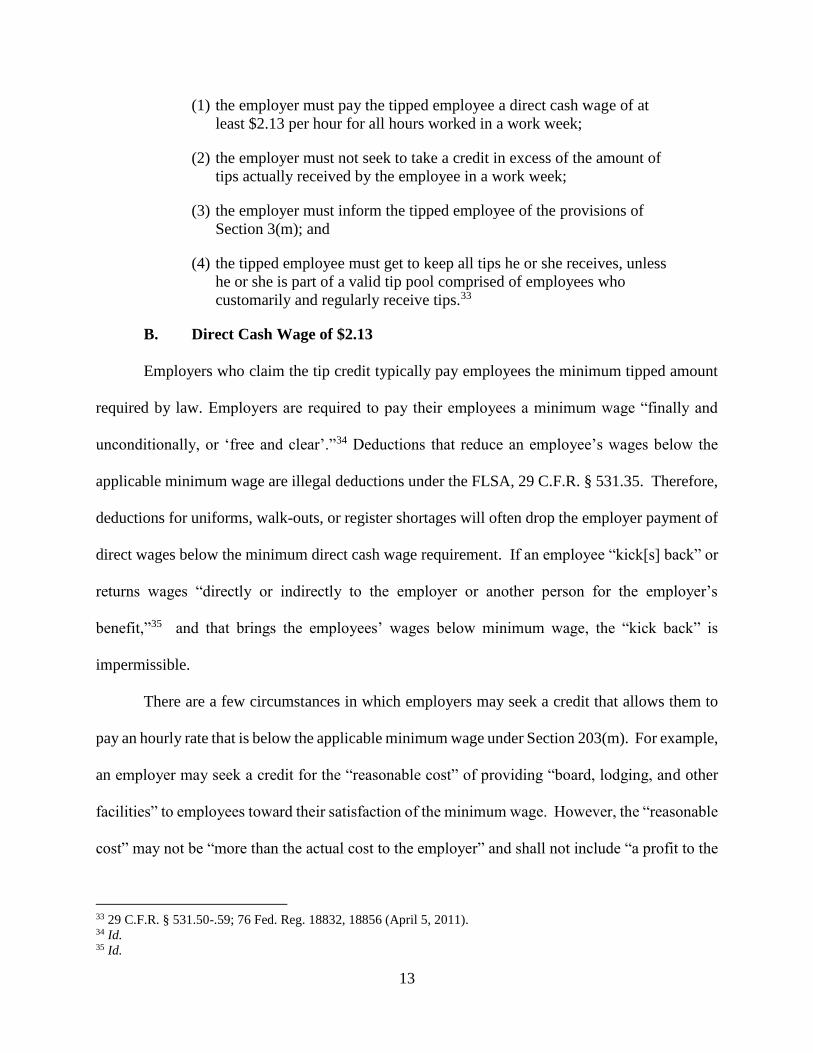

203(m), the DOL explained for an employer to be eligible for a tip credit (up to maximum credit

of $5.12 per hour under the FLSA) the following requirements must be met:

30 29 U.S.C. § 206(a)(1)(c) 31 29 U.S.C. § 203(m). 32 29 C.F.R. § 531 et seq. See 76 Fed. Reg. 18832, 18856 (April 5, 2011).

13

(1) the employer must pay the tipped employee a direct cash wage of at

least $2.13 per hour for all hours worked in a work week;

(2) the employer must not seek to take a credit in excess of the amount of

tips actually received by the employee in a work week;

(3) the employer must inform the tipped employee of the provisions of

Section 3(m); and

(4) the tipped employee must get to keep all tips he or she receives, unless

he or she is part of a valid tip pool comprised of employees who

customarily and regularly receive tips.33

B. Direct Cash Wage of $2.13

Employers who claim the tip credit typically pay employees the minimum tipped amount

required by law. Employers are required to pay their employees a minimum wage “finally and

unconditionally, or ‘free and clear’.”34 Deductions that reduce an employee’s wages below the

applicable minimum wage are illegal deductions under the FLSA, 29 C.F.R. § 531.35. Therefore,

deductions for uniforms, walk-outs, or register shortages will often drop the employer payment of

direct wages below the minimum direct cash wage requirement. If an employee “kick[s] back” or

returns wages “directly or indirectly to the employer or another person for the employer’s

benefit,”35 and that brings the employees’ wages below minimum wage, the “kick back” is

impermissible.

There are a few circumstances in which employers may seek a credit that allows them to

pay an hourly rate that is below the applicable minimum wage under Section 203(m). For example,

an employer may seek a credit for the “reasonable cost” of providing “board, lodging, and other

facilities” to employees toward their satisfaction of the minimum wage. However, the “reasonable

cost” may not be “more than the actual cost to the employer” and shall not include “a profit to the

33 29 C.F.R. § 531.50-.59; 76 Fed. Reg. 18832, 18856 (April 5, 2011). 34 Id. 35 Id.

14

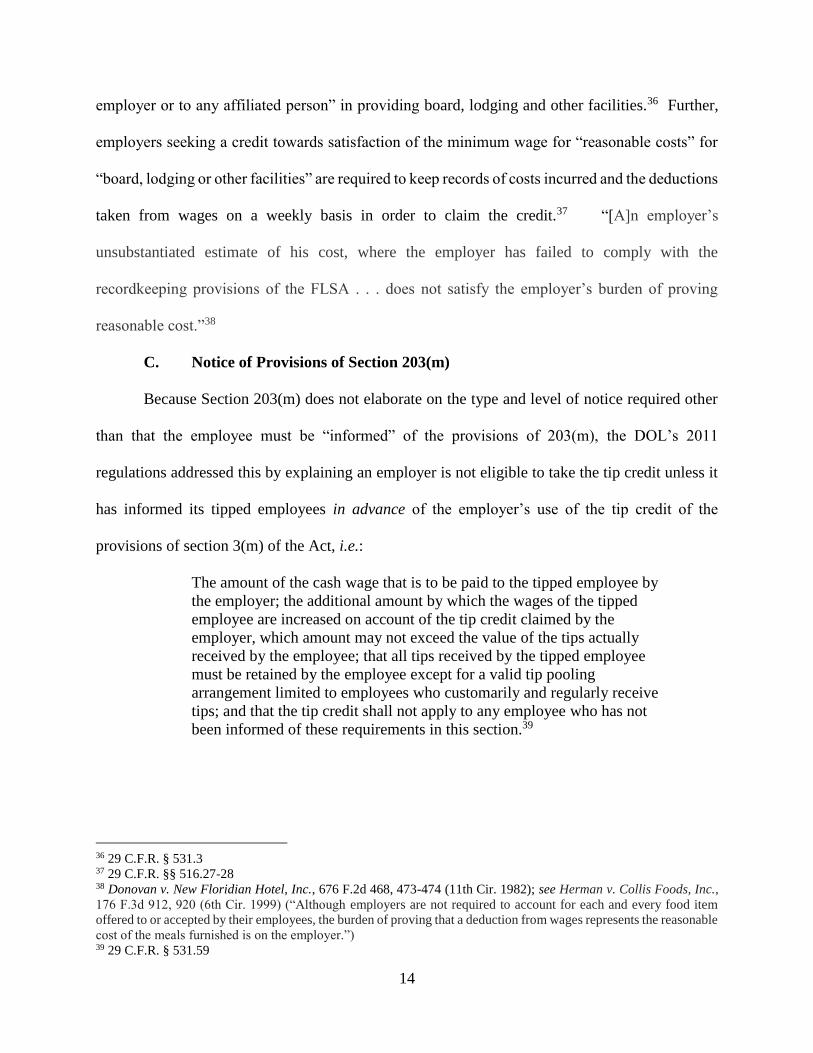

employer or to any affiliated person” in providing board, lodging and other facilities.36 Further,

employers seeking a credit towards satisfaction of the minimum wage for “reasonable costs” for

“board, lodging or other facilities” are required to keep records of costs incurred and the deductions

taken from wages on a weekly basis in order to claim the credit.37 “[A]n employer’s

unsubstantiated estimate of his cost, where the employer has failed to comply with the

recordkeeping provisions of the FLSA . . . does not satisfy the employer’s burden of proving

reasonable cost.”38

C. Notice of Provisions of Section 203(m)

Because Section 203(m) does not elaborate on the type and level of notice required other

than that the employee must be “informed” of the provisions of 203(m), the DOL’s 2011

regulations addressed this by explaining an employer is not eligible to take the tip credit unless it

has informed its tipped employees in advance of the employer’s use of the tip credit of the

provisions of section 3(m) of the Act, i.e.:

The amount of the cash wage that is to be paid to the tipped employee by

the employer; the additional amount by which the wages of the tipped

employee are increased on account of the tip credit claimed by the

employer, which amount may not exceed the value of the tips actually

received by the employee; that all tips received by the tipped employee

must be retained by the employee except for a valid tip pooling

arrangement limited to employees who customarily and regularly receive

tips; and that the tip credit shall not apply to any employee who has not

been informed of these requirements in this section.39

36 29 C.F.R. § 531.3 37 29 C.F.R. §§ 516.27-28 38 Donovan v. New Floridian Hotel, Inc., 676 F.2d 468, 473-474 (11th Cir. 1982); see Herman v. Collis Foods, Inc.,

176 F.3d 912, 920 (6th Cir. 1999) (“Although employers are not required to account for each and every food item

offered to or accepted by their employees, the burden of proving that a deduction from wages represents the reasonable

cost of the meals furnished is on the employer.”) 39 29 C.F.R. § 531.59

15

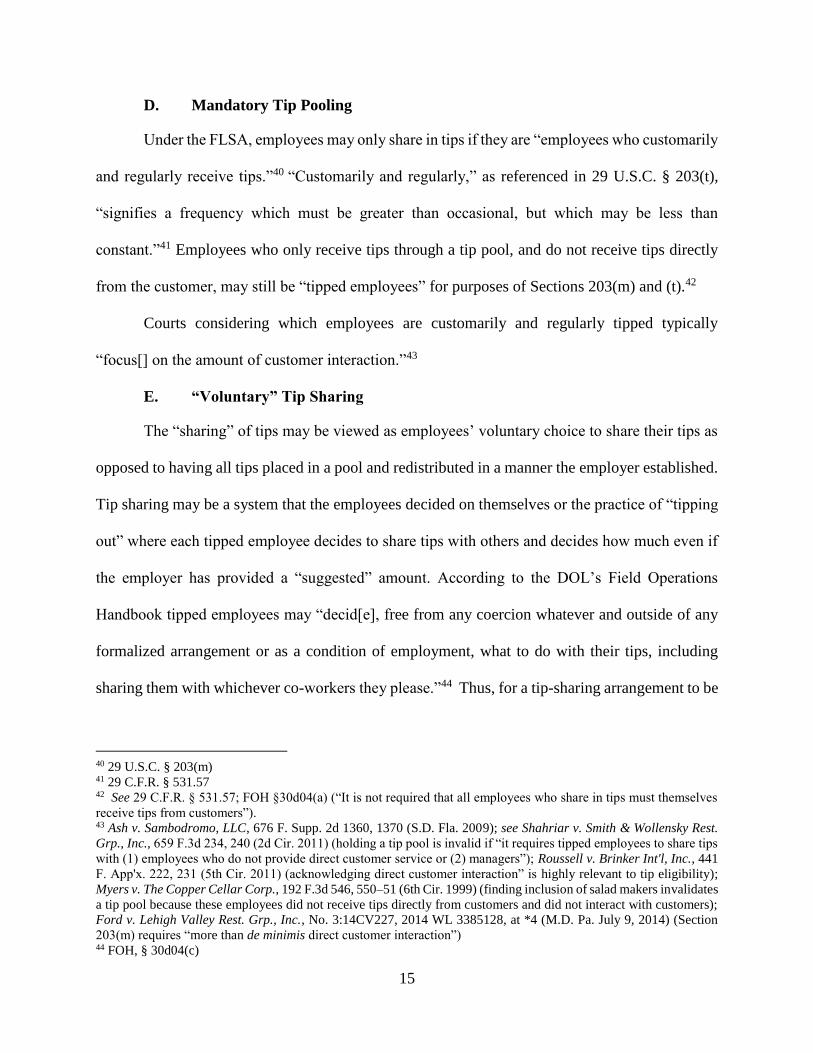

D. Mandatory Tip Pooling

Under the FLSA, employees may only share in tips if they are “employees who customarily

and regularly receive tips.”40 “Customarily and regularly,” as referenced in 29 U.S.C. § 203(t),

“signifies a frequency which must be greater than occasional, but which may be less than

constant.”41 Employees who only receive tips through a tip pool, and do not receive tips directly

from the customer, may still be “tipped employees” for purposes of Sections 203(m) and (t).42

Courts considering which employees are customarily and regularly tipped typically

“focus[] on the amount of customer interaction.”43

E. “Voluntary” Tip Sharing

The “sharing” of tips may be viewed as employees’ voluntary choice to share their tips as

opposed to having all tips placed in a pool and redistributed in a manner the employer established.

Tip sharing may be a system that the employees decided on themselves or the practice of “tipping

out” where each tipped employee decides to share tips with others and decides how much even if

the employer has provided a “suggested” amount. According to the DOL’s Field Operations

Handbook tipped employees may “decid[e], free from any coercion whatever and outside of any

formalized arrangement or as a condition of employment, what to do with their tips, including

sharing them with whichever co-workers they please.”44 Thus, for a tip-sharing arrangement to be

40 29 U.S.C. § 203(m) 41 29 C.F.R. § 531.57 42 See 29 C.F.R. § 531.57; FOH §30d04(a) (“It is not required that all employees who share in tips must themselves

receive tips from customers”). 43 Ash v. Sambodromo, LLC, 676 F. Supp. 2d 1360, 1370 (S.D. Fla. 2009); see Shahriar v. Smith & Wollensky Rest.

Grp., Inc., 659 F.3d 234, 240 (2d Cir. 2011) (holding a tip pool is invalid if “it requires tipped employees to share tips

with (1) employees who do not provide direct customer service or (2) managers”); Roussell v. Brinker Int'l, Inc., 441

F. App'x. 222, 231 (5th Cir. 2011) (acknowledging direct customer interaction” is highly relevant to tip eligibility);

Myers v. The Copper Cellar Corp., 192 F.3d 546, 550–51 (6th Cir. 1999) (finding inclusion of salad makers invalidates

a tip pool because these employees did not receive tips directly from customers and did not interact with customers);

Ford v. Lehigh Valley Rest. Grp., Inc., No. 3:14CV227, 2014 WL 3385128, at *4 (M.D. Pa. July 9, 2014) (Section

203(m) requires “more than de minimis direct customer interaction”) 44 FOH, § 30d04(c)

16

lawful under the FLSA four requirements must be met: (1) the tipped employees themselves must

“decid[e]” to share the tips; (2) that decision must be “free from any coercion whatever”; (3) the

tip-sharing must be “outside of any formalized arrangement”; and (4) the tip-sharing must not be

“as a condition of employment.”

V. DOL REGULATIONS & GUIDANCE UNDER SCRUTINY DURING THE

TRUMP YEARS

A. The Impact of Dual Jobs & Non-Tip Producing Duties on Employers’ Use of

the Tip Credit

The issue as to whether the tip credit may be applied to hours employees work performing

non-tip producing duties seemed to be settled by the Eighth’s Circuit decision in Fast v. Applebee's

Int'l, Inc.,45 until a recent decision issued on September 6, 2017, by the Ninth Circuit in Marsh v.

J. Alexander’s LLC, 869 F.3d 1108 (9th Cir. 2017) (consolidating nine cases).46 In Fast, the

plaintiffs were servers and bartenders. In Marsh, the plaintiffs, also servers and bartenders,

similarly claimed they spent more than 20% of their time on duties related to their tipped

occupation and therefore, the restaurant improperly took a tip credit for time spent on these “related

duties.”

Both cases examined the “dual jobs” regulation promulgated by the DOL, 29 C.F.R. §

531.56(e), interpreting §§ 203(m) and 203(t) of the FLSA, and particularly, the temporal nature of

certain duties performed in conjunction with, or apart, from an occupation in which an employee

“customarily and regularly receives more than $30 a month in tips,” Id. § 230(t):

(e) Dual jobs. In some situations an employee is employed in a dual job,

as for example, where a maintenance man in a hotel also serves as a

waiter. In such a situation the employee, if he customarily and regularly

45 No. 06-4146-CV-C-NKL, 2010 WL 816639, at *2 (W.D. Mo. Mar. 4, 2010), aff'd by 638 F.3d 872 (8th Cir. 2011) 46 Plaintiffs appealed the district court order granting defendant’s motion to dismiss and denying as futile plaintiffs’

motion for leave to amend the complaint. Plaintiffs’ proposed amended complaint, inter alia, sought to add a

separate count alleging that non-tipped duties performed by plaintiffs were “unrelated” to the tipped occupation.

17

receives at least $30 a month in tips for his work as a waiter, is a tipped

employee only with respect to his employment as a waiter. He is

employed in two occupations, and no tip credit can be taken for his hours

of employment in his occupation of maintenance man. Such a situation is

distinguishable from that of a waitress who spends part of her time

cleaning and setting tables, toasting bread, making coffee and

occasionally washing dishes or glasses. It is likewise distinguishable from

the counterman who also prepares his own short orders or who, as part of

a group of countermen, takes a turn as a short order cook for the group.

Such related duties in an occupation that is a tipped occupation need not

by themselves be directed toward producing tips.47 (emphasis added)

The DOL, however, has also developed guidelines for determining how much non-tipped

work can be assigned to the employee before the employee effectively has moved into a non-

tipped occupation and becomes a dual employee. Section 30d00(f) of the DOL's Wage and Hour

Division Field Operations Handbook (“FOH”) (December 15, 2016) states:48

(f) Dual jobs

(1) When an individual is employed in a tipped occupation and a non-

tipped occupation, for example, as a server and janitor (dual jobs), the

tip credit is available only for the hours spent in the tipped occupation,

provided such employee customarily and regularly receives more than

$30.00 a month in tips.49

(2) 29 CFR 531.56(e) permits the employer to take a tip credit for time

spent in duties related to the tipped occupation of an employee, even

though such duties are not by themselves directed toward producing

tips, provided such related duties are incidental to the regular duties of

the tipped employees and are generally assigned to the tipped

employee. For example, duties related to the tipped occupation may

include a server who does preparatory or closing activities, rolls

silverware and fills salt and pepper shakers while the restaurant is

open, cleans and sets tables, makes coffee, and occasionally washes

dishes or glasses.

(3) However, where the facts indicate that tipped employees spend a

substantial amount of time (i.e., in excess of 20 percent of the hours

worked in the tipped occupation in the workweek) performing such

47 32 FR 13575, Sept. 28, 1967, as amended at 76 FR 18855, Apr. 5, 2011 48 The most recent guidance was issued in 2016 and is currently available in Chapter 30 of the FOH posted on the

DOL’s website: www.dol.gov/whd/foh/foh_ch30.pdf 49 See 29 CFR 531.56(e)

18

related duties, no tip credit may be taken for the time spent in those

duties. All related duties count toward the 20 percent tolerance.

(4) Likewise, an employer may not take a tip credit for the time that a

tipped employee spends on work that is not related to the tipped

occupation. For example, maintenance work (e.g., cleaning bathrooms

and washing windows) are not related to the tipped occupation of a

server; such jobs are non-tipped occupations. In this case, the

employee is effectively employed in dual jobs.

Where the cases differed was the amount of deference, if any, should be afforded the

DOL’s guidance set forth in the FOH. Whereas the Eighth Circuit deferred to the DOL under the

Auer doctrine, the Ninth Circuit found that no such deference was warranted.50 “While we

generally defer to an agency’s interpretations of its own ambiguous regulations, we do not do so

when the interpretation is ‘plainly erroneous or inconsistent with the regulation,’51 or when such

deference would impermissibly ‘permit the agency, under the guise of interpreting a regulation, to

create de facto a new regulation,’ Christensen v. Harris County, 529 U.S. 576, 588 (2000).”52 The

Marsh Court found the latter to be true with respect to FOH Section 30d00(f).

In Marsh, the Court found that the “[p]erformance of dispersed, related and generally

assigned duties is consistent with the waitress and counterman examples in the dual jobs

regulation, which are examples of a tipped occupation.”53 The Court rejected the plaintiffs’ theory

that discrete related tasks or duties, performed intermittently during the workday, and intermingled

with tip-generating duties, comprised a dual job when aggregated over the course of a workweek.

The Court seemed particularly bothered by the perceived impact such a rule would impose on

employers to engage in time tracking and minute-by-minute accounting of diverse tasks performed

despite existing regulations mandating that employers record detailed hourly records of when

50 See Auer v. Robbins, 519 U.S. 452 (1997) 51 Auer, 519 U.S. at 461 52 Marsh, 2017 U.S. App. LEXIS 17199, at *14 (9th Cir. September 6, 2017) 53 Marsh, 2017 U.S. App. LEXIS 17199, at *37; 29 C.F.R. § 531.56(e)

19

purported tipped employees earn tips.54 Although the Court followed the district court’s rationale,

it ultimately vacated the lower court’s orders and remanded providing plaintiffs with an

opportunity to propose a new amended complaint that does not rely on the guidance under FOH §

30d00(f).

On September 20, 2017, the plaintiffs-appellants in Marsh filed a petition for en banc

review with the Ninth Circuit. As of the date of this publication, Defendant-appellees were to file

a response by October 12, 2017.

Prior to the Ninth Circuit’s decision in Marsh, a number of courts followed the analysis in

Fast and held the DOL’s 20% rule is entitled to deference.55

This circuit split has created a new battleground of the FLSA’s tip credit provisions and

the DOL’s role and authority in interpreting the law related to tipped employees.

B. Who Owns The Tips When No Tip Credit Is Taken?

Significant litigation has arisen around whether the DOL has any authority to regulate what

happens to tips where the employers pay all employees the full minimum wage.

In Cumbie v. Woody Woo,56 the plaintiff was a server who was paid more than the Oregon

state minimum wage, but a portion of her tips were distributed to kitchen staff, including cooks

54 Marsh, 2017 U.S. App. LEXIS 17199, at **23-24, 37-38 (“no provision with the force of law permits the DOL to

require employers to engage in time tracking and accounting for minutes spent in diverse tasks before claiming a tip

credit”); Cf. 29 C.F.R. § 516.28(a) 55 See e.g. Knox v. Jones Grp., No. 15-CV-01738SEBTAB, 2016 WL 4371630, at *6–7 (S.D. Ind. Aug. 15, 2016)

(concluding, “consistent with the Eighth Circuit's holding in Fast v. Applebees Int'l, Inc., that the DOL's interpretation

of § 531.56(e) is entitled to deference”); Langlands v. JK & T Wings, Inc., No. 15-13551, 2016 WL 4073548, at *3

(E.D. Mich. Aug. 1, 2016) (same); McLamb v. High 5 Hosp., No. 16-00039 GMS, 2016 WL 3751946, at *4 (D. Del.

July 12, 2016) (same); see also Flood v. Carlson Restaurants Inc., 94 F. Supp. 3d 572, 582–84 (S.D.N.Y. 2015)

(collecting cases and recognizing district court across the country have “endorsed the twenty percent rule” and its

application); Irvine v. Destination Wild Dunes Mgmt., Inc., 106 F. Supp. 3d 729, 734 (D.S.C. 2015) (evaluating the

application of 20% rule and finding “it is not a real burden on an employer to require that they be aware of how

employees are spending their time before reducing their wages by 71%”); Crate v. Q's Rest. Grp. LLC, No. 813CV2549T24EAJ, 2014 WL 10556347, at *3–4 (M.D. Fla. May 2, 2014) (finding the “the [DOL] Handbook's

twenty percent limitation persuasive and practical”) 56 596 F.3d 577 (9th Cir. 2010)

20

and dishwashers. The Ninth Circuit held that “[t]he FLSA does not restrict tip pooling when no tip

credit is taken.”57 The Court was guided by Williams v. Jacksonville Terminal Co.,58 in which the

Supreme Court held “where tipping is customary, the tips, in the absence of an explicit contrary

understanding, belong to the recipient. Where, however, [such] an arrangement is made ..., in the

absence of statutory interference, no reason is perceived for its invalidity.” (emphasis in Cumbie).

Because the Court found there was such an agreement to redistribute the plaintiff’s tips to kitchen

employees and because the FLSA does not prohibit the practice because no tip credit was taken,

Woody Woo’s practice did not violate the FLSA.

This issue was brought to a head in 2011 when the DOL revised 29 C.F.R. § 531.52, as

follows, “to make it clear that tips are the property of the employee following the statutory silence

Cumbie exposed.”59

Tips are the property of the employee whether or not the employer has

taken a tip credit under section 3(m) of the FLSA. The employer is

prohibited from using an employee's tips, whether or not it has taken a tip

credit, for any reason other than that which is statutorily permitted in

section 3(m): As a credit against its minimum wage obligations to the

employee, or in furtherance of a valid tip pool.

The DOL explained:

Under the 1974 amendments to section 3(m), an employer's ability to

utilize an employee's tips is limited to taking a credit against the

employee's tips as permitted by section 3(m). Section 3(m) provides the

only method by which an employer may use tips received by an employee.

An employer's only options under section 3(m) are to take a credit against

the employee's tips up to the statutory differential, or to pay the entire

minimum wage directly.60

57 Id. at 580-583 58 315 U.S. 386, 397 (1942) 59 76 FR 18841–42 60 76 F.R. 18832-01. See Wage and Hour Opinion Letter WH-536, 1989 WL 610348 (October 26, 1989) (defining

when an employer does not claim a tip credit as when the employer does not retain any tips and pays the employee

the minimum wage)

21

In Oregon Rest. & Lodging Ass'n v. Perez, the DOL’s 2011 rule was challenged.61

Consolidated for appeal were two cases, one brought by the Oregon Restaurant and Lodging

Association against the DOL and the other casino dealers suing Wynn Las Vegas, LLC. The

district courts held in those cases, relying in large part on Cumbie, “that Cumbie foreclosed the

DOL’s ability to promulgate the 2011 rule and that the 2011 rule was invalid because it was

contrary to Congress’s clear intent.”62

In ORLA v. Perez, the Ninth Circuit reversed both district court decisions holding “the

FLSA is silent regarding the tip pooling practices of employers who do not take a tip credit” and

accorded Chevron deference to the DOL’s new regulations. Specifically, the Court stated, “[W]e

conclude that Congress has not addressed the question at issue because section 203(m) is silent as

to the tip pooling practices of employers who do not take a tip credit. There is no convincing

evidence that Congress’s silence, in this context, means anything other than a refusal to tie the

agency’s hands. In exercising its discretion to regulate, the DOL promulgated a rule that is

consistent with the FLSA’s language, legislative history, and purpose.”

On September 6, 2016, the Ninth Circuit denied rehearing en banc.63 Ten judges joined in

dissenting. On the same day, the Oregon Restaurant and Lodging Association, among other amici,

filed an amicus curiae petition with Supreme Court for review in Cesarz v. Wynn Las Vegas, LLC.

The Oregon Restaurant and Lodging Association, along with the National and other state

restaurant associations, filed a petition for writ of certiorari in ORLA v. Perez in the Supreme Court

61 816 F.3d 1080, 1085 (9th Cir. 2016) (“ORLA v. Perez”) 62 Or Rest.. & Lodging v. Solis, 948 F. Supp. 2d 1217, 1218, 1226 (D.Or. 2013); Cesarz v. Wynn Las Vegas, LLC, No.

2:13–cv–00109–RCJ–CWH, 2014 WL 117579, at *3 (D. Nev. Jan. 10, 2014) 63 ORLA v. Perez, No. 13-35765, 2016 WL 4608148 (9th Cir. Sept. 6, 2016)

22

on January 13, 2017.64 As of the date of this publication, response briefs have not been fully

submitted.

Among the arguments for cert review, is that ORLA v. Perez creates a circuit split with

Trejo v. Ryman Hosp. Properties, Inc., which held “the statutory requirements that an employer

inform an employee of § 203(m) and permit the employee to retain all his tips unless the employee

is in a tip pool with other regularly tipped employees does not apply to employees, like the

plaintiffs, who are seeking only the recovery of the tips unrelated to a minimum wage or overtime

claim.”65 In reaching its decision, the Fourth Circuit in Trejo reasoned that the FLSA “does not

state freestanding requirements pertaining to all tipped employees, but rather creates rights and

obligations for employers attempting to use tips as a credit against the minimum wage.66 Several

district courts have endorsed the reasoning in Trejo.

Recently, the Tenth Circuit in Marlow v. New Food Guy, Inc., also addressed the issue and

affirmed a motion for judgment on the pleadings in favor of an employer who paid above minimum

wages and did not supplement employee wages with gratuities paid by customers.67 In so doing,

the Tenth Circuit reasoned that “[i]f an employer pays more than the minimum wage without

regard to tips, the FLSA does not restrict the employer’s use of tips.”68 The Eleventh Circuit has

also now weighed in. In Malivuk v. Ameripark, LLC, the Eleventh Circuit held the plaintiff had

no claim for retention of tips because she did not assert a violation with respect to minimum wage

or overtime.69

64 S.Ct. Case No. 16-920 65 795 F.3d 442, 448 (4th Cir. 2015) 66 Id. at 445 67 861 F.3d 1157 (10th Cir. 2017) 68 Id. at 1159 69 No. 16-16310, 2017 WL 2491498 (11th Cir. June 9, 2017)